Robots And Social Distancing Will Revolutionize Restaurants In Post-COVID World Tyler Durden

Thu, 06/04/2020 – 22:25

Prior to the COVID-19 outbreak, the trend was in place for artificial intelligence and automation to displace tens of millions of jobs over this decade. Replacing workers with robots has certainly been thrown into hyperdrive in a post-corona world.

Strict social distancing enforced by some countries has now given way to reduced forms of distancing in daily life. This is precisely what is happening in South Korea, with some bars and restaurants reopening.

At Coffee Bar K in Seoul, a robo-bartender has replaced a human, can make perfect cocktails in the fraction of the time, reported Reuters.

Coffee Bar K’s Robo-bartender

The bar is encouraging customers to return, promoting its use of robots preparing drinks in a contactless environment, as a bid to attract patrons and increase sales.

“Since this space is usually filled with people, customers tend to feel very anxious,” human bartender Choi Won-woo said. “I think they would feel safer if the robot makes and serves the ice rather than if we were to do it ourselves.”

Down the street, a robot arm shakes up drinks for thirsty consumers at the Cafe Bot Bot Bot coffee bar. Manager Kim Tae-wan said customers feel much safer with robots handling their drinks than humans.

Cafe Bot Bot Bot’s drink robot

A post-corona world will be filled with many challenges for bars and restaurants. The most difficult question for operators and managers is how to instill enough confidence in people to bring them back.

One way to do this is by automating the back and front end of the restaurant. Allowing robots to prepare drinks and food in a contactless environment in the future and will drive confidence among patrons.

Robots to replace bartenders, cooks, and waiters is already here:

Concentrating on the front end of the restaurant. Operators and managers will likely have to readjust the dining floor with social distancing plexiglass dividers at tables, ultraviolet thermal body scanner at the entrance, and increasing online delivery via food lockers.

Another way to boost sales and save the collapsing restaurant industry is to install plexiglass bubbles, called Plex’Eat, which are suspended from the ceiling and sit around a patron’s head. At the same time, they have dinner, ensuring social distancing and a reduction in virus transmission inside the facility. This is what they look like:

Plex’Eat

While robots and social distancing measures seem radical, and quite frankly absurd, they could be the new standard for restaurants and bars in a post-corona world. However, there’s a trade-off — the automation part of this will lead to permeant job loss to some degree.

via ZeroHedge News https://ift.tt/3gURgI2 Tyler Durden

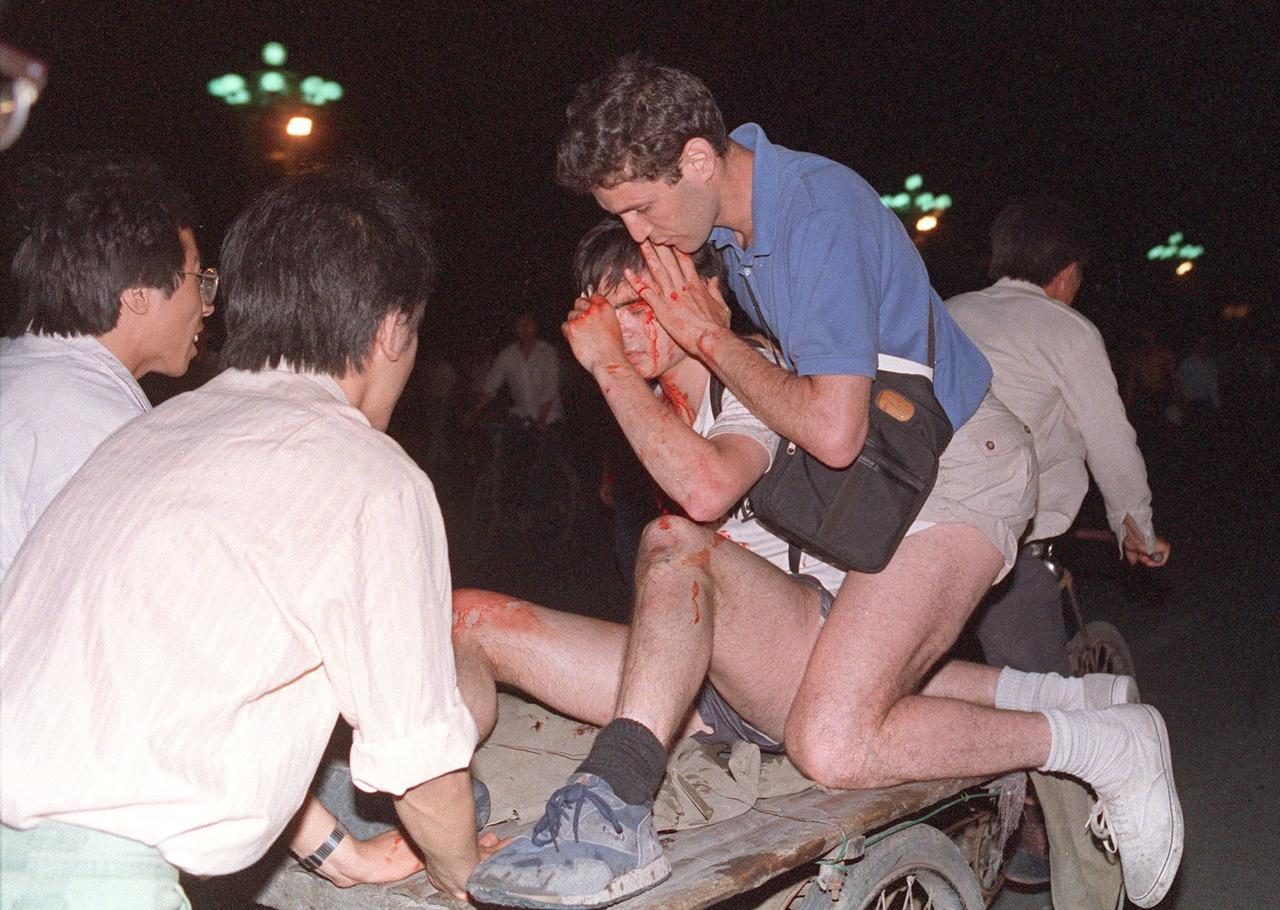

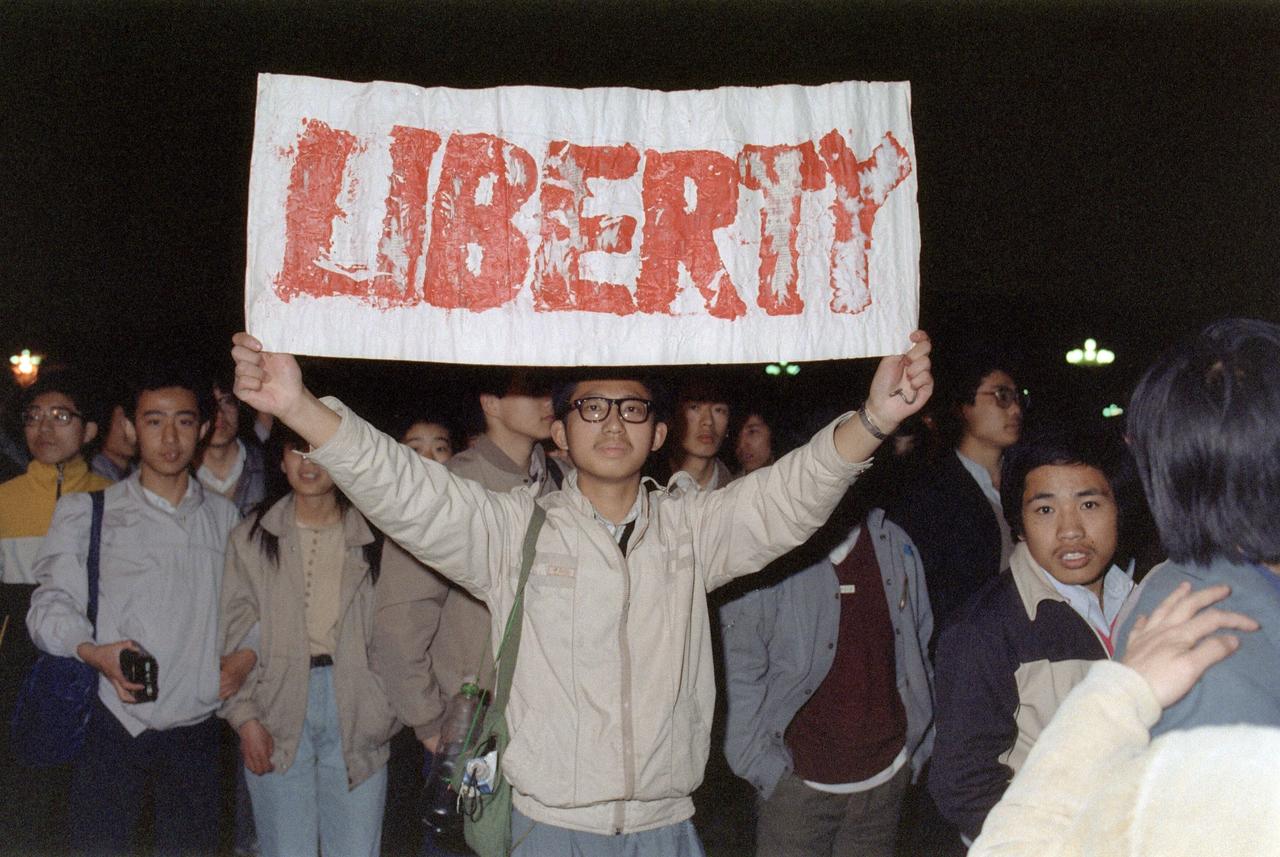

Following the sudden death of a beloved political reformer, Hu Yaobang, 200,000 students gathered at Tiananmen Square on April 22, 1989, to await the hearse carrying Hu’s body – but it never arrived. The mass of students were angered, and their burning desire for freedom could be contained no more.

For the next few weeks, Tiananmen Square was occupied by these student protesters, who aimed at making reality their dream of ridding the country of communist tyranny and bringing democratic reform to China. Their non-violent demonstration perhaps brought a glimmer of hope … until the army moved in. Although martial law was declared on May 20 that year, what caused the army to suddenly go on a killing rampage on June 4?

L: Thousands of Chinese gather on June 2, 1989, in Tiananmen Square around “The Goodness of Democracy,” demanding democracy despite martial law in Beijing. (CATHERINE HENRIETTE/AFP via Getty Images). R: “The Goddess of Democracy,” a 10-meter replica of the Statue of Liberty created by students from an art institute to promote the pro-democracy protest against the Chinese government. (TOSHIO SAKAI/AFP via Getty Images)

1. Mass-Murdered by the Chinese Regime

At least 10,454 people were mass-murdered by the Chinese communist regime on Tiananmen Square, according to an unnamed source from the Chinese State Council. The figure is far greater than the “official” fatality count of 200.

On June 4, 1989, students were gunned down in droves and “mown down” by tanks. “APCs (Armored personnel carriers) then ran over bodies time and time again to make ‘pie’ and remains collected by bulldozer. Remains incinerated and then hosed down drains,” reads part of a declassified statement, which was obtained by Alan Donald, Britain’s ambassador to China in 1989.

It’s still unconfirmed how many more were massacred during and after the students’ unarmed protest.

Waving banners, high school students march in Beijing streets near Tiananmen Square on May 25, 1989, during a rally to support the pro-democracy protest against the Chinese regime. (CATHERINE HENRIETTE/AFP via Getty Images)

2. The Ringleader Is Still Alive

In addition to rolling over the students with tanks, the army fired high-explosive shells that expand on impact, also known as dum-dum bullets, (forbidden by the Geneva Convention) to kill the students in the most harm-inflicting way possible.

The question remains—what kind of a human being would order such a brutal mass murder of freedom-seeking civilians?

Former leader of the Chinese Communist Party Jiang Zemin (Feng Li/Getty Images)

Former paramount leader of the party Deng Xiaoping was impressed with Jiang Zemin’s iron-fisted proposition to use the army to crack down on the students, and promoted him from Party Chief of Shanghai to General Secretary of the Chinese Communist Party days before the massacre, giving him free rein to do as he liked.

Jiang Zemin, the mastermind behind the massacre, ordered the army to carry out his bloody strategy on June 4. The “gate of heavenly peace” was suddenly turned into hell on Earth.

Taken care of by others, an unidentified foreign journalist (2nd-R) is carried out from the clash site between the army and students on June 4, 1989, near Tiananmen Square. (TOMMY CHENG/AFP via Getty Images)

3. Ruthless Abuse of Power

The Tiananmen Square Massacre was just the start of Jiang’s ruthless abuse of power. He went on to commit the most heinous crimes that couldn’t bear the light of day. In the bloody wake of the massacre, Jiang became Deng’s ideal heir for the next Party Chief, a position Jiang secured in 1993.

Jiang, a Marxist hardliner and ex-senior spy for the KGB’s Far-East Bureau, had only begun to show his true colors with how he dealt with the protesting students and went on to orchestrate even bloodier campaigns. In 1999, Jiang sought to “eradicate” Falun Gong—a popular spiritual practice—after the number of people practicing it rose some 100 million, outnumbering the then 70 million Party members, according to state-run reports at the time.

Falun Gong practitioners doing the group exercise in Guangzhou, China, in 1998. (Minghui)

Under Jiang’s rule, an adroit misinformation campaign inundated China, turning public opinion against Falun Gong by subjecting the spiritual practice to extreme vilification—including the infamous Tiananmen Square “self-immolation” hoax, which successfully deceived the nation—paving the way for Jiang’s next phase: to forcibly “transform” or “eliminate” the meditators who refused to give up the practice.

In response to Jiang’s genocidal policy, believed to have caused a widespread yet unascertainable amount of state-approved killings, including forced organ harvesting, over 209,000 lawsuits have since been filed against Jiang, making him the most sued dictator in history.

Falun Gong practitioners at a rally in front of the Chinese embassy in New York City on July 3, 2015, to support the global effort to sue Jiang Zemin. (Larry Dye/The Epoch Times)

4. Horrifying Accounts Kept Secret

A Blacklock’s Reporter obtained secret telex messages concerning horrifying accounts of what really happened on Tiananmen Square that day via access-to-information laws.

“An old woman knelt in front of soldiers pleading for students; soldiers killed her,” the Canadian embassy in Beijing reported at the time.

Blacklock’s writes: “A boy was seen trying to escape holding a woman with a 2-year old child in a stroller, and was run over by a tank”; “The tank turned around and mashed them up”; “Soldiers fired machine guns until the ammo ran out.”

An unbelievable amount of bullets were fired on civilians at Tiananmen that “they ricocheted inside nearby houses, killing many residents.”

“The embassy described the killings as ‘savage,’” according to Blacklock’s Reporter.

“They are now entering a period of vicious repression during which denunciations and fear of persecution will terrorize the population,” reads another cable obtained.

Chinese onlookers run away as a soldier threatens them with a gun on June 5, 1989, as tanks took position at Beijing’s key intersections next to the diplomatic compound. (CATHERINE HENRIETTE/AFP via Getty Images)

Diplomats added that some 1,000 executions took place following the massacre, but an exact figure is unconfirmed. “It was probably thought that the massacre of a few hundreds or thousands would convince the population not to pursue their protests. It seems to be working,” reads a statement by the diplomats.

The secret British cable, obtained by news website HK01, reveals more detail about the crimes of the 27 Army of Shanxi Province on the day.

“27 Army ordered to spare no one and shot wounded SMR soldiers. Four wounded girl students begged for their lives but were bayoneted. A 3-year-old girl was injured but her mother was shot as she went to her aid as were six others who tried.”

“A thousand survivors were told they could escape via Zhengyi Lu but were then mown down by specially prepared M/G (machine gun) positions.”

Ailing student hunger strikers from Beijing University receive first aid treatment under a makeshift tent set up on May 17, 1989, at Tiananmen Square as students enter the 5th day of a marathon hunger strike as part of a mass pro-democracy protest against the Chinese government. (CATHERINE HENRIETTE/AFP via Getty Images)

5. “June 4”: A Highly Taboo Subject in China Today

Despite Hong Kong lighting up every evening on June 4 in an annual candlelight vigil to commemorate the victims of the massacre, Chinese mainlanders across the border are without such freedom of speech. Talking about the Tiananmen Square Massacre, or even mentioning “June 4,” or “6.4,” could have one disappear.

In 2007, Zhang Zhongshun, a lecturer from Yantai University, showed his class a video of the massacre he obtained from an overseas website. He was subsequently jailed for three years by Laishan City Court on Feb. 28, 2008.

Tens of thousands of people hold candles during a vigil in Hong Kong on June 4, 2018, to mark the 29th anniversary of the 1989 Tiananmen crackdown in Beijing. (ANTHONY WALLACE/AFP via Getty Images)

“I imagined that the worst case would just be that the university president would criticize me in front of my colleagues in a meeting. I would not have thought that the communist regime would imprison me,” Zhang told The Epoch Times in an interview after his release from the detention.

“Is it illegal even if I include a historical event into my lecture?” he asked.

A student displays a banner with one of the slogans chanted by the crowd of some 200,000 pouring into Tiananmen Square on April 22, 1989, in Beijing in an attempt to participate in the funeral ceremony of former Chinese Communist Party leader and liberal reformer Hu Yaobang. His death in April triggered an unprecedented wave of pro-democracy demonstrations. The April-June 1989 movement was crushed by Chinese troops in June when army tanks rolled into Tiananmen Square June 4, 1989. (CATHERINE HENRIETTE/AFP via Getty Images)

Who’d dare raise this for discussion in China knowing the consequences? This year marks the 31st anniversary of the Tiananmen Square Massacre. Will the current Chinese leaders redress the issue and bring Jiang Zemin to justice for his litany of crimes? Only time will tell.

via ZeroHedge News https://ift.tt/2zTJRbC Tyler Durden

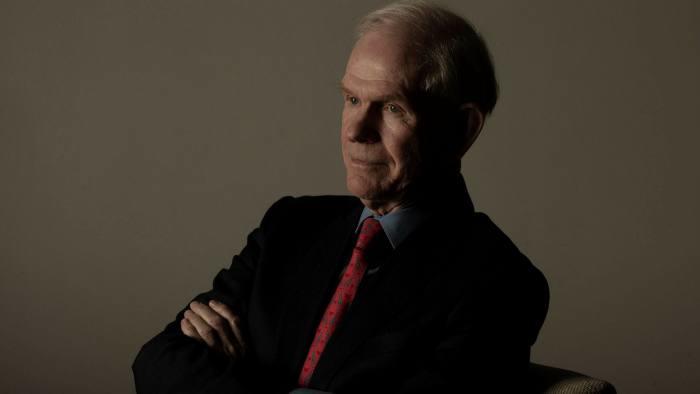

… many veteran investors are throwing in the towel on what is emerging as the most furiously ridiculous rally in history in what is now better known as “Jay’s market” (with 73% of Wall Street claiming that the market is only up due to the artificial gimmick of the Fed’s balance sheet explosion and not due to fundamental factors). And with one after another investing legend such as Warren Buffett, Stanley Druckenmiller, David Tepper boycotting the artificial rally, and either selling or pulling out, today GMO’s Jeremy Grantham became the latest to bail on what Bank of America recently called a “fake market.”

In a letter to GMO investors, Grantham writes that “we have never lived in a period where the future was so uncertain” and yet “the market is 10% below its previous high in January when, superficially at least, everything seemed fine in economics and finance. And if not “fine,” well, good enough. The future paths include many that could change corporate profitability, growth, and many aspects of capitalism, society, and the global political scene.”

Jeremy Grantham.

In short, the veteran value investor known for calling several of the biggest market turns of recent decades admits he has lost his faith in an upside case – unlike the retail daytrading army – and his sense of direction in a world of record uncertainty “which in some ways seems the highest in my experience” and as a result “in terms of risk and return – particularly of the worst possible outcomes compared to the best – the current market seems lost in one-sided optimism when prudence and patience seem much more appropriate.“

Grantham also highlights the obvious: that the market and the economy have never been more disconnected, and points out that while “the current P/E on the U.S. market is in the top 10% of its history… the U.S. economy in contrast is in its worst 10%, perhaps even the worst 1%…. This is apparently one of the most impressive mismatches in history.“

As a result of this total loss of coherence driven by trillions in central bank liquidity that have propelled a massive wedge between fundamentals and stock prices, GMO, the Boston fund manager Mr Grantham co-founded in 1977, cut its net exposure to global equities in its biggest fund from 55% to just 25%, near the lowest levels it reported during the global financial crisis, according to a separate update from GMO’s head of asset allocation, Ben Inker.

That decision, according to the FT, slashed GMO’s Benchmark-Free Allocation Fund exposure to US equities from a net 3-4% to a net short position worth about 5% of the $7.5bn portfolio, said Inker, perhaps the first time the fund has turned net short US stocks since the crisis. This, after GMO loaded up on stocks during the sell-off but has since cut offloaded its exposure to the US market following the unprecedented 40% rally in the past 2 months.

“The Covid-19 pandemic “should have generated enhanced respect for risk and it hasn’t. It has caused quite the reverse,” Grantham told the Financial Times. He noted that trailing price-earnings multiples in the US stock market were “in the top 10 per cent of its history” while the US economy “is in its worst 10 per cent, perhaps even the worst 1 per cent”, echoing what he said in his quarterly letter.

And while markets seem to be taking all the negative news in stride, Grantham is worried that the wave of devastation that is coming is unlike anything experienced before:

At GMO we dealt with three major events prior to this crisis, and rightly or wrongly, we felt “nearly certain” that sooner or later we would be right. We exited Japan 100% in 1987 at 45x and watched it go to 65x (for a second, bigger than the U.S.) before a downward readjustment of 30 years and counting. In early 1998 we fought the Tech bubble from 21x (equal to the previous record high in 1929) to 35x before a 50% decline, losing many clients and then regaining even more on the round trip. In 2007 we led our clients relatively painlessly through the housing bust. In all three we felt we were nearly certain to be right. Japan, the Tech bubbles, and 1929, which sadly I missed, were not new types of events. They were merely extreme cases akin to South Sea Bubble investor euphoria and madness. The 2008 event also was easier if you focused on the U.S. housing euphoria, which was a 3-sigma, 100-year event or, simply, unique. We calculated that a return trip to the old price trend and a typical overrun in those extreme house prices would remove $10 trillion of perceived wealth from U.S. consumers and guarantee the worst recession for decades.All these events echoed historical precedents. And from these precedents we drew confidence.

But this event is unlike all those. It is totally new and there can be no near certainties, merely strong possibilities. This is why Ben Inker, our Head of Asset Allocation, is nervous and this is why you are nervous, or should be.

While the uncertainties are indeed large, one can triangulate a sufficiently material dose of “certainty” about what is coming, and as Grantham explains further, it is not pretty, especially with the US economy already on the back foot heading into the crisis:

We had U.S. and global problems looming before the virus: an increasingly disturbed climate causing global floods, droughts, and farming problems; slowing population growth, in the developed world, soon to be negative; and steadily slowing productivity gains, especially in the developed world, and therefore a slowing GDP trend. In the U.S., our 3%+ a year trend is down to, at best, 1.5% in my opinion. It is closer to a 1% maximum in Europe. We had, as mentioned, top 10% historical P/Es in the U.S. and much the highest debt level ever in the U.S. for both corporations and peacetime government. So, after a 10-year economic recovery, this would have been a perfectly normal time historically for a setback.

And then the virus hit.

Simultaneously, it is causing supply and demand shocks unlike anything before. Ever. It is generating a much faster economic contraction than that of the Great Depression. And unlike 1989 Japan, 2000 Tech (U.S.), and 2008 (U.S. and Europe), it is truly global. The drop in GDP and rise in unemployment in four weeks have equaled what took one to four years to reach in the Great Depression and were never reached in the other events. Rogoff & Reinhart, Harvard Professors who wrote the definitive analysis of the 2008 bust, agree that this event is indeed completely different and suggest it will take at least 5 years to regain 2019 levels of activity. But this is a guess. We really don’t know how long it will take. Nearly certain is that a V-shaped recovery looks like a lost hope. The best possible outcome would be that there will be, almost miraculously, billions of doses of effective vaccine by year-end. But most viruses have never had a useful vaccine and most useful vaccines have taken well over five years to develop and when developed have been only partially successful. Yes, this time there will be an enormous effort with unprecedented spending. But still, a leading vaccine expert says quick success would be like “drawing successfully to several inside straights in a row.” And even if all works out well with a vaccine there will remain deep economic wounds.

Meanwhile, as the world waits for a vaccine, and buys stocks confident one is imminent, the “bankruptcies have already started (Hertz on May 22nd) and by year-end thousands of them will arrive into a peak of already existing corporate debt. It will need spectacular management, which it may get. But it may not. Throwing money – paper and electronic impulses – at the problem can help psychology and, particularly, the stock market, where extra stimulus money can end up but does not necessarily put people back to work; there will be up to 20% unemployment for at least a moment.”

In response to this historic economic collapse, central banks’ unprecedented stimulus efforts have “temporarily overwhelmed” underlying economic realities but “it’s hard to believe that will continue.”

And when it stops, watch out below: Grantham told the FT in an interview that after seeing markets price in “total recovery” over recent weeks, “my confidence that this will end badly is increasing.”

Speaking as protests against police brutality and racism filled the streets of US cities, Grantham said previous outbreaks of social instability had had few lasting effects on the US economy, but “there are more things going wrong than normal“.

However, the value investing legend’s most dire prediction was that “if you look back in two to three years and this market turns around and drops 50%, the history books will say ‘That looked like one of the great warnings of all time. It was pretty obvious it was destined to end badly,” Grantham said, adding: “If it does end badly the history books are going to be very unkind to the bulls.” For the sake of an entire generation of Robinhooders who will lose everything if there is a 50% crash, one hopes Grantham is wrong.

Finally, Grantham also chimed in on the “most important question in finance right now”, revealing that he was proud of not having “made a fuss about inflation” in 20 years of writing his widely followed letters, but said that record amounts of monetary easing from central banks had now created the possibility of inflationary pressures.

“With a generous stimulus program in many countries you can just about daydream about inflation for the first time in 30 years.”

To this, all we can add is that in the very near future that daydream will become a nightmare.

via ZeroHedge News https://ift.tt/2XzeYSE Tyler Durden

“Coronavirus hasn’t been a thing since Friday,” said a friend.

“The new story is racism.”

Following American media culture can make one’s head spin.

For three months, all we heard was the danger to life and civilization presented by a novel virus. Millions will die! Few will be spared! There will be unprecedented suffering unless we completely shatter the normal functioning of life. Lock down, shelter in place, and stand six feet apart – very strange exhortations never before heard in the modern history of annual viruses or any public policy in many lifetimes.

All of it enforced by the police power. The same police power that eventually landed on the neck of George Floyd.

They screamed that we had to close schools, shopping centers, sports, and only allow “essential” business to function even if tens of millions lose their jobs, because lives – lives that the police power has utterly disregarded during the protests – are just that important. Lockdown required that the law change on a dime, in violation of every legal precedent, every slogan in American civic mythology, and contradicting the whole of what made America great.

In three days in mid-March 2020, everything we previously believed had to end because we had to implement a new experiment in social control as cobbled together by “public health officials” some 14 years ago. They sat around for a decade and a half, bored and waiting to use the new way to combat viruses. Any old virus would do so long as it was a slow news day. COVID-19 was as good an excuse as any. Out was every foundational belief in liberty, property, and free association, in the blink of an eye.

That was 75 days ago. People were surprisingly compliant, but what could they do? They were scared, thanks to media frenzy, and they weren’t allowed out of their houses to protest in any case. When they did defy the orders to protest in front of capitol buildings, instead of staying home and watching CNN, they were derided by CNN as disease spreaders and enemies of public health.

I’m looking at the headlines today and all the news on the coronavirus is below the fold or in its own section. It’s all about the protests, riots, and looters. Racism.

Trump is screaming for a crackdown while the media demands justice for police brutality. As for social distancing, this was absolutely yesterday’s news. Now a new ethos has taken hold: gather in the largest possible groups to demand social justice. And loot.

Absolute hymns to the glory of protestors and even rioters are the rule of the day, as if the public health threat of COVID-19 is so last week. “Each night, tens of thousands exercise their right to assemble in protest and millions of Americans follow along at home,” writes the New York Times rhapsodically and correctly, failing to point out that this same venue said the opposite about lockdown protestors a few weeks ago.

Weeks! Is it an indication of the extremely short attention span of the American public or a demonstration of the sheer cynicism of media culture?

Meanwhile, on the corona front – yes that still exists even if you have to dig for information on it – states are still (still!) gradually ending the lockdown with cockamamie rules: you can sit (or stand) in bars but you can’t stand (or sit). Customers can buy things but not try on clothing. People can buy perfume but not spray on samples. In daycare facilities, the kids can play together in groups of more than 10 and they must stay apart, even though there is near zero threat to the kids from the virus.

These states that are imposing these crazy rules are four days behind the times. You look at the protests and you see free people doing what they believe they should do in the face of injustice. Many wanted to do this months ago but they were prohibited by law. The law eventually had to acquiesce to people’s sense of their human rights.

Why states do not instantly and immediately end all restrictions they wrongly imposed indicates the sheer stupidity of public policy, and the myth that it can ever be scientific. Instead we get curfews, even in the city that never sleeps.

The same governments that were only recently controlling your movements to protect you from a virus are now blasting people with tear gas.

As for lockdown “science,” the Centers for Disease Control keeps lowering its infection fatality rate. It’s becoming normalized like any virus: bad but not the end of the world. Best treated by medical professionals, not politicians – as we long knew until very recently.

The lockdown carnage from missed cancer diagnostics and forgone elective surgeries are only now presenting themselves. Then there are the 100 thousand wrecked businesses, the 40 million unemployment, the blown budgets of every government, the scary monetary policies. SWAT teams were entering bars to arrest people — in the name of health. Churches were shuttered on Easter. No restaurants, no shopping, no sports, no theaters, no gyms, no outdoor activities. We were all treated like animals, and told to cage ourselves in our homes. And so on it went for 75 days.

It’s hard to imagine a better recipe for social unrest.

Then the protests began. They were about the death of George Floyd, an unemployed man but they were also what he represented: the overwhelming presence of state violence in all of our lives.

Then the looting started. That too should not be a surprise. Lockdowners and looters use the same method (violence) to destroy property and commerce. One class of criminals learns from another class of criminals. It’s copycat criminology.

Now, as if to take that next step on the Road to Serfdom, all major cities have curfews.

Based on the speed and duplicity of the news cycle, we can predict with confidence that within six months, you won’t find a single person in public life willing to defend the lockdown. And yet it was this event that laid the foundation for the rest of the tragic unfolding of events that is wrecking this country.

There should be justice. There should be compensation. Political heads should metaphorically roll, along with the “public health officials” who advised them. And then we need a completely new direction: one that rejects the unscientific use of state force to battle a disease, recognizes the wisdom of the Bill of Rights and freedom, and treats people with the dignity that is inherent to every human life.

If we understand this desperate need – if we see what went wrong these months and the right way forward – we can rebuild. If we do not, the destruction and rights violations will continue.

via ZeroHedge News https://ift.tt/2BB2FN9 Tyler Durden

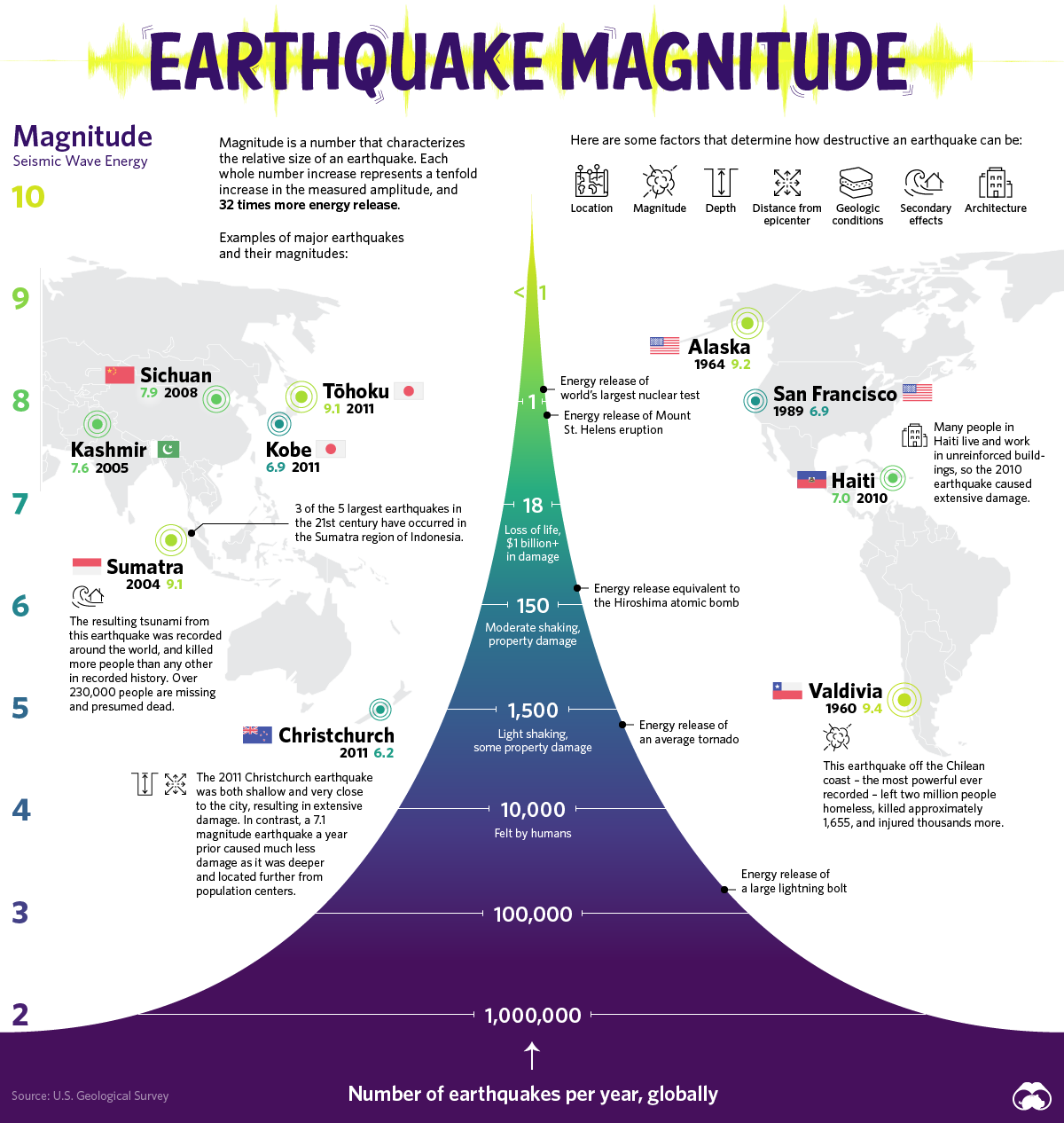

Visualizing The Power And Frequency Of Earthquakes Tyler Durden

Thu, 06/04/2020 – 21:05

The surface of our planet is in a constant state of creation and destruction as the plates of the Earth collide. It is this movement of the Earth’s crust that causes earthquakes, sending tremors throughout the world.

Today’s graphic by Visual Capitalist is inspired by a classic USGS diagram that tracks the scale and frequency of earthquakes.

Shifting Foundations

Earthquakes occur because the crust of the Earth is made up of several plates. The boundaries of these plates create faults that can run into one another.

Earthquakes describe both the mechanism that causes a sudden stress release along plate boundaries and also the ensuing ground shaking.

They occur when stress builds up along a tectonic fault. This stress causes the two surfaces of the fault, which had previously been stuck together due to friction, to suddenly move, or slide, releasing energy in the form of seismic waves.

Measuring an Earthquake’s Impact

There are three factors to assess the impact of Earthquakes – magnitude, energy, and intensity.

Magnitude is a number most commonly associated with the Richter scale, describing the size of an Earthquake on a scale from 0 to 10 – the latter of which is the maximum motion recorded by a seismograph. Each increase by one on the scale represents a tenfold increase in the amplitude. There are over a million tremors around the planet each year, but it’s not until an earthquake reaches a magnitude of 4 that humans can typically feel it.

Another way to measure the size of an earthquake is by how much energy it releases. The amount of energy radiated by an earthquake is a measure of the potential for damage to man-made structures.

An earthquake releases energy at various frequencies, and in order to calculate accurately, you have to include all frequencies of shaking for the entire event. Some research suggests technology could harness this energy for power generation.

Intensity describes the severity of an earthquake with a qualitative evaluation of its effects on the Earth’s surface and on the built environment. An earthquake may have a high magnitude but if a city or landscape experiences little damage, it can be said that the intensity is low. The Modified Mercalli Intensity Scale measures this intensity.

The World’s Largest Earthquakes by Magnitude

Prior to the development and use of seismographs, around 1900, scientists could only estimate magnitudes, based on historical reports of the extent and severity of damage.

Earthquakes are a fact of life on Earth and mark distinct moments in history. One would think given our knowledge of earthquakes, that humans would avoid these locations – however, the very faults of the Earth also create its greatest advantages.

Living with Your Faults

It’s extremely common to find human settlements along the fault lines where earthquakes occur most frequently. Some could say that this is because these decisions were made before a complete understanding of science enabled us to know the potential risks involved.

However, a recent scientific study reveals that there may be more to the pattern than previously thought. Tectonically active plates may have produced greater biodiversity, more food, and water for our human predecessors.

Certain landscape features formed by tectonic processes such as cliffs, river gorges, and sedimentary valleys create environments that support access to drinking water, shelter, and an abundant food supply.

This inherent problem reveals that humans are more connected to their environments than previously thought. It comes down to a question of how well humans can adapt their lifestyle and built environments to a dynamic planet.

“A waiter, again unbidden, brought the chessboard and the current issue of The Times, with the page turned down at the chess problem.”

While America burns, the dollar tumbles, stock markets soar, Germany announces a massive bailout programme which dwarfs the pennies Italy desperately needs, the ECB gets ready for another money dump, and UK politicians grumble about queues… life goes on…

There is something deeply tragic about yesterday’s announcements from HSBC and Standard Chartered supporting the imposition of China’s Security Law in Hong Kong. We can all act shocked and damn them for supping with the devil, but neither bank had any real choice but to make the unpalatable decision to support the unsupportable. Both know their futures depend too much on China’s patronage to survive without kow-towing.

Yesterday, they each wrote the first lines of the final few paragraphs of their own obituaries.

10-years ago I wrote in the Porridge why HSBC was my top bank stock. I said something along the lines of while other banks will remain vulnerable, HSBC had the franchise, strength and depth to survive and thrive. Its dividend policy was strong and would provide dull, boring, predictable returns for the long-term. The Long-term is so over.

Read the comments following any article about the two Hong Kong banks this morning and are they full of earnest virtue signalling from angry clients who say they will close their accounts. I will probably switch mine.. but only because now there is zero chance the service will get any better.

Timing is everything. I laughed out loud at a post on Linked-In from HSBC claiming leadership in ESG matters and Green funding. Really… this is not the time for HSBC to be bragging about its ethical credentials.

The sad reality is HSBC has become a patron of the Chestnut Tree Café – the bar where the purged characters from 1984 spend their last few months in isolation, irrelevancy and waiting for the axe to fall. HSBC and Standard Chartered’ future is window dressing the new Hong Kong. HSBC has become as yesterday as Deutsche Bank.

It could have been so different.

In the early 2000s HSBC’s tag line was The World’s Local Bank. The Hexagon Logo dominated airports and appeared everywhere. Its ambition was to generate one third of its profits from each of the main global markets; Asia, Europe and North America. By market capitalisation it was the largest bank on the planet. When it bought US sub-prime credit lender Household in 2002, it was a clear signal the bank was on the move with expansion plans everywhere.

I joined HSBC in 2002. It was a bit of a shock after 10 years at an aggressive but highly innovative US investment bank.

HSBC people were lovely. They were friendly, they were nice. Yet, they were fiercely tribal and regional in their mindset. There was a cadre of International Officers who’d been drilled in the HSBC tau of things since they joined straight from school. The regarded outside hires as mere hired hands. You could not argue with the IOs – they knew best. And then there were the old Hong Kong hands, trading hotshots from Hong Kong who knew even better. They’d been big fish in the small pool that was then Asia. They couldn’t grasp that Wall Street and City traders swam in much larger more aggressive oceans. The firm was naturally hierarchical in the way only a thoroughly English bank could be – even though its DNA was broadly Presbyterian Scots!

Yet, the bank failed to make much a mark on the global markets. It owned multiple diverse and unconnected business, united only by the logo. The way the bank’s independently minded German operation operated had nothing to do with the London hub. The Paris operation delighted in doing things differently. Asia had little interest in what New York or London were doing. It sold global clients a grand vision of access to Asia – but any second rate US firm knew more of the top Asian accounts.

Successive waves of hired guns were hired to enliven its sub-par investment banking activities, but without much enthusiasm from across the firm which remained siloed. The senior management were good, knew the issues and the bank– they were some of the best in the business. But they were trying to run an enormous bloated bureaucracy of dissimilar banking businesses, investment and commercial banking operations, consumer banking around the globe, an Asian franchise, while trying to grow new businesses in areas they perceived the bank understrength. They faced pushback from local fiefdoms, and became jacks of all and masters of nothing.

The crunch came following the global financial crisis in 2007/08. HSBC was the only UK bank that avoided disaster and bailout. (So did Barclays, but by the skin of their teeth and some dubious chicanery which Amanda Stavely will no-doubt shortly reveal in court.) Household went from being an inspired purchase to toxicity overnight – and dragged the whole North American operation down. A succession of banking scandals in Latin America followed – HSBC discovering to their shock that putting the logo on a Mexican bank did not suddenly cleanse it of endemic corruption and drug money laundering.

The result was a bank that was no longer managed from growth and the future, but in order to placate the regulators.

This is the critical lesson of HSBC. The brand was brilliant but hollow. Its’ businesses were individually good, but collectively poor. Rationalising them into a strong single force was a massive ask – and would have required more than the best banking management on the planet. But that management was totally focused on placating the regulators to avoid them purging the bank. At one time the board seriously feared the US SEC might close them down as more South American scandals came to light.

While US banks thrived through the 20-Teens HSBC plodded and became more bloated. Its ambitions a global bank vanished like an early morning mist. It contracted. Asia’s share of profitability – to be blunt, Hong Kong savers – rose through 80%. It became classically squeezed in its home market. The levels of dissatisfaction with its consumer banking division means it’s among the most complained about banks.

I figured out how bad things were a few years ago when I walked into the Premier Branch of HSBC at its Canary Wharf Global HQ a few years ago. No one greeted me. There were last week’s papers sprawled across a table, and dead pot plant in the corner coated in dust. I pressed the desk bell, and a bored looking girl sauntered out to tell me to go downstairs to the public branch because she was too busy to help. I sold all my stock soon after.

Except that it is, it wasn’t the fault of senior management. They tried. But the bureaucracy won. Banks run to please regulators rather than customers seldom thrive. Across the bank the middle management are shuffling papers and waiting for the a long-delayed axe to fall as cuts are finally enacted.

It’s a shame. The Home for Scottish Bank Clerks will join the list of other banks that once were contenders…..

via ZeroHedge News https://ift.tt/3eV09zN Tyler Durden

Garcetti spoke of “reinvesting in black communities and communities of color.”

The mayor proceeded to announce $250 million in cuts to the proposed budget and to reallocate those dollars to communities of color, “so we can invest in jobs, in education and healing.” L.A. Police Commission President Eileen Decker then announced that $100 million-$150 million of those cuts would come from the police department budget.

I doubt this will on balance help black and Hispanic Angelenos, who are especially at risk of the violent crime that police are most needed to fight (much more so than of the violent crime that the police do indeed sometimes commit), see, e.g., these homicide statistics. But it surely will lead more people to conclude that, as police protection declines, self-protection becomes all the more valuable—as does private security, for the few rich enough to afford it.

from Latest – Reason.com https://ift.tt/3eW14jr

via IFTTT

Garcetti spoke of “reinvesting in black communities and communities of color.”

The mayor proceeded to announce $250 million in cuts to the proposed budget and to reallocate those dollars to communities of color, “so we can invest in jobs, in education and healing.” L.A. Police Commission President Eileen Decker then announced that $100 million-$150 million of those cuts would come from the police department budget.

I doubt this will on balance help black and Hispanic Angelenos, who are especially at risk of the violent crime that police are most needed to fight (much more so than of the violent crime that the police do indeed sometimes commit), see, e.g., these homicide statistics. But it surely will lead more people to conclude that, as police protection declines, self-protection becomes all the more valuable—as does private security, for the few rich enough to afford it.

from Latest – Reason.com https://ift.tt/3eW14jr

via IFTTT

he New York Timesreports optimistically that “Japan Approves Fresh $1.1 trillion Stimulus to Combat Pandemic Pain.” As the Times elaborates, Japan’s “record stimulus of 117 trillion yen ($1.09 trillion), which will be funded partly by a second extra budget, followed another 117 trillion yen ($1.09 trillion) package rolled out last month. The new package takes Japan’s total spending to combat the virus fallout to 234 trillion yen ($2.18 trillion), or about 40% of gross domestic product.” “The packages (this year) took the size of the budget to a record 160 trillion yen, with new bond issuance making up 56.3% of annual budget revenue and raising the spectre of more bond issues later to offset falling tax income.”

It’s a “record stimulus,” the Times gushes. Very exciting stuff! Surely it will work!?

But why would any of it help “combat” a “virus fallout” or “stimulate” Japan’s economy? By “economy” do we not, as economists, refer to output, the production of goods and services, to real GDP at the least? If so, how can deficit spending create wealth? There is no evidence for that.

The “fresh” part of the Times’ headline is best translated as “recent” because for the past three decades, amid various crises, Japan has adopted literally dozens of alleged “stimulus” schemes – including not just massive deficit spending but rate-cutting, a zero-interest rate policy (ZIRP), “QE” (central bank monetization of public debts), and even direct purchases of private debt and equity securities. None of these programs has ever been proved to improve Japan’s economic-financial performance. Indeed, its performance has eroded amid the cascade of higher spending.

Japan’s economic-financial performance peaked in 1989-1991 and periodic revivals aside, it has stagnated since, amid degeneration in public finances. The causes of the peak and subsequent “lost decades” are worth recalling. In the late 1980s the Bank of Japan (BoJ), on the advice of leading economists, interpreted the decade as artificial, a mere “bubble,” and set out to “pop” it with punitive interest-rate hikes. The BoJ inverted the yield curve, which is a recession signal in part because it makes credit intermediation (“borrowing short, lending long”) unprofitable.

After the BoJ-authored yield curve inversion, Japan’s real GDP decelerated from growth of 9.4% in 1988 to only 4% in 1989; by 1993 GDP was contracting. Industrial production also decelerated, from 7.4% in 1988 to only 3.5% in 1989 before contracting by 13% between 1991 and 1993. Today Japan’s industrial production index remains 12% below its 1991 peak. The NIKKEI equity index also crashed after the BoJ’s policy assault, by 60% from the end of 1989 to mid-1992. The index low in 2009 was 80% below the 1989 peak; today the index remains 46% below its 1989 peak.

One could say the BoJ certainly “succeeded” in its mission to combat the supposed artificiality of Japan’s economic-financial performance in the 1980s; since then, Japan’s policymakers have dutifully followed the advice of Keynesians like Paul Krugman, implementing dozens of “stimulus schemes;” in effect, they’ve tried to artificially revive Japan’s economy, not by deregulating it, not by cutting tax rates or restraining growth in government but by massive public deficit spending.

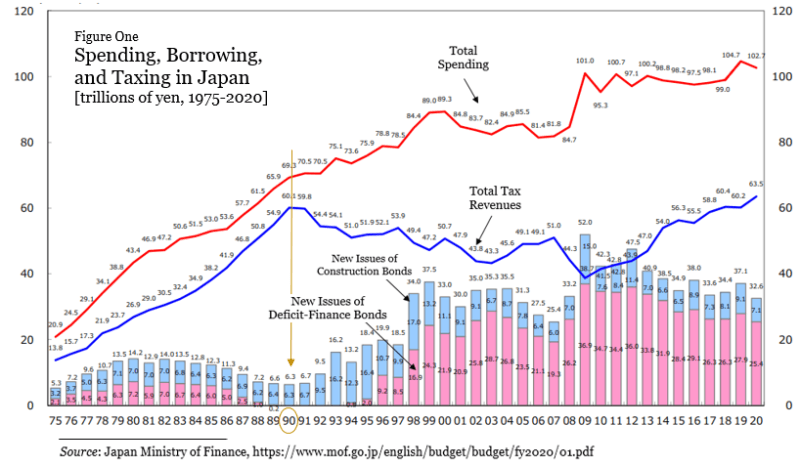

Figure One illustrates the dramatic shift in Japan’s public finances after 1990. In the fifteen years prior to 1990, growth in public spending and tax revenues closely tracked; new debt issuance was limited and even declined between 1982 and 1990. Since then, however, spending growth has far outpaced growth in tax revenues, due mainly to tax rate hikes and a stagnant economy. Deficit spending and new debt issuance have been preferred – the genuine Keynesian prescription.

Decades of chronic deficit spending have boosted Japan’s public leverage (debt-to-GDP ratio). Figure Two shows debt is now 235% of GDP, up from 175% in 2010, 125% in 2000, 64% in 1990, and 50% in 1980. Having boosted its policy rate in the late 1980s to fight a “fake” prosperity, the BoJ has since cut the rate dramatically. For a quarter century the rate has been below 1%, not, it seems, to “stimulate” the economy (or lending) but to enable the Treasury to borrow more affordably. The BOJ has been politically dependent, serving mainly Japan’s deficit spenders.

Surely one might expect that eventually this stupendous, multi-decade deficit-spending would “stimulate” Japan’s economy or equities. But mostly Keynesians (and some monetarists) would expect it. Adherents of Saysian economics, in contrast, would not expect it; indeed, they’d predict that vast increases in public spending and borrowing would more probably impede prosperity.

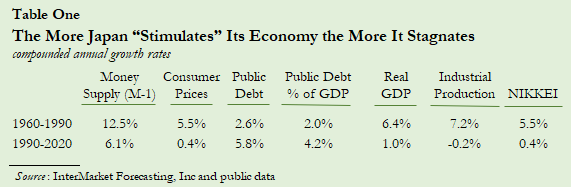

Table One contrasts Japan’s performance over the past three “lost decades” (1990-2020) and the prior three decades of robust growth (1960-1990). Public debt has grown 5.8% p.a. in the three decades since 1990 while public leverage has increased 4.2% p.a.; meanwhile, real GDP has grown only 1.0% p.a., the NIKKEI has risen by only 0.4% p.a., and industrial production has contracted. So much for Japan’s “stimulus.” The Keynesian prescription has been worse than useless. It’s been harmful. Yet the more it fails, the more its adherents insist on still larger doses of deficit spending.

In the three decades prior to 1990, before Keynesian policy advice became dominant in Japan, the nation enjoyed robust and sustainable economic growth amid fiscal rectitude. Table One makes clear that Japan’s public debt and public leverage increased by only 2.6% p.a. and 2.0% p.a., respectively, while real GDP grew 6.4% p.a., industrial output grew 7.2% p.a., and the NIKKEI advanced 5.5% p.a. In each case pre-1990 performance outpaced post-1990 performance. The difference is due mainly to the tragic suspicion of prosperity which took hold in Japan in the late 1980s, and to later adoption of so-called “stimulus” schemes, which, I argue, are depressive:

Many economists believe public spending and money issuance create wealth or purchasing power. Not so. Our only means of obtaining real goods and services is from wealth creation — production. Under barter no one comes to market expecting to buy stuff without also offering stuff. A monetary economy does not alter this key principle. What we spend must come from income, which itself must come from producing. Say’s Law teaches that only supply constitutes demand; we must produce before we demand, spend or consume. Demand is not a mere desire to spend but desire plus purchasing power.

Believers in “stimulus” also claim that government spending entails a magical “multiplier” effect on aggregate output, unlike most private sector spending. They tout a government’s greater “propensity to consume.” But consuming is the opposite of producing. Welfare states certainly consume and redistribute wealth. They divide it up. But math teaches that nothing – wealth included – can be multiplied by division. The so-called “multipliers” imagined by today’s economists are, in fact, divisors. Many studies have verified the principle.

To see why “stimulus” truly depresses, consult the basics. The creation of public money and public debt is not the creation of wealth; it is not food, clothing, shelter, energy or the like. Even privately generated money and debt, which reflect the needs of trade and lengthy production chains, represent, facilitate and circulate wealth but are not themselves wealth. Meanwhile, the savings borrowed by governments are unavailable to productive enterprises, and when a government creates fiat money beyond what money holders demand, the money loses purchasing power, which boosts the cost of living. These are not roads to prosperity.

A tragically wrong public policy should be abandoned, not emulated. Sadly (and tragically), the U.S. since 2001 has been copying Japan’s approach, with a lag of a decade or so. What some here called “unorthodox” fiscal-monetary policy was first “normalized” in Japan. The two nations differ in some important ways, including demographically, but that does not nullify the laws of economics (or of public finance). The U.S. and Japan are old welfare states that can’t afford what they’re doing; nonetheless, their politicians can’t seem to succeed electorally without persisting in their profligacy. Japan’s history signals the likely outcome for copycats: prolonged stagnation.

via ZeroHedge News https://ift.tt/3cwzIi5 Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}