Another year, another disaster, another economically misguided tug of war over the merits of “price gouging.” The arrival of COVID-19, otherwise known as coronavirus, ushered in a predictable boost in prices for essential goods, as well as well-intentioned but ill-advised government attempts to cap what businesses can charge for those items. Such measures certainly leave an impact: eBay, for example, responded to that pressure yesterday, announcing that it would leave the market entirely and pull all coronavirus-related supplies from its virtual stores.

“As you may have noted, we are seeing literally small hand sanitizers like this going for as much as $17,” said California Governor Gavin Newsom, a Democrat, calling the widespread price increases in the state “unconscionable” and “usurious.” Violators in Newsom’s jurisdiction face up to a $10,000 fine and a year in jail. Sen. Ed Markey (D–Mass.) specifically turned to Amazon: While the company and the suppliers it works with “have a right to expect a reasonable return on the products they sell,” he wrote in a letter to CEO Jeff Bezos, “they do not have a right to impose unjustifiably high prices on consumers who are seeking to protect themselves against the coronavirus.”

The immediate implications are alarming: How can a private business owner be subject to crippling fines (or even imprisonment) for setting his or her own prices? Yet that question misses the full point. It fails to address that prices responding to the market—as they tend to do—is a good thing, even in the face of a deadly pandemic.

Accusations of greed hurdled toward price-gouging business owners are understandable, particularly when people are suffering. But compare that with a world of government-imposed price caps. Those ceilings force businesses to sell in-demand goods at artificially low prices, which fail to signal that said goods are scarce. Absent that marker, supplies are then quickly exhausted, depriving many vulnerable people of the ability to get their hands on any.

Though most critics claim price-gougers are the ones depriving needy people of important goods, that’s rarely true in practice. Consider this hypothetical: Businesses across the state of California (a nod to Newsom) opt to not raise prices on hand sanitizer, greatly increasing the likelihood that a small cohort of people concerned about coronavirus will buy a large share of the item in bulk. Since there is a limited supply of hand sanitizer in the marketplace, the immobile elderly woman next door who hadn’t yet made her assisted sojourn to CVS is basically out of luck. And, in this case, she is more at risk of succumbing to the disease, should she contract it.

Perhaps worst of all, regulatory restrictions on pricing can, in some cases, force third-party sellers to exit the market entirely, as seen with eBay. Though it sounds like a doomsday scenario, it’s exactly what the retail giantchose to do yesterday when it began pulling all surgical face masks, hand sanitizers, and disinfectant wipes, opting not to go head-to-head with the 34 states that have strict price-gouging regulations. While the consequences vary across the U.S., the liabilities clearly outweighed the risk of selling vital goods.

“We will continue to monitor the evolving situation and quickly remove any listing that mentions COVID-19, coronavirus, 2019nCoV (except books) in the title or description,” the company wrote in a blog post. “These listings may violate applicable US laws or regulations, eBay policies, and exhibit unfair pricing behavior for our buyers.”

This is quite literally why we can’t have nice things.

from Latest – Reason.com https://ift.tt/2PToT18

via IFTTT

NIMBY Seattle-Area Residents Resist Coronavirus Quarantine Plan For Local Motel

Seattle residents are pushing back against officials in King County, Washington, who plan to use emergency powers to buy and renovate an Econo Lodge located south of the city to house coronavirus patients, according to Bloomberg.

The mayor of Kent, Washington – a Seattle suburb near the airport where the 85-bed motel is located, was livid over the plan. While local workers and residents are staunchly opposed as well.

“We’re one of the largest cities in the county, and we know we have a role to play in preventing the spread of the virus,” said Kent Mayor Dana Ralph in a phone interview. “But we were not included in the conversation or decision making.”

This type of consternation is common when a community pushes back against an unwanted project — inspiring the term Nimby for “not in my backyard.” This time, the backlash comes as health officials try to contain a spreading public health crisis, revealing a challenge that many communities across the U.S. may face as they try to slow the outbreak.

“Washington state counties are not the only places where that is going to be discussed,” said Irwin Redlener, a disaster preparedness expert and public health professor at Columbia University in New York. “We might have to adopt procedures and protocols that would be unacceptable in the absence of a true national emergency. In other words, our standards might have to get much more lax.” –Bloomberg

Residents of Kent aren’t the only ones resisting quarantine plans. Last month, federal officials were forced to scrap a plan to house coronavirus evacuees from a cruise ship to a FEMA facility in Anniston, Alabama, after locals and the city council opposed the move.

In Orange County, California, residents are also up in arms over a proposal to place some patients in a state-owned facility.

The Econo Lodge plan would include $4 million for the purchase of the motel and an additional $1.5 million in emergency funds to renovate it, as well as hire as many as 11 existing employees to run the facility. It would be used to house coronavirus patients who are infected but not seriously ill, as part of an effort to keep hospital beds available for those who need them, according to Bloomberg. According to county officials, it was the only property on the market that met their criteria of separate heating and cooling systems for each room, and doors which open to the outside, rather than a hallway.

“From that perspective, a motel is a very good solution,” said NYU School of Public Health professor David Abramson. “They’re almost entirely private spaces.”

On Thursday morning, cars raced by on the highway behind the motel, where a room with a single bed was going for $78.68 a night. Trucks were parked at the edge of the property, which sits near a Denny’s, a bowling alley and a Ford dealership.

Inside, confusion and anger reigned. The front-desk worker at the motel, who asked to not be identified by name, said that she had learned about the plan to quarantine coronavirus patients from news reports and was strongly opposed. She had yet to hear from her manager whether she would still have a job. And, even if she did, she wasn’t sure she wanted it for fear of infecting her family. –Bloomberg

Without interference, the facility could open within two weeks. According to the report, King County officials are also looking at other quarantine locations, including in Seattle.

That is, if the locals don’t stand in the way.

“I’m sorry for the people who are going through this,” said 35-year-old Rupali Handa, who said that officials should quarantine people “somewhere else.”

Are you ready for this week’s absurdity? Here’s our Friday roll-up of the most ridiculous stories from around the world that are threats to your liberty, your finances, and your prosperity… and on occasion, poetic justice.

* * *

Hillary Clinton’s Email Scandal Just Rose From the Dead

Ignorance of the law is no excuse for you or me.

But somehow when Hillary Clinton broke the law while Secretary of State, it was her intentions that mattered.

As everyone knows by now, Clinton stored confidential, top secret emails on a personal, unsecured email server while she was Secretary of State.

She got off the hook because she claimed that she didn’t intend to violate the law… she didn’t realize that what she was doing was totally illegal.

That’s why she’s not rotting in a prison cell, even though you or I would be turning big rocks into little rocks in a DayGlo Orange jumpsuit if we had committed an equivalent crime.

But a group called Judicial Watch wasn’t as quick to let it go.

Using Freedom of Information Act requests, they continued to uncover more and more details of the case and bringing it all to court. And as the judge in the case commented, “With each passing round of discovery, the Court is left with more questions than answers.”

Therefore a federal judge has permitted another round of discovery. This means Hillary Clinton will be forced to sit for an interview with government officials to answer “significant questions” about her violation of the law.

Police in Scotland have a list of people who tell offensive jokes

Scottish Internet users better be careful of the jokes they tell online– you might end up on a government watchlist.

A Freedom of Information request revealed that 3,300 “non-crime hate incidents” have been logged in a police database.

Hundreds of people were added to the list last year for making offensive jokes or rude comments online.

Police say they track these individuals just in case their humor crosses the line into illegal territory.

For example, a couple years ago a Scottish YouTuber was arrested and convicted for teaching his pug a Nazi salute.

They guy may have been way too sophomoric… but when did it become a crime to be immature and offensive?

And now free speech is being monitored for signs of criminality.

Plus, with certain types of background checks, potential employers could see that these innocent people have been logged social media posts deemed to be offensive by the government.

School forbade kids from saying no when asked to dance

I just love it when wokeness contradicts itself.

A middle school in Utah was gearing up to host its Valentine’s Day dance. And in an effort to make sure that all students felt “welcome, comfortable, safe, and included,” the school adopted a policy forcing the kids to dance with anyone who asked them.

And sure enough, when an 11-year old girl was asked to dance by a boy who creeped her out, the principal forced them to dance together.

This is pretty much the opposite of #MeToo.

And in their ridiculous effort to make sure that no student was upset or offended, they violated one of the most basic consent rules in our society.

This is the paradox of wokeness: it’s absolutely impossible to prevent people from feeling upset, offended, excluded, or rejected.

Update: woman pleads guilty to being topless in her own home

We’ve been following the case of Tilli Buchanan who was charged with sex crimes for being topless in her own home.

She and her husband had removed their shirts after installing insulation. Because her step-children saw her barechested, Tilli was charged with “child sex abuse” under Utah criminal code 76-9-702.5(2)(a)(ii)(B) for exposing “the female breast below the top of the areola. . .”

That left her facing the possibility of having to register as a child sex offender.

Originally she tried to challenge the law itself under equal protection grounds, since it treated male and female nipples differently.

But when she lost that case, she opted to take a plea deal. The charges were downgraded so she won’t be considered a sex offender.

Tilli will pay $600 and the case will be dismissed in a year if she doesn’t commit any crimes.

It’s pretty pathetic that she was ever charged in the first place, and sad that this is what the justice system wastes resources on.

With markets tumbling and confirmed cases of coronavirus rising, President Donald Trump is reportedly considering a fiscal stimulus plan. Already the president has urged Congress to pass a payroll tax cut and said the Federal Reserve should cut interest rates beyond what it already has done.

Others are pushing for even more aggressive actions. In an op-ed published Thursday in The Wall Street Journal, Jason Furman argues that Congress should “swiftly” pass a $350 billion stimulus to counter the “mounting economic risks posed by the spread of the novel coronavirus.” While Trump has considered a temporary payroll tax cut to boost the economy, Furman, a former economic advisor to President Barack Obama, prefers straight cash. “Congress should pass a simple one-time payment of $1,000 to every adult who is a U.S. citizen or a taxpaying U.S. resident, and $500 to every child,” he argues—an amount that would be even more generous than the 2008 stimulus passed during the Bush administration.

There are at least three good reasons to question whether any economic stimulus would be a wise response to the coronavirus—over and above the obvious questions about the federal government’s ability to finance a big stimulus while already running a $1 trillion annual budget deficit.

First, the severity of any economic shock caused by the coronavirus is still unknown.

Keep in mind that—despite the president’s obsession with it—the stock market is not a gauge of the economy itself. It’s a gauge of how people think the economy will be in the future. This week’s sell-off reflects pessimism, but that’s not the same as an actual economic shock. If the virus’ impact ends up being less bad than expected, the stock market will recover the lost value.

So far, that unknown seems to be keeping the White House from doing anything too aggressive. In an interview with CNBC on Friday morning, the president’s top economic advisor, Larry Kudlow, said the preference is for a “targeted approach” aimed at “individuals who might lose paychecks” and “small businesses that might get hurt” by the economic disruption expected to be caused by the outbreak. Of course, big businesses like airlines can be expected to have their hands out too if there is any talk of a coronavirus bailout.

Second, there’s the time it would take for any economic stimulus to have an effect.

As Furman conceded, studies show that it takes as much as a full year for monetary policy stimulus—for example, the Fed lowering interest rates—to have a measurable effect on the economy. That’s because lower interest rates encourage people and businesses to borrow money for big purchases (homes, new plants, etc.) but those decisions aren’t made overnight.

If the timing of the crisis rules out monetary stimulus, then what about fiscal stimulus—sending a thousand bucks to every American? That may not work either, partly because of the nature of the disruption that’s expected from the coronavirus and partly because of how fiscal stimulus works.

Most economists are worried about a supply-side shock—that is, a disruption in getting enough goods to market to meet demand. If China’s factories are closed for a substantial period of time or ships are unable to travel from port to port for fear of spreading the disease, global supply chains will be disrupted. The economic effects of the virus are fundamentally different from those of, say, the 2008 recession. Most of the long-term effects of the recession were demand-side problems—not enough people buying houses, for example, or the general slackening in demand that comes when millions of people suddenly lose their jobs. In short, there were too many sellers and not enough buyers.

This is a different problem. If global supply chains are seriously disrupted, there will not be enough goods to sell and too many people wanting to buy. That’s why you can’t find hand sanitizer on Amazon right now.

That’s the third problem with the stimulus idea. Putting more money in the pockets of every American, either by cutting payroll taxes or by mailing checks, would tend to juice the economy faster than cutting interest rates. But that assumes there are goods and services available for them to buy.

“You cannot buy stuff that does not exist,” writes economist Tony Lima. And as he warns, dumping more cash into an economy experiencing a supply-side shock is likely to trigger inflation.

The good news is that history suggests supply-side disruptions tend to pass pretty quickly. Demand usually bounces back quickly too. “You get a V[-shaped recovery] because people now do the spending they didn’t do the last quarter,” Doug Holtz-Eakin, president of the conservative American Action Forum and former economic advisor to George W. Bush, tellsNew York.

In arguing for a stimulus, Furman compares it to the coronavirus vaccine that scientists are working to develop. “It would be nice if there existed a comparably targeted medicine for economic policymakers to administer,” he writes.

Indeed it would. But as doctors will tell you, administering vaccines to patients with weakened immune systems can be disastrous. Given the United States’ already perilous national debt and rising deficit, the White House and Congress should be cautious about spending additional money to avoid a coronavirus-caused recession—especially since the “vaccine” doesn’t seem like a sure bet.

from Latest – Reason.com https://ift.tt/2InoH6e

via IFTTT

The qualifying criteria for the next Democratic debate are out, and they manage to exclude the only veteran and only woman of color left in the race: Rep. Tulsi Gabbard (D–Hawaii).

This afternoon, Politico reported that the candidates still in the running for the Democratic presidential nomination will need to have earned at least 20 percent of the delegates awarded thus far in order to participate in the March 15 debate hosted by CNN and Univision in Phoenix, Arizona.

That means that only former Vice President Joe Biden and Sen. Bernie Sanders (I–Vt.), who respectively have 48 percent and 41 percent of the delegates so far, will be on next Sunday’s stage.

Despite her strong showing in the American Samoa caucuses where she won two delegates, Gabbard still falls short of that very high threshold.

Had the Democratic National Committee stuck with its criteria for the last debate it held on February 25—which only required each candidate to have won a single delegate—Gabbard would have qualified.

DNC Communications Director Xochitl Hinojosa foreshadowed this decision on Super Tuesday, saying on Twitter that “by the time we have the March debate, almost 2,000 delegates will be allocated. The threshold will reflect where we are in the race, as it always has.”

We have two more debates– of course the threshold will go up. By the time we have the March debate, almost 2,000 delegates will be allocated. The threshold will reflect where we are in the race, as it always has.

In response to the expected rule change, Gabbard tweeted Thursday about her campaign’s foreign policy focus, and how that can’t be separated from the domestic issues that have gotten the most attention in past debates.

I welcome the opportunity to raise & discuss the foreign policy challenges we face, like the new cold war/nuclear arms race, Turkey's efforts to drag the U.S. into a war with Russia over Syria, the coronavirus, & more. Domestic policy cannot be separated from foreign policy. https://t.co/jgVxSz1huX

Biden and Sanders have sparred in the past over the former’s initial support for the Iraq War, so there is some chance that the two candidates’ contrasting foreign policy visions will be on display come the next debate.

Still, it might have been interesting to have Gabbard, an Iraq War veteran, up on stage to offer her own unique perspective on foreign policy. She’s repeatedly argued that rising tensions between the U.S., Russia, and China is putting the country on the road to nuclear war.

A Bernie-Biden smackdown will likely feature less talk of a nuclear apocalypse and a lot more bickering about health care. That’s enough to get anyone running for their fall out shelter.

from Latest – Reason.com https://ift.tt/3cAZ4g0

via IFTTT

With markets tumbling and confirmed cases of coronavirus rising, President Donald Trump is reportedly considering a fiscal stimulus plan. Already the president has urged Congress to pass a payroll tax cut and said the Federal Reserve should cut interest rates beyond what it already has done.

Others are pushing for even more aggressive actions. In an op-ed published Thursday in The Wall Street Journal, Jason Furman argues that Congress should “swiftly” pass a $350 billion stimulus to counter the “mounting economic risks posed by the spread of the novel coronavirus.” While Trump has considered a temporary payroll tax cut to boost the economy, Furman, a former economic advisor to President Barack Obama, prefers straight cash. “Congress should pass a simple one-time payment of $1,000 to every adult who is a U.S. citizen or a taxpaying U.S. resident, and $500 to every child,” he argues—an amount that would be even more generous than the 2008 stimulus passed during the Bush administration.

There are at least three good reasons to question whether any economic stimulus would be a wise response to the coronavirus—over and above the obvious questions about the federal government’s ability to finance a big stimulus while already running a $1 trillion annual budget deficit.

First, the severity of any economic shock caused by the coronavirus is still unknown.

Keep in mind that—despite the president’s obsession with it—the stock market is not a gauge of the economy itself. It’s a gauge of how people think the economy will be in the future. This week’s sell-off reflects pessimism, but that’s not the same as an actual economic shock. If the virus’ impact ends up being less bad than expected, the stock market will recover the lost value.

So far, that unknown seems to be keeping the White House from doing anything too aggressive. In an interview with CNBC on Friday morning, the president’s top economic advisor, Larry Kudlow, said the preference is for a “targeted approach” aimed at “individuals who might lose paychecks” and “small businesses that might get hurt” by the economic disruption expected to be caused by the outbreak. Of course, big businesses like airlines can be expected to have their hands out too if there is any talk of a coronavirus bailout.

Second, there’s the time it would take for any economic stimulus to have an effect.

As Furman conceded, studies show that it takes as much as a full year for monetary policy stimulus—for example, the Fed lowering interest rates—to have a measurable effect on the economy. That’s because lower interest rates encourage people and businesses to borrow money for big purchases (homes, new plants, etc.) but those decisions aren’t made overnight.

If the timing of the crisis rules out monetary stimulus, then what about fiscal stimulus—sending a thousand bucks to every American? That may not work either, partly because of the nature of the disruption that’s expected from the coronavirus and partly because of how fiscal stimulus works.

Most economists are worried about a supply-side shock—that is, a disruption in getting enough goods to market to meet demand. If China’s factories are closed for a substantial period of time or ships are unable to travel from port to port for fear of spreading the disease, global supply chains will be disrupted. The economic effects of the virus are fundamentally different from those of, say, the 2008 recession. Most of the long-term effects of the recession were demand-side problems—not enough people buying houses, for example, or the general slackening in demand that comes when millions of people suddenly lose their jobs. In short, there were too many sellers and not enough buyers.

This is a different problem. If global supply chains are seriously disrupted, there will not be enough goods to sell and too many people wanting to buy. That’s why you can’t find hand sanitizer on Amazon right now.

That’s the third problem with the stimulus idea. Putting more money in the pockets of every American, either by cutting payroll taxes or by mailing checks, would tend to juice the economy faster than cutting interest rates. But that assumes there are goods and services available for them to buy.

“You cannot buy stuff that does not exist,” writes economist Tony Lima. And as he warns, dumping more cash into an economy experiencing a supply-side shock is likely to trigger inflation.

The good news is that history suggests supply-side disruptions tend to pass pretty quickly. Demand usually bounces back quickly too. “You get a V[-shaped recovery] because people now do the spending they didn’t do the last quarter,” Doug Holtz-Eakin, president of the conservative American Action Forum and former economic advisor to George W. Bush, tellsNew York.

In arguing for a stimulus, Furman compares it to the coronavirus vaccine that scientists are working to develop. “It would be nice if there existed a comparably targeted medicine for economic policymakers to administer,” he writes.

Indeed it would. But as doctors will tell you, administering vaccines to patients with weakened immune systems can be disastrous. Given the United States’ already perilous national debt and rising deficit, the White House and Congress should be cautious about spending additional money to avoid a coronavirus-caused recession—especially since the “vaccine” doesn’t seem like a sure bet.

from Latest – Reason.com https://ift.tt/2InoH6e

via IFTTT

The qualifying criteria for the next Democratic debate are out, and they manage to exclude the only veteran and only woman of color left in the race: Rep. Tulsi Gabbard (D–Hawaii).

This afternoon, Politico reported that the candidates still in the running for the Democratic presidential nomination will need to have earned at least 20 percent of the delegates awarded thus far in order to participate in the March 15 debate hosted by CNN and Univision in Phoenix, Arizona.

That means that only former Vice President Joe Biden and Sen. Bernie Sanders (I–Vt.), who respectively have 48 percent and 41 percent of the delegates so far, will be on next Sunday’s stage.

Despite her strong showing in the American Samoa caucuses where she won two delegates, Gabbard still falls short of that very high threshold.

Had the Democratic National Committee stuck with its criteria for the last debate it held on February 25—which only required each candidate to have won a single delegate—Gabbard would have qualified.

DNC Communications Director Xochitl Hinojosa foreshadowed this decision on Super Tuesday, saying on Twitter that “by the time we have the March debate, almost 2,000 delegates will be allocated. The threshold will reflect where we are in the race, as it always has.”

We have two more debates– of course the threshold will go up. By the time we have the March debate, almost 2,000 delegates will be allocated. The threshold will reflect where we are in the race, as it always has.

In response to the expected rule change, Gabbard tweeted Thursday about her campaign’s foreign policy focus, and how that can’t be separated from the domestic issues that have gotten the most attention in past debates.

I welcome the opportunity to raise & discuss the foreign policy challenges we face, like the new cold war/nuclear arms race, Turkey's efforts to drag the U.S. into a war with Russia over Syria, the coronavirus, & more. Domestic policy cannot be separated from foreign policy. https://t.co/jgVxSz1huX

Biden and Sanders have sparred in the past over the former’s initial support for the Iraq War, so there is some chance that the two candidates’ contrasting foreign policy visions will be on display come the next debate.

Still, it might have been interesting to have Gabbard, an Iraq War veteran, up on stage to offer her own unique perspective on foreign policy. She’s repeatedly argued that rising tensions between the U.S., Russia, and China is putting the country on the road to nuclear war.

A Bernie-Biden smackdown will likely feature less talk of a nuclear apocalypse and a lot more bickering about health care. That’s enough to get anyone running for their fall out shelter.

from Latest – Reason.com https://ift.tt/3cAZ4g0

via IFTTT

Massacre In Kabul Targeted Politicians, Leaves 27 Dead – Presidential Candidate Barely Escapes

At a crucial moment at which the historic US-Taliban peace deal appears hanging by a thread – if not already dead altogether – and as Pompeo is dubiously pledging to keep it alive and push forward, gunmen have carried out a massacre in Kabul which nearly killed top Afghan political leader, Abdullah Abdullah.

At a moment top national leaders were attending a Shia commemoration ceremony in the Afghan capital, gunmen unleashed a hail of bullets in a major coordinated attack, killing at least 27 people, according to a health ministry statement.

British soldiers responded to the massive Friday attack, via AP/CNN.

“Twenty-seven bodies and 29 wounded transported by … ambulance so far,” a health ministry spokesman told Reuters in the aftermath. The number of wounded was later updated to at least 55 injured in the attack.

Crucially, the country’s Chief Executive and presidential candidate Abdullah Abdullah escaped unharmed, as well as the chairman of the Afghan High Peace Council Karim Khalili — who was giving a speech at the very moment the attack started, said to include rockets fired toward the crowd.

Khalili is seen in video frantically leaving the stage mid-speech as gunfire rings out, fleeing for his life:

“The attack started with a boom, apparently a rocket landed in the area, Abdullah and some other politicians … escaped the attack unhurt,” Abdullah’s spokesman, Fraidoon Kwazoon, told Reuters.

CNN describes that armed men began firing down on the crowd from a nearby high-rise building, and in the hours after security forces were described as still pursuing the attackers.

Afghanistan’s Chief Executive under President Ashraf Ghani, Abdullah Abdullah, via DW.

Abdullah Abdullah said after escaping: “I will not blame anybody for this because I don’t have a full picture from our security forces, but we need to know who is, or who were, behind it,” according to CNN.

Crucially, the Taliban denied any involvement in the attack, and it’s as yet unclear just who was behind it, though the same commemoration event of a prior Shia national unity figure has in past been subject of armed attack.

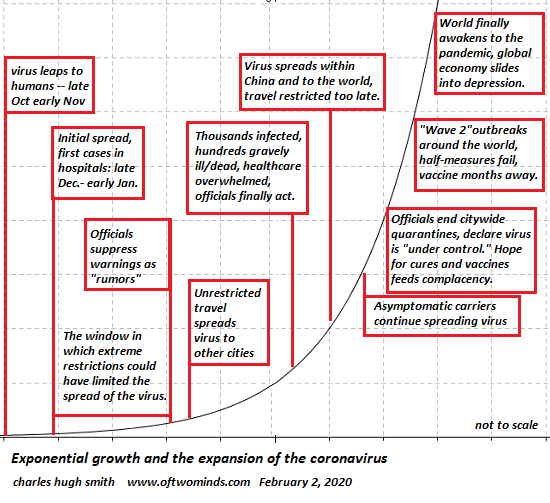

The present disconnect between the science of Covid-19 and the status quo’s complacency is truly crazy-making, as we face a binary situation: either the science is correct and all the complacent are wrong, or the science is false and all the complacent are correct that the virus is no big deal and nothing to fret about.

Complacency is ubiquitous: readers on Facebook leave comments on my posts “this is silly.” Correspondents report that people don’t even cover their mouths when coughing, much less use a tissue. People keep repeating like a mantra that a bad flu season kills 35,000 in the U.S. alone, and so why worry about a couple thousand deaths globally?

Another common trope is “hepatitis kills far more people in the U.S., so why worry about the coronavirus?”

So let’s look at some data and consider what science can tell us about the potential consequences of the Covid-19 virus spreading as widely as conventional flu viruses.

The fallacy made by the complacent is that the number of cases will remain small (in the dozens or hundreds) and so the number of deaths will also remain small.

Since the evidence suggests the Covid-19 virus is more contagious than conventional flu viruses, a reasonable assumption is that it will eventually infect more people than a conventional flu, which according to the CDC infects up to 45 million Americans annually.

According to the CDC, viral hepatitis B caused 5,600 deaths in the U.S. in 2017, and hepatitis C caused 19,000 deaths, for a total of 24,600. That certainly exceeds reported deaths of Covid-19, but since the statistics presented by the Chinese government are unreliable, we have no idea how many people have the virus and how many have died.

According to the CDC, influenza and pneumonia together caused 55,000 deaths in the U.S. in 2017.

Given the scientific evidence that Covid-19 is highly contagious, let’s do a Pareto Distribution (80/20 rule) projection and estimate that 20% of the the U.S. population gets Covid-19. That’s 66 million people, roughly 50% higher than the 45 million who catch a flu virus in a “bad flu” season.

Data suggests between 2% and 3.4% of all Covid-19 cases end in death, but the deaths are concentrated in the 20% of cases that become severe, and in the vulnerable populations within the 20% severe cases that require hospitalization.

Using the lower CFR (case-fatality rate) rate, 2% of 66 million is 1.3 million, so if Covid-19 infects only 20% of the U.S. populace, current data suggests 1.3 million people will die. This is considerably more than 24,600,or 55,000. (Total annual deaths in the U.S. are around 2.8 million.)

But these mortality data are drawn from small numbers of patients who have had access to intensive care. Anecdotal evidence from places where the healthcare system has been overwhelmed (Wuhan) so intensive care is unavailable to the majority of severely ill patients suggest much higher death rates around 15%, with worst-case scenarios going as high as 80% mortality for untreated severe cases in vulnerable populations (elderly and chronically ill).

If 20% of all cases can be expected to be severe and require hospitalization/intensive care (20% of 66 million is 13 million people), then intensive care will quickly become unavailable due to the low number of intensive care beds in the U.S. (94,000). The total number of all hospital beds in the U.S. is around 931,000. (Recall that the majority of these beds are already in use, so the number available to those severely ill with Covid-19 is a fraction of the total.)

If 15% of untreated severely ill patients die, that is 13 million X 15% = 1.95 million.

So let’s cut all these numbers in half: let’s assume only 10% of the U.S. populace gets the Covid-19 virus (33 million), so only 6.6 million people become severely ill. If 15% of untreated severely ill patients eventually die, that’s 1 million deaths in the U.S. alone.

In other words, the death rate is only low if the number of severely ill patients remains very low. Once the number of patients needing hospitalization exceeds the number of ICU beds, the death rate leaps dramatically.

Authorities are well aware of the potential for the Covid-19 to spread rapidly and cause a great many deaths. But they’re also concerned about the consequences of an economic crash as people avoid public places (i.e. “social distancing”) as the most effective preventative measure to reduce the chances of contracting the virus.

The resulting layoffs and business closures will trigger financial and economic consequences that may not be recoverable if these trends self-reinforce (more layoffs cause consumption to decline, triggering more layoffs, etc.).

If authorities downplay the Covid-19 pandemic and encourage people to continue flying, gathering in public, etc. in order to keep the economy humming, that will accelerate the spread of the virus.

When people awaken to the dangers of the pandemic (for example, when ICU beds are all filled and severely ill patients are being turned away), they will panic and pursue “social distancing” regardless of what officials say. When complacency gives way to panic (yes, it can happen here and yes, it can happen to you), the economy will crash.

In other words, the economy will crash either way: if authorities force “social distancing” to limit the spread of the virus or if they downplay the pandemic and let the virus spread to the point that people panic and “socially distance” themselves regardless of official entreaties to get out there and buy, buy, buy.

Forcing “social distancing” won’t stop the eventual spread of the virus, because as soon as restrictions are eased the virus will enter the newly open cities via asymptomatic carriers and a second wave of infections will spread. Forcing “social distancing” while thousands of airline flights and railway travel continue to spread asymptomatic carriers to every transportation node on the planet is not going to stop the spread of the virus.

The science suggests a significant percentage of the human populace will eventually get the Covid-19 virus. Estimates run from 40% to 70%; You’re Likely to Get the Coronavirus (The Atlantic).

Common sense suggests complacency is misplaced, and efforts should be made to minimize the risk of getting the virus until a reliable vaccine is available, which those with experience in the field suggest might be a year or 18 months away.

The science is telling us that the global economy will experience a depression as these realities sink in. Authorities pushing complacency as a short-term financial panacea are doing an enormous disservice to the people who entrusted them with power. The more effective strategy would be to prepare to deal with a global depression while limiting the spread of the virus by whatever means are available, which at present boils down to social distancing and increased hygiene.

Here is an example of status quo complacency in the U.S.: the person returns from Japan with symptoms of Covid-19, tests negative for conventional flu and other viruses, CDC refuses to test for Covid-19, no special protocols despite the obvious risk of Covid-19, staff tells the patient to go home by whatever transport he/she normally uses. My COVID-19 Story. Brooklyn. (via Maoxian)

So either the science is wrong and the complacent will be proven correct, or the science is correct and the complacent will be wrong.

Carnage Crushes Credit, Crude, & The Yield Curve As Fed Admits “Credibility Eroding”

The global equity market cap collapsed by a record $9tn – or two-thirds of China’s GDP – in 9 days, while global; sovereign 10-year bond yields crashed below 1.00% for the first time ever…

Source: Bloomberg

Even the veteran-ist of veteran traders were shocked by this week’s moves…

“Panic moved up a few notches from already extremely high levels,”said one trader today,

“I thought last Friday was the blow off top and then a few times this week before today but now its beyond belief,” he said, noting the rally in 30-yr to all- time lows.

The flip from Extreme-est Greed to Extreme-est Fear was unprecedented…

Or put another way…

But the real shock was from Federal Reserve Bank of St. Louis President James Bullard, who admitted central banks are losing their credibility rapidly: “Many central banks have consistently missed their stated inflation targets to the low side for many years… Critically, the central bank has to be able to actually deliver the required.” Which means…

“Credibility of central banks, instead of improving over time based on the achievement of stated goals, seems to be eroding instead.”

That’s quite an admission but 100% correct and this week’s carnage after an emergency 50bps rate-cut did nothing to calm fears is a perfect example…

And despite a huge resurgence in the Fed’s balance sheet, stocks were not playing along at all…

Source: Bloomberg

Today was quite a day across every asset class. We gathered some of the most shocking market move headlines of the day for some perspective:

GLOBAL CONFIRMED CORONAVIRUS CASES SURPASS 100,000

EUROPE DEBT RISK GAUGE EXTENDS RISE TO HIGHEST SINCE JUNE 2016

GERMANY’S 10-YEAR BOND YIELD FALLS TO RECORD LOW

GERMANY’S 30-YEAR BOND YIELDS FALL TO ALL-TIME LOW

EUROPE SENIOR FINANCIAL DEBT-RISK JUMPS MOST SINCE 2018

JPMORGAN EMBIG DIVERSIFIED SOVEREIGN SPREAD RISES ABOVE 400 BPS

EMERGING-MARKET USD SOV.-BOND PREMIUM JUMPS MOST SINCE 2011

U.S. TREASURY 5-YEAR YIELD FALLS BELOW 0.50%

U.S. 30-YEAR YIELD FELL AS MUCH AS 30BP ON INTRADAY BASIS

U.S. 30-YEAR YIELD SET FOR BIGGEST ONE-DAY DROP SINCE 2009

U.S. CREDIT MARKET FEAR GAUGE SURGES MOST SINCE AT LEAST 2011

VIX’S 3-WEEK CHANGE IS BIGGEST EVER – BIGGER THAN LEHMAN

WTI CRUDE FUTURES DOWN 10.% – BIGGEST FALL SINCE 2014

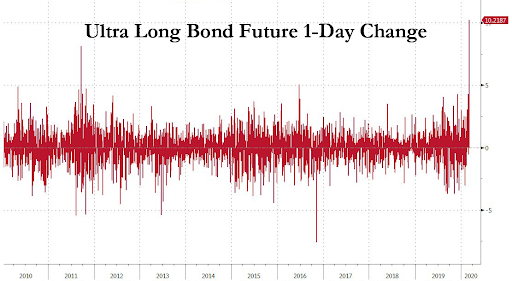

For some context – the recent bond market collapse has never, ever happened before…

If you can tell from my tone, this troubles me, so I went back and looked into this, we have never had a 50% change in 10y yield levels in either direction over a 2-wk window. We have had larger rallies (yup in 4Q08) but nothing comes close to cutting rates in half this fast… https://t.co/tP2fJAdbvfpic.twitter.com/8308IzVmwW

And as The Fed cut rates, the 30Y Yield chased it down, along with the rest of the curve…

Source: Bloomberg

As Nomura’s Charlie McElligott details, panic moves in US Rates as Duration / Convexity goes “offer-less,” with 10Y yields hitting a fresh record low of 0.6932%, multiple “limit-UP” halts in UST Ultra bond futures and 30Y UST yields crashing down -22bps at the extremes (5s30s was flatter by -14bps at one point) in an investor climate that is fixated on “imminent global recession” via pandemic “lock-down”-NYT piece stating that over 2700 people have quarantined themselves in New York City, while new cases in S Korea frighteningly re-accelerate

This obviously has the look of a Rates “convexity-event”(forced hedging / buying at the highs from mortgage investors, insurance companies and those who are “short options”—i.e. all the Vol dealer desks selling low-strike receivers for the past few years, or the market makers short those 350k ED$ “Par Calls” for Jun expiry!)…

…but this is also a simple function of OIS markets now pricing-in a full ADDITIONAL 50bps rate cut on March 18th from the Fed already, as well as the obvious dynamic where “Rates are your everything hedge” from cross-asset investors (i.e. Equity L/S investors buying ED$ upside).

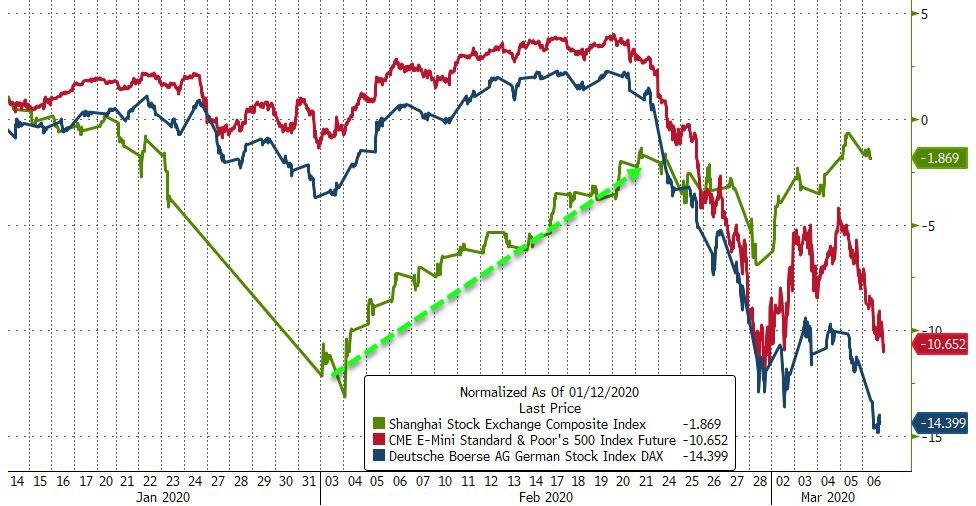

China is still massively outperforming US and Europe since the start of the Covid-19 crisis…

Source: Bloomberg

Today’s US equity market carnage sent all the majors into the red for the week, but the last 30 minutes saw the machines work ultra-hard to get the Dow, S&P, and Nasdaq green…

Was The PPT in the house again?

Somebody do something!

Another late-Friday panic-buy?

The Elon Musk Ramp? “The coronavirus panic is dumb”

So are we due for a bounce now?

Source: Bloomberg

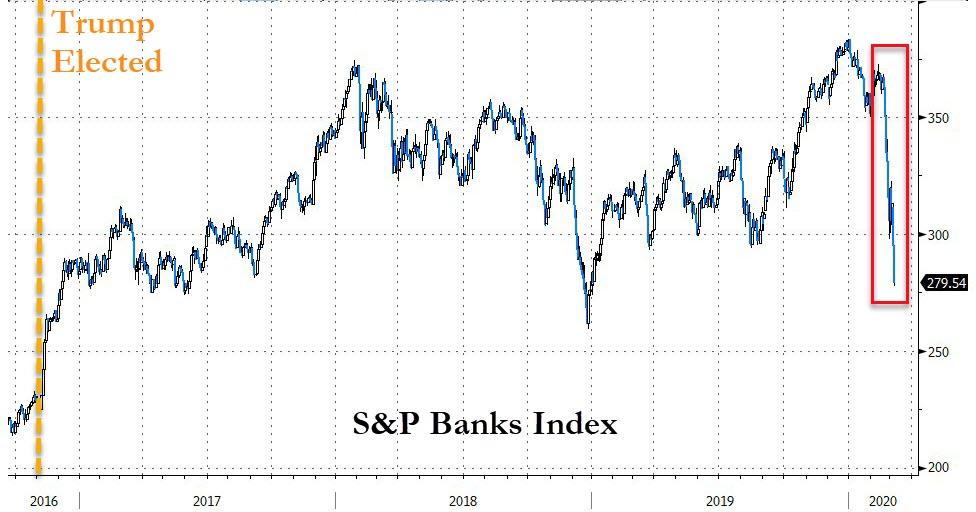

US Banks have now crashed over 27% from their early Jan highs…

Source: Bloomberg

The biggest US banks have been bloodbath’d…

Source: Bloomberg

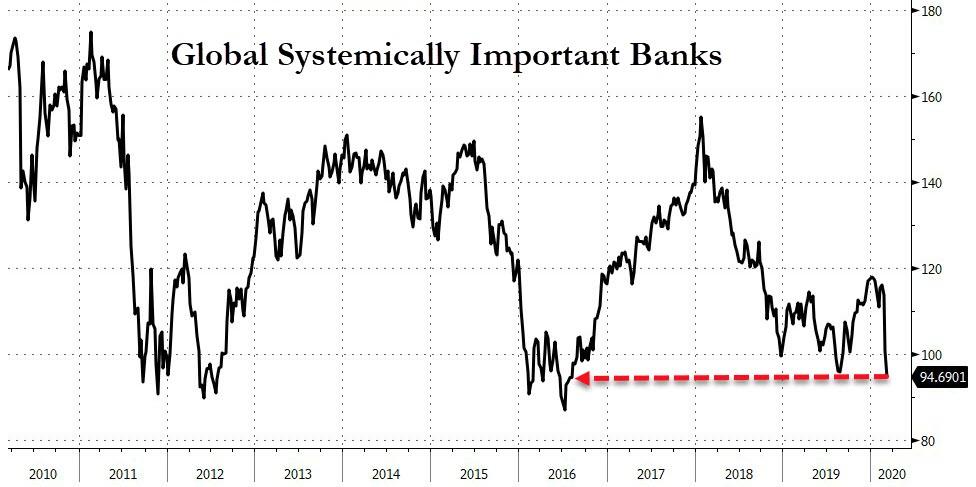

But, more worryingly, Global Systemically Important Banks stocks have crashed to their lowest since 2016…

Source: Bloomberg

While energy stocks were already getting clubbed like baby seals, the last two weeks have seen them collapse 22%…

Source: Bloomberg

MAGA Stocks have now lost over $750 billion in market cap (Note that the Q4 2018 collapse wiped just over $1 trillion)…

Source: Bloomberg

The week saw defensives dominate as cyclicals were hammered…

Source: Bloomberg

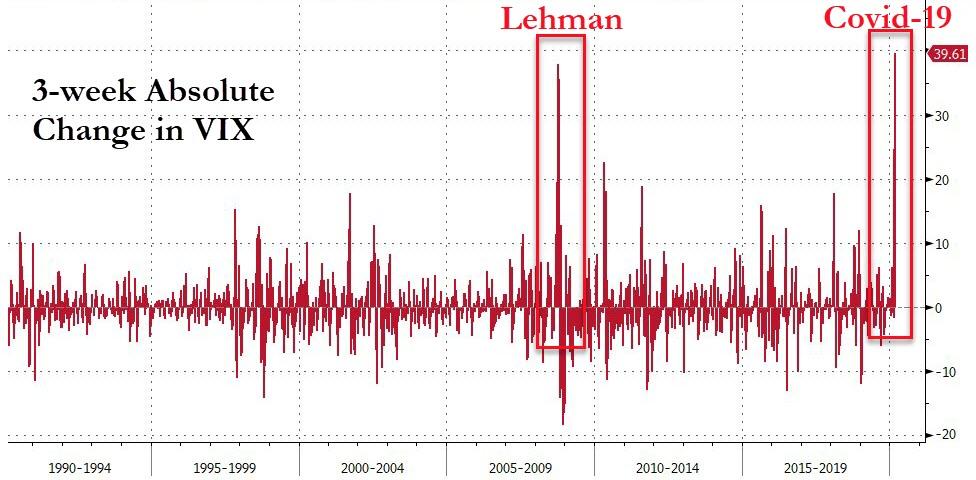

VIX topped 54 intraday for the first time since 2009…

This is the biggest 3-week surge in VIX… ever…

Source: Bloomberg

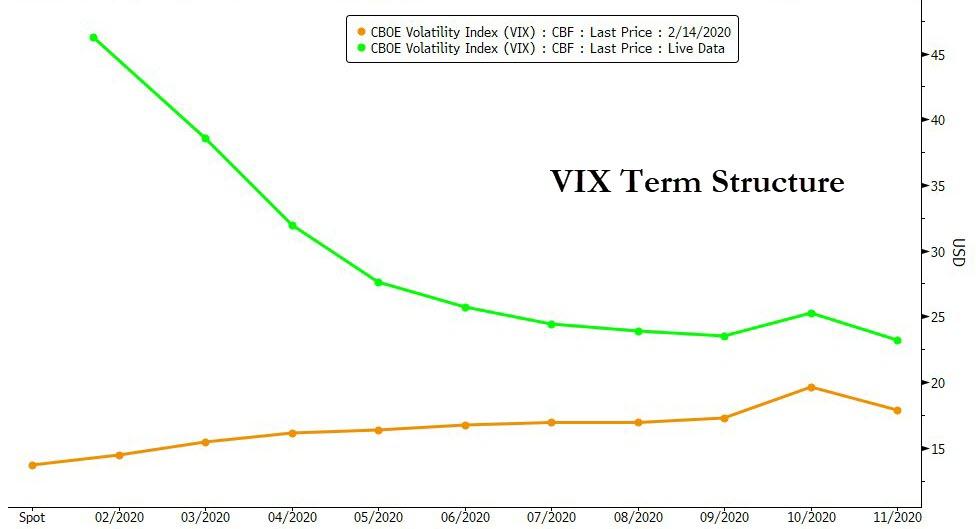

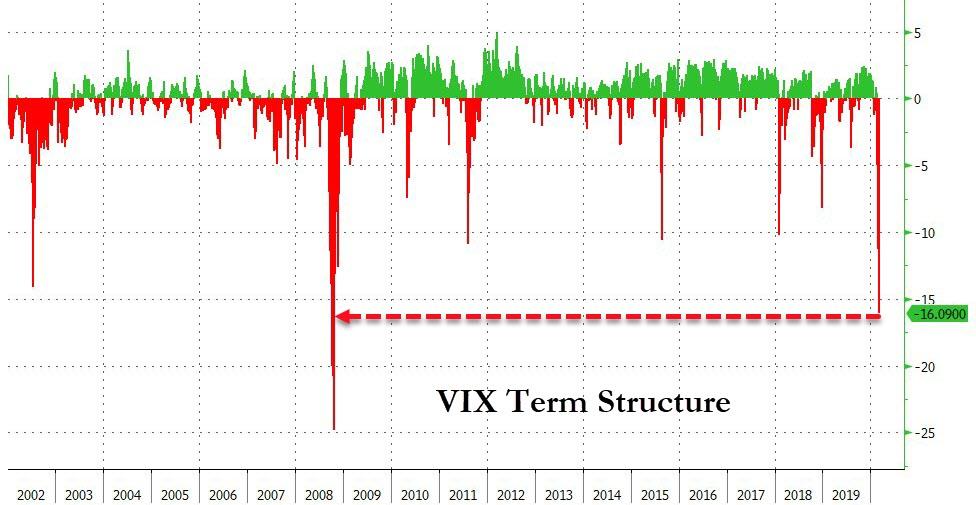

The VIX term structure is in massive backwardation…

Source: Bloomberg

The VIX Term structure hasn’t been this inverted since Lehman…

Source: Bloomberg

Europe’s VIX exploded this week, closing at its highest since the 2011 crisis…

Source: Bloomberg

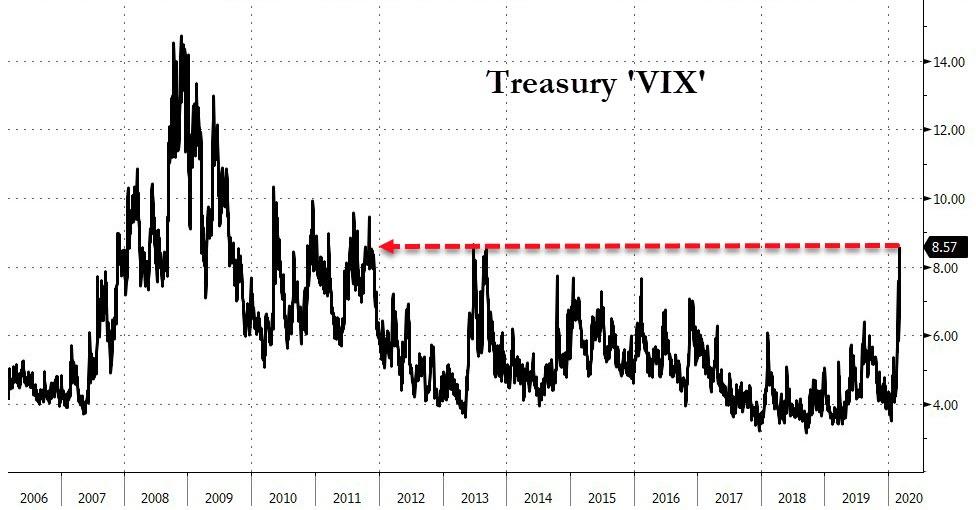

Treasury ‘VIX’ surged today to its highest since 2011…

Source: Bloomberg

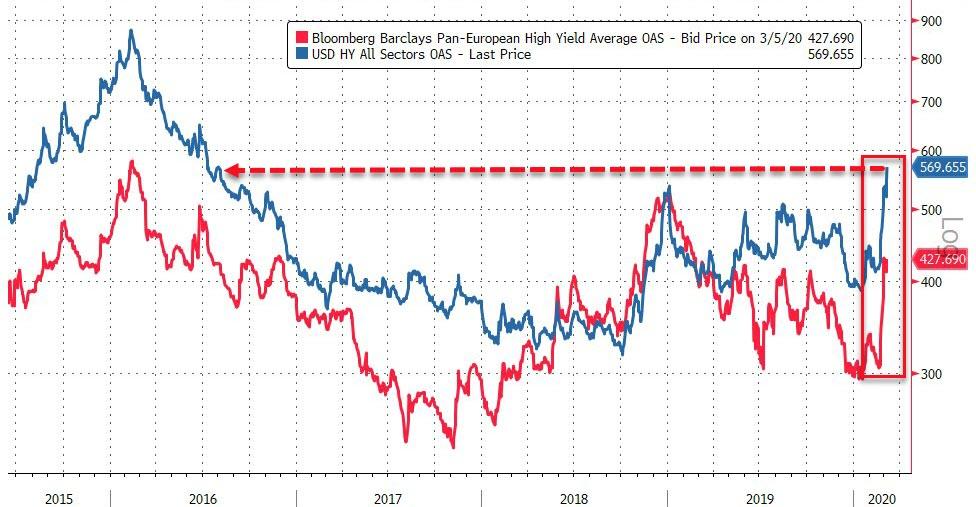

Credit markets were a bloodbath this week, with both HY and IG blowing out in US and EU…

Source: Bloomberg

And if you thought that credit’s biggest blowout ion a decade was notable, it’s nothing if it starts to catch up to its capital structure colleague on risk…

Source: Bloomberg

US Treasury yields collapse this week was nothing short of stunning with the entire curve down 40-50bps!!

Source: Bloomberg

10Y Yields crashed to a stunning 65bps overnight…

Source: Bloomberg

The 30Y Yield accelerated lower in the last hour, crashing below the Fed Funds Rate!

Source: Bloomberg

The yield curve flattened drastically,,,

Source: Bloomberg

Some perspective to where were just over a month ago…

Source: Bloomberg

The Dollar Index fell for the 2nd straight week (down 6 of the last 7 weeks)…

Source: Bloomberg

On a broad trade-weighted basis, the dollar has been gaining against the rest of its fist peers, but crashing relative to hard money…

Source: Bloomberg

Cryptos rallied on the week led by Bitcoin Cash…

Source: Bloomberg

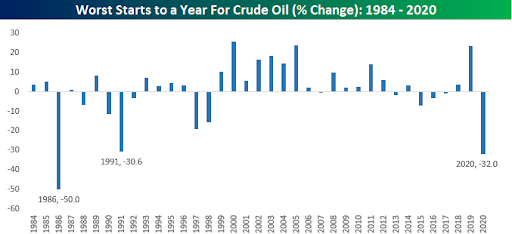

Crude was obviously the week’s biggest commodity loser , copper went nowhere as PMs were bid…

Source: Bloomberg

WTI crashed over 10% today after the collapse of OPEC+ talks, its biggest drop since 2014…

Source: Bloomberg

Brent was worse, with its biggest drop since Jan 2009…

Source: Bloomberg

Oil ‘VIX’ has exploded higher…

Source: Bloomberg

This is the worst start to a year for crude since 1986…

Spot Gold soared up to $1690 – the highest since Jan 2013

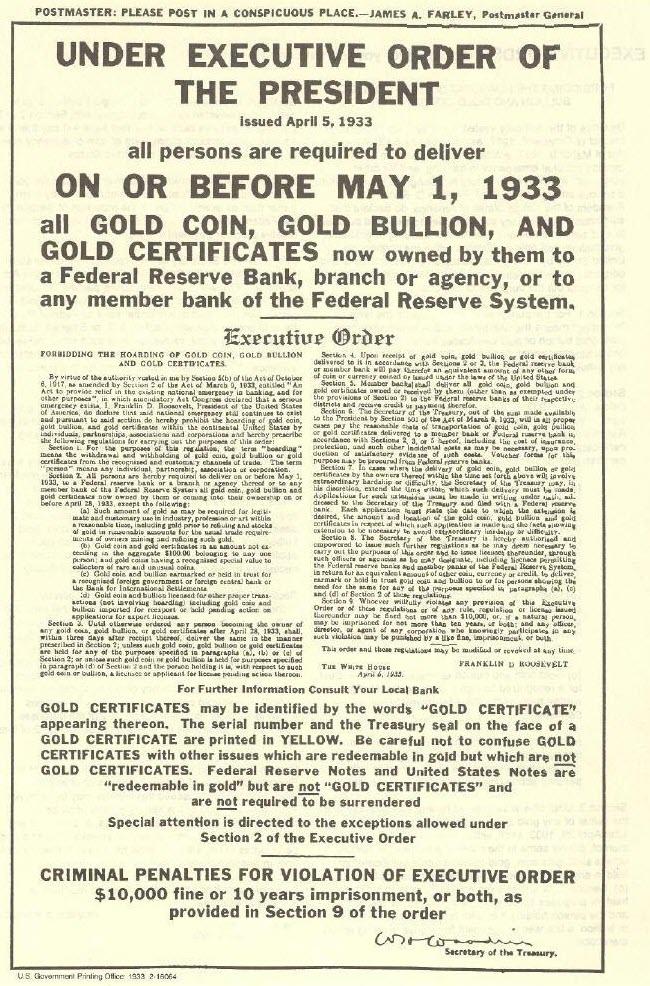

And here is the stunning punchline: out of the five historical instances of this week’s pattern of trading (leaving out the present case for obvious reasons), Nomura finds that the only instance that was followed by a sustained market rally was that of April 1933, when the US abandoned the gold standard in the midst of the Great Depression.

And while it would be next to impossible to confiscate gold, a massive dollar devaluation against the yellow metal may be just what the Fed is planning next (as Harley Bassman suggested in 2016)

As Sven Henrich tweeted into the close:

“A world without central banks in control is a scary world indeed. People actually have to actively think about their investments.”

{kind=link}

{kind=link}