Georgia’s film industry gets some big tax credits from the state government—$800 million’s worth in 2018. Both the government and the movie production companies love to claim that these subsidies bring a huge return. The eye-popping figure you usually see claims that the credits produced $9.5 billion in economic benefits in 2018 alone.

But that number is almost certaily wrong. It includes less than $3 billion in direct spending from the film industry. The rest is supposed to come from the multiplier effect, in which each dollar spent creates more spending throughout the economy. And economists have some serious questions about how valid that estimate is.

J.C. Bradbury of Kennesaw State University has argued that using a more realistic multiplier, the film industry generates, at most, $4.2 billion in annual economic output. Similarly, Bruce Seaman of Georgia State University thinks the film industry is responsible for just $6 billion in economic benefits. The state Department of Economic Development estimates that for every dollar the film industry spends in the state, overall spending increases by $3.57; Seaman argues the real value is closer to $1.87.

Georgia isn’t the only state to inflate the benefits of film production.

One especially dubious study of film tax credits, prepared for the New Mexico State Film Office, claimed that tourism alone driven by the filming of No Country for Old Men, 3:10 to Yuma, Indiana Jones and the Kingdom of the Crystal Skull, and Wild Hogs (a forgettable 2007 comedy starring Tim Allen, Martin Lawrence, William H. Macy, and John Travolta as an over-the-hill biker gang) generated more than $100 million in income for state residents over a four-year span.

Most research on film tax credits show that they don’t have much of an impact on economic growth. A National Bureau of Economic Research study from this June found that film subsidies only have a marginal impact on where TV series are filmed, and that they do not increase feature film location, employment, economic growth, or wages. Studies from Michigan and Massachusetts have found that the average length of a job credited to a film tax incentive program lasts less than a month.

Subsidies can even hurt a stateeconomy, by shifting economic resources away from productive industries and toward politically connected ones. If it weren’t for the tax subsidies, the money that Georgia directs to film production could instead go to reducing taxes broadly, allowing the people of the state to decide which businesses to support. In the meantime, there’s a good chance production companies would come even without the subsidies.

from Latest – Reason.com https://ift.tt/2XlLp8u

via IFTTT

Georgia’s film industry gets some big tax credits from the state government—$800 million’s worth in 2018. Both the government and the movie production companies love to claim that these subsidies bring a huge return. The eye-popping figure you usually see claims that the credits produced $9.5 billion in economic benefits in 2018 alone.

But that number is almost certaily wrong. It includes less than $3 billion in direct spending from the film industry. The rest is supposed to come from the multiplier effect, in which each dollar spent creates more spending throughout the economy. And economists have some serious questions about how valid that estimate is.

J.C. Bradbury of Kennesaw State University has argued that using a more realistic multiplier, the film industry generates, at most, $4.2 billion in annual economic output. Similarly, Bruce Seaman of Georgia State University thinks the film industry is responsible for just $6 billion in economic benefits. The state Department of Economic Development estimates that for every dollar the film industry spends in the state, overall spending increases by $3.57; Seaman argues the real value is closer to $1.87.

Georgia isn’t the only state to inflate the benefits of film production.

One especially dubious study of film tax credits, prepared for the New Mexico State Film Office, claimed that tourism alone driven by the filming of No Country for Old Men, 3:10 to Yuma, Indiana Jones and the Kingdom of the Crystal Skull, and Wild Hogs (a forgettable 2007 comedy starring Tim Allen, Martin Lawrence, William H. Macy, and John Travolta as an over-the-hill biker gang) generated more than $100 million in income for state residents over a four-year span.

Most research on film tax credits show that they don’t have much of an impact on economic growth. A National Bureau of Economic Research study from this June found that film subsidies only have a marginal impact on where TV series are filmed, and that they do not increase feature film location, employment, economic growth, or wages. Studies from Michigan and Massachusetts have found that the average length of a job credited to a film tax incentive program lasts less than a month.

Subsidies can even hurt a stateeconomy, by shifting economic resources away from productive industries and toward politically connected ones. If it weren’t for the tax subsidies, the money that Georgia directs to film production could instead go to reducing taxes broadly, allowing the people of the state to decide which businesses to support. In the meantime, there’s a good chance production companies would come even without the subsidies.

from Latest – Reason.com https://ift.tt/2XlLp8u

via IFTTT

The Dow Jones just had its best June since 1938. Overall, stocks were up around 7% last month. It was also the best first half for stocks in 22 years.

Meanwhile, gold gained about 8% on the month. As Peter pointed out in his latest podcast, while stocks had significant gains in dollar terms, they actually lost value in terms of real money.

And as Peter pointed out, when you look at the recent stock market gains, you have to put them into context.

The only reason that the market has done so well this year is because it got destroyed in the fourth quarter of last year. Remember, we had the worst December since the Great Depression as well.”

In fact, if you factor in the fourth quarter of last year, the Dow is only up one-half percent. The S&P 500 has gained about 1% and the Nasdaq is up .5%. In fact, the Dow Transports are actually down about 9% over the last three quarters, and the Russell 2000 is down 8%.

So, there you get a much better picture of what’s actually going on in the US stock markets than if you just focus on what’s happened in 2019 and ignore what happened in the end of 2018.”

To really put it into perspective, look at the price of gold. Since the end of Q3 2018 the yellow metal is up 18%.

That is a huge move in the price of gold during that period of time. Now, I think that in the future we can see even bigger moves than what we’ve just seen, but that put the rise in the Dow in perspective because it’s not the Dow that’s going up. Gold has gone up, so in gold-terms, the Dow has lost value.”

And why has this happened?

It’s all about the Fed.

The Fed has done a complete 180 on monetary policy and that is what has driven what I believe is a bear market rally in the US stock market.”

And Peter said he thinks the last three quarters are really more indicative of what we’re going to see over the next several years then what we’ve seen over the past few years when investors were delusional. They were operating under the false premise that everything was great and the Federal Reserve could simply unwind its stimulus and normalize interest rates and shrink its balance sheet.

None of that was true. That was a fantasy. And as reality replaces that fantasy, US stocks are going to have a very, very tough time and the dollar is going to have even a tougher time.”

Peter highlighted some more negative economic data that came out last week — specifically weak manufacturing numbers.

All the actual data that we’re getting is indicating that the economy is weakening, which is the only thing that is powering the stock market rally, because the stock market is preparing for a new injection of monetary stimulus. The Fed is going to be cutting interest rates next month and I think the rate cuts are going to be followed by more quantitative easing.”

Peter reiterated that he doesn’t think it’s going to work this time. Nobody really expected the aggressive easy-money policy we got for nearly a decade after the 2008 crash. Now, everybody expects it. They are even begging for it.

When they get what they want, I don’t think it’s going to work because I think it will be more of a buy the rumor sell the fact.”

Peter said he doesn’t think it’s going to have the same effect as it did the last time around. He thinks long-term interest rates will rise despite the Fed’s efforts to suppress them. He thinks consumer prices will rise sharply.

And the political climate could make things even worse – especially if one of these 20 Democratic Party presidential candidates wins the 2020 election.

Peter goes on to break down some of the political dynamics.

via ZeroHedge News https://ift.tt/2NoNtYZ Tyler Durden

The Los Angeles Press Club just held its annual awards ceremony to recognize the best journalism produced by media companies headquartered in Southern California. Reason, which is based in Los Angeles, was nominated in 19 categories; we walked away from Sunday night’s gala with four wins, six second-place awards, and two third-place prizes. Our crew is quite pleased, and we hope that our supporters and readers are as well.

First place in humor and satire writing across all platforms: Austin Bragg, Meredith Bragg, and Andrew Heaton for “Groundhog Day: 2018”

Judges’ comment: “Tightly written, devastatingly funny and spot on media critique.”

Judges’ comment: “This is the most thorough and complete entry, although it lacks the humanity of the second-place finisher. In fact, this was a toss-up to decide, because each story expertly hit the mark it was aiming for. But given the immigration news of the past year, a deep policy dive might be the more crucial journalism.”

Second place for a non-entertainment profile or interview in TV or film: Nick Gillespie, Justin Monticello, and Todd Krainin for “Theranos, Elizabeth Holmes, and the Cult of Silicon Valley.”

Third place for a news feature over five minutes: Zach Weissmueller for “Trump, Ryan, and Walker Want to Seize Wisconsin Homes to Build a Foxconn Plant.”

Going through Reason‘s published work from 2018 in order to put together our awards submissions reminded me that this team punches far above its annual budget across platforms and categories. I am deeply grateful to our readers, to our donors, and to our colleagues in the media industry, who judged these awards. They are not the only—and certainly not the most significant—way to measure our reach and impact, but we are nevertheless proud. If you give to Reason or share our work, you should be proud too.

from Latest – Reason.com https://ift.tt/2J6ijl7

via IFTTT

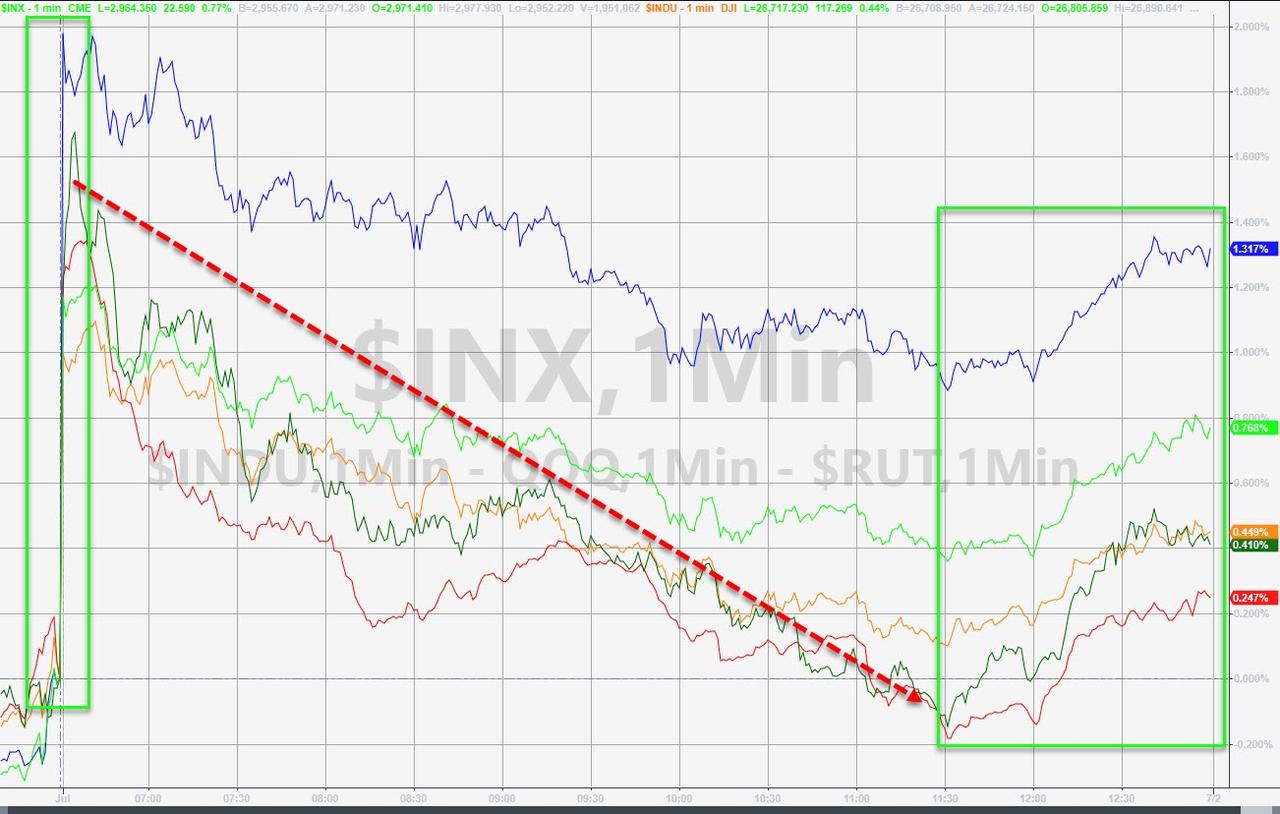

A China trade truce, surging chip stocks, and bad (economic) news that must be good ammo for The Fed to cut, BUT stocks faded all the gains – simply put, it’s never enough!!

Chinese stocks surged on the trade-truce and while they maintained gains, the afternoon session saw barely any follow-through…

European stocks opened dramatically higher (on the trade truce) but faded practically non-stop from the open with Italy ending unch…

German bund yields fell to new record (negative) lows today and Italian yields dropped below 2.00% for the first time since May 2018…

Almost from the cash market open, US equities went in only one direction as “sell the news” dominated the nothing-burger truce deal…

Stocks managed a pretty good run into the close starting at 3pmET to ensure The S&P closed at a record closing high…

The Nasdaq outperformed however, helped by the biggest gap-up opening in SOX (Semis dramatically outperformed) in its history…

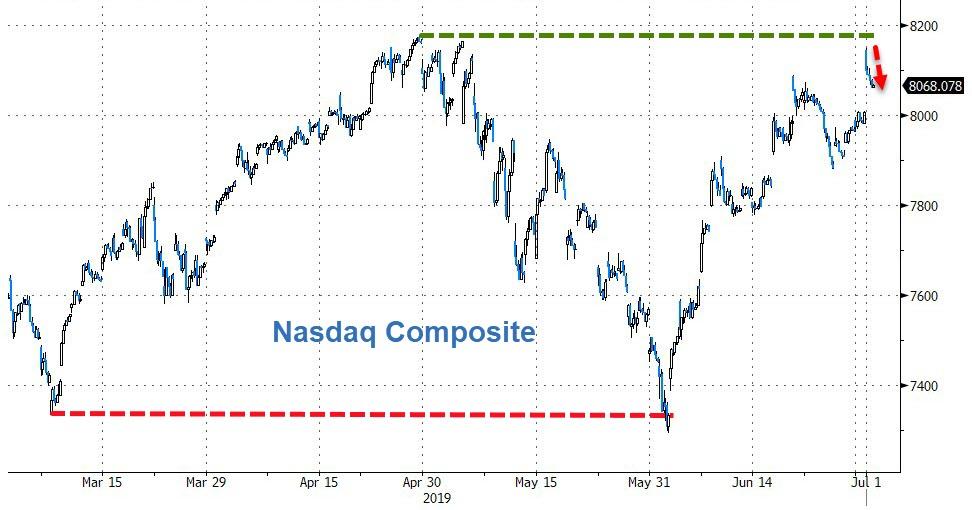

But notably, Nasdaq Composite failed to make new highs and was down by around 100 points from the highs…

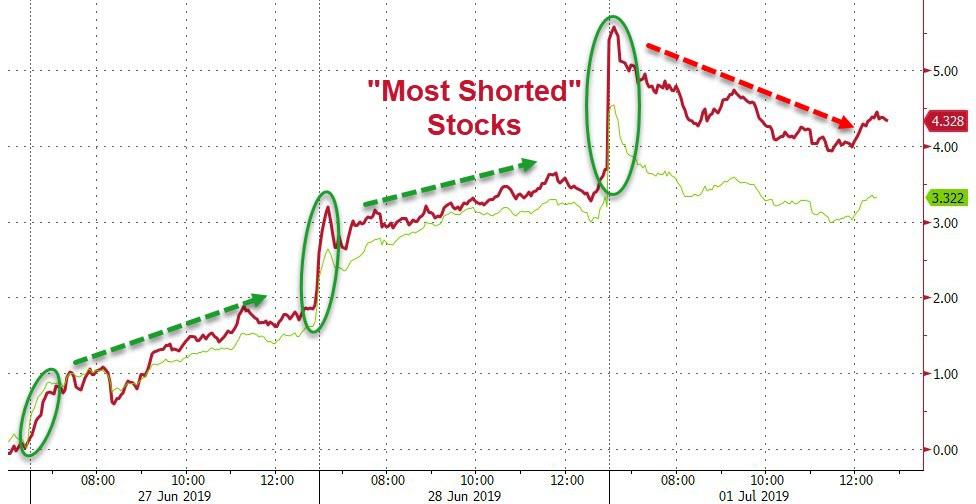

Giant short-squeeze at the US cash open – for the 3rd day in a row…

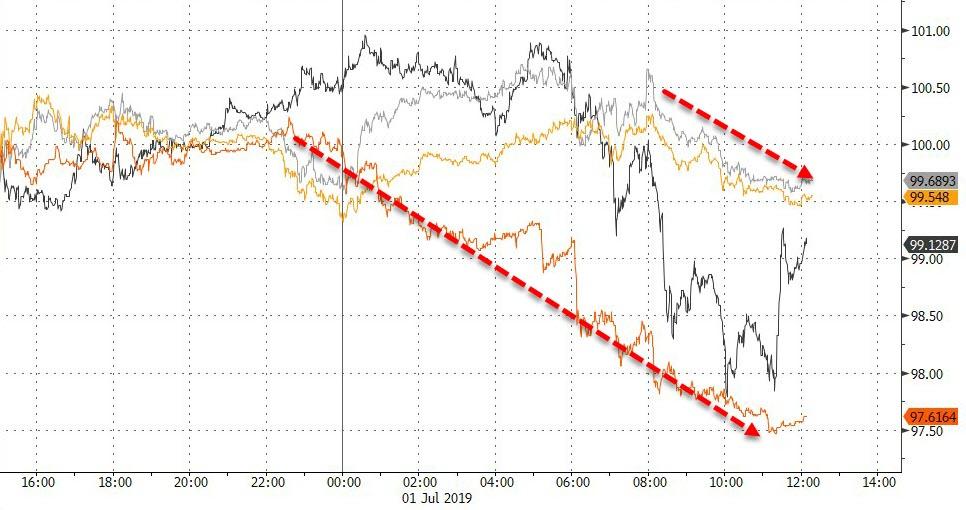

Treasury yields were higher on the day by around 2-3bps across the curve (after rallying from the higher yield open to unchanged)…

10Y Yields tested down to 2.00% once again (but bounced)…

As it seems “sell all the things hit shortly after the US open)

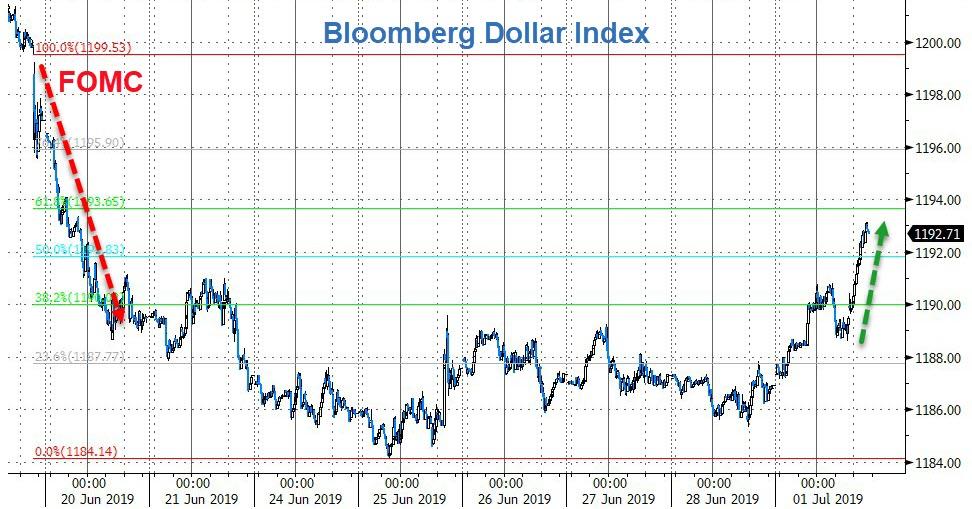

The dollar surged (retracing almost the Fib 61.8% of the post-FOMC losses)…

Yuan erased almost all of its trade-truce gains…

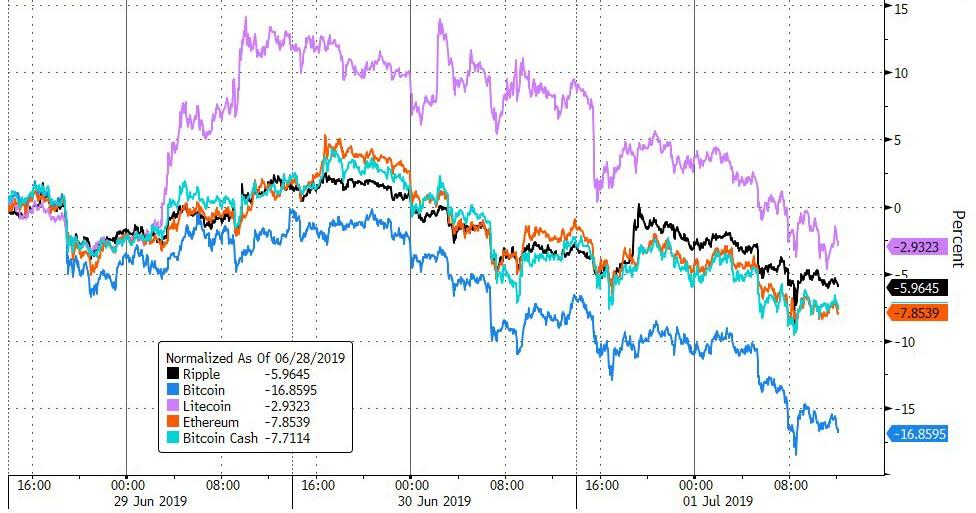

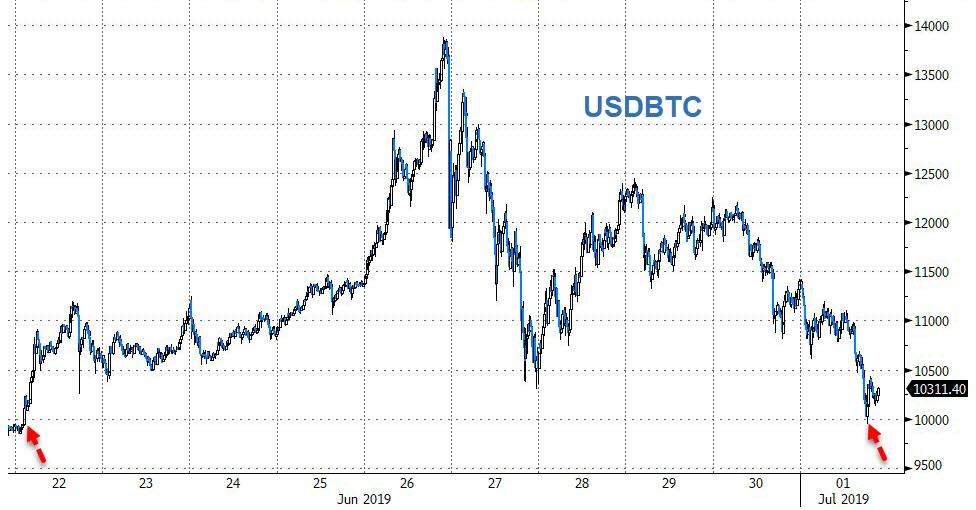

Cryptos extended the weekend’s declines…

Led by Bitcoin which tested below $10,000 briefly…

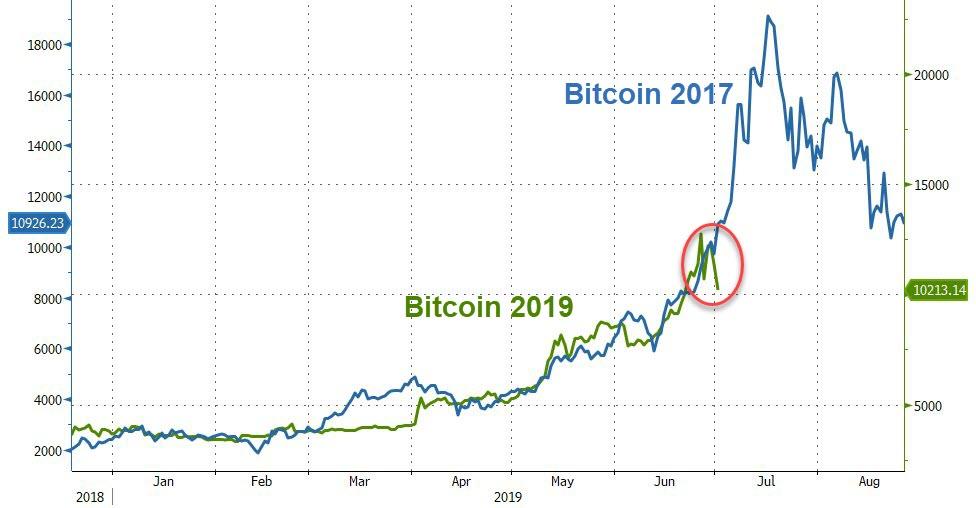

As the 2017 analog loses its trajectory…

Dollar strength sent commodities broadly lower (even WTI faded despite OPEC+ deal chatter), gold and silver was least hit…

Gold fell back below $1400…

Oil price behavior was quite shocking, spiking on hype about an OPEC+ deal (Russia and Saudi agreeing a deal at G-20), then rolling over from the US equity market open, then spiking towards the NYMEX close…

And if the trade truce is so awesome, why did copper crap the bed?

Finally, more dismal global macro data today, not helped at all by the US…

Seems to confirm bonds have it right…

So for all those buying stocks, do you really feel that lucky?

via ZeroHedge News https://ift.tt/2Lwz22r Tyler Durden

The Los Angeles Press Club just held its annual awards ceremony to recognize the best journalism produced by media companies headquartered in Southern California. Reason, which is based in Los Angeles, was nominated in 19 categories; we walked away from Sunday night’s gala with four wins, six second-place awards, and two third-place prizes. Our crew is quite pleased, and we hope that our supporters and readers are as well.

First place in humor and satire writing across all platforms: Austin Bragg, Meredith Bragg, and Andrew Heaton for “Groundhog Day: 2018”

Judges’ comment: “Tightly written, devastatingly funny and spot on media critique.”

Judges’ comment: “This is the most thorough and complete entry, although it lacks the humanity of the second-place finisher. In fact, this was a toss-up to decide, because each story expertly hit the mark it was aiming for. But given the immigration news of the past year, a deep policy dive might be the more crucial journalism.”

Second place for a non-entertainment profile or interview in TV or film: Nick Gillespie, Justin Monticello, and Todd Krainin for “Theranos, Elizabeth Holmes, and the Cult of Silicon Valley.”

Third place for a news feature over five minutes: Zach Weissmueller for “Trump, Ryan, and Walker Want to Seize Wisconsin Homes to Build a Foxconn Plant.”

Going through Reason‘s published work from 2018 in order to put together our awards submissions reminded me that this team punches far above its annual budget across platforms and categories. I am deeply grateful to our readers, to our donors, and to our colleagues in the media industry, who judged these awards. They are not the only—and certainly not the most significant—way to measure our reach and impact, but we are nevertheless proud. If you give to Reason or share our work, you should be proud too.

from Latest – Reason.com https://ift.tt/2J6ijl7

via IFTTT

The playwrights of yore had a neat way of resolving sticky plots: when it seemed all was lost among the confounded mortals on stage, a supernatural figure would descend from the riggings above the proscenium, lowered in a basket on a cable — Moliere liked to use an actor playing Louis XIV, his patron — to resolve, untangle, forgive, and pardon all the complications of the story. This device is known as the Deus ex Machina, God in a machine.

Rep. Jerrold Nadler (D-NY) announced last week that ex-Special Counsel Robert Mueller has agreed to descend from on-high into the witness chair of Mr. Nadler’s House committee chamber on July 17, presumably to resolve all the conundrums left by his semi-inconclusive RussiaGate report. Remember, in his nine-minute homily on May 29, Mr. Mueller said that if called to testify, he would only answer by referring to the text of his report — hallowed in Wokesterdom until its disappointing release.

Mr. Mueller’s notion of testimony-by-script is at least as unorthodox as his innovation of pronouncing the object of his criminal inquiry “not exonerated,” an unprecedented and certainly extra-legal spin to the prosecutorial standard of finding an indictable offense or not — without added aspersions, insinuations, and defamations. Meanwhile, Mr. Mueller’s standing as a potent God figure has eroded badly. He started out in 2017 as the Avenging Angel in a Brooks Brother’s suit, morphed into Yahweh as the RussiaGate Mob patiently awaited his Last Judgment, and then got demoted to mere Sphinx-hood after his Sacred Text failed its basic task: to oust the Golden Golem of Greatness from his unholy occupation of the White House.

Did Mr. Nadler summon Mr. Mueller from beach or lake-side to just recite chapter and verse from his report? What would be the point of that? Well, perhaps to whip up enough media froth to refresh the public’s memory of how Comrade Trump stole the 2016 election at the bidding of his Russian handlers. Is that all?

Could be.

The problem is that Mr. Nadler’s majority Democrat members are not the only ones who get to ask questions. Did the Chairman forget that? Or did he think the minority — including Reps. Collins, Jordan, Gohmert, and Gaetz — would just lob softballs at the witness?

I can think of a few 90-mph sliders I’d like to pitch to Mr. Mueller, some of them already floated in the press: like,

why did you allow the GI cell phones of Peter Strzok and Lisa Page to be destroyed shortly after you were informed about their unprofessional and compromising text exchanges, for which they were fired off your “team?”

When did you learn that international men-of-mystery Stefan Halper and Josef Mifsud, whose operations spurred your prosecutions, were not Russian agents but rather in the employ of US and British government intel agencies?

Your deputy, Andrew Weissmann, was informed by Deputy Attorney General Bruce Ohr in the summer of 2016, months before your appointment, that the predicating documents for your inquiry, known as the Steele Dossier, amounted to a Clinton campaign oppo research digest — when did he happen to tell you that?

You devoted nearly 20 pages of your report to the Trump Tower meeting between the president’s son, Donald, Jr., and two Russians, lawyer Natalia Veselnitskaya and lobbyist Rinat Akhmetshin. Why did you omit to mention that both Russians were in the employ of Glenn Simpson’s Fusion GPS company, candidate Clinton’s oppo research contractor, and met with Mr. Simpson both before and after the Trump Tower meeting?

How did it happen that you hired attorney Jeannie Rhee for your team, knowing that she had previously worked as a lawyer for the Clinton Foundation?

Under what legal standard did you pronounce Mr. Trump to be “not exonerated” in the obstruction of justice matter, considering you told the Attorney General, Mr. Barr, that it was not based on findings by the DOJ Office of Legal Counsel concerning presidential immunity from indictment?

The public has been well-distracted by the Democratic Party primary circus, and all reporting about the aftermath of RussiaGate has vanished from the front pages of the news media.

Ostensibly, Hillary Clinton is enjoying her solitary walks in the Chappaqua woods and all seems well in the Deep State world. Yet, consider that wild things lurk in those thickets. The DOJ Inspector General, Mr. Horowitz, is overdue with his own report — perhaps stymied by a lack of cooperation in wringing declassified documents from the hands of the many intel agencies involved… while Mr. Barr and his deputy, John Durham, are at work in the background on their own investigation. There will also be repercussions upcoming in the matter of General Flynn, who switched attorneys recently and may be reconsidering his guilty plea based on Mr., Mueller’s prosecutorial misconduct in withholding exculpatory evidence from Judge Emmet Sullivan’s court.

It’s just possible that Robert Mueller will not be reading chapter and verse from his sacred report, like an old-school Episcopal priest, but rather pleading the Fifth Amendment to avert his own potential prosecution.

via ZeroHedge News https://ift.tt/2FLgAQ5 Tyler Durden

According to fire officials in Menlo Park, two Facebook employees may have been exposed to Sarin at a company mailing facility, NBC Bay Area reports.

#BREAKING: At least 2 employees may have been possibly exposed to sarin after coming in contact with the chemical at a Facebook mailing facility, Menlo Park fire officials say. https://t.co/fnKE1CC8OW

InPart 1,we discussed the problems with the “savings” side of the equation as it relates to building wealth. Part 2,covered the issues of counting on average, or compound, returns as it relates to future outcomes.

This final chapter is going to cover some concepts which will destroy the best laid financial plans if they are not accounted for properly.

Just recently, CNBC ran a story discussing the “Magic Number” needed to retire:

“For many people who adhere to the mission, there’s a savings target they want to hit, at which point they will have reached financial independence, as they define it. It’s called their FIRE number, and typically, it’s equal to 25 times a household’s annual spending, invested in low-cost, passive stock funds. Many wannabe-early retirees aim to save between $1 million and $2 million.”

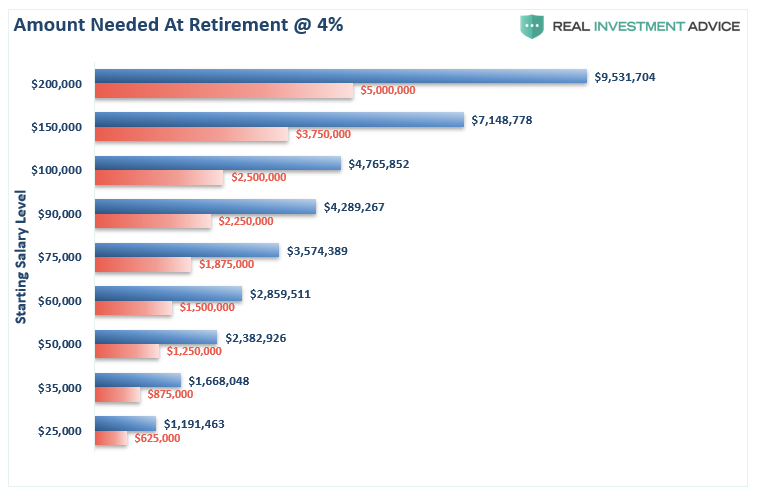

This was the savings level we addressed in part one, which is erroneous because it is based on today’s income-replacement level and not the future inflation-adjusted replacement level, as it requires substantially higher savings levels. To wit:

“The chart below takes the inflation-adjusted level of income for each bracket and calculates the asset level necessary to generate that income assuming a 4% withdrawal rate. This is compared to common recommendations of 25x current income.”

“If you need to fund a lifestyle of $100,000 or more today. You are going to need $5 million at retirement in 30-years.

Not accounting for the future cost of living is going to leave most individuals living in tiny houses and eating lots of rice and beans.”

The Cost Of Miscalculation

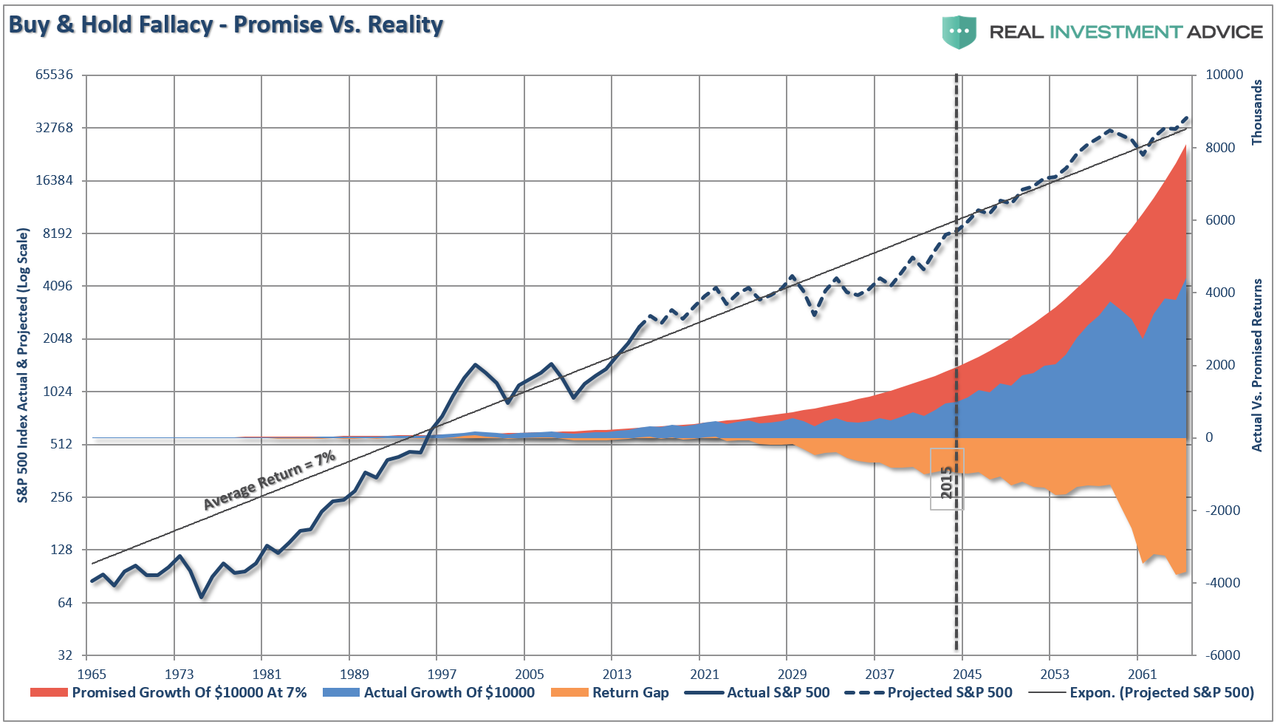

As noted in the CNBC article above, it is recommended that you invest your savings into low-cost index funds. The assumption, of course, is that these funds will average 8% annually. As discussed in Part One, markets don’t operate that way.

“When imputing volatility into returns, the differential between what investors were promised (and this is a huge flaw in financial planning) and what actually happened to their money is substantial over long-term time frames.”

During strongly trending bull markets, investors tend to forget that devastating events happen. Major events such as the “Crash of 1929,”“The Great Depression,” the “1974 Bear Market,” the “Crash of ’87”, the “Dot.com” bust, and the “Financial Crisis,” etc. often written off as “once in a generation” or “1-in-100-year events.” However, these financial shocks have come along much more often than suggested.Importantly, all of these events had a significant negative impact on an individual’s “plan for retirement.”

It doesn’t have to be a “financial crisis” which derails the best laid of financial plans either. An investment gone wrong, an unexpected illness, loss of job, etc. can all have devastating impacts to future retirement plans.

Then there is just “life,” which tends to screw up things without a tragedy occurring.

Making the correct assumptions in your planning is critical to your eventual success.

Your Personal Returns Will Be Less Than An “Index”

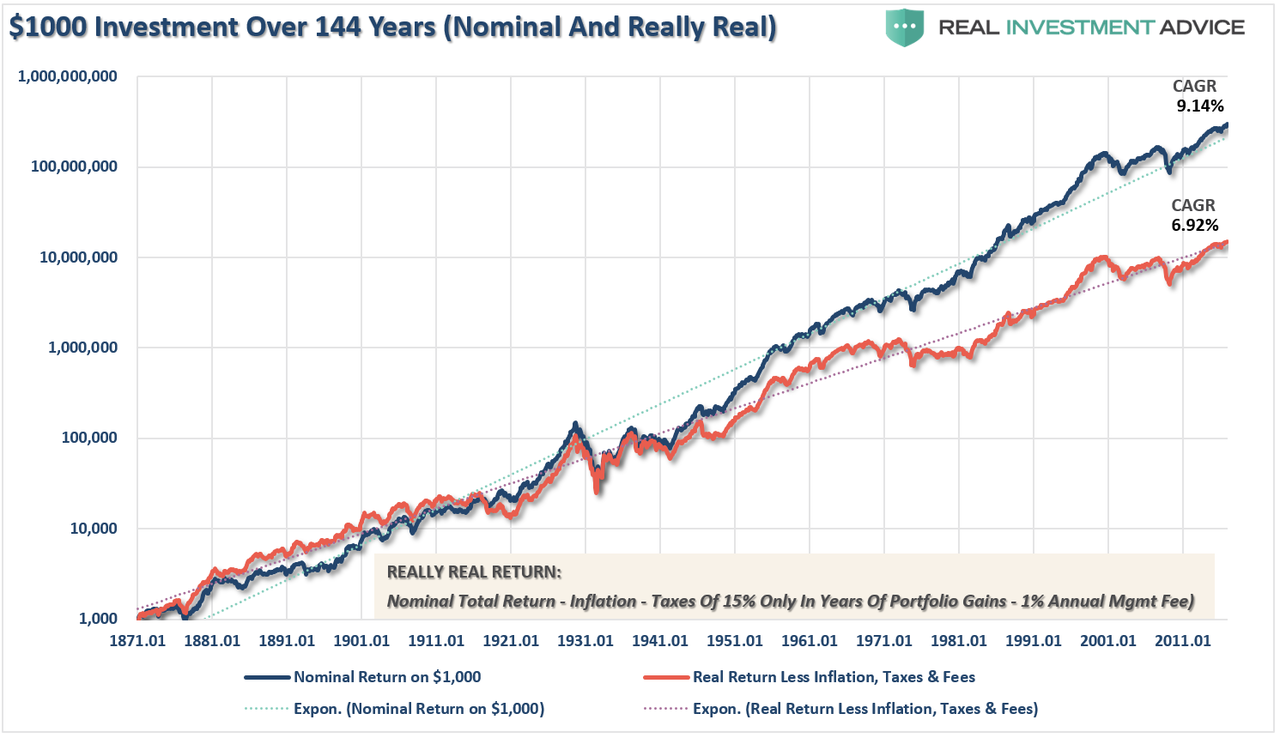

One of the biggest mistakes made is assuming markets will grow at a consistent rate over the given time frame to retirement. As noted, there is a massive difference between compounded returns and real returns as shown above. Furthermore, the shortfall is compounded further when you begin to add in the impact of fees, taxes, and inflation over the given time frame.

The chart below shows what happens to a $1000 investment from 1871 to present, including the effects of inflation, taxes, and fees. (Assumptions: I have used a 15% tax rate on years the portfolio advanced in value, CPI as the benchmark for inflation and a 1% annual expense ratio.)

An index has no life expectancy requirements – but you do.

It doesn’t have to compensate for distributions to meet living requirements – but you do.

It requires you to take on excess risk (potential for loss) in order to obtain equivalent performance – this is fine on the way up, but not on the way down.

It has no taxes, costs or other expenses associated with it – but you do.

It has the ability to substitute at no penalty – but you don’t.

It benefits from share buybacks (market capitaliziaton) – but you don’t.

As an individual you have very little in common with a “benchmark index.” Investing is not a “competition”and treating it as such has had disastrous consequences over time.

Financial Planning Gone Wrong

I know, you still don’t believe me. Let’s use CNBC’s example and then break it down.

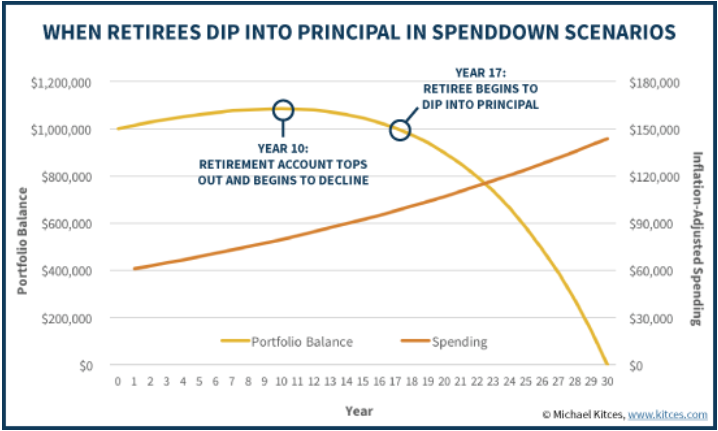

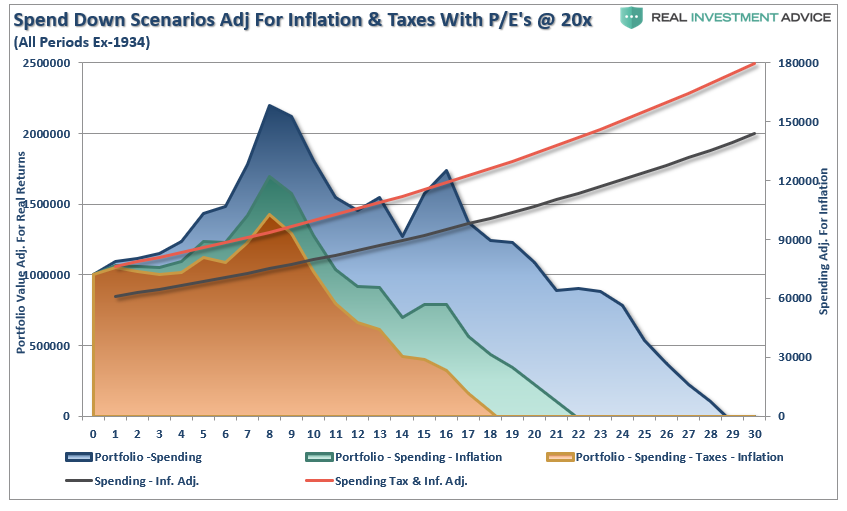

“For instance, imagine a retiree who has a $1,000,000 balanced portfolio, and wants to plan for a 30-year retirement, where inflation averages 3% and the balanced portfolio averages 8% in the long run. To make the money last for the entire time horizon, the retiree would start out by spending $61,000 initially, and then adjust each subsequent year for inflation, spending down the retirement account balance by the end of the 30th year.”

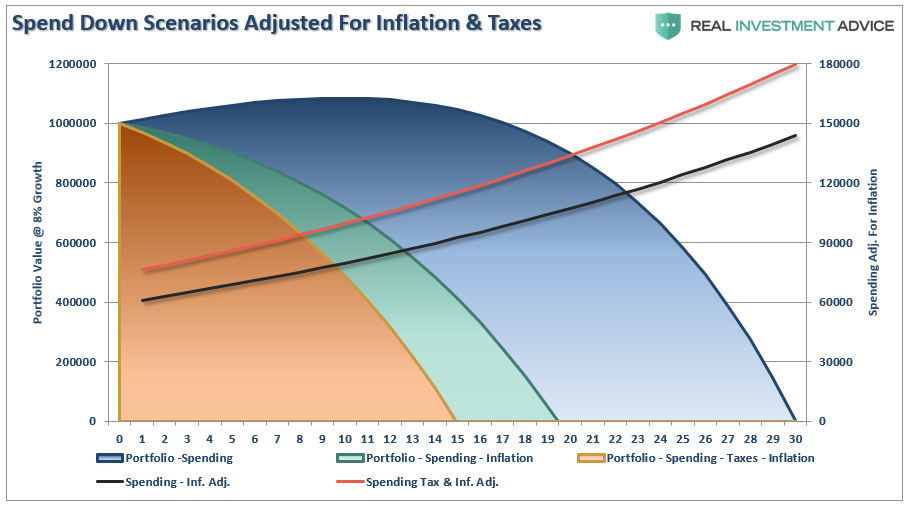

This assumption on expanding inflationary pressures later in retirement is correct, however, it doesn’t take into account the issue of taxation. So, let’s adjust the chart and include not only the impact of inflation-adjusted returns but also taxation. The chart below adjusts the 8% return structure for inflation at 3% and also adjusts the withdrawal rate up for taxation at 25%.

By adjusting the annualized rate of return for the impact of inflation and taxes, the life expectancy of a portfolio grows considerably shorter.

However, we must also consider the impact of variable rates of returns in retirement as well.

The Impact Of Variability

Over the last 120-years, the market has indeed averaged 8-10% annually. Unfortunately, you do NOT have 90, 100, or more years to invest. All that you have is the time between today and when you want to retire to reach your goals. If that stretch of time happens to include a 12-15 year period in which returns are flat, which happens with some regularity, the odds of achieving goals are massively diminished.

But what drives those 12-15 year periods of flat to little return? Valuations.

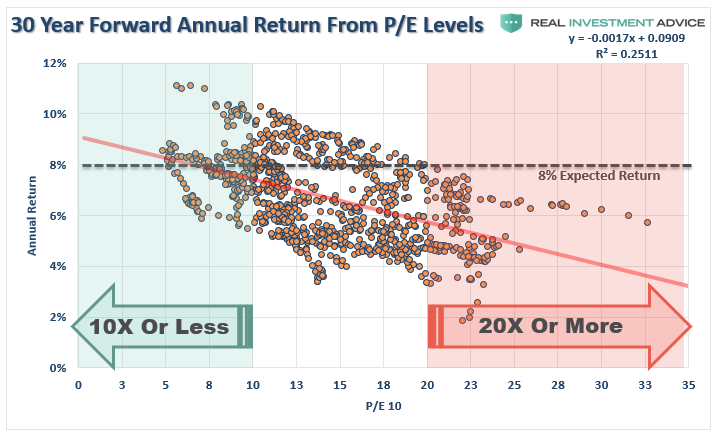

Understanding this, we can use valuations, such as CAPE, to form expectations around risk and return. The graph below shows the actual 30-year annualized returns that accompanied given levels of CAPE.

As evidenced by the graph, as valuations rise future rates of annualized returns fall. This should not be a surprise as simple logic states that if you overpay today for an asset, future returns must, and will, be lower.

Math also proves the same. Capital gains from markets are primarily a function of market capitalization, nominal economic growth plus the dividend yield. Using the Dr. John Hussman’s formula we can mathematically calculate returns over the next 10-year period as follows:

(1+nominal GDP growth)*(normal market cap to GDP ratio / actual market cap to GDP ratio)^(1/10)-1

Therefore, IF we assume that

GDP maintains, 4% annualized growth indefinitely

Which means recessions have been eliminated, AND

Current market cap/GDP stays flat at 1.25, AND

The current dividend yield remains at 2%:

We would get forward returns of:

(1.04)*(.8/1.25)^(1/30)-1+.02 = 4.5%

These are some “big” assumptions. If we assume inflation remains stagnant at 2%, as the Fed hopes, such would mean a real rate of return of just 2.5%. This is far less than the 8-10% rates of return currently being counted on in many of the financial plans I see regularly.

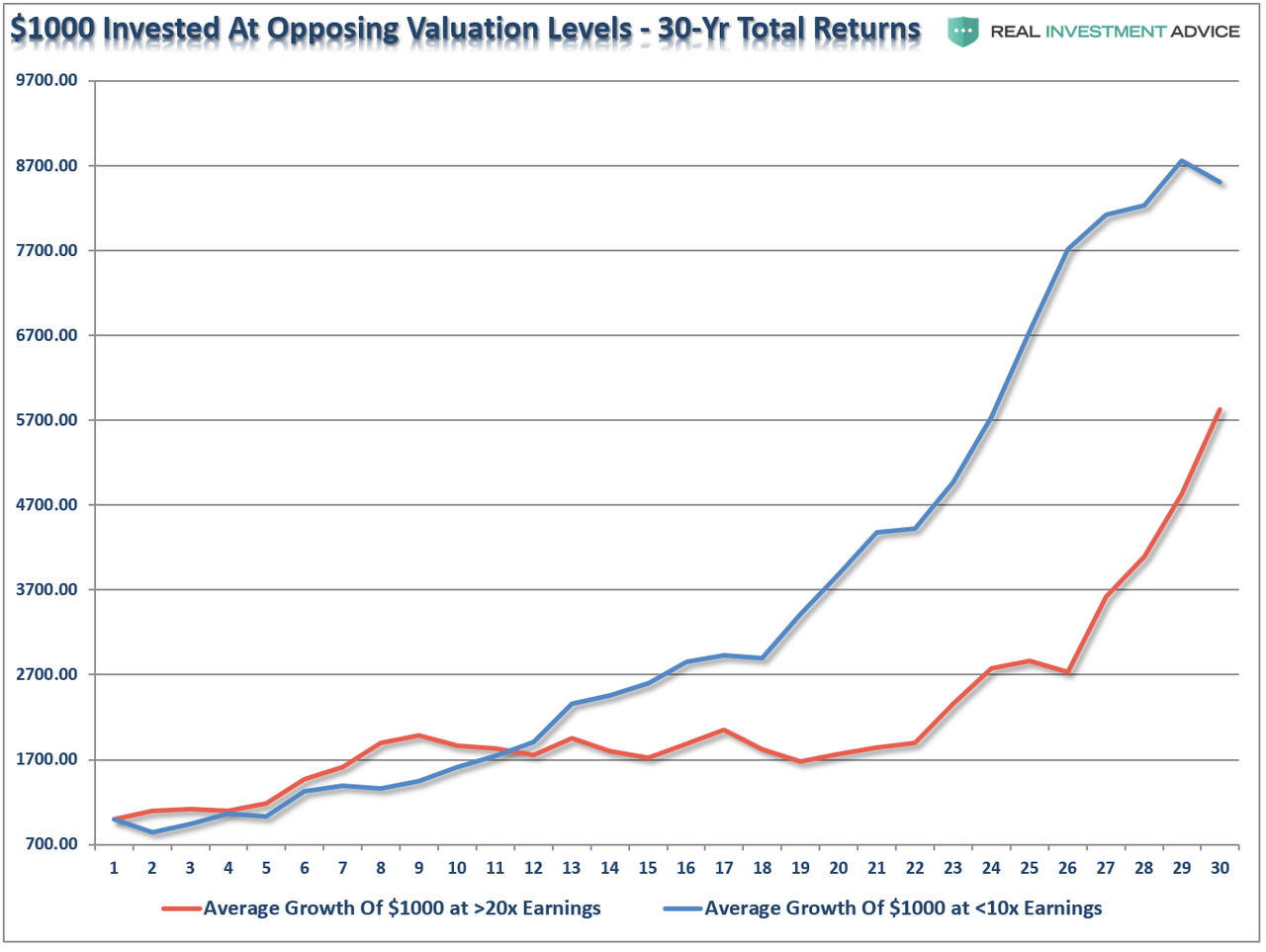

Let’s take this a step further. For the purpose of this article, we went back through history and pulled the 4-periods where trailing 10-year average valuations (Shiller’s CAPE) were either above 20x earnings or below 10x earnings. We then averaged those periods and ran a $1000 investment going forward for 30-years on a total-return, inflation-adjusted, basis.

Not surprisingly, the starting level of valuations has the greatest impact on your future results.

If we apply the math of valuations to our example, a much different, and far less favorable, financial outcome emerges – the retiree runs out of money not in year 30, but in year 18.

With current valuations elevated, and total returns in excess of 300% over the last decade, planning on using the stock market to make up for a savings short-fall may be misguided. This is the same trap that pension funds all across this country have fallen into and are now paying the price for.

What Your Financial Planning Should Consider

The analysis above reveals the important points individuals should consider in their financial planning process:

Expectations for future returns and withdrawal rates should be downwardly adjusted.

The potential for front-loaded returns going forward is unlikely.

The impact of taxation must be considered in the planned withdrawal rate.

Future inflation expectations must be carefully considered.

Drawdowns from portfolios during declining market environments accelerates the principal bleed. Plans should be made during up years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

The yield chase over the last 8-years, and low interest rate environment, has created an extremely risky environment for retirement income planning. Caution is advised.

Expectations for compounded annual rates of returns should be dismissed in lieu of plans for variable rates of future returns.

Investing for retirement, no matter what age you are, should be done conservatively and cautiously with the goal of outpacing inflation over time. This doesn’t mean you should never invest in the stock market, it just means that your portfolio should be constructed to deliver a rate of return sufficient to meet your long-term goals with as little risk as possible.

Save More And Spend Less: This is the only way to ensure you will be adequately prepared for retirement. It ain’t sexy, or fun, but it will absolutely work.

You Will Be WRONG. The markets go through cycles, just like the economy. Despite hopes for a never-ending bull market, the reality is “what goes up will eventually come down.”

RISK does NOT equal return. The further the markets rise, the bigger the correction will be. RISK = How much you will lose when you are wrong, and you will be wrong more often than you think.

Don’t Be House Rich. A paid off house is great, but if you are going into retirement house rich and cash poor, you will be in trouble. You don’t pay off your house UNTIL your retirement savings are fully in place and secure.

Have A Huge Wad. Going into retirement have a large cash cushion. You do not want to be forced to draw OUT of a pool of investments during years where the market is declining. This compounds the losses in the portfolio and destroys principal which cannot be replaced.

Plan for the worst. You should want a happy and secure retirement – so plan for the worst. If you are banking solely on Social Security and a pension plans, what would happen if the pension was cut? Corporate bankruptcies happen all the time and to companies that most never expected. By planning for the worst, anything other outcome means you are in great shape.

Most likely what ever retirement planning you have done is most likely overly optimistic.

Change your assumptions, ask questions, and plan for the worst.

The best thing about “planning for the worst” is that all other outcomes are a “win.”

via ZeroHedge News https://ift.tt/2xluweH Tyler Durden

From Friday’s Seventh Circuit decision in Doe v. Purdue Univ., written by Judge Amy Coney Barrett and joined by Judges Diane Sykes and Amy St. Eve:

After finding John Doe guilty of sexual violence against Jane Doe, Purdue University suspended him for an academic year and imposed conditions on his readmission. As a result of that decision, John was expelled from the Navy ROTC program, which terminated both his ROTC scholarship and plan to pursue a career in the Navy…. [We conclude that] John has adequately alleged violations of both the Fourteenth Amendment and Title IX.

The court concluded that, under Indiana law, university students have no property right in their continuing attendance at the university, and thus they can’t sue for deprivation of property without due process. (Federal courts disagree on this question: “The First, Sixth, and Tenth Circuits have recognized a generalized property interest in higher education. The Fifth and Eighth Circuits have assumed without deciding that such a property interest exists. The Second, Third, Fourth, Ninth, and Eleventh Circuits join [the Seventh Circuit] in making a state-specific inquiry to determine whether a property interest exists.”)

But the court held that Doe adequately alleged that he was being deprived of his liberty, on a so-called “stigma plus” theory: Purdue had been accusing him of a crime, and combining the stigma of this accusation with a one-year suspension, which led to his expulsion from the Navy ROTC program. (Mere alleged defamatory falsehoods aren’t seen as deprivations of liberty for Due Process Clause purposes, but alleged defamatory falsehoods coupled with tangible government action often are.) And, the court concluded, this deprivation of liberty was done without due process:

John’s circumstances entitled him to relatively formal procedures: he was suspended by a university rather than a high school, for sexual violence rather than academic failure, and for an academic year rather than a few days. Yet Purdue’s process fell short of what even a high school must provide to a student facing a days-long suspension.

“[D]ue process requires, in connection with a suspension of 10 days or less, that the student be given oral or written notice of the charges against him and, if he denies them, an explanation of the evidence the authorities have and an opportunity to present his side of the story.” John received notice of Jane’s allegations and denied them, but Purdue did not disclose its evidence to John. And withholding the evidence on which it relied in adjudicating his guilt was itself sufficient to render the process fundamentally unfair. “[F]airness can rarely be obtained by secret, one-sided determination of facts decisive of rights….”

John has adequately alleged that the process was deficient in other respects as well. To satisfy the Due Process Clause, “a hearing must be a real one, not a sham or pretense.” At John’s meeting with the Advisory Committee, two of the three panel members candidly admitted that they had not read the investigative report, which suggests that they decided that John was guilty based on the accusation rather than the evidence.

And in a case that boiled down to a “he said/she said,” it is particularly concerning that [Dean of Students Katherine] Sermersheim and the committee concluded that Jane was the more credible witness—in fact, that she was credible at all—without ever speaking to her in person. Indeed, they did not even receive a statement written by Jane herself, much less a sworn statement. It is unclear, to say the least, how Sermersheim and the committee could have evaluated Jane’s credibility.

Sermersheim and the Advisory Committee’s failure to make any attempt to examine Jane’s credibility is all the more troubling because John identified specific impeachment evidence. He said that Jane was depressed, had attempted suicide, and was angry at him for reporting the attempt. His roommate—with whom Sermersheim and the Advisory Committee refused to speak—maintained that he was present at the time of the alleged assault and that Jane’s rendition of events was false. And John insisted that Jane’s behavior after the alleged assault—including her texts, gifts, and continued romantic relationship with him—was inconsistent with her claim that he had committed sexual violence against her. Sermersheim and the Advisory Committee may have concluded in the end that John’s impeachment evidence did not undercut Jane’s credibility. But their failure to even question Jane or John’s roommate to probe whether this evidence was reason to disbelieve Jane was fundamentally unfair to John.