“Yeah, sure they are environmentally friendly.. says so on the plastic wrapper.”

The glorious march forward of the correct thinking European superstate takes another great leap forward this morning with the launch of the first socially targeted bonds under the most intelligently designed SURE programme. All credit to the diligent double-plus-good Eurocrats of Brussels for their foresight in launching this epoch defining issue!

The EU will issue its first 10 and 20-year SURE bonds this morning. Officially the €100 bln programme is to finance “the social needs of EU Member States following the coronavirus pandemic and its consequences.” The SURE Programme is part of a larger €750 bln Recovery bond binge cooked up between the EU and ECB to solve Europe’s growth issues in the wake of the virus. The SURE Programme will run till the Recovery Bonds kick in next year with over 200 bln issuance expected.

[ZH: As Bloomberg reports, social bonds are defined by funding for projects that help society, such as improving social welfare or serving disadvantaged populations. They are the “perfect financial response” to the shock that welfare systems experienced from the pandemic, according to a report by Maia Godemer, a research analyst for green and sustainable finance at BNEF.]

Whoopee.

I shall avoid obvious cynicism… but… it’s difficult to keep a straight face at the way these bonds are being marketed as “social bonds” by the EU and its bankers to smokescreen what they really achieve.

Today’s bonds will be priced with a negative yield, but investors will lap them up because they are slightly less of a negative yield than Bunds, and they expect the EU bonds will tighten in price as the ECB drives European rate ever lower into the sub-zero zone to create the recovery and inflation that has thus far eluded them. (A policy that has achieved nothing the last 5 years.. but, hey, keep trying..)

“I was expecting a three-digit book but not quite this high,” said Jan von Gerich, chief strategist at Nordea Bank Abp.

“These bonds were clearly eagerly awaited, and these issues only strengthen the picture that there is a huge demand for bonds at the moment.”

More to the point, this afternoon investors will be able to sell the bonds in the secondary market back to the ECB, probably at a small profit because of oversubscription, via its QE infinity programmes. The 5 investment banks leading the sale – which curiously includes Barclays, a bank domiciled on Airstrip1the UK – will be delighted to be sharing about €20 mm in fees.

Meanwhile.. back in Frankfurt (the not-quite-the-centre of European finance the Germans imagine it to be) lone EU critic, Bundesbanker Jens Weidemann, is desperately saying any EU joint-borrowing should be one-off, and should not become a common budgetary tool. Sadly…. No one is listening Jens. He is a lone voice in the Frankfurt wilderness.. No one is listening.

Too late. Common issuance looks inevitable. Today’s bonds establish a clear pathway towards a single European Bond Issuance vehicle, allowing AAA/Aaa/AAA rated Europe to dominate global issuance and for Brussels to set the funding agenda.

ECB Head Christine Lagarde wants joint issuance to be part of her armoury. While Jens points out that much “closer political integration would be needed and for the EU to develop into a democratic state” before common bond issuance is even contemplated, the reality is its happened. This bond redefines and strengthens the role of Brussels’ unelected Eurocrats in terms of financial power. This bond completes the state-capture of European national financing by Brussels. There will still be Bunds, Bonos, BTPs and OATs… for a while… for a while..

Wiedemann and the Germans had this curious notion that when countries joined the Eurozone they meet the strict membership rules of the Euro by exercising sound fiscal responsibility, reforming their economies, and ensuring solid accountable finances. Silly Germans.

What this programme achieves is the centralisation of European finance despite the absence of any real democratic process or agreement on a European polity. Instead the ECB and Brussels will decide. They have captured the system. European states will no longer go to the market to raise Euros to bulwark unemployment or stem job losses – nope, now they apply to Brussel for handouts. No longer will they need to finance much needed projects via markets in their own name – Brussels now runs their budgets.

The new EU funding programmes fit perfectly with the rules of Euro membership – independent nations can’t run up large state deficits under the terms of the Euro, but client states beholden to Brussels just need to ask nicely.

Of course, you won’t find Brussels’ capture of national finances clearly stated on the bond prospectus or sales pitch this morning. Nope. Instead we have a very complex and convoluted smokescreen as the EU focuses the attention of the market and the market press on these bonds being sold to the world as a Social Bond Programme.

WTF?

It’s deflection and distraction. I read through the issue pitch and there are lots of reassuring objective phrases like “spirit of solidarity”, “preserving productive capacity” and “mitigating direct societal and economic impact”, which I am sure are very laudable goals, but of anyone can explain this one, I am all ears:

“The SURE instrument can be seen as an emergency operationalisation of the European Unemployment Reinsurance Scheme announced by the President of the European Commission in her Political Guidelines.”

Thank you Chairman Leyen for your political wisdom….

It goes on to assure potential investors the bonds meet ICMA Social Bond Principles – even appointing an external party to opine they are aligned with ICMA! The pitch conclusively says these are suitable as ESG investments. I know what you are thinking… Can these bonds get any better?

To ensure investors are satisfied the bond proceeds are being used for the designated social purposes there will be regular reports (imposed by article 13(2) of the SURE regulation relating to the implementation of the planned public expenditure..) I can’t wait to read these reports – it will be fascinating to hear how the EU traces, say, the €504 mm it’s just given to Bulgaria under the programme. I wonder if they will do it as effectively as they’ve traced the billions skimmed off grants and aid programmes by Italian gangsters under previous aid programmes?

And just in case you are confused by the jargon the EU helpfully explains:

“It is EU’s ambition to align future EU bonds with the forthcoming EU Taxonomy for environmentally sustainable activities. To avoid any confusion, the bonds under the present Framework will be named “EU SURE Social Bonds”: they are not prefiguring the social part of the future EU Taxonomy nor a possible action of the Commission in the area of the EU Green/Social Bond Standard.”

I simply can’t wait… for the EU to institute their next programme: Governance bonds! These will lend EU cash directly to European companies that do exactly what Brussels tells them to do.. (US readers: dripping Sarcasm alert.)

Now in case you are wondering – no, these bonds are not joint and severally guaranteed by European Community member states.. but they are guaranteed by €25 mm voluntarily contributed by member states.. Don’t ask how that works, but the EU is AAA rated.. so what’s the problem…? and the ECB will buy them.

Actually.. if you have any questions on the bond… they can all easily be answered: The ECB will buy them. What’s to worry? Buy the bonds. Pay the EU 26 basis points per annum for the privilege of owning them and what can possibly go wrong when the ECB will buy them.

I give up…

Meanwhile… back in the UK – I did a video y’day explaining why Rishi Sunak would be mad to listen to Tory MPs telling him to balance the budget. Last thing the UK needs is austerity and tax hikes – and since the UK controls its own money we can make as much money as we like… Please nip on to the Shard Website and give it a like…

via ZeroHedge News https://ift.tt/3dG5fjZ Tyler Durden

“This Is Not A Russian Hoax”: ‘Nonpublic Information’ Debunks Letter From ’50 Former Intel Officials’ Tyler Durden

Tue, 10/20/2020 – 08:45

Hours before Politico reported the existence of a letter signed by ’50 former senior intelligence officials’ who say the Hunter Biden laptop scandal “has all the classic earmarks of a Russian information operation” – providing “no new evidence,” while they remain “deeply suspicious that the Russian government played a significant role in this case,” Tucker Carlson obliterated their (literal) conspiracy theory.

According to the Fox News host, he’s seen ‘nonpublic information that proves it was Hunter’s laptop,‘ adding “No one but Hunter could’ve known about or replicated this information.”

“This is not a Russian hoax. We are not speculating.”

Watch:

TUCKER: “This afternoon, we received nonpublic information that proves it was Hunter’s laptop. No one but Hunter could’ve known about or replicated this information. This is not a Russian hoax. We are not speculating.” pic.twitter.com/cl2ktdmdVc

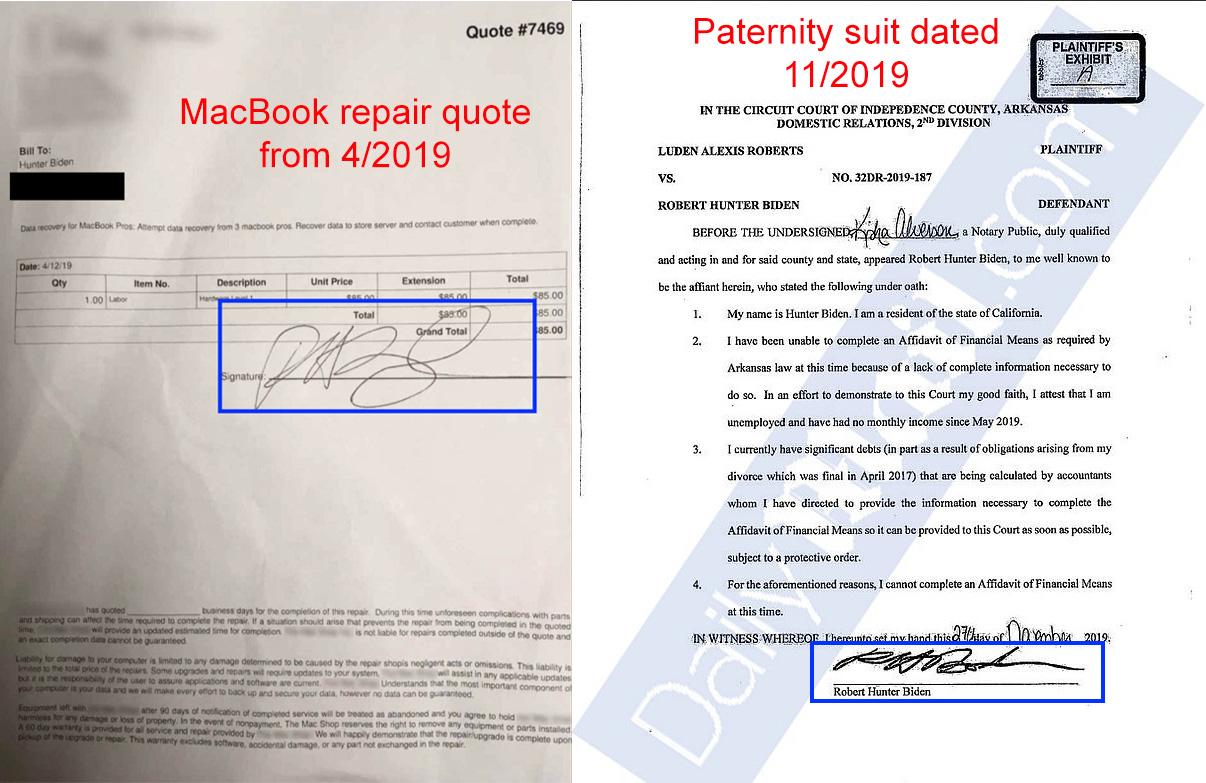

Meanwhile, the Delaware computer repair shop owner who believes Hunter dropped off three MacBook Pros for data recovery has a signed work order bearing Hunter’s signature. When compared to the signature on a document in his paternity suit, while one looks more formal than the other, they are a match.

Going back to the ’50 former senior intelligence officials’ and their latest Russia fixation, one has to wonder – do they think Putin was able to compromise Biden’s former business associate, Bevan Cooney, who gave investigative journalist Peter Schweizer his gmail password – revealing that Hunter and his partners were engaged in an influence-peddling operation for rich Chinese who wanted access to the Obama administration?

Did Putin further hack Joe Biden in 2011 to make him take a meeting with a Chinese delegation with ties to the CCP – arranged by Hunter’s group, two years they secured a massive investment of Chinese money?

The implications boggle the mind.

Here’s the clarifying sentences from the ’50 former senior intelligence officials’ that exposes the utter farce of it all:

While the letter’s signatories presented no new evidence, they said their national security experience had made them “deeply suspicious that the Russian government played a significant role in this case” and cited several elements of the story that suggested the Kremlin’s hand at work.

“If we are right,” they added, “this is Russia trying to influence how Americans vote in this election, and we believe strongly that Americans need to be aware of this.”

“Hunter Biden’s laptop is not part of some Russian disinformation campaign.”

And then there’s the fact that no one from the Biden campaign has yet to deny any of the ‘facts’ in the emails.

I’ve read a lot of stories about the process through which the Hunter Biden story has been handled inside newsrooms and not one yet that has said these critical words: “they are not true”

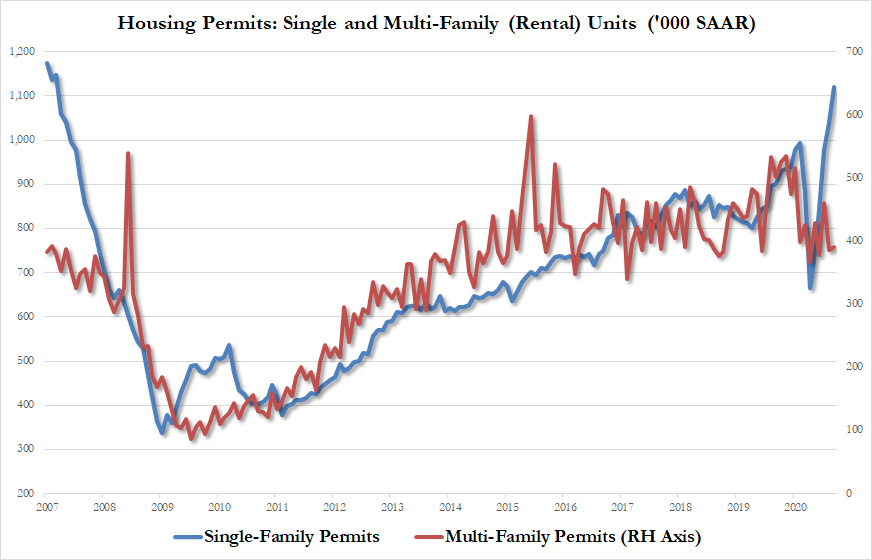

Single-Family Housing Starts/Permits Soar To Highest Since 2007 Tyler Durden

Tue, 10/20/2020 – 08:37

Despite soaring, record high homebuilder sentiment, US housing starts and permits disappointedly dropped in August but analysts now expect another rebound in September.

The data was mixed with Starts up 1.9% MoM (worse than the expedcted 3.5% jump) but Permits popped 5.2% MoM (ebtter than the expected 3.0%)…

Source: Bloomberg

This is the highest level for Building Permits since Feb 2007…

Source: Bloomberg

Driven by a surge in single-family housing permits (up 24.3% YoY to their highest since March 2007)

Additionally, single-family starts jumped 22.3% YoY to 1.108mm – the highest since June 2007…

Finally, a reminder that while homebuilders are ebullient, homebuyers are not…

Source: Bloomberg

If we build it, will they come?

via ZeroHedge News https://ift.tt/37n6Ytl Tyler Durden

DoJ Finally Files Sweeping Antitrust Lawsuit Against Google Tyler Durden

Tue, 10/20/2020 – 08:16

Just as we previewed roughly 6 weeks ago following a report published in the New York Times, the DoJ has finally brought a sweeping anti-trust case against Google, according to a WSJ scoop.

The landmark antitrust case will focus on alleged Google-controlled monopolies in search and search advertising. These businesses are the cornerstone of Google owner Alphabet’s profits. At least 10 state AGs are expected to join the suit.

Google shares are sliding on the news.

The DoJ has scheduled a press briefing for 0945ET.

via ZeroHedge News https://ift.tt/2Tan4hB Tyler Durden

Futures Rebound On Stimulus Optimism Ahead Of “Do Or Die” Deadline Tyler Durden

Tue, 10/20/2020 – 08:09

If futures are higher, it’s due to stimulus optimism; if futures are lower, then stimulus fears dominate etc, you know the drill by now… so by that logic with Eminis trading 0.7% higher this morning, optimism is apparently on the rise again after yesterday’s rout, even as we approach today’s deal ultimatum, or “do-or-die” moment as Bloomberg called it, for Nancy Pelosi and Steven Mnuchin to clinch a pre-election virus relief deal. Late on Monday, the two were said to narrow their differences after a 53-minute telephone conversation on Monday where they “continued to narrow their differences” about the coronavirus aid package, and will talk again today but still remain at odds over the scope of aid. In any case, the good news is that after today the farce may finally be over at least until after the election. Treasury yields rose and the dollar slipped, while oil and gold fluctuated. The Aussie slid after an RBA official suggested short-term rates may fall below zero.

Sure enough, as Reuters puts it, “stock index futures rose on Tuesday on expectations that Washington lawmakers would be able to settle their differences for an economic stimulus bill to pass before the Nov. 3 presidential elections.” And as Reuters also adds “Uncertainty over the fiscal stimulus weighed on Wall Street’s main indexes on Monday, with analysts expecting market turbulence to increase with only two weeks left until Election Day.” So simple, a 99 cent algo could write this market narrative.

Elsewhere, Goldman is in focus after a Bloomberg report it reached a long-awaited settlement with the DOJ to pay more than $2 billion for the bank’s role in Malaysia’s 1MDB scandal, to avoid criminal charges. Procter & Gamble shares rose in the pre-market on the best organic sales growth since 2005. Netflix Inc added 0.9% in premarket trading as investors awaited the the streaming giant’s membership additions in the third quarter. International Business Machines Corp tumbled – again – after cloud growth slowed and total revenue hit a new 21st century low: its shares were down 2.9% last after the company stayed away from issuing a current-quarter forecast, citing economic uncertainty related to the COVID-19 pandemic.

European stocks recovered from early losses on Friday, following a bearish Asian session where investors adjusted their risk exposure before the U.S. elections two weeks away. Record COVID-19 cases in Europe also weighed on sentiment. MSCI’s European Index was up 0.4% while the STOXX 600 was up 0.2, after initially falling as fears about the economic impact of lockdown restrictions outweighed some strong earnings. UBS gained the Swiss banking giant’s credit, FX and rates traders performed better than almost all of their rivals in New York as they took advantage of a virus-fueled trading bonanza. Total revenue rose 41%, beating JPMorgan and Citi but falling short of Goldman. UBS also beat on profit and said it lined up $1.5 billion for share buybacks.

New, tougher restrictions to limit the spread of coronavirus in Europe weighed on sentiment. Ireland announced some of Europe’s strictest constraints on Monday, telling people not to travel more than five kilometers from home. New restrictions were also approved in the Lombardy region of Italy. France reported a massive increase in the number of people hospitalised.

Earlier in the session, Asian stocks fell, led by the energy and finance sectors, after climbing in the last session. Markets in the region were mixed, with South Korea’s Kospi and China’s Shanghai Composite gaining, while Japan’s Topix and Australia’s S&P/ASX 200 slid. The Topix lost 0.7%, with SoftBank and Nintendo contributing the most to the move. The Shanghai Composite Index rose 0.5%, driven by Kweichow Moutai and Foshan Haitian.

With just two weeks until the U.S. presidential elections on Nov. 3, analysts said that investors were reining in their riskier bets. Meanwhile attention is on the outcome of today’s stimulus negotiations.

“The likelihood of a deal taking place appears no more likely now than it was a week ago,” said Michael Hewson, chief market analyst at CMC Markets. The lack of action is particularly concerning in light of rising COVID-19 cases in the United States, he said. “While equity markets appear to be struggling in the short term, the lack of a fiscal stimulus deal in the next two weeks is probably neither here nor there. Most investors expect to see some sort of fiscal stimulus in the next six months, whoever gets in, with the only unknown being around the size and scale, and the timing. The problem for stock markets is that they want to see it now.”

In FX, the dollar was again lower with the Bloomberg Dollar Index sliding as the greenback fell against most of its Group-of-10 peers; the euro advanced, topping 1.18 per dollar as European equities reversed an early decline. Australia’s dollar weakened after RBA Assistant Governor Kent said the Board is considering the case for further easing, there is some room to cut the Cash Rate further, one option is to purchase longer-dated bonds – bond purchases would be regular and aimed to bring down yield. Kent also said expansion of balance sheet is adding monetary stimulus, need policy support to be provided for some time given. Kent remarked that the Bank Bill Swap Rate (BBSW) could move into negative territory in the case of further RBA easing. He also reiterated that the central bank will not increase Cash Rate until actual inflation is sustainably in the target range. RBA has not done a formal policy framework review.

RBA Minutes noted the Board discussed the case for additional monetary easing to support jobs and the overall economy. As in previous meetings, members discussed the options of reducing the targets for the cash rate and the 3-year yield towards zero, without going negative, and buying government bonds further along the yield curve. While members noted that the Australian dollar exchange rate was broadly consistent with its fundamental determinants, a lower exchange rate would provide more stimulus to the Australian economy in the recovery phase.

New Zealand’s currency also declined on speculation the central bank may act to lower borrowing costs. In minutes of its October meeeting, Australia’s central bank said further policy easing is likely to “gain more traction” as restrictions are lifted across the economy and agreed the governor would flag the shift to targeting actual over forecast inflation. The pound swung between gains and losses after the U.K. rebuffed the European Union’s effort to restart deadlocked trade negotiations and as investors waited for evidence that the two sides are reconciling their differences.

In rates, Treasuries were lower again with the curve steeper in early U.S. trading as front-end yields remain anchored while long-end yields were cheaper by ~2bp, 10-year by 1.5bp at 0.784% after breaching Monday’s high. Risk appetite stirred during Asia session and European morning, lifting S&P 500 futures, as investors eyed potential for agreement in stimulus talks today. Euro zone government bond yields rose, with the benchmark 10-year German yield holding near recent seven-month lows at -0.623%.

Gold edged down while oil prices were little changed after three days of declines on fears that a resurgence of COVID-19 infections would stifle the recovery in fuel demand. Brent crude futures were trading down 2 cents, or 0.4%, at $42.44 a barrel recovering ground after falling as low as $42.19 earlier in the session.

Looking at the day ahead, we have earnings from Procter & Gamble, Netflix, Texas Instruments, Philip Morris International and Lockheed Martin. Central bank speakers include Fed Vice Chair Quarles, the Fed’s Bostic and Evans, the ECB’s Hernandez de Cos and the BoE’s Vlieghe. And data releases include US housing starts and building permits for September.

Market Snapshot

S&P 500 futures up 0.6% to 3,442.50

Brent futures down 0.6% to $42.38/bbl

Gold spot up 0.1% to $1,905.95

U.S. Dollar Index down 0.2% to 93.29

STOXX Europe 600 up 0.2% to 367.49

MXAP down 0.3% to 175.21

MXAPJ down 0.01% to 582.59

Nikkei down 0.4% to 23,567.04

Topix down 0.8% to 1,625.74

Hang Seng Index up 0.1% to 24,569.54

Shanghai Composite up 0.5% to 3,328.10

Sensex up 0.2% to 40,518.88

Australia S&P/ASX 200 down 0.7% to 6,184.58

Kospi up 0.5% to 2,358.41

German 10Y yield rose 0.4 bps to -0.624%

Euro up 0.07% to $1.1777

Italian 10Y yield rose 6.9 bps to 0.518%

Spanish 10Y yield rose 1.6 bps to 0.175%

Top Overnight News from Bloomberg

Ireland and Wales announced renewed lockdowns and Italy’s financial center sought a curfew, as Europe steps up efforts to regain control of the coronavirus pandemic

The European Union’s first offering of social bonds was said to receive orders of more than 233 billion euros ($275 billion), a record in the euro area

The ECB takes the crusade to revive faith in its inflation- fighting credentials to members of the public on Wednesday. They’ll get to share their views with President Christine Lagarde, who vowed at the start of her term just under a year ago to make the central bank better understood, and chief economist Philip Lane

Goldman Sachs Group Inc. has reached a long-awaited pact with the U.S. Department of Justice to pay more than $2 billion for the bank’s role in Malaysia’s 1MDB scandal, and the deal may be announced within days, according to people familiar with the matter

China’s hotels and restaurants, one of the hardest-hit sectors of the economy during the coronavirus pandemic, remained a significant drag on growth in the third quarter even as the recovery gained momentum

A quick look at global markets courtesy of NewsSquawk:

Major Asia-Pac indices traded with losses across the board after Wall Street suffered a broad decline following reports which suggested a State-side stimulus deal is not sounding imminent based on comments from the House Speaker and Committee Chairs. US equity futures opened electronic trade in modest positive territory, but have since came off highs and traded sideways throughout the night, with ES, NQ and YM still holding onto some gains heading into the European open. Back to APAC, ASX 200 (-0.7%) was pressured by its mining sector, albeit the index saw some fleeting upside in light of further the dovish RBA rhetoric, this time from Assistant Governor Kent. Nikkei 225 (-0.5%) failed to benefit from the JPY dynamics as the index felt the weight of losses across its industrial sector. KOSPI (+0.5) initially conformed to the losses in the region, with Hyundai and its affiliate Kia posting losses between 3-4% after the former warned that Q3 profits will be hit by charges related to engine problems. Meanwhile, SK Hynix traded in the red after the chipmaker confirmed that it is to purchase Intel’s NAND memory business. Elsewhere, the humdrum tone reverberated into China, with Hang Seng (U/C) and Shanghai Comp. (+0.4%) modestly softer for much of the session despite another PBoC liquidity injection and a non-event LPR setting as anticipated; however, the bourse did pick up somewhat in the tail-end of APAC trade.

Top Asian News

Orr Says RBNZ Prepared to Use All Tools to Counter Deflation

Thai Central Bank Chief Signals Support Amid Uneven Recovery

RBA Sees Monetary Policy Having More Traction as Economy Reopens

H.K.- Singapore Bubble May Have 1 Return Flight per Day Initially

European equities (Eurostoxx 50 +0.1%) trade mixed to flat in what has been a relatively indecisive session thus far with little in the way of incremental macro newsflow since yesterday’s close. Slightly outperformance has been observed in the CAC 40 (+0.3%) with Accor (+6.0%) top of the index after a broker upgrade from JP Morgan with the bank upbeat on the Co. “as it streamlines costs, simplifies its business, whilst its sound BS should support small/midscale M&A, allowing the company to emerge from the crisis stronger”. Sectors are mixed with not much in the way of breadth across the broader categories; oil & gas is the main outlier to the downside amid modest losses in the crude complex. Travel & leisure names have been granted some reprieve amid plans to open up international travel to the UK with Heathrow implemented a rapid COVID-19 testing operation for some destinations. As such, IAG (+6.3%), whose British Airways will be one of the first to offer testing, sit at the top of the Stoxx 600, gains are slightly less pronounced for some of the budget airlines such as easyJet (+4.0%) and Ryanair (+2.5%). Elsewhere, support has also been observed in the banking sector post-earnings from UBS (+2.2%) with the Co. far exceeding Q3 net income expectations in what was its “best Q3 earnings in a decade”. Additionally, the Co. announced it has set aside USD 1.5bln for potential share buybacks and currently has USD 1bln available to be paid out as a cash dividend in 2021. Reckitt Benckiser (+1.4%) are another gainer this morning after Q3 earnings were boosted by surging Dettol sales throughout the pandemic. To the downside, Tele2 (-1.5%) are the Stoxx 600 laggard post-earnings, albeit having pared back much of the initial downside, in a session that has featured several Scandi updates, including Stora Enso, Swedbank and Yara International.

Top European News

Lockdowns Return to Ireland and Wales in Europe’s Virus Response

Italian State Lender CDP Bids With Funds for 88% of Autostrade

Boohoo Falls on Report Audit Firms Decline to Work With Retailer

ECB Carves Out Its Own Path in the Mission to Revive Inflation

In FX, the race to the bottom is back on down under, and even though a 15 bp RBA rate cut looms larger than the next batch of RBNZ stimulus, the tables have turned to the detriment of the Kiwi. Indeed, Nzd/Usd has relinquished 0.6600+ status and breached the 100 DMA at 0.6586, as the Aud/Nzd cross rebounds from sub-1.0700 and Aud/Usd pivots 0.7050. To recap, minutes from the October policy meeting coupled with comments from RBA Deputy Governor Kent all but sealed an ease early next month, with the latter also noting that Bank Bill Swap rates may also fall below 0% if benchmark rates are reduced further, while RBNZ Governor Orr remarked that there is ample room to deliver more QE and an update on tools will be forthcoming in November.

USD – Antipodean underperformance aside, the Buck is mixed vs G10 rivals as broad risk sentiment recovers and the DXY hovers just above Monday’s base within a 93.204-512 range ahead of US housing data, a few Fed speakers and House Speaker Pelosi’s deadline for a pre-election fiscal stimulus deal that looks unrealistic or optimistic at this stage.

EUR/CHF/GBP/CAD/JPY – The Euro is maintaining momentum above 1.1750 vs the Greenback and seems well flanked by decent option expiry interest at 1.1745 (1.4 bn) and between 1.1790-1.1800 (1.3 bn) to the upside that also incorporates yesterday’s high and the 50 DMA (1.1795). Meanwhile, the Franc continues to straddle 0.9100 with little reaction to Swiss trade data showing a narrower surplus, but key watch exports declining at a similar pace to the previous month, and the Pound is holding around 1.2950 awaiting BoE commentary from Vlieghe and any further Brexit developments ahead of speeches by the European Commission President von der Leyen and her VP Sefcovic. However, Sterling looks a bit leggy against the single currency as Eur/Gbp probes 0.9100 amidst reports of RHS flows, though recent peaks circa 0.9120-25 may cap further upside irrespective of charts indicating a break of a descending channel. Elsewhere, the Loonie is hovering just above 1.3200 in advance of Canadian inflation on Wednesday and the Yen has slipped a fraction to trade either side of 105.50 following overnight source reports suggesting that the BoJ will downgrade GDP and CPI forecasts when it meets next week.

SCANDI/EM – Not a lot of movement or deviation in Eur/Sek around 10.2800 on the back of standard Riksbank rhetoric, but Usd/Cnh and Usd/Cny have fallen further to fresh 2+ year troughs near 6.6700 and 6.6800 respectively as the PBoC gradually lowers its daily midpoint setting for the onshore Yuan and maintained LPRs for the 6th consecutive month.

In commodities, a relatively slow session for the commodity space thus far in terms of fundamental updates as the dust settles following yesterday’s JMMC meeting, which ended up making no recommendation to change policy prior to 2021; the next gathering is November 17th ahead of the full OPEC+ event at the month’s end. Perhaps most notably from the meeting, reports highlight there was no indication of Russia putting forward a compensation plan for their 430k/bbl of overproduction; as such, attention will turn to whether the likes of Saudi put pressure on Russia to unveil a plan and whether some of the other over-complying members follow Russia’s lead on this matter in the months ahead. Price action throughout the session has been choppy but relatively contained compared with the action seen yesterday; currently, benchmarks remain in proximity to the unchanged mark but closer to the top-end of the day’s range. Crude explicitly, the sessions highlight will be the private inventory report which may well display another crude drawdown given a significant magnitude of production remained shut-in last week given the after-effects of Hurricane Delta. As a reminder, last week’s report printed a draw of 5.4mln which was followed by the EIA reading of a 3.818mln draw. Moving to metals, spot gold has been uneventful and in proximity to flat levels for the majority of the session following similar price action in the later-half of APAC trade. However, most recently the precious metal has gleaned some strength from further downside in the DXY as sentiment stateside remains cautiously firm as the Democrats stimulus deadline approaches. Separately, BHP updated that their copper operations in South America are still being affected by COVID-19 related measures but nonetheless copper production came in at 413k/T vs. Exp. 394k/T for Q1.

US Event Calendar

8:30am: Housing Starts, est. 1.47m, prior 1.42m; MoM, est. 3.46%, prior -5.1%

8:30am: Building Permits, est. 1.52m, prior 1.47m; MoM, est. 2.98%, prior -0.9%

DB’s Jim Reid concludes the overnight wrap

US equity markets lost significant ground yesterday amidst ongoing stimulus discussions as investors awaited a raft of earnings releases which heat up from today. Over the weekend speaker Pelosi set the end of today as the deadline to make progress ahead of the election. So today could be interesting.

In terms of the latest, Treasury Secretary Mnuchin and Speaker Pelosi spoke late in the session yesterday, but the Speaker told fellow Democratic lawmakers afterwards that significant areas of disagreement continue to get in the way of a deal. The two sides remain talking ahead of today’s deadline. While the Republican-led Senate has been reluctant to pass a stimulus bill above the $500 billion level that Majority leader McConnell has supported, President Trump has indicated that he is willing to go up to the $2.2 trillion range that Democrats have demanded. Mr Trump said yesterday that if an agreement with Democrats is reached, he would “lean” on Republican Senators to “come along.”

Regardless, the confirmation that the two sides remain significantly apart saw the S&P 500 fall over 1.1% in the last 90 minutes of trading, though the index had been dripping lower throughout the day as risk sentiment soured after a healthy start. By the end of the session, the S&P 500 had lost -1.63%, while the VIX index rose +1.8pts in its 6thconsecutive move higher.

Overnight, S&P 500 futures (+0.34%) are trading back up a little on headlines that the House Speaker Pelosi and Treasury Secretary Mnuchin have “continued to narrow their differences” on a coronavirus relief package. So expect the dance to continue today.

The large losses yesterday saw every industry in the S&P lower on the day, with the Tech (-1.87%) and Energy (-2.10%) sectors leading the declines. In spite of the heavy tech losses, especially among the recent mega cap winners, the NASDAQ (-1.65%) fell largely in line with the S&P. The Dow Jones (-1.44%) also moved lower, while in Europe, the STOXX 600 lost just -0.18% – having closed prior to the US stimulus headlines roiling markets.

Asian markets are trading lower tracking Wall Street’s move from yesterday. The Nikkei (-0.55%), Hang Seng (-0.09%), Shanghai Comp (-0.13%), Kospi (-0.21%) and Asx (-0.63%) are all down.

On the coronavirus, there were further concerning developments from the US and Europe, as the number of confirmed global cases passed the 40m mark yesterday, and governments around the world moved to re-impose restrictions once again. Here in the UK, a further 18,830 cases were reported yesterday as Wales announced a 2-week ‘firebreak’ that would start on Friday evening. In practice, this means that people will be told to stay at home, apart from certain exceptions, with pubs, restaurants and non-essential shops all closing. Prime Minister Johnson has come under pressure to pursue a similar move in England, with opposition Labour leader Keir Starmer having already called for one to be imposed. Elsewhere in Europe, case numbers also remained at elevated levels as you’ll see in the table below. Monday reporting is always a little challenging to interpret though due to the weekend impact.

In terms of further restrictions, Ireland is moving closer towards a full lockdown as of Wednesday night. The new restrictions will close all retail, restaurants and pubs, while schools will remain open. Elsewhere Austria changed the limit on gatherings to 6 people indoors and 12 people outdoors, while Slovenia announced that a 9pm-6am curfew would come into force from today. So far most countries seem relatively keen to keep schools open as much as possible which is a huge economic swing factor given that it governs what parents can do.

Over in the US, weekly cases are set to rise above 400k per week for the first time since early August, with the majority of the outbreaks in regions that either had yet to experience significant caseloads or had relatively moderate first waves. Overnight, the US CDC has issued a “strong recommendation” for mask-wearing by both passengers and operators on planes, trains, buses and taxis. On a related note, Our chart of the day yesterday (link here) actually looked at the average age of deaths across a number of countries from Covid-19, and the US stood out in having a much lower average age of death than the other developed countries at 75.8 (vs. 80-82) in most of the others. Separately, one note of optimism from the US was that the Transport Security Administration said that they had over 1 million passengers go through a security checkpoint on Sunday for the first time since March, while the weekly volume from Oct 12-18 was also the highest since the start of the pandemic.

On the vaccine front, Moderna said overnight that the US government could authorise emergency use of its Covid-19 vaccine in December if it gets positive interim results in November from a large clinical trial. A reminder that even the UK is working to mobilise for a possible vaccine rollout by December. So a month to watch.

Over in fixed income, sovereign bonds lost ground for the most part yesterday, with yields on 10yr Treasuries up +2.3bps, as the 2s10s curve also steeped +1.9bps. Meanwhile in southern Europe, yields on 10yr Italian BTPs came off their all-time closing low on Friday, as they moved up +7.5bps, whilst Spanish (+4.1bps) and Greek (+4.1bps) bonds similarly lost ground. Bunds and gilts were the exception to this pattern however with 10yr bund yields down another -0.6bps to a fresh 7-month low of -0.63%, while those on gilts fell -1.3bps.

Onto Brexit, and in spite of Prime Minister Johnson’s Friday statement that the UK should get ready to leave the transition period without a trade agreement in place, the two sides’ chief negotiators spoke once again yesterday. In a tweet afterwards, the EU’s Michel Barnier said that “I confirmed that the EU remains available to intensify talks in London this week, on all subjects, and based on legal texts. We now wait for the UK’s reaction.” Sterling strengthened by +0.26% against the US dollar yesterday, though this seemed to be more of a dollar-negative story as the dollar index lost -0.27%. Overnight, Bloomberg has reported that the UK is rebuffing the EU’s effort to restart their deadlocked trade negotiations, holding out for more concessions from the bloc before it is prepared to restart talks. The same report though quoted three unidentified EU officials as saying that they expect the negotiations to resume in London by the end of the week. A bit like the US fiscal stimulus, this is now a political dance. We hope no one stumbles!

Staying on politics, there weren’t a great deal of updates on the US election yesterday as the polls continued to show a solid lead for Joe Biden. His chances of victory in FiveThirtyEight’s model now stand at a campaign high of 88%, while the Democrats’ odds of controlling the Senate are at 74%. This week’s debate on Thursday will be the main highlight, but the unprecedented quantity of early voting in this election means that the ability to change the trajectory of the race is diminishing with each passing day. Overnight, the Commission on Presidential Debates has said that President Donald Trump and Democratic nominee Joe Biden will have their microphones turned off during parts of the final presidential debate while adding that each candidate will have an uninterrupted two minutes to speak at the beginning of each of the six 15-minute segments of the debate. Their mics will be turned on again for “a period of open discussion” in the segment’s remaining time. The change comes after the chaotic first debate in which both the candidates talked over the moderator and each other. The list of topic in this Thursday’s debate include Covid-19, American families, race in America, climate change, national security and leadership.

There also wasn’t much in the way of data yesterday, though the NAHB’s housing market index in the US for October rose to another record high of 85 (vs. 83 expected).

via ZeroHedge News https://ift.tt/34gGnw9 Tyler Durden

A person who claims to be a program manager at Google Cloud has told investigative journalists with Project Veritas that the search engine is intentionally manipulating results in order to benefit the Democrats and to hinder President Trump’s campaign.

Ritesh Lakhkar, who identified himself as a technical program manager at Google’s Cloud service, made the comments in footage released Monday. The interview appears to have been filmed without Lakhkar’s knowledge.

The project manager accused Google of “playing god” with US politics, and of ‘skewing’ it’s algorithms to project negative news and talking points where Trump is concerned.

BREAKING: @Google Program Manager Confirms Election Interference In Favor of @JoeBiden

Google search “skewed by owners and drivers of the algorithm”

When asked if Google favours one party over another, Lakhkar commented that “The wind is blowing toward Democrats, because GOP equals Trump and Trump equals GOP. Everybody hates it, even though GOP may have good traits, no one wants to acknowledge them right now.”

“So the wind is blowing toward Democrats, so let’s skew the results toward Democrats,” he added.

“It’s skewed by the owners or the drivers of the algorithm,” Lakhkar explains, adding “Like, if I say ‘Hey Google, here’s another two billion dollars, feed this data set of whenever Joe Biden is searched, you’ll get these results.’”

Remember when Google had that meeting in 2016 after Trump won and vowed to never let it happen again?

Have you tried finding anything on Google in the last 2 years that doesn’t amplify Democrat talking points?

Lakhkar slammed Big Tech for “playing god and taking away freedom of speech on both sides.”

He emphasised that “Like, if it was fraud it doesn’t matter, but for Trump or Melania Trump, it matters… Trump says something, misinformation. You’re going to delete that because it’s illegal under whatever pretext. And if a Democratic leader says that, you’re going to leave it.”

Describing the working environment at Google, Lakhkar said “your opinion matters more than your work.”

“When Trump won the first time, people were crying in the corridors of Google. There were protests, there were marches. There were like, I guess, group therapy sessions for employees organized by HR,” he said.

The whistleblower continued, “I guess that’s one of the reasons I feel suffocated [at Google]. Because on one side you have this unprofessional attitude, and on the other side you have this ultra-leftist attitude. Your entire existence is questioned.”

Google has not responded to the allegations at time of writing.

via ZeroHedge News https://ift.tt/37vwvQS Tyler Durden

Crime Pays: Goldman Strikes $2BN Deal With DoJ To Avoid All Charges Tied To 1MDB Tyler Durden

Tue, 10/20/2020 – 07:30

Goldman Sachs is reportedly on the cusp of settling one of the biggest criminal cases involving a Wall Street bank since the financial crisis: According to a Bloomberg News report published late Monday evening, the Vampire Squid has reached a tentative agreement with the DoJ to pay more than $2 billion in penalties – a figure that BBG noted is “broadly in line with analysts expectations” – and – here’s the key bit – allows the bank to avoid all criminal penalties.

That last bit is especially important, because, as we’ve chronicled over the past few years, many of the bank’s top executives appeared to have been personally involved with the deal, which was initially brought in by Tim Leissner, formerly the bank’s top man in Southeast Asia, before he was suspended over the deal, before agreeing to cooperate with the Feds against his former employer (where he reportedly told authorities about the endemic “culture of corruption” at play within the bank).

Though we can’t be certain, we suspect that the timing of former Goldman chief Lloyd Blankfein’s departure was influenced by the unfurling scandal; he suddenly left the bank right around the time that Leissner flipped. Word on the street was that Goldman would be made to admit guilt as part of the deal. Indeed, a leak about an ‘imminent’ deal published nearly 1 year ago claimed that the bank had reluctantly agreed to the plea. Apparently, the bank’s legal team was able to avert this, amid whispers that connections between Goldman’s representatives and the current leaders of the DoJ might create conflicts of interest (a negotiating tactic that the bank appears to have leveraged to its advantage; note the deal is reportedly coming just weeks before a close American presidential election).

The deal comes just months after Goldman agreed to pay $3.9 billion in “reparations” to the government of Malaysia for its role in raising the $6.5 billion that seeded the 1MDB sovereign wealth fund, which was supposed to be used to finance public projects, but was instead drained by cronies of former Malaysian Prime Minister Najib Razak, who has been convicted in Malaysia for his role in the region’s largest-ever financial fraud.

That settlement included $2.5 billion in cash payments from Goldman to the Malaysian government.

But the fraud’s true ringleader was a mysterious financier named Jho Low, who allegedly orchestrated the siphoning off of money from the fund, which was disbursed to bank accounts controlled by Razak, and others controlled by Low and presumably other cronies. Low went on to spend the money on a seemingly endless stream of luxury goods – jewels, fine art, yachts – Low even used some of the money to finance the film “the Wolf of Wall Street”.

The DoJ has seized billions of dollars of these ill-gotten gains, and even returned some of the stolen money to Malaysia.

Goldman has struck deals with prosecutors in at least three countries over its role in 1MDB: in Singapore, the bank could face serious criminal penalties if it is caught violating its settlement agreement. All told, the bank will pay $5 billion in cash penalties tied to 1MDB, an amount that’s roughly in line with expectations.

Goldman pays $2 Bn in 1MBD corruption probe, avoids criminal conviction.

In return, the bank and its top executives will simply walk away, while Leissner (who pleaded guilty two years ago per his plea deal) and another banker who was arrested in connection with the investigation are left to face the music.

via ZeroHedge News https://ift.tt/31q2fmH Tyler Durden

COVID-19 diagnostic testing has been greatly scaled up from a few thousand tests per week back in early March to 2 million tests per week in early August. But the summer upsurge in COVID-19 diagnoses, hospitalizations, and deaths in the U.S. highlights the fact that we still don’t have enough testing to provide individual Americans and health care professionals with the information needed to squelch the pandemic.

A huge part of the problem is that most asymptomatic, presymptomatic, and mildly afflicted people don’t know they’re infected, even as they spread the virus to others while working, shopping, and gathering in enclosed spaces such as bars and restaurants. Making cheap, fast tests available for use at workplaces, schools, and homes could solve this information deficit problem. “The way forward is not a perfect test,” Harvard medical professor Ashish Jha argued in Time, “but one offering rapid results.”

The good news is that a number of companies, including biotech startup E25Bio, diagnostics maker OraSure, and the 3M Co., are working on and could quickly deploy rapid at-home COVID-19 diagnostic tests. These antigen tests work by detecting, within minutes, the presence of coronavirus proteins using specific antibodies embedded on a paper test strip coated with nasal swab samples or saliva. Somewhat like at-home pregnancy tests, the antigen tests change color or reveal lines if COVID-19 proteins are recognized.

But there is one major problem. “Everyone says, ‘Why aren’t you doing this already?’ My answer is, ‘It is illegal to do this right now,'” Harvard epidemiologist Michael Mina told The Harvard Gazette in August. “Until the regulatory landscape changes, those companies have no reason to bring a product to market.”

It took Food and Drug Administration regulators until July to finally issue the agency’s template for approving tests that “can be performed entirely at home or in other settings besides a lab” and without a prescription.

It would cost around $20 billion to provide 330 million Americans with rapid at-home test kits costing $1 each for weekly use. Given that the federal government has already borrowed $3 trillion in response to the pandemic and appears interested in borrowing trillions more, that would be a real bargain. Such a testing regime “will stop the vast majority of transmission and it will cause these outbreaks to disappear in a matter of weeks,” Mina said. “This is something we can actually do at warp speed.”

from Latest – Reason.com https://ift.tt/2FIAe27

via IFTTT