“Very Challenging” – Norway Wealth Fund Lost Record $113 Billion, Withdraws Money To Fight Virus Crisis

The stock market crash around the world, triggered by coronavirus pandemic, has led to unprecedented losses for the world’s biggest sovereign wealth fund.

According to Bloomberg, Norway’s sovereign wealth fund lost $113 billion in the first quarter. The fund has generally used stock market declines or even bear markets to buy the dip. But maybe this time is different: The fund is offloading assets to cover emergency spending that the government needs to combat the virus.

As a whole, the fund lost 14.5% last quarter, clawing back some losses after a monster rip in global stocks last week. Still, its stock portfolio was down 21.1% over the period, with a slight gain in fixed income investments of 1.3%.

“The market situation is very challenging,” said Yngve Slyngstad, CEO of Norges Bank Investment Management (NBIM). “However, the fund has a long-term horizon.”

The virus situation in Norway is quickly deteriorating. There are now 4,848 positive cases and 44 people dead. What’s concerning health officials is that with increased cases, more and more people need hospitalization, which is straining the country’s healthcare system.

With its equity portion of the fund falling five percentage points below the 70% target, the fund will need to rebalance. Slyngstad said in the last week of March that rebalancing would likely happen through selling bonds rather than buying stocks.

The government withdrew $6.49 billion from NBIM last quarter as the virus crisis worsened in March.

We noted last week that traders were waiting for a rebalancing of sovereign pension funds such NBIM to buy the stock market dip and force a V-shape recovery, but we are finding out this week, that might not be the case.

Here’s how social media is reacting to the news:

Norway’s sovereign wealth fund lost a record $113bn in Q1 2020

Another example that this is an insolvency crisis.

— The Sirius Report (@thesiriusreport) April 2, 2020

Norway has the world’s largest sovereign wealth fund, but no gold reserves. Sold it all in 2004!

NB! Norway Sovereign Wealth Fund lost USD 113 billion in Q1!!

This is why a centralised wealth fund is not a good solution, and why Maggie T’s decision to let the profits from N. Sea oil flow back into the economy through the market was a much better solution for UK economy.

The world’s biggest sovereign wealth fund is about to start liquidating assets. Norway is facing its worst economic shock in 50 years & needs to withdraw record amounts from its sovereign wealth fund. Source: Bloomberg *Exposure to Indian companies*

Pl give ur opinion

The unknown that lays ahead for all of us is both exhilarating and scary. Exhilarating in the long term, but rather scary in the short term. All empires eventually die and we’re in the terminal phase of the New World Order that will not recover from the Russian roulette game it has been playing, for Vladimir Putin handed it a loaded gun and it pulled the trigger.

The last few weeks put everything in place for the last battle. There are so many different facts and events, left and right, and I will try to do my best to remain methodical in this complicated expose. Bare with me, I’ve been struggling for three weeks with this article because of the insane amount of additional details that each day provides. It might have been a wrong time to quit smoking, but I enjoy a good challenge.

Dropping dollars

A little context is required. The New World Order concept is simply the wish of a handful of international bankers that want to economically and politically rule the whole planet as one happy family. It started in 1773 and if it went through important changes over the years, but the concept and objective haven’t changed an iota. Unfortunately for them, international banks that have been looting the planet through the US dollar since 1944 are now threatened by hyperinflation, as their printing machine has been rotating for years to cover their absurd spendings to sustain oil and resource wars that they’ve all ultimately lost. In order to prevent this upcoming hyperinflation, they generated a virus attack on four countries (China, Iran, Italy and now the United States) to spread panic in the population, with the precious help of their ignominious medias. Even though this corona virus isn’t different from any new viruses that attack humans every year, the media scare pushed people to voluntarily isolate themselves through fear and terror. Some lost their jobs, companies are going bankrupt, the panic created a stock exchange crash that emptied wallets and dried assets, resulting in a few trillion virtual dollars off the market to release pressure off the currency.

So far, so good, but everything else went wrong in this desperate and ultimate banzai. The top virologist on the planet confirmed that chloroquine was being used by the Chinese with spectacular results to cure patients, then he improved his magic potion by adding a pneumonic antibacterial called azythromicin, and saved everyone of his first 1000 cases, but one. Donald Trump immediately imposed the same treatment through a fight against his own Federal Drug Administration, bought and owned by the deep state. This forced all medias to talk about Dr Didier Raoult’s Miracle Elixir, signing the death warrant on our confidence in all Western governments, their medical agencies, the World Health Organization, and medias that were trying to destroy the impeccable doctor’s reputation, while inventing sudden «dangerous side effects» of a nearly inoffensive drug that has been used for 60 years to treat malaria. Not so far away in Germany, internationally praised Dr Wolfgand Wodarg noted that the engineered panic was totally useless, since this virus isn’t any different than the others that affect us every years. This has been an amazing victory for Trump and the general population on social medias, whom exposed together the pathological lies of the official communication channels of every New World Order country. De facto, the credibility’s of these puppet governments have vanished in the air, and from the eye of the storm, Italy will surely exit the EU right after the crisis, which will trigger a domino effect running through every EU countries and NATO members. My friends, globalism is dead and ready for cremation.

Digging the abyss

International bankers couldn’t see it coming in 1991, when they dominated 95% of the planet after the fall of the Soviet Union. It seemed that nothing could halt their ultimate mission to complete their Orwellian dream: destroy a few countries in the Middle East, enlarge Israel, and get the total control over the world oil market, the last piece of their Xanadu puzzle that they’ve been working on for a whole century, starting with the Balfour declaration in 1917.

When Vladimir Putin got charge of Russia, there was no sign that he would do better than the drunk he had replaced. An ex KGB officer seemed like a choice more driven by nostalgia rather than ideology, but Putin had many more assets going for him than first met the eyes: patriotism, humanism, a sense of justice, cunning ruse, a genius economist friend named Sergey Glazyev whom openly despised the New World Order, but above all, he embodied the reincarnation of the long lost Russian ideology of total political and economical independence. After a few years spent at draining the Russian swamp from the oligarchs and mafiosis that his stumbling predecessor had left in his trail of empty bottles, Vlad rolled his sleeves and got to work.

Because his opponents had been looting the planet for 250 years through colonization insured by a military dominance, Vlad knew that he had to start by building an invincible military machine. And he did. He came up with different types of hypersonic missiles that can’t be stopped, the best defensive systems on the planet, the best electronic jamming systems, and the best planes. Then to make sure that a nuclear war wouldn’t be an option, he came up with stuff which nightmares are made of, such as the Sarmat, the Poseidon and the Avangard, all unstoppable and able to destroy any country in a matter of a few hours.

Russian President Vladimir Putin, center, gestures while speaking during an annual meeting with top military officials in the National Defense Control Center in Moscow, December 24, 2019. Putin said that Russia is the only country in the world that has hypersonic weapons even though its military spending is a fraction of the U.S. military budget. Russian Defense Minister Sergei Shoigu, left, and Chief of General Staff of Russia Valery Gerasimov, right, attend the meeting.

With a new and unmatched arsenal, he could proceed to defeat any NATO force or any of its proxies, as he did starting in September 2015 in Syria. He proved to every country that independence from the NWO banking system was now a matter of choice. Putin not only won the Syrian war, but he won the support of many New World Order countries that suddenly switched sides upon realizing how invincible Russia had become. On a diplomatic level, it also got mighty China by its side, and then managed to protect independent oil producers such as Venezuela and Iran, while leaders like Erdogan of Turkey and Muhammad Ben Salman of Saudi Arabia decided to side with Russia, who isn’t holding the best poker hand, but the whole deck of cards.

Ending in the conclusion that Putin now controls the all-mighty oil market, the unavoidable energy resource that lubricates economies and armies, while the banksters’ NATO can only watch, without any means to get it back. With the unbelievable results that Putin has been getting in the last five years, the New World Order suddenly looks like a house of cards about to crumble. The Empire of Banks has been terminally ill for five years, but it’s now on morphine, barely realizing what’s going on.

Tragedy and hope

Since there is no hope in starting WW3 which is lost in advance, the last banzai came out of the bushes in the shape of a virus and the ensuing media creation of a fake pandemic. The main focus was to avoid a catastrophic hyperinflation of the humongous mass of US dollar that no one wants anymore, to have time to implement their virtual world crypto-currency, as if the chronically failing bankers still have any legitimacy to keep controlling our money supplies. It seemed at first that the plan could work. That’s when Vlad took out his revolver to start the Russian roulette game and bankers blew their brains out upon the pressure on the trigger.

He called a meeting with OPEP and killed the price of oil by refusing to lower Russia’s production, taking the barrel to under 30 dollars. Without any afterthought and certainly even less remorse, Vlad killed the costly Western oil production. All the dollars that had been taken out of the market had to be re-injected by the Fed and other central banks to avoid a downslide and the final disaster. By now, our dear bankers are out of solutions.

In the meantime, Trump also poked at the tie-wearing gangsters. While medias avoided the corona-killing chloroquine subject, an old pill designed to cure malaria, Trump imposed to the FDA the use of this life-saving drug on US infected patients. Medias didn’t have any choice but to start talking about it, which ignited a chain reaction: big pharmas CEO’s were fired because they had just lost the vaccine contract, countries like Canada looked like genocidal fools for not using the cheap and inoffensive medication, while a most outrageous criminal act by a government was exposed in full light: the Macron government had proclaimed in January 2020 that chloroquine was harmful and had restrained its use, just a couple of weeks before the burst of the fake pandemic! Russian roulette is a popular game in Western governments these days around.

On Saturday March 28th, Russia announced its own corona-killing brew, based on Dr Raoult’s magic potion. Yet another Cossack blow, this time to the big pharmas jugular vein, while most Western countries now have to implement the good doctor’s treatment, or face the slap of a Russian pill coming to save its citizen. Putin is in the lifesaving business these days: in the last week of March, he sent 15 military planes filled with doctors and supplies directly to North Italy, after an aid plane from China was blocked by the Czech Republic. We’re about to learn that European countries fear that China or Russia finds the truth in the Lombardy region, where people are not dying from some corona bug, but probably from a deadly cocktail hybrid from two earlier vaccines for meningitis and influenza, that they were injected in separate vaccination campaigns.

The punchline

I said earlier that everyday brings amazing news. Well on Sunday March 29th, the most stunning of them all fell like a ton of bricks on social medias: confined onlookers learned that Trump had taken control over the Federal Reserve, that is now handled by two representatives of the Treasury of State. Of all the crazy news within the last month, this is by far the best and most shocking. After three years in power, Trump has finally fulfilled his electoral promise of taking private banks out of the US public affairs, ending a century of exploitation of the American citizens. He has put the infamous Blackrock investment group to start buying important corporations for the Fed, meaning that he’s nationalizing chunks of the economy, while avoiding the crash of the market by implicating important private investors in the deal.

President Donald Trump gestures with Jerome Powell, his nominee to become chairman of the U.S. Federal Reserve at the White House in Washington, U.S., November 2, 2017

This utmost daring move comes at a crucial point in time, and faces us with the realization that Vladimir Putin and Donald Trump are united and have taken humanity to the crossroads of the New World Order and freedom. As I have stated often before, I thought that the world would deeply change between 2020 and 2024, because these would be the last 4 years of these two heroes in political power of their nations.

The New World Order is facing the two most powerful countries on the planet, and this fake pandemic changed everything. It showed how desperate the banksters are, and if we don’t want to end up with nuclear warheads flying in both directions, Putin and Trump have to stop them now.

Terminate the BIS, the World Bank, the IMF, the European Central bank, the EU, NATO, now. Our world won’t be perfect, but it might get much better soon.

Easter resurrection is coming. This might get biblical.

Because not only food, but – most importantly – toilet paper is being stockpiled during the worldwide coronavirus pandemic, producers of precious TP are on a roll.

Sales of toilet paper in the U.S. rose by an estimated 60 percent in March compared to the same month last year.

As Statista’s Katharina Buchholz notes, the increase was more than double that in Italy, which was hit by the outbreak earlier than the U.S. There, revenues generated with bathroom tissue rose by 140 percent.

The Statista Consumer Market Outlook compared data and calculated estimates for 16 countries to show that revenues had risen most in Italy, followed by Vietnam and Australia. In other countries hit hard by the virus, for example Spain and France, the sale of toilet paper rose by 82 percent and 30 percent, respectively.

Week 1 in a country in complete shutdown. Austria has been at the forefront of forcing its citizens to “shelter in place” by enacting measures so severe that even the country’s elderly cannot remember anything similar.

To snuff out a virus that originated in China in November and has since made its way around the world, roughly a month ago, the Austrian government, led by Chancellor Sebastian Kurz, thankfully heeded a dire warning by Israeli Prime Minister Benjamin Netanyahu, took hard a look at Austria’s neighboring country, Italy, and immediately enacted a first set of measures, followed by the drastic rules mentioned above, that were first extended until April 13 and stepped up on March 30.

The new measures include wearing compulsory masks when grocery shopping, which, in due course, will be extended to the wearing masks when outdoors at any time. In addition, vulnerable men and women, that is, those whose immune systems are compromised, are required to stay home, with their salaries covered by the government. The chancellor warned the population that “what we are witnessing right now is the quiet before the storm” and added that if measures are loosened, they will start with the opening of shops and some restaurants; universities and schools will follow at the very end of this process. Schools in Austria are therefore unlikely to reopen before the fall, although there are already extensive courses online.

Noteworthy findings turned up, however, such as what public issues matter and what do not:

Borders matter.

For many years, Europeans have been told by their leaders that borders could not be closed to curb illegal migration due to the Schengen Agreement, to the detriment of security in European countries. Suddenly, with the numbers of COVID-19 deaths rising, and with the spread of the virus traced across Europe, border controls, barriers and other measures were swiftly introduced. The United States followed suit in closing its borders with Canada and Mexico. Strict border security helps to stop the virus from spreading. In the 14th century, Polish King Casimir III knew what to do in order to save his country from the plague, which had spread from China to Europe and killed countless millions of people. Poland was less affected by the plague because King Casimir isolated his country, closed borders and quarantined the border regions. Border security is health security.

Freedom of speech matters.

The Austrian government has installed a “ministry of truth” in the office of the chancellor, staffed by police cadets. In times of crisis, the search for the truth is more challenging than ever. Abundant propaganda, fake news and rumors are disseminated, even by the governments (here and here). But a cow remains a cow even if it is called a sheep. The Austrian government and the UK government have set up special task forces to weed out so-called fake news and “‘defend the country’ from misinformation” with respect to anything concerning Covid-19.

“It is absolutely stunning that a large police unit has now started to officiate in the Chancellery….The government acts as if it were in possession of the absolute truth amid a sea of lies and half-truths. On the contrary, the opposite is true… whenever a government got its hands on truth control, it has massively abused it within a very short time to gag and ban critical and oppositional voices. Once they have the power to control opinion, it is a massive temptation for those in power to use it in the self-interest of a government. The government ministers fail to realize the most important connection: the more a government carries out opinion control, the more people inevitably trust alternative sources of information, and not the government officials or those financed by the government.”

Sadly, not just the government but also Amazon, has discreetly eliminated a sizeable list of books from its listing, citing “dubious” information or even “conspiracy theories” on the defense against or even cure for Covid-19. Who decides what is a conspiracy theory? Amazon? Where has the marketplace of ideas disappeared to? Where, in fact, is the marketplace?

Sovereignty and nationalism matter.

The president of the American Freedom Alliance, Karen Siegemund, notes:

“Notice how each country – country! – took upon itself its right to sovereign action to protect its citizens.

Italy imposed quarantines; Austria closed its borders and implemented various restrictions on gatherings and mandated closures of entertainment venues, restaurants etc. Even Germany has now closed its borders.

Borders in the context of Europe is an astounding thing, and it’s heartbreaking that it took a virus, and the deaths it’s left in its wake, rather than the years-long invasions for [the countries] to assert sovereignty, and to finally, finally, turn to protecting their citizens.

“‘Europe’ in the form of the European Union has been silent. The United Nations does not even seem to be speaking out although, in a rational world they would — and should — be calling for “Crimes against humanity” charges to be brought against China. That silence under these circumstances is simply further proof of the UN’s uselessness at best, and of the EU’s utter irrelevance.

“It is nations putting the health, safety and security of their people above all else that will stem the spread of this virus; the nightmare is that it took this pandemic to wake governments up to the primacy of their people as the core of their responsibility.”

Leadership matters.

Whether the greatly differing measures taken by continental Europe or those in the United Kingdom are successful remains to be seen, but leadership in times of crisis is crucial. In the UK, it is prime minister Boris Johnson who on March 3 launched a four-step plan to combat the outbreak in the UK, later backing away from herd immunity. New and tough measures, including a lockdown, were later implemented. In Austria, Chancellor Sebastian Kurz exhibited tough leadership. It is too early to assess whether the government is taking the “right” steps; however, remaining calm and in control are key to garnering support even among his critics. Kurz is adept at team-building, by including all members of his government as well as by keeping the political opposition informed. This approach has led to bi-partisan support for all implemented measures. In the United States, President Donald J. Trump has been personally leading an extremely popular daily televised press briefing with members of his Covid-19 task force.

Receding into the background have been topics such as climate change, Greta Thunberg, and Fridays for Future. Health measures have clearly taken precedence over kids cutting school. Nevertheless, many have always been adept at “never letting a crisis go to waste” (Rahm Emanuel) and at using one to do things that could not be done before; they will probably be back to doing their best to see what they can land in their “dream catcher”.

Armed forces matter.

Germany has mobilized its military to assist in maintaining public order, with German Minister of Defense Annegret Kramp-Karrenbauer reassuring Germans that “in these difficult times, the citizens can rely on their Bundeswehr.” Despite being financially starved in recent years, the Austrian armed forces were mobilized early on in the crisis to assist the Ministry of Foreign Affairs in repatriating Austrians from abroad, providing support in logistical tasks such as stocking grocery stores, and relieving police by protecting foreign embassies in Vienna. The move proved right the rejection of the 2013 referendum to end conscription and introduce a professional army.

Civil vigilance matters.

A particularly worrisome trend is having politicians using crises to increase the power of the state — a terrifying thought. Although in this instance, people actually did need to be quarantined to prevent the rolling spread of the virus, the widespread lockdowns in the UnitedStates, Europe and in Israel — which, in Austria’s case, took place after unprecedented accelerated parliamentarydiscussion — are likely bound for even more debate after the return to normalcy. Also potentially problematic is the British Coronavirus Bill, which “will enable the police and immigration officers to detain a person, for a limited period, who is, or may be, infectious and to take them to a suitable place to enable screening and assessment”. In a different situation, the words “may be” could be ominous in their broadness. For now, however, we should be thankful to our governments for trying to contain a runaway virus to which we have no immunity until some form of limiting its medical and economic harm can be found.

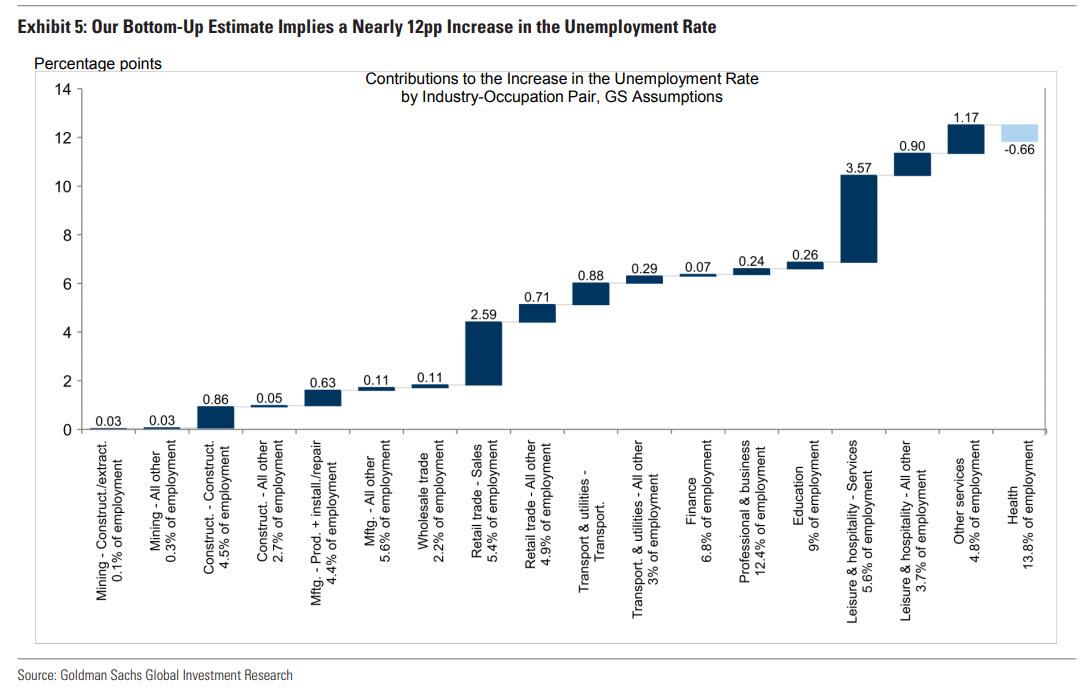

March Jobs Preview: The First Negative Print In Ten Years, And Then All Hell Breaks Loose

As RanSquawk notes, the data for March are already stale, given the release of the timelier initial jobless claims data, which showed another record high number of claims, and some 10 million laid off workers in the past 2 weeks. Additionally, the survey period of the BLS Employment Situation Report runs through the month ending 12th March, and therefore does not capture the full effect of the coronavirus disruptions on the US labor market, with “stay at home” orders being issued only after the 19th March in some US states.

Still, even though it captures only the slowdown in the first half of the month, the March jobs report will almost certainly show a decline in monthly payrolls – the first since Sept 2010 – and breaking the longest stretch of positive payroll prints on record.

That said none of that matters: with the Fed having now gone full tilt in perpetuity no matter what the data says, we know that the data for the next 3-6 months will be catastrophic, with Goldman predicting 15% unemployment in Q2, meaning that in the next two months tens of millions of people will lose their job.

As such what the BLS reports tomorrow is completely meaningless. Still, for what it’s worth, here’s what Wall Street expects:

Non-farm Payrolls: Exp. -100K, Prev. +273K

Unemployment Rate: Exp. 3.8%, Prev. 3.5%

Avg. Earnings M/M: Exp. 0.2%, Prev. 0.3%

Avg. Earnings Y/Y: Exp. 3.0%, Prev. 3.0%

Avg. Work Week Hours: Exp. 34.1, Prev. 34.4

Private Payrolls: Exp. -163k, Prev. +228k

Manufacturing Payrolls: Exp. -20k, Prev. +15k

Government Payrolls: Prev. +45k

U6 Unemployment Rate: Prev. +7.0%

Labor Force Participation: Prev. 63.4%

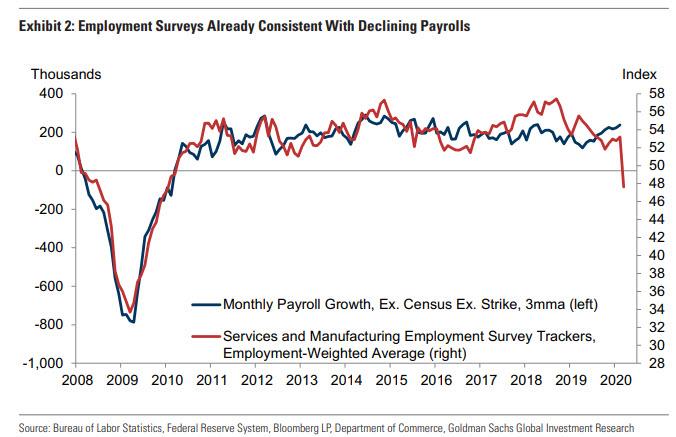

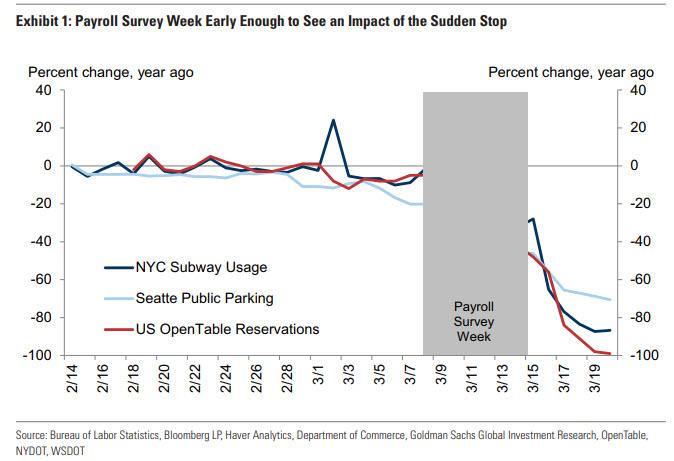

Speaking of Goldman, the bank estimates nonfarm payrolls declined 180k in March, below consensus of -100k. In addition to employment surveys falling into contractionary territory and jobless claims rebounding dramatically, sharp declines in commuting patterns in both New York City and Seattle indicate a sizeable drag from the coronavirus in those MSAs during the survey week. Goldman also estimate declining payrolls in the food services, accommodation, recreation services, social assistance, and temporary help subindustries (both in these cities and nationwide). Goldman also thinks the unemployment rate rose three tenths to 3.8%, with risks skewed towards a larger increase (consensus 3.8%). Jobless claims data indicate that the pace of layoffs increased sharply and an NPR/PBS poll found that 18% of employees were laid off or had their hours reduced. The silver lining, at least for those who still have jobs, is that the average hourly earnings increased 0.2% month-over-month and 3.0% year-over-year, reflecting negative calendar effects but a possible composition shift towards higher-paid workers (consensus also +0.2%/+3.0%).

And as noted above, while Goldman looks for a weaker-than-consensus report tomorrow, the March employment numbers are already fairly stale and insignificant in our view, “because the April report will likely show job losses in the millions.”

Here are some general observations courtesy of RanSquawk:

TREND RATES: The trend rates are meaningless going into the data, given disruptions caused by coronavirus. After the release of the February data, the 3-month average trend rate was at 243k (prev. 239k); 6-month was 231k (prev. 220k); 12-month at 201k (prev. 178k).

ADP EMPLOYMENT: ADP reported 27k payrolls were shed from the US economy in March, better than the consensus view for -150k. However, while the data appear encouraging, the ADP itself noted that the survey period ran through the 12th of the month, meaning that much of the COVID impact has not been captured in the data. It is also worth noting that the official BLS employment situation report also runs through that same period and therefore may be subject to similar caveats.

WEEKLY INITIAL JOBLESS CLAIMS: Weekly jobless claims for the week ending 28th March rose to a fresh record high 6.648mln, around double last week’s tally which was in itself a record high. The latest spike in jobless claims will not have an impact on the BLS data; in the corresponding survey period for the BLS data, initial jobless claims rose from 211k to 282k. But ahead, the data signals April’s Employment Situation Report will be grim, given accelerating claims; and ahead, analysts are not convinced the peak is in yet. Total layoffs between the March and April payroll surveys look destined to reach perhaps 16-to-20mln, according to Pantheon Macroeconomics, which would be consistent with the unemployment rate rising to 13- to-16%. “We have consistently argued from the beginning that the USD 2trln CARES Act is nothing like big enough; these data, and the numbers which will follow, make another huge package inevitable,” Pantheon said.

Additionally, some individuals may classify themselves as “employed but not at work”, which could limit the magnitude of the increase in the jobless rate tomorrow. Taken together, the March unemployment rate likely rose three tenths to 3.8%. And while the risks tomorrow are skewed towards a larger increase, the majority of the unemployment rise will occur in April and subsequent reports, with the jobless rate reaching 15% by midyear.

CHALLENGER JOB CUTS: Job cuts announced by US-based employers surged to 222,288 in March from 56,660, the highest monthly tally since January 2009; challenger noted that the data did not include the hundreds of thousands of workers who were furloughed in March. “The virus has caused total whiplash for HR, hiring managers, and recruiters. The labor data for February showed a strong economy with a tight labor market. Companies were fighting for talent across industries. Now, millions of workers have filed for unemployment, companies have frozen hiring, and in many cases, cut operations or closed completely,” Challenger said. It notes that the shut-down of nonessential businesses caused 141,844 cuts, primarily in entertainment/leisure; of the 54,300 cuts announced where no specific reason was provided, Challenger suspects many are due to COVID-19. Challenger notes that despite the jump in job cut announcements, hiring announcements have also surged during the outbreak. Instacart recently announced they would hire 300,000 new drivers, while grocery stores, like Kroger and Albertsons, are hiring tens of thousands of workers, and Pizza Hut, Domino’s, and Papa John’s are hiring thousands of delivery drivers. “The pandemic has created an opportunity for grocers and food delivery services, as well as consumer products delivery services, to thrive right now. The issue is whether they can find the workers to do jobs that now come with inherent risks that did not previously exist,” said Challenger.

BUSINESS SURVEYS: Not all of the business surveys are in ahead of the March jobs report. However, the March manufacturing ISM report saw the employment sub-index fall by 3.1 points to 43.8; ISM said this was the eighth month of employment contraction, and at a faster rate compared to February. It is again worth highlighting that the manufacturing sector accounts for around 11% of the US economy, and as such, it is difficult to infer what the ISM means for the BLS Data, particularly since manufacturing surveys have held up better than their services equivalent, of late. Additionally, some analysts, like those at UBS, have questioned the usefulness of survey data at the moment, noting that they are subject to quirks around a) some of the treatment of supply chains, which has flattered data, b) the fact that many respondents will not be replying to surveys during the virus disruption period, and c) survey data will give more accurate assessments during ‘normal’ times, perhaps not as much in unusual times.

CORONAVIRUS: As shown below, Seattle public parking and NYC subway usage both declined 30% during the survey week (and by -14% and -18% on the Monday of the survey week, respectively), consistent with a sizeable drag on economic activity and employment from the 6.5mn payroll employees in these cities. And across the entire country, OpenTable reservations declined 25% year-on-year during the survey week, with declines in 35 out of 37 major cities on Monday of the survey week. Because of the coronavirus, expected declining payrolls in the food services, accommodation, recreation services, social assistance, and temporary help subindustries in this week’s report (both nationwide and in New York City and

Seattle).

Mnuchin Says Energy Firms Can Be Bailed Out By The Fed

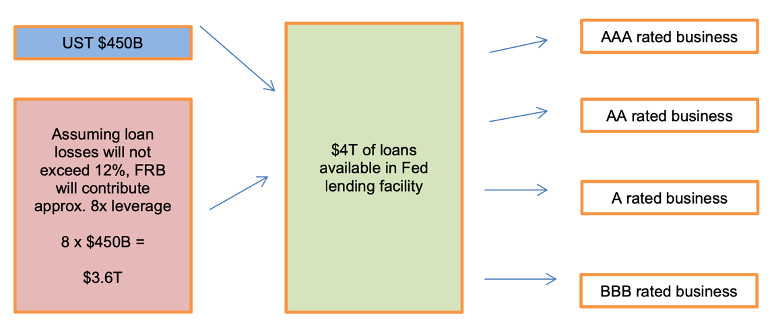

As part of the Coronavirus CARES Act, the $2 trillion fiscal stimulus meant to resuscitate the US economy, Congress allocated $454 billion to help underwrite the special lending programs from the Federal Reserve. This could generate up to $4.540 trillion in new lending (assuming 10x leverage for highly-rated assets) likely geared toward small and medium-sized businesses.

It now turns out that the first industry to benefit from direct Fed loans is the imploding US energy sector, which for the past decade benefited indirectly from Fed generosity by issuing junk bonds to yield starved investors who are now facing near certain bankruptcy in the face, as the price of oil – if it stays at this level – assures they will never be repaid.

Speaking at a White House news conference on Thursday, Treasury Secretary Steven Mnuchin said energy companies squeezed by the oil-price war can turn to the Federal Reserve’s lending facilities for aid but won’t get direct loans from his department.

“I have very limited ability to do direct loans out of the Treasury,” he said, suggesting that distressed shale companies should instead beg the Fed.

As Bloomberg notes, the $2.2 trillion coronavirus-related economic package authorizes the secretary to provide loans and grants to passenger airlines, cargo airlines, contractors and companies important to national security, Mnuchin said. Other companies must turn to the Fed, which is authorized to inject $4 trillion into the U.S. economy through various lending facilities approved by Congress.

“Our expectation is the energy companies, like all our other companies, will be able to participate in broad-based facilities, whether it’s the corporate facility or whether it’s the main street facility, but not direct lending out of the Treasury,” he said, leaving the Fed as the only option.

And now we look forward to the populist backlash when a line of insolvent shale CEOs forms outside the Marriner Eccles all begging to have their junk bonds taken out at par, and refinance with a Fed loan yielding, well, nothing and ideally forgiveable if the new round of cheap debt manages to bankrupt Saudi Arabia as the price of oil goes negative.

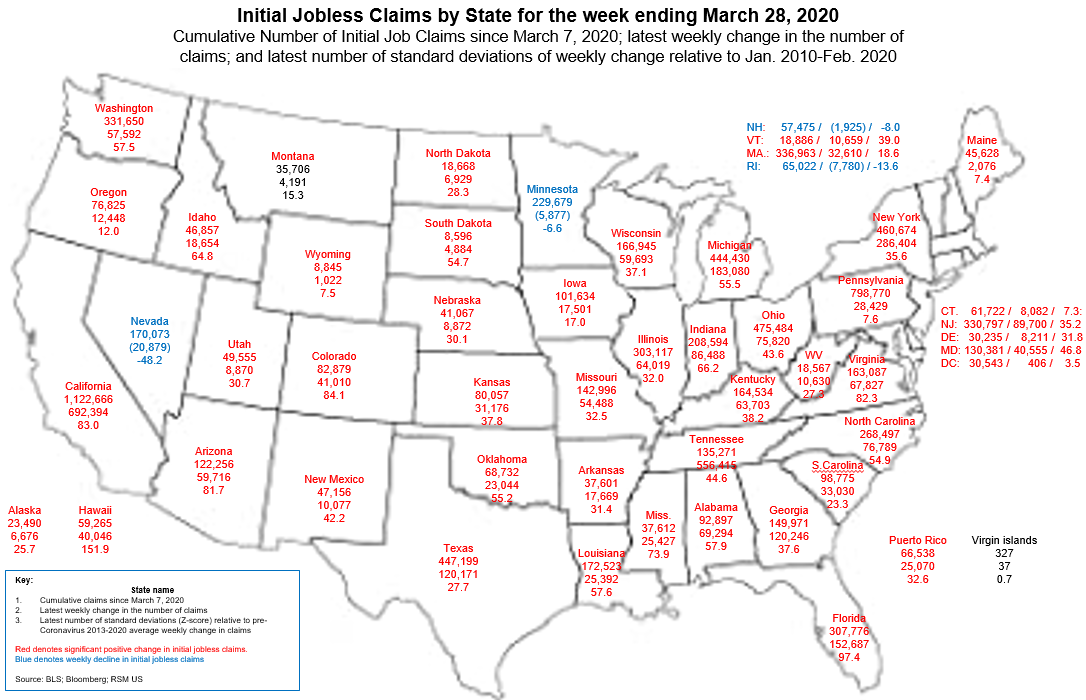

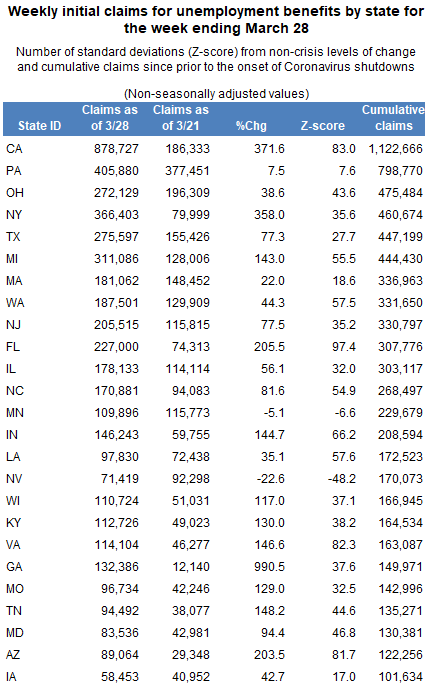

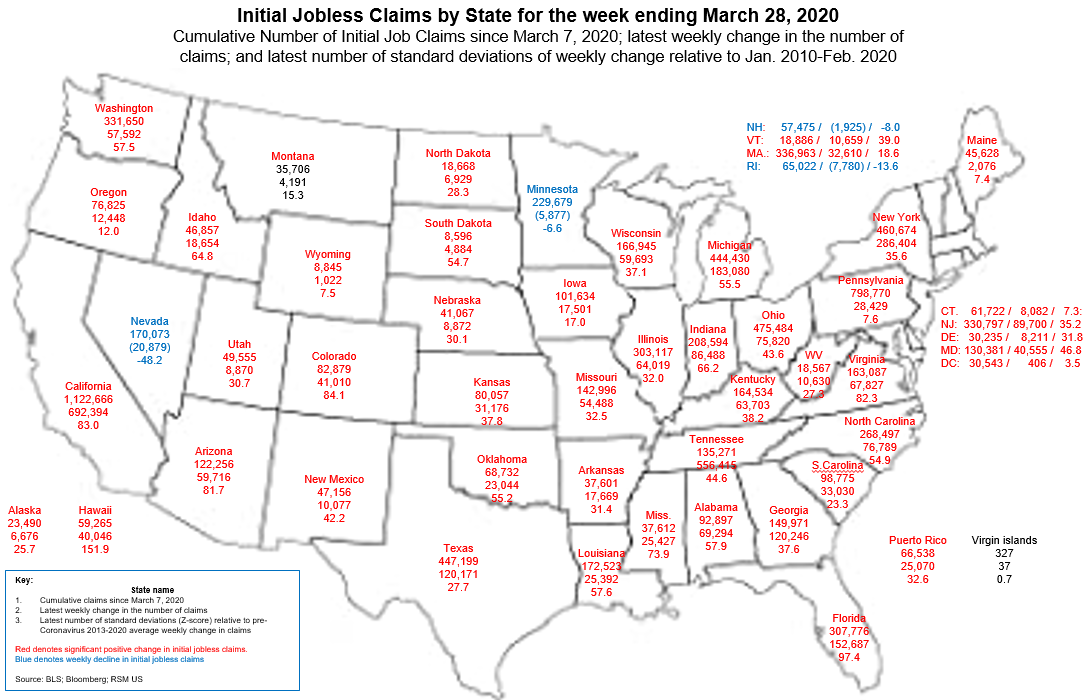

The widespread layoffs of American workers worsened in the third week of the coronavirus shutdown, with all states (with the exception of the Virgin Islands) now having reported a significant increase in initial jobless claims at some point during the three-week period.

This strongly suggests that Congress will have to make state and municipal finance a policy priority to prevent a spillover of the recent carnage in the labor market into the public sector.

Nationally, there were 6.6 million initial jobless claims for the week ending March 28 on a seasonally adjusted basis. That amounts to a nearly 300-standard-deviation shock to the labor force that is likely to have a long-run impact on consumer spending and the economy as a whole.

To identify which states have experienced the largest unemployment increases, WalletHub compared the 50 states and the District of Columbia across two key metrics. These metrics compare initial unemployment claim increases for the week of March 23, 2020 to both the same week in 2019 and the first week of 2020. Below, you can see highlights from the report, along with a WalletHub Q&A.

Nevada, Minnesota, New Hampshire and Rhode Island reported fewer claims in the latest week of reporting (March 28) than in the first week of widespread layoffs, but that’s not to say things are getting better.

For example, Nevada reported 71,000 initial claims in the week ending March 28, versus 92,000 in the week ending March 21. By comparison, the average number of claims in Nevada was 2,900 per week in the pre-crisis period.

And Minnesota reported 110,000 initial claims in the week ending March 28, versus 116,000 in the week ending March 21. By comparison, the average number of claims in Minnesota was 4,300 per week in the pre-crisis period.

Also discouraging is that 6,000 of those claims involved plant closings during the month of March, as reported by Minnesota Department of Employment and Economic Development, which suggests that the impact of the virus is moving beyond the service sector.

The map below shows three numbers below the state name:

The cumulative number of initial unemployment claims since March 7, the before the effect of shutdowns began in earnest.

The latest increase (decrease) in the number of claims.

The Z-score of the latest increase (decrease) in claims, which is the number of standard deviations above (below) the pre-coronavirus average.

The first number indicates the depth of the impact of the virus on the labor force.

The second number indicates the direction of the claims (i.e., a first derivative of sorts): Positive numbers indicate an increase in claims and labor market distress; positive numbers approaching zero indicate the deceleration in new filings; zero would suggest a plateauing of claims; while negative numbers are an indication that businesses and employees are returning to normal.

The third number shows the unprecedented degree of the shock, with Z-scores outside the range of plus-or-minus two standard deviations considered to be outside of normal occurrences.

WHO Targeted In Major COVID-19 Data-Hacking Campaign Believed Tied To Iran

A new report by Reuters alleges a major attempted hack of the World Health Organization (WHO) during the worldwide coronavirus pandemic linked to Iranian state entities.

WHO officials described“a sustained digital bombardment” by hackers described as seeking internal information on the deadly coronavirus, further said to be “more than doubled” compared to prior hacking attempts of the United Nations health agency.

Iran has vehemently denied that it or any of its intelligence arms were behind the computer network attacks, with the Islamic Republic’s information technology ministry dismissing the reports as “sheer lies to put more pressure on Iran.” Instead, the ministry said, “Iran has been a victim of hacking.”

Image source: Cybercrime Magazine

Iran’s leaders have of late lashed out at the US and Western humanitarian organizations for sanctions, which have exacerbated the intensity of the deadly outbreak inside Iran.

Reuters cited an unnamed source only described as working for a large technology company which monitors global cyber-threats as alleging, “We’ve seen some targeting by what looks like Iranian government-backed attackers targeting international health organizations generally via phishing.”

The latest effort has been ongoing since March 2 and attempted to steal passwords from WHO staff by sending malicious messages designed to mimic Google web services to their personal email accounts, a common hacking technique known as “phishing,” according to four people briefed on the attacks. Reuters confirmed their findings by reviewing a string of malicious websites and other forensic data.

Western intelligence sources interviewed further pointed to an Iranian pattern of intensifying cyber-attacks against European and American institutions and targets during times of major international crisis.

Over the past year there’ve been multiple instances of hackers infiltrating US federal websites and displaying pro-Iranian messages on them, especially becoming more intense following the Jan.3 assassination of the IRGC’s Gen. Soleimani.

Reuters referenced the pattern as follows: “Other details in this phishing attempt point to links with Tehran. For example, Reuters found that the same malicious websites used in the WHO break-in attempts were deployed around the same time to target American academics with ties to Iran,” according to the report.

“The related activity – which saw the hackers impersonate a well-known researcher – parallels cases Reuters previously documented where alleged Iranian hackers masqueraded as media figures from organizations such as CNN or The New York Times to trick their targets,” it said.

Upon information and belief, Iran or its proxies are planning a sneak attack on U.S. troops and/or assets in Iraq. If this happens, Iran will pay a very heavy price, indeed!

Since last summer when tensions began soaring between Tehran and Washington, eventually nearly leading to war and tit-for-tat military strikes in January of this year, cyber operations between the US and Iran have reportedly ramped up dramatically, with both sides considering the covert digital intrusions of each others’ classified data an ‘act of war’.

This week the White House has put US forces in the Middle East on a state of alert, with Trump on Wednesday alleging that Iranian proxies in Iraq are preparing a major attack on American bases there.

As much as Covid-19 is a circuit breaker, a time bomb and an actual weapon of mass destruction (WMD), a fierce debate is raging worldwide on the wisdom of mass quarantine applied to entire cities, states and nations.

Those against it argue Planet Lockdown not only is not stopping the spread of Covid-19 but also has landed the global economy into a cryogenic state – with unforeseen, dire consequences. Thus quarantine should apply essentially to the population with the greatest risk of death: the elderly.

With Planet Lockdown transfixed by heart-breaking reports from the Covid-19 frontline, there’s no question this is an incendiary assertion.

In parallel, a total corporate media takeover is implying that if the numbers do not substantially go down, Planet Lockdown – an euphemism for house arrest – remains, indefinitely.

Michael Levitt, 2013 Nobel Prize in chemistry and Stanford biophysicist, was spot on when he calculated that China would get through the worst of Covid-19 way before throngs of health experts believed, and that “What we need is to control the panic”.

Let’s cross this over with some facts and dissident opinion, in the interest of fostering an informed debate.

The report Covid-19 – Navigating the Uncharted was co-authored by Dr. Anthony Fauci – the White House face of the fight –, H. Clifford Lane, and CDC director Robert R. Redfield. So it comes from the heart of the U.S. healthcare establishment.

The report explicitly states, “the overall clinical consequences of Covid-19 may ultimately be more akin to those of a severe seasonal influenza (which has a case fatality rate of approximately 0.1%) or a pandemic influenza (similar to those in 1957 and 1968) rather than a disease similar to SARS or MERS, which have had case fatality rates of 9 to 10% and 36%, respectively.”

On March 19, four days before Downing Street ordered the British lockdown, Covid-19 was downgraded from the status of “High Consequence Infectious Disease.”

John Lee, recently retired professor of pathology and former NHS consultant pathologist, has recently argued that, “the world’s 18,944 coronavirus deaths represent 0.14 per cent of the total. These figures might shoot up but they are, right now, lower than other infectious diseases that we live with (such as flu).”

He recommends, “a degree of social distancing should be maintained for a while, especially for the elderly and the immune-suppressed. But when drastic measures are introduced, they should be based on clear evidence. In the case of Covid-19, the evidence is not clear.”

No less than 22 scientists – see here and here – have expanded on their doubts about the Western strategy.

Dr. Sucharit Bhakdi, Professor Emeritus of Medical Microbiology at the Johannes Gutenberg University in Mainz, has provoked immense controversy with his open letter to Chancellor Merkel, stressing the “truly unforeseeable consequences of the drastic containment measures which are currently being applied in large parts of Europe.”

Even New York governor Andrew Cuomo admitted on the record about the error of quarantining elderly people with illnesses alongside the fit young population.

The absolutely key issue is how the West was caught completely unprepared for the spread of Covid-19 – even after being provided a head start of two months by China, and having the time to study different successful strategies applied across Asia.

There are no secrets for the success of the South Korean model.

South Korea was producing test kits already in early January, and by March was testing 100,000 people a day, after establishing strict control of the whole population – to Western cries of “no protection of private life”. That was before the West embarked on Planet Lockdown mode.

South Korea was all about testing early, often and safely – in tandem with quick, thorough contact tracing, isolation and surveillance.

Covid-19 carriers are monitored with the help of video-surveillance cameras, credit card purchases, smartphone records. Add to it SMS sent to everyone when a new case is detected near them or their place of work. Those in self-isolation need an app to be constantly monitored; non-compliance means a fine to the equivalent of $2,800.

Controlled demolition in effect

In early March, the Chinese Journal of Infectious Diseases, hosted by the Shanghai Medical Association, pre-published an Expert Consensus on Comprehensive Treatment of Coronavirus in Shanghai. Treatment recommendations included, “large doses of vitamin C…injected intravenously at a dose of 100 to 200 mg / kg per day. The duration of continuous use is to significantly improve the oxygenation index.”

That’s the reason why 50 tons of Vitamin C was shipped to Hubei province in early February. It’s a stark example of a simple “mitigation” solution capable of minimizing economic catastrophe.

In contrast, it’s as if the brutally fast Chinese “people’s war” counterpunch against Covid-19 had caught Washington totally unprepared. Steady intel rumbles on the Chinese net point to Beijing having already studied all plausible leads towards the origin of the Sars-Cov-2 virus – vital information that will be certainly weaponized, Sun Tzu style, at the right time.

As it stands, the sustainability of the complex Eurasian integration project has not been substantially compromised. As the EU has provided the whole planet with a graphic demonstration of its cluelessness and helplessness, everyday the Russia-China strategic partnership gets stronger – increasingly investing in soft power and advancing a pan-Eurasia dialogue which includes, crucially, medical help.

Facing this process, the EU’s top diplomat, Joseph Borrell, sounds indeed so helpless:

“There is a global battle of narratives going on in which timing is a crucial factor. […] China has brought down local new infections to single figures – and it is now sending equipment and doctors to Europe, as others do as well. China is aggressively pushing the message that, unlike the U.S., it is a responsible and reliable partner. In the battle of narratives we have also seen attempts to discredit the EU (…) We must be aware there is a geo-political component including a struggle for influence through spinning and the ‘politics of generosity’. Armed with facts, we need to defend Europe against its detractors.”

That takes us to really explosive territory. A critique of the Planet Lockdown strategy inevitably raises serious questions pointing to a controlled demolition of the global economy. What is already in stark effect are myriad declinations of martial law, severe social media policing in Ministry of Truth mode, and the return of strict border controls.

These are unequivocal markings of a massive social re-engineering project, complete with inbuilt full monitoring, population control and social distancing promoted as the new normal.

That would be taking to the limit Secretary of State Mike “we lie, we cheat, we steal” Pompeo’s assertion, on the record, that Covid-19 is a live military exercise: “This matter is going forward — we are in a live exercise here to get this right.”

All hail BlackRock

So as we face a New Great Depression, steps leading to a Brave New World are already discernable. It goes way beyond a mere Bretton Woods 2.0, in the manner that Pam and Russ Martens superbly deconstruct the recent $2 trillion, Capitol Hill-approved stimulus to the U.S. economy.

Essentially, the Fed will “leverage the bill’s $454 million bailout slush fund into $4.5 trillion”. And no questions are allowed on who gets the money, because the bill simply cancels the Freedom of Information Act (FOIA) for the Fed.

The privileged private contractor for the slush fund is none other than BlackRock. Here’s the extremely short version of the whole, astonishing scheme, masterfully detailed here.

Wall Street has turned the Fed into a hedge fund. The Fed is going to own at least two thirds of all U.S. Treasury bills wallowing in the market before the end of the year.

The U.S. Treasury will be buying every security and loan in sight while the Fed will be the banker – financing the whole scheme.

So essentially this is a Fed/ Treasury merger. A behemoth dispensing loads of helicopter money – with BlackRock as the undisputable winner.

BlackRock is widely known as the biggest money manager on the planet. Their tentacles are everywhere. They own 5% of Apple, 5% of Exxon Mobil, 6% of Google, second largest shareholder of AT&T (Turner, HBO, CNN, Warner Brothers) – these are just a few examples.

They will buy all these securities and manage those dodgy special Purpose Vehicles (SPVs) on behalf of the Treasury.

BlackRock not only is the top investor in Goldman Sachs. Better yet: Blackrock is bigger than Goldman Sachs, JP Morgan and Deutsche Bank combined. BlackRock is a serious Trump donor. Now, for all practical purposes, it will be the operating system – the Chrome, Firefox, Safari – of Fed/Treasury.

This represents the definitive Wall Street-ization of the Fed – with no evidence whatsoever it will lead to any improvement in the lives of the average American.

Western corporate media, en masse, have virtually ignored the myriad, devastating economic consequences of Planet Lockdown. Wall to wall coverage barely mentions the astonishing economic human wreckage already in effect – especially for the masses barely surviving, so far, in the informal economy.

For all practical purposes, the Global War on Terror (GWOT) has been replaced by the Global War on Virus (GWOV). But what is not being seriously analyzed is the Perfect Toxic Storm: a totally shattered economy; The Mother of All Financial Crashes – barely masked by the trillions in helicopter money from the Fed and the ECB; the tens of millions of unemployed engendered by the New Great Depression; the millions of small businesses that will simply disappear; a widespread, global mental health crisis. Not to mention the masses of elderly, especially in the U.S., that will be issued an unspoken “drop dead” notice.

Beyond any rhetoric about “decoupling”, the global economy is already, de facto, split in two. On one side, we have Eurasia, Africa and swathes of Latin America – what China will be painstakingly connecting and reconnecting via the New Silk Roads. On the other side, we have North America and selected Western vassals. A puzzled Europe lies in the middle.

A cryogenically induced global economy certainly facilitates a reboot. Trumpism is the New Exceptionalism – so that means an isolationist MAGA on steroids. In contrast, China will painstakingly reboot its market base along the New Silk Roads – Africa and Latin America included – to replace the 20% of trade/exports to be lost with the U.S.

The meager $1,200 checks promised to Americans are a de facto precursor of the much touted Universal Basic Income (UBI). They may become permanent as tens of millions of people will be permanently unemployed. That will facilitate the transition towards a totally automated, 24/7 economy run by AI – thus the importance of 5G.

And that’s where ID2020 comes in.

AI and ID2020

The European Commission is involved in a crucial but virtually unknown project, CREMA (Cloud Based Rapid Elastic Manufacturing) which aims to facilitate the widest possible implementation of AI in conjunction to the advent of a cashless One-World system.

The end of cash necessarily implies a One-World government capable of dispensing – and controlling – UBI; a de facto full accomplishment of Foucault’s studies on biopolitics. Anyone is liable to be erased from the system if an algorithm equals this individual with dissent.

It gets even sexier when absolute social control is promoted as an innocent vaccine.

ID2020 is self-described as a benign alliance of “public-private partners”. Essentially, it is an electronic ID platform based on generalized vaccination. And its starts at birth; newborns will be provided with a “portable and persistent biometrically-linked digital identity.”

GAVI, the Global Alliance for Vaccines and Immunization, pledges to “protect people’s health “ and provide “immunization for all”. Top partners and sponsors, apart from the WHO, include, predictably, Big Pharma.

At the ID2020 Alliance summit last September in New York, it was decided that the “Rising to the Good ID Challenge” program would be launched in 2020. That was confirmed by the World Economic Forum (WEF) this past January in Davos. The digital identity will be tested with the government of Bangladesh.

That poses a serious question: was ID2020 timed to coincide with what a crucial sponsor, the WHO, qualified as a pandemic? Or was a pandemic absolutely crucial to justify the launch of ID2020?

As game-changing trial runs go, nothing of course beats Event 201, which took place less than a month after ID2020.

The Johns Hopkins Center for Health Security in partnership with, once again, the WEF, as well as the Bill and Melinda Gates Foundation, described Event 201 as “a high-level pandemic exercise”. The exercise “illustrated areas where public/private partnerships will be necessary during the response to a severe pandemic in order to diminish large-scale economic and societal consequences.”

With Covid-19 in effect as a pandemic, the Johns Hopkins Bloomberg School of Public Health was forced to issue a statement basically saying they just “modeled a fictional coronavirus pandemic, but we explicitly stated that it was not a prediction”.

There’s no question “a severe pandemic, which becomes ‘Event 201’ would require reliable cooperation among several industries, national governments, and key international institutions”, as spun by the sponsors. Covid-19 is eliciting exactly this kind of “cooperation”. Whether it’s “reliable” is open to endless debate.

The fact is that, all over Planet Lockdown, a groundswell of public opinion is leaning towards defining the current state of affairs as a global psyop: a deliberate global meltdown – the New Great Depression – imposed on unsuspecting citizens by design.

The powers that be, taking their cue from the tried and tested, decades-old CIA playbook, of course are breathlessly calling it a “conspiracy theory”. Yet what vast swathes of global public opinion observe is a – dangerous – virus being used as cover for the advent of a new, digital financial system, complete with a forced vaccine cum nanochip creating a full, individual, digital identity.

The most plausible scenario for our immediate future reads like clusters of smart cities linked by AI, with people monitored full time and duly micro-chipped doing what they need with a unified digital currency, in an atmosphere of Bentham’s and Foucault’s Panopticum on overdrive.

So if this is really our future, the existing world-system has to go. This is a test, this is only a test.

New York’s Unemployment Fund Will Be Insolvent In 2 Months

With 92,381 total cases, surging by 8,669 in one day, and resulting in 2,373 deaths, New York has emerged the epicenter of the coronavirus pandemic.

Just as concerning, is that it is also among the states least prepared to deal with the record surge of unemployment claims by workers in restaurants, retail shops and hotels closed to slow the outbreak.

New York’s unemployment insurance trust had about $2.7 billion at the end of 2019, less than half the minimum needed to remain solvent during a recession, according to the U.S. Department of Labor. Alas, it is now facing a depression and with claims skyrocketing, the state has enough money to cover the checks for only 10 weeks, according to an estimate by the Tax Foundation, a Washington-based think tank.

“New York’s unemployment compensation trust fund is basically insolvent,” wrote Jared Walczak, director of state tax policy at the Tax Foundation as quoted by Bloomberg. “Funds will be exhausted even more quickly should unemployment compensation claims continue to rise.”

Almost 10 million American applied for unemployment benefits in the last two weeks, highlighting the devastating economic impact of the coronavirus as shutdowns widened across the country. About 450,000 of them were New Yorkers, according to the state’s Department of Labor. Only California, Pennsylvania and Ohio saw more claims.

During the Great Recession, the majority of states exhausted their unemployment insurance reserves and either borrowed from the U.S. Treasury or issued bonds to rebuild their trusts, according to Kroll Bond Rating Agency.

States that have rebuilt reserves such as Georgia and North Carolina will have less pressure to raise unemployment taxes, Kroll wrote in a report Wednesday. New York, unfortunately, is not among them.

New York’s trust fund had a solvency level of 0.36 as of Dec. 31, where a level of 1.0 means the state could pay out claims for a year at the average level of the worst three years of the past twenty, according to the U.S. Labor Department. California, Texas, New York, Illinois, Ohio and Pennsylvania are among the 22 states and jurisdictions that do not meet the recommended standard of solvency. Only California’s unemployment trust fund is in worse shape than New York’s, according to the department: almost as if the most liberal states also happen to be most insolvent.

It gets worse: there are now nearly twice as many people claiming or already receiving unemployment benefits as there were over the comparison period, meaning that with current claims, states would run out twice as fast, the Tax Foundation’s Walczak wrote.

The economic stimulus signed by President Donald Trump provides additional federally-funded benefits to unemployed workers, and expands eligibility to previously uncovered workers, but states are still on the hook for regular benefits.

“The state will have to borrow from the federal government, and will ultimately have to pay back those loans with interest, while New York employers will eventually face higher federal unemployment insurance taxes to compensate the federal government for extending loans to the state,” Walczak wrote, who clearly is unaware that under helicopter money nobody will repay anything, ever again, and instead the perpetual Minsky moment will be stretch forever, defying every law of finance, and physics, just because the Fed will monetize it all, and everyone will live happily ever after.

{kind=link}