WTI Tumbles To $19 Handle After Biggest Crude Build Since 2016

After its worst quarter ever, as COVID-19 lockdowns crushed demand, raising fears about overflowing storage tanks amid a price war that has flooded the market with extra supply, all eyes are glued to today’s official inventory data (after API reported a major surprise build in crude and gasoline stocks) as Standard Chartered analysts, including Emily Ashford warned in a report, oil tanks around the world could fill in six weeks, a move that will likely force significant production shut-downs,

“Huge inventory builds, potentially exhausting spare storage capacity, will mean that market balance requires an unprecedented output shutdown by producers,” they wrote.

So, eyes down…

“There is the very real possibility that this week’s storage reports could be the energy patch version of last Thursday’s Weekly Jobless Claims,” Robert Yawger, Mizuho Securities USA’s director of energy said in a note.

“I would expect the numbers to be supersized and challenge multi-year highs/lows on multiple data points. Of course, I have been expecting big numbers for the past couple week, but the fireworks have not happened. That leads me to believe that the data explosion will likely happen this week … Exports will likely be down big, and refinery utilization will likely pull back dramatically. That will leave a lot of crude oil on the sidelines … EIA crude oil storage has been higher for nine weeks in a row. Storage will likely double up and increase at the rate of around 10 million for another nine weeks…at least.”

API

Crude +10.485mm (+4.6mm exp) – biggest build since Feb 2017

Cushing +2.926mm – biggest build since Feb 2019

Gasoline +6.058mm (+3.6mm exp) – biggest build since Jan 2020

Distillates -4.458mm (-600k exp)

DOE

Crude +13.833mm (+4.6mm exp) – biggest since Oct 2016

Cushing +3.521mm – biggest build since Mar 2018

Gasoline +7.524mm (+3.6mm exp) – biggest build since Jan 2020

Distillates -2.194mm (-600k exp)

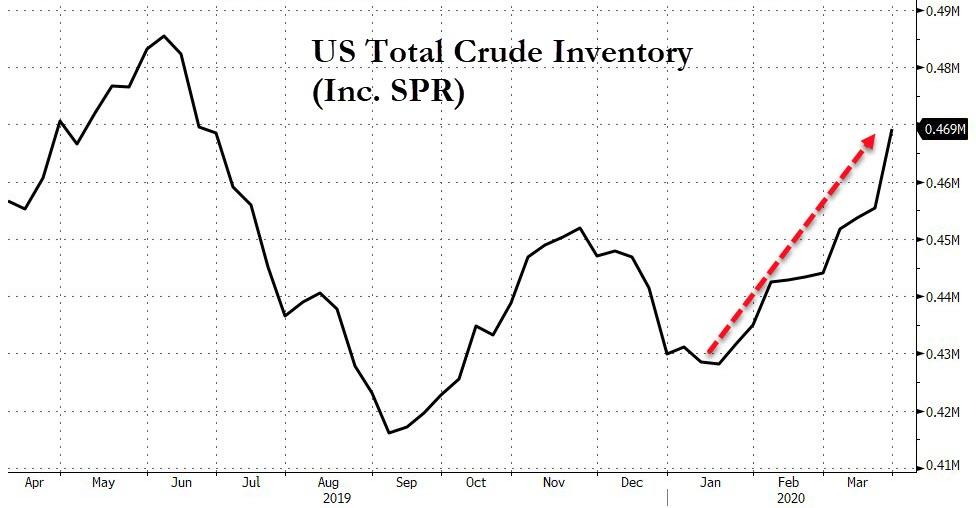

API reported a massive crude build (and gasoline build) overnight but the official data showed an even bigger 13.8mm barrel crude build – the biggest since Oct 2016 and a huge increase in stocks at Cushing…

Source: Bloomberg

Total US crude inventories are now at their highest since June 2019…

Source: Bloomberg

U.S. oil production has remained at a strong 13-13.1 million barrels a day in recent weeks, despite a big drop in the rig count last week (which could presage a shift)…

Source: Bloomberg

Bloomberg notes that it’s important to remember that while prices are low, we haven’t seen the sort of uniform production cut that many are expecting. There are a few reasons.

For one, many of these firms are hedged, so even with WTI trending at $20, that’s not necessarily the price a shale firm receives (there’s nuance here, but that’s another issue). Also, many of these firms may be just completing their wells instead of drilling new ones, which means production continues to rise. The trickle down effect of the rout isn’t quite here yet, but hold on – it might be here soon, particularly if oil remains at these levels.

WTI hovered around $20.20 ahead of the official inventory print and tumbled to a $19 handle after the big build…

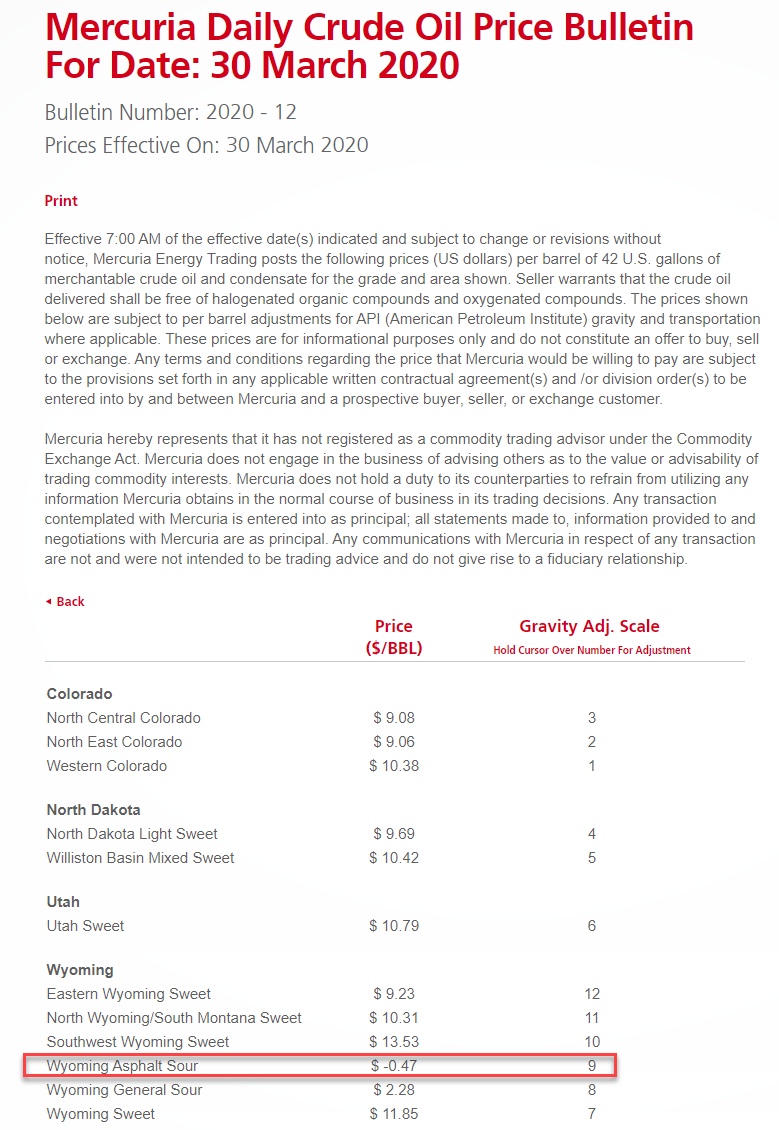

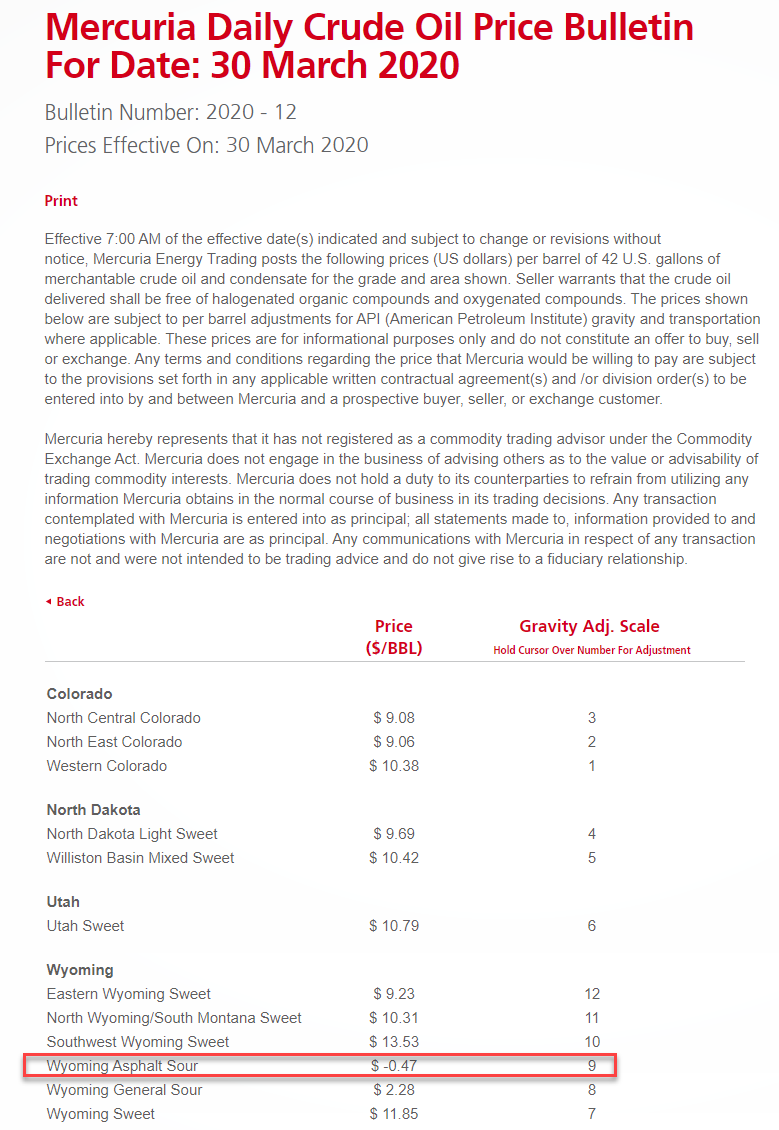

How low can prices go? Well, as we detailed last night,the first crude stream to price below zero was Wyoming Asphalt Sour, a dense oil used mostly to produce paving bitumen. Energy trading giant Mercuria bid negative 19 cents per barrel in mid-March for the crude, effectively asking producers to pay for the luxury of getting rid of their output.

Echoing Goldman, Elisabeth Murphy, an analyst at consultant ESAI Energy said that “these are landlocked crude with just no buyers. In areas where storage is filling up quickly, prices could go negative. Shut-ins are likely to happen by then.”

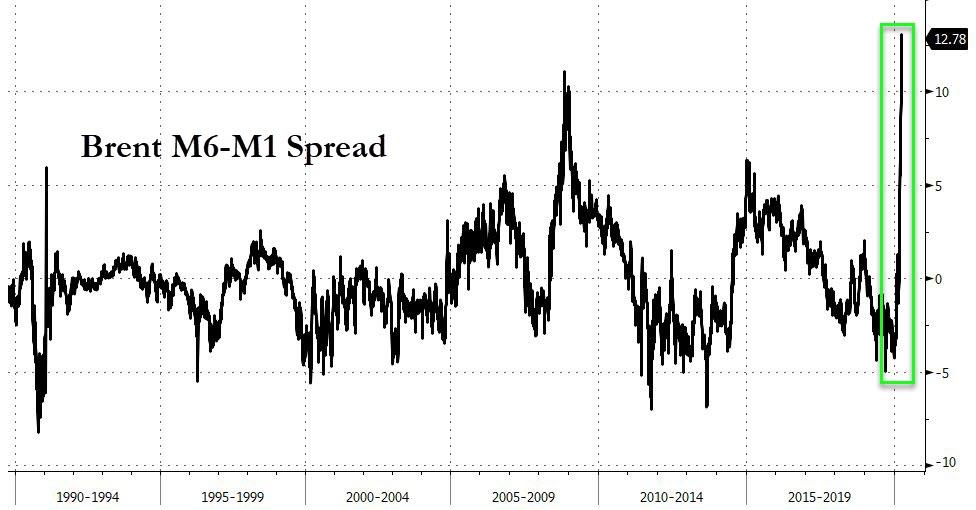

Finally, we note that Brent futures are signaling a historic glut is emerging.

The May contract traded at a discount of $13.66 a barrel to November, a more bearish super-contango than the market saw even in the depths of the 2008-09 global financial crisis.

The Fed Blows Biggest Bond Bubble Ever: March IG Bond Issuance Hits $271BN, An Absolute Record

When the Fed broke the last frontier of moral hazard – at least until it starts openly purchasing ETFs and single stocks after the next market crash, thereby fully nationalizing the market – and announced it, or rather Blackrock, would not only expand its QE to “unlimited” but also buy investment grade bonds and the IG ETF, LQD, it effectively tore the bond market into two categories: that backstopped by the Fed, and that which isn’t (something we described in “Bond Market Tears In Two: Distressed Debt Is Cratering, As Fed Buying Of Investment Grade Sends LQD NAV Soaring“).

It also unleashed the biggest debt bubble of all time.

Why? Because by explicitly guaranteeing investment grade debt, the Fed – by making BBB and higher rated debt effectively risk-free – not only precipitated the biggest one-day surge and inflow into LQD, but unleashed an unprecedented free for all as every single investment grade company – especially those soon to be fallen angels who will be downgraded to junk – have rushed into the bond market to issue debt and raise cash while they can at artificially low yields.

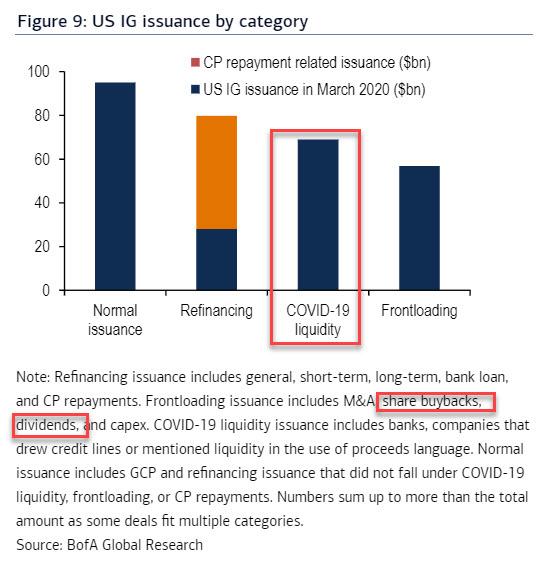

And the data confirms it: according to BofA, after the IG market was largely shut down in the two weeks ahead of the Fed’s March 23 bond buying announcement, US new issuance reached a new monthly record of $260.7 billion in March 2020, bringing YtD to $509.7 billion – the fastest ever start to a year and 47% ahead of 2019’s pace.

Looking at the use of proceeds, BofA observes that refinancings continued at a strong $79.8bn, but as the commercial paper market froze $51.8bn was specifically earmarked for terming that out. In addition, there was roughly $69bn of COVID-19 liquidity-related issuance from banks and companies that drew credit lines or mentioned liquidity in the use of proceeds language. What is more remarkable is that is that another $57bn was for frontloaded issuance for capex, M&A as well as – drumroll – share buybacks and dividends.

Yes, even at this moment, having seen the Boeing blowback which repurchased over $50BN in stock pushing its debt load to record highs and now demands a $60BN bailout, companies have the gall to issue debt and buyback stock! Something tells us there will be a lot of angry articles in the NYT singling out each and every one of those companies, especially if they have or plan to fire even one single worker.

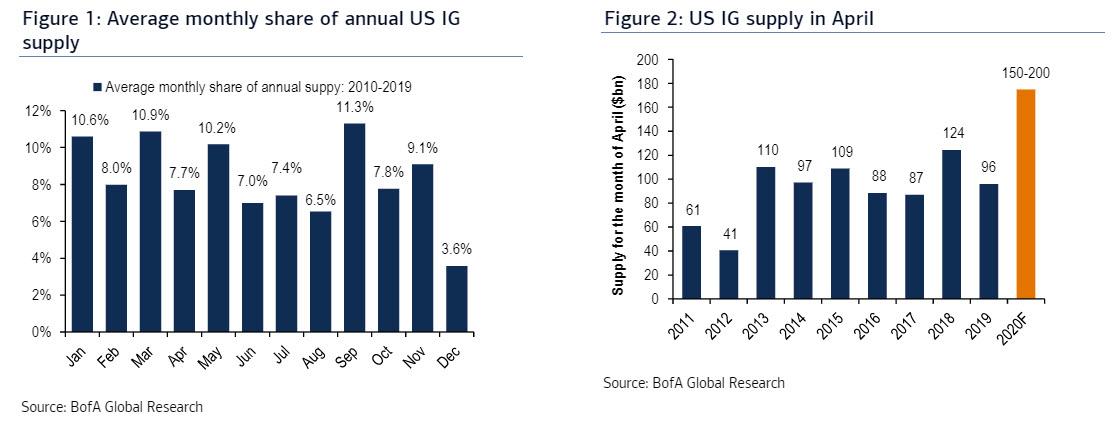

And it’s just starting. Looking ahead, BofA notes that April is seasonally a lighter month than March in primary, accounting for 7.7% of annual issuance on average with a five-year run-rate of $102bn.

However, with the economic shutdown IG companies will continue to issue bonds for liquidity needs while others frontload as the market is wide open. M&A issuance totaled just $2.2bn in March and that may continue in April as global markets remain fragile, and T-Mobile/Sprint using a $23bn bridge loan for the April 1st closing with the IG bond refinancing delayed till when market conditions improve.

On the other hand, 1Q20 earnings-related blackouts will begin in the coming weeks, somewhat limiting the industrial pipeline as far as seasonality goes. As a result, BofA now looks for a wide range of $150-200bn of gross issuance in April. With $36.7bn of maturities in April and another $4.6bn of additional redemptions announced so far for a total of $41.3bn, the implied net issuance in April is $133.7bn.

If correct, total issuance in just the first 4 months of the year could reach a mindblowing $700BN, an unheard of number and one which means the Fed will very soon end up owning equity stakes in hundreds of bankrupt companies once its bonds are equitized as dozens of formerly IG companies are downgraded to junk, and then file for bankruptcy, convering the pre-petition debt into equity.

We, for one, can’t wait to see what the Fed will do when it ends up owning controlling post-petition equity stakes across countless US corporations.

Trader: “Maybe We Can’t Handle The Truth After All”

Authored by Richard Breslow via Bloomberg,

Most of us have lower pain thresholds than we would like to admit. And have developed various coping mechanisms to deal with it. We opt to hear what we want to. This tendency is often accommodated by enablers who long ago realized that catering to this preference can win friends and influence people. It contradicts the dictum of under-promising and over-delivering. But is a sleight of hand that often buys time. It can also occasionally lead to heads-I-win, tails-you-lose outcomes, moments of severe disappointment and hurt people.

Today is one of those days. Maybe we can’t handle the whole, unvarnished truth, but would be better served getting more of it and earlier. I don’t want to suggest things are more nefarious than they might really be. But, consider today’s market price action as an example of this in microcosm. It’s also worth pointing out that, at least some of what is going on, is an unwind of the front-running and rote positioning that came with what was a well-advertised and potentially difficult month-end portfolio rebalancing exercise that we just completed. Possibly more than it seems. It won’t take long to find out.

Risk assets are not having a happy start to the quarter. Not horrendous, but certainly discouraging nevertheless. And there are a number of factors that have conspired to drag us down. We were told, yesterday evening, that we are still in the very dangerous stages of surviving the pandemic. “It will be a very difficult two weeks.” Should that have come as a surprise to anyone watching the news? Apparently so. There’s still light at the end of the tunnel, just not as soon as we were told to hope. And with potentially greater human toll. Sometimes, it is just so much better to get out ahead of things. That’s exactly what NIAID Director Anthony Fauci was trying to do. And then he suggested a believable path toward achieving a better result than the models they use suggest.

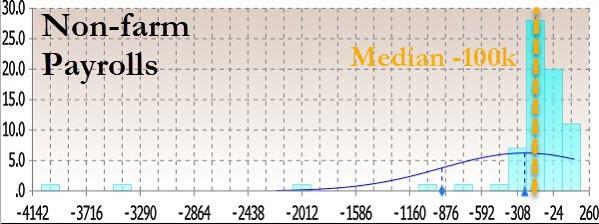

Global economic numbers are going to be disappointing. Today’s certainly were uninspiring. We know we are in recession. Bad data comes with that. The lesson to learn is to follow the trajectory, one way or the other, and not get solely hung up on the absolute levels. We are in danger of slipping from looking beyond the numbers to merely being unnerved by them. Accept that precise estimates are hard to come by and aren’t really the point. Just look at the dispersion of forecasts for Friday’s nonfarm payrolls.

What may have tipped the balance, given our current mood, is the new realization that the V-shaped recovery is unlikely to happen exactly on schedule as we were promised. New realization? It was an unrealistic expectation that shouldn’t have been stated as the base case. Have we not already been discussing a fourth stimulus plan?

European banks are having to cut out dividends and share buybacks. We’ve been discussing the weakness of this sector and other uses for these funds ad nauseam. This can’t have come as a total bolt from the blue. The market’s reaction should be taken as an object lesson in understanding the concept of asking, “whose ox is being gored” more than anything else.

Some fund managers are bearish. Earnings season will be disappointing and revenue expectations too high. Enough said. Although, I did read that cigarette companies seem to be doing just fine.

The point is, we know these are bad times. And sometimes the bad news gangs up on us. That surely can’t come as a surprise, nor should we pretend it does. If that is the case, we aren’t doing enough to overcome the challenges we face.

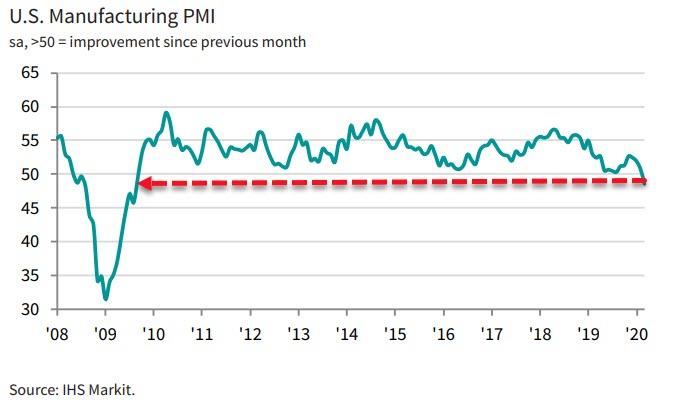

US Manufacturing Slumps To Biggest Contraction Since Financial Crisis

After a bloodbath in European PMIs (and a ‘surprise’ surge back to growth in China), and following some serious collapses in regional Fed surveys (and this morning’s tumble in Canadian PMIs), today’s US manufacturing survey data was expected to slide further into contraction (though not as much as the Services surveys collapsed).

Markit’s US Manufacturing PMI fell modestly from 49.2 to 48.5 in March (modestly better than the 48.0 flash print) – a considerably smaller drop than many expected.

ISM’s US Manufacturing survey fell modestly from 50.1 to 49.1 in March (far better than the 44.5 print expected)

Source: Bloomberg

This move follows the carnage seen in US Services PMI and shows very little relative declines (perhaps the survey was premature)…

Source: Bloomberg

Once again, the driver of this relatively positive print is the same as has caused problems with surveys since the crisis began – supplier delivery times rising at the fastest pace since 2005 – typically seen as a sign of expansion. However, in this case it is caused by collapsing global supply chains, and along with prices paid rising rapidly means a stagflationary collapse in global trade… not exactly the positive signal the index is trying to send.

“The final PMI data for March are even worse than the initial flash estimate, with manufacturing output slumping to the greatest extent since the height of the global financial crisis in 2009.

“Growing numbers of company closures and lockdowns as the nation fights the COVID-19 outbreak mean business levels have collapsed. While some producers reported being busier as a result of stockpiling and anti-virus activities, notably in the food and healthcare sectors, these are very much the minority, and most sectors reported a rapid deterioration in demand and production.

“Orders for capital equipment have deteriorated at a rate not seen since data were first available in 2009 as firms stopped investing in machinery. Companies have meanwhile reined-in spending on inputs and households have pulled back sharply on many forms of spending, especially for non-essential and big ticket items. With export sales also sliding, factories are facing a broad-based slide in demand which is already resulting in the largest job losses recorded since the global financial crisis.”

Finally, manufacturers cut their workforce numbers at the sharpest rate since October 2009, reporting an increase in redundancies and the need for lower operating capacity. Specifically, looking at ISM’s Employment sub-index – at 2009’s lows – suggests Friday’s payrolls data will be extremely ugly (despite ADP’s miraculously timed survey)…

Source: Bloomberg

We give the last word to Williamson: “Worse is likely to come as consumer spending falls further in coming months as lockdowns intensify and unemployment spikes higher.”

After noting for the nth time yesterday that not all currencies are equal, and that the Eurodollar system–that is to say, offshore USD liquidity–remains a structural issue regardless of the recent introduction of (too small) Fed swap lines with (too few) central banks, it’s not surprising that we saw movement on that Front. Indeed, the Fed introduced a new repo facility for any central banks that with an account with the Federal Reserve Bank of New York, who can now swap their holdings of US Treasuries held on account for good ol’ USD cash. The key takeaways from this move are as follow:

The stress on USD liquidity is real and isn’t going away despite the alphabetti spaghetti of Fed channels to try to get USD from A (them) to B (everyone);

It means country C (and let’s just say ‘C’ is particularly apt in this instance) doesn’t have to sell US Treasuries to gain access to USD, alleviating the risks of a move higher in Treasury yields should this need to happen on scale in what are currently far from normal market conditions;

However, it is not actually going to solve any real problems if country C (or D or E) are short of USD, as those USD are still gone once they have been used to pay for imports or settle USD debts; yet

The fact that the universe of foreign central banks being offered this facility is now anyone, not G-10, speaks volumes about the structural issues relating to the global role of the USD; and hence

This is net structurally positive for USD even while it looks negative.

In short, the Fed might, in its navel-gazing kind of way, only care about smooth functioning of the US Treasury market; yet this is still a step towards one of the only logical end-points of having USD as de facto global currency – the Fed as not just US but de facto global central bank. Don’t like that? Well, the other end-points are that the system collapses due to a lack of USD and/or USD being far too high for all involved, which will make what happened in Q1 look like a picnic; or that the system lasts in some places lucky enough for the Fed to look up from its navel at, which will be similar globally if not as bad.

One might not want to recognise any of this from a small, technical change in Fed policy, but it’s not hard to join the dots and project them forward. The only question is how far those dot-plots extend into the future. (As I have said before, if unsustainable systems didn’t ultimately change, we would probably all be Romans.)

On which front, in the US we yesterday had the President once again flipping between his two different characters – Dr.. Donald and Mr. Trump, the former this time urging people and businesses to take the virus seriously and promising a very difficult few weeks ahead as the range of virus deaths has been shunted up to 100,000-240,000.

Yet we also had Mr. Trump tweeting: “With interest rates for the United States being at ZERO, this is the time to do our decades long awaited Infrastructure Bill. It should be VERY BIG & BOLD, Two Trillion Dollars, and be focused solely on jobs and rebuilding the once great infrastructure of our Country! Phase 4”

Yes, it’s election season; and yes, it’s odd that the US last elected a real estate developer who in office has refused to develop any real estate; and it would need to pass Congress. However, when we already had a USD1 trillion deficit; then added USD2.2 trillion in a virus-fighting package; and are planning a UD600bn top up; why not go the whole hog and actually do something stimulatory and much needed like USD2 trillion on infrastructure rather than just trying to lean against the huge negative impact of the virus?

What fiscal deficits! USD5.8 trillion is being bandied around in the way USD580bn was two years ago. And yet, as Trump implies, what fiscal deficits? Rates are zero and are unlikely to be anything other than zero for a looooong time. The Fed will see to that. There is enormous domestic demand for some decent US infrastructure. And there is enormous global USD demand. In short, this is potentially about as clear an argument as one is going to see put forward by a politician for MMT – or here MMT-rump. As another aside, I had many conversations with colleagues when Trump was first elected, and the conclusion was always that if there was ever a US president prepared to use a crisis to go MMT, it was T: nobody even once went ‘Mmm’ about that prospect. Would you want to be a Democratic candidate running against spending USD2 trillion on infrastructure in a weak economy? Good luck with that!

Yes, once again we are dot-plotting here. But when a structural break of this size is presented, one should be paying attention. Particularly as while the rest of the world might be hearing USD2 trillion and licking its lips, I am sure that MMT will be M(MAGA)MT in the US case: buy American, use American, hire American. In which case, the bulk of that liquidity is going to be for domestic not global reflation – or at least that will be the aim.

Of course, if the US does this, expect other countries to go the same route. Today’s Tankan survey was bad but not as bad as had been feared for large firms: perhaps it was covering the period before the Olympics got cancelled – or perhaps PM Abe announcing USD554bn, 10% of GDP, in fiscal stimulus is helping? Of course, for those wanting to follow the US and Japan this will mean either having to run current account surpluses to protect their currencies while doing so, which means more protectionism, or watch their currencies collapse, which likely means more US protectionism and less USD flow: the Fed is going to be oh-so busy in coming years, even if rates are not going to be doing anything at all.

Elsewhere, in China we saw a further attempt to say all is well post-virus with the Caixin PMI suggesting we are now above 50 – when actually the report merely said things had stabilized. In Australia we saw the virus in action today: the mind virus of the housing bubble and its associated “The Block” mentality. Building approvals soared 19.9% m/m in February and CoreLogic house prices went up 0.7% m/m in March, even as everyone is locked down in their homes. Indicative of just how obsessed – and I mean obsessed – Australia is with housing, CoreLogic actually has a day-to-day house price index, so once can track how much “wealthier” one has become each morning. As MMT pointed out decades ago, if businesses won’t invest in capital stock, or the state in new infrastructure, and you still pump in liquidity, you just elevate asset prices. Look how well that has worked out. Fortunately, the latest RBA minutes show that they have finally woken up: a recession is expected; and policy is now to anchor both rates and 3-year yields for as long as needed while waiting for the government to do more on the fiscal front. Might that even include infrastructure at some point?

Ford Is Delaying North American Production “Indefinitely”

With what are sure to be ugly March sales numbers looming, Ford has now decided it is cancelling plans to re-start production in the U.S. and Mexico over the next two weeks.

Citing risks associated with the coronavirus, the automaker has said the the suspension is “indefinite” and has not set a timeline to bring its facilities back online, according to Bloomberg. The company is currently working with the UAW to establish new guidelines for safety procedures before re-opening.

The union announced the death of two Ford plant workers on March 28 as a result of the coronavirus.

UAW President Rory Gamble said on Tuesday: “Today’s decision by Ford is the right decision for our members, their families and our nation. Would I send my family member — my own son or daughter — into that plant and be 100% certain they are safe?”

The shutdowns continue to cost Ford billions of dollars. Despite this, there is no rush to re-open as demand will likely be “depressed for months”. Meanwhile, Ford’s plans to produce ventilators during the week of April 20, in conjunction with GE, remains on schedule.

Kumar Galhotra, Ford’s president of North America said: “The health and safety of our workforce, dealers, customers, partners and communities remains our highest priority.”

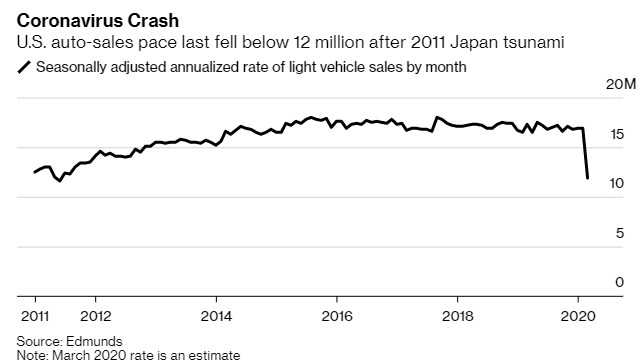

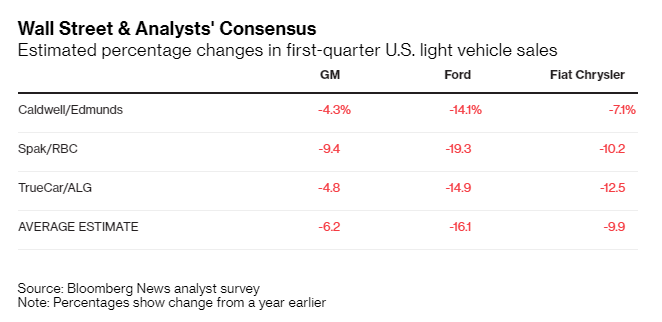

Recall, as we noted yesterday, the entire U.S. auto industry has basically entered full collapse.

The industry was already barely holding on by a thread before the coronavirus pandemic started, with China leading the rest of the globe’s auto industries into recession over the last 18 months. Now, in a post-coronavirus world, automakers in the U.S. are expecting nothing less than full collapse.

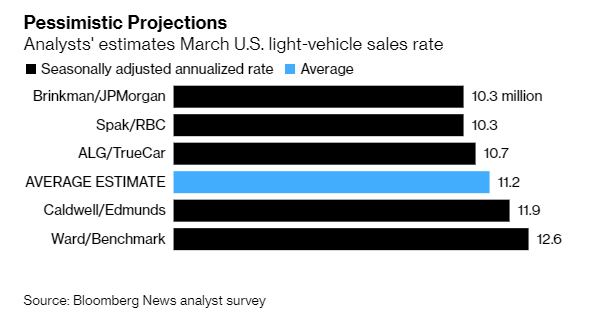

And the things that were barely holding the industry up to start 2020, namely low rates and modest consumer confidence, don’t matter. Businesses are closed, would-be buyers are strapped for cash and the country’s economy has simply been turned off. The industry’s annualized selling rate could slow to 11.9 million in March, according to Edmunds.

Jessica Caldwell, executive director of insights for market researcher Edmunds, told Bloomberg: “The whole world is turned upside down right now.”

Morgan Stanley analyst Adam Jonas put it simply: “There are basically no U.S. auto sales right now. Investors have fully embraced the reality that the U.S. auto industry may be shut down for one or two full months. We’re now being asked to run scenarios of six-month or nine-month shutdowns.”

The President’s extension of his social distancing guidelines to the end of April will also act as a headwind for the industry. Factory shutdowns that started in March will now head toward their second month of no production, as the U.S. consumer, for the most part, remains stuck at home.

Jeff Schuster, senior vice president of forecasting for research LMC Automotive commented: “We just don’t know when and how this ends, and that’s the biggest problem right now. All of this uncertainty creates a lot of angst and that has been spreading really like a wildfire through the industry.”

He predicts that the industry’s annualized selling rate will continue to plummet to between 9 million and 10 million vehicles. Those numbers are well below the 10.4 million autos sold in 2009, the year GM and Chrysler both filed for bankruptcy. J.P. Morgan has an even more pessimistic view, with estimates of a pace of 6 million to 7 million vehicles over the next month.

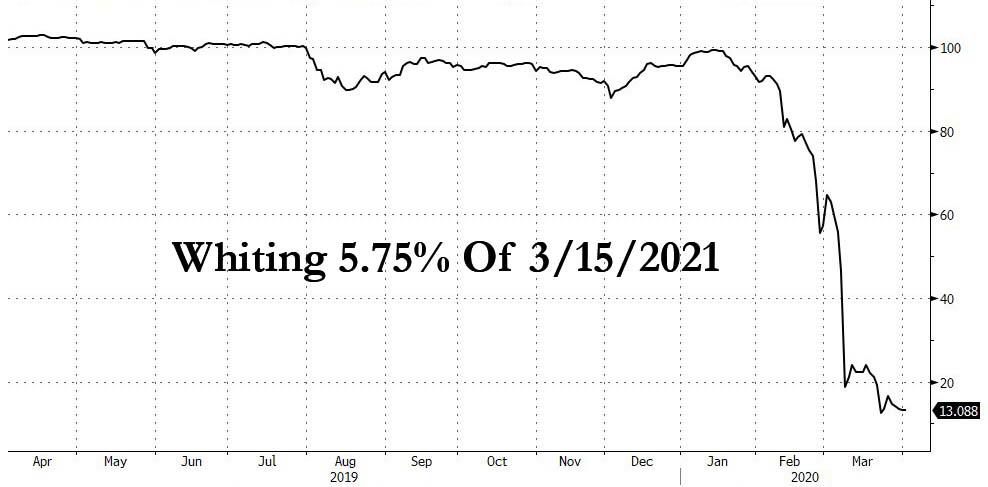

Whiting Petroleum Files For Prepackaged Bankruptcy

Talk about a coincidence: just as we were discussing why April would be “apocalyptic” for the oil industry, as Saudi Arabia just unleashed an unprecedented record amount of oil to buyers in a scramble to put its high-priced competitors out of business, warning that “countless oil producers would file for bankruptcy”, former shale darling Whiting Petroleum did just that, filing a pre-packaged Chapter 11 deal in the Southern District of Texas Bankruptcy Court after reaching an agreement with certain note holders to pursue a “comprehensive” and “consensual” financial restructuring.

Whiting, which in Q4 pumped 123,000 bpd of which 80,000 bpd was nat gas, said it concluded that given a “severe downturn” in oil and gas prices resulting from the Saudi Arabia-Russia oil price war and COVID-19-related impact on demand a financial restructuring was the “best path forward.” Creditors may disagree: the company’s bonds due March 2021 were trading at par as recently as mid-January, even though we warned as far back as 2015 that it would be the first company to go under: truly a testament to how idiotic the junk bond market has been for the past 4 years.

The company said that the plan provides for de-leveraging of capital structure by more than $2.2 billion, and listed $1-$10 billion in debt and more than $585 million of cash on its balance sheet, noting that it expects to have sufficient liquidity to meet its financial obligations during the restructuring without the need for additional financing.

More importantly, it will continue to operate its business and pump oil for the duration of the Chapter 11 proceedings, meaning that oil production won’t decline by even one drop.

Commences Chapter 11 Reorganizational Process to Right-Size Capital Structure

DENVER–(BUSINESS WIRE)–Apr. 1, 2020– Whiting Petroleum Corporation (NYSE: WLL) and certain subsidiaries (collectively, “Whiting” or the “Company”) today announced that they had commenced voluntary Chapter 11 cases under the United States Bankruptcy Code in the U.S. Bankruptcy Court for the Southern District of Texas (the “Bankruptcy Court”). The Company has more than $585 million of cash on its balance sheet and will continue to operate its business in the normal course without material disruption to its vendors, partners or employees. Whiting currently expects to have sufficient liquidity to meet its financial obligations during the restructuring without the need for additional financing.

The Company has also reached an agreement in principle with certain holders (the “Supporting Noteholders”) of its 1.25% convertible senior notes due 2020, 5.750% senior notes due 2021, 6.250% senior notes due 2023, and 6.625% senior notes due 2026 (collectively, the “Notes”) regarding a term sheet (the “Term Sheet”) that contemplates a comprehensive restructuring. The proposed financial restructuring, the terms of which will be set forth in a forthcoming restructuring support agreement between the Company and the Supporting Noteholders, would significantly reduce the Company’s debt and establish a more sustainable capital structure pursuant to a consensual chapter 11 plan of reorganization (the “Plan”) that would be supported by the Supporting Noteholders on the terms of such restructuring support agreement.

The Plan will provide for, among other things: (1) significant de-leveraging of the Company’s capital structure by over $2.2 billion through the exchange of all of the Notes for 97% of the new equity of the reorganized Company to be issued pursuant to the Plan; (2) payment in full in cash and/or refinancing of the Company’s revolving credit facility; (3) the payment in full in cash of all other secured creditors, tax and other priority claimants, and employees; and (4) the Company’s existing equity holders receiving 3% of the new equity of the reorganized Company and warrants (as described in the Term Sheet). Consummation of the Plan will be subject to confirmation by the Bankruptcy Court in addition to other conditions to be set forth in the Plan and related transaction documents.

Bradley J. Holly, the Company’s Chairman, President and CEO, commented, “In 2019, we took proactive steps to reduce our cost structure and improve our cash flow profile. We continue to build on these actions in 2020. The Company has also explored a wide variety of alternatives to address our balance sheet and looming note maturities in a highly capital constrained market environment.

Given the severe downturn in oil and gas prices driven by uncertainty around the duration of the Saudi / Russia oil price war and the COVID-19 pandemic, the Company’s Board of Directors came to the conclusion that the principal terms of the financial restructuring negotiated with our creditors provides the best path forward for the Company. We are pleased to have secured a highly constructive restructuring framework with a critical mass of our noteholders. Through the terms of the proposed restructuring, we believe a right-sized balance sheet will enable us to capitalize on our enhanced cost structure, high-quality asset base and successfully compete in the current environment.”

Mr. Holly continued, “I want to express my gratitude to the employees for their continued dedication and hard work, and to our service providers and business partners for their ongoing support during this time. Following the restructuring process, we look forward to having substantially less debt and a significantly improved outlook for our Company and its stakeholders.”

Moelis & Company is acting as financial advisor for the Company, Kirkland & Ellis is acting as legal advisor, Alvarez & Marsal is acting as restructuring advisor and Jeffrey S. Stein of Stein Advisors LLC is the Company’s Chief Restructuring Officer.

PJT Partners is acting as financial advisor for the Consenting Noteholders and Paul, Weiss, Rifkind, Wharton & Garrison LLP is acting as legal advisor.

End result: Whiting will emerge from bankruptcy in a few weeks, leaner and meaner, with almost no debt, yet pumping as much oil as before.

For those confused, this is confirmation that companies can and will continue to operate even under bankruptcy, something which the airline and cruise industry may want to realize, or perhaps the Trump admin, because if any company is to be bailed out, the existing equity has to be wiped out, period end of story.

“It’s Hard To Envision That”: Biden Doubts Democratic National Convention Will Go Forward As Planned

Joe Biden doesn’t think the Democratic National Convention in Milwaukee will go off as planned this summer, telling MSNBC “It’s hard to envision that.”

“Again, we should listen to the scientists,” he added.

On the Democratic National Convention going forward in July

Brian Williams: Can you really envision every prominent Democrat in this country from all 50 states inside a hot arena 104 days from now?

The DNC has been considering contingency plans for the event – currently scheduled for July 13-16, though no final decisions have been made, according to Bloomberg, which notes that last Thursday President Trump claimed that the Republican National Convention would go ahead as planned.

In his interview, Biden also said states should prepare for the possibility of remote voting in November. The former vice president added that he was beginning to lay the groundwork to select his running mate, saying a team to oversee that process will be in place by mid-April.

Biden said six to 10 women would likely make the list, including Michigan Governor Gretchen Whitmer. –Bloomberg

Biden holds an insurmountable lead in delegates vs. his primary Democratic opponent Bernie Sanders. Sanders, meanwhile, remains in the race and has insisted that Biden debate him again.

The former Vice President says he feels “confident” about being the nominee – and that his staff has reached out to Sanders to discuss “a way we could accommodate his concerns” over a variety of issues.

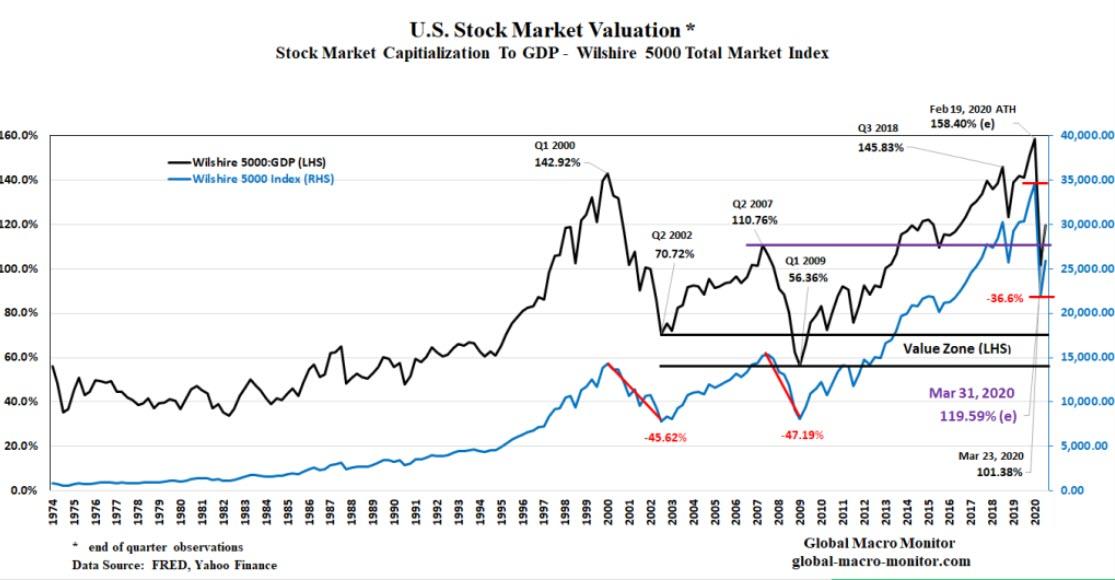

The stock market has completed the first phase of a bear market with a rapid and sharp Q1 sell-off caused by massive deleveraging

Stocks still need to deal with its valuation problem as well as discounting the long-term financial and economic impact of the Coronavirus shock

Even with the 25 percent sell-off since the February 19th high, stock market capitalization-to-GDP remains extremely elevated, still higher than its pre-GFC high and at the 85th valuation percentile

Our analysis illustrates that stocks still have 40-56 percent of downside to reach the valuation levels where the past two major bear market’s bottomed

Time, rather than price, could bring valuations back into line with historical valuation levels as stocks settle in for a protracted bear market

A loss of confidence in the dollar as the world’s reserve currency could spark inflation and boost stocks as an inflation hedge

As the historic Q1 2020 (Wilshire 5000 down 21.25%) comes to a close, we take a look at the current valuation of the U.S. stock market as defined by the Wilshire 5000-to-Nominal GDP ratio also known as the Buffet Indicator.

…the Buffett indicator is the total market capitalization of all U.S. stocks relative to the country’s gross domestic product. When it’s in the 70% to 80% range, it’s go time. When it moves well above 100%, it’s time to tap the brakes.

Of course, sustained periods of divergence can occur when profit margins experience rapid expansion. The diminished bargaining power of labor, technology-led productivity gains, and the emergence of new economic/market paradigms, such as the rise of Chimerica – though rapidly fading rapidly into the dustbin of history – have all contributed to the expansion of corporate profit margins over the past 20 years.

That is until an event or major shock comes along to reset the economy and financial markets.

Business As Usual?

To believe the economy returns to “business as usual” is a hope based on fantasy and ignores the political winds that coronavirus pandemic has stirred up. Nobody could have ever envisioned the possibility of a tenant “rent strike,” which is now gaining support and almost encouraged by some state and local governments. There is probably no more an applicable case for TINA than this.

Furthermore, corporations who now engage in buybacks, one of the main drivers of demand for stocks over the past few years, and do not “take care of their employees” are now viewed as market lepers. The financial zeitgeist is changing rather quickly.

It is interesting to watch the purest of ideologues suspend their economic theology during this pandemic, which is not a bad thing, in our opinion. To paraphrase Voltaire, when the ship is sinking, you can’t allow the perfect to destroy the good.

We Are All Socialists Now

Wall Street and the financial system has been bailed out and saved from itself once again. What else is new? Maybe the third time in twenty years is the charm?

Nevertheless, we are all socialists now. If you doubt that, go ask “Bernie” Trump.

Still Grossly Overvalued

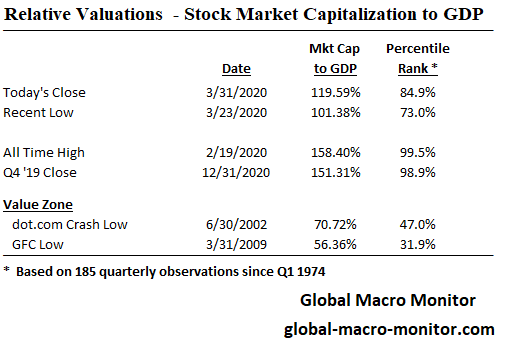

At today’s close, the stock market remains extremely overvalued even with a generous assumption Q1 nominal GDP contracted only 1.41 percent on an annual basis. Market cap-to-GDP finished the quarter at 119.59 percent of GDP, which is still 9 points higher than its peak at the end of Q2 2007, just before the Great Financial Crisis (GFC) began.

That is a very difficult metric for the bulls, who are now touting “the bottom is in,” to digest.

Moreover, today’s close puts the stock market at its 85th percentile in terms of its 185 end-of-quarter valuation levels since 1974, the year the Wilshire 5000 Total Market Index was created. Even at the March 23rd low, 18 percent below today’s level, the Wilshire 5000-to-GDP ratio was at 101.38 percent, the 73rd percentile, hardly a “generational buying opportunity,” in our book.

What’s Up?

Our perception is that markets are dealing with and trying to sort out the confluence of several issues, including financial, economic, and political, which have created a financial and economic “perfect storm.”

Financial Bubbles

Though the catalyst was the Coronavirus, the first leg of the downdraft has been mainly driven by the bursting of multiple asset bubbles, including stocks, bonds, and real estate, which during its initial phase is a massive deleveraging leading to a rapid and trapdoor sell-off. This was inevitable even without the pandemic shock and was a very long time in coming due to the technical condition of most asset markets. The supply and demand imbalance for assets remained favorable for an extended period until it didn’t. See our post, The New “Supply-Side Economics” Fueling Asset Bubbles.

Economic Consequences

The magnitude and speed of the sell-off were sparked by the biggest economic shock the world has experienced since the Great Depression and then some.

It is our opinion, the market still has to grapple and come to grips with its valuation problem, i.e, regress to mean valuations, even before it evaluates the long-term damage and impact the coronavirus shock will have on the global economy.

Politics

Additionally, we have little doubt the domestic and geopolitical landscape is going to look much different on the other side. We have our priors that the political winds, out of necessity, are blowing in favor of:

3) the willingness to finally address the country’s growing wealth gap, though the current bear market is already in the process of closing the disyance between the richest and poorest Americans.

All of the above are not stock market positive.

Where Now?

In the last table, we run a couple scenarios based on two trajectories of nominal GDP and what we deem as the “value zone” where the market should/could/or might bottom based on the past two bear markets. Though we can’t stress enough that nobody knows for certain where the bottom is, or that if it is already in, our analysis is not based on a hunch, gut feel, or wishful thinking but on the historical precedent of the prior two major bear markets, excluding the December 2018 Nightmare Before Christmas mini-bear market.

The upper band of the value zone is the market cap-to-GDP ratio where the dot.com bear market bottomed at 70.72 percent. The lower band is the level where the 2007-09 GFC bear market bottomed at a market cap of 56.36 percent of GDP.

The two scenarios are based on the trajectory of nominal GDP to the end of June 2020.

The first scenario assumes GDP declines by an annual rate of 12.73 percent in the first half of 2020, while the second scenario assumes nominal GDP is at the end-2019 level, very generous and not likely.

Both show that the stock market has a long way down until it reaches the “value zone,” a downside range of 40.7 to 55.8 percent lower, or an S&P500 equivalent of 1123.65 to 1509.31. Take these as approximations and don’t get hung up on the exact figures.

It is important to note, our analysis is based on end-of-quarter observations, which may or may not be the high/low points for each particular three-month period.

Time

Our analysis assumes price is the main determinant in regressing stocks to these valuation levels and that it happens at relatively light speed. Alternatively, the stock market could bang around and slowly drift lower for years as the economy recovers and grows into a more realistic historic valuation. That doesn’t seem likely, however, given the rise of the quants, HFT, and algorithmic trading.

Inflation Hedge As The Upside Target

One possible path, which is not a zero probability, is that with all the current monetization of spending and bailouts, with more surely to follow, inflation begins to take off and stocks become an inflation hedge.

The coronavirus could be the beginning of the end of the dollar’s reserve currency status,

The coronavirus crisis should still wreak far less human damage than the Great War, which precipitated the fall of the Austro-Hungarian Empire, but the shock to the global system may be comparably great. According to Michael Howell of London’s CrossBorder Capital Ltd., this is reason to prepare ourselves for another change of global financial leadership. After a century in which the financial world orbited around the dollar, he believes that we are at the beginning of the Chinese century.

If this sounds outlandish, remember that almost everyone suddenly seems to agree life after the coronavirus will be different. This crisis will change us. The disagreement is over exactly what it will change us into.

If so, the demand for the dollar will diminish while the supply is skyrocketing from all the monetization, leading to severe weakness or even its collapse and thus generating a wave of monetary inflation. Not the “good” demand-pull inflation as central bankers have been trying to generate or have been miscalculating.

Upshot

We don’t know for certain how this all plays out but now you have our analysis. We would love to hear from you if you disagree and to see yours. No happy talk, no hunches, no warm feelings in your tummy but hard analysis with the data.

“Apocalyptic April”: Trump Fails To End Oil Price War As Saudis Unleash Oil Tsunami On The World

Oil held steady near $20 on Wednesday, after President Trump’s pledge to meet with feuding producers Saudi Arabia and Russia (whose real feud is with US Shale producers) to support the market failed to bolster prices after their worst ever quarter.

Having crashed by a record 66% in the first three months of the year, as the coronavirus destroyed demand and the world’s biggest producers embarked on a catastrophic supply free-for-all, oil prices extended losses on Wednesday even after Trump said he discussed the collapse with his Russian and Saudi counterparts, adding that Moscow and the kingdom would “get together” to seek a solution.

However, as Goldman noted last night, any agreement to cut output is likely too late and would fall short of the loss in consumption, not that one is imminent mind you because after Trump’s comments last night, on Wednesday Russia said it is not in talks with Saudi Arabia on oil market situation and President Vladimir Putin has no immediate plans to speak with Saudi Arabian leadership, though Moscow remains open for talks, Kremlin spokesman Dmitry Peskov tells reporters on conference call.

“Russian side traditionally welcomes mutual dialog and cooperation in order to stabilize energy markets” Peskov said adding that “our relations with Saudi Arabia remain on a high level. Of course, we may have certain disagreements, but in general our bilateral relations with SaudiArabia allow us to act effectively when there is such need.”

In short, no meetings between the two oil exporters any time soon, and yet they may have no choice but to arrange a deal.

“I do think both Russia and Saudi Arabia will be forced to cut back production, not because there’s a deal or they’re talking, but because of market forces,” Amrita Sen, chief oil analyst at Energy Aspects said in a Bloomberg TV interview.

“The possibility of negotiations is offering a rare ray of light to a heavily beleaguered market,” said Howie Lee, a Singapore-based analyst at Oversea-Chinese Banking Corp. “There are too many uncertainties involved to determine how strong a driver this would be, but it would probably take more than output cuts to lift prices back to pre-crash levels.”

So there is some hope, but for now with Trump failing to defuse the oil price war, Saudi Arabia has flooded the market as it warned it would less than a month ago, with Saudi Aramco’s oil supply surpassed 12 million bpd on the first day of April, up from 9.7mmb/d in March, and is boosting its production to its maximum, Bloomberg and the WSJ reported. As a reminder, in early March, Saudi Arabia instructed its state-owned oil company to boost supply to 12.3m b/d in April, and told Aramco to boost maximum production capacity to 13m b/d as soon as possible, something it has taken quite seriously as a tweet it just sent would indicate.

الموثوقيّة ليست مجرّد مؤشّر أداء، بل هي ثقافة الاستدامة في إمداد العالم بالطاقة. نفخر في أرامكو بتحميل 15 ناقلة نفط بـ 18.8 مليون برميل

In it, Aramco says that it is loading 15 oil tankers with 18.8 million barrels of oil.

As a result of this unprecedented surge in output coupled with plunging demand, the outlook for oil looks terrible, with Bloomberg noting that “oil is facing a potentially apocalyptic April“, according to top industry analysts. Making matters worse, Iraq has pledged to boost its output this month, while U.S. industry data is signaling the biggest weekly increase in American stockpiles since 2017.

Fears that oil storage space may run out as early as 2 months from now have already pushed certain crude grades to negative prices as we reported last night.

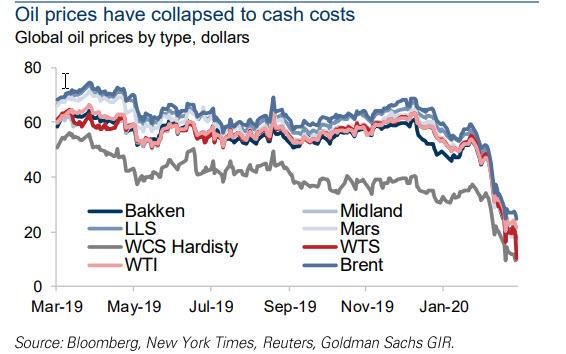

Meanwhile, virtually all energy products are now trading at cash costs, and set to drop further as countless oil producers file for bankruptcy.