Did The Fed’s Monetary Policy Experiment Just Fail?

Authored by Lance Roberts via RealInvestemntAdvice.com,

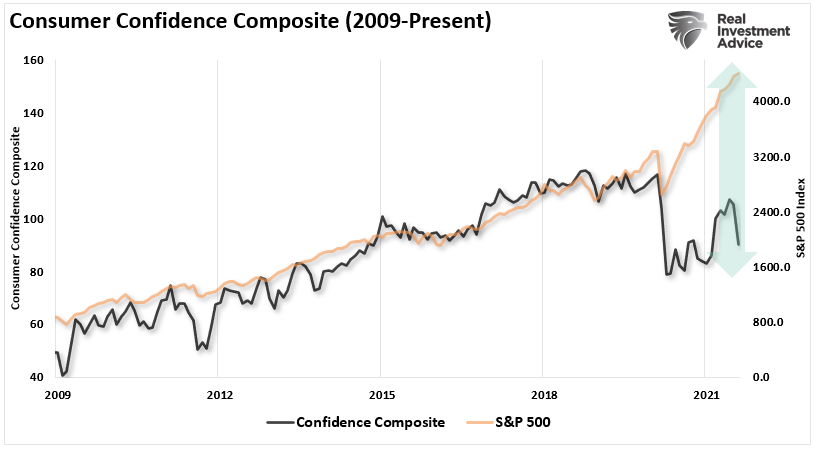

Did the Fed’s “monetary policy experiment” fail? The recent dislocation between consumer confidence and the financial markets may indicate just that.

“U.S. consumer sentiment dropped sharply in early August to its lowest level in a decade, in a worrying sign for the economy as Americans gave faltering outlooks on everything from personal finances to inflation and employment,” – Reuters

However, to understand why I am asking the question, we have to revisit whatBen Bernanke said in 2010 to support the idea of a second round of “Quantitative Easing.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose, and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

What he is referring to is known as “Animal Spirits.”

Animal spirits came from the Latin term “spiritus animals,” which means the “breath that awakens the human mind.” Its modern usage came about in John Maynard Keynes’ 1936 publication, “The General Theory of Employment, Interest, and Money.” Ultimately, “animal spirits was adopted by Wall Street to describe the psychological factors driving investor actions.

Specifically, Ben Bernanke realized that investors would respond to that stimulus and increase asset prices by providing accommodation.

In other words, as long as individuals “believe” the Fed is lifting asset prices higher, they take action buying stocks and driving asset prices higher. Thus, investor actions deliver the desired outcome.

It Was All Going According To Plan

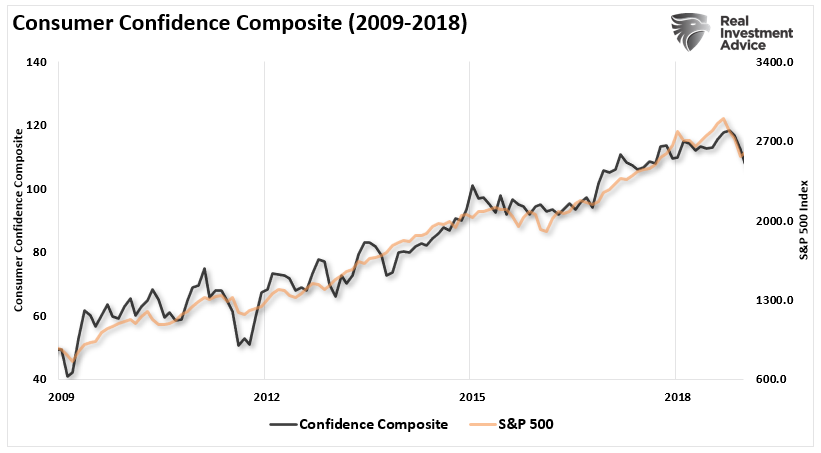

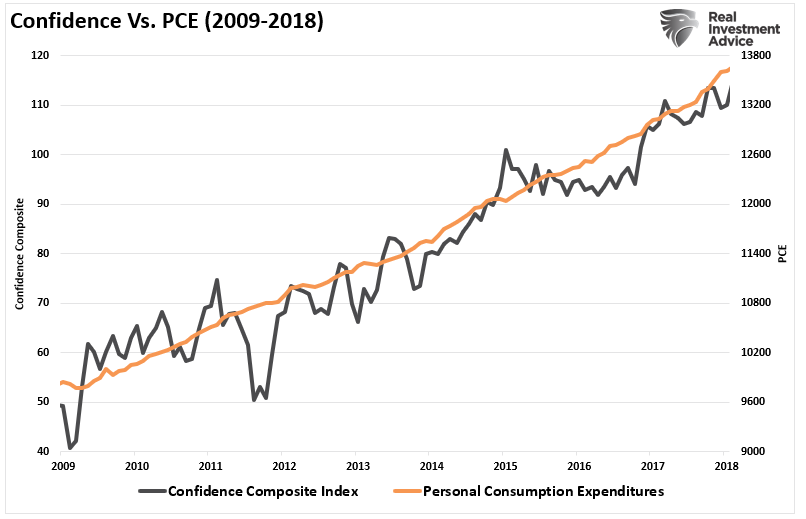

Since the Fed began its monetary interventions, the correlation between the asset prices and confidence remains high.

As noted, the entire premise of monetary policy was to spur consumer spending. Everything seemed to be according to plan.

The problem was that while the Fed lifted asset prices, the economy didn’t strengthen as expected. As discussed recently:

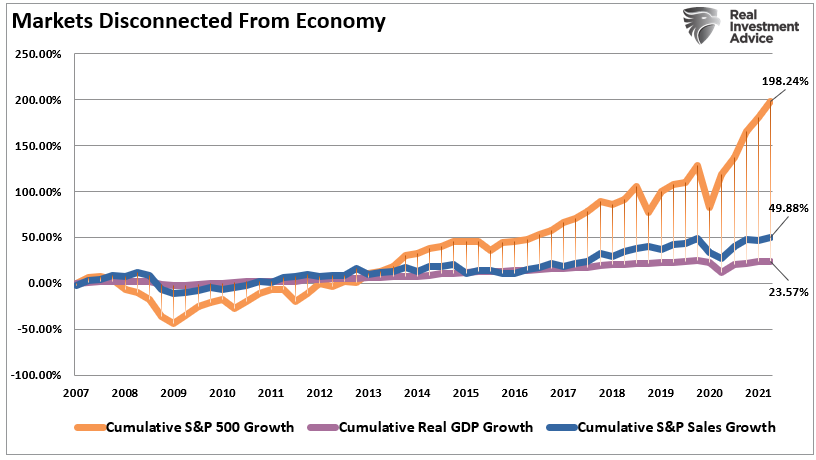

“However, while the Federal Reserve got the desired outcome of increasing asset prices, “quantitative easing” failed to “trickle down.” Despite the massive expansion of the Fed’s balance sheet and the surge in asset prices, there was relatively little translation into wages, full-time employment, or corporate profits after tax which ultimately triggered very little economic growth.“

“Since 2007, the stock market returned nearly 200%, which is more than twice the growth in GDP and nearly 4-times the growth in corporate revenue. (I use SALES growth as it happens at the top line of income statements and is not subject to as much manipulation.)”

Again, it was all going according to plan, sort of.

Until now.

Did The Monetary Policy Experiment Just Fail?

“Over the past half century, the Sentiment Index has only recorded larger losses in six other surveys, all connected to sudden negative changes in the economy,” Richard Curtin, chief economist for the University of Michigan’s Surveys of Consumers, said in a release. Two of those larger month-over-month movers were April 2020 amid the pandemic and October 2008, during the financial crisis.” – CNBC

The decline was extremely sharp.

“Not only was the release dramatically worse than the last update, but it was a huge miss relative to expectations. Today’s release came in 11 points below expectations. The only other month going back to 1999 that even comes close was a 9.9 point miss in February 2004.” – Bespoke Investment Group

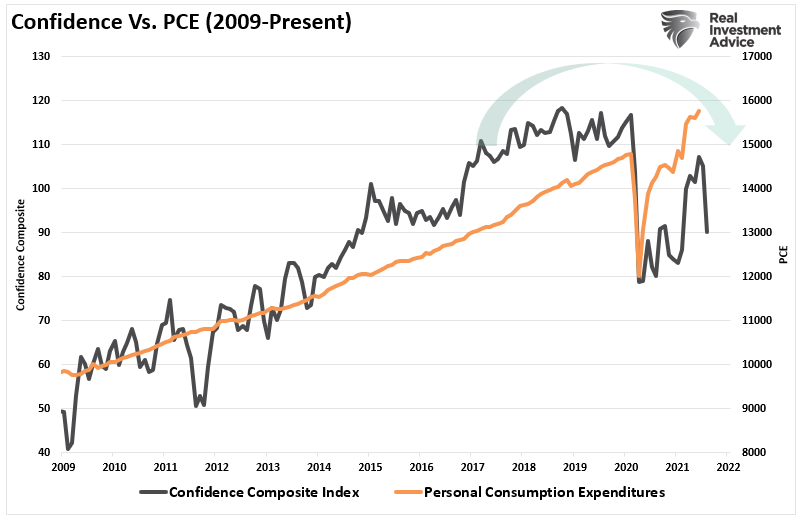

The mainstream analysis missed that the correlation between confidence and markets broke down in 2019. Notably, while the Fed is engaged in monetizing $120 billion in debt monthly, higher asset prices isn’t inflating confidence.

That breakdown of consumer confidence will likely show up in consumption in the coming quarter. Such is mainly due to stimulus and other financial supports fading.

A decent warning sign such may be the case was the weak retail sales report this past week. The large gap between retail sales and employment will likely get filled sooner than expected and not necessarily by higher employment.

If the most giant “monetary policy experiment” just failed, the Fed has an enormous problem.

The Problem For The Fed

Over the next couple of weeks, all eyes are on the Fed. Lately, there has been an abundance of communication from Fed members discussing the need to “taper” its monetary interventions.

As Morgan Stanley recently noted:

“If the July FOMC minutes suggest that there was strong consensus and Chair Powell’s indication on tapering at Jackson Hole is therefore much firmer, we could see that as consistent with the FOMC gearing up to move on tapering sooner.”

Such is something the markets are probably not ready for.

So far, market participants have ignored weakening economic data, the collapse of Afghanistan, and rising risks of infections across the U.S. As long as the Fed is engaged in providing liquidity, the “risk of missing out” outweighs being more conservative with allocations.

However, the Fed remains trapped between two very tough policy choices.

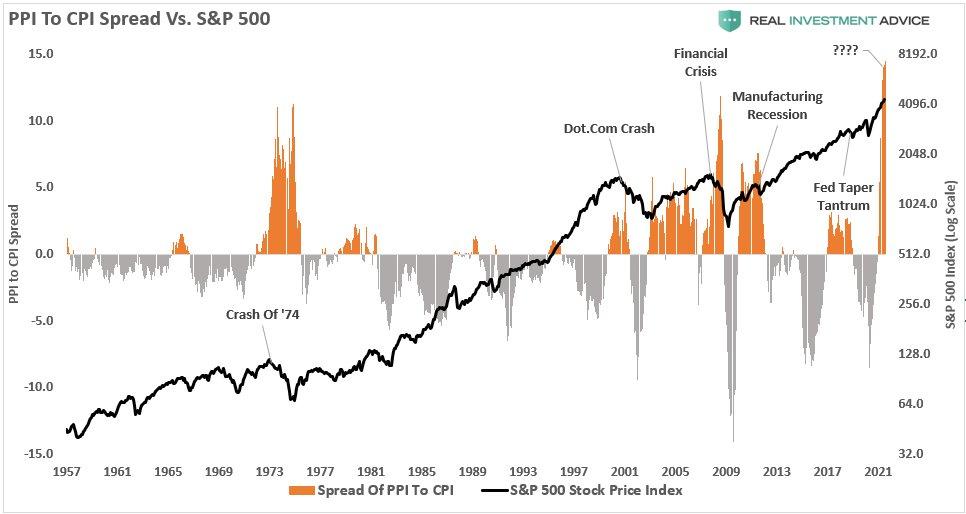

The system has elevated inflation levels, as indicated by the spread between the PPI and CPI inflation measures. Currently, with PPI at the highest spread to CPI in history, it suggests producers can’t pass on costs to customers. Such equates to weaker profit margins and earnings in the future. However, if they elect to pass those costs onto consumers, such will raise living costs well above wages.

With unemployment levels dropping, and inflation rising, the Fed should be tapering monetary policy.

However, the reduction in liquidity will trigger a decline in asset prices, hinder consumer confidence, and contract economic growth further.

It’s a tough choice.

Conclusion

We agree with Morgan Stanley’s assessment on the likely path of “taper” when it comes.

“The path of least resistance is to follow the path most traveled, that is, the playbook established in the last cycle when the Fed began to reduce its purchases of longer-term assets following the 2013 taper tantrum. That playbook included a long lead-time to signal the start, a promise that tapering would be gradual and flexible, and assurances to the market that tapering would have nothing to do with the timing of first rate hike. Indeed, the Fed did not first raise rates until six months following the end of tapering.”

While such is undoubtedly the path of least resistance, it is unlikely the market will like it much. As discussed in “3-Signs Of The Next Bear Market:”

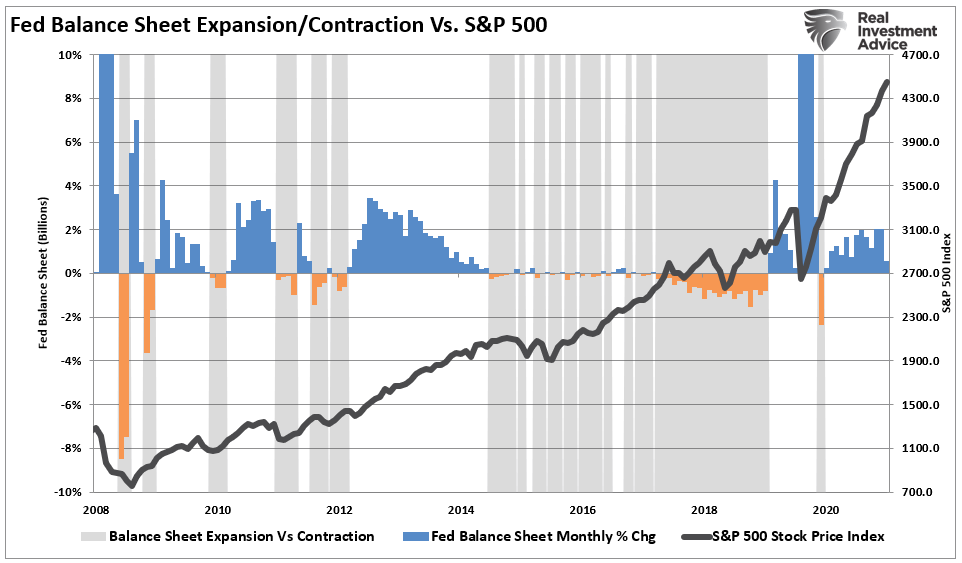

“Therefore, it should also not be surprising that when the Fed starts ‘tapering’ their bond purchases, the market tends to witness increased volatility. The grey shaded bars in the chart below show when the balance sheet is either flat or contracting.”

Notably, the time from the initial tapering of assets and a market correction is almost immediate.

If “monetary policy” has lost effectiveness in supporting consumer confidence and “animal spirits,” the significant risk to investors could be a market decline the Fed cannot halt.

Currently, investors are highly confident the Fed can support markets against any risk.

But what if they can’t?

Tyler Durden

Fri, 08/20/2021 – 10:50

via ZeroHedge News https://ift.tt/3D72lAQ Tyler Durden

Tweeter Only In Theory

Tweeter Only In Theory