Last week, President Donald Trump was calling for Americans living under shelter-in-place orders to “liberate” their states. Now, he’s condemning governors for daring to take his advice. On Wednesday, Trump said it’s “too soon” for reopening plans like the one Georgia plans to implement on Friday.

The about-face provides even more evidence that Trump’s big “liberation” energy was nothing more than a cynical political calculation.

It goes something like this: Push loudly for “reopening the economy”—knowing full well that local leaders, state authorities, and many individuals will resist. When collective reluctance to rush back to normalcy keeps the COVID-19 death toll lower than it otherwise might be, point to the low death toll as evidence that people were overreacting about the virus all along. As we draw closer to the election, Trump can then claim that the country’s economic pain could have been avoided if only everyone had listened to his advice by going out to eat and swarming the beaches months earlier.

Trump only gets to have his cake and eat it if the U.S. avoids a massive spike in new COVID-19 cases and many more deaths. And that’s less likely to happen if local leaders and business owners aren’t extremely careful about how and when they decide to open things back up.

Doing it too soon or too haphazardly will not only mean more COVID-19 infections but longer and worse economic hardship, unemployment, and unrest (and no boost for Trump come November). A president can sometimes survive mass unemployment or mass deaths, but probably not both.

It’s no wonder Trump is now acting like he never meant for people like Georgia Gov. Brian Kemp to allow movie theaters, gyms, bowling alleys, and a broad swath of other businesses to open back up on Friday.

Due to favorable data & more testing, gyms, fitness centers, bowling alleys, body art studios, barbers, cosmetologists, hair designers, nail care artists, estheticians, their respective schools & massage therapists can reopen Friday, April 24 with Minimum Basic Operations. #gapol

“Maybe you wait a little bit longer until you get to a phase two,” Trump said during his nightly televised Q&A session on Wednesday. “I’m going to let him make his decision, but I told him, I totally disagree.”

Trump added that “it’s just too soon” for the likes of “spas and the beauty parlors and the barber shops”—the very types of small business owners out protesting shutdown orders— to open up.

Anthony Fauci put it more strongly:

I plead with the American public, with the governors, with the mayors for the people of your responsibility, although I know one has the need to leap frog over things, don’t do that. Do it in a measured way. This is a successful formula. The problem is if we don’t do that, there is a likelihood that we will have a rebound.

“According to some models,” Georgia is “one of the last states that should be reopening,” suggest Washington Post health reporters. “The state has had more than 830 covid-19 deaths” and “tested less than 1 percent of its residents,” with “the limited amount of testing so far shows a high rate of positives at 23 percent.”

And you already know how the next step goes.

If everything works out in Georgia, it will be because Trump said re-opening the economy was the right thing to do.

And if Georgia turns into the next NYC, it will be all Brian Kemp's fault and Trump warned him not to do it.

Good piece from @Ashkhen on how we can use technology to do contact tracing while still protecting privacy.

Five factors:

1. Transparency 2. No law enforcement access 3. Sunset provision 4. Clear guidelines for collection 5. Limits on data retention pic.twitter.com/pmcA6XSJWH

— Matt Navarra | ???? #StayAtHome (@MattNavarra) April 23, 2020

QUICK HITS

• “I didn’t say that this was going to be worse. I said it was going to be more difficult,” CDC Director Robert Redfield said yesterday, asked to clarify his earlier comment to The Washington Post that “there’s a possibility that the assault of the virus on our nation next winter will actually be even more difficult than the one we just went through.” Trump had tried to claim earlier in the day that Redfield had been “totally misquoted by Fake News.”

• There’s more evidence that COVID-19 was infecting Americans earlier and in greater numbers than initially realized. “By the time New York City confirmed its first case of the coronavirus on March 1, thousands of infections were already silently spreading through the city, a hidden explosion of a disease that many still viewed as a remote threat as the city awaited the first signs of spring,” reportsThe New York Times.

• Jobless claims again exceed predictions:

Weekly jobless claims come in at 4.4 million, against expectations of 4.2 million.

Over the last six weeks, there have now been over 26 million that have filed for unemployment benefits. Still hard to imagine.

• An Illinois judge cleared the way for the Libertarian Party to get on the state’s ballot even though COVID-19 has prevented traditional methods of gathering signatures to petition for obtain ballot access. Brian Doherty explains how.

Tucker Carlson Slams Lockdowns As “Largest And Most Expensive Experiment In Human History”

Fox News host Tucker Carlson railed against the lockdowns in most US states aimed at slowing the spread of coronavirus.

In a compelling presentation Wednesday night, Carlson questioned the “science” behind the decision to shut down much of the country, which has resulted extreme economic hardship as more than 26.3 million workers have filed for unemployment claims as of last week.

“What country is this?” asked Carlson. “It’s a country in a lockdown. We’re told we have no choice but to do this — to stop our lives completely.”

“Mass quarantines, they tell us again and again, are the only way to save lives,” Carlson added. “But that’s a lie. They don’t know it’s true, despite what they’ve claimed. There’s no scientific record to consult. It’s never been done. We’re currently living through the largest and most expensive experiment ever conducted in human history. We’ve spent trillions of dollars, and crushed millions of people, purely on the guess that a nationwide lockdown would save us from the coronavirus. Has it worked? Was the guess correct?”

Carlson then noted that the eight US states which haven’t issued shelter-in-place orders are “below the national average of coronavirus cases, and deaths, per capita” – quoting Professor Wilfred Reilly of Kentucky State University, who found that “a state’s lockdown strategy had virtually no effect on how severe its outbreak of the Wuhan coronavirus was.”

“Are you surprised by this?” Carlson asked. “Maybe you shouldn’t be. You can see the same trend at work in other countries. Sweden, most famously, has never locked down. Restaurants there have never closed. That country is still suffering from coronavirus, suffering more in fact than we are in the U.S. But the country’s epidemic appears to have peaked. And without locking down, Sweden has, and this is the key, has fared far better than other European countries that did lock down. That includes Britain, Italy, Spain and Belgium.” –Daily Caller

Perhaps most damning is new studies which suggest that far more people may have already had coronavirus.

“Up to 320,000 adults in Los Angeles apparently had already had it,” said Calrson, citing the world of USC researchers who found that as of early April, upwards of 5.6% of the entire county had possibly contracted the coronavirus.

“At the time, the official number of infected people was about 8,000 people. City officials had no clue. They weren’t even close. The virus had spread throughout a huge population right in the middle of the most restrictive quarantine in American history. What does that tell you? It tells you the lockdown didn’t work.”

According to Carlson, officials in lockdown states are “by and large ignoring any evidence that indicts their policies, or that might threaten their new and much-loved power.”

“They don’t want to know what the facts are,” he said. “Indeed, some are now promising even longer lockdowns, maybe through the end of the summer, and even tougher punishments for those who flout them.”

“This is insanity,” Carlson concluded. “It is definitely not science. This is not science. It has nothing to do with the public’s health, much less the broader public interest. This is instead what happens when mediocre people suddenly find themselves with God-like power: deciding who can go outside, when people can get married, which medical procedures you’re allowed to have. That’s a feeling of omnipotence, and they like that feeling. It fills an empty place inside. They don’t want to give it up. They want it to last forever, even as the country dies. But it can’t last forever. Because it’s not their country. It’s ours.”

Carlson then interviewed Dr. John Ioannidis, a professor of medicine at Stanford University who authored a report which found that roughly 1.5% of 3,300 volunteers tested for COVID-19 antibodies were positive, and extrapolated (after adjusting for differences between the sample and the population of the county as a whole) that an between 2.5% and 4% of Santa Clara County residents have antibodies – suggesting that 48,000 – 81,000 people had already been infected in the county by early April.

Commenting on the effectiveness of the lockdowns, Ioannidis suggested that we need to wait until the virus waves are “mature,” because “we can have some surprises.”

“The science is telling us that this is a common infection. Most people probably don’t recognize that they’re infected, they’re asymptomatic. At the same time it can be a devastating infection, it can kill lots of people” said Ioannidis.

West Texas Intermediate, the oil grade most associated with American production, plunged down to -$40 April 20. You read the right. For a while this week, sellers had to pay people forty bucks to take a barrel of crude.

As with any product, the business of oil isn’t a once-and-done. It must be produced, shipped and processed, and then the refined product must be shipped and retailed. What happened April 20 is a bottleneck in that process. Production surged ahead of pipeline shipping capacity, leaving some producers with nowhere to put their crude.

The real kicker is that this is not the “negative prices” outcome I predicted a couple weeks back. “All” the April 20 event was was a single facility in a single country running out of future leased storage capacity for the month of May. The April 20 price crash will happen again in the same place and it will be bigger: June WTI futures contracts are now spazzing, and America’s Cushing oil storage and transport nexus undoubtedly will be actually full by then. But even this is nothing but the warmup for the big show.

That will happen when the world runs out of storage.

Numbers are fuzzy in this corner of global oil markets. In part because everyone classifies and categories their oil storage capacity differently. In part because they should (gasoline storage is functionally different from raw oil storage). In part because some countries don’t share data because they’re lazy or secretive. But no one thinks there’s a whole lot of storage capacity left. Global oversupply of crude right now is over 20mpbd (with 30mbpd seeming to be the “average” guestimate). Most folks in the know are now musing that what storage remains will be filled up completely sometime in May or early-June.

And filled up it will be, because that is the express goal of the world’s largest oil exporter, Saudi Arabia. The Saudi price war started out as a spat with the Russians over carrying the burden of a production cut. It has since expanded into the Saudis targeting the end markets of every single one of what the Saudis’ consider to be inefficient producers. The Saudis are directly targeting markets previously serviced not just by US shale and Russian, but those serviced by Kazakhstan and Azerbaijan and Libya and Iraq and Iran and Malaysia and Indonesia and Mexico and Norway and the United Kingdom and Nigeria and Chad and you get the idea.

As of this morning, there are still at least 24 supertankers carrying at least 50 million barrels of Saudi crude en route to the U.S. Gulf Coast. Most will arrive in May, seeking to fill up as much of what remains of U.S. storage as possible. Similar volumes are in route to Europe and even bigger volumes to Northeast Asia. In most cases the destinations are the transshipment nodes that enable distribution of inland-produced oil to coastal locations: Rotterdam, Suez, Singapore, Korea.

Assuming you’ve got deep pockets, and Saudi Arabia’s are some of the world’s deepest, it isn’t a stupid strategy. If the Saudis can push prices firmly negative, it will absolutely crush many of the world’s energy producers. My back-of-envelope math suggest some 20 million barrels per day of production capacity – one-fifth of global output – will go offline for years. And then Riyadh will have what it wants: the ability to raise prices as much as it wants and to reign supreme over the world of oil for at least several years. (There are still a veritable swarm of flies that will need to be dealt with in that particular ointment, but the Saudi plan seems sure of generating plenty of ointment nonetheless.)

The WTI price crash on April 20 confirms that if the Saudis didn’t realize the potential for their strategy’s explosive success before, they certainly do now. They have no reason to back down.

There are a few producers worthy of callouts.

Canada’s Alberta province has the most to lose. Not only landlocked, it must sell all its oil into the American market that is already so saturated. Its production must be shut in for years.

Venezuela was facing civilizational collapse due to mismanagement before oil prices tanked. As oil is the government’s only remaining income stream, this marks the end of Vene as a country. Its oil will not come back for at least a decade, and even then only if an outside power first physically invades the place to rebuild the country from scratch.

America’s sanctions regime against Iran has been so successful the country isn’t an oil exporter any longer. Its output will absolutely collapse this summer, and the country lacks the funds to bring in foreigners to help restart it or the skills to do the work itself.

Russian fields are in swamps and permafrost. Drilling is only possible during the winter. Any shut-ins means the wells freeze solid, necessitating completely new drilling. Last time this happened it took the Russians nearly 15 years to get production back.

Azerbaijan and Kazakhstan are both dependent upon other countries (in some cases, Russia) to transit their crude to market. High production costs plus finicky neighbors equals long-haul shut-ins.

Nigeria is a mess on a good day, and the supermajors who have made Nigerian output possible have steadily moved offshore to get away from the chaos and violence. Once they turn off their wells, they won’t even consider returning until global prices rise to the point that they are once again willing to subject their staff to frequent kidnapping. That’s several years off.

Iraq has been in a state of near civil war for some 15 years. The country is now producing over 4mbpd, the income of which helps hold the place together. Negative prices will remove the “near” from the country’s political condition and (at best) make the place a ward of the Arab states of the Persian Gulf.

It is also worth noting that the speed that this could all go from head-spinning to head-chopping is intensely short. Right now there’s still a fair amount of spare oil tankers to shuttle about the world. The Saudis have been leasing out every tanker they can find, so before long all the the world’s tankers will be full as well.

Oil has been a panacea for all sorts of inefficient, compromised, and in some cases evil regimes for decades. Huge demand in the West and Northeast Asia allowed a raft of previously insignificant or morally reprehensible leaders and societal situations to effectively print dollars out of the ground and count the industrialized world as a hungry customer. Not anymore. Demand patterns have shifted, the United States is now an exporter of crude oil and products, and the petro-economy that has kept ayatollahs and ideologues afloat is crumbling. Before anyone cheers it’s worth remembering that things will get a lot uglier before they have any hope of improving.

“Most, If Not All” Of The American Economy Should Reopen By Summer’s End, Mnuchin Says

During an appearance on Fox Business yesterday, Treasury Secretary Steven Mnuchin said he expects “most, if not all,” of the American economy to reopen by the end of August, offering one of the first timelines – however informal – for what American workers should expect regarding their near-term financial future.

“We’re operating under the environment that we are going to open up parts of the economy and we’re looking forward to – by the time we get later in the summer – having most of the economy, if not all of the economy, open,” Mnuchin said.

Federal programs have dedicated some $600 billion to supporting businesses, Mnuchin said, and that figure can be leveraged by the Fed into some $6 trillion of liquidity. The secretary said he “hopes” this lofty sum will be enough.

“I hope it is enough,” Mnuchin said.Part of the rescue funds provided to the Treasury Department can be leveraged through Federal Reserve lending facilities for as much as $6 trillion in liquidity.

We hope so, too. Because even before this latest bill passes, the 2019-2020 federal budget deficit has already tripled to $4 trillion.

“We need to spend what it takes to win the war,” Mnuchin said, adding that interest rates on the additional debt will be relatively low. “On the other hand, we are sensitive to the economic impact of putting on debt and that’s something that the president is reviewing with us very carefully.”

But Americans can worry about fiscally responsibility later. Right now, we have a virus to kill, and many wealthy investors at risk of potentially needing to sell one of their summer homes.

A week ago, I didn’t know what a ‘Karen’ was. Today I can’t stop seeing Karens everywhere I look. It’s like that moment in They Live! when Nada puts on the glasses for the first time.

The problem now is I can’t take the glasses off.

And I’m not the only one. In recent weeks the failed Karen meme of a few years ago has returned with a vengeance as people realize just how much damage Karens have done to our society.

A Karen is a person, usually a woman, who is never satisfied with the service she’s receiving and demands to talk to the manager. It doesn’t matter if Karen’s complaints are valid or not.

This is because Karen has been incentivized by cowardly corporate officers and government officials (but, I repeat myself) to get something she doesn’t deserve simply because they want her to shut up and not disturb everyone else.

It was one thing to indulge Karen her entitled behavior when she was getting a free order of fries or month of cable. It’s quite another when Karens become the State’s target audience for public policy.

And the true Karens are the ones who are never satisfied. When they get the first thing they want it gives them the impetus to continually push the boundaries of what they can get away with.

Karens, at heart, are simply spoiled children who have never had boundaries properly set. A little power creates a self-reinforcing feedback loop.

Progressives are the ultimate Karens, never satisfied with having moved society in a terrible direction through their constant complaining. Never once do they self-reflect that maybe they’ve been wrong and all of their demands have made things materially worse rather than us not having indulged them enough.

Progressives are the worst winners I’ve ever met. They’ve won every political battle of note for the past 100+ years and are still whining in their lattes about us electing Trump, whose presidency they’ve destroyed with their incessant Karen-isms and his inherent weakness.

So is is any surprise that we’ve reached a point where the government is more worried about keeping the Karens from complaining than actually governing effectively?

And when we really look at how we’ve responded to COVID-19 it’s clear that the people behind the lock down of hundreds of millions of people knew they would have an army of Karens screaming on Twitter to ‘flatten the curve’ and quote bogus statistics they don’t understand from official smart people to justify giving full flower to their inner harpy.

You know who I’m talking about. These are the suburban women ratting out their neighbors for not social distancing, for *gasp* walking their dog or *gasp gasp* letting their kids play in the yard!

And that have enabled the worst people in the world to destroy the global economy because a bunch of frightened Karens can’t cope with the stress of living. The State cannot have people engaging in peaceful noncompliance with their edicts.

Karen-ness is a mental disorder. It’s the horrific admixture of narcissism, self-importance and solipsism which can only come from being encouraged to act badly thanks to cowardice. It leads to treating everyone else like they exist only to serve them.

Karens used to be a joke at best. They used to be Violet Beauregard in Willy Wonka or the starting point of a female lead in a rom-com.

Now they run the world.

Karens are proto-Brown Shirts. They are the ultimate useful idiots of the Elite and they are destroying the world we live in. Because they are the happiest when the State does something. They have no boundaries at home, so they welcome any time the State gives them what they want and use that to bludgeon everyone else into line.

And the worst part is in this new age of gender fluidity, Karens are now found in both sexes. As guys who should know better join in the chorus of complaining about everything they don’t like.

It’s the worst in genre fandom, FYI. All you Cheeto-dusted message board warriors sitting on your gaming thrones bitching about Star Wars or Marvel are simply Karens with doobs (Dude Boobs) because you feel entitled a particular story to fill your pathetic lives with meaning.

And when you don’t get them you want someone fired.

Sound familiar?

In truth, if you were real men you’d grow up and spend that time acquiring skills to become a man worthy of allaying the fears of all the Karens you say are destroying your favorite stories.

Who knows? You might even get laid!? Just sayin’

But it means looking in the mirror rather than at porn. So I guess that’s a non-starter.

At the heart of this is cultural Marxism and its unquenchable envy for what the other guy has. And the Marxists have worked long and hard to undermine the institutions of culture — family, religion, community — by deconstructing everything, destroying meaning and robbing a generation of hope.

And if you don’t think it wasn’t done on purpose you’re wrong. The goal has always been to break us down into dependence and psychosis. This is what John Carpenter was warning us about in They Live!

The difference is we aren’t asleep. This isn’t The Matrix anymore. We jacked out of that nightmare to find a world even worse than we thought and now we’re crazy from being sleep deprived.

So now we’re a nation of noradrenaline-addicted, cortizol-drenched doom porn addicts as we realize there’s no one competent in charge and our neighbors are a bunch of whiny Karens.

The world is melting down financially, politically and culturally.

We’ve run out of time to suffer Karens. We don’t need anymore Nancy Pelosis and Alexandria Ocasio-Cortezes extolling the virtue of Karen’s endless complaints.

Things are this way because men have abdicated their role in the division of labor that is sexual dimorphism as the check on poor female behavior. It’s our job to exude quiet competence, bear the burdens of keeping the society from collapsing.

So, what we actually need is Ceasar Milan to come in and tell them all, “Shh!”

Because when we don’t do that, Karens turn to the State, exactly as the Marxists wanted.

This has given rise to the kind of toxic femininity that is fully encapsulated in the Meme of Karen.

And it’s why the Karens are screaming such bloody murder with the return of the meme. They know it’s true and that the jig is up.

And the irony is that what most Karens really need is someone calling them out for being Karens and not indulging their anxiety-driven insanity.

Shh!

This is why the Karen meme has returned with such ferocity. The lock down of society in fear of COVID-19, a virus the more we learn about the less fearful we are, has a critical mass of people reaching their breaking point with being a member of Karen Nation.

Because to continue on this path leads to depravity and violence; a breakdown of the basics of civil society.

And to leave it is to end the rule of incompetent, cowardly men like Bill DeBlasio, Barack Obama and George W. Bush and the women who rule them.

565 Americans Have Lost Their Job For Every Confirmed COVID-19 Death In The US

In the last week 4.427 million Americans filed for unemployment benefits for the first time.

Source: Bloomberg

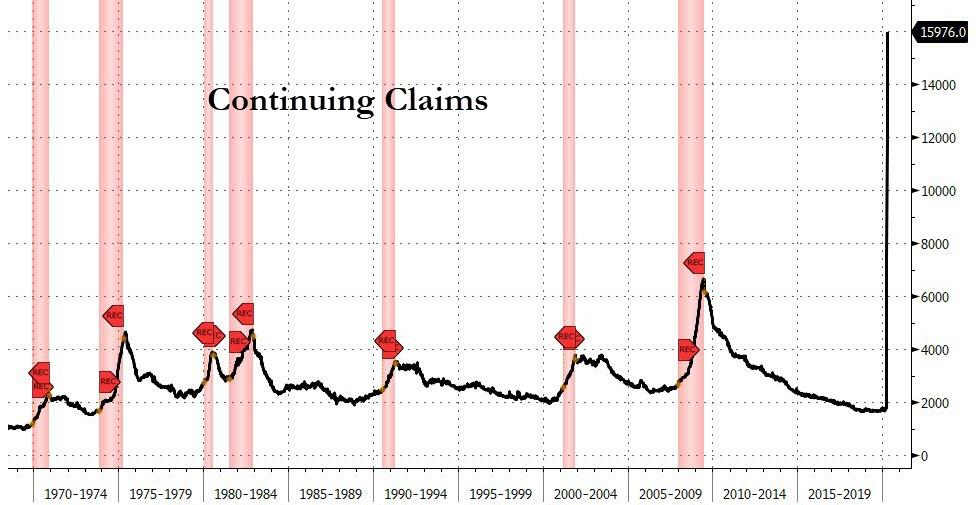

That brings the four-week total to 26.5 million, which is over 10 times the prior worst five-week period in the last 50-plus years.

And of course, last week’s “initial” claims and this week’s “continuing” claims… the highest level of continuing claims ever

Source: Bloomberg

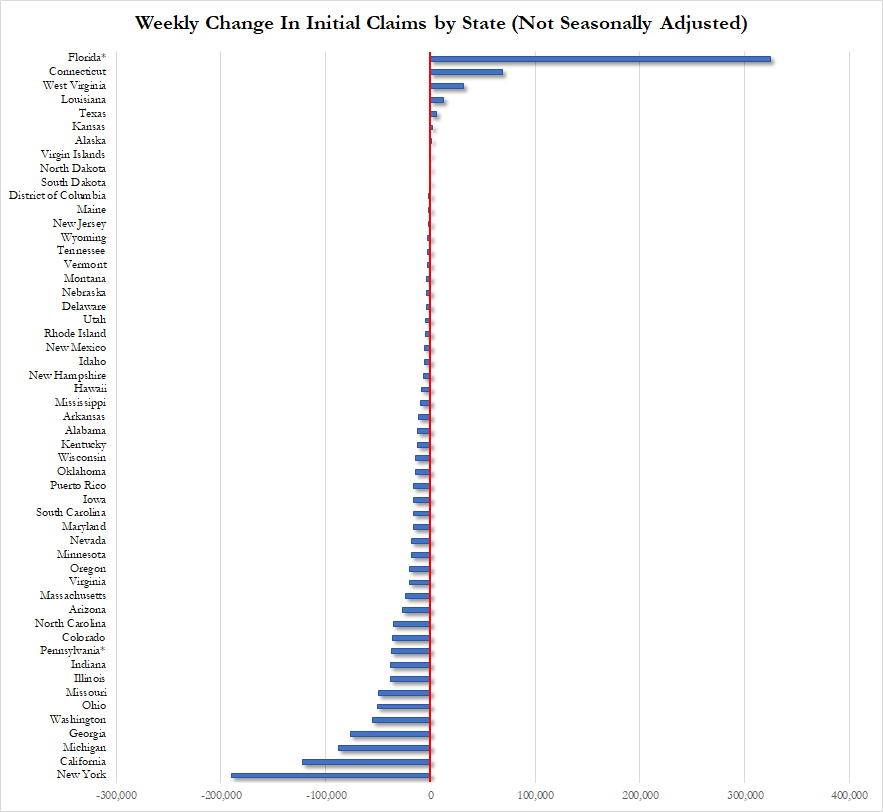

A breakdown of initial claims by state shows that the weekly devastation is easing, with the number of (not seasonally adjusted) claims in New York, California and Michigan declining notably over the past week, while Florida and Connecticut still showing dramatic increases.

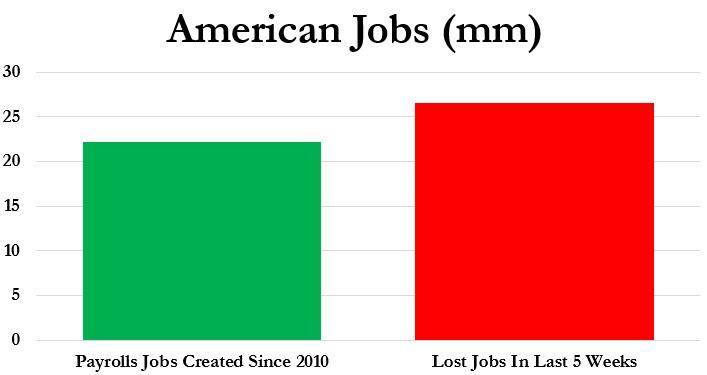

And as we noted previously, what is most disturbing is that in the last five weeks, far more Americans have filed for unemployment than jobs gained during the last decade since the end of the Great Recession… (22.13 million gained in a decade, 26.46 million lost in 5 weeks)

Worse still, the final numbers will likely be worsened due to the bailout itself: as a reminder, the Coronavirus Aid, Relief, and Economic Security (CARES) Act, passed on March 27, could contribute to new records being reached in coming weeks as it increases eligibility for jobless claims to self-employed and gig workers, extends the maximum number of weeks that one can receive benefits, and provides an additional $600 per week until July 31. A recent WSJ article noted that this has created incentives for some businesses to temporarily furlough their employees, knowing that they will be covered financially as the economy is shutdown. Meanwhile, those making below $50k will generally be made whole and possibly be better off on unemployment benefits.

Furthermore, as families across the nation grapple with lost jobs and struggle to get meals on the table, The Epoch Times’ Zachary Stieber reports that food stamp benefits are up 40%, according to the Department of Agriculture.

The increase will “ensure that low-income individuals have enough food to feed themselves and their families during this national emergency,” Secretary of Agriculture Sonny Perdue said in a statement.

“President Trump is taking care of America’s working-class families who have been hit hard with economic distress due to the coronavirus. Ensuring all households receive the maximum allowable SNAP benefit is an important part of President Trump’s whole of America response to the coronavirus.”

Families receiving food stamps can typically get a maximum benefit of $768. Through the increase in emergency benefits, the average five-person household can get an additional $240 monthly for buying food. Families already at the maximum won’t get additional benefits. SNAP normally costs the U.S. government approximately $4.5 billion each month. The allotments made under the Families First Coronavirus Response Act, which President Donald Trump signed, is adding nearly $2 billion per month to that total. The emergency funds are made available through waivers the Department of Agriculture makes for each state.

But, hey, there’s good news… well optimistic headlines as Treasury Secretary Steven Mnuchin said he anticipates most of the economy will restart by the end of August.

Finally, it is notable, we have lost 565 jobs for every confirmed US death from COVID-19 (46,785).

Futures Flat Despite Record Eurozone Business Collapse Ahead Of Latest Claims Shocker

US equity futures and global stock markets were surprisingly uneventful on Thursday on the back of a continued modest rebound in oil prices despite a record collapse in European business activity, as investors braced for another staggering jobless claims report as sweeping lockdown measures hammer economic growth.

The S&P500 jumped on Wednesday on a recovery in oil prices and signs Congress was set to pass $500 billion more in relief for small businesses and hospitals. The bill is expected to clear the House of Representatives later in the day. Still, the benchmark index is 17% below its February record high as statewide shutdowns sparked layoffs and crushed consumer spending. Surveys on U.S. manufacturing and services firms are likely to mirror dismal readings from Asia and Europe issued earlier on Thursday. As noted earlier, a composite European business index plunged to its lowest print on record.

Data set to be announced shortly is also likely to show a record 26 million Americans sought unemployment benefits over the last five weeks, confirming that all the jobs created during the longest employment boom in U.S. history were wiped out in about a month.

Retailer Target Corp tumbled 7% in premarket trading despite a surge in digital sales in March and April which offset a slump in-store sales. Eli Lilly gained 1.5% as it reported a jump in first-quarter sales, boosted by its diabetes drug and also benefiting from customers stockpiling its medicines during the pandemic.

Europe’s Stoxx 600 Index drifted as the abovementioned PMI index plunged far more than economists anticipated. Credit Suisse slipped after the bank said first-quarter profitability rose but that it’s taking a greater than expected $1 billion in writedowns and provisions for bad loans after the pandemic.

Earlier in the session, Asian stocks gained, led by materials and energy, after rising in the last session. Most markets in the region were up, with Japan’s Topix Index gaining 1.4% and India’s S&P BSE Sensex Index rising 1.2%, while Shanghai Composite dropped 0.2%. The Topix gained 1.4%, with Jeans Mate and Showcase Inc/Japan rising the most. The Shanghai Composite Index retreated 0.2%, with Xinjiang Winka Times Department Store and Zhejiang Meilun Elevator posting the biggest slides.

Crude futures jumped for a second day despite a swelling global glut.

Looking ahead, investors will focus on the latest weekly jobless numbers from Washington that are estimated at 4.5 million. While governments across the world have pledged more than $8 trillion to fight the pandemic, a sharper picture of a crippled global economy is emerging from unprecedented layoffs, chaos in the oil market, poor European data and a mixed bag of corporate earnings, as Bloomberg summarizes.

There were some good news on the virus front, where New York fatalities were at the lowest rate since early April, while Treasury Secretary Steven Mnuchin said he anticipates most of the economy will restart by the end of August. House lawmakers on Thursday are set to pass another round of aid. Infections and deaths spiked higher in Spain, home to the world’s most extensive outbreak after the U.S., even amid its sixth week of strict lockdown.

The most important event today is the long-awaited European Council summit via videoconference this afternoon, where the big question will be over how the idea of a European Recovery Fund is financed. Yesterday, Bloomberg News reported that the Commission would propose a €2 trillion plan that would in part use the bloc’s 7-year multi-annual budget with a €300bn recovery fund included, but also establish a new temporary financing mechanism that would raise up to €320bn. However, this could prove controversial given the issuance of joint debt, to which the northern member states are strongly reluctant.

In rates, Treasuries steadied while commodity currencies advanced on a rise in oil prices; Spanish bonds extended an advance, leading peripheral outperformance over euro-area peers; bunds erased declines after French PMIs missed median estimates. Gilts fell then rose after the U.K. DMO announced it will raise in four months of debt sales almost as much as it did during the height of the global financial crisis.

In FX, the Bloomberg dollar index inched up, erasing losses after coming under pressure from short covering in crosses into the London open. The euro fell after much worse than anticipated German consumer confidence data. The Norwegian krone shrugged off a plunge in industrial confidence and rose versus all major peers. Australian and New Zealand dollars traded higher against the greenback as the recovery in oil futures sparked short covering among commodity currencies

Looking at the day ahead, and along with the aforementioned European Council meeting, PMIs and initial jobless claims from the US, other data releases include Germany’s GfK consumer confidence reading for May, the UK’s public sector net borrowing for March, along with the US new home sales for March and April’s Kansas City Fed manufacturing activity index. From central banks, we’ll hear from the BoE’s Vlieghe, while earnings out today include Intel, Eli Lilly and Company, NextEra Energy and Union Pacific.

Market Snapshot

S&P 500 futures down 0.1% to 2,786.75

STOXX Europe 600 down 0.1% to 329.81

MXAP up 0.8% to 142.65

MXAPJ up 0.5% to 460.76

Nikkei up 1.5% to 19,429.44

Topix up 1.4% to 1,425.98

Hang Seng Index up 0.4% to 23,977.32

Shanghai Composite down 0.2% to 2,838.50

Sensex up 1.4% to 31,805.19

Australia S&P/ASX 200 down 0.08% to 5,217.11

Kospi up 1% to 1,914.73

German 10Y yield fell 0.3 bps to -0.41%

Euro down 0.2% to $1.0800

Italian 10Y yield fell 7.6 bps to 1.902%

Spanish 10Y yield fell 8.9 bps to 1.048%

Brent futures up 7% to $21.80/bbl

Gold spot up 0.6% to $1,724.11

U.S. Dollar Index up 0.1% to 100.44

Top Overnight News from Bloomberg

Confidence among European businesses and consumers is in free fall as shutdowns to contain the coronavirus push the economy into recession

The Federal Reserve’s beefed-up swap program is having some unintended consequences, especially in Europe. It helped bring down the cost of dollars to such an extent they’re cheaper to borrow in cross-currency markets than any major currency. But that’s driving opportunistic players to tap local markets to swap into dollars, which ends up elevating domestic borrowing costs

The effect of the U.K.’s emergency spending to combat coranavirus began to show up in public finance data for March, as a jump in spending caused the budget deficit to widen more than expected

The U.K. government is to survey 20,000 households in a bid to track the spread of the coronavirus in Britain, five weeks after it abandoned a strategy of community testing for the disease

Asian equity markets mostly benefitted from the more constructive handover from Wall St where sentiment rebounded in tandem with oil prices amid touted bargain buying and increased US-Iran geopolitical risks after US President Trump instructed the US Navy to destroy any and all Iranian gunboats if they harass US ships at sea, with the Senate’s recent passage of the USD 480bln relief bill also adding to the bout of optimism stateside. ASX 200 (-0.1%) advanced at the open but with gains later pared after mixed data releases, as well as weakness in defensives and the largest weighted financials sector. Nikkei 225 (+1.5%) traded higher although upside was restricted by an indecisive currency and following abysmal PMIs in which Manufacturing PMI posted its worst reading since 2009 and both Services and Composite PMIs were at record lows, while the KOSPI (+1.0%) outperformed after it eventually shrugged off the largest contraction for South Korea GDP in more than 11 years. Elsewhere, Hang Seng (+0.4%) and Shanghai Comp. (-0.2%) were indecisive with price action kept rangebound amid a lack of fresh drivers and continued PBoC liquidity inaction, while Hong Kong policymakers remained focused on defending the currency peg. Finally, 10yr JGBs initially weakened amid the early broad optimism but then recovered from lows as the regional stock indices retraced some of the gains and following stronger results at 2yr JGB auction.

Top Asian News

South Korea’s Economy Shrinks Most Since 2008 Amid Pandemic

Singapore Traders Say They’re Healthy Amid Hin Leong Saga

Operation Twist Returns to Send India’s Bond Yields Plunging

The optimism seen in the APAC session faded as European trade went underway [Euro Stoxx 50 -0.1%], with the deterioration attributed to a string of dismal April Flash PMIs across the region and as participants look ahead to the Eurogroup summit later today (Primer available on the Newsquawk headline feed). A meeting which could see disagreement over the rollout of the European Recovery Fund – officials touting a launched in 2021; however, Italy stated they cannot wait until June 2020 for approval. European bourses trade mixed with no standout under/outperformers, whilst broader sectors also paint a mixed picture and fail to reflect a clear risk tone – albeit the energy sector outperforms as the complex continues to post gains. The breakdown also sees a similarly mixed picture – again with Oil & Gas leading the gains. A slew of earnings were reported in the pre-market, including prelim figures for Daimler (+0.9%) and Software AG (+0.8%), whilst Renault (+2.3%), Orange (+0.5%), Pernod Ricard (+0.3%), Accor (+1.1%), Swedbank (-0.7%), Volvo (-7.0%) all reported quarterly numbers – with Renault firmer despite a downbeat earnings release on reports Renault CEO is to unveil cost-cutting measures next month, whilst Volvo is pressured after substantially missing on its EPS and adj. operating profit expectations. Moving to Credit Suisse’s (-2.2%) earnings, the group topped net income forecasts but reported a deterioration in revenue and a Q1 loan loss provision over double its expectations. That being said, market volatility saw its FICC and Equity trading and sales both higher in excess of 20% YY. Elsewhere, Wirecard (+8.0%) sees itself at the top of the DAX after an independent audit of the Co. has uncovered no substantial findings with regards to questionable accounting methods; however, the full report is yet to be published. Results from the audit are now expected for April 27th and the Co’s FY results are to be published on April 30th. Finally, Tullow Oil (+30%) opened with gains above 60% and holds its place at the top of the Stoxx 600 after divesting its stake in Uganda to reduce net debt, whilst also seeing tailwinds from favourable price action in oil.

Immofinanz Names Investor Ronny Pecik as New Chief Executive

Orban Blinks After Decade Fighting Foreign Sway Over Economy

In FX, the single currency is languishing at the bottom of the G10 table and looking precarious under 1.0800 vs the Dollar not to mention across the board as Eur/crosses teeter over psychological or key technical levels, like Eur/Chf on the verge of 1.0500, Eur/Jpy edging towards 116.00 and even Eur/Gbp testing the 200 DMA (0.8736). Much worse than anticipated preliminary Eurozone PMIs, and particularly poor services sector prints have undermined the Euro, but Eur/Usd is holding in just above or around chart supports ahead of 1.0750 in the form of April 6’s so called reaction low at 1.0769 and a 1.0757 Fib retracement level, for now, with some additional buffers provided by option expiries extending from 1.0800-1.0790 to 1.0750 in 3.1 bn and 1.2 bn respectively.

NZD/AUD/JPY/GBP – The Kiwi and Aussie continue to see-saw vs their US counterpart, with the former recovering from a stop-induced slide overnight after 0.5900 held and subsequently retesting resistance ahead of 0.6000, while the latter was able to withstand weak PMIs with the aid of trade data revealing a much wider surplus as exports outpaced imports nearly 3-fold. Aud/Usd has reclaimed 0.6300+ status and briefly extended gains to circa 0.6370 before fading alongside Aud/Nzd ahead of 1.0650. Meanwhile, the Yen continues to retain an underlying safe-haven bid between 108.00 and 107.50 with decent option expiry interest also keeping the pair contained (1 bn at 107.50 and 1.6 bn from 107.85 to 108.00). Elsewhere, Sterling has (somehow) taken bleak UK PMI and CBI surveys in stride and resisting Greenback advances after Cable came close to filling bids touted at 1.2300, though this could be due to the aforementioned Eur/Gbp correction from recent 0.8800+ peaks rather than anything especially or uniquely Pound positive.

USD – The Buck may be primed for a fall after the latest US initial claims release and/or Markit PMIs, but for now the DXY is establishing a more assured base on the 100.000 handle and building momentum through 100.500, albeit with indirect traction from the Euro underperformance noted above and more pronounced Franc depreciation below 0.9700 through 0.9750.

SCANDI/EM – The Scandi Crowns are back on the front foot as crude prices continue to stabilise and sharp falls in Swedish sentiment indicators are acknowledged, but partially taken in context when compared to the starker deterioration elsewhere in Europe. However, in contrast to crude-related recoveries for EM currencies like the Rouble, COVID-19 contagion has intensified in SA where the Rand is back under 19.0000 vs the Dollar in the run up to President Ramaphosa setting out plans to re-open the economy after rolling out fiscal stimulus representing around 10% of the country’s GDP..

In commodities, WTI and Brent front month futures trade on a firmer footing as geopolitical risks continue to be priced in following US President Trump’s tweet regarding his order to the US Navy to shoot down all Iranian gunboats that harass US vessels. Aside from that, the underlying fundamentals remain broadly unchanged. The supply glut remains, and storage space remains scarce. “Given the glut we have in the oil market, it is difficult to see this offering lasting support to the market, unless the situation does escalate further” – ING says. Elsewhere and in fitting with recent source reports, Saudi Aramco has started to implement the OPEC+ pact ahead of its inauguration on May 1st. Aramco will be lower output to 8.5mln BPD, the output level mentioned under the terms of the of the deal – markets are yet to see if other producers follow suit, with Kuwait the only other country to publicly announce their early cuts thus far. WTI resides around USD 15.5/bbl having had briefly topped USD 16/bbl in early trade ahead of yesterday’s high of USD 16.18/bbl. Brent futures meanwhile meander just above 22/bbl after printing a current intraday high at USD 23.22/bbl. Elsewhere, spot gold remains relatively steady north of USD 1700/oz thus far and briefly topped 1725/oz. Meanwhile, copper trades on a firmer footing after Anglo American’s copper production showed a YY decline, meanwhile, Antofagasta also stated it expects copper output this year towards the lower end of its guidance.

US Event Calendar

8:30am: Initial Jobless Claims, est. 4.5m, prior 5.25m; Continuing Claims, est. 16.7m, prior 12m

9:45am: Markit US Manufacturing PMI, est. 35, prior 48.5

9:45am: Markit US Services PMI, est. 30, prior 39.8

9:45am: Markit US Composite PMI, prior 40.9

10am: New Home Sales, est. 644,000, prior 765,000; New Home Sales MoM, est. -15.82%, prior -4.4%

11am: Kansas City Fed Manf. Activity, est. -37, prior -17

DB’s Jim Reid concludes the overnight wrap

This working from home routine is good for productivity if not my social skills. My wife won’t get too close to me at the moment as I refuse to shave off a four week old bristly beard. We’ll see who holds out the longest. On the productivity front we published two quick notes yesterday. The first ( link here ) where we rank the severity of this pandemic relative to 24 we’ve found going back over 2000 years and make some observations of where it’ll end up and also some markers for the future. Secondly we published a chart looking at 150 years of oil prices in nominal and real terms ( link here ). This week the price of oil in nominal terms was lower than it was in 1870 and at any point in history. The note shows what inflation and the S&P 500 have done over the same period for comparison. Guess before you look at the answer. At least how many figures the latter runs into in percentage terms. If anyone can think of a financial related asset that still trades today that had a lower price this week than it did 150 years ago then I will give them a virtual prize. Even if you can think of one from 100 or even 50 years ago.

We’ll come back to oil a little later but the most important event today is the long-awaited European Council summit via videoconference this afternoon, where the big question will be over how the idea of a European Recovery Fund is financed. Yesterday, Bloomberg News reported that the Commission would propose a €2 trillion plan that would in part use the bloc’s 7-year multi-annual budget with a €300bn recovery fund included, but also establish a new temporary financing mechanism that would raise up to €320bn. However, this could prove controversial given the issuance of joint debt, to which the northern member states are strongly reluctant.

Frankly, if we saw a full agreement today that would be a surprise but progress and something that Italy can sign up to will be the key. In his blog on Monday, DB’s Mark Wall said that while he expects an eventual agreement on a recovery fund, it would be a positive surprise if the important details were agreed today, since the question of burden sharing is politically complex and the ECB’s purchases are absorbing market pressure for now. Mark says that the things to watch out for are the size, speed and structure of the fund, but he thinks joint bonds are unlikely for obvious reasons due to the Northern states current lack of desire to go down that route. We’ve also seen increasing speculation around grants recently, which could be the principle means of buying solidarity, but that would also lead to tough debates around the ratio of grants to loans within the Recovery Fund and eligibility for the grants. This would fit into the idea that we shouldn’t expect a fully detailed agreement today.

Ahead of that, sovereign debt continued to sell off in Europe yesterday, though it should be noted that Italian BTPs actually outperformed, with yields falling by -7.7bps by the end of the session. Nevertheless, in the rest of southern Europe sovereign bond spreads moved wider, with the spread of Spanish (+6.3bps) debt over bunds reaching its highest level since the aftermath of the Brexit vote back in June 2016. Having said that they did complete a successful syndicated deal which would have led to pressure elsewhere in the curve – similar to Italy on Tuesday. The ECB last night said it would accept some HY bonds as collateral if they were rated IG before April 7th and stay above BB. This clearly looks designed to mainly help Italy if they get downgraded to HY over the coming weeks or months. Next stop is S&P’s review of their BBB rating due to be announced tomorrow. Finishing off on sovereigns, 10yr Treasury yields rose by +5.0bps yesterday, up from their second-lowest closing level ever the previous day to reach 0.619%.

Staying on today, we’ll also get the much-anticipated April flash PMIs this morning. For our readers who thought that the March readings were dire, today’s numbers are likely to show an even bigger deterioration. That’s because when the surveys were taken back in March, plenty of economies hadn’t actually fully locked down yet, or only did so towards the latter part of the survey. The one country that was in a full lockdown for the March survey was Italy, where the services PMI fell to 17.4, which gives you some idea of how low these could go today. Given that these are diffusion indices they lose some meaning in extreme events as they don’t give a scale of the severity of declines (and rebounds when they occur) just whether things were worse or better than the prior month for the various respondents.

We’ve already had a taste for how the PMIs look in Asia overnight where Japan’s flash services PMI slid to 22.8 (vs. 33.8 last month), a record low, while the manufacturing PMI printed at 43.7 (vs. 44.8 last month). The accompanying text highlighted that “PMI data for Japan tells us that the crippling economic impact from the global coronavirus pandemic intensified in April,” and “the decline in combined output across both manufacturing and services was the strongest ever recorded by the survey in almost 13 years of data collection.” Meanwhile, Australia’s services PMI also printed at a record low of 19.6 (vs. 38.5 last month) while the manufacturing reading came in at 45.6 (vs. 49.7 last month).

In other overnight news, Bloomberg is reporting that Germany’s government has agreed on an additional EUR 10bn stimulus package that would temporarily reduce value added taxes for restaurants and increase the amount of money paid as state wage support as part of a seven-point plan to fine-tune the government’s economic crisis response. Elsewhere, Singapore’s trade and industry minister Chan Chun Sing said that the country is bracing for a sharper economic contraction this year than an earlier forecast of as much as a -4% slump. We also got South Korea’s Q1 2020 GDP print this morning which printed at -1.4% qoq (vs. -1.5% qoq expected), the worst contraction since the GFC. Elsewhere, the US Treasury Secretary Steven Mnuchin said that he expects most of the US economy will restart by the end of August.

Asian markets are trading mixed this morning with the Nikkei (+0.74%), Hang Seng (+0.23%) and Kospi (+0.47%) all up while the ASX (-0.38%) and Shanghai Comp (-0.06%) are in the red. In FX, the Australian dollar is down -0.32% following the PMI data. Elsewhere, futures on the S&P 500 are down -0.42% while yields on 10y USTs are down -1.8bps to 0.603%.

The final expected highlight today comes from the weekly initial jobless claims in the US, which have become an important high frequency indicator over the last month. Over the last 4 weeks, a cumulative total of more than 22m claims have been made, which is around the number of jobs that were created in the decade of expansion. So it’s no exaggeration to call the scale of the declines unprecedented. For today, our US economists are forecasting claims at 5m, which would be down from last week’s 5.245m, and if realised would mark the 3rd consecutive week that the number has fallen, which would suggest we could be past the most rapid period of job losses for now. The S&P 500 rose by +0.58% last Thursday for a 4th successive positive close on multi-million claims day. The previous 3 Thursdays came in at +6.24%, +2.28% and +3.41% for the S&P 500. Will the streak extend for a 5th straight week?

With all that to come later, markets rebounded yesterday following their poor start to the week, with the S&P 500 (+2.29%), the NASDAQ (+2.81%) and the STOXX 600 (+1.53%) all moving higher. Energy stocks led the rebound on both sides of the Atlantic thanks to another day of sizeable swings in oil markets, where Brent Crude managed to pare back its losses from a 21-year low to actually end the session up +5.38% at $20.37/barrel. June and July WTI saw even larger rises, up by +19.10% and +10.70% respectively to $13.78 and $20.69/barrel. June WTI is up a further +4.28% this morning to $14.37. The catalyst seemed to be a tweet from President Trump, who said that “I have instructed the United States Navy to shoot down and destroy any and all Iranian gunboats if they harass our ships at sea.” While geopolitics has rather moved out of the headlines since the start of the year, it’s worth noting that it was only last week that the US Central Command said in a statement that 11 Iranian ships crossed the bows and sterns of US vessels at close range. So one to keep an eye on. In related news, the largest oil-ETF, USO, has altered its fund holdings further away from near-term WTI. The fund has over $3 billion in AUM and is the largest single-holder of WTI futures according to Bloomberg. The ETF will now roll exposure to August and September, while lowering June and July, in order to shield itself from the price action in near-term contracts. Oil ETFs have been a hot topic over the last couple of days given the recent turmoil. When these were structured no-one could have contemplated a negative price on the contracts they invested in. It’s fair to say it’s caused some chaos.

There wasn’t a lot in the way of data yesterday, though we did get the European Commission’s advance consumer confidence reading for April, which plummeted to -22.7, its lowest level since March 2009. Otherwise, we got February’s FHFA house price index for the US, which saw a +0.7% increase month-on-month before the impact of the pandemic began to be felt. And in the UK, the CPI reading for March fell to 1.5% as expected, down from 1.7% in February.

Corporate earnings were mixed again. Chipotle Mexican Grill (+12.44%) rose after 1Q digital sales grew over 80% yoy and EPS came in well ahead of analyst’s estimates at $3.17 vs. $3.08 expected. Heineken (-3.05%) cancelled its interim dividend, while volumes were down 14% and net income fell 69%. Kering (-4.92%) announced on its earnings call that it doesn’t expect a recovery in the U.S. or Europe before at least June or July, while sales at its brand Gucci tumbled 23% year-over-year. The company did announce that sales in mainland China turned positive this month as tourist spending rose.

To the day ahead now, and along with the aforementioned European Council meeting, PMIs and initial jobless claims from the US, other data releases include Germany’s GfK consumer confidence reading for May, the UK’s public sector net borrowing for March, along with the US new home sales for March and April’s Kansas City Fed manufacturing activity index. From central banks, we’ll hear from the BoE’s Vlieghe, while earnings out today include Intel, Eli Lilly and Company, NextEra Energy and Union Pacific.

“In a time of universal deceit – telling the truth is a revolutionary act”

Trump is not a complete fool. He knows enough to move oil prices up. Threaten to start a war in the Middle East. Works every time..! Sure enough stocks followed higher.

But, even St George would struggle to slay the microscopic dragon at the core of this unfolding crisis. Just a few months ago none of us foresaw just how deep the downturn the COVID virus triggered could possibly go. In early Feb I suggested we faced an economic hit similar to the SARs epidemic – a $40 bln hit to the global economy, and a 16% slide in markets. I massively underestimated.

There are a number of brutal realities:

1) We still don’t know how much deeper the Virus will dig. The news is very mixed – the first wave is apparently passing in Europe and US, but there are still doubts on subsequent waves, and uncertainty about renewed infections around the globe. Lockdowns are being extended. The social distancing and lockdowns that have trounced the global economy in the short-term aren’t going to end overnight. They are set to continue with only limited easing – for months, maybe through the year. We just don’t know – which means the real economic damage continues to escalate.

2) Don’t look to Global Markets for guidance – they are detached from the economic reality because of renewed financial distortions from QEI (QE Infinity) govt supports and bailouts. There is still an element of denial in markets – but sentiment is beginning to shift as the evidence mounts. A host of indicators such as the rate of downgrades to upgrades being nearly 10/1, central banks buying Fallen Angel junk, and mandatory dividend cuts – all point to rising crisis. (There are still sound investment opportunities out there – but prices are seriously distorted.) The number of recommendations to buy gold is soaring – a sure sign of trouble.

Readers might be wondering why the authorities are apparently conniving at the market’s extraordinary levels? Why do they appear so keen to bail markets and maintain the illusion of normality?

That’s a story of consequences and pensions..

This story began back in 2008 when central banks, bank regulators and frustrated politicians played the blame game on the Global Financial Crisis. It was decided it was the banks who’d been at fault, but since governments now owned the banks and crisis had conclusively demonstrated the importance of banks within the global economy, they embarked on a programme to de-risk banks and their importance in the system. Remember all these promises about separating banks from investment banking, no bank being too big to fail, SIFIs and other such gibberish?

As a result, the most important trend of the last 12 years has been the transfer of risk from the then fragile banking systems to the wider, more diverse and less individually systemically important asset management sector. Converting bank credit risks into corporate bonds was one aspect. That risk is now largely held by asset managers is just one factor. Others included the rise of alternative lenders to SMEs, packaging receivables, debts, loans into formats asset managers could buy. Junk debt packaged as CLOS anybody?

Guess where all the risk now resides?

There was a time when banks had whole floors, even buildings, full of credit officers busily doing the calculations on lending risks. They were supported by networks of bank managers, sector specialists and analysts who lived, breathed and understood every aspect of bank lending risk within the economy.

Today’s risk management department of a mid-sized asset manager is likely to be a small number of very clever accountants, who are massively underpaid in comparison to the front office Portfolio Managers.

These guys are managing our future financial security.

Over the last 12 years we’ve seen massive inflation in financial assets – stocks and bonds – as a result of financial repression, QE and ultralow interest rates. The last thing the Authorities can contemplate now is a collapse or reset in financial asset prices. While incomes remained flat through the last decade, most Boomers and Gen Xers approaching retirement were placated and encouraged by the growth of their pension pots (missing the fact the asset management business have actually creamed off most of the appreciation of their financial assets as fees..).

If markets collapse, and financial asset prices reset.. the Government are going to face very angry voters who will literally have lost their retirement pots, and a massive ongoing future debt burden.

Here in the UK we are already moving to a future where £1.10 in every pound of tax collected by government will be going towards paying Civil Service and State pensions. (Yes, it means the government will be borrowing more and more.) You could argue that doesn’t matter under Modern Monetary Theory. But it does. The numbers will become even less sustainable if all the private self-saving pension schemes collapse, leaving a growing population of destitute elderly retires to care for.

This spawns enormous challenges for governments:

What are the implications and limits of unbounded Modern Monetary Theory on economies, inflation and currencies? Can some nations simply write off the balance of National Debt held by central banks as a result of QE? Do taxes matter? What will monetary creation trigger in terms of inflation? How will FX markets react to burgeoning debt and inflation?

It’s going to be ever tougher for Europe – which has pretty much agreed already that today’s crisis meeting will simply keep kicking the can down the road. (I suspect the acceptance of fallen angels as collateral is anticipating the possibility S&P downgrades Italy to Junk tomorrow.) They are still coping – badly – with implications of the deeply flawed single currency, and the ultimate riddle remains:

How does the consensual committee government of the EU deal with the crisis of avoiding economic shutdown by mutualising debt in a community that won’t accept it?

The situation is likely to get even more difficult.

The planet is now headed into de-facto global recession – with a very strong likelihood it turns into a deepest and sustained global depression on record. The degree to which governments around the globe are ditching every vestige of monetary and fiscal orthodoxy to sustain economic activity is astounding. Some will succeed, but many will fail – re-ordering the global economy for when it eventually recovers. The consequences in terms of social, political and geopolitical outcomes could be enormous.

If it goes wrong we face social unrest, revolutions and, because all the environment, over-population, and poverty issues remain, don’t rule out an escalation of resource driven wars.

The confusion and complexity of this crisis is truly extraordinary. But like most things – here in the West we will probably muddle through.

“Unprecedented Damage To The Euro Zone” – European PMIs Hammered By Record Collapse

Economic activity across the eurozone ground to a halt this month as the new coronavirus sweeping across the world forced governments to impose lockdowns and firms to down tools and shut their businesses.

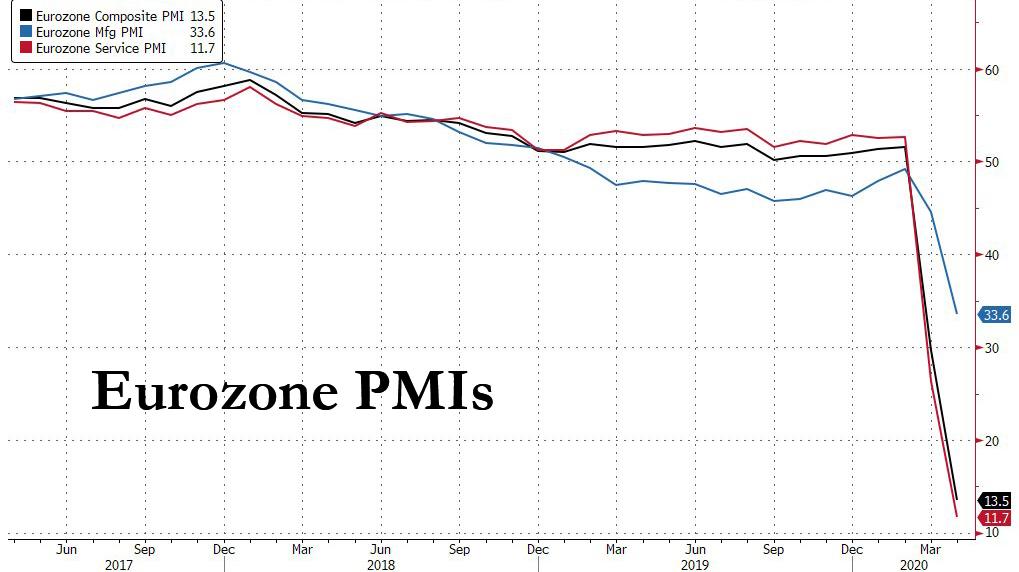

The latest monthly PMI manufacturing and service surveys illustrated the severity of the crash in economic activity across Europe and the UK, as lockdowns stifle businesses from Paris to Frankfurt. Overall, the eurozone composite purchasing manager’s index – which monitors manufacturing and services activity – fell to 13.5 in April, from 29.7 in the previous month, a record low in more than 22 years of the history of the survey, and blow even the lowest estimate of 18.0. The manufacturing component tumbled from 44.5 in March to 33.6 in April, below the 39.2 expected, but it was the collapse in Services that was shocking, collapsing more than 50% from 26.4 to 11.7.

According to Markit, demand all but dried up this month, headcount was reduced at a record pace and firms cut prices at one of the steepest rates since the survey began.

“April saw unprecedented damage to the euro zone economy amid virus lockdown measures coupled with slumping global demand and shortages of both staff and inputs,” said Chris Williamson, chief business economist at IHS Markit.

“The ferocity of the slump has also surpassed that thought imaginable by most economists.”

Williamson said the PMI was consistent with the European GDP contracting 7.5% this quarter. A Reuters poll published on Wednesday had a 9.6% contraction pencilled in. Unsurprisingly therefore, optimism was also at a survey low. The future output sub-index, which almost halved last month, was 34.5.

With restaurants, bars and other leisure activities shuttered, holidays cancelled and travel restricted the situation in the bloc’s dominant services industry was dire. The flash services PMI sank to a new record low of 11.7 from 26.4.

A new business index dropped to a record low of 11.6 from 24.0, and firms completed outstanding demand at the fastest rate in the survey’s history. April is also proving to be a grim month for the bloc’s factories.

The preliminary manufacturing PMI dropped to a survey low of 33.6 from March’s 44.5. An index measuring output, which feeds into the composite PMI, more than halved to 18.4 from 38.5. Demand was barely existent and with many of their factories closed, manufacturers cut staffing levels sharply. The employment sub-index fell to 35.7 from 44.3, its lowest since April 2009, around the start of the euro zone debt crisis.

“In the face of such a prolonged slump in demand, job losses could intensify from the current record pace and new fears will be raised as to the economic cost of containing the virus,” Williamson said.

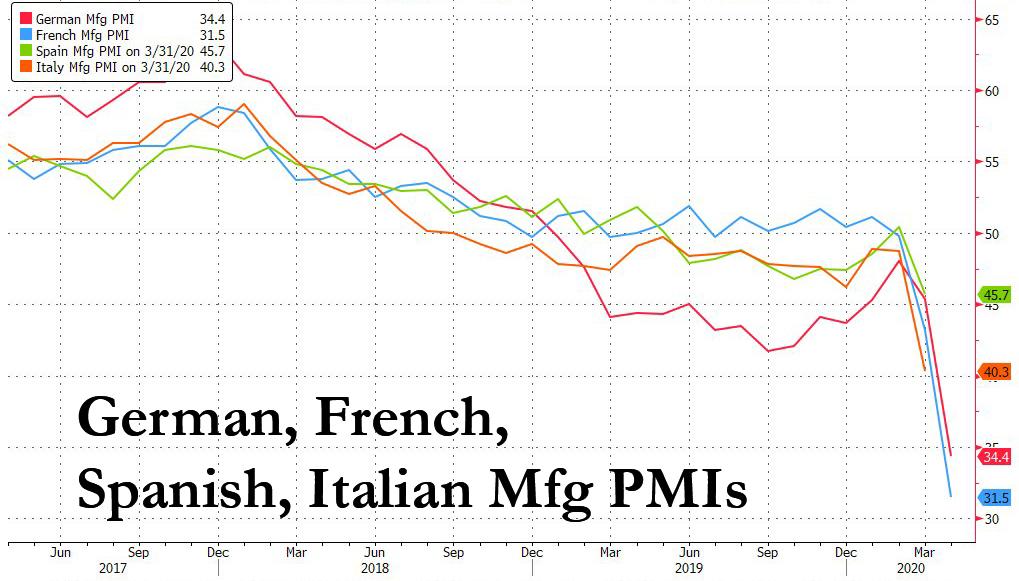

Earlier, French and German business activity also fell to record lows, in readings that suggest the region faces a major economic downturn, with manufacturing hit hard …

… but once again it was Services that were crushed as virtually all of the continent was put on lockdown.

As can be seen above, business in Germany – the eurozone’s economic powerhouse – crashed this month, following France in recording its lowest readings of services and manufacturing activity on record. The IHS Markit flash purchasing managers’ index for services fell to 15.9 in April from 31.9 in March, the lowest since record began more than 22 years ago as about three-quarters of companies reported a fall in activity.

The index for manufacturing output also dropped to a record low at 19.4 in April, from 41 in the previous month. The IHS composite index, an average of services and manufacturing fell to 17.1 in April, also a record low. April’s PMI surveys show “business activity across manufacturing and services falling at a rate unlike anything that has come before,” said Phil Smith, principal economist at IHS Markit.

Summarizing the catastrophic data, economist Daniel Lacalle said that “the collapse is much larger than expected and the largest ever seen. With most of the stimuli aimed at the wrong areas of the economy (mostly zombie states and enterprises) while keeping high taxes and regulatory burdens, the recovery will be long and painful.”

Shocking New Data Show 90% Of COVID-19 Patients On Ventilators Won’t Survive: Live Updates

Just 48 hours before Georgia was set to become the first state in the country to start reopening its economy, President Trump revealed in what sounded like an offhanded answer to a reporter’s question that he “strongly disagrees” with Gov Kemp’s decision because it didn’t follow the federal guidelines.

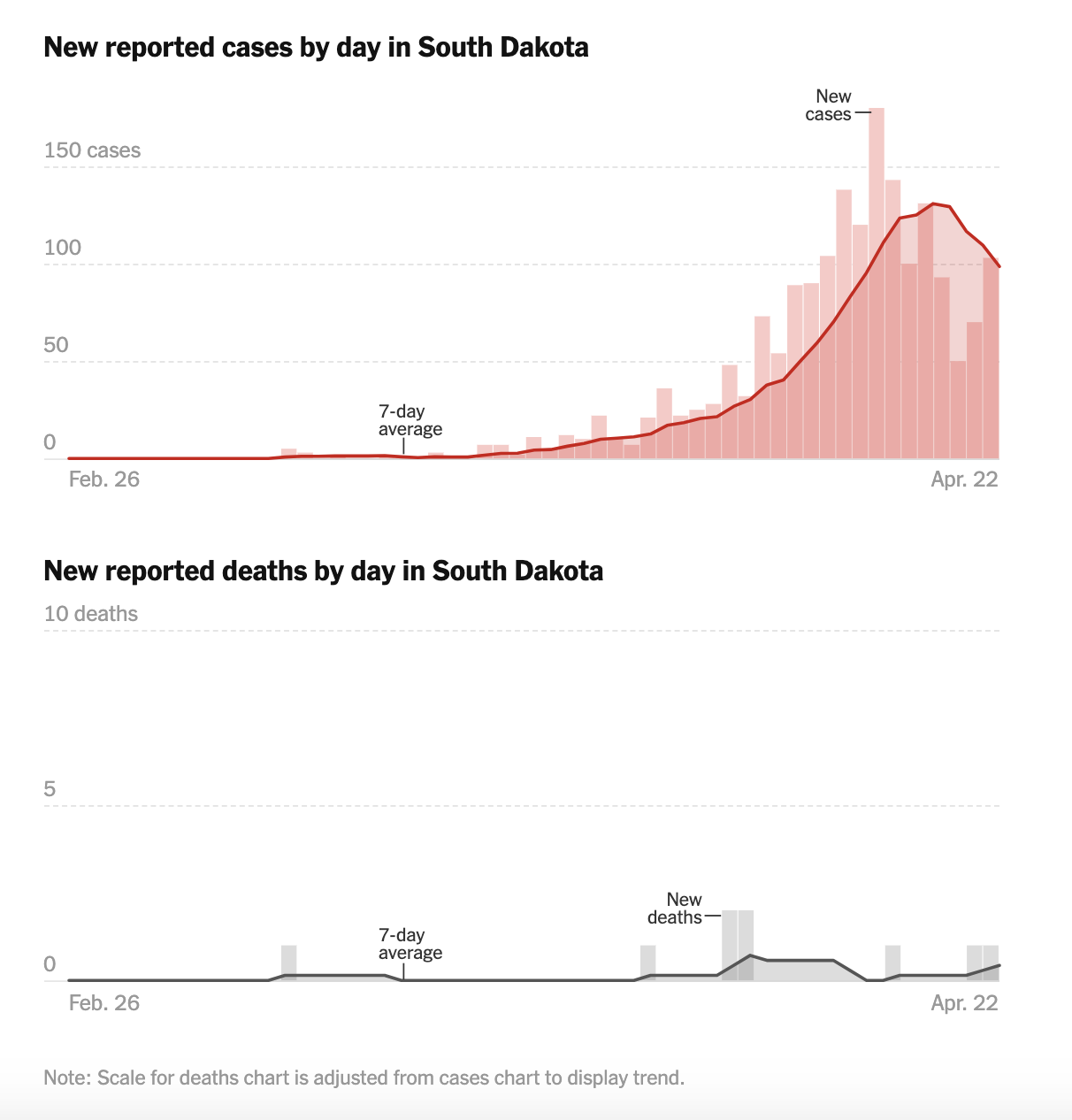

Trump’s u-turn outraged some supporters who believe the lockdown “cure” is worse than the viral “disease”, just in time for the latest reminder of how many jobs have been destroyed by the pandemic so far. Before blaming them as “covidiots”, it’s worth remembering that many red states haven’t been hit nearly as badly as most other states. Even the outbreak at the Smithfield Food’s processing plant in South Dakota – an incident that the MSM labeled “the biggest outbreak in the country” and cited as evidence of GOP Gov. Kirsti Noem’s “anti-science” agenda – has already subsided, and the rate of new cases has slowed, and the state has only recorded 9 deaths.

Millions of people around the world are beginning to question the wisdom of strict lockdown strategies. Sweden, a country that was once routinely bashed by conservatives for refusing to close its economy and borders, has found that its approach appears to be working. As once doctor who appeared on CNBC Thursday morning pointed out, the number of deaths and cases per capita in Sweden is higher than its neighbors. But not by much. For the record, Sweden has left its schools, gyms, cafes, bars and restaurants open throughout the spread of the pandemic. Instead, the government has urged citizens to act responsibly and follow social distancing guidelines. The country has suffered fewer than 2,000 deaths, and has only confirmed 16k cases, and the strategy has proved broadly popular: Swedish Prime Minister Stefan Lofven is now one of the most popular leaders in the modern history of Sweden.

To be sure, even Lofven has admitted that Sweden made mistakes – for example, authorities should have invested more resources in protecting the elderly – and when deaths and cases started to spike a few weeks ago, there were a few uncomfortable days when he faced a hail of doubt and criticism. But he stayed the course, and the country appears to be emerging from the pandemic relatively unscathed. In what is perhaps the country’s biggest sign of renewal, Volvo, which was forced to halt production across Europe and furlough about 20,000 Swedish employees, will resume production at its Swedish plants on Monday.

Earlier this week, the mainstream press flew into a tizzy following a report that a leading American vaccine expert named Rick Bright had been ousted as director of the Biomedical Advanced Research and Development Authority, allegedly for resisting efforts to join President Trump in pushing hydroxychloroquine. A recent small-scale VA study recently found the drug to be ineffective, news that liberals have weaponized to bash the president, after dismissing virtually every other study suggesting the opposite (particularly when the drug is taken in combination with a Z-Pak).

As it turns out, Bright’s claim that his ouster was an act of retaliation for not “toeing the line” turned out to be somewhat embellished.

Possible for several things to be true:

— Trump’s push on malaria drugs was inappropriate

— That push alarmed health officials like Bright

— But some of those officials sent mixed messages about it

— Efforts to oust Bright predated Covid-19, as officials told me months ago

In the UK, where daily death numbers have remained stubbornly, the government’s top medic said Thursday that restrictions on everyday life in Britain will likely remain in place in one form or another until the “next calendar year” due to the time needed to develop and roll out vaccines or find a cure, the country’s top medic said on Wednesday.

South Korea, meanwhile, is already preparing for a second wave of the virus in the fall and winter, according Yoon Tae-ho, director general of health ministry, who announced the plans during a press briefing. Many public health experts – including FDA Director Dr. Stephen Hahn, before he “clarified” his statement the other day – have warned that the virus could come roaring back in the fall, combining with the seasonal flu to overwhelm hospitals once again.

The country also plans to secure more medical resources in the event of a bigger outbreak than what it experienced in Daegu, the city at the epicenter of the crisis. SK will continue to remain “on alert” until a vaccine is available.

Indonesia reported 357 new cases of the virus, bringing its total to 7,775. The country has reported a total of 647 deaths and 950 recovered cases, numbers that experts say are likely well short of the totals for both cases and deaths.

US Secretary of State Mike Pompeo called on China to permanently close all wet markets and other illegal markets selling wildlife for human consumption – something that China has already technically outlawed, just like they ‘outlawed’ the production of black-market fentanyl.

As more countries begin rolling back lockdown measures, tiny Vietnam, which has reported fewer than 300 cases of coronavirus and no deaths since the first infections were detected in January, said on Wednesday it would start lifting tough movement restrictions, according to Reuters, even as many of its neighbors remain on lockdown. Greece extended its lockdown until May 4, but said some small businesses will start reopening after that date, per the FT. A spokesman for the Greek government warned that “at each stage the impact on public health will be assessed. We’re going to take it week by week,” he added. A detailed timetable for re-starting the economy will be announced next week.”

More countries appear to be reopening as millions confront the undeniable reality that, when faced with the choice of sacrificing their livelihoods or risking infection, most people would opt for the second, even as the WHO’s Dr. Tedros warned during a press briefing on Wednesday that the rolling back the quarantines too soon might cause the virus to reignite.

The situation in Russia, which took early steps to keep foreigners out yet never followed up with widespread testing and surveillance, continued to worsen as the country reported 4,774 new cases of coronavirus and 42 new deaths, another record number of new cases, bringing the country’s total of 62,773 cases and 555 deaths.

Perhaps the biggest news overnight came out of Australian, where PM Scott Morrison called on all member states of the WHO to support an “independent review” of the origins of the novel coronavirus outbreak, further jeopardizing what has been an incredibly prosperous economic relationship with China that had helped the Aussie economy achieve an unprecedented 30-year stretch of growth.

Finally, the Washington Post reports that new data from New York’s largest hospital system showed that survival rates for patients placed on ventilators are even lower than previously believed. The data showed that a staggering 88% of coronavirus patients who were placed on ventilators in the state’s hospitals didn’t survive. Doctors, meanwhile, are also seeing more strange complications from the disease involving blood clots and the cardiovascular system. One doctor in China who barely survived his struggle with the virus experienced an extremely strange shift in skin pigmentation.

This news follows yesterday’s report which found more than 10,000 nursing home residents in 35 states have succumbed to the virus, representing roughly one-fifth of all deaths in the US.

The number of confirmed deaths from the virus around the world is approaching 200k, while the number of confirmed cases has surpassed 2,645,000.