Just as we saw last week, this week’s vaccine news has prompted a positive response across cyrptocurrencies with Bitcoin soaring above $17,000…

Source: Bloomberg

…for the first time since Jan 2018.

Source: Bloomberg

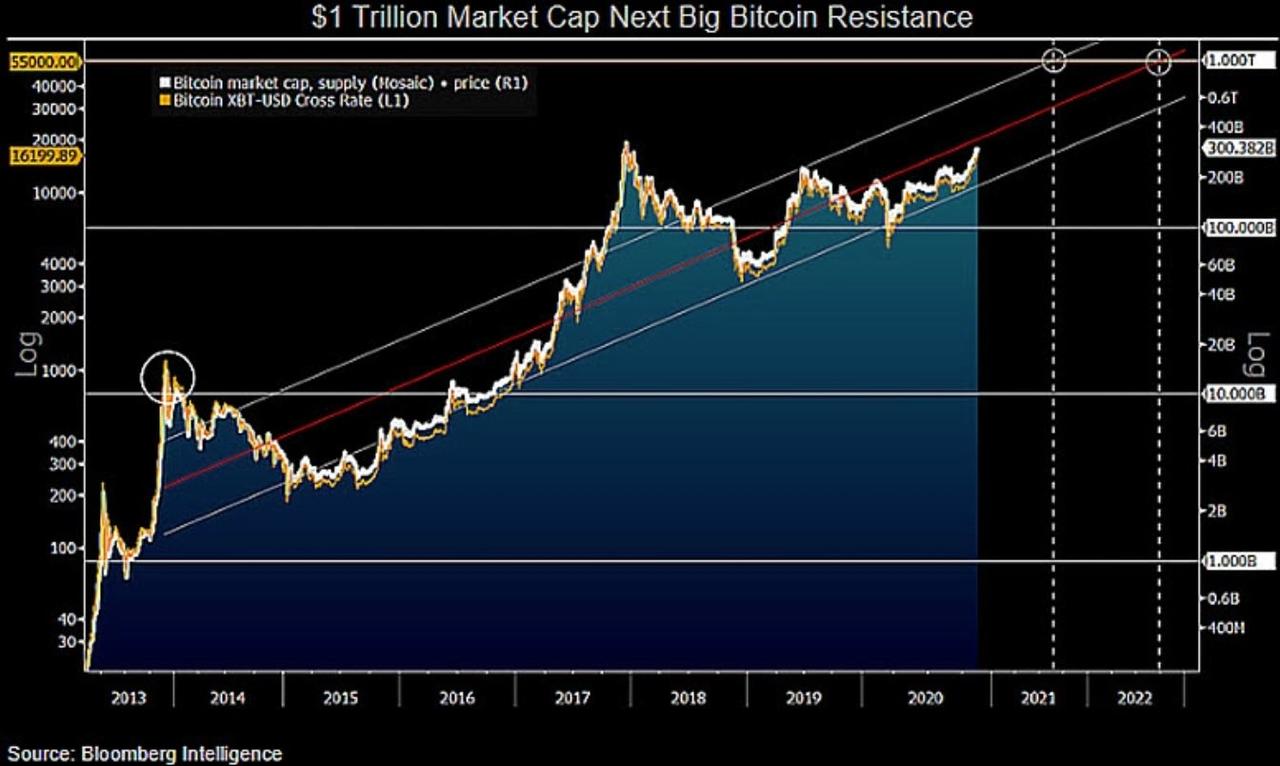

And as CoinTelegraph’s William Suberg reports, Bitcoin hitting its all-time highs of $20,000 again is not the end but the start of its explosion to a $1 trillion asset, a senior Bloomberg analyst said.

In a tweet on Monday, as BTC/USD reclaimed $16,000, Mike McGlone, senior commodity strategist at Bloomberg Intelligence, delivered a fresh bullish forecast for the largest cryptocurrency.

Bloomberg Intelligence: BTC will keep rising in 2021

Bitcoin saw lower levels over the weekend, briefly dipping to $15,800 before conspicuously rising on Monday to see highs of $16,400 at press time.

“$20,000 #Bitcoin Is Primary Hurdle Toward $1 Trillion Market Cap — The digital version of #gold but with more-limited supply and a history of adding zeros, appears to be in an early price-discovery stage and may simply continue its ascent in 2021,” McGlone wrote.

“Mainstream adoption is rising.”

Bitcoin market cap vs. price historical chart. Source: Mike McGlone/ Twitter

An accompanying chart described a $1 trillion market capitalization as the “next big resistance” for Bitcoin.

McGlone is known for his increasingly positive Bitcoin outlooks. As Cointelegraph reported, he argued in September that Bitcoin should, in fact, trade at $15,000 based on active addresses, something which soon became reality.

Brandt signals bull run still in early stages

McGlone is far from the only markets veteran doubling down on the lucrative prospects for Bitcoin in its current bull run.

On Monday, trader Peter Brandt suggested that based on previous bull runs from 2013 and 2017, the current price performance was only the start of the cycle.

“During the 2015–2017 bull market in Bitcoin $BTC, there were 9 significant corrections with the following averages: 37% decline from high to low, 14 weeks from one ATH to the next ATH,” he explained.

“Since the early Sep low there have been two 10% corrections.”

Peter Brandt’s highlighted Bitcoin bull run characteristics chart. Source: Peter Brandt/ Twitter

Statistician Willy Woo likewise believes that there is far more mileage left in the current uptrend. His argument was based on Bitcoin’s relative strength index (RSI), which he described as “just warming up.”

Beyond Bitcoin circles, a Citibank market analyst this week announced that he foresaw a $318,000 Bitcoin price by December next year.

via ZeroHedge News https://ift.tt/38RCznO Tyler Durden

Global Stocks Slide As Attention Turns To Global Economic Shutdowns Tyler Durden

Tue, 11/17/2020 – 08:12

Monday’s global stock rally unleashed by a 2nd round of covid vaccine hopes this time courtesy of Moderna, and which pushed the Dow and all major indexes to new record highs, fizzled on Tuesday as investors shifted focus back to the accelerated near-term spread of the virus and the creeping shutdowns which are certain to hammer the US economy. S&P futures dropped 0.5% or 20 points as New Jersey, California and Iowa imposed fresh restrictions as the number of new US cases hit a record, and threatened to worsen as the colder weather sets in. Nasdaq 100 futures were boosted by yet another reversal in the reflation trade, as well as a jump in Tesla on the prospect of the electric-car maker’s shares joining the S&P 500.

Curiously, the same 3,600 “gamma wall” level which we warned yesterday would complicate a major push higher in the S&P ahead of op-ex, is now serving as a buffer to the downside, and will limit losses. Sure enough, the Emini session low so far today has been… 3,600.

S&P 500 futures slid a day after the underlying benchmark closed at an all-time high on news that Moderna’s vaccine was shown to be 94.5% effective. Drug retailers such as Walgreens Boots Alliance tumbled 10%, while CVS Health Corp fell 6.4% after Amazon launched an online pharmacy for delivering prescription medications in the U.S.

“We might be transitioning from a defensive bull market to a more cyclically offensive one but more clarity is required in terms of when social mobility will normalize,” said Chris Iggo, chief investment officer of core investments at Axa Investment Managers. “The euphoria created by the presidential election result and the vaccine announcement will give way to a more sober analysis of how long and smooth the road to recovery will be.”

Not everything was red: Tesla soared 12.4% premarket in anticipation of a $51 billion trade by index funds adjusting their holdings when the company is added to the benchmark S&P 500 in December. At $400 billion, Tesla’s market capitalization is a hundred times that of the S&P’s smaller companies, according to Refinitiv data, making it the biggest ever addition to the index.

In Europe, the Stoxx 600 Index slipped 0.4% by 7:45 am ET, following a sharp drop to session lows just after 6am, with travel shares and banks leading the decline. S&P 500 futures pointed to a small drop at the open, the 10-year Treasury yield was at 0.895%, oil held over $41 a barrel and gold was broadly unchanged.

Earlier in the session, MSCI Asia Pacific Index added 0.2% led by the finance and energy sectors, while Japan’s Topix index closed 0.2% higher. Most Asian markets were up, with Singapore’s Straits Times Index advancing 1.1% and Indonesia’s Jakarta Composite rising 0.6%, although China’s Shanghai Composite slid 0.2%. Trading volume for MSCI Asia Pacific Index members was 15% above the monthly average for this time of the day. The Topix added 0.2%, with MUFG and Tokio Marine contributing the most to the move. The Shanghai Composite Index retreated 0.2%, driven by Kweichow Moutai.

In FX, the pound led gains among G-10 currencies on optimism of a Brexit breakthrough, rising for a third day, followed by the Swiss franc and Japanese yen. The Bloomberg Dollar Spot Index fell for a third consecutive session, to touch more than a one-week low, as the greenback fell against almost all Group-of-10 peers; the euro advanced after briefly dipping below $1.1850. Yield curves in Australia and New Zealand bear steepened amid speculation that funds may be shifting from these markets to Treasuries. China’s yuan strengthened to the highest level since June 2018, fueled by optimism over the country’s economic recovery and its interest-rate premium over the rest of the world.

In rates, Treasury futures held small gains as the U.S. trading day began after erasing earlier declines, leaving yields richer by about 2bp at long end of the curve. Yields were little changed at front end of the curve, flattening 2s10s, and 5s30s by 1bp-2bp; 10-year around 0.89% is richer by 1.8bp, outperforming bunds and gilts by 1bp to 1.5bp. The rates market is underpinned by weakness in S&P 500 futures following Monday’s equity rally. Deal flow is in focus with Saudi Aramco setting initial spread guidance on a five-tranche jumbo bond sale.

In commodities, WTI crude oil hovered around $41 a barrel. Gold was modestly higher, trading at $1,889/oz last.

On today’s calendar, data highlights include October’s retail sales, industrial production and capacity utilisation, as well as the NAHB housing market index for November. Earnings releases include Walmart and Home Depot. Fed Chair Jerome Powell speaks while four regional Fed presidents take part in a virtual conference on racism and the economy. The Senate will hold a procedural vote on Fed nominee Judy Shelton. September TIC flow data is released at 4:00 p.m. The OPEC+ joint ministerial monitoring committee meets, and Facebook Inc. and Twitter Inc. CEOs testify before the Senate. We’ll hear from a number of central bank speakers including ECB President Lagarde, BoE Governor Bailey and Deputy Governor Ramsden, and the Fed’s Bostic, Daly, Kashkari, Rosengren and Barkin.

Market Snapshot

S&P 500 futures down 0.4% to 3,609.00

Stoxx Europe 600 down 0.05% to 389.55

MXAP up 0.2% to 188.08

MXAPJ up 0.05% to 620.99

Nikkei up 0.4% to 26,014.62

Topix up 0.2% to 1,734.66

Hang Seng Index up 0.1% to 26,415.09

Shanghai Composite down 0.2% to 3,339.90

Sensex up 0.7% to 43,946.93

Australia S&P/ASX 200 up 0.2% to 6,498.21

Kospi down 0.2% to 2,539.15

German 10Y yield fell 0.4 bps to -0.549%

Euro up 0.1% to $1.1868

Brent futures up 0.7% to $44.12/bbl

Italian 10Y yield fell 1.3 bps to 0.541%

Spanish 10Y yield fell 0.8 bps to 0.091%

Brent futures little changed at $43.82/bbl

Gold spot up 0.2% to $1,891.94

U.S. Dollar Index down 0.2% to 92.42

Top Overnight News from Bloomberg

French bars and restaurants will remain closed until mid-January as the government tries to stem the resurgent coronavirus outbreak, France Info radio reported, as officials weigh when to allow shops to reopen

The OPEC+ oil alliance should consider delaying its planned output boost by between three and six months, a technical panel that advises ministers suggested

Currency markets are back in the spotlight for investors punting on the global economic outlook after the pandemic. Given the progress in developing an effective coronavirus vaccine, risk appetite is making a strong comeback. It’s driving trade-sensitive currencies such as the Australian dollar toward fresh highs, while havens like the Japanese yen and the Swiss franc are feeling the heat

U.K.’s chief Brexit negotiator David Frost told Prime Minister Boris Johnson to expect a trade deal with the EU as soon as Tuesday, The Sun reports, without attribution

Boris Johnson should consider “strengthening” regional coronavirus restrictions after England exits its second national lockdown next month, a senior government medical adviser said

Singapore Prime Minister Lee Hsien Loong said U.S. President-elect Joe Biden should seek constructive ties with China following “quite a tumultuous ride” over the past four years

Chinese Vice President Wang Qishan called for global solidarity and a shift away from protectionism as his nation prepares for a Biden administration

Federal Reserve Vice Chairman Richard Clarida said prospects for the economic recovery were brightening due to progress in the development of vaccines to fight the Covid-19 pandemic

RBA’s November meeting minutes showed that the central bank decided to inject further monetary stimulus into the economy as it became clear that unemployment would stay high and inflation remain subdued for an extended period

A quick look at Global markets courtesy of NewsSquawk

Asian equity markets were somewhat indecisive and only mildly benefitted from the performance on Wall St where both the S&P 500 and DJIA posted record levels and cyclicals outperformed on vaccine optimism following the encouraging update regarding Moderna’s Phase 3 vaccine trial. ASX 200 (+0.2%) and Nikkei 225 (+0.4%) were both lifted at the open as energy and financials resumed the cyclical-led surge in Australia, while the Japanese benchmark rallied to above the 26k level to print its highest since May 1991 but then reversed course and briefly gave back all its gains as risk appetite waned. Elsewhere, the Hang Seng (+0.1%) and Shanghai Comp. (-0.2%) were mixed with underperformance in the mainland following a liquidity drain by the PBoC and as US-China tensions lingered with China’s Global Times Editor recently warning that China will ignore some of the Trump administration’s political stunts but will resolutely hit back for attacks that might cause real harm, while it was also reported that Huawei is to sell its Honor brand to ensure its survival amid the US crackdown. Finally, 10yr JGBs were flat amid the tentative gains in stocks but with downside stemmed after recently finding support at the 152.00 level, while the BoJ’s presence in the market for over JPY 1.3tln of JGBs with 1yr-10yr maturities did little to spur prices.

Top Asian News

Courier Giant SF Express Is Said to Mull Share Sale in Hong Kong

DBS to Allow Employees to Work Remotely for up to 40% of Time

Philippine Central Bank Reduces Government Bond Purchases

Southeast Asia’s Virus Hotspot Counts on Early Vaccine Rollout

European equities have kicked the session off with marginal losses (Eurostoxx 50 -0.5%) as markets take a breather from yesterday’s Moderna-inspired gains with little in the way of incremental newsflow since Monday’s close. Sectors are mostly lower on the session with cyclicals such as oil & gas, banks and travel & leisure lagging peers. The latter has been dragged lower easyJet (-2.4%) after the Co. posted a FY loss of GBP 1.27bln and noted that it is expecting to fly no more than 20% of planned capacity in Q1 2021. For banking names, besides the broader thematic moves at play this morning, BBVA (-4.6%) are a standout underperformer after noting it is in merger talks with Sabadell (+6.4%), accordingly, the IBEX 35 (-1.3%), of which BBVA accounts for 7.6% in weighting terms, is trailing its peers. Elsewhere, early strength in European tech names has somewhat abated with the sector roughly unchanged on the session, however, stateside the e-mini Nasdaq 100 (+0.2%) outperforms peers (e-mini S&P -0.5%, e-mini Russell 2000 -0.7%) as the ongoing rotation into cyclical/value companies pauses for breath. Tesla (+12% pre-market) are likely exerting some influence on this front with shares set to open firmer amid news that the Co. is set to join the S&P 500 prior to the open on December 21st. Corporate updates from Europe have been on the lighter side this morning as earnings season draws to a close with the one of the main standouts for the session being Imperial Brands (+6.1%) with shares higher post FY earnings and outlining a more upbeat outlook for 2021.

Top European News

Italy’s Government Signs Off on 38 Billion-Euro Aid Package

France’s Bars, Restaurants May Stay Closed Until Mid- January

Pound Seen Falling 5% if U.K. Trade Talks With EU Go Nowhere

Merkel Sees German Recovery Accelerating Once Virus Is Tamed

In FX, the Yen is leading the G10 charge against the Buck and having another look at offers ahead of the 104.00 level after tripping stops around 104.34 according to market contacts, but YUAN gains are even more pronounced as the Cnh and Cny extend their rallies towards 6.5450 and 6.5500 respectively from another solid PBoC platform overnight. Elsewhere, the Franc has rebounded further to retest 0.9100 despite further physical and verbal intervention from the SNB and Euro has also shrugged off latest ECB qualms about moves vs the Greenback to clear 1.1850 on the way to circa 1.1875. However, Eur/Usd may yet be drawn to a hefty option expiry at the half round number (2.1 bn) if not decent interest at 1.1830 (1 bn) and a more concerted attempt to reach 1.1900 could be repelled by expiries at the strike (1.1 bn). Meanwhile, the Aussie appears to have taken RBA minutes in stride given no additional policy guidance from last week’s post-meeting statement, but Aud/Usd has piggy-backed the Renminbi and gleaned traction on the 0.7300 handle from closer ties between Japan and Australia to compensate for ongoing strains with China. Similarly, Sterling is deriving momentum above 1.3200 and through 0.9000 in Eur/Gbp terms on positive sounding Brexit reports in the UK media, with chief negotiator Frost briefing PM Johnson about a potential deal by next Tuesday and an EU diplomat suggesting a willingness to be creative in finding a deal to avoid an accidental no deal scenario.

DXY/CAD/NZD – Given all the advances noted above, the Dollar index is holding up relatively well, albeit in a lower 92.614-372 range compared to Monday awaiting some top tier US data in the form of retail sales and ip before another raft of Fed speakers. Moreover, the Greenback has clawed back some lost ground against the Loonie and Kiwi amidst a dip in broad risk sentiment following yesterday’s Moderna vaccine boost, with Usd/Cad straddling 1.3075 and Nzd/Usd pivoting 0.6900 in the run up to Canadian housing starts and wholesale trade and NZ PPI.

SCANDI/EM – The Norwegian Korona is keeping pace with the Euro in wake of encouraging GDP updates rather than a deterioration in consumer sentiment, but other oil and commodity currencies are not coping with crude prices retreating from recent highs or the aforementioned waning risk appetite, as the Turkish Lira and SA Rand look forward to CBRT and SARB rate decisions on Thursday.

In commodities, WTI and Brent have experienced a choppy European morning as participants prepare for today’s JMMC meeting in otherwise relatively quiet price action thus far. Currently, WTI and Brent are pivoting around the U/C mark with a range of USD ~0.50/bbl thus far. The OPEC JMMC gathering is scheduled to commence from around 13:00GMT/08:00EST today. Yesterday’s JTC event concluded that most countries support a 3-month extension of the current cuts according to sources; such a decision would imply a production reduction level of 7.7mln BPD throughout the Q1 and as such would be relatively in-line with the source reports prior to the COVID-19 vaccine updates. Subsequently, Energy Intel has reports that JMMC delegates are said to be looking to recommend an extension of 3-6 months at current quotas. Given these updates attention throughout the session will be on how closely the final JMMC recommendation adheres to these reports and how the Committee intends to address the likely mid-term improvements on the demand front given COVID-19 vaccine updates. While on the supply side Libya’s increasing output is a possible concern particularly as they have intimated they will not comply with OPEC+ quotas until production hits 1.6mln BPD. As a reminder, the JMMC can only make policy recommendations and cannot implement policy changes themselves – with attention on the end-of-month OPEC/OPEC+ gatherings for any such alteration which would require unanimous consent to be passed. Moving to metals, spot gold is relatively unchanged on the session with the metal following and as such exhibiting similar action to the range-bound USD this morning. Currently, the yellow metal is just shy of the USD 1890/oz mark and towards the lower-end of the day’s range. Elsewhere, UBS believes palladium prices will rise to USD 2600/oz in 2021 given vaccine updates, strong China auto sales and a general recovery in global economic activity assisting the metal.

US Event Calendar

8:30am: Retail Sales Advance MoM, est. 0.5%, prior 1.9%; Retail Sales Ex Auto MoM, est. 0.6%, prior 1.5%

8:30am: Retail Sales Control Group, est. 0.5%, prior 1.4%

8:30am: Import Price Index MoM, est. 0.0%, prior 0.3%; Import Price Index YoY, est. -0.75%, prior -1.1%

8:30am: Export Price Index MoM, est. 0.2%, prior 0.6%; Export Price Index YoY, prior -1.8%

9:15am: Industrial Production MoM, est. 1.0%, prior -0.6%; Capacity Utilization, est. 72.3%, prior 71.5%

10am: Business Inventories, est. 0.6%, prior 0.3%

10am: NAHB Housing Market Index, est. 85, prior 85

4pm: Net Long-term TIC Flows, prior $27.8b;

DB’s Jim Reid concludes the overnight wrap

After the last couple of weeks we should be aware that getting lunch early on a Monday could see you miss moves in markets that sometime take years to achieve in normal times. Moderna (11:56am GMT) yesterday followed Pfizer/BioNTech (11:45am GMT) last Monday in releasing the all important efficacy numbers just before the US was arriving at their virtual desks. So let’s see what arrives next Monday morning just before noon GMT.

The impact of yesterday’s announcement wasn’t as big for markets as last week’s though but it continued to fuel the rotation trade. With similar technology to Pfizer/BioNTech, expectations had already been raised for Moderna. However make no mistake that this was very good news. A 94.5% efficacy rate to date puts it up there with the most reliable vaccines we have. Below we have updated a CoTD from last week that has efficacy numbers for both these Covid-19 vaccines so far against diseases that we commonly vaccinate for. They both score very highly especially versus the flu vaccine.

In a further positive development, the Moderna vaccine “only” needs to be transported at minus 20C, which is well above the minus 70C that the Pfizer/BioNTech vaccine seemingly requires, so that’s more promising news when it comes to its wider distribution. In terms of the next steps, Moderna said that they intended to submit for an Emergency Use Authorization with the US FDA “in the coming weeks”. Later on in the day Federal Reserve Vice Chairman Clarida said that the positive vaccine news means he’s “got more conviction in (his) baseline for next year and more conviction that the recovery from the pandemic shock in the U.S. can potentially be much more rapid than it was from the global financial crisis.” So some rare recent signs from a Fed official of upside risks to growth.

Nevertheless, though the vaccine developments were incredibly positive, markets still have a bit of a “show me the logistics” side to it, and are also awaiting further info on availability and whether it’s as good at protecting the most vulnerable – namely the elderly. One of the successes that were highlighted by both the Moderna CEO and Dr Fauci was the ability to protect against severe cases, as no participants who got the vaccine developed a severe case of Covid-19, compared with 11 volunteers who received placebo shots.

Just on that logistics side, Pfizer/ BioNTech has said overnight that it has started a pilot Covid-19 immunisation program in four US states – Rhode Island, Texas, New Mexico, and Tennessee – to help refine the plan for the delivery and deployment of the vaccine.

In the meantime though, case growth continues to move in the wrong direction throughout the world, with governments moving to impose further restrictions. Cases have now risen on a weekly basis in all 50 US states with the Northeast now joining the rest of the nation as the weather turns colder. The New Jersey Governor announced that indoor gatherings would be limited to a maximum of 10, the Michigan’s Governor imposed a partial three-month shutdown, while in Philadelphia indoor dining has been banned and schools closed. California has also reinstituted bans on many indoor businesses and warned that a curfew is possible.

Even in Sweden, which had been relatively relaxed in its restrictions early on in the pandemic, the Prime Minister announced that gatherings of more than 8 people would be banned from next week. Here in the UK, Susan Hopkins, deputy director of Public Health England, said overnight that the three-tier system of social-distancing rules put in place before PM Johnson ordered a four-week lockdown in England was not wholly effective, and a winter of tougher measures may be needed until the vaccine is available for everyone. In more positive news France saw the running 7-day tally of new cases fall for a ninth-consecutive day and the country’s positive-test rate fall to 16.4%, down over 3pts in a week.

As with the Pfizer news the previous week, risk assets responded positively to the vaccine developments, and the S&P 500 climbed +1.16% to reach a new all-time high of 3626.91. That puts the index up +12.26% on a YTD basis, which probably isn’t what you’d have guessed for the S&P at this point had you been told the US economy was going to see its biggest annual contraction in decades. Looking at the sectoral moves, energy stocks (+6.50%) led the advance against the backdrop of a surge in oil prices, which themselves were supported by hopes of stronger economic demand and greater mobility in a post-Covid world. Indeed by the close, both Brent Crude (+2.43%) and WTI (+3.02%) oil prices had witnessed major gains. On the other hand, tech stocks lagged but they also ended the session higher, with the NASDAQ up +0.80%. And the S&P 500 wasn’t the only index to reach an all-time high, with the Dow Jones (+1.60%) climbing to its highest ever closing level, falling just shy of the 30,000 mark. Also on the S&P, there was confirmation that Tesla would be entering the S&P 500 on its next rebalancing on December 21, when it will likely be the largest ever new member and comfortably in the top 10 with its current market cap. The stock was up as much as 15% in after-market trading. This sort of gain is actually more than the market cap of Moderna which is pretty stunning.

Some of the stay-at-home stocks such as Zoom (-1.10%) lagged but the only sector that pulled back in the US was ironically Healthcare (-0.19%) as some businesses that were more profitable during the pandemic were repriced. The losses in the sector were led in part by Pfizer (-3.26%) with the difference in storage temperature between the two vaccines driving part of the divergence as Moderna rallied +9.63%.

For Europe it was much the same story, with the STOXX 600 rising +1.18% to a fresh post-pandemic high as energy stocks led the charge there too. Indices made gains across the continent, with the FTSE 100 (+1.66%), the CAC 40 (+1.70%) and the DAX (+0.47%) all moving higher. Southern Europe in particular outperformed, with Spain’s IBEX 35 (+2.60%) and Italy’s FTSE MIB (+1.98%) seeing the strongest gains on the continent. And this outperformance in southern Europe was also reflected in their sovereign bond spreads, which tightened to their lowest in years in some cases. In fact by the close, the spread of Italian 10yr yields over bunds had fallen -1.6bps to a 2-year low of 1.20%, while the equivalent Greek spread was down -4.1bps to 1.263%, its tightest level in over a decade.

Overnight in Asia the rally in risk assets has stalled a little with the Nikkei (+0.44%), Hang Seng (+0.02%), Kospi (+0.09%) and Asx (+0.21%) all making quite modest gains. The Shanghai Comp (-0.30%) is down. However, the rotation trade is continuing in Asian markets towards cyclicals. Meanwhile, futures on the S&P 500 are down -0.43% overnight. European futures are also pointing to a weaker open.

We heard from the ECB Chief Economist Philip Lane overnight as he reaffirmed that the ECB will provide enough monetary stimulus at its next meeting to make sure governments, companies and households have access to cheap credit throughout the coronavirus crisis. He added that, “Our orientation is to keep financing conditions favorable.”

Back to markets and sovereign bonds had a much less rosy time yesterday, selling off in response to the positive vaccine news as investors viewed it as lowering the likelihood of prolonged easy monetary policy. Despite the fact that yields had started the day by moving lower, those on 10yr US Treasuries ended up rising +1.0bps to move back above the 0.9% mark, while those on 10yr bunds (+0.2bps) and gilts (+1.1bps) similarly moved higher. They did all rally off the session highs in yield though.

It was somewhat down the headlines given the vaccine news, but there was a blockage in progress on the EU’s long-term budget and recovery fund yesterday, after Hungary and Poland opposed its progress because of conditions attached over the rule-of-law. This poses a risk since there has to be unanimity among the 27 member states for the European Commission to be able to issue joint debt. The bloc’s leaders are going to be holding a video conference on Thursday which is scheduled to focus on their response to the pandemic, so we can expect a strong discussion there. And although Hungary and Poland are against the conditions, others remain strongly in favour.

To the day ahead now, and we’ll hear from a number of central bank speakers including ECB President Lagarde, BoE Governor Bailey and Deputy Governor Ramsden, and the Fed’s Bostic, Daly, Kashkari, Rosengren and Barkin. Data highlights from the US include October’s retail sales, industrial production and capacity utilisation, as well as the NAHB housing market index for November. Finally, earnings releases include Walmart and Home Depot.

via ZeroHedge News https://ift.tt/3nxSWKk Tyler Durden

As mentioned in “Markets” today, we want to take a deep dive into Wall Street’s S&P 500 profit projections for 2021 in Data. Three points here, using FactSet’s weekly Earnings Insight report for the Street’s out-year expectations (link to their full report below).

#1: Analysts expect 2021 to be a record year for S&P 500 profitability, the fastest return to new-high earnings since at least the 1980s.

Based on the latest FactSet data, the Street is looking for $168.38/share on the S&P next year. This would be 3.9 percent higher than 2019’s all-time high of $163.02/share.

The more typical recovery time to new-high profits is 3 ½ to 4 years, as the following quarterly historical analysis using S&P’s own data for operating EPS shows:

In the late 1980s – early 1990s cycle, it took 4 years for the S&P to see earnings per share get back to their old highs (Q3 1989’s $6.53/share to Q3 1993’s $6.57/share).

In the late 1990s – early 2000s cycle, it took 3 ½ years (Q3 2000’s $14.88/share to Q4 2003’s $14.88/share).

After the Financial Crisis, it took the S&P 4 years to recoup its earnings power (Q3 2007’s $24.06/share to Q3 2011’s $24.86/share).

While it therefore might seem a stretch to think 2021 can post record-high earnings, keep in mind that Q3 2020 was so strong that we’re only talking about 9 percent growth in 2021 from Q3 2020. The S&P posted $38.74/share in Q3, which annualizes to $155/share. Next year’s estimate of $168.38/share is 8.6 percent higher.

Takeaway: start with a solid base of corporate earnings in Q3 2020, add what we all hope is a highly effective virus vaccine, stir in still-low interest rates and decent (for the conditions) consumer spending, and you SHOULD get record high 2021 earnings. A presumably still-split Congress means corporate tax rates should not rise next year, another important ingredient of course.

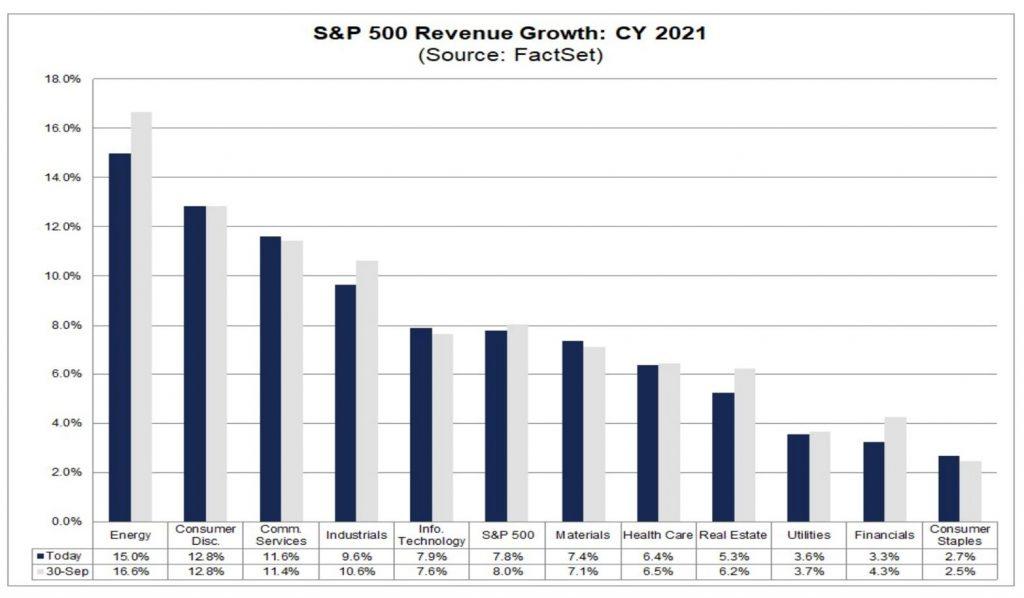

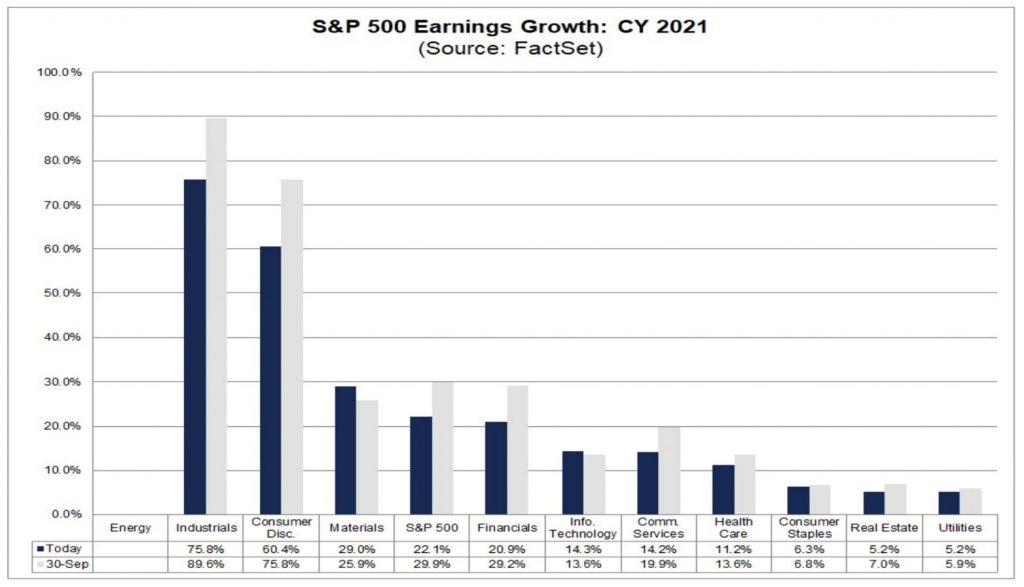

#2: This earnings growth should come from more cyclical sectors like Industrials, Consumer Discretionary and Materials, but the Street expects every sector to show at least 5 percent bottom line improvement and 3 percent revenue comps to 2020.

Here are the FactSet charts showing the sector-by-sector revenue (first image) and earnings (second image) comps for 2021:

The important thing to note here is just how much 2021’s expected earnings growth outpaces revenue growth everywhere except Real Estate. Look at the aggregate S&P numbers: 7.8 percent revenue growth translates into 22.1 percent earnings growth. Three points on this:

Typical earnings leverage is more like 3-4 points. Revenue growth of 3 percent yields earnings growth of 6-7 percent because some portion of a company’s cost structure is fixed. But… under more ordinary circumstances there’s always cost-creep in corporate income statements that make 3-4 points of leverage more of a ceiling than a floor.

The only time you can pencil in 14 points of leverage (as the Street is doing now for 2021) is very early in an economic cycle. That’s because managements are still very cautious about adding unnecessary expenses right after a recession and this – along with better/richer mix revenue streams – creates outsized earnings leverage.

Look at the 3 leftmost bars in the second graph, and you’ll see they are all high fixed cost industries where operating leverage is high (Industrials, Consumer Discretionary, Materials). Energy may not post a profit in 2021, but you’ll see in the first graph that it is expected to see the largest percentage revenue improvement of any S&P sector.

Takeaway: as much as the Street’s assumption of 14 points of S&P 500 operating leverage in 2021 might sound way too high, given all that’s occurred in 2020 it could actually be low if revenues recover more strongly and cost containment measures remain in place. Also worth considering: many companies are still not giving earnings guidance for Q4 2020 or 2021CY. Both those points add up to a lot of uncertainty, to be sure, but also a lot of potential for upside earnings leverage in 2021.

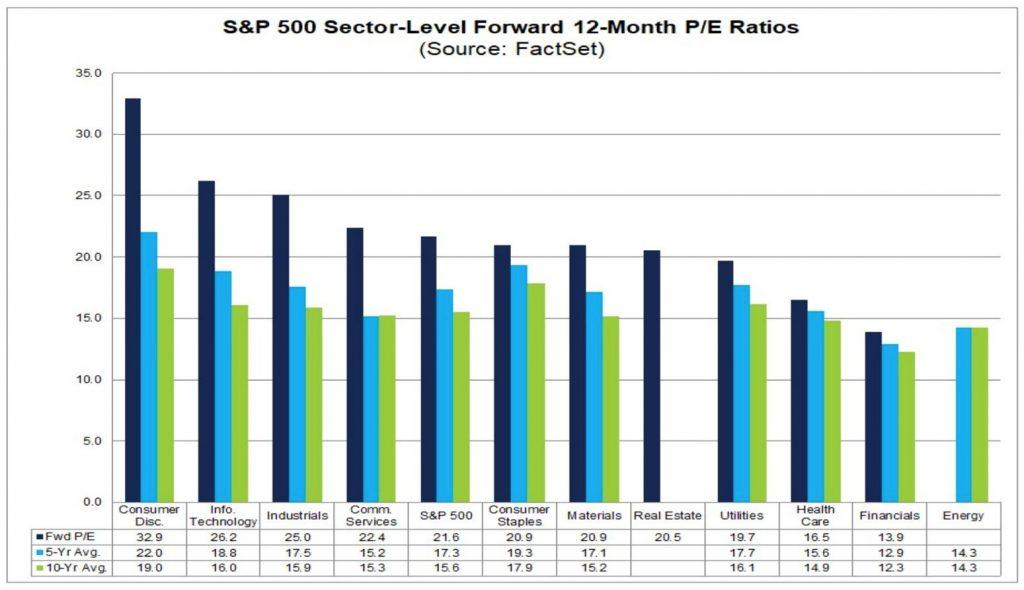

#3: Everyone knows US equities are richly valued just now, but given the dynamic we’re laying out here today that’s entirely understandable. Consider this FactSet chart, which shows each sector’s valuation based on 12-month forward expected earnings:

The dark blue bars represent current forward PE ratios, and the light blue/green bars show the 5-/10-year averages. The widest spreads between dark blue and light blue/green are either in sectors that have proven themselves largely recession-proof in 2020 (Tech, Comm Services) or have outsized earnings leverage in 2021 (Consumer Discretionary, Industrials, and Materials).

Takeaway: the S&P 500 is trading at 21.6x earnings, 40 percent its 10-year average, for basically one fundamental (i.e. not interest rate-related) reason. Markets think Wall Street’s 2021 numbers are too low by at least 10 percent. If 2021 comes in at $185/share rather than $168/share, then the S&P would be trading for 19x earnings today. Given long term rates are at 1 percent, that sort of multiple makes sense.

The bottom line to all this: equity valuations during cyclical recoveries always feel high, and the US stock market right now is no exception. We have a few unusual factors to put in the mix as well, ranging from the effect of the virus on the Q4/Q1 global economy to a new political setup in Washington. We’ll close on this thought, though: if you don’t believe US corporate earnings can show dramatic operating leverage in 2021 then now is the time to consider lightening up on risk exposure.

via ZeroHedge News https://ift.tt/2IAvQny Tyler Durden

Zuckerberg, Dorsey Return To Capitol Hill For Post-Election ‘Rematch’ With Senate Judiciary Tyler Durden

Tue, 11/17/2020 – 07:52

Two of Silicon Valley’s top tech CEOs, Facebook’s Mark Zuckerberg and Twitter’s Jack Dorsey, will appear Tuesday morning before the Senate Judiciary Committee (led by a newly reelected Lindsey Graham) in their first post-election Congressional hearing.

This isn’t the first time the two men have appeared before the Congress in 2020: there have been at least two big hearings with a mix of CEOs from the various American tech megacaps before this, focusing mostly on election interference (for the Dems) and censorship of conservative voices (for the GOP).

This time around, the animus behind the hastily organized hearing is pretty clear: With President Trump and his team coming up empty-handed in their push to challenge the election results, both CEOs will once again be pressed on efforts to tip the scales in Biden’s favor.

But this time around, the social media culture war isn’t their only concern: with the rise of Parler, a new anti-censorship social media platform that has been courting conservative influencers, is becoming a real problem for Twitter. Over the past few years, frustration with Big Tech’s personal-data abuses has led both Democrats and Republicans to support an anti-monopoly review.

However, Joe Biden has notably been filling his transition team with “inside players” from the tech world. Yesterday, Politico published a story examining the “tug of war” going on inside the Biden transition team. During the campaign, many Biden campaign officials felt that Facebook was the real opponent, given the overwhelming popularity of a handful of conservative commentators who rely on FB to reach a base of older consumers.

Former Facebook board member Jeff Zients is co-chairing Biden’s transition team, and another former board member is an adviser. Two others, one who was a Facebook director, and another who was a company lobbyist, have taken leadership roles. Biden himself has a friendly relationship with former UK Deputy Prime Minister Nick Clegg, who was essentially purchased by Zuckerberg to act as a sort of political buffer.

During their last appearance before the Judiciary Committee back in October, the two CEOs (alongside Google’s Sundar Pichai) were pressed to explain why they suppressed a New York Post story exposing private emails from Hunter Biden purporting to show that his father’s comments about having never discussed business with his son were untrue. At the time, they conceded that there was zero evidence the story was the work of Russian hackers, or a foreign adversary, as was widely – and baselessly – reported by the MSM.

Changing or even removing Section 230 protections for social media companies bestowed by the Communications Decency Act will likely be discussed, as both CEOs could be pressed to defend the reasoning for these protections and why they should continue to exist.

According to Bloomberg, which got a sneak peak of some of Dorsey’s testimony, Dorsey is planning to tell Congress that he’s open to changes to the liability shield that would place more of a burden on tech firms to remove posts, however, according to Dorsey, changes should be made slowly and methodically to help avoid unintended consequences.

“Completely eliminating Section 230 or prescribing reactionary government speech mandates will neither address concerns nor align with the First Amendment,” according to Dorsey’s remarks. Lawmakers from both parties have criticized the law, but many Republicans have sought changes to force the companies to leave up more conservative content.

Readers might remember during Dorsey’s last appearance on Capitol Hill when Sen. Ted Cruz exploded on him after Dorsey acknowledged that Twitter allowed mobs of hypersensitive leftists to censor conservatives by abusing the report post feature.

“Who the hell elected you and put you in charge of what the media are allowed to report and what the American people are allowed to hear?” Cruz shouted on camera.

Tuesday’s hearing is set to begin at 1000ET. Readers can stream it live.

via ZeroHedge News https://ift.tt/3nwVNTz Tyler Durden

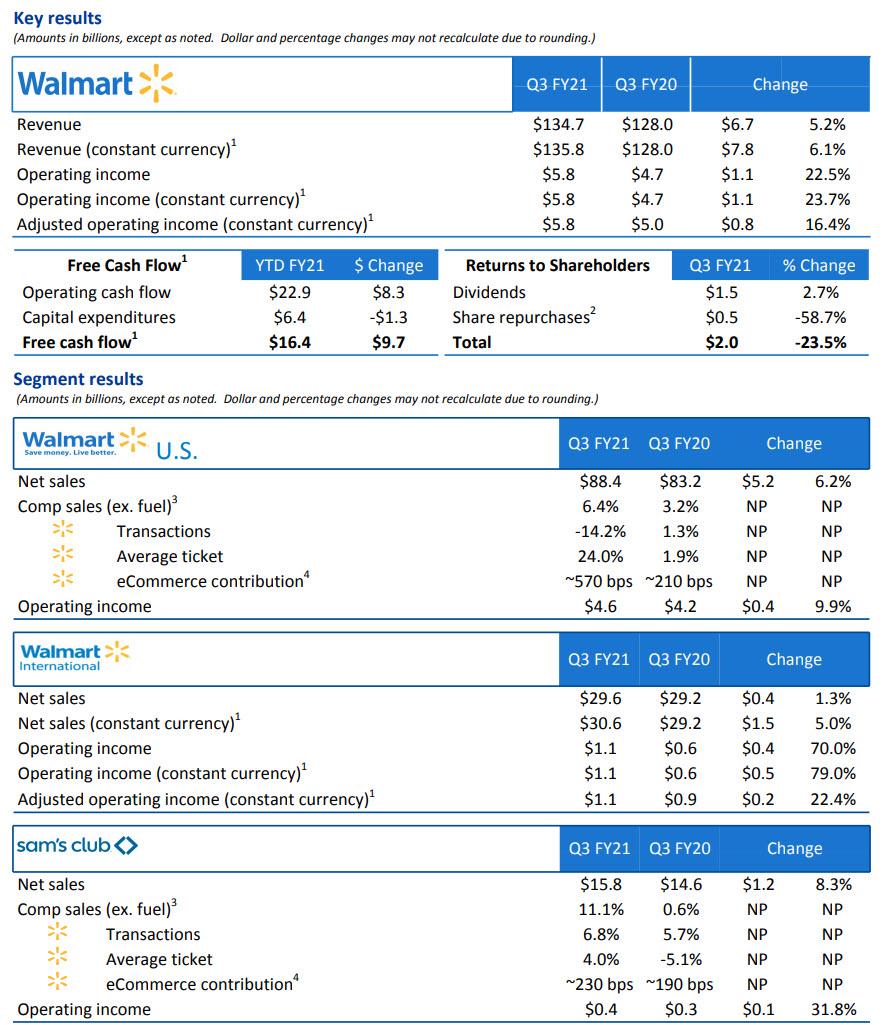

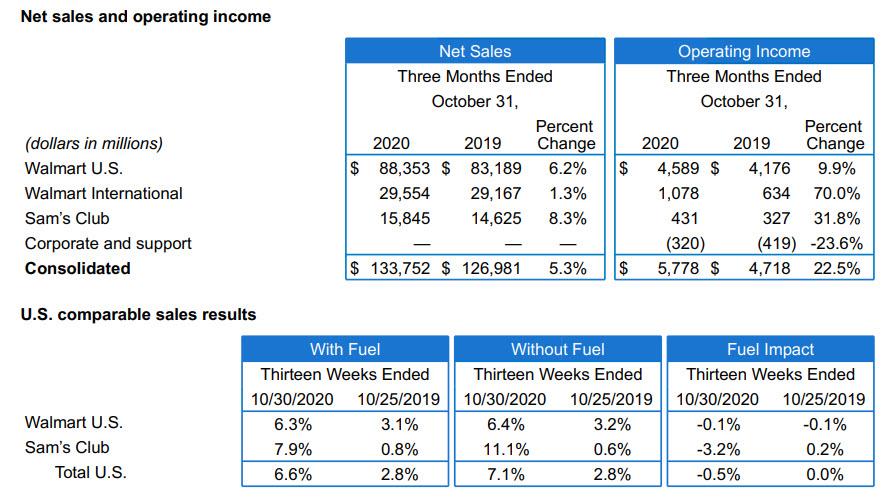

Walmart Jumps After Smashing Expectations As Average Ticket Soars 24% Tyler Durden

Tue, 11/17/2020 – 07:39

While it may be facing an uncertain near-term future with partial economic shutdowns returning, at least for its brick and mortar stores, Walmart’s immediate past was quite impressive with the world’s largest retailer reporting stellar Q3 earnings which surged past estimates as consumers continued to flock to the essential retailer to stock up on stay at-home products and entertainment while the virus rages on.

Walmart beat handily on the top and bottom line:

Q3 adjusted EPS of $1.34, smashing estimates $1.18 and coming above the highest sellside forecast (range $1.06 to $1.26)

The adjusted EPS excluded the effects, net of tax, of an unrealized gain of $0.80 on equity investments and $0.34 for the loss of Walmart Argentina

Q3 revenue $134.71 billion, up 5.2% Y/Y and also beating estimates of $132.42 billion (range $130.52 billion to $135.50 billion)

More good news: the company said new member sign-ups and renewal rates were strong, particularly Plus membership. Membership income increased 10.4%. In terms of covid-linked disclosure, Walmart said it incurs 3Q incremental costs related to COVID-19 of 0.6 billion.

But the most impressive result was that same store sales blew estimates out of the water, with Walmart-only US comps of 6.4% almost double the 3.8% estimate.

Q3 Walmart-only U.S. stores comparable sales ex-gas +6.4%, estimate +3.8%

Q3 Sam’s Club U.S. comparable sales ex-gas +11.1%, estimate +7.10%

Q3 total U.S. comparable sales ex-gas +7.1%, estimate +4.3%

What is notable is that the 6.4% surge in comps was even as the number of transactions tumbled 14.2% Y/Y at U.S. Walmart locations, yet the average purchase surged 24.0% which means shoppers are consistently buying more every time they place an order.

Alternatively, Sam’s Club also reported sales that beat estimates as it pushes to lure more members with delivery, pickup and smaller serving sizes to appeal to those not planning large holiday gatherings this year, according to Bloomberg. Sam’s Club same-store sales growth of 11.1% surpassed expectations for a 7.1% gain, the result of an increased number of transactions (+6.8%) and higher average ticket (+4.0%).

As the company continues to ramp up its online offering, U.S. e-commerce sales at Walmart rose 79% in the quarter and 41% at its warehouse chain. The company said in September that it would hire more than 20,000 workers to prepare for a surge in online shopping amid the pandemic. According to Bloomberg, that was the company’s first large seasonal hiring in five years.

As a reminder, Walmart’s response to Amazon Prime, Walmart+, launched in September at a price of $98 a year that includes unlimited free delivery from stores and gasoline discounts. There were few details on this venture in the release, so investors will be waiting to hear more on the call today.

Walmart shares spiked in kneejerk reaction to the report, then faded some of their gains, but were comfortably higher from Monday’s open.

via ZeroHedge News https://ift.tt/36MVPjo Tyler Durden

I agree with the general thrust of Eugene’s post yesterday, in which he describes the phenomenon in which “white” has come to mean “relatively successful as a group,” with “Asians” often being described, implicitly or explicitly, as white because they are deemed a socioeconomic success.

But I would like to add a more radical critique, which is that lumping together people whose recent origins range geographically from India to the Philippines is itself not very useful, and that if we need to gather statistics about, or discuss, “Asians,” at most we should be discussing the attributes of various national (and better yet subnational, though getting such statistics is difficult) groups, rather than “Asians.”

The Asian American category includes people descended from wildly disparate national groups, who do not have similar physical features, practice different religions, speak different languages, vary dramatically in culture, and belong to gropus that sometimes have long histories of conflict with one another. Various subgroups of Asian Americans have differing levels of average socioeconomic success in the United States —Indian-Americans, for example, on average have significantly higher-than-average incomes and levels of education, while on average the incomes of Hmong and Burmese Americans are well-below the American mean. Korean-Americans have the highest rate of business formation for any ethnic group in the United States, while Laotians have the lowest. The Asian category meanwhile excludes people from the Western part of Asia, such as Muslim Americans of Yemeni origin, who may face discrimination based on skin color (often dark), religion, and Arab ethnicity. Only a minority of people in the Asian category identify with the “Asian” or “Asian American” labels.

When we talk about “Asian Americans” being “overrepresented” (ughh…) in American higher education, we are referring primarily to Indian-Americans (who are by far the most “overrepresented” “Asian” group) and Chinese Americans. By contrast, Filipinos (the largest Asian-American minority), Vietnamese, and other Asian groups are not especially prominent at elite schools.

And while we’re on the general subject, lumping together the groups we call “Hispanic” or “Latino” also makes little sense:

The Hispanic category generally includes everyone from Spanish immigrants (including people whose first language is Basque or Catalan, but not Spanish) to Cuban Americans of mixed European extraction to Puerto Ricans of mixed African, European, and indigenous heritage to individuals fully descended from indigenous Mexicans. Members of the disparate groups that fall into the “Hispanic” or “Latino” category often self-identify as white, feel more connected to the general white population than to other Spanish-language national-origin groups, and sometimes diverge from members of other Hispanic demographic groups in political outlook as much or more than from the general white population. Moreover, “census data show substantial differences in levels of income and educational attainment among the national origin groups in which data about ‘Hispanics’ are usually classified.” Not all Hispanics, meanwhile, consider themselves to be part of a minority group, and “some who claim minority status for themselves would reject that status for others” (for example, they might reject it for well-educated professionals who immigrate from South American countries and are considered white in their home countries). People of Portuguese or Brazilian ancestry, who are not of Spanish culture or origin, are nevertheless sometimes defined as Hispanic by legislative or administrative fiat.

I’ve delved a bit into the “intersectional” literature, to try to understand how scholars who believe that success in American life is primarily about the “privilege” of one’s group explain the relative success and failure of groups like “Asian” writ large, but also the obvious difference in subgroups. It’s a huge, risible mess. For example, one scholar posits that whites “let” Chinese and Japanese immigrants succeed because, unlike Vietnamese and Cambodian immigrants, they are relatively light-skinned. Putting aside whether the skin color thing is even true, one wonders how and when whites got together to decide this, how they enforce it, and how it explains why the most “successful” of all immigrant groups are Indian-Americans, who are relatively dark-skinned. But to an ideological hammer, everything looks like a nail.

from Latest – Reason.com https://ift.tt/3ny3TeE

via IFTTT

I agree with the general thrust of Eugene’s post yesterday, in which he describes the phenomenon in which “white” has come to mean “relatively successful as a group,” with “Asians” often being described, implicitly or explicitly, as white because they are deemed a socioeconomic success.

But I would like to add a more radical critique, which is that lumping together people whose recent origins range geographically from India to the Philippines is itself not very useful, and that if we need to gather statistics about, or discuss, “Asians,” at most we should be discussing the attributes of various national (and better yet subnational, though getting such statistics is difficult) groups, rather than “Asians.”

The Asian American category includes people descended from wildly disparate national groups, who do not have similar physical features, practice different religions, speak different languages, vary dramatically in culture, and belong to gropus that sometimes have long histories of conflict with one another. Various subgroups of Asian Americans have differing levels of average socioeconomic success in the United States —Indian-Americans, for example, on average have significantly higher-than-average incomes and levels of education, while on average the incomes of Hmong and Burmese Americans are well-below the American mean. Korean-Americans have the highest rate of business formation for any ethnic group in the United States, while Laotians have the lowest. The Asian category meanwhile excludes people from the Western part of Asia, such as Muslim Americans of Yemeni origin, who may face discrimination based on skin color (often dark), religion, and Arab ethnicity. Only a minority of people in the Asian category identify with the “Asian” or “Asian American” labels.

When we talk about “Asian Americans” being “overrepresented” (ughh…) in American higher education, we are referring primarily to Indian-Americans (who are by far the most “overrepresented” “Asian” group) and Chinese Americans. By contrast, Filipinos (the largest Asian-American minority), Vietnamese, and other Asian groups are not especially prominent at elite schools.

And while we’re on the general subject, lumping together the groups we call “Hispanic” or “Latino” also makes little sense:

The Hispanic category generally includes everyone from Spanish immigrants (including people whose first language is Basque or Catalan, but not Spanish) to Cuban Americans of mixed European extraction to Puerto Ricans of mixed African, European, and indigenous heritage to individuals fully descended from indigenous Mexicans. Members of the disparate groups that fall into the “Hispanic” or “Latino” category often self-identify as white, feel more connected to the general white population than to other Spanish-language national-origin groups, and sometimes diverge from members of other Hispanic demographic groups in political outlook as much or more than from the general white population. Moreover, “census data show substantial differences in levels of income and educational attainment among the national origin groups in which data about ‘Hispanics’ are usually classified.” Not all Hispanics, meanwhile, consider themselves to be part of a minority group, and “some who claim minority status for themselves would reject that status for others” (for example, they might reject it for well-educated professionals who immigrate from South American countries and are considered white in their home countries). People of Portuguese or Brazilian ancestry, who are not of Spanish culture or origin, are nevertheless sometimes defined as Hispanic by legislative or administrative fiat.

I’ve delved a bit into the “intersectional” literature, to try to understand how scholars who believe that success in American life is primarily about the “privilege” of one’s group explain the relative success and failure of groups like “Asian” writ large, but also the obvious difference in subgroups. It’s a huge, risible mess. For example, one scholar posits that whites “let” Chinese and Japanese immigrants succeed because, unlike Vietnamese and Cambodian immigrants, they are relatively light-skinned. Putting aside whether the skin color thing is even true, one wonders how and when whites got together to decide this, how they enforce it, and how it explains why the most “successful” of all immigrant groups are Indian-Americans, who are relatively dark-skinned. But to an ideological hammer, everything looks like a nail.

from Latest – Reason.com https://ift.tt/3ny3TeE

via IFTTT

This week sees yet another Trump administration initiative to hasten America’s decoupling from China. As with MIRV warheads, the theory seems to be that if you launch enough of them, the next administration can’t shoot them all down. Brian Egan lays out this week’s initiative, which lifts from obscurity a DoD list of Chinese military companies and excludes the companies from U.S. capital markets.

Our interview is with Frank Cilluffo and Mark Montgomery. Mark is Senior Fellow at the Foundation for Defense of Democracies and Senior Advisor to the congressionally mandated Cyberspace Solarium Commission. Previously, he served as Policy Director for the Senate Armed Services Committee under Senator John S. McCain—and before that served for 32 years in the U.S. Navy as a nuclear trained surface warfare officer, retiring as a Rear Admiral in 2017. Frank is director of Auburn University’s Director of Auburn University’s McCrary Institute for Cyber and Critical Infrastructure Security. He served on the Cyberspace Solarium Commission and chaired the Homeland Security Advisory Council’s subcommittee on economic security.

We talk about the unexpected rise of the industrial supply chain as a national security issue. Both Frank and Mark were moving forces in two separate reports highlighting the issue, as was I. (See also my op-ed on the same topic.) So, if we seem suspiciously in agreement on supply chain issues, it’s because we are suspiciously in agreement on supply chain issues. Still, as an introduction to one of the surprise hot issues of the year, it’s not to be missed.

After our interview in episode 336 of a Justice Department official on how to read Schrems II narrowly, you knew it was only a matter of time before we heard from Europe. Charles Helleputte reviews the European Data Protection Board’s effort to give more authoritative and less comfortable advice to U.S. companies that want to keep relying on the standard contractual clauses. The Justice Department take on the topic manages to squeak through without a direct hit from the privacy bureaucrats. Still, the EDPB (and the EDPS even more so) makes clear that anyone following the DOJ’s lead is in for an uphill fight. (For those who want more of Charles’s thinking on the topic, see this short piece.)

Zoom has been allowed to settle an FTC proceeding for deceptive conduct (claiming that its crypto was end to end when it wasn’t, and more). Mark MacCarthy gives us details. I throw shade on the FTC’s failure to ask any serious national security questions about a company that deserves some.

Brian brings us up to speed on TikTok. Only one of the Trump administration penalties remains unenjoined. My $50 bet with Nick Weaver—that CFIUS will overcome the judicial skepticism that IEEPA could not—is hanging by a thread. Casey Stengel makes a brief appearance to explain why TikTok might win.

Brian also reminds us that export control policymaking is even slower and less functional on the other side of the Atlantic, as Europe tries, mostly ineffectively, to adopt stricter limits on exports of surveillance tech.

Charles explains and I decry the enthusiasm of European courts for telling Americans what they can say and read on line, as an Austrian court tells Facebook to take down worldwide the description of an Austrian politician as belonging to a “fascist party.” Apparently, we aren’t allowed to say that political censorship is what members of a fascist party tend to advocate; but don’t worry about our liability; we can’t pronounce the plaintiff’s name.

Brian gives the government credit for preventing foreign interference. I question the whole narrative of foreign interference, which didn’t have much effect in 2016 or 2020 (other than the hack and dump operation against the DNC) but did align conveniently with Democratic messaging in both years (Hillary only lost because of the Russians! Ignore Trump’s corruption allegations because they’re just more Russian interference!).

Mark and I wonder what Silicon Valley thinks it’s accomplishing with its extended bans on political advertising after the election. After all, it’s almost always election season somewhere (see, e.g., Georgia).

DHS’s CISA did produce a detailed rumor control site that helped correct misunderstandings—but may have corrected one too many of the President’s tweets. In consequence, Under Secretary Chris Krebs, familiar to Cyberlaw Podcast listeners, may be on the chopping block. That would be a shame for DHS and CISA; for Chris it’s probably a badge of honor. Frank Cilluffo and Mark Montgomery weigh in with praise for Chris as well.

You can subscribe to The Cyberlaw Podcast using iTunes, Google Play, Spotify, Pocket Casts, or our RSS feed. As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect the opinions of their institutions, clients, friends, families, or pets.

from Latest – Reason.com https://ift.tt/3f8KH4i

via IFTTT

11/17/1880: The United States and China sign treaty that protects Chinese laborers residing in the United States. This treaty was implicated in Yick Wo v. Hopkins (1886).

from Latest – Reason.com https://ift.tt/36JEtnB

via IFTTT

This week sees yet another Trump administration initiative to hasten America’s decoupling from China. As with MIRV warheads, the theory seems to be that if you launch enough of them, the next administration can’t shoot them all down. Brian Egan lays out this week’s initiative, which lifts from obscurity a DoD list of Chinese military companies and excludes the companies from U.S. capital markets.

Our interview is with Frank Cilluffo and Mark Montgomery. Mark is Senior Fellow at the Foundation for Defense of Democracies and Senior Advisor to the congressionally mandated Cyberspace Solarium Commission. Previously, he served as Policy Director for the Senate Armed Services Committee under Senator John S. McCain—and before that served for 32 years in the U.S. Navy as a nuclear trained surface warfare officer, retiring as a Rear Admiral in 2017. Frank is director of Auburn University’s Director of Auburn University’s McCrary Institute for Cyber and Critical Infrastructure Security. He served on the Cyberspace Solarium Commission and chaired the Homeland Security Advisory Council’s subcommittee on economic security.

We talk about the unexpected rise of the industrial supply chain as a national security issue. Both Frank and Mark were moving forces in two separate reports highlighting the issue, as was I. (See also my op-ed on the same topic.) So, if we seem suspiciously in agreement on supply chain issues, it’s because we are suspiciously in agreement on supply chain issues. Still, as an introduction to one of the surprise hot issues of the year, it’s not to be missed.

After our interview in episode 336 of a Justice Department official on how to read Schrems II narrowly, you knew it was only a matter of time before we heard from Europe. Charles Helleputte reviews the European Data Protection Board’s effort to give more authoritative and less comfortable advice to U.S. companies that want to keep relying on the standard contractual clauses. The Justice Department take on the topic manages to squeak through without a direct hit from the privacy bureaucrats. Still, the EDPB (and the EDPS even more so) makes clear that anyone following the DOJ’s lead is in for an uphill fight. (For those who want more of Charles’s thinking on the topic, see this short piece.)

Zoom has been allowed to settle an FTC proceeding for deceptive conduct (claiming that its crypto was end to end when it wasn’t, and more). Mark MacCarthy gives us details. I throw shade on the FTC’s failure to ask any serious national security questions about a company that deserves some.

Brian brings us up to speed on TikTok. Only one of the Trump administration penalties remains unenjoined. My $50 bet with Nick Weaver—that CFIUS will overcome the judicial skepticism that IEEPA could not—is hanging by a thread. Casey Stengel makes a brief appearance to explain why TikTok might win.

Brian also reminds us that export control policymaking is even slower and less functional on the other side of the Atlantic, as Europe tries, mostly ineffectively, to adopt stricter limits on exports of surveillance tech.

Charles explains and I decry the enthusiasm of European courts for telling Americans what they can say and read on line, as an Austrian court tells Facebook to take down worldwide the description of an Austrian politician as belonging to a “fascist party.” Apparently, we aren’t allowed to say that political censorship is what members of a fascist party tend to advocate; but don’t worry about our liability; we can’t pronounce the plaintiff’s name.

Brian gives the government credit for preventing foreign interference. I question the whole narrative of foreign interference, which didn’t have much effect in 2016 or 2020 (other than the hack and dump operation against the DNC) but did align conveniently with Democratic messaging in both years (Hillary only lost because of the Russians! Ignore Trump’s corruption allegations because they’re just more Russian interference!).

Mark and I wonder what Silicon Valley thinks it’s accomplishing with its extended bans on political advertising after the election. After all, it’s almost always election season somewhere (see, e.g., Georgia).

DHS’s CISA did produce a detailed rumor control site that helped correct misunderstandings—but may have corrected one too many of the President’s tweets. In consequence, Under Secretary Chris Krebs, familiar to Cyberlaw Podcast listeners, may be on the chopping block. That would be a shame for DHS and CISA; for Chris it’s probably a badge of honor. Frank Cilluffo and Mark Montgomery weigh in with praise for Chris as well.

You can subscribe to The Cyberlaw Podcast using iTunes, Google Play, Spotify, Pocket Casts, or our RSS feed. As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect the opinions of their institutions, clients, friends, families, or pets.

from Latest – Reason.com https://ift.tt/3f8KH4i

via IFTTT