More than two decades ago, Virginia Postrel published a prescient book with a wonderful title: “The Future and Its Enemies.” The technological revolution that has led to “greater wealth, health, opportunity and choice than at any time in history,” she argued, has resulted in “a chorus of intellectuals and politicians [that] loudly laments our condition.”

Sadly, the future’s enemies use the government to fight inevitable innovation and progress.

These critics bemoan the economic insecurity such advances have wrought, as well as other first-world problems ranging from our “enslavement” to technology to the supposed (but not actual) despoliation of the Earth. When she published the book, “smart phones” were rather dull. They were large, clunky, and served solely to make phone calls. It’s inconceivable how far those—and other common products—have developed in the ensuing years.

I recall my prized eight-track tape player, my first car with its whopping 70 horsepower and AM-only radio, phone booths, library card catalogs, pneumatic tubes for delivering office documents (Google it), video stores, and, my favorite, Qwip machines. The latter was cutting-edge in the 1970s. The sender put a document on a cylinder that would spin. It slowly transmitted a facsimile of the document—line by line and in crude fashion—to carbon paper at the other end.

Today I scanned and emailed dozens of documents and shudder at the thought of doing things in that archaic manner. By the way, it’s easy to get caught up in the consumer-oriented improvements we cherish while forgetting about, say, the vast improvements in food production that have dramatically reduced world hunger and the many life-saving medical advancements.

In California this year, the fight over the future centers on Proposition 22, which would allow companies such as Uber, Lyft, and DoorDash to classify workers as independent contractors rather than as permanent employees. Obviously, technology has disrupted the way we travel, shop, and work, which has made our lives much better—but has infuriated labor unions, which find it tougher to organize workers in the flexible new work world.

I’ve noted this before, but they’ve clearly taken on the role of the 19th Century British Luddites—textile workers who couldn’t compete with mechanized looms, so they vandalized them. Modern unions don’t destroy property these days—but they lobby the government to do something worse. They try to hobble those industries that are moving the world forward.

A few weeks ago, I took a taxicab for the first time in months. The driver didn’t want my business because, apparently, it wasn’t a good-enough fare. The cab was grimy. He balked at my credit card, and it took time to process it after I insisted. Compare that to the friendly and seamless experiences we have with Uber and Lyft. Think about the deliveries we receive—and how they allow us to avoid those laborious trips to box stores and restaurants.

Proposition 22 is a reaction to Assembly Bill 5, which went into effect in January. The law, signed by Gov. Gavin Newsom and championed by unions, codified a 2018 California Supreme Court decision (Dynamex) that applied a strict test to companies that want to hire freelancers. The measure would exempt drivers from A.B. 5’s provisions—and provide them with some portable benefits.

After A.B. 5 became law, it had vast should-have-been-seen consequences. Instead of bringing workers onboard full-time and paying them benefits, companies started laying off their California contractors. Californians who had good jobs but used freelance and contractor work to earn some side income had to give up their lucrative gigs. Consumers suffered, too, as they endured rising prices and fewer choices—all in the midst of a pandemic.

That’s why even the union-controlled California Legislature exempted more than 100 industries from A.B. 5’s strict provisions. They exempted almost every major industry, except for those increasingly vital transportation and delivery services.

If voters approve Proposition 22, the state will have a groundbreaking labor law that applies to virtually no one, yet that hasn’t stopped the labor movement from touting it as a nationwide model. If California voters approve it, they will slow this new Luddite movement from spreading.

Unions can’t stop the future, but they can cause misery as we await its arrival. For instance, our union-allied attorney general, Xavier Becerra, has filed lawsuits against the transportation companies to force them to comply with A.B. 5 as we await the election. The companies were hours away from suspending operations here until a court issued a temporary stay. This is nonsensical in a state that sees itself as the embodiment of progress.

Even if labor wins at the polls this November, it will have no more long-term success than any other group that has tried to fight a changing world. Like water rolling down a hill, creative minds will find their way around every obstacle. Sorry, but the union vision of factory floors and cubicles is a vestige of the past—not a roadmap to the future.

This column was first published in The Orange County Register.

from Latest – Reason.com https://ift.tt/3jFfbeY

via IFTTT

Futures Rebound From Overnight Tech Wreck Tyler Durden

Fri, 10/30/2020 – 08:06

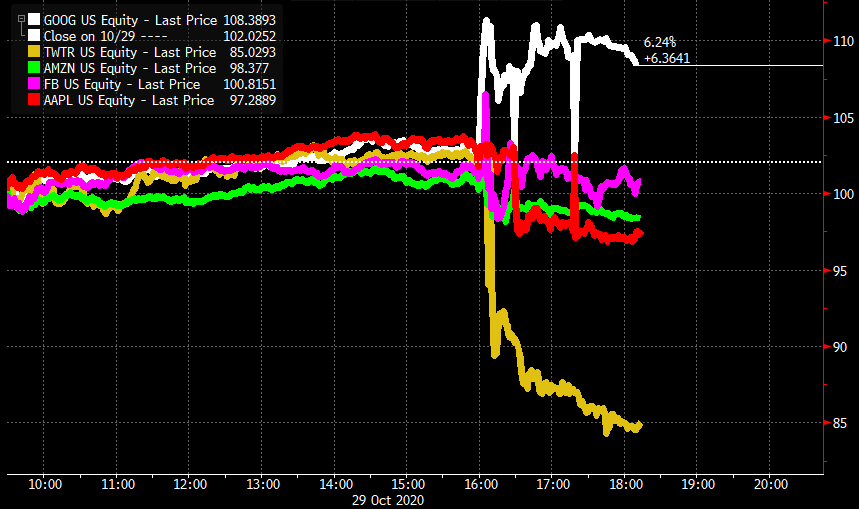

On Monday we presented readers with the latest observations from BofA quants who pointed out that Q3 earnings “smacked of the tech bubble” because despite impressive beats, in many cases stocks dropped (or outright tumbled) in kneejerk response as virtually everything has now been priced to (and beyond) perfection with little chance of upside surprise. Nowhere was this more obvious than Thursday afternoon when the world’s 4 biggest tech companies all reported blockbuster earnings and yet all but Google sank subsequently with the exception of Alphabet which popped after hours (while Twitter plunged as countless conservatives bailed on the ultra-partisan and liberal social network).

Nasdaq futures fell about 1%, erasing more than half of what was a 2.7% slide earlier after Apple’s iPhone sales and Twitter’s user growth both missed estimates. The two stocks sank in pre-market trading. Amazon.com fell 1.4% after it forecast a jump in costs related to COVID-19, while Facebook shed 2% as it warned of a tougher 2021. Google parent Alphabet was the only bright star among the FAAMGs with its shares jumping 7% after it beat estimates for quarterly sales as businesses resumed advertising.

Ahead of the overnight tech rout, global stock were already on course for the worst weekly decline since March as lockdown measures and the collapse of stimulus talks (which “nobody” could have predicted) crippled trader optimism. Treasuries, the dollar, oil and gold were little changed.

Third-quarter earnings season is past its halfway mark and about 84.8% of S&P 500 companies have beaten estimates for earnings, according to Refinitiv data. Overall, profit is expected to tumble 13.4% from a year ago.

The broad-based weakness in the market-leading giga-tech stocks added to trader concerns about a surge in coronavirus cases, and hammered stock futures on Friday, although futures are now off their worst levels of the day.

S&P e-minis fell 25.00 points or 0.9% and Nasdaq 100 E-minis were down 121 points, or 1.1%. A longer-term chart shows the precarious positioning for the S&P, with any further declines set to take out the Sept 24 lows and open up a trapdoor to much lower levels.

Shares of tech heavyweights had jumped ahead of tech results on Thursday, helping the S&P 500 close higher. Still, the benchmark index is set to wrap up its worst week since mid-June, while Wall Street’s fear gauge held at a 20-week high, also on fears of a contested election next week. Ahead of the final weekend before Election Day on Tuesday, President Donald Trump and Democratic challenger Joe Biden will barnstorm across battleground states in the Midwest where the coronavirus pandemic has exploded anew.

“Our short-term risk-appetite indicator is firmly in negative territory,” said Credit Agricole CIB head of global markets research Jean-Francois Paren. “The adjustment of risky asset prices to the weaker epidemic and economic outlook could continue, which is not encouraging for risk asset prices in the coming days, especially given the uncertainty regarding the U.S. elections.”

European shares fluctuated amid a string of mixed earnings reports. Europe’s Stoxx 600 Index erased declines of as much as 0.9%, climbing 0.3%, led by energy and banks, with E&P giants Total and Shell among biggest gainers; Total posted 3Q profit that exceeded the highest analyst estimate; Barclays raised Shell to equalweight, saying newly presented financial framework addresses main concerns. Tech stocks faltered as did Danish drug giant Novo Nordisk A/S, whose earnings underwhelmed analysts. Bank stocks advanced after Spain’s BBVA SA and the U.K.’s NatWest Group Plc reported improved pictures for soured loans.

Earlier in the session, Asian stocks fell, led by the health care and IT sectors. Trading volume for MSCI Asia Pacific Index members was 28% above the monthly average for this time of the day. The Topix lost 2%, with Takeda and Hoya contributing the most to the move. The Shanghai Composite Index retreated 1.5%, driven by China Life and Yili Industrial.

As Bloomberg notes, weakness in technology shares has added to volatility that’s likely to remain elevated heading into next week’s U.S. election. Global equities are on course for the worst weekly decline since March as lockdown measures in some countries and the lack of an agreement on U.S. stimulus dent sentiment. New U.S. coronavirus cases topped 89,000, setting a daily record.

In FX, the Bloomberg Dollar Spot Index steadied after swinging between gains and losses; the euro steadied but was set for its biggest weekly drop against the dollar since September. Sweden’s krona led gains among Group-of-10 peers, though the Japanese yen remained supported on haven demand. The Australian dollar advanced on month-end flows, with a stronger yuan also spurring appetite for the commodity-linked currency.

In rates, Treasuries were unchanged with long-end supported ahead of month-end. Yields are off richest levels of the day as e-minis recouped some early losses. Treasury yields are within a basis point of Thursday’s close, slightly lower across the curve; 10-year yields around 0.82%, remain toward cheaper end of 0.74% to 0.84% weekly range and outperforming bunds, gilts by almost a basis point each. Treasuries rallied in early Asia session as Apple stock fell over 4% in after-market trading on Thursday; into early U.S. session Nasdaq e-minis remain lower by 1.2%, S&P e-minis are off 0.9%.

In commodities, oil was flat after suffering a recent rout, while spot gold headed for its third consecutive monthly decline. Crude oil was little changed in New York.

On today’s calendar AbbVie, Exxon and Charter Communications are among Friday’s scheduled earnings. Personal spending, U. of Michigan sentiment are due.

Market Snapshot

S&P 500 futures down 1.4% to 3,257.75

STOXX Europe 600 up 0.1% to 342.16

MXAP down 1.3% to 172.21

MXAPJ down 1.2% to 572.11

Nikkei down 1.5% to 22,977.13

Topix down 2% to 1,579.33

Hang Seng Index down 2% to 24,107.42

Shanghai Composite down 1.5% to 3,224.53

Sensex down 0.6% to 39,523.90

Australia S&P/ASX 200 down 0.6% to 5,927.58

Kospi down 2.6% to 2,267.15

Brent Futures down 0.03% to $37.64/bbl

Gold spot up 0.2% to $1,871.30

U.S. Dollar Index down 0.04% to 93.92

German 10Y yield rose 1.4 bps to -0.622%

Euro down 0.05% to $1.1668

Brent Futures down 0.03% to $37.64/bbl

Italian 10Y yield fell 7.3 bps to 0.489%

Spanish 10Y yield rose 1.7 bps to 0.15%

Top Overnight News from Bloomberg

Germany and the rest of the euro area’s biggest economies surged in the third quarter, in a rebound that’s now being derailed by an intensifying pandemic and new government restrictions on businesses

European Central Bank policy maker Robert Holzmann said it is right to assume that President Christine Lagarde signaled more monetary stimulus is coming, though not until December

U.K. house prices posted their biggest annual gain since 2015 this month as a revival in the housing market defied a wider economic malaise

Jeremy Corbyn’s suspension from the U.K. Labour Party he led until April threatened to re-open divisions in the party after six months of relative calm under new leader Keir Starmer

Treasury Secretary Steven Mnuchin accused House Speaker Nancy Pelosi of pulling a “political stunt” and holding up a new stimulus bill by refusing to offer compromises, in an escalation of acrimonious finger-pointing over stalled virus-relief negotiations

U.S. new virus cases topped 89,000, setting a new daily record, as the outbreak intensifies ahead of next week’s presidential election. The U.S. is seeing a jump in cases in New York and New Jersey again, and a record outbreak across the Midwest states

France is aiming to limit the drop in economic activity to 15% during the country’s second coronavirus lockdown starting on Friday, Finance Minister Bruno Le Maire said in a government briefing on Thursday

German Chancellor Angela Merkel delivered a wake-up call to fellow leaders in the 27-nation European Union, saying they all failed to step in quickly enough to control the pandemic as the cost of a second lockdown begins to come into focus

Oil is poised for the biggest monthly decline since March as a resurgent coronavirus across the U.S. and Europe raised concerns the fragile demand recovery will be derailed.

Here’s a quick look at global markets courtesy of NewsSquawk

Asian equity markets weakened heading into month-end and after US stock index futures faded the recovery seen on Wall Street amid disappointment from the big tech earnings despite Apple, Alphabet, Amazon, Facebook and Twitter all beating on top and bottom lines. Apple shares declined over 4% in extended trade with investors discouraged by the miss on iPhone sales and lack of guidance, as well as a 29% Y/Y drop in its Chinese revenue which pressured its supply Chain in Asia and Twitter slumped nearly 18% after hours on slower user growth. ASX 200 (-0.6%) and Nikkei 225 (-1.5%) were weaker with industrials and tech frontrunning the declines in Australia although losses in the index were briefly pared by financials as AMP shares surged over 20% following a takeover approach by Ares Management, while the mood in Tokyo was clouded by currency effects and soft inflation data but with Panasonic shares a notable gainer on reports it is working with Tesla to build a new battery cell production line at the Gigafactory. Elsewhere, the Hang Seng (-2.0%) and Shanghai Comp. (-1.5%) remained cautious amid a plethora of large-cap earnings and with participants mulling over the initial details of the 5-year plan which seeks to build the nation into a technological powerhouse and emphasized quality growth over speed but refrained from specifying a targeted pace of growth. Finally, 10yr JGBs were lower and fell below support near 152.00 on spillover selling from T-notes as Wall Street initially nursed losses and following an uninspiring 7yr auction stateside, although the downside for JGBs was cushioned with the BoJ in the market for nearly JPY 1.3tln of JGBs with up to 10yr maturities.

Top Asian News

Hong Kong Economy Shows Early Signs of Revival as Exports Jump

Singapore Overtakes Thailand to Become Asia’s Worst Stock Market

BOJ Widens Buying Ranges While Cutting Frequency for Short Bonds

European equities (Eurostoxx 50 -0.1%) have trimmed opening losses throughout the session despite underpeformance of Stateside peers. After a mixed close yesterday, equities in the region initially succumbed to some of the heavy selling pressure seen after the Wall St. close in the wake of earnings from US tech mega-caps. Despite the likes of Apple, Alphabet, Amazon, Facebook and Twitter recording beats on top and bottom lines, earnings (ex-Alphabet; up 5.6% pre-market) were received poorly with Apple shares currently lower by 4.5% in pre-market trade following a miss on iPhone sales and lack of guidance, as well as a 29% Y/Y drop in its Chinese revenue. Social media names Facebook (-2.4%) and Twitter (-17.5%) are seen lower ahead of the cash open, whilst e-commerce giant Amazon (-2.1%) are also lagging with some citing soft operating income guidance for December. In Europe, given the gravitational pull of the aforementioned large-caps, stocks across the continent commenced the session on the backfoot before staging a mild recovery with little in the way of clear fundamentals behind the move; as context the Eurostoxx 50 is lower by 6.4% on the week. Sectoral performance is somewhat mixed with oil & gas names the clear outperformer in the wake of earnings from Total (+2.3%) who reported a heavy beat on Q3 net income and maintained its dividend despite the likes of BP, Shell and Eni trimming theirs in 2020. Elsewhere, banking names are also performing well this morning following Q3 results from Natwest Group (+5.6%) which saw the Co. beat expectations for quarterly pre-tax profits and suggest that FY impairments are seen at the lower end of the range. IAG (+2.6%) have lent some support to the travel & leisure sector despite reporting a wider than expected loss for Q3 operating income with the CEO noting that his top priority will be reducing the Co.’s cost base. To the downside, underperformance has been observed in personal & household goods and food & beverage names. Health care names are also softer on the session following earnings from Novo Nordisk (-1.5%) with the insulin producer missing on expectations for EBIT and net profits.

Top European News

Spanish Banks Join EU Peers in Painting Rosier Bad Loans Picture

Continental CEO Degenhart to Resign, Citing Health Reasons

Italy in Talks With Paschi on $1.75 Billion Capital Increase

U.K. House Prices Jump Most in Five Years as Boom Gathers Pace

In FX, the Dollar remains relatively firm and resilient given a loss of safe-haven status or less demand amidst a fragile recovery in risk sentiment, month end portfolio rebalancing and positioning ahead of next week’s US Presidential Election. However, the index is back below 94.000 and Thursday’s 94.105 high within a 93.983-762 range as several major counterparts claw back some lost ground before another raft of data, the Chicago PMI and final Michigan sentiment.

JPY/AUD – Leading the aforementioned G10 recovery in spite of somewhat mixed Japanese CPI, unemployment and ip updates, the Yen is back above 104.50 and a key Fib at the half round number alongside hefty option expiry interest (2.2 bn). On the flip-side, 1.4 bn expiries at the 104.00 strike will act as a barrier and support for Usd/Jpy after the pair got to within 2-3 pips of the level yesterday, and conversely the Aussie appears to be drawing comfort from the fact that it survived an equally close shave with 0.7000 to probe 0.7050 with assistance from ANZ’s CEO arguing against an RBA ease next week on the grounds it would flood the financial system with more liquidity, impair bank profitability and only boost the economy and jobs marginally.

GBP – Also firmer vs the Buck after losing 1.2900+ status on Wednesday and maintaining momentum against the Euro close to 0.9000 in wake of the ECB, though wary of ongoing Brexit uncertainty and end of month Eur/Gbp cross flows that can deviate from RHS to LHS quite sporadically.

NZD/EUR/CAD/CHF – All narrowly mixed vs the Greenback, as the Kiwi regains hold of the 0.6600 handle in wake of another upbeat sentiment survey (ANZ consumer confidence up to 108.7 in October from 100.0 previously), and the Euro pares some post-ECB losses after basing at 1.1650. Note, this coincided with the 100 DMA, which is now 5 pips firmer and the 2 chart points also align with 1.5 bn option expiries for today’s NY cut. Perhaps predictably, market contacts tout stops on a break of 1.1650 that would expose a virtual double bottom from late September (1.1615-12). Elsewhere, the Loonie is deriving a degree of comfort from stability in oil prices and the generally less risk averse tone to retest 1.3300 from 1.3390 or so, but the Franc is still lagging below 0.9150 and hovering near 1.0700 against the Euro.

In commodities, WTI and brent are modestly firmer this morning in a pull-back from some of the overnight losses after sentiment took a hit on the earnings-spurred downside in US equities last night. Following this, the crude complex has continued to lift off lows throughout the session alongside sentiment in general; WTI and Brent are currently firmer by around USD 0.30/bbl. Turning to OPEC where the Iraq oil minister pushed back on reports that the country and others are considering a rollover of existing OPEC+ output cuts into 2021 given developments on both the demand & supply side. While the remark is interesting there is still over a month until the next OPEC+ gathering and as such a pushback on such commentary at this stage is perhaps not too surprising. Elsewhere, the BSEE report of 43-companies had just shy of 85% of oil shut-in for the Gulf given Storm Zeta; its worth noting the storm is continuing to dissipate and as such production should be restored to the Gulf over the next few days – assuming no damage occurred. Moving to metals, spot gold is modestly firmer this morning as the USD has dipped as sentiment sees a moderate pick up from a European perspective. Separately, mining updates saw Glencore confirm their FY production guidance with the exception of coal given strike action at the Cerrjeon site; additionally, their YTD copper production is -8% vs. the prior period.

US Event Calendar

8:30am: Personal Income, est. 0.4%, prior -2.7%

8:30am: Personal Spending, est. 1.0%, prior 1.0%

8:30am: Employment Cost Index, est. 0.5%, prior 0.5%

8:30am: PCE Core Deflator YoY, est. 1.7%, prior 1.6%

9:45am: MNI Chicago PMI, est. 58, prior 62.4

10am: U. of Mich. Sentiment, est. 81.2, prior 81.2; Current Conditions, est. 84.9, prior 84.9; Expectations, est. 78.8, prior 78.8

DB’s Jim Reid concludes the overnight wrap

For the first 40-odd years of my life Halloween was a minor curiosity. My Dad’s dislike of trick or treaters didn’t help cement it in my social calendar as a kid. However since we’ve had kids my wife has slowly ensured it’s become a bigger and bigger event. Last night I learnt that she has gone into overdrive and bought what I thought were pretty expensive costumes ahead of us going to a pumpkin picking Halloween themed afternoon tomorrow at a local farm. Apparently I have an extravagant ghost costume and the twins have matching baby ghost costumes. My wife and Maisie have mother and daughter witch costumes and broomsticks. I’m not sure what the Halloween version of bah humbug is (maybe boooo humbug), but I’m slowly having it drummed out of me.

Over the last 24 hours we’ve gone from treat to trick as the prospect of big tech earnings first lured investors back in and then disappointed when they arrived after the bell. The S&P 500 was up over +2% late in the actual session last night prior to a sharp 70bp pullback in the last half hour of trading. It still closed +1.19%, with the NASDAQ rising a greater +1.64%.

After the close, Apple (+4.53% daily gain) fell over -4% even as its quarterly results beat estimates with record sales of Macs and services. However the largest US company also revealed that iPhone revenues fell -21% with revenue in Greater China, one of the company’s most important regions, falling by -29% to the lowest level since 2014. Amazon (+2.33% earlier) was down nearly -2% after giving up an immediate postmarket gain as revenue and earnings both solidly beat analyst estimates. The dip came after the CFO indicated that covid-related expenses will go up to $4 billion. Facebook’s (+5.75% earlier) shares were down over -2.5% in the after-market, even as revenues and user growth both beat estimates. On a more positive note, Google’s (+4.16% earlier) parent company, Alphabet, gained over +6% in after-market trading with news that the company’s digital advertising profits bounced back strongly from the previous quarter.

As a result, S&P 500 and Nasdaq futures are down -1.39% and -1.90% respectively as we type. Asian markets have also taken another leg lower with the Nikkei (-0.84%), Hang Seng ( -0.50%), Asx (-0.55%) and Kospi (-1.43%) all down. Chinese markets are more mixed with the Shanghai Comp up +0.08% while the CSI is down -0.09%. In FX, cable is down -0.18% to $1.2907 as more and more areas in England are moving to the topmost tier of restrictions. Meanwhile, yields on 10yr USTs are down -1.8bps this morning

Overnight, we also got a look into some details of China’s new five-year economic plan, which had tech in focus. The new plan elevated China’s self-reliance in technology into a national strategic pillar. Senior party officials of the Communist Party said that the nation would accelerate development of the kind of technology needed to spur the next stage of economic development with focus on bold measures to cut reliance on foreign know-how.

Back to yesterday and European stocks tried to turn positive after three straight days of declines to start the week as ECB President Lagarde outlined steps the central bank could take in December to recalibrate monetary policy in light of the worsening pandemic (more below). Her comments saw the STOXX 600 rise +1.76% off the lows of the day, however part of those gains were given back in the last half hour of trading with the index ending down -0.12% on the day. While the DAX (+0.32%) gained, other bourses such as the CAC (-0.03%) and FTSE (-0.02%) were not able to stay above water. European futures are down around -1.2% this morning.

As our economists point out (see their note here) this was a unique ECB meeting as for the first time we saw a unanimous post-dated decision to act at the next meeting (December in this case). The composition of that action remains to be determined however, and will be a function of events, both pandemic and economic, over the next six weeks. Our economists suggest that the emphasis on “all instruments” being under consideration is a message to think beyond just PEPP. The sensitivity to weak private credit implies changes to the TLTRO framework. For the time being, they hold onto their view of a composite easing strategy in December: a package of measures, including tweaks to the TLTRO framework, to complement more PEPP in one form or another to address the pandemic risk and more APP to address the persistent low inflation problem.

As they also point out, six weeks can be a long time in a non-linear pandemic. However, post-dated action is not to be confused for ECB inactivity for the next six weeks. ECB President Lagarde emphasised the flexibility of existing programmes like PEPP to respond to any downside surprises. There is still more than half the PEPP available and it is flexible enough to be deployed on an “anytime, anyplace, anywhere” basis. The pace of purchases can re-accelerate if necessary.

The euro fell -0.61% by the end of the day to one month lows but that was as much due to dollar strength as half the move occurred before the ECB meeting. 10yr bund yields fell -1.1bps to -0.64%. With the signal of added ECB support peripheral bond yields fell, with Italian (-6.2bps), Spanish (-3.4bps), Greek (-10.7bps) and Portuguese (-3.5bps) 10yr bonds all tightening to 10yr bunds. US Treasuries fell with the risk on sentiment, as yields rose +5.2bps to 0.823%, the largest one day rise in over three weeks.

In terms of data, the US economy expanded at a record 33.1% (annualised) pace off the lows of the pandemic, with business reopening and consumer spending powered by stimulus injections. The rise in GDP, which on a quarterly basis is 7.4%, slightly beat market expectations of 32.0%, and comes after Q2’s also record decline of -31.4%. Overall, GDP is now -3.5% below pre-virus (Q4 2019) levels. In terms of components, consumer services spending was -7.7% below pre-virus levels, but consumer goods spending +6.7% above. There was also initial jobless claims out of the US, where claims in regular state programs totaled 751k in the week ended Oct. 24, down 40k from the prior week. Continuing claims decreased 709k to 7.76mn in the week ended Oct. 1, having now fallen for five straight weeks. Overall these were positive data points, but the virus’s progression may impact the winter readings going forward.

With less than five full days before polls close in the US elections, former Vice President Joe Biden is currently in a strong position with the fivethirtyeight.com model giving him an 89% chance of winning, the highest so far, and a national polling average lead of +8.8. Biden holds strong polling leads in the key Midwest swing states of Pennsylvania (+5.2pts), Wisconsin (+8.4pts), and Michigan (+8.1pts), and is also leading to a smaller degree in the Sunbelt swing states of Florida (+2.1pts), North Carolina (+2.2pts) and Arizona (+2.7pts). Biden can win by just carrying the Midwest but, as has been highlighted before, we are likely to know results from the latter group of states earlier because they process mail-in ballots ahead of the election and both Florida and North Carolina will also be allowed to count votes ahead of time. A quick win there for Biden and the “Blue Wave” could materialise rapidly, but a Trump win in that part of the map and we could be waiting until the end of the week at least. The Secretary of State in Pennsylvania has said that the “overwhelming majority” of votes should be counted by next Friday, but that is still at least 3 days of uncertainty and that is before we get to any implications of Supreme Court rulings.

Staying on politics EU Commission President Ursula von der Leyen stated that Brexit talks are ‘making good progress’ and are now ‘boiling down to the two topics that are the most important – Level Playing Field and fisheries’. These two issues as well as a mechanism in the final treaty for resolving future disputes are among the most important outstanding points. European Council President Michel, expressed the expectation that the state of the negotiations would probably be assessed next week with his hope being to start the ratification process in mid-November.

On the coronavirus, hospitalisation rates in some countries are approaching peak levels seen during the first wave. Belgium reported 5,924 patients currently hospitalised, surpassing its previous peak from back in April. While in Portugal, the number of ICU patients is now 269, just short of its previous peak of 271. Similarly in Italy, there are now 17,615 patients in hospitals, though capacity still remains there compared to the nearly 29,000 back in April. This is why countries throughout Europe have been enacting new restrictions to try to flatten the curve again. Yesterday Sweden, whose actions have been among the most scrutinised, announced that residents in Stockholm are to avoid shops, gyms and any other indoor venues that don’t provide essential services. This comes as the country has seen around 3,000 new cases, a record daily rise. In the US, weekly cases have hit record highs as the virus continues to spread through the Southern and Midwestern regions. However yesterday there was troubling news out of the northeast, which had been resistant to a second wave, as New Jersey’s and New York’s positivity rates of covid-19 tests hit their highest levels since May. Lastly Dr Fauci predicted yesterday that normality may not return until late 2021 even with an effective vaccine broadly distributed.

Looking ahead to today there will be readings of France, German, Italian and Euro Area Q3 GDP. As well as CPI data for France and Italy and unemployment data for Italy and the Euro Area. In the US, we will get personal spending and income data along with PCE core deflator. There is also the MNI Chicago PMI and final University of Michigan sentiment reading for October. In terms of Central Banks, the ECB’s Weidmann is expected to speak. About halfway through earnings, we will see results today from Novo Nordisk, AbbVie, ExxonMobil, Charter Communications, Chevron, Total and NatWest Group.

via ZeroHedge News https://ift.tt/3mOiUJd Tyler Durden

In my final guest post, I’ll turn to the implications of the original meaning of the citizenship clause for originalism and modern law. Before I do, I want again to thank Eugene Volokh and the Volokh Conspiracy for inviting me, and to thank everyone for your comments and criticisms. The discussion may continue over at my regular blog, The Originalism Blog.

With some oversimplification, originalism is the view that the Constitution’s original meaning should bind modern governmental actors (what Lawrence Solum calls the constraint principle). As described in prior posts, the original meaning indicates that persons born in U.S. overseas territories are born “in” the United States and that U.S.-born children of people not lawfully present in the U.S. are born “subject to the jurisdiction” of the United States. Originalism’s constraint principle would require modern governmental actors to recognize people in these categories as U.S. citizens.

This originalist outcome may seem odd, though. The clause’s enactors likely did not foresee that their constitutional language would resolve either question. Neither question was part of the 1866-1868 citizenship debates. The U.S. didn’t have material overseas territories until 1898. Materially restrictive federal immigration law didn’t begin until the 1880s. The originalist resolution is therefore accidental: the enactors could have chosen other language to accomplish their goals that might have affected these modern debates differently. What justifications for originalism explain enforcing outcomes that the enactors could not contemplate?

Several common justifications seem unhelpful here. One is that modern law should respect the wisdom of the framers. A related idea invokes the framework in which the Constitution was adopted. John McGinnis and Michael Rappaport argue that the supermajority process required to adopt constitutional provisions tends to produce good results. Similarly, it’s said that adopting or amending a Constitution occurs in an atmosphere in which people undertake unusually thoughtful reflection on long-term goals and structures, in contrast to ordinary short-term political thinking.

These approaches share the common feature that they suppose adherence to original meaning produces (on balance) desirable substantive outcomes due to the way the text was adopted as law. Invoking the constraint principle to bind modern political actors is justified by the results. But this justification seems inadequate where the enactors didn’t choose the constraint that is now applied. With the citizenship clause, for example, the enactors likely didn’t understand the policy questions involving birth in overseas territories or birth to persons not lawfully present in the United States. Invoking the constraint principle to resolve these policy questions today (instead of leaving them to the political branches) is difficult to justify on the basis of the enactors’ wisdom or the enactment’s structural advantages. The text’s resolution of the policy questions arises from fortuity, not choice.

A second set of justifications for originalism rests on popular sovereignty. Regardless of the desirability of the enactors’ choices, those choices should (it is said) be honored because they were made through a democratic process encompassing the people’s will. Again, though, it is not clear why modern political actors should be bound to outcomes not deliberately chosen by the people at the time of enactment. If “the People” in adopting the Fourteenth Amendment couldn’t have foreseen that they were resolving key modern debates over citizenship, the resolution is only a fortuity of the language chosen, not a deliberate constitutional commitment of the popular sovereign.

These concerns might not worry those, such as my colleague Larry Alexander, who adopt an “original intent” view of originalism. Intentionalists might say that the best originalist way to apply the framers’ enactment is to constrain the political branches only in the paradigm situations the enactors actually understood and confronted, while leaving further extensions or non-extensions to the political branches.

But most modern originalists call themselves “original meaning” originalists (following Justice Scalia), not “original intent” originalists. So they need a justification for treating the citizenship clause’s text as binding even in its “accidental” applications.

I think there are two related justifications. The first is modern originalism’s core commitment to rule-of-law values, specifically (in the case of a written document) to the rule of written law. Professor Solum discusses this commitment at length in justifying the constraint principle. Rule-of-law values such as stability, objectivity, and predictability are served by following the text’s original meaning even if that meaning constrains modern political actors in ways the enactors couldn’t foresee.

Originalism’s rule-of-law commitment also arises from a formalistic idea of what the law is. This commitment underlies Justice Scalia’s pioneering shift from original intent to original meaning. The law, he insisted, is what was enacted: the text, not the intentions. A formalist conception of law requires that the text be applied to the full extent of its meaning even if that goes beyond (or not as far as) the enactors’ conscious design.

Originalism’s commitment to formalism and rule-of-law values isn’t incompatible with commitments to the framers’ wisdom, the structure of the enactment process, or the idea of popular sovereignty. In many (perhaps most) cases, the justifications will run in parallel. Commitment to the text’s original meaning commonly validates these other justifications because the text is (usually) the best evidence of the enactors’ design. But as the citizenship clause indicates, original meaning and the enactors’ design will sometimes diverge. At that point, rule-of-law considerations appear to dominate and justify original meaning originalism’s adherence to the text without exception.

Categorical adherence to original meaning is reinforced by an important practical concern. To this point, I’ve assumed that it’s possible to separate clearly situations in which the enactors deliberately resolved a modern policy choice and situations in which they resolved it only accidentally. But those situations may not be so easily distinguished. Even with the citizenship clause, some authorities have suggested that the enactors could have foreseen the issues of overseas possessions and undocumented migrants. Beyond the citizenship clause, categorization difficulties become even more apparent. What if the enactors deliberately chose to constrain the political branches in a certain way, but new policy considerations, not present at the time of enactment, arise to suggest that the policy decision has additional dimensions the enactors could not foresee? Pursuing such inquiries necessarily injects uncertainty and subjectivity into the interpretive process. Originalism applied with such qualifications may resemble non-originalism and cease to provide dependable constraint on judges or the political branches. Originalism’s commitment to rule-of-law values will sharply oppose such moves as undermining objectivity, stability, and predictability; originalism’s formalism will insist that the solution is the (relatively) concrete rule of original textual meaning, irrespective of whether that meaning reflects a deliberate policy choice of the enactors.

The formalist approach is compatible with other justifications for originalism. Those who rest originalism on the framers’ wisdom may believe that, on balance, the best way to effectuate the framers’ wisdom is to apply the framers’ text categorically, even to situations in which it may appear that the framers did not make a deliberate policy choice. The alternative is case-by-case evaluation of the text’s compatibility with the framers’ choices, which, in addition to being unstable and unpredictable, may, due to institutional limitations and bias, not deliver superior results. Thus, other justifications for originalism may combine with and complement originalism’s formalism, rather than stand as an alternative to it. But the example of the citizenship clause indicates, I think, that formalism is originalism’s core.

from Latest – Reason.com https://ift.tt/3ecd7dd

via IFTTT

More than two decades ago, Virginia Postrel published a prescient book with a wonderful title: “The Future and Its Enemies.” The technological revolution that has led to “greater wealth, health, opportunity and choice than at any time in history,” she argued, has resulted in “a chorus of intellectuals and politicians [that] loudly laments our condition.”

Sadly, the future’s enemies use the government to fight inevitable innovation and progress.

These critics bemoan the economic insecurity such advances have wrought, as well as other first-world problems ranging from our “enslavement” to technology to the supposed (but not actual) despoliation of the Earth. When she published the book, “smart phones” were rather dull. They were large, clunky, and served solely to make phone calls. It’s inconceivable how far those—and other common products—have developed in the ensuing years.

I recall my prized eight-track tape player, my first car with its whopping 70 horsepower and AM-only radio, phone booths, library card catalogs, pneumatic tubes for delivering office documents (Google it), video stores, and, my favorite, Qwip machines. The latter was cutting-edge in the 1970s. The sender put a document on a cylinder that would spin. It slowly transmitted a facsimile of the document—line by line and in crude fashion—to carbon paper at the other end.

Today I scanned and emailed dozens of documents and shudder at the thought of doing things in that archaic manner. By the way, it’s easy to get caught up in the consumer-oriented improvements we cherish while forgetting about, say, the vast improvements in food production that have dramatically reduced world hunger and the many life-saving medical advancements.

In California this year, the fight over the future centers on Proposition 22, which would allow companies such as Uber, Lyft, and DoorDash to classify workers as independent contractors rather than as permanent employees. Obviously, technology has disrupted the way we travel, shop, and work, which has made our lives much better—but has infuriated labor unions, which find it tougher to organize workers in the flexible new work world.

I’ve noted this before, but they’ve clearly taken on the role of the 19th Century British Luddites—textile workers who couldn’t compete with mechanized looms, so they vandalized them. Modern unions don’t destroy property these days—but they lobby the government to do something worse. They try to hobble those industries that are moving the world forward.

A few weeks ago, I took a taxicab for the first time in months. The driver didn’t want my business because, apparently, it wasn’t a good-enough fare. The cab was grimy. He balked at my credit card, and it took time to process it after I insisted. Compare that to the friendly and seamless experiences we have with Uber and Lyft. Think about the deliveries we receive—and how they allow us to avoid those laborious trips to box stores and restaurants.

Proposition 22 is a reaction to Assembly Bill 5, which went into effect in January. The law, signed by Gov. Gavin Newsom and championed by unions, codified a 2018 California Supreme Court decision (Dynamex) that applied a strict test to companies that want to hire freelancers. The measure would exempt drivers from A.B. 5’s provisions—and provide them with some portable benefits.

After A.B. 5 became law, it had vast should-have-been-seen consequences. Instead of bringing workers onboard full-time and paying them benefits, companies started laying off their California contractors. Californians who had good jobs but used freelance and contractor work to earn some side income had to give up their lucrative gigs. Consumers suffered, too, as they endured rising prices and fewer choices—all in the midst of a pandemic.

That’s why even the union-controlled California Legislature exempted more than 100 industries from A.B. 5’s strict provisions. They exempted almost every major industry, except for those increasingly vital transportation and delivery services.

If voters approve Proposition 22, the state will have a groundbreaking labor law that applies to virtually no one, yet that hasn’t stopped the labor movement from touting it as a nationwide model. If California voters approve it, they will slow this new Luddite movement from spreading.

Unions can’t stop the future, but they can cause misery as we await its arrival. For instance, our union-allied attorney general, Xavier Becerra, has filed lawsuits against the transportation companies to force them to comply with A.B. 5 as we await the election. The companies were hours away from suspending operations here until a court issued a temporary stay. This is nonsensical in a state that sees itself as the embodiment of progress.

Even if labor wins at the polls this November, it will have no more long-term success than any other group that has tried to fight a changing world. Like water rolling down a hill, creative minds will find their way around every obstacle. Sorry, but the union vision of factory floors and cubicles is a vestige of the past—not a roadmap to the future.

This column was first published in The Orange County Register.

from Latest – Reason.com https://ift.tt/3jFfbeY

via IFTTT

The Witches raises a number of questions, primarily Why?

Why has Anne Hathaway, as the head witch here, been allowed to affect a braying Zsa-Zsa-Lugosi Hungarian accent that might have been designed to trigger tension headaches in anyone exposed to it?

Why was it felt wise to digitally accessorize Hathaway with a huge stretchy mouth filled with huge razory teeth, as though she were auditioning for an all-female Venom spinoff?

Why does this whole movie, from the singing-dancing rodents to the madly tumbling witches, look as if it had been marinated in pricey CGI? It’s not that the digital animation isn’t good – it’s top-shelf, with characters capering through chase scenes and interacting with their environments in highly complex ways. Great stuff. Also, after a short while, kinda boring.

The tech overload here is no surprise, actually. The director, Robert Zemeckis, has made a number of very popular (and some very good) films over the years—Back to the Future, Forrest Gump, Used Cars. But he was also an early fan of computer-generated imagery and has created such Uncanny Valley classics as Polar Express and Beowulf. Anyone who’s sat dozing through those two films might want sit out this one.

The Witches is the second big-screen adaptation of Roald Dahl’s 1983 fantasy novel. (The first, still warmly regarded, was directed by Nicolas Roeg and starred Anjelica Huston.) The story remains pretty much the same. A young orphan (Jahxir Bruno) —nameless in the book but dubbed “Hero Boy” in the movie’s credits—is living with his grandmother (Octavia Spencer) at her home in rural Alabama. Grandma, we learn—at a somewhat mopey pace—was once a witch hunter, and so knows what’s happening when spooky crone sightings begin to crop up. To protect her grandson, she takes him to a fancy seaside resort. But it turns out that a coven of witches has also booked rooms there, styling themselves the International Society for the Prevention of Cruelty to Children. (Witches are great kidders.) The group’s maximum leader, the Grand High Witch (Hathaway), has come up with a nasty new plan for the human race: It involves a “mouse maker” potion, of which the GHW has brought along a copious supply. She wants her minions to return to their various hometowns and start opening candy stores. Then she wants them to lace their candy with the “mouse maker” concoction. After the kids transform into rodents, their own parents might unwittingly kill them.

As a longtime Anne Hathaway fan, it pains me to ask how much better this movie might have been without her in it. Her over-the-top sashaying will surely send some viewers rearing back in alarm, while others might be put off by the telltale witchy signs with which her character has been adorned – the scabby scalp rash (from the wigs she must wear—witches are bald), the three-fingered hands, the single-taloned feet. Hathaway puts a lot of effort into this un-charming character—not a moment passes in which she’s not killin’ it—but it’s tiresome.

On the plus side, there’s deluxe production design by Gary Freeman that makes you want to slip onto the cozy sets and take a restorative nap. There’s also the great Stanley Tucci, reuniting with Hathaway for the first time since The Devil Wears Prada. Tucci can improve a movie just by walking through a scene; here, unfortunately, playing the hotel manager, Mr. Stringer, he’s mainly called upon to dither.

The dialogue is fine, for the most part, with the exception of a few potted homilies like “Never give up what you are inside—the sort of soft-focus thinkery that cries out for a punchline.

from Latest – Reason.com https://ift.tt/3mw95z6

via IFTTT

Biden Campaign Accuses Facebook Of Favoring Trump After ‘Glitch’ Takes Down 1000s Of Ads Tyler Durden

Fri, 10/30/2020 – 07:12

Facebook announced last month that it would bar new political ads from being run on its platform during the last week of the election, part of CEO Mark Zuckerberg’s effort to signal to Democratic lawmakers that the company was taking its role as a ‘guardian of democracy’ seriously.

Barring new ads during the final week of the campaign seemed more like a kafkaesque nuisance, rather than a sensible tactic to try and cut down on mudslinging and misinformation associated with the election. And since no half-hearted attempt at virtue-signaling goes unpunished, Facebook is facing backlash from Joe Biden’s campaign, which has accused the company of favoring President Donald Trump after thousands of Joe Biden ads were inexplicably blocked.

Facebook has mistakenly blocked thousands of Joe Biden advertisements from appearing on its platform with just days to go until the US presidential election, according to the Democratic challenger’s campaign, as the company struggles to implement its latest policy to combat misinformation.

Mr Biden’s campaign said on Thursday night that many of its Facebook advertisements were still not appearing on the site after the social media company attempted to clamp down on new political ads in the final stretch of the campaign.

Facebook blamed the glitches on “unanticipated issues”, brushing off suggestions that they were evidence of bias towards the campaign of President Donald Trump or the Republicans.

Ironically, despite all the company’s attempts to keep itself out of the media crossfire, the glitches have “once more placed Facebook at the center of a political row in the heat of a US presidential campaign.” Biden campaign digital director Rob Flaherty said in a statement that “We find ourselves five days out from election day, unable to trust that our ads will run properly, or if our opponents are being given an unfair, partisan advantage.”

Facebook delivered a lengthy explanation to Bloomberg, claiming that the glitch had also disrupted Trump Campaign ads as well.

Facebook Inc. revealed Thursday how internal technical glitches had disrupted the delivery of some ads from the Joe Biden and Donald Trump campaigns, but said it made changes to resolve those hiccups in the run-up to the November U.S. presidential election.

The social media giant’s admission followed complaints from the Biden camp about how thousands of its ads had been blocked. Facebook said in a blog post it spotted “unanticipated issues” affecting both campaigns, including technical flaws that caused a number of ads to be “paused improperly.”

“No ad was paused or rejected by a person, or because of any partisan consideration,” Facebook said in its post. “The technical problems were automated and impacted ads from across the political spectrum and both Presidential campaigns.”

Facebook issued a rule for this election season to prevent new ads from entering the system in the week before the vote, to make it easier to address problems with misinformation, such as candidates announcing victory prematurely. But political ads were supposed to be allowed if they were in by the deadline.

Well, now that Facebook has settled that, the Biden campaign and its Democratic allies can go back to bashing the company for allowing the ‘information terrorists’ Ben Shapiro and Dan Bongino to share dangerous conservative talking points.

via ZeroHedge News https://ift.tt/35KAA1n Tyler Durden

The Witches raises a number of questions, primarily Why?

Why has Anne Hathaway, as the head witch here, been allowed to affect a braying Zsa-Zsa-Lugosi Hungarian accent that might have been designed to trigger tension headaches in anyone exposed to it?

Why was it felt wise to digitally accessorize Hathaway with a huge stretchy mouth filled with huge razory teeth, as though she were auditioning for an all-female Venom spinoff?

Why does this whole movie, from the singing-dancing rodents to the madly tumbling witches, look as if it had been marinated in pricey CGI? It’s not that the digital animation isn’t good – it’s top-shelf, with characters capering through chase scenes and interacting with their environments in highly complex ways. Great stuff. Also, after a short while, kinda boring.

The tech overload here is no surprise, actually. The director, Robert Zemeckis, has made a number of very popular (and some very good) films over the years—Back to the Future, Forrest Gump, Used Cars. But he was also an early fan of computer-generated imagery and has created such Uncanny Valley classics as Polar Express and Beowulf. Anyone who’s sat dozing through those two films might want sit out this one.

The Witches is the second big-screen adaptation of Roald Dahl’s 1983 fantasy novel. (The first, still warmly regarded, was directed by Nicolas Roeg and starred Anjelica Huston.) The story remains pretty much the same. A young orphan (Jahxir Bruno) —nameless in the book but dubbed “Hero Boy” in the movie’s credits—is living with his grandmother (Octavia Spencer) at her home in rural Alabama. Grandma, we learn—at a somewhat mopey pace—was once a witch hunter, and so knows what’s happening when spooky crone sightings begin to crop up. To protect her grandson, she takes him to a fancy seaside resort. But it turns out that a coven of witches has also booked rooms there, styling themselves the International Society for the Prevention of Cruelty to Children. (Witches are great kidders.) The group’s maximum leader, the Grand High Witch (Hathaway), has come up with a nasty new plan for the human race: It involves a “mouse maker” potion, of which the GHW has brought along a copious supply. She wants her minions to return to their various hometowns and start opening candy stores. Then she wants them to lace their candy with the “mouse maker” concoction. After the kids transform into rodents, their own parents might unwittingly kill them.

As a longtime Anne Hathaway fan, it pains me to ask how much better this movie might have been without her in it. Her over-the-top sashaying will surely send some viewers rearing back in alarm, while others might be put off by the telltale witchy signs with which her character has been adorned – the scabby scalp rash (from the wigs she must wear—witches are bald), the three-fingered hands, the single-taloned feet. Hathaway puts a lot of effort into this un-charming character—not a moment passes in which she’s not killin’ it—but it’s tiresome.

On the plus side, there’s deluxe production design by Gary Freeman that makes you want to slip onto the cozy sets and take a restorative nap. There’s also the great Stanley Tucci, reuniting with Hathaway for the first time since The Devil Wears Prada. Tucci can improve a movie just by walking through a scene; here, unfortunately, playing the hotel manager, Mr. Stringer, he’s mainly called upon to dither.

The dialogue is fine, for the most part, with the exception of a few potted homilies like “Never give up what you are inside—the sort of soft-focus thinkery that cries out for a punchline.

from Latest – Reason.com https://ift.tt/3mw95z6

via IFTTT

The terrorist who beheaded a woman and killed two others near a church in Nice, France has been revealed to be a Tunisian boat migrant who arrived on the Mediterranean island of Lampedusa last month.

The attack followed the beheading of Samuel Paty earlier this month, a school teacher who was targeted as part of a revenge attack for showing cartoons of the Prophet Muhammad to pupils in a class about free speech.

It’s now confirmed that the jihadist in Nice, who yelled “Allahu Akbar” during the attack, arrived in Europe as a boat migrant.

“He entered France from Italy – travelling through the southern Italian city of Bari on 9 October – after reaching the Mediterranean island of Lampedusa on 20 September,” reports Sky News.

“He was carrying an Italian Red Cross identity document, and a bag containing two unused knives was found.”

Other sources name the terrorist as 21-year-old Brahim A., saying he was rescued by an Italian rescue boat on September 20 and placed in quarantine due to COVID.

The Tunisian had apparently been subject to an expulsion order by Italian authorities but was able to travel to France via Bari.

This is at least the fourth time that migrants arriving in France as “refugees” have gone on to commit terrorism.

The Chechen teen who beheaded school teacher Samuel Paty earlier this month had been granted a 10-year residency in France as a refugee in March.

The majority of the Paris massacre terrorists exploited the refugee wave to enter Europe.

The three terrorists who went on a knife rampage in Lyon back in April were also Sudanese refugees.

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Also, I urgently need your financial support here.

via ZeroHedge News https://ift.tt/3egM9RF Tyler Durden