12/6/1865: The 13th Amendment is ratified.

The post Today in Supreme Court History: December 6, 1865 appeared first on Reason.com.

from Latest – Reason.com https://ift.tt/31zKSCQ

via IFTTT

another site

12/6/1865: The 13th Amendment is ratified.

The post Today in Supreme Court History: December 6, 1865 appeared first on Reason.com.

from Latest – Reason.com https://ift.tt/31zKSCQ

via IFTTT

‘Never Seen Anything Like It’: Los Angeles Residents Stunned As Violent Crimes Creep Into Wealthier Communities

After two years of rising crime in Los Angeles, residents of upscale neighborhoods are finally starting to freak out after a spate of ‘flash mob‘ lootings at high-end retail stores have been accompanied with a disturbing increase in violent crimes committed in the suburbs, according to the LA Times.

Crews of burglars publicly smashing their way into Los Angeles’ most exclusive stores. Robbers following their victims, including a star of “The Real Housewives of Beverly Hills” and a BET host, to their residences. And this week, the fatal shooting of 81-year-old Jacqueline Avant, an admired philanthropist and wife of music legend Clarence Avant, in her Beverly Hills home.

…these incidents have sparked a national conversation and led to local concern about both the crimes themselves and where the outrage over the violence will lead.

“The fact that this has happened, her being shot and killed in her own home, after giving, sharing, and caring for 81 years has shaken the laws of the Universe,” said Oprah Winfrey, expressing grief over Avant’s killing via Twitter. “The world is upside down.”

The Times notes that while overall crime rates within Los Angeles remain far below the notoriously violent 1990s, much of it has been concentrated in poor communities – so it receives virtually no attention. Now that crime has “crept up in wealthier enclaves and thrust its way to the center of public discourse” across the city.

Turning point?

In 2020, polls showed that California voters largely supported criminal justice reform, as well as rolling back tough sentencing laws to reduce prison populations without nary a thought to how it might affect the crime rate. Now, those concerned about crime and blame liberal policies for its rise are growing more vocal.

For others, it’s been a serious wake-up call.

“I have never seen anything like it,” said Dominick DeLuca, owner of the Brooklyn Projects skateboard shop on Melrose Avenue where burglaries and robberies have seen a sharp enough spike in recent months that he’s now carrying a gun to work. “In the last two years, I have been broken into three times.”

On Thursday, Mayor Eric Garcetti and LAPD Chief Michael Moore advocated for locking offenders up, and questioned several pandemic-related policies that put nonviolent arrestees back on the street without bail.

Moore said arrests had been made in several high-profile “smash-and-grab” burglaries but lamented that the suspects had all been released pending trial. Garcetti said warehousing criminals in jails without rehabilitating them is not a solution, but neither is ceding the streets to repeat offenders.

Los Angeles County Dist. Atty. George Gascón, whose progressive policies around prosecution and sentencing many blame for the uptick in crime, was notably absent at the press conference but said through his office that he is working closely with law enforcement partners to hold perpetrators accountable for such brazen crimes. -LA Times

According to LAPD data through Nov. 27, property crime is up 2.6% YoY, but is down 6t.6% from 2019, while robberies are up 3.9% YoY and down 13.6% from 2019. Burglaries are down 8.4% from last year and 7.7% from 2019. Car thefts, meanwhile, are up nearly 53% vs. 2019.

The difference? Rich people are now getting hit, so officials are officially concerned.

What’s more, violent crime is way up – with homicides jumping 46.7% and shootings up 51.4% vs. 2019. As of the end of last month, there were 359 homicides year-to-date, compared with 355 in all of 2020. That said 2008 was LA’s deadliest year with 384 homicides.

Read the rest of the report here.

Tyler Durden

Mon, 12/06/2021 – 03:44

via ZeroHedge News https://ift.tt/31lCFCQ Tyler Durden

Electric-Car Maker Lucid Plunges After Receiving SEC Subpoena

Lucid Group Inc shares plunged premarket after it released a filing that revealed it received a subpoena last week from the U.S. Securities and Exchange Commission (SEC) about documents related to its blank-check deal.

The Luxury electric-car maker released an 8-K filing Monday morning indicating it “received a subpoena” from the SEC related to an investigation. “Although there is no assurance as to the scope or outcome of this matter, the investigation appears to concern the business combination between the Company (f/k/a Churchill Capital Corp. IV) and Atieva, Inc. and certain projections and statements,” the filing said.

Shares of Lucid fell as much as 11% on the news.

Unlike other EV companies, Lucid insider transactions appear to be mute.

Lucid said the company is “cooperating fully with the SEC in its review.”

Tyler Durden

Mon, 12/06/2021 – 06:54

via ZeroHedge News https://ift.tt/3Ds3imr Tyler Durden

Davos Is Making The Central Bank Case For Gold

Authored by Tom Luongo via Gold, Goats, ‘n Guns blog,

A few months ago I talked about the upcoming changes to the way adoption of Basel III’s new bank reserve rules would alter the gold market.

In short my conclusion was similar to that of Alistair MacLeod’s and others, that Basel III should collapse the egregious manipulation of the gold market through the use of using futures and unallocated gold as bank reserves.

In May I wrote:

In effect, Basel III, if implemented in its current form, would change the gold market from a speculative one based on perceptions of the efficacy of monetary policy to control real interest rates to one that should force price discovery in an almost purely physical market. As I told my Patrons in May 16th’s Market Report video, physical gold will go from being the price taker to the price maker.

I didn’t then nor do I think now that will happen immediately after Basel III goes into effect in the U.K. on January 1st. But I do think the recent weakness in gold has been an early sign of stress within the gold market brought on by the upcoming rules implementations.

And that has sent gold lower in recent weeks despite rising inflation and falling real interest rates. Of course this is because the markets have been overpricing the ‘transitory inflation’ argument put forth by the major central banks.

So, when Jerome Powell came out, in his first important statement post-reappointment announcement, and put a fork in ‘transitory’ inflation the markets were properly shocked. This happened on the heels of OmicronVID-9/11 dominating the headlines and also creating some overblown market reactions thanks to poorly-programmed headline trading algorithms.

For those who have been confused or disagreed with my assessment of Powell for the past six months, thinking Powell was lying about inflation as proof he’s just another idiot Fed Chair, I give you the counter argument. He had to survive the obvious coup attempt put on by Obama and Lael Brainard to oust those not controlled by Davos from the FOMC.

Once that happened, Powell could speak openly because the political storm clouds over his head dissipated. Cue his forcing Treasury Secretary Janet Yellen to finally agree with him on inflation after he put his cards on the table.

Now, we have policy clarity from the Fed.

They will be tapering QE and they will be raising rates in 2022. Now the markets can begin the task of readjusting themselves into year-end. With that in mind, it makes perfect sense to see gold, which has been a losing trade all year under pressure just from tax-loss selling alone, no less expectations of a stronger U.S. dollar.

It also makes sense for high-flying equities to take a hit along with junk bonds which were yielding less than inflation. There are trillions in misallocated capital out there that go far beyond the simple idea that the Fed’s only mandate is to prop up the equity markets.

Powell and those that stand behind him, I have strenuously argued, can see the fight for the future of the monetary system clearly, and it doesn’t include a place for the commercial banks in a world of CBDCs. While one could argue the Fed would like that power CBDCs confer, one could also clearly make the counter argument that it also loses a tremendous amount of power now being just one central bank among many and the dollar just another digital token without value.

Does anyone really believe Wall St. is happy to sign up for this nonsense? City of London?

To get a really good sense of where I think we are in this now, check out my recent appearance on Bitcoin Magazine’s Fed Watch Podcast and Livestream.

Okay so, all that said, let’s really talk about what’s happening in gold.

Because this week we saw two major announcements by two very different central banks vis a vis gold.

Singapore has now joined the ranks of Russia, Turkey, Hungary, Serbia, Poland and others in adding to their central bank gold reserves. This is a very significant move because this is the first country outside of those in Russia’s nominal orbit.

Singapore, outside of Hong Kong, is a major clearinghouse for offshore Chinese yuan settlements. ICBC opened up a branch there in 2012 to handle such transactions and things have only progressed from there.

I don’t necessarily see this as a China-related move by the MAS — Monetary Authority of Singapore — as their monetary policy is very independent and pretty much algorithmic.

They manage the exchange rate of the Singapore dollar (SGD) within a 1% band of expected rates against a basket of currencies, rather than publishing a benchmark rate. Moreover, the MAS is moving away from the old SIBOR / SOR system. SIBOR is Singaporean LIBOR — the interbank overnight lending rate. And SOR is the SGD overnight swap rate.

They, like the U.S., are move to an analogue of SOFR — the Secured Overnight Funding Rate — to replace LIBOR. SORA is Singaporean SOFR for all intents and purposes.

So, why is this important?

If Singapore is worried, like everyone else is about a collapse of the current financial system which is expressly on the table via Davos and the Great Reset, then those with the gold will be in a much better position to defend their currencies during a crisis and maintain a relatively stable global exchange rate.

Since Singapore aims to be the independent broker between East and West, especially now that Hong Kong has all but been taken over by China, this move is very interesting to say the least.

From the Zerohedge article on this there’s is this great point:

For a central bank which actively publishes reams of publications and reports on all sorts of topics related to Singapore’s financial sector and markets and it’s international financial position, this omission about Singapore’s sizeable gold purchases could be considered quite strange, but then again, given that we are dealing with the secretive world of gold and central banks, maybe it’s not so strange.

In addition, MAS is famous for it’s obsession with maintaining and controlling the exchange rate of the Singaporean dollar (versus a basket of currencies), so perhaps MAS prefers not to draw attention to the amount of gold in it’s international reserves as this might encourage FX markets to view the gold purchase as a move that strengthens Singapore’s reserve position and hence could put upward pressure on it’s exchange rate.

Singapore is a key player for the future of pan-Asian finance. If the very savvy MAS is buying gold then they are scared. They are making plans for a very different future where debt becomes the dirtiest word in English.

Moreover, they bought this gold back in May and June and it has only now been discovered on their balance sheet. Why would they not announce these purchases?

For the same reason the Bank of Ireland didn’t tell anyone they nibbled on some physical gold over the summer, so as to not move the price. What’s really significant here is that Ireland is the first euro-zone country to announce gold purchases. Previous to this it was only non-euro EU members like Hungary, Poland and Czechia.

That we’re seeing euro-zone countries begin shoring up their currency reserves with gold feeds the argument I made back in May.

Moreover, just so everyone is also clear what both of these central banks are facing, it isn’t just Europe that is now dealing with insane natural gas prices. Singapore is looking at a catastrophic rise in energy costs. So, if you think the MAS isn’t still toe-dipping without telling anyone into gold to stabilize the SingDollar well, you have a reading comprehension problem.

Now let’s go back to Basel III and talk about how it was supposed to be the thing that finally got gold out of its slump.

Back in May, Powell hadn’t begun defending the U.S. dollar. He hadn’t even had his public spat with ECB President Christine Lagarde yet. Nor had he raised the Reverse Repo Rate he was paying to 0.05%.

So, with Basel III on the horizon and the U.K. exempt until January 1st, 2022, there is still the basic infrastructure in place that if the Fed tightens, which it did through the RRP rate, then gold would be under constant pressure by those needing dollars at cheap rates regardless of the fundamentals.

Short term funding needs always trump long-term fundamentals.

So, the Fed still needs gold kept under wraps to maintain its primacy. But at the same time, the ECB and other Central Banks accumulating gold need it to rise, or at least keep pace with their currency vs. the dollar.

I still believe that dynamic is in play for 2022 and it will finally be the full expression of Basel III that will continue putting a higher floor underneath gold.

Remember, as I wrote back in that May article:

The ECB, on the other hand [vs. the Fed], can go bankrupt, since it has no capacity to [create infinite amounts of elastic money]. All it can do is buy the sovereign debt of the member countries’ central banks and hand them back euros, while swapping around deckchairs on this monetary Titanic. There is a definable limit to this process, especially if rates rise as people lose confidence in the underlying economic activity of those countries and their fiscal positions.

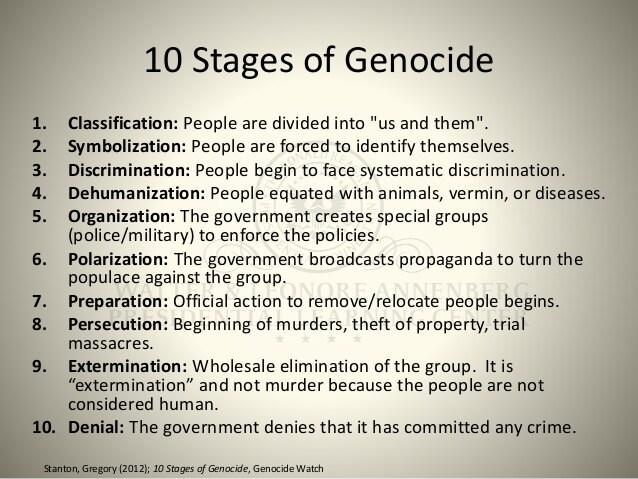

Europe is locking down its economy over OmicronVID-9/11 and removing the unvaccinated from society. They are between steps 7 and 8of 10 on the path to genocide.

Does any rational person believe there will be a renaissance of European economic dynamism in 2022 under these conditions? If you do, you might be a shitlib who believes in unicorn farts, 69 genders and that Elizabeth Warren is an economic genius.

For the rest of us who live in reality-land, of course Europe is the most vulnerable here.

Once Basel III goes fully into effect and paper and unallocated physical gold will no longer be considered as bank collateral for balance sheet purposes, the demand for physical gold because of this need for it as a central bank asset to back national currencies, becomes even more acute.

Those countries lining up on the opposite side of the Great Reset are buying gold while it is still cheap. Powell’s dollar drain since June’s RRP rate hike has gifted everyone with cheaper gold prices for another 6 months.

The MAS buying gold is telling you that what I said back in May is reality:

So, Basel III is coming to destroy the paper gold markets and destroy the money center banks in New York and London while setting the stage to bail out the euro-zone. Higher gold prices are the answer to all of these things. Think of it this way, in a world where debt assets are failing and new private forms of custodial assets are rising in mindshare [bitcoin and crypto], what’s the only real weapon the central banks have to maintain credibility?

Their gold reserves.

This is the essence of why Davos, I think inadvertently, is creating the new role for gold during these times of change.

For the ECB to survive the bankruptcy of Europe gold has to rise.

For emerging market central banks to survive the turmoil unleashed by an epic U.S. dollar rally because of Europe’s bankruptcy gold has to rise.

When China decides to assert itself as the dominant economic player, which I think it would do in the event of a kinetic conflict between it and the U.S., it’s first move will be upwardly revising its official gold reserves… by a lot.

Gold will really rise on that.

Remember the entire Great Reset rests on Davos destroying the current banking system and rolling it up to the central banks, cutting out the classic two-track monetary system with the commercial bankers being the transmission mechanism.

It means them getting control over the Fed, which looks like a lost cause now. Powell is fully in control of FOMC policy, which I expect him to make very clear at the next meeting. This is why Pelosi so easily cut a deal over the debt ceiling.

There will be no further stupid and dangerous brinksmanship calling into question U.S. policy. The markets are demanding clarity from the U.S. Davos’ manufactured chaos through the Democrats’ shenanigans on Capitol Hill should be a thing of the past. That alone will help push capital back towards the U.S.

Davos’ agenda has failed on Capitol Hill, despite winning battles all across Europe and in the English Commonwealth. Those countries are now dead letters until their current governments are overthrown or the people throw off their shackles… not likely.

Despite the market jitters because of the necessary reallocation to global capital, Powell and the Fed now have to pursue tight monetary policy to force the ECB into openly inflationary policy. This will further trash the euro and finally overwhelm the ECB’s bond buying to the point where rates there start rising.

Davos has responded with gutting Europe to the bone with OmicronVID-9/11 lockdowns and forced vaccinations to take down the global demand side of the monetary equation while forcing diplomatic conflicts on China and Russia neither want to stop the flow of goods around the world.

This is why NATO and the Neocons are going wild in Eastern Europe.

It’s why the Israelis are threatening a war with Iran.

And it’s why the O’Biden administration is looking increasingly desperate to bring us to the brink of war without there actually being one.

Just enough conflict, sanctions, sabre rattling and embarrassments to upset China and Russia’s domestic politics while draining them of their economic dynamism through provocations in places like Afghanistan, Syria, Ukraine, Belarus and yes, even Taiwan while trying to force energy prices higher.

Europe is Davos’ power base. That power looks tenuous at best in a geopolitical sense. The best way for it to reassert what power it has left over the U.S. is forcing a massive revaluation in the price of gold while preparing Europe for further federalization, debt default and population reduction, as I discussed in my last article.

The main path for the central banks to maintain any semblance of credibility in the minds of investors rightly freaked out over the events of the past two years is to add to their gold reserves to offset any currency risk to their fiat reserves.

And while the Fed has fought the good fight against this, with the end of QE and rising rates, a flattening yield curve and more turmoil in overseas funding markets as a result of a much stronger dollar, gold will assert itself (alongside bitcoin) as the safe haven asset of choice in 2022.

So, watch the news flow for more signs of Central Bank gold purchases.

So far in 2021, through September, according to the World Gold Council, central banks have purchased 385.4 tonnes of gold, after adding Singapore’s numbers but not Ireland’s. This is roughly on track with expectations for this year of around 15% of total gold demand.

If not for Turkey’s net outflows thanks to the collapse of its banking system (-27.8 tonnes) and the Philippines who sell local mine production to finance the government, the demand would be well over 400 tonnes this year.

But, as I said throughout this piece, it is the players who are doing this now that matters. Earlier Japan made headlines, adding 80.8 tonnes in March. Then Poland began a very Russian monthly buying program in May. Now Singapore is on board trying to offset US dollar strength with gold in an inflationary environment.

And the Irish are now trying to stave off a monetary famine in Europe.

The times they are a’changing rapidly.

* * *

Join my Patreon if you have a role for gold in your life.

BTC: 3GSkAe8PhENyMWQb7orjtnJK9VX8mMf7Zf

BCH: qq9pvwq26d8fjfk0f6k5mmnn09vzkmeh3sffxd6ryt

DCR: DsV2x4kJ4gWCPSpHmS4czbLz2fJNqms78oE

LTC: MWWdCHbMmn1yuyMSZX55ENJnQo8DXCFg5k

DASH: XjWQKXJuxYzaNV6WMC4zhuQ43uBw8mN4Va

WAVES: 3PF58yzAghxPJad5rM44ZpH5fUZJug4kBSa

ETH: 0x1dd2e6cddb02e3839700b33e9dd45859344c9edc

DGB: SXygreEdaAWESbgW6mG15dgfH6qVUE5FSE

Tyler Durden

Mon, 12/06/2021 – 06:30

via ZeroHedge News https://ift.tt/3355h3B Tyler Durden

The Future Of Food Is Now An ETF

As if there wasn’t an ETF for literally everything already…

On Thursday of this week, VanEck announced it would be launching a “future of food” ETF that will trade under the ticker YUMY. The actively managed product is going to “provides exposure to companies engaged in agri-food technology and innovation”.

VanEck says that YUMY “is the first VanEck ETF to incorporate bottom-up, fundamental company research” and is going to be managed by Shawn Reynolds and Ammar James.

Reynolds, who already oversees VanEck’s Environmental Sustainability and Natural Resources Equity Strategies, said: “The growing global population and the concurrent threats from climate change are driving the need for more sustainable agri-food processes and technologies in order to provide for a future with more affordable, nutritious and safe food for all.”

He continued: “We are now in the early stages of a multi-decade agri-food system transformation. Growth opportunities in this space currently exist, but the market remains nascent. A number of private firms appear poised to enter the public markets and several established companies are pivoting their business models to embrace the future of food, so an active approach to stock selection will position YUMY and its investors to capitalize on emerging trends.”

VanEck says that “the growing global population is driving the need for innovation as the population is expected to increase by 25% from 7.8 billion today to nearly 10 billion by 2050.” The company thinks that it may take as much as 70% more food production to feed the middle class of the future.

James said: “These growing needs have to be met with innovation, but they will also have to take into account the demands from both governments and consumers for cleaner, healthier and more environmentally sustainable approaches to feeding the world,”

He concluded: “We’re thrilled to be bringing YUMY to the marketplace and look forward to continuing to share our insights and research with investors and advisors around this essential topic and key investment category.”

Tyler Durden

Mon, 12/06/2021 – 05:45

via ZeroHedge News https://ift.tt/3rF04JW Tyler Durden

Ferguson: Omicron Sounds The Death Knell For Globalization 2.0

Authored by Niall Ferguson, op-ed via Bloomberg.com,

On top of an intensifying cold war between the U.S. and China and other seismic changes, the rapid spread of Covid-19’s newest variant could finish off our most recent phase of global integration.

“Somewhere out there,” I wrote here two weeks ago, “may lurk what I grimly call the ‘omega variant’ of SARS-CoV-2: vaccine-evading, even more contagious than delta, equally or more deadly. According to the medical scientists I read and talk to … the probability of this nightmare scenario is very low, but it is not zero.”

Indeed. Little did I know, but even as I wrote those words something that appears to fit this description was spreading rapidly in South Africa’s Gauteng province: not the omega variant, but the omicron variant.

As I write today, major uncertainties remain, but what we know so far is not good. People are emotionally predisposed to look on the bright side — we are all sick of this pandemic and want it to be over — so it pains me to write this. Nevertheless, I’ll stick to my policy of applying history to the best available data, even if it means telling you what you really don’t want to hear.

First the data: South African cases were up 39% on Friday, to 16,055. The test positivity rate rose from 22.4% to 24.3%, suggesting that the true case number is rising even faster. A Lancet paper suggests that Omicron is likely by far the most transmissible variant yet. There are three possible explanations for this:

A higher intrinsic reproduction number (R0),

An advantage in “immune escape” to reinfect recovered people or evade vaccines, or

Both of the above.

An important preprint published on Dec. 2 pointed to immune escape. South Africa’s National Institute for Communicable Diseases has individualized data on all its 2.7 million confirmed cases of Covid-19 in the pandemic. From these, it identified 35,670 suspected reinfections. (Reinfection is defined as an individual testing positive for Covid-19 twice, at least 90 days apart.) Since mid-November, the daily number of reinfections in South Africa has jumped far faster than in any previous wave. In November, the hazard ratio was 2.39 for reinfection versus primary infection, meaning that recovered individuals were getting Covid at more than twice the rate of people who had never had Covid before. And this was when omicron made up less than a quarter of confirmed cases. By contrast, the same study found no statistically significant evidence that the beta and delta variants were capable of reinfection. And, crucially, at least some of these new infections are leading to serious illness. On Thursday, the number of Gauteng patients in intensive care for Covid almost doubled from 63 to 106.

Data from a private hospital network in South Africa that has over 240 patients hospitalized with Covid indicate that 32% of the hospitalized patients were fully vaccinated. Note that around three-quarters of the vaccinated in South Africa received the Pfizer Inc.-BioNTech SE vaccine. The rest got the Johnson & Johnson vaccine.

Yet these are not the data that worried me the most last week. Those had to do with children. Between Nov. 14 and 28, 455 people were admitted to hospital with Covid-19 in Tshwane metro area, one of the largest hospital systems in Gauteng. Seventy (15%) of those hospitalized were under the age of five; 117 (25%) were under 20. And this is not just a story of precautionary hospitalizations. Twenty of the 70 hospitalized toddlers progressed to “severe” Covid. Up until Oct. 23, before experts estimate omicron began circulating, under-fives represented only 1.8% of cumulative Covid hospital admissions in South Africa. As of Nov. 29, 10% of those now hospitalized in Tshwane were under the age of two.

If this trend holds as omicron spreads to advanced economies — and it is spreading very fast, confirming omicron’s high transmissibility — the market impact could be much bigger than is currently priced in. Unlike with the delta wave, many schools would return to hybrid instruction, parents would withdraw from the labor force to provide childcare and consumption patterns would again shift away from retail, hospitality and face-to-face services. Hospital systems would also face shortages of pediatric intensive care beds, which have not been much needed in prior Covid waves.

South Africa’s top medical advisor Waasila Jassat noted on Dec. 3 that hospitalizations on average are less severe than in previous waves and hospital stays are shorter. But she also noted a “sharp” increase in hospital admissions of under-fives. Children under 10 represent 11% of all hospital admissions reported since Dec. 1.

Here’s what we don’t know yet. We do not know how far prior infection and vaccination will protect against severe disease and death in northern hemisphere countries, where adult vaccination rates are much higher than in South Africa (just 24%). And we do not know if omicron will prove as aggressive toward children in those countries, especially the very young children we have not previously contemplated vaccinating. (Because South Africa has limited testing capacity, we do not know the total number of under-fives infected with omicron in Gauteng, so we do not know what percentage of children are falling sick.) We may not know these things for another week, possibly longer. So panic is not yet warranted. Nor, however, is wishful thinking. It may prove a huge wave of mild illness, signaling the final phase of the transition from pandemic to endemic. But we don’t know that yet.

Now the history.

First, it makes all the difference in the world whether or not children fall gravely ill in a pandemic. Covid has so far spared the very young to an extent rarely seen in the recorded history of respiratory disease pandemics. (The exception seems to be the 1889-90 “Russian flu,” which modern researchers suspect was in fact a coronavirus pandemic.) The great influenza pandemics of 1918-19 and 1957-58 killed the very young as well as the very old. The former also carried off young adults in the prime of life. The latter caused significant excess mortality among teenagers. Up until this point, Covid was the social Darwinist disease: It disproportionately killed the old, the sick and the gullible (the vulnerable people who allowed themselves to be persuaded that the vaccine was more dangerous than the virus).

A hundred years ago, many experts would have hailed such a disease for the same reasons they promoted eugenics. We think differently now. However, emotionally and rationally, we still dread the deaths of children much more than the old, the sick and the foolish. The moment children become seriously ill — as has already happened in Gauteng — the nature of the pandemic fundamentally alters. Risk aversion will be far higher in the Ferguson family, for example, if its youngest members are vulnerable for the first time.

The second historical point is that this may be how our age of globalization ends — in a very different way from its first incarnation just over a century ago. The first age of globalization, from the 1860s until 1914, ended with a bang, not a whimper, with the outbreak of World War I. Within a remarkably short space of time, that conflict halted trade, capital flows and migration between the combatant empires. Moreover, the war and its economic aftershocks strengthened and ultimately empowered new political movements, notably Bolshevism and fascism, that fundamentally repudiated free trade and free capital movements in favor of state control of the economy and autarky. By 1933, the outlook for liberal economic policies seemed so utterly hopeless that, in a lecture he gave in Dublin, even John Maynard Keynes threw in the towel and embraced economic self-sufficiency.

Now, there is an argument (made by my Bloomberg colleague and occasional editor James Gibney) that the pandemic will not kill globalization. I am not so sure. Defined too broadly, to include any kind cross-border interaction, the word loses its usefulness. Yes, there were all kinds of “transnational networks in science, health, entertainment,” as well as increasingly ambitious international agencies between the wars. But the fact that (for example) the Pan European movement was founded by Richard von Coudenhove-Kalergi in the 1920s does not mean that the subsequent decades were a triumph of European integration. There was a great deal of international cooperation and cross-border activity between 1939 and 1945, too. That does not mean that the 1940s were a time of globalization. For the word to be meaningful, globalization must refer to relatively higher volumes of trade, capital flows, migration flows and perhaps also cultural integration on a global scale.

On that basis, globalization peaked — or maybe “maxed out” would be more accurate — in around 2007. Calculate it how you like: Whether the ratio of global exports to GDP, the ratio of gross foreign assets to GDP, global or national migrant flows in relation to total population, they all tell the same story of a sustained rise of globalization hitting a peak around 14 years ago.

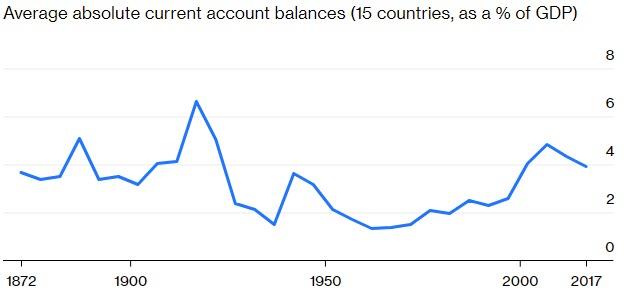

The economic historian Alan M. Taylor has long argued that we should measure globalization by looking at current account imbalances, which tell us when a lot of trade and lending are happening. On that basis, too, globalization peaked in 2007.

Even Before Covid, Trade and Lending Were Trending Down

Source: Our World in Data from Maurice Obstfeld and Alan M. Taylor, “Global Capital Markets: Integration, Crisis, and Growth,” Japan–US Center UFJ Bank Monographs on International Financial Markets; and International Monetary Fund, World Economic Outlook Database.

Note: The data shown is the average absolute current account balance (as a percentage of GDP) for 15 countries in five-year blocks. The countries in the sample are Argentina, Australia, Canada, Denmark, Finland, France, Germany, Italy, Japan, Netherlands, Norway, Spain, Sweden, U.K., U.S..

Since the financial crisis of 2008-9, however, the volume of world trade has flatlined relative to the volume of industrial production. The U.S. current account deficit peaked in the third quarter of 2006 at -6.3% of GDP. The latest read? -3.3%.

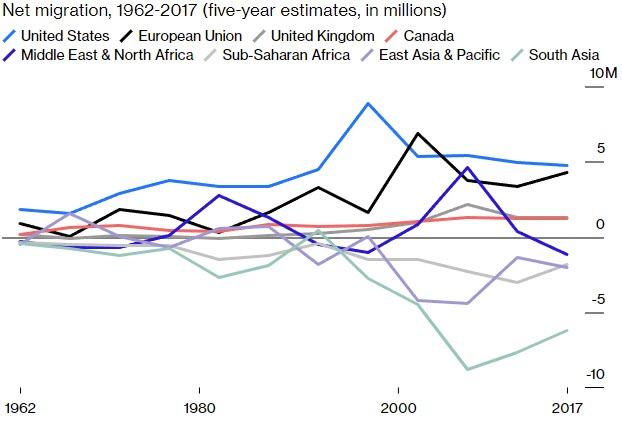

The same story emerges when one turns to migration. The foreign-born share of the U.S. population rose rapidly from its nadir in 1970 (4.7%) to a peak of 13.7% in 2019. But the rate of growth clearly slowed after 2012. It remains below its historic peak of 14.7%, back in 1890. Data for net migration similarly point to peaks prior to the financial crisis. Net emigration from South Asia peaked in 2007, for example. So did net immigration to the United Kingdom.

Source: United Nations Population Division

What about cultural globalization? My guess is that peaked in 2012, which was the last year that imported films earned more at the Chinese box office than domestic productions. The highest-grossing movie in the history of the People’s Republic is this year’s “Battle of Lake Changjin,” a Korean War drama in which heroic Chinese troops take on the might of the U.S. Army—and win. (Watch the trailer. Then tell me globalization is going to be fine.)

What has caused globalization to recede? Let me offer a six-part answer.

First, global economic convergence. This may come as a surprise. An influential story over the past two decades was Branco Milanovic’s thesis that globalization had increased inequality. In particular, Milanovic argued in 2016 that “large real income gains [had] been made by people around the median of the global income distribution and by those in the global top 1%. However, there [had] been an absence of real income growth for people around the 80-85th percentiles of the global distribution.” He illustrated this argument with a famous “elephant chart” of cumulative income growth between 1988 and 2008 at each percentile of the global income distribution.

On closer inspection, the elephant was a statistical artifact. Strip out the data for Japan, the former Soviet Union and China, and the elephant vanishes. The story Milanovic’s chart told was of the decline of ex-Soviet and Japanese middle-class incomes following the collapse of the USSR and the bursting of Tokyo’s bubble in 1989-90, and the surge of Chinese middle-class incomes, especially after China’s entry into the World Trade Organization in 2001.

The real story of globalization turns out to be a sustained reduction in global inequality as Chinese incomes caught up rapidly with those in the rest of the world, combined with big increases in national inequality as the “one percent” in some (not all) countries got a whole lot richer. At the heart of globalization was what Moritz Schularick and I called “Chimerica”—the symbiosis between the Chinese and American economies that allowed American capital to take advantage of low-cost Chinese labor (offshoring or outsourcing), American borrowers to take advantage of abundant Chinese savings, and American consumers to take advantage of cheap Chinese manufactures.

It could not last. In 2003 Chinese unit labor costs were around a third of those in the U.S. By 2018 the two were essentially on a par. In that sense, the glory days of globalization were bound to be numbered. For as Chinese incomes rose, the rationale for relocating production to China was bound to become weaker.

Secondly, and at the same time, new technologies — robotics, three-dimensional printing, artificial intelligence — were rapidly reducing the importance of human labor in manufacturing. With the surge of online commerce and digital services, globalization entered a new phase in which data rather than goods and people crossed borders, even if the Great Firewall of China partly cordoned off China’s internet from the rest of the world’s.

Chimerica, as Schularick and I argued back in 2007, was in many ways a chimera — a monstrous creature with the potential to precipitate a crisis, not least by artificially depressing U.S. interest rates and inflating a real estate bubble. When that crisis struck in 2008-9, it was the third blow to globalization. For those who suffered the heaviest losses in the United States and elsewhere, it was not illogical to blame free trade and immigration. A 2015 study by the McKinsey Global Institute showed clearly that people in the U.S., U.K. and France who saw themselves as “not advancing and not hopeful about the future” were much more likely than more optimistic groups to blame “legal immigrants,” “the influx of foreign goods and services,” and “cheaper foreign labor” for, respectively, “ruining the culture and cohesiveness in our society,” “leading to domestic job losses” and “creating unfair competition to domestic businesses.”

The only surprising thing was that these feelings took as long as seven years to manifest themselves as an organized political backlash against globalization, in the form of Britain’s vote to exit the European Union and America’s vote for Donald Trump. Dani Rodrik’s famous trilemma — which postulated that you could have any two of globalization, democracy and sovereignty — was emphatically answered in 2016: Voters chose democracy and sovereignty over globalization. This was the fourth strike against “the globalists,” a term invented by the populists to give globalization a more easily hateable human face.

The financial crisis and the populist backlash didn’t sound the death knell for globalization. They merely dialed it back — hence the plateau in trade relative to manufacturing and the modest decline (not collapse) of international capital flows and migration. The fifth blow was the outbreak of Cold War II, which should probably be dated from Vice President Mike Pence’s October 2018 Hudson Institute speech, the first time the Trump administration had taken its anti-Chinese policy beyond the confines of the president’s quixotic trade war (which only modestly reduced the bilateral U.S.-Chinese trade deficit).

Not everyone has come to terms with this new cold war. Joseph Nye (and the administration of President Joe Biden) would still like to believe that the U.S. and China are frenemies engaged in “coopetition.” But Hal Brands and John Lewis Gaddis, John Mearsheimer and Matt Turpin have all come round to my view that this is a cold war — not identical to the last one, but as similar to it as World War II was to World War I. The only question worth debating is whether or not, as in 1950, cold war turns hot. There is no Thucydidean law that says this is inevitable, as Graham Allison has shown. But I agree with Mearsheimer: The risk of a hot war in Cold War II may actually be higher than in Cold War I. Nothing would kill globalization faster than the outbreak of a superpower war over Taiwan. (And “The Battle of Lake Changjin” is blatantly psyching Chinese cinemagoers up for such a conflict.)

The decoupling of the U.S. and Chinese economies would almost certainly have continued even if the sixth blow — the Covid pandemic — had not struck. It has been astounding how little the Biden administration has changed of its predecessor’s China strategy. However, the pandemic has delivered the coup de grace — “a brutal end to the second age of globalization,” as Nicholas Eberstadt put it last year.

True, the volume of merchandise trade has recovered even more rapidly in 2021 than the World Trade Organization anticipated back in March. But the emergence of a new, contagious and lethal coronavirus has caused a collapse of international travel and tourism. The number of passengers carried by the global airline industry plunged by 60% in 2020. It will be not much better than 50% of its pre-pandemic level this year. International tourist arrivals are down by even more this year than last year — close to 80% below their 2019 level. In Asia, international tourism has all but ceased to exist this year.

Meanwhile, both the U.S. and the Chinese governments keep devising new ways to discourage their nationals from investing in the rival superpower. Didi Global Inc., the Chinese Uber, just announced it is delisting its shares from the New York Stock Exchange. And the pressure mounts on Wall Street financiers — as Bridgewater Associates founder Ray Dalio discovered last week — to wind up their “long China” trade and stop turning a blind eye to genocide in Xinjiang and other human rights abuses. Next up: the campaign to boycott the 2022 Winter Olympics in Beijing.

Strikingly, a growing number of Western sports stars and organizations such as the Women’s Tennis Association are already willing to defy Beijing — in the case of the WTA by suspending tournaments in China in response to the disappearance of the tennis star Peng Shuai, who accused a senior Communist Party official of sexually assaulting her. China’s leaders should be even more worried by a recent Chicago Council of World Affairs poll, which showed that just over half of Americans (52%) favor using U.S. troops to defend Taiwan if China invades the island — the highest share ever recorded in surveys dating back to 1982.

Last month I asked a leading American lawmaker how he explained the marked growth in public hostility toward the Chinese government. His answer was simple: “People blame China for Covid.” And not without reason, as Matt Ridley’s new book “Viral” makes clear.

For the avoidance of doubt, I do not foresee as complete a collapse of globalization as happened after 1914. Globalization 2.0 seems to be going out with a whimper — or perhaps a persistent cough — rather than with a bang. Income convergence and technological change were bound to reduce its utility. Having overshot by 2007, globalization settled at a lower level after the financial crisis and was less damaged by populist policies like tariffs than might have been anticipated. But the advent of Cold War II and Covid-19 struck two severe blows. How far globalization is rolled back depends on how far the two phenomena persist or worsen.

Maybe — let us pray — the alarming data from Gauteng will not imply a major new wave of illness and death in the wider world. Maybe the omicron variant will not, after all, be that nightmare variant I have feared: more infectious, more lethal, vaccine-evading, not ageist.

But omicron is only the 15th letter in the Greek alphabet. In all of Africa only 7.3% of the population are fully vaccinated and there are countless immunocompromised individuals with HIV. Even if omicron turns out to be, like delta, a variant we can live with, there is still some non-zero chance that at some point we get my “omega variant.” In that scenario, the pandemic does not oblige us, weary as we are of it, by ending, but recurs in a succession of waves extending for years. One begins to wonder if China will ever lift its stringent restrictions on foreign visitors. Under such circumstances, I see little chance of Cold War II reaching the détente phase earlier than Cold War I.

In addition to applying history, I have come to believe that we should also apply science fiction, on the principle that its authors are professionally incentivized to envision plausibly the impact of social, technological and other changes on the future. (Fact: an Italian sci-film called “Omicron,” in which an alien takes over a human body, was released in 1963.) No living author is better at this kind of thing than Neal Stephenson, whose “Snow Crash” coined the word “metaverse,” and whom I got to know — appropriately via Zoom — through my friends at the Santa Fe Institute.

When Stephenson and I met for a late-night Scotch at a bar in Seattle a few weeks back, we swiftly found common ground. Never have I seen a longer list of wines and spirits: We could have scrolled down on the iPad the server handed us for an hour and still not reached the end. Eventually, we found the malt whisky. And immediately we agreed: Laphroaig — the standard 10-year-old version.

Stephenson’s latest novel is “Termination Shock.” Buy it. You will be catapulted into a future Texas of intolerable heat, man-eating hogs, and other nightmares, the effect of which will be to make your present circumstances seem quite tolerable. Part of Stephenson’s genius is his use of the throwaway detail.

“RVs,” he writes, were “already at a premium because of Covid-19, Covid-23 and Covid-27.”

It’s not really part of the plot, but it stopped my eyeballs in their tracks. And remember: He predicted the metaverse. In 1992.

Tyler Durden

Mon, 12/06/2021 – 05:00

via ZeroHedge News https://ift.tt/3xYm1ET Tyler Durden

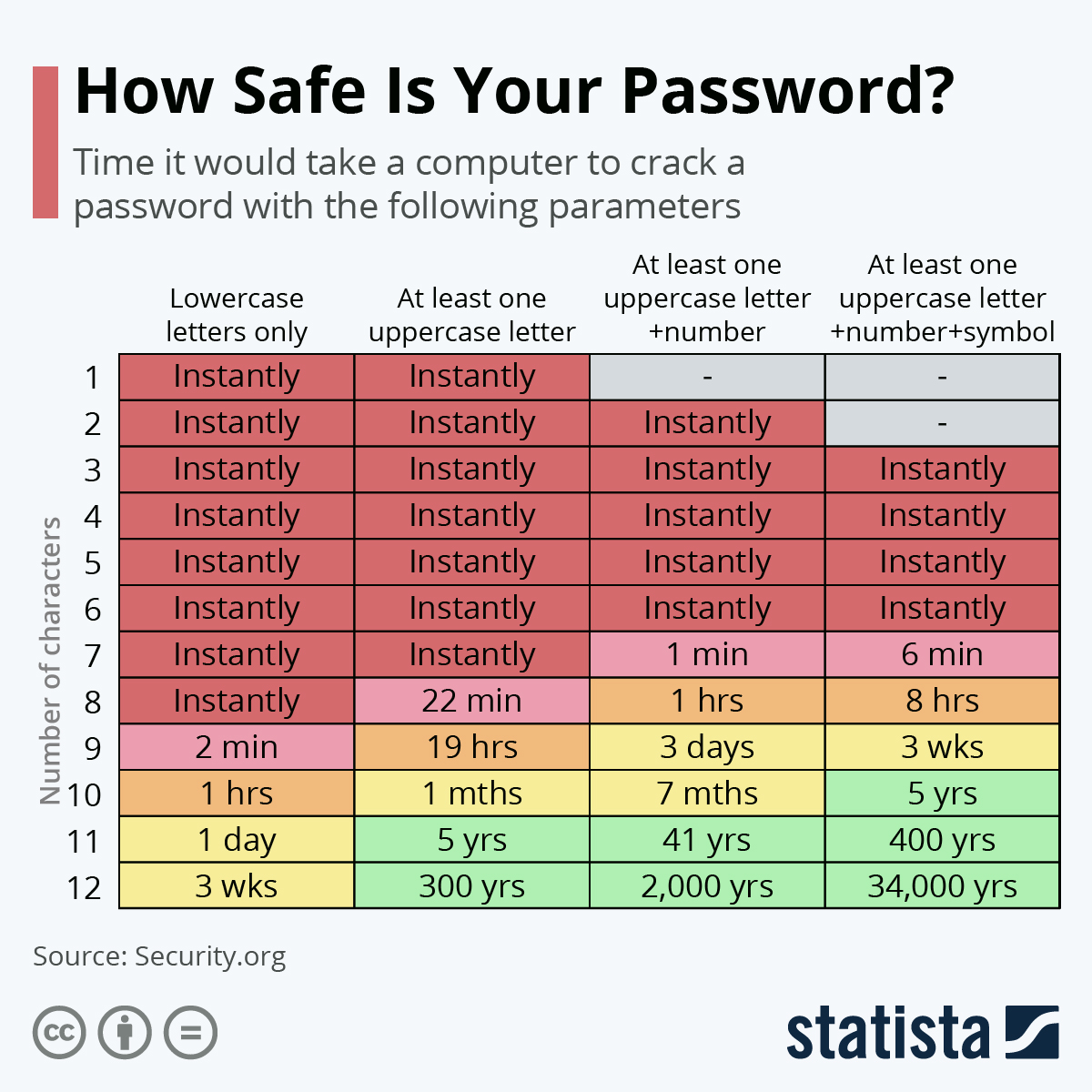

How Safe Is Your Password?

Password, 123456, qwerty… While passwords which appear on the list of the most common passwords should definitely be retired from use, as Statista’s Katharina Buchholz details below that even a more unique password can be easy to crack if a computer program is tasked with systematically breaking it.

As seen in data by website Security.org, adding even one upper case letter to a password can already dramatically alter its potential. In the case of an eight-character password, it can now be broken in 22 minutes instead of instantaneously in one second – an increase of more than 1000 percent.

You will find more infographics at Statista

While the added time in this case is definitely not good enough to end up with a satisfactory password, the high security gains of using characters other than lower case letters can be multiplied. When using at least one upper case letter and one number, an eight-character password now would take a computer 1 hour to crack. Add another symbol and it takes eight. To make a password truly secure, even more characters or more than one uppercase letter, number or symbol can be added.

A twelve-character password with one uppercase letter, one number and one symbol is almost unbreakable, taking a computer 34,000 years to crack.

This happens because when we use more types of characters, the potential combinations making up the password increase exponentially.

With just 26 lower case letters, a password of eight characters has 26^8, so around 209 billion possible combinations. Adding the uppercase, we already arrive at 52^8, around 53.5 trillion combinations. With the numbers in there, it’s 62^8 or 218 trillion combinations.

Symbols add another great potential for security, but since only the handful displayed on computer keyboards are convenient to use, this ups the number of combinations once more to around 90^8 or 430 trillion combinations.

Tyler Durden

Mon, 12/06/2021 – 04:15

via ZeroHedge News https://ift.tt/3InKRTD Tyler Durden

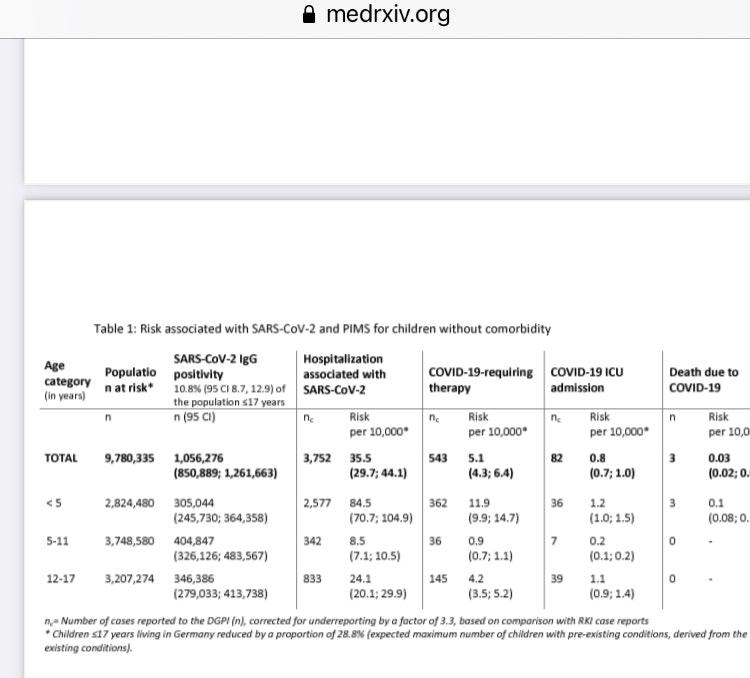

Huge New Study Shows Zero COVID Deaths Among Healthy German Kids

Authored by Alex Berenson via ‘Unreported Truths’ substack,

The findings, in a nutshell: if you let your healthy child or teenager receive the mRNA Covid vaccine, you are insane…

German physician-scientists reported Monday that not a single healthy child between the ages of 5 and 18 died of Covid in Germany in the first 15 months of the epidemic.

Not one.

Even including children and adolescents with preexisting conditions, only six in that age range died, the researchers found.

Germany is Europe’s largest country, with more than 80 million people, including about 10 million school-age children and adolescents.

Serious illness was also extremely rare. The odds that a healthy child aged 5-11 would require intensive care for Covid were about 1 in 50,000, the researchers found. For older and younger children, the odds were somewhat higher, about 1 in 8,000.

Another eight infants and toddlers died, including five with preexisting conditions. In all, 14 Germans under 18 died of Covid, about one per month. About 1.5 million German children or adolescents were infected with Sars-Cov-2 between March 2020 and May 2021, the researchers found.

“Overall, the SARS-CoV-2-associated burden of a severe disease course or death in children and adolescents is low,” the researchers reported.

“This seems particularly the case for 5-11-year-old children without comorbidities.”

The researchers reported their findings in an 18-page paper published to the medrxiv preprint server on Monday.

The data came from a registry Germany established in March 2020 intended to capture all hospitalizations of people under 18 with Covid. All German children’s hospitals, pediatric infectious disease specialists, and pediatric societies were invited to participate.

(SOURCE: https://www.medrxiv.org/content/10.1101/2021.11.30.21267048v1.full.pdf)

British researchers have posted similar findings, reporting that only six healthy children (including those under 18) out of 12 million died of Covid.

Given the known risks of vaccine-induced myocarditis in young men, the fact that Pfizer tested its mRNA vaccines on barely 3,000 children 5-11 and followed most of them for only weeks after the second dose, the German data again raises the question of how health authorities can possibly justify encouraging children or teenagers to be vaccinated.

But they have.

So parents will have to decide what’s best for their children (at least in those states that bar vaccine fanatics from trying to vaccinate teenagers without parental consent).

* * *

Subscribe to Unreported Truths here.

Tyler Durden

Mon, 12/06/2021 – 03:30

via ZeroHedge News https://ift.tt/3Ew1XMF Tyler Durden

Electric Cars But No Chargers?

In a lot of respects, progress regarding sustainability and climate change is still far too slow for what the world needs.

One area where the pace is really picking up however is that of electric vehicles. That is, the production and purchase of them. But, as Statista’s Martin Armstrong details below, when it comes to public infrastructure to match this growing demand, a lot of countries are still a long way behind in providing charging points.

As this infographic using International Energy Agency data shows, there is a large discrepancy in countries like New Zealand, where there were 52 electric vehicles for every one public charging point in 2020.

You will find more infographics at Statista

It doesn’t have to be like this though, as exemplified by South Korea where fighting over the parking space at the charging station is surely a very rare occurrence. Here, there is a public charger for every two EVs in the country.

Tyler Durden

Mon, 12/06/2021 – 02:45

via ZeroHedge News https://ift.tt/3ImiuVO Tyler Durden

Escobar: Russia Is Primed For A Persian Gulf Security ‘Makeover’

Authored by Pepe Escobar via TheCradle.co,

It’s impossible to understand the resumption of the JCPOA nuclear talks in Vienna without considering the serious inner turbulence of the Biden administration.

Everyone and his neighbor are aware of Tehran’s straightforward expectations: all sanctions – no exceptions – must be removed in a verifiable manner. Only then will the Islamic Republic reverse what it terms ‘remedial measures,’ that is, ramping up its nuclear program to match each new American ‘punishment.’

The reason Washington isn’t tabling a similarly transparent position is because its economic circumstances are, bizarrely, far more convoluted than Iran’s under sanctions. Joe Biden is now facing a hard domestic reality: if his financial team raises interest rates, the stock market will crash and the US will be plunged into deep economic distress.

Panicked Democrats are even considering the possibility of allowing Biden’s own impeachment by a Republican majority in the next Congress over the Hunter Biden scandal.

According to a top, non-partisan US national security source, there are three things the Democrats think they can do to delay the final reckoning:

First, sell some of the stock in the Strategic Oil Reserve in coordination with its allies to drive oil prices down and lower inflation.

Second, ‘encourage’ Beijing to devalue the yuan, thus making Chinese imports cheaper in the US, “even if that materially increases the US trade deficit. They are offering trading the Trump tariff in exchange.” Assuming this would happen, and that’s a major if, it would in practice have a double effect, lowering prices by 25 percent on Chinese imports in tandem with the currency depreciation.

Third, “they plan to make a deal with Iran no matter what, to allow their oil to re-enter the market, driving down the oil price.” This would imply the current negotiations in Vienna reaching a swift conclusion, because “they need a deal quickly. They are desperate.”

There is no evidence whatsoever that the team actually running the Biden administration will be able to pull off points two and three; not when the realities of Cold War 2.0 against China and bipartisan Iranophobia are considered.

Still, the only issue that really worries the Democratic leadership, according to the intel source, is to have the three strategies get them through the mid-term elections. Afterwards, they may be able to raise interest rates and allow themselves time for some stabilization before the 2024 presidential ballot.

So how are US allies reacting to it? Quite intriguing movements are in the cards.

Less than two weeks ago in Riyadh, the Gulf Cooperation Council (GCC), in a joint meeting with France, Germany and the UK, plus Egypt and Jordan, told the US Iran envoy Robert Malley that for all practical purposes, they want the new JCPOA round to succeed.

A joint statement, shared by Europeans and Arabs, noted “a return to mutual compliance with the [nuclear deal] would benefit the entire Middle East, allow for more regional partnerships and economic exchange, with long-lasting implications for growth and the well-being of all people there, including in Iran.”

This is far from implying a better understanding of Iran’s position. It reveals, in fact, the predominant GCC mindset ruled by fear: something must be done to tame Iran, accused of nefarious “recent activities” such as hijacking oil tankers and attacking US soldiers in Iraq.

So this is what the GCC is volunteering to the Americans. Now compare it with what the Russians are proposing to several protagonists across West Asia.

Essentially, Moscow is reviving the Collective Security Concept for the Persian Gulf Region, an idea that has been simmering since the 1990s. Here is what the concept is all about.

So if the US administration’s reasoning is predictably short-term – we need Iranian oil back in the market – the Russian vision points to systemic change.

The Collective Security Concept calls for true multilateralism – not exactly Washington’s cup of tea – and “the adherence of all states to international law, the fundamental provisions of the UN Charter and the resolutions of the UN Security Council.”

All that is in direct contrast with the imperial “rules-based international order.”

It’s too far-fetched to assume that Russian diplomacy per se is about to accomplish a miracle: an entente cordiale between Tehran and Riyadh.

Yet there’s already tangible progress, for instance, between Iran and the UAE. Iranian Deputy Foreign Minister Ali Bagheri held a “cordial meeting” in Dubai with Anwar Gargash, senior adviser to UAE President Khalifa bin Zayed Al Nahyan. According to Bagheri, they “agreed to open a new page in Iran-UAE relations.”

Geopolitically, Russia holds the definitive ace: it maintains good relationships with all actors in the Persian Gulf and beyond, talks to all of them frequently, and is widely respected as a mediator by Iran, Saudi Arabia, Syria, Iraq, Turkey, Lebanon, and other GCC members.

Russia also offers the world’s most competitive and cutting edge military hardware to underpin the security needs of all the parties.

And then there’s the overarching, new geopolitical reality. Russia and Iran are forging a strengthened strategic partnership, not only geopolitical but also geoeconomic, fully aligned to the Russian-conceptualized Greater Eurasian Partnership – and also demonstrated by Moscow’s support for Iran’s recent ascension to the Shanghai Cooperation Organization (SCO), the only West Asian state to be admitted thus far.

Furthermore, three years ago Iran launched its own regional security framework proposal for the region called HOPE (the Hormuz Peace Endeavor) with the intent to convene all eight littoral states of the Persian Gulf (including Iraq) to address and resolve the vital issues of cooperation, security, and freedom of navigation.

The Iranian plan didn’t get far off the ground. While Iran suffers from adversarial relations with some of its intended audience, Russia carries none of that baggage.

And that brings us to the essential Pipelineistan angle, which in the Russia–Iran case revolves around the new, multi-trillion dollar Chalous gas field in the Caspian Sea.

A recent sensationalist take painted Chalous as enabling Russia to “secure control over the European energy market.”

That’s hardly the story. Chalous, in fact, will enable Iran – with Russian input – to become a major gas exporter to Europe, something that Brussels evidently relishes. The head of Iran’s KEPCO, Ali Osouli, expects a “new gas hub to be formed in the north to let the country supply 20 percent of Europe’s gas needs.”

According to Russia’s Transneft, Chalous alone could supply as much as 52 percent of natural gas needs of the whole EU for the next 20 years.

Chalous is quite something: a twin-field site, separated by roughly nine kilometers, the second-largest natural gas block in the Caspian Sea, just behind Alborz. It may hold gas reserves equivalent to one-fourth of the immense South Pars gas field, placing it as the 10th largest gas reserves in the world.

Chalous happens to be a graphic case of Russia-Iran-China (RIC) geoeconomic cooperation. Proverbial western speculative spin rushed to proclaim the 20-year gas deal as a setback for Iran. The final breakdown, not fully confirmed, is 40 percent for Gazprom and Transneft, 28 percent for China’s CNPC and CNOOC, and 25 percent for Iran’s KEPCO.

Moscow sources confirm Gazprom will manage the whole project. Transneft will be in charge of transportation, CNPC is involved in financing and banking facilities, and CNOOC will be in charge of infrastructure and engineering.

The whole Chalous site has been estimated to be worth a staggering $5.4 trillion.

Iran could not possibly have the funds to tackle such a massive enterprise by itself. What is definitely established is that Gazprom offered KEPCO all the necessary technology in exploration and development of Chalous, coupled with additional financing, in return for a generous deal.

Crucially, Moscow also reiterated its full support for Tehran’s position during the current JCPOA round in Vienna, as well as in other Iran-related issues reaching the UN Security Council.

The fine print on all key Chalous aspects may be revealed in time. It’s a de facto geopolitical/geoeconomic win-win-win for the Russia, Iran, China strategic partnership. And it reaches way beyond the famous “20-year agreement” on petrochemicals and weapons sales clinched by Moscow and Tehran way back in 2001, in a Kremlin ceremony when President Putin hosted then Iranian President Mohammad Khatami.

There’s no two ways about it. If there is one country with the necessary clout, tools, sweeteners and relationships in place to nudge the Persian Gulf into a new security paradigm, it is Russia – with China not far behind.

Tyler Durden

Mon, 12/06/2021 – 02:00

via ZeroHedge News https://ift.tt/3xVubxO Tyler Durden