After a surprisingly exuberant day in the stock market, filled with hope at all the optimistic awesomeness that the mega-tech hegemons would “told you so” to any naysayers who weren’t already balls-deep long these over-valued and over-hyped names, things have gone just a little bit turbo after hours.

It wasn’t pretty with only GOOGL shares higher…

Twittersinks in late trading after user growth expectations were off. The company added 20 million new users in Q2.It added just 1 million new users in Q3. Expectations were that Twitter would report growth of 9 million new users in the quarter so this is a definite miss. The company also said there will be a delay in its MAP direct response ad product.

Facebook’sshares are modestly lower. Revenue blew past estimates as the company weathered the ad boycott from big advertisers. Also, user growth over overall exceeded expectations, but the company lost traction in the U.S. and Canada. Also, Facebook said it will be investing heavily on employees and new technology.

Amazonshares are down despite reporting profit and net sales that beat quarterly estimates. The retailer sees up to $121 billion in fourth-quarter sales. Bezos expects an “unprecedented” holiday season. CFO says Covid-related expenses will go up to $4 billion.

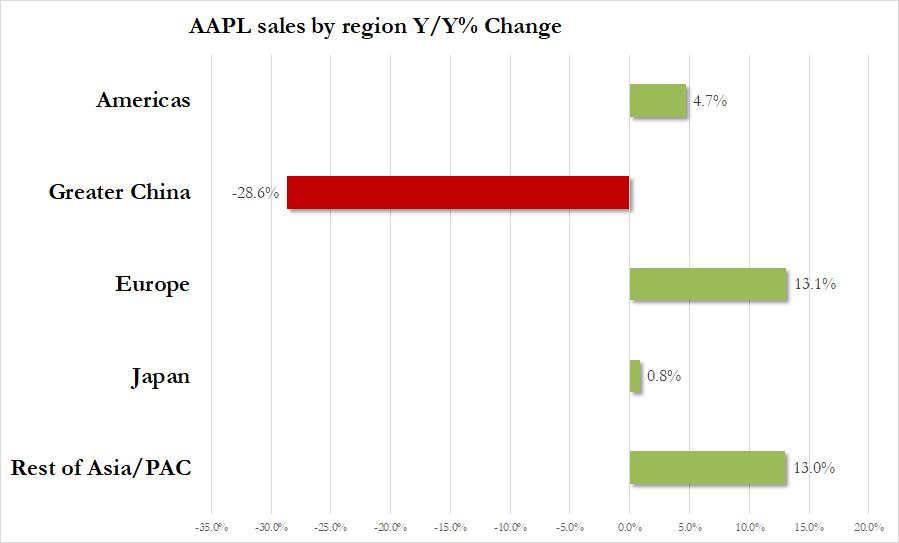

Applesales plunge 29% in China, grow in other regions. IPhone revenue falls short of analysts’ estimates. Lack of revenue forecast dissapoints some observers. Shares fall, dragging suppliers down in late trading.

Alphabetreturned to growth in the third quarter after a decline in the previous period, fueled by digital advertising that has rebounded along with the American economy. The shares rose about 6% in extended trading.

All of which sent futures tumbling…

Erasing all the day’s gains in the S&P and Dow…

Of course, it’s early yet and we would strongly expect some dip-buyers to charge in. Just bear in mind that “large lot” sellers have been active all week…

Trade accordingly.

via ZeroHedge News https://ift.tt/3kBfvMZ Tyler Durden

Managing editor, Ed Harrison, welcomes Stephen Kalayjian, chief market strategist of Ticker Tocker, to discuss the elevated levels of volatility and his forward outlook for markets over the coming months. With the U.S. election coming up in less than a week, Kalayjian describes how not only are markets are being worn down by the torrent of uncertainty surrounding policy outcomes with each respective administration, but also by how the sensitivity of this year’s election and the events that will unfold in the coming weeks are keeping markets on edge with COVID-19 exacerbating tensions further. He explains where he sees the opportunities and downside risk in U.S. equities in light of these circumstances and why the perception of economic growth in large cap tech stocks will propel their prices up further for the rest of 2020 through the beginning of 2021. Real Vision reporter Haley Draznin analyzes the U.S. economy’s record GDP growth, but explains the real obstacles going forward that will slow the recovery, perhaps severely.

via ZeroHedge News https://ift.tt/31SmIRi Tyler Durden

Report Alleges Trump Quashed Criminal Probe Into Turkish Bank That Funneled Billions To Iran Tyler Durden

Thu, 10/29/2020 – 18:05

Prior bombshell claims in former national security advisor John Bolton’s book released last summer alleging that President Trump had agreed to quash a federal probe into a Turkish state-owned bank as a personal favor to Recep Tayyip Erdoğan just got a major boost.

Bolton wrote of scandal-hit Halkbank that in a 2018 phone call after Erdoğan insisted the bank was innocent of sanctions-busting by funneling billions of dollars in cash and gold to neighboring Iran: “Trump then told Erdoğan he would take care of things, explaining that the [New York] southern district prosecutors were not his people but were Obama people, a problem that would be fixed when they were replaced by his people,” according to the book.

Trump last summer slammed Bolton’s presentation of events as “misleading” and “manipulative” but now a fresh New York Times investigation is spotlighting the scandal with new details of the fierce confrontation between top federal prosecutor in Manhattan Geoffrey Berman and Attorney General William Barr.

File image via AP

Berman balked when he was pressed by Barr to allow the Turkish state bank to cut a sweetheart deal despite key individuals – some with close ties to Erdogan himself – still being under active investigation. The pressure from the US administration was also unusual given the strong suspicions Halkbank was secretly helping finance Iran’s alleged push to obtain nuclear weapons.

When Mr. Berman sat down with Mr. Barr, he was stunned to be presented with a settlement proposal that would give Mr. Erdogan a key concession.

Mr. Barr pressed Mr. Berman to allow the bank to avoid an indictment by paying a fine and acknowledging some wrongdoing. In addition, the Justice Department would agree to end investigations and criminal cases involving Turkish and bank officials who were allied with Mr. Erdogan and suspected of participating in the sanctions-busting scheme.

Mr. Berman didn’t buy it.

“This is completely wrong,” Berman later complained to DOJ lawyers. “You don’t grant immunity to individuals unless you are getting something from them — and we wouldn’t be here.”

“This is not how we do things at the Southern District,” he would also tell Barr directly amid the negotiations in which top bank officials seemed to think that Trump and Erdogan’s relationship gave them immense leverage.

“That is not how we do things in the Southern District.”

Berman’s reported reaction when Barr pressured him to drop charges against Erdogan’s cronies, including the Turkish strongman’s ex-economy minister Zafer Caglayan.

Among the defendants with charges pending were Halkbank’s former general manager, Suleyman Aslan, and Turkey’s former economy minister, Mehmet Zafer Caglayan.

The suggestion that the Justice Department would offer Turkish officials protection from criminal charges, even without their agreement to assist in the investigation, was unacceptable and unethical, Mr. Berman argued, according to lawyers close to the investigation. Justice Department policy specifically says that criminal conduct by individuals is not resolved when a company admits wrongdoing.

At one point Barr argued that settling the issue without charges would help enforce US sanctions law while also ensuring the positive American-Turkish relationship at a moment of multiple sensitive national security priorities at risk in the Middle East. This was also at a moment of intense Turkish lobbying on capitol hill which had already been in full swing for years.

Berman pushed through undeterred and announced charges against Halkbank in Oct. 2019, saying the “bank’s audacious conduct was supported and protected by high-ranking Turkish government officials, some of whom received millions of dollars in bribes to promote and protect the scheme.” The indictment listed charges of money laundering, bank fraud and conspiracy to violate the Iran sanctions.

It was considered a direct affront to Erdogan and the special relationship with Trump.

A Halbank branch in Istanbul, via Bloomberg

As the Times writes further, “In June, eight months after the indictment was returned, Mr. Trump fired Mr. Berman. Justice Department officials cited his handling of the Halkbank matter, including his blocking of the proposed global settlement, as a key reason for his removal.”

Strangely, the whole episode and pressure exerted from the administration in what was perceived as ultimately an attempt to please Erdogan ran completely counter to what otherwise has been the White House’s top foreign policy priority of ‘maximum pressure’ on Iran. Bolton had previously described the apparent contradiction in priorities in his memoir as Trump giving “personal favors to dictators he liked” so that favors would be returned at key junctures down the road.

These contradictions were somewhat resolved once the US and Turkey clashed over Syria and the fate of US-backed Kurds. “In the case of Halkbank, it was only after an intense foreign policy clash between Mr. Trump and Mr. Erdogan over Syria last fall that the United States would proceed to lodge charges against the bank, though not against any additional individuals,” NY Times concludes. “Yet the administration’s bitterness over Mr. Berman’s unwillingness to go along with Mr. Barr’s proposal would linger, and ultimately contribute to Mr. Berman’s dismissal.”

via ZeroHedge News https://ift.tt/3jzWOIc Tyler Durden

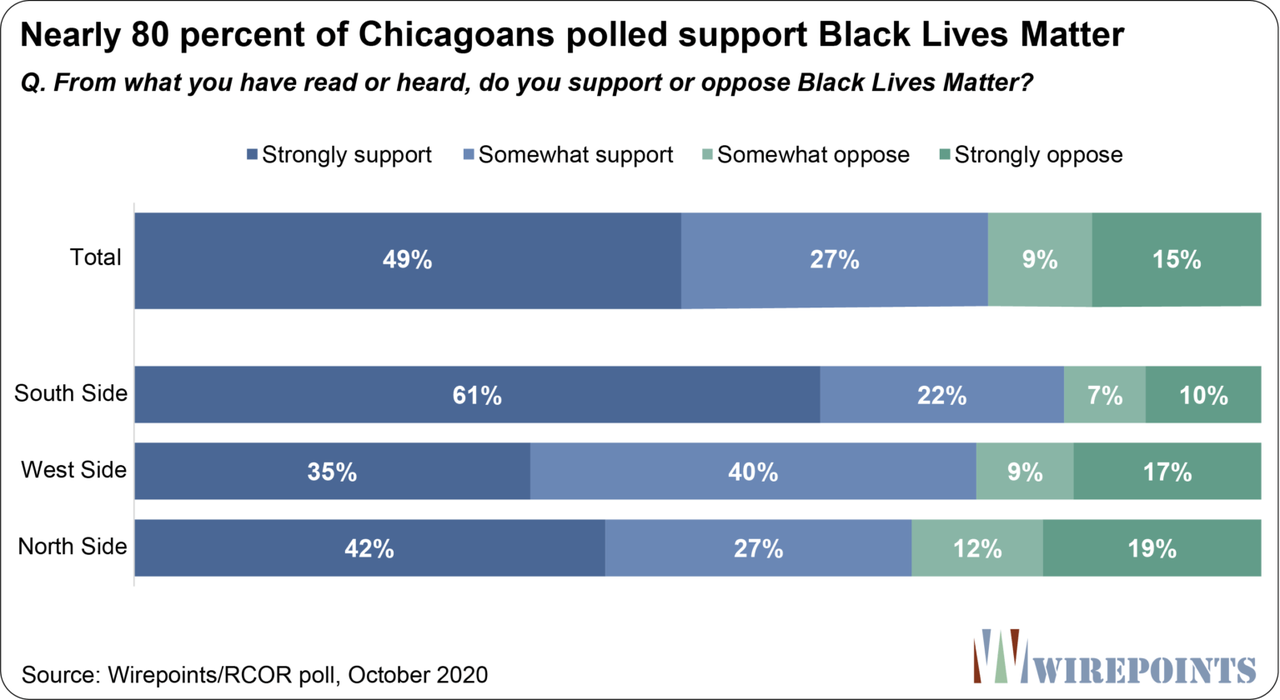

Chicagoans Categorically Reject Progressive/BLM Demands To Defund The Police Tyler Durden

Thu, 10/29/2020 – 17:45

By Ted Dabrowski, John Klingner and Julie Schmidt of Wirepoints

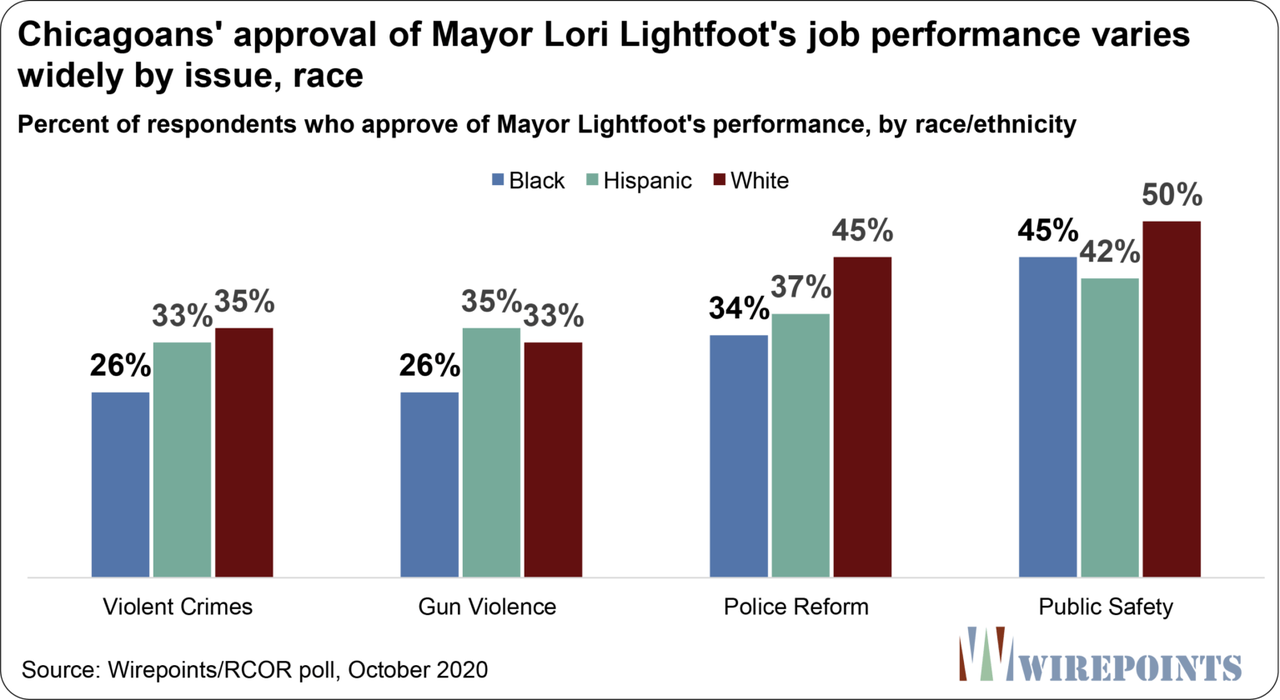

While Chicagoans share many concerns over the city’s policing practices, 79% want the police to spend the same amount of time or more in their neighborhoods. That’s one of the key findings of a new Wirepoints/Real Clear Opinion Research poll that looked at a range of attitudes in Chicago on policing, race and Mayor Lori Lightfoot’s performance.

The desire for more police holds true across the city’s North (76%), South (80%) and West Sides (85%), as well as across whites (79%), blacks (77%) and Hispanics (87%).

Only 15% of blacks and 10% of Hispanics citywide said they want the police to spend less time in their neighborhoods.

The Wirepoints/RCOR poll surveyed 895 registered voters in Chicago from September 26th through October 4th using a mixed phone and online methodology. The margin of error is +/- 3.28 percentage points at the 95% confidence level.

Although Chicagoans overwhelmingly indicated they want more police, they were also very clear in their desire for better-quality policing. Half (51%) of all Chicagoans polled said they believe the Chicago Police Department is currently handling its job badly. More than six out of ten black residents (63%) held that view.

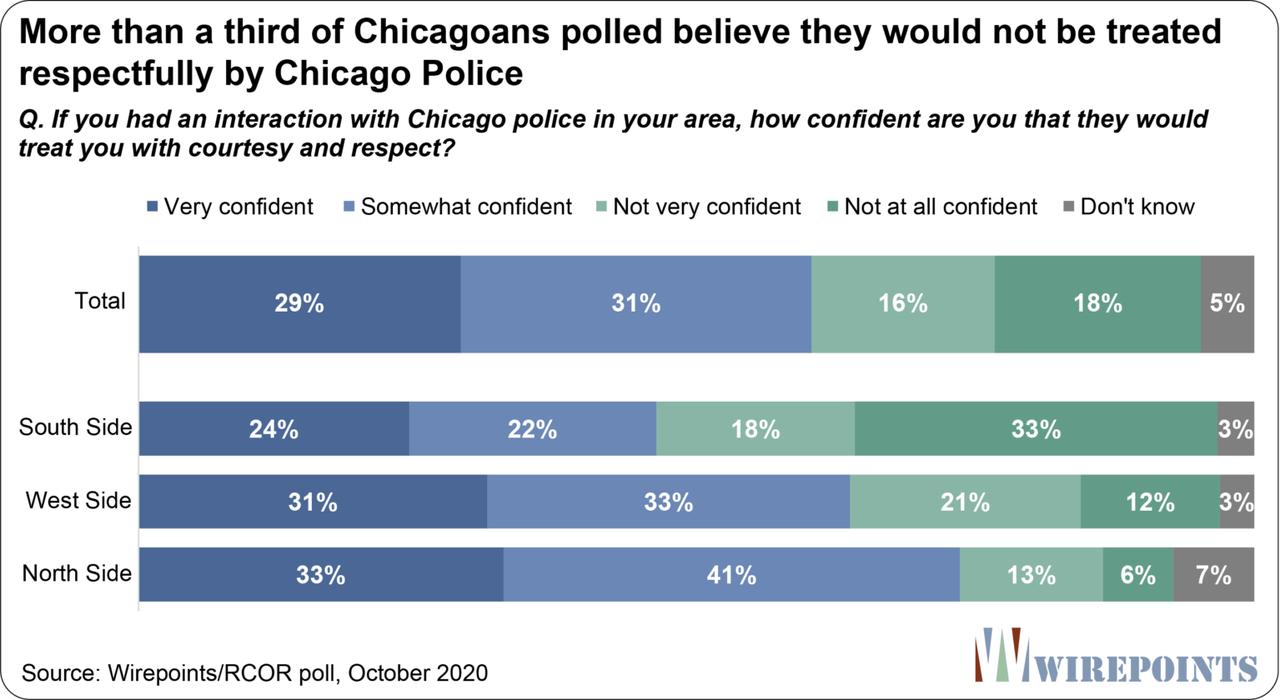

More than a third (35%) of all respondents felt they would not be treated respectfully in an encounter with police, a percentage that jumps to 54% among black residents.

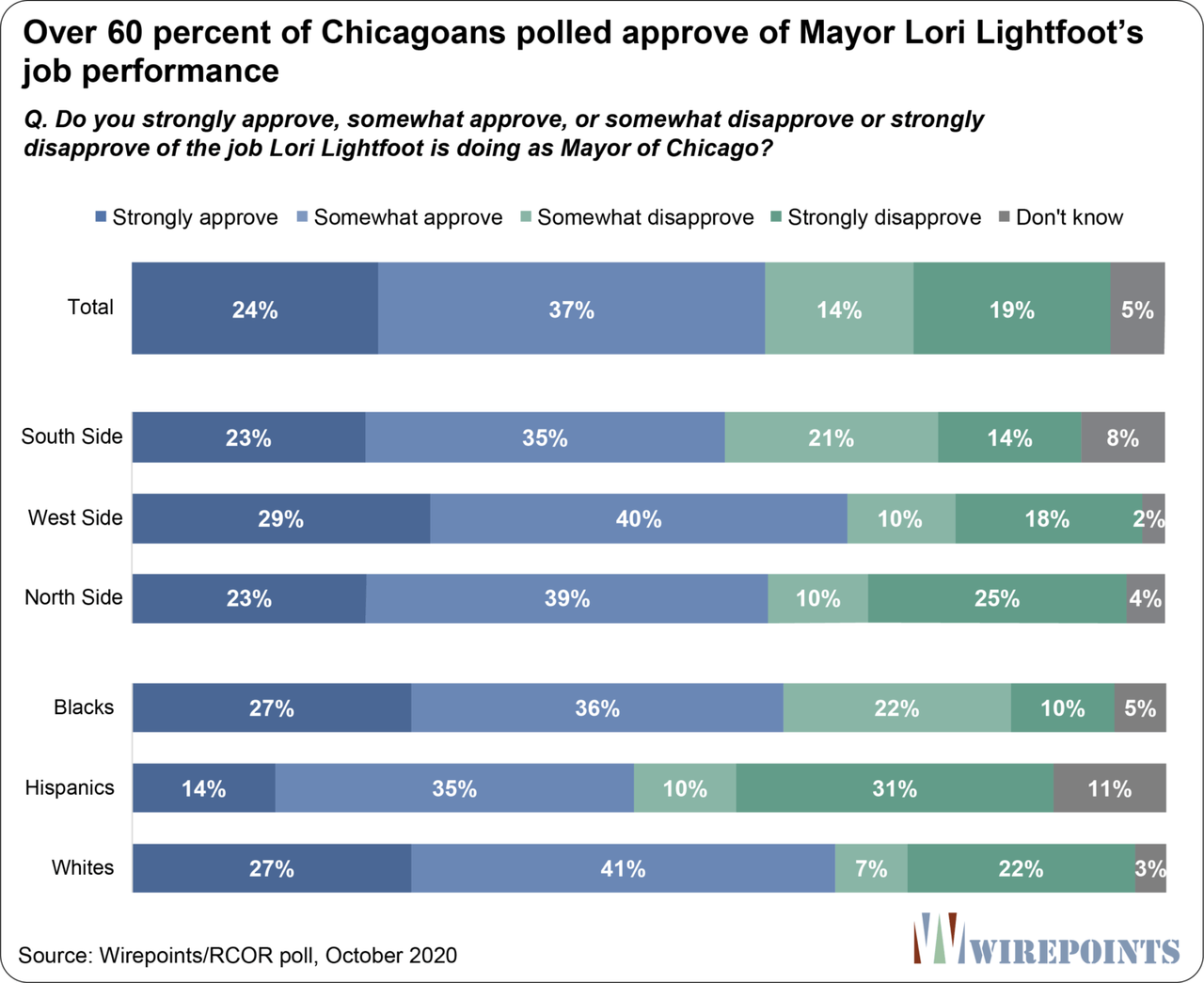

The polling also finds that while 61% of residents approve of the job that Mayor Lightfoot is doing, some of her lowest issue performance ratings come in how she is dealing with police reform, gun violence and violent crime.

Chicagoans support both BLM and more policing

George Floyd’s death and the subsequent protests expanded the influence of Black Lives Matter across the country, including in Chicago. Unsurprisingly, more than three-quarters (76%) of surveyed Chicagoans reported they strongly support or somewhat support BLM. Black Chicagoans maintained the highest support for BLM (86%), followed by whites (74%) and then Hispanics (61%). Geographically, South Side support of BLM is the highest (83%).

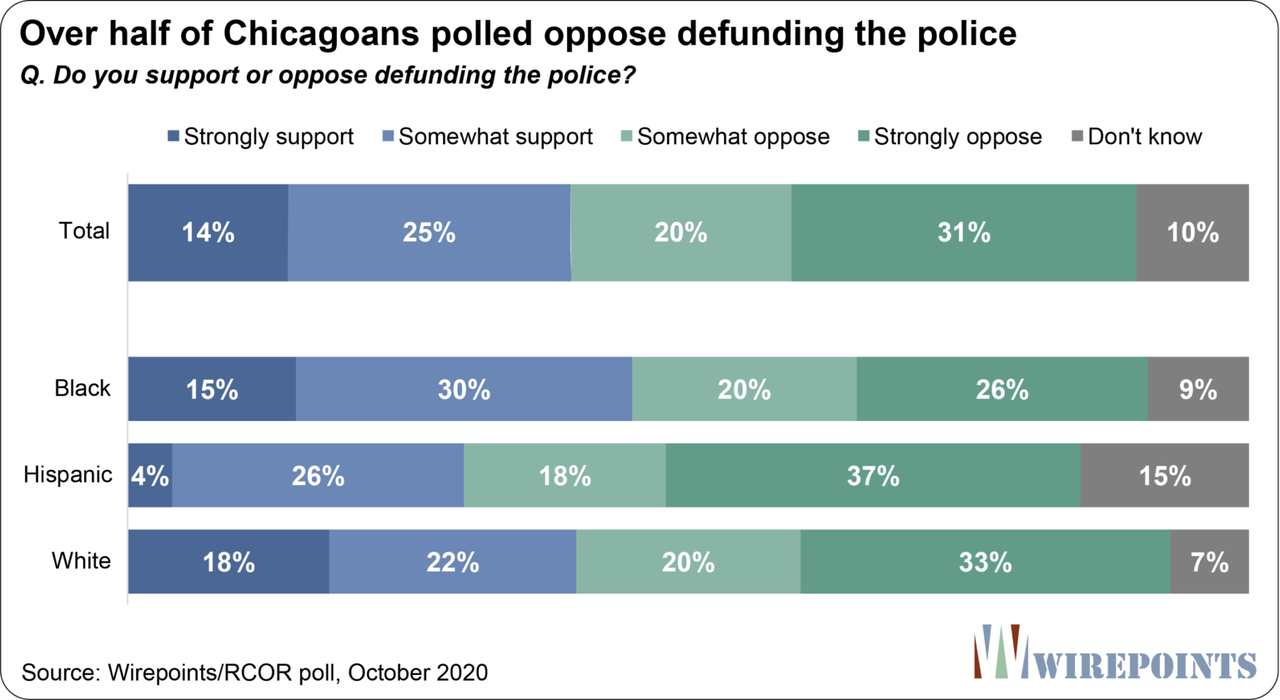

But when Chicagoans were asked directly if they support defunding the police, only 39% said they were in favor, while 51% were opposed. Opposition to defunding exceeded support in every region, with North Side residents expressing the most opposition (57% oppose / 36% support).

Along racial/ethnic lines, opposition exceeded support slightly among blacks (46% oppose / 45% support) and most strongly among Hispanics (55% oppose / 30% support).

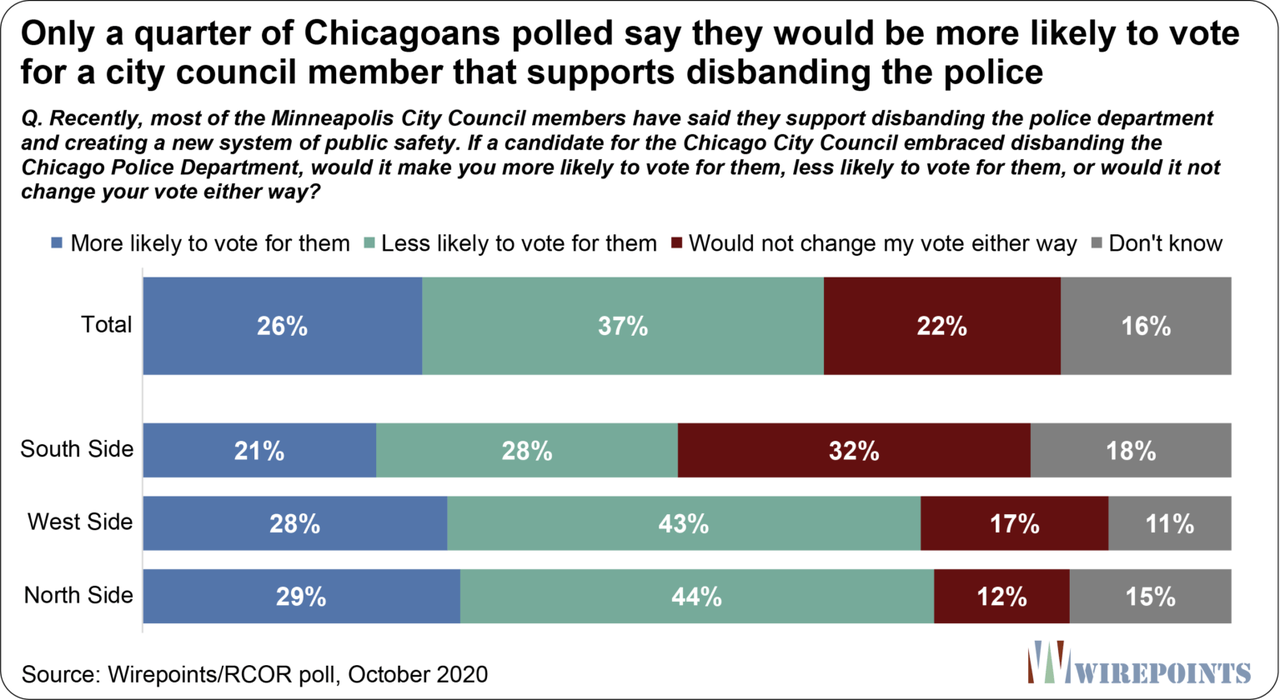

The support for BLM has also failed to translate into political support for wholly disbanding the CPD. Only 26% of Chicagoans polled would be more likely to vote for city council members that support disbanding the police, while 37% would be less likely to vote for them. Even fewer South Siders (21%) would be more likely to vote for members supporting disbanding.

By race, whites and Hispanics were most opposed to politicians supporting disbanding the CPD, with 43% and 41% saying they would be less likely to vote for a council member that pushed disbanding, respectively. Black residents were at 27%.

Instead of less police presence, most Chicagoans polled want more officers on the street. A vast majority (79%) of voters indicated they wanted police to spend more or the same amount time in their neighborhood.

The desire for additional policing was strongest on the South and West Sides, with more than half (57%) of residents in both areas wanting more police presence in their neighborhoods despite their concerns about current CPD practices. The number of Chicagoans polled who want police to spend less time amounted to less than 15% of those surveyed. On the West Side, only 9% of those polled wanted less police.

Chicagoans want better-quality policing

When questioned on a variety of topics, including job performance, systemic racism, police behavior, general safety and more, a majority or sizable minority of Chicagoans showed they have negative opinions of and/or have suffered negative encounters with Chicago officers.

Chicagoans’ overall negative rating of the CPD (51%) varied widely by geography. More than half of citizens from the North Side (54%) and the West Side (51%) said the CPD was doing a good or excellent job, while only 32% of voters from the South Side said the same.

When asked what needs to be reformed in the department, systemic racism or a few bad apples, nearly half of all those polled (45%) chose systemic racism. Hispanic residents were least likely to say systemic racism (33%) while black residents were the most likely (57%).

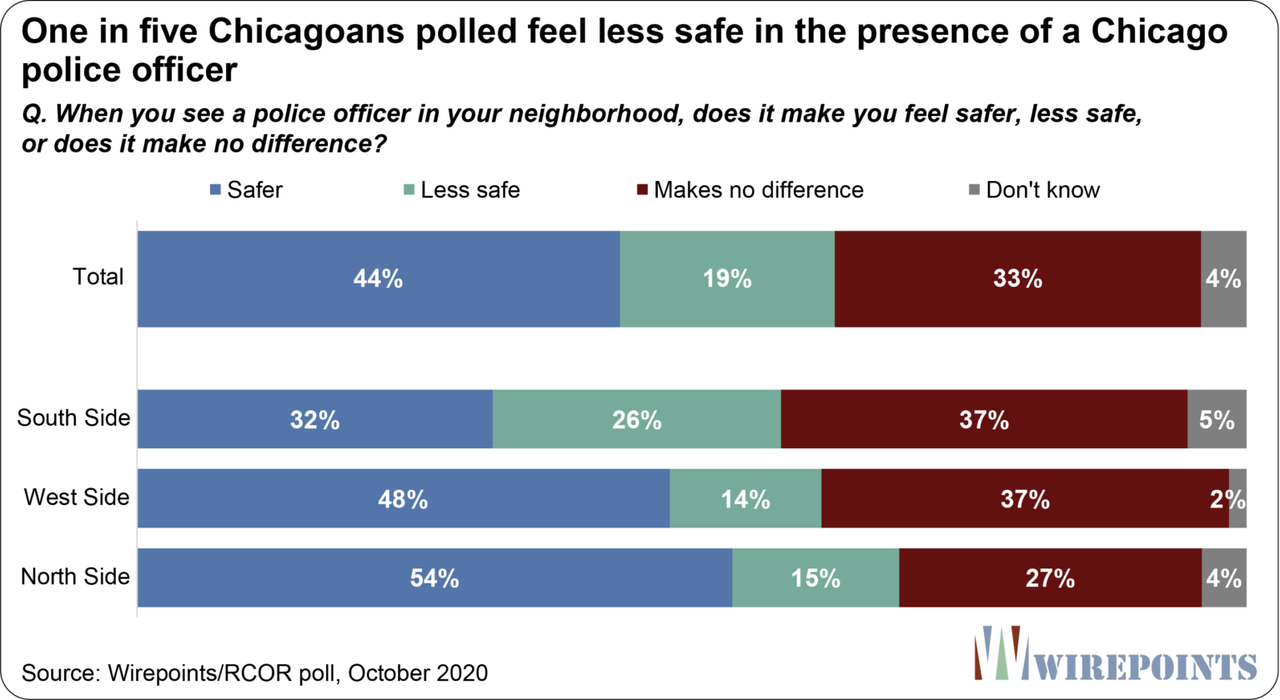

When asked how they thought they would be treated by officers, more than a third of Chicagoans (35%) said they were not very or not at all confident they would be treated with courtesy and respect. And in a similar vein, one in five of those surveyed (19%) said that seeing a police officer made them feel less safe.

In summary, while white and Hispanics ultimately have a mixed view of the city’s police force, black residents report more negative opinions/experiences:

63% of black residents think the Chicago Police Department is handling its job badly, while only 48% of Hispanics and 39% of whites feel the same way.

More than half (57%) believe reforms should focus on systemic racism in the Chicago Police Department, while only 33% of Hispanics and 41% of whites believe the same.

More than half (54%) aren’t confident they’ll be treated with courtesy and respect by officers, while only 38% of Hispanics and 16% of whites aren’t confident.

Nearly a third (31%) of blacks feel less safe in the presence of an officer, while only 11% of Hispanics and 13% of whites feel less safe.

Mayor Lightfoot has her work cut out for her on race and public safety

Of the 61% of respondents who approve of the job Mayor Lightfoot is doing, Chicago’s white residents gave her the highest marks (68%), followed by blacks (63%) and then Hispanics (48%).

Her biggest support came from the West Side, where 69% of responders approved of her performance. South Side residents favored her performance the least, giving an approval rating of 57%.

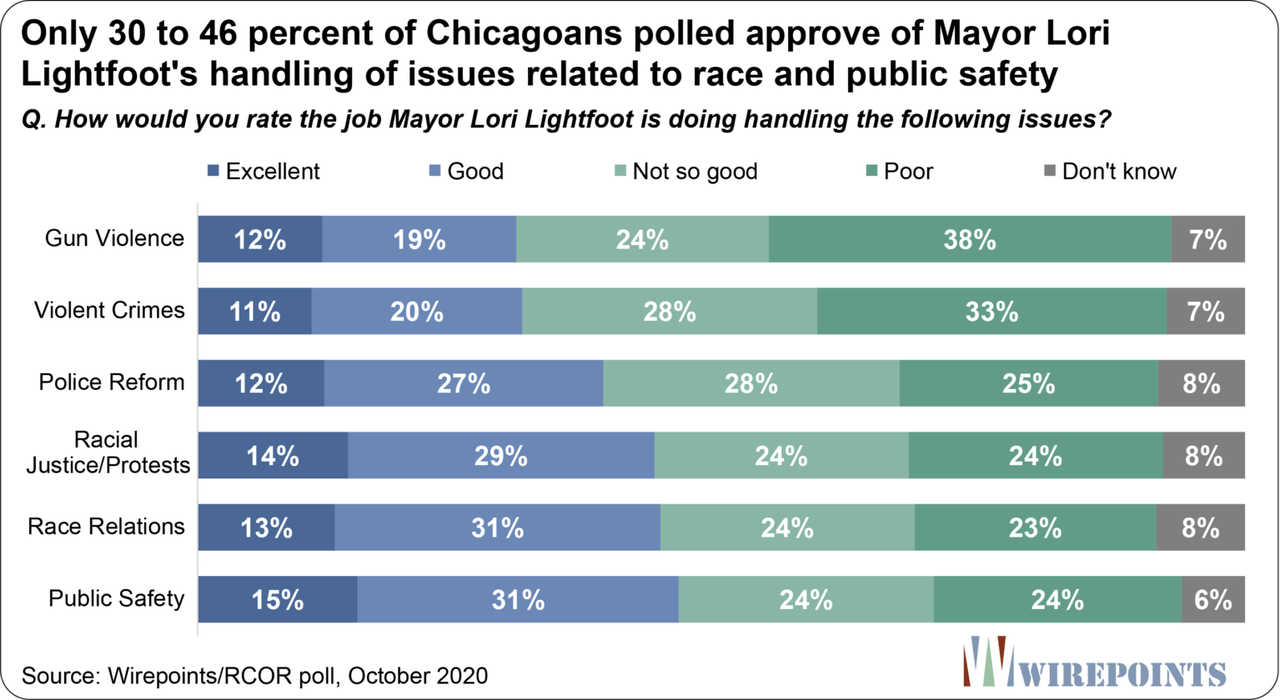

On individual issues, Mayor Lightfoot achieved her best ratings on her handling of the Coronavirus (58% excellent or good; 39% not so good or poor) and economic development (50% excellent or good; 37% not so good or poor). However, her ratings on those related to race relations and public safety are lower.

Lightfoot’s handling of public safety has an approval rating of 46%. Her overall approval on racial justice is 44%. On police reform, 39%. And just 31% on gun violence.

Her lowest approval ratings come from black Chicagoans. Just 26% approve of the way the mayor is handling both violent crime and gun violence.

via ZeroHedge News https://ift.tt/37YZKfv Tyler Durden

DoubleLine: Digital Currencies Will End The Dollar’s Status As The World’s Reserve Currency Tyler Durden

Thu, 10/29/2020 – 17:25

We most recently described the Fed’s stealthy plan to deposit digital dollars to “each American” during the next crisis as an unprecedented monetary overhaul, but more importantly, a truly stealthy one: there has barely been any media coverage of what may soon be a money transfer by the Fed – a direct stimulus to any and all Americans – bypassing the entire Legislative branch in an attempt to spark inflation after years of losing the war with deflation.

That’s why two weeks ago we we delighted to read that none other than Jeff Gundlach’s DoubleLine, one of the highest profile asset managers today, published a paper authored by fixed income portfolio manager Bill Campbell exposing what it called “The Pandora’s Box of Central Bank Digital Currencies”, in which it echoed our claims, writing that “such a mechanism could open veritable floodgates of liquidity into the consumer economy and accelerate the rate of inflation. While central banks have been trying without success to increase inflation for the past decade, the temptation to put CBDCs into effect might be very strong among policymakers. However, CBDCs would not only inject liquidity into the economy but also could accelerate the velocity of money. That one-two punch could bring about far more inflation than central bankers bargain for.”

Alas, that was not enough to bring the topic of central bank digital currencies into the mainstream financial media, which is perhaps understandable for two reasons: i) everyone’s attention is glued to the outcome and the implications of the election and ii) most media members think of CBDCs as some useless version of bitcoin, when nothing could be further from the truth.

So perhaps in hopes of attracting much needed attention to just how profound the monetary overhaul that is quietly taking place behind the scenes, Doubleline’s resident digital currency expert, Bill Campbell has penned a follow up note to his original report, in which he explains in stark and vivid clarity what is about to happen. In a nutshell, “the world’s central banks and the Bank of International Settlements (BIS) envision a network of multiple cross-border payment systems featuring direct bilateral exchanges in the world’s different currencies. Such a regime would discard the decades-long mediation through the world’s reserve currency, the U.S. dollar.” In short, central banks are preparing to launch cross-border payment systems which represent a new global order which poses a “major threat to the dollar and its status as the world’s reserve currency.”

Below we republish the full note in whole due to its accurate and succinct assessment of how profoundly CBDCs will change the existing monetary architecture once they are launched in a few years (or earlier):

* * *

Bilateral Digital Currency Payments and the Twilight of the Dollar

by Bill Campbell, fixed income Portfolio Manager at DoubleLine (link)

If launched, central bank digital currencies (CBDCs), as I have recently warned, will put at risk the independence of monetary policy and what little is left of fiscal discipline within their borders of circulation.1 Central banks are not stopping at the replacement of money as we have known it. In conjunction with their developmental work on digital currencies proper, monetary authorities are devising a new structure for electronic payments to sweep aside the decades-long framework for payment settlements, both domestic and international. The world’s central banks and the Bank of International Settlements (BIS) envision a network of multiple cross-border payment systems featuring direct bilateral exchanges in the world’s different currencies. Such a regime would discard the decades-long mediation through the world’s reserve currency, the U.S. dollar. This paper examines implementation plans for cross-border payment systems and the threat this new global order would pose to the dollar and its status as the world’s reserve currency.

King Dollar: A Brief History

The dollar has stood as the world’s reserve currency since taking that crown from the British pound in 1944. In July of that year, delegates from 44 nations met in Bretton Woods, N.H., convening the United Nations Monetary and Financial Conference, where they reached a series of agreements for the post-WWII international monetary system. The dollar formed the monetary linchpin of the new order. Participating nations pegged their currencies to the U.S. dollar and in exchange received the privilege to redeem dollars in gold from the U.S. (the world’s largest holder of gold reserves) at the congressionally set rate of $35 an ounce. This started a period of “exorbitant privilege” for the U.S., to quote former French Presidents Charles de Gaulle and Valéry Giscard d’Estaing. Ever since then, thanks to the dollar’s reserve status, the U.S. can run a balance-of-payments deficit without the need to adjust domestic policy in order to settle its international trade bill. Because most international trade is transacted in dollars, which I explain in more detail below, in the most-extreme cases, the U.S. can print dollars to settle its balance of payment needs.2 All other nations must purchase dollars to fund their imports, and one way to attract foreign capital is with high real interest rates (interest rates above the domestic rate of inflation). On the margin, tighter monetary policy slows growth and compresses imports while attracting foreign capital. The U.S. doesn’t face that trade-off thanks to the dollar’s privileged status as the world’s reserve currency.

By the end of the 1960s, rising inflation and a surplus of overseas dollars had made dollar-gold convertibility unsustainable, and President Richard Nixon unilaterally canceled it on Aug. 15, 1971.3 The “closing of the gold window” effectively doomed the system of fixed currency exchange rates elaborated at Bretton Woods. By 1973, the regime of fixed exchange rates gave way to free-floating exchange rates. Despite de facto nullification of Bretton Woods, the U.S. dollar has remained unquestioned as the world’s reserve currency. Most of the world’s trade is transacted in dollars, with the majority of commodities traded in dollars. According to the International Monetary Fund, the dollar plays a dominant role in global invoicing. Through April 2020, the BIS reported, “The US dollar retained its dominant currency status, being on one side of 88% of all trades. The share of trades with the euro on one side expanded somewhat, to 32%.” The Japanese yen ranked third, with the currency being used on one side of 17% of all trades.4

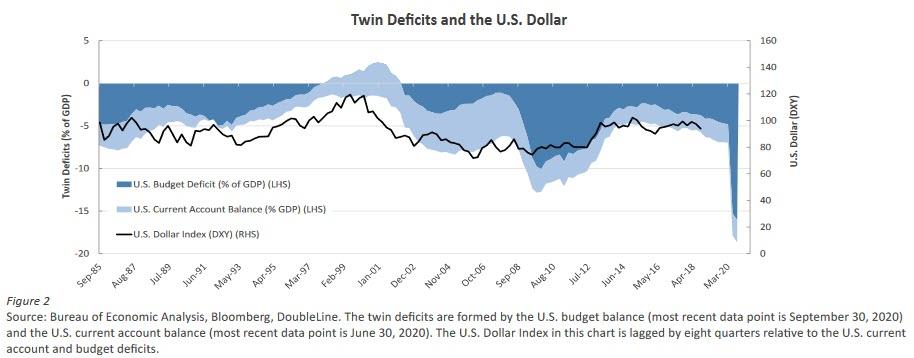

The grumblings of French heads of state and other critics notwithstanding, a reserve currency is useful. (Figure 1) It facilitates global transactions, investments and international debt issuance, and interest payment and repayment by acting as a common denominator accepted by all countries. However, new conditions might be converging to depreciate the dollar in the forex markets and even one day topple its crown as the world’s reserve currency. In that event, the past of the British pound might not be prologue for the dollar. If central banking and the BIS dethrone King Dollar, I suspect no single currency will seize the crown of reserve currency. Instead, cross-border payments would be mediated by a conglomeration of bilateral arrangements.

Admittedly, for countries outside the U.S., such a system offers a very positive, even compelling feature: All countries would be able to settle their import bills in their own currencies, a privilege afforded predominantly to the United States and, to a lesser but noteworthy extent, the 19 countries constituting the eurozone and Japan. Even these countries, however, are obliged to settle payments for certain non-U.S. imports, notably oil and other commodities, in dollars.

SWIFT and Usurpers in the Wings

A key to the longevity of the dollar’s reign as the world’s reserve currency is its occupation as the principal medium of exchange by the Society for Worldwide Interbank Financial Telecommunication (SWIFT), the dominant provider of cross-border payment settlements. On May 3, 1973, which is to say, around the time fixed-rate forex regimes gave up the ghost, SWIFT was founded in Brussels with the support of 239 banks in 15 countries. Today, according to its website, the company connects more than 11,000 banks, securities organizations, market infrastructures and corporations in 200 countries. With the propagation of blockchain and cryptocurrency technologies, SWIFT faces fair and inevitable competition from new players in the private sector as well as older competitors in the business of the settlement of cross-border payment orders.5 SWIFT has been updating its infrastructure as well. In January 2017, the company rolled out its global payments innovation (gpi). In 2019, cross-border transfers via gpi exceeded $77 trillion, accounting for 56% of all cross-border payments for that year and 65% of SWIFT’s total cross-border payments, making gpi by far the most-used messaging system for international payment in the world.6

Whatever its resilience or vulnerability to private-sector challengers, SWIFT’s dominance faces a serious threat from outside the private sector – namely, the central banks, coordinated by the BIS. In a recently issued paper, the BIS and cosignatories, including the U.S. Federal Reserve Board of Governors and the European Central Bank, stated, “Central bank innovation is an opportunity for cooperation. Simultaneous research and exploration of CBDC by central banks could inform ways to improve cross-border payments.”7 The BIS has been spearheading research into “faster, cheaper, more transparent and more inclusive cross-border payment services [which] would deliver widespread benefits for citizens and economies worldwide, supporting economic growth, international trade, global development and financial inclusion.”8 The BIS has acknowledged that, despite technological advances in creating a new cross-border payments infrastructure, some of these central bank initiatives “are still in their design phase and others remain theoretical.”9 In a working paper published by the BIS, authors Raphel Auer, Giulio Cornelli and Jon Frost wrote, “Central banks are considering multiple technological options simultaneously, current proofs-of-concept tend to be based on distributed ledger technology (DLT) rather than a conventional technological infrastructure.”10 However, the landscape is quickly changing as more central banks scale up research into payment systems.

We have already started to see movement on these initiatives. China and Russia have already rolled out competing settlement systems to SWIFT, and both are looking into more bilateral settlement capabilities with their trading partners. In 2014, Russia implemented an alternative to SWIFT called the System for Transfer of Financial Messages (SPFS). SPFS was seen as a response to the U.S. using its dominance in the global financial system to implement sanctions on Russia, its companies and individuals. In 2015, China launched its Cross-Border Interbank Payments System (CIPS). Stung like Moscow by U.S. financial sanctions, Beijing is encouraging its financial sector to make the switch from SWIFT. As more central banks work on their own settlement systems, Russia and China have shown that implementation can be a realistic goal.

“Uneasy lies the head that wears a crown.”

I foresee several big implications of the implementation of a new global payments system based on the bilateral regimes, all of which would put structural pressure on the dollar.

First, such a decentralized global payments system would take the world a big step toward removing the need for the dollar, or for that matter any other currency, to remain as the world’s reserve currency. Cross-border counterparties would settle payments in bilateral transactions in their own currencies, bypassing the dollar as an intermediary. The U.S. imports much more than it exports. These large current-account deficits create the need to have foreigners put their excess savings into U.S. assets to help stabilize the dollar. If foreign savings cease flowing into the U.S., the dollar will depreciate unless the import-export imbalance is corrected. (Figure 2)

Second, global central banks would no longer need to stockpile dollars and instead could diversify their foreign exchange (FX) reserves to a mix more commensurate with the countries with which they trade and conduct financial transactions. Dollar debt remains a large source of financing for many countries around the globe, but sovereign, corporate and other institutional borrowers have already begun to move some of this external financing into other denominations such as the euro and the yen.

Third, disintermediation of the dollar in cross-border payments could erode the greenback’s central role in pricing commodities and invoicing global trade. This would reduce a structural buyer of dollars. Outside the U.S., central banks have been forced to build up their dollar FX reserves in order to prevent a disorderly sell-off if exporters do not repatriate their dollar profits. In addition, in a reversal of norms in place since Bretton Woods, non-U.S. central banks might look to increase their holdings of gold relative to their dollar reserves.11 Central banks might increase the portion of their reserves allocated to gold, whose finite supply could help reduce debasement fears with respect to infinitely creatable CBDCs.

The End of a Single World Reserve Currency?

With the exception of two world wars in the first half of the 20th century, the world’s financial systems since 1815 have calibrated their international payments and banking reserves to a single reserve currency, first the British pound and the U.S. dollar since 1944. The nearly 80-year absence of viable alternatives has left Americans complacent about the dollar’s perpetuity as the world’s reserve currency. Outside the U.S., however, central banks and governments appear to foresee a future untethered from the dollar. The technology for such a delinking is here or soon will be. Central banks will possess the infrastructure to match their FX reserves to the currency mix and weightings of their balance of payments – and one day displace the dollar without the need to crown a new reserve currency.

Policymakers continue to steer intently into the uncharted waters of central bank digital currencies and decentralized global payment systems. Despite most of these initiatives still being in their theoretical design phase, global coordination among central banks will speed up their development and potential implementation. Armed with these currency and payment technologies, the world could rescind the exorbitant privilege the U.S. has enjoyed as printer of the world’s reserve currency and place structural pressure on the dollar to depreciate.

2 The balance of payments includes all transactions made between entities in one country and the rest of the world over a defined period of time.

3 “Foreigners’ liquid gold claims on US dollars increased tenfold from around $7 billion in 1953 to around $70 billion in 1971. Over the same period US gold reserves fell from over $22 billion to less than $11 billion. The inescapable decision facing the US authorities was taken on 15 August 1971 when the convertibility of the dollar at the fixed price of $35 per ounce of gold was ended,” Glyn Davies, A History of Money (4th edition: revised by Duncan Connors; 2016), pp. 465-466. University of Wales Press

7 “Central bank digital currencies: foundational principles and core features,” Oct. 9, 2020, p. 3. Bank of Canada, European Central Bank, Bank of Japan, Sveriges Riksbank, Swiss National Bank, Bank of England, Board of Governors Federal Reserve System and the Bank for International Settlements. https://www.bis.org/publ/othp33.pdf

8 “Enhancing cross-border payments: building blocks of a global roadmap,” Committee on Payments and Market Structures, BIS, July 2020. https://www.bis.org/cpmi/publ/d193.pdf

9 Ibid, page 4.

10 Raphael Auer, Giulio Cornelli and Jon Frost, “Rise of the central bank digital currencies: drivers, approaches and technologies,” BIS, August 2020, p. 5. https://www.bis.org/publ/work880.pdf

Earlier today, attorneys for Luzerne County, Pennsylvania, filed a notice of withdrawal of their prior motion seeking the recusal of Associate Justice Amy Coney Barrett from Republican Party of Pennsylvania v. Boockvar. As I noted here, after the initial motion was submitted, the Luzerne County Council voted in support of withdrawing the motion.

The notice of withdrawal makes no mention of the County’s vote. It reads as follows:

Given the Supreme Court’s safety protocols, I understand that the Motion to Recuse which was electronically submitted on October 27, 2020, has not yet been officially filed. Given the Supreme Court’s refusal to expedite consideration of the petition for a writ of certiorari, thus allowing the Order of the Supreme Court of Pennsylvania to stand presently, we therefore request that the Motion be considered withdrawn.

The docket for the case now indicates that the prior motion was not accepted for filing.

For reasons I explained here, I do not believe the applicable standards or relevant precedent supports Justice Barrett’s recusal, though each justice ultimately decides whether to recuse in a given case.

from Latest – Reason.com https://ift.tt/37SNEEv

via IFTTT

Earlier today, attorneys for Luzerne County, Pennsylvania, filed a notice of withdrawal of their prior motion seeking the recusal of Associate Justice Amy Coney Barrett from Republican Party of Pennsylvania v. Boockvar. As I noted here, after the initial motion was submitted, the Luzerne County Council voted in support of withdrawing the motion.

The notice of withdrawal makes no mention of the County’s vote. It reads as follows:

Given the Supreme Court’s safety protocols, I understand that the Motion to Recuse which was electronically submitted on October 27, 2020, has not yet been officially filed. Given the Supreme Court’s refusal to expedite consideration of the petition for a writ of certiorari, thus allowing the Order of the Supreme Court of Pennsylvania to stand presently, we therefore request that the Motion be considered withdrawn.

The docket for the case now indicates that the prior motion was not accepted for filing.

For reasons I explained here, I do not believe the applicable standards or relevant precedent supports Justice Barrett’s recusal, though each justice ultimately decides whether to recuse in a given case.

from Latest – Reason.com https://ift.tt/37SNEEv

via IFTTT

A Columbia University School of Social Work adjunct lecturer said that the American flag is a symbol of genocide.

Responding to a tweet stating that “the hammer and sickle is a symbol of genocide” and comparing the communist emblem to the swastika, Anthony Zenkus placed the American flag in the same category.

“The American Flag is a symbol of genocide,” said Zenkus.

“Unless centuries of slavery and the vanquishing of Native American nations doesn’t figure into your equation.”

The American Flag is a symbol of genocide. Unless centuries of slavery and the vanquishing of Native American nations doesn’t figure into your equation. https://t.co/cSmea0zcNX

Zenkus’ faculty profile explains that he is an “activist on issues of racial justice, income inequality, and climate justice.” He was additionally “trained by Vice President Al Gore as a presenter in his Climate Reality Project, and has been an organizer with Occupy Wall Street, the fight for a $15 minimum wage, and an ally in the Movement for Black Lives.”

Similarly, a postdoctoral researcher at Brown University, Carycruz Bueno, tweeted that vacation rental company Airbnb “doesn’t understand the trauma” of Trump signs for a Black person, as previously reported by Campus Reform. A Virginia Tech professor also recently suggested that Vice President Mike Pence’s use of the phrase “the American people,” during the vice presidential debate was also racist.

The researcher even said that the American flag can be “used in many places to scare Black people.”

Campus Reform reached out to Zenkus to ask for additional comments but did not receive a response in time for publication.

via ZeroHedge News https://ift.tt/2JiDFOC Tyler Durden

AAPL Plunges After iPhone Sales Miss, China Revenues Plummet, Lack Of Forecast Tyler Durden

Thu, 10/29/2020 – 16:52

Moments after earnings disappointments by Twitter and Amazon, the world’s largest company, Apple whiffed when it reported Q4 revenue and earnings that beat expectations, but a big miss on iPhone revenues, a collapse in Chinese sales and the lack of guidance is why the stock is tumbling after hours.

Below are the highlights from Q4:

Revenue $64.70 billion, beating estimates of $63.47 billion

EPS 73c (down from 76c y/y), and beating estimates of 70c

Service revenue $14.55 billion, beating estimates of $13.87 billion

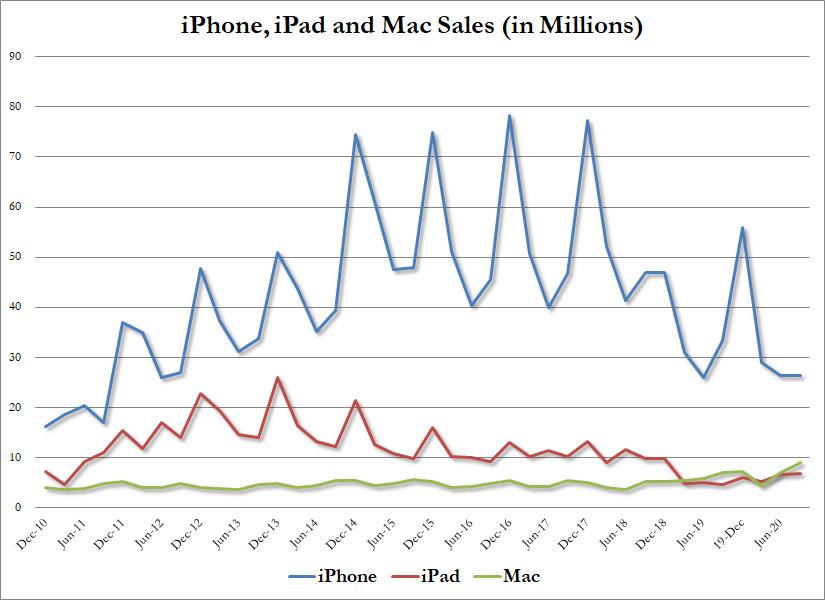

So far so good. But where things got ugly was the breakdown in unit sales and here there was a rather painful miss in iPhone revenue which came in at $26.44 billion, below the estimate of $27.06 billion, and down 20% from the $33.3BN a year ago. Wall Street was not amused. Other segments generated the following revenues:

Mac sales were $9 billion, up 29%, above expectations of $8.04 billion.

IPad revenue came in at $6.797 billion, up 46%, and also better than expectations of $6.06 billion.

Wearables provided Apple with $7.87 billion of sales, up 21%, beating estimate of $7.35 billion.

And visually, it is becoming quite clear that the star of the iPhone – which peaked in 2017 – has now set.

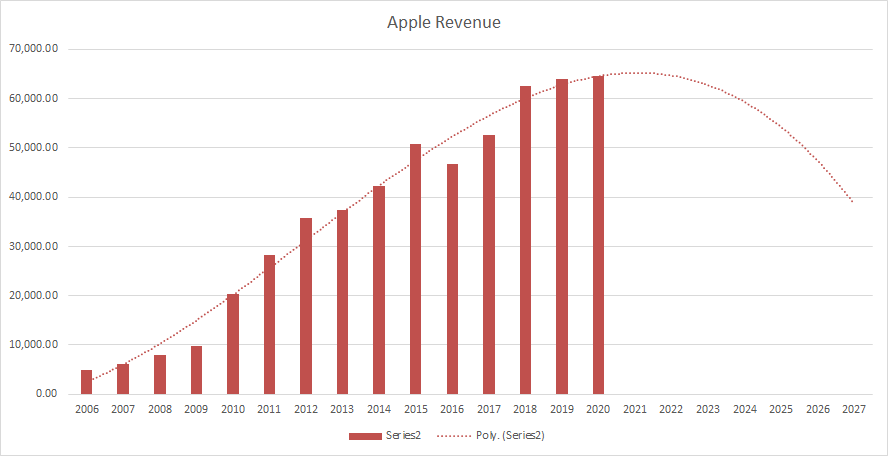

One wonders if the peak in iPhone sales isn’t also the peak of the company’s revenues, as the following chart would suggest.

And while AAPL’s service revenue was clearly impressive, surging to a record $14.55BN, and above the $13.87BN estimate…

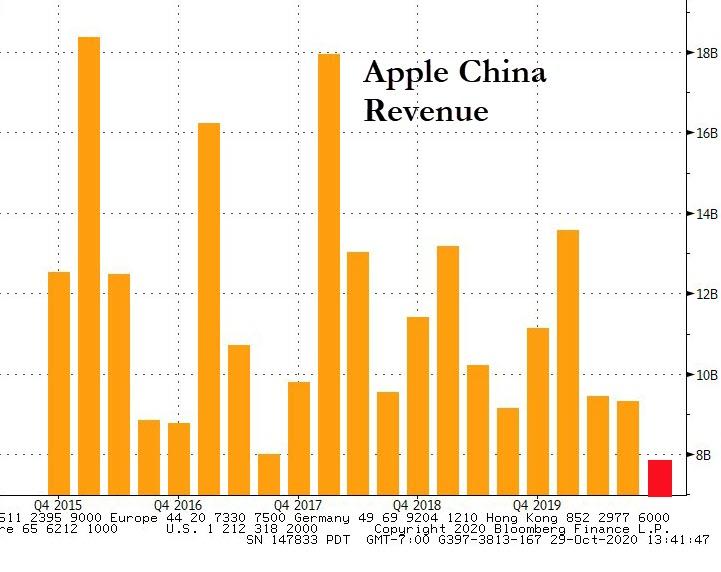

… this was more than offset by another major flashing red alert, namely the collapse in China revenues, which plunged a whopping 29% in Q4…

… from $11.134BN to just $7.9BN, the lowest on record.

And one final reason why investors were less than excited: for yet another quarter, AAPL refused to provide a forecast, suggesting that the storm has more to go.

Commenting on the results, CEO Tim Cook was of course upbeat saying that “Apple capped off a fiscal year defined by innovation in the face of adversity with a September quarter record, led by all-time records for Mac and Services,” and adding that “despite the ongoing impacts of COVID-19, Apple is in the midst of our most prolific product introduction period ever, and the early response to all our new products, led by our first 5Genabled iPhone lineup, has been tremendously positive.”

Alas, shareholders did not see things that way and the stock plunge after hours No forecast, weak iPhone revenue and a very bad quarter in China are what’s giving investors pause here.

via ZeroHedge News https://ift.tt/2TCnnSA Tyler Durden

Peter Schiff delivered a key-note speech at the Virtual Investor Day Conference. He walked through the history of the Federal Reserve’s monetary policy over the last several decades and explained the inevitable outcome. Peter’s recap of Fed history leads you to an undeniable conclusion: the Federal Reserve has never been right. And it has set us up for an even bigger crisis.

Peter opened his talk saying that he thinks we are entering the final chapter of the book Alan Greenspan started to write.

And I have a feeling he had an understanding of how badly it was going to end. But unfortunately, a lot of people who have been adding pages or chapters to that book since Greenspan resigned really don’t have any idea what’s coming.”

Greenspan started the book by unleashing the loose money policy that blew up the dot-com bubble.

When that bubble popped, instead of admitting his mistakes, Greenspan ignored them and tried to revive the economy by inflating a bigger bubble in the real estate market than the bubble that had just popped in the stock market. And the Fed succeeded in inflating that bubble. But that was not a success. It was a failure.”

Peter reminds us that he warned that the Fed policy was distorting the economy. He knew that it was creating a bubble economy. People were using the inflated value of their homes as ATMs and that drove consumer spending. People were living beyond their means. Nobody was saving.

So, the whole economy was distorted by the malinvestments and bad decisions that were being made as a result of artificially low interest rates.”

When the Fed tried to normalize, the bubble popped, the mortgage market blew up, and that gave us the Great Recession.

In the wake of the 2008 financial crisis, the Federal Reserve repeated the process, dropping interest rates to zero and launching quantitative easing. Ben Bernanke promised QE was just temporary – that the Fed was not monetizing the debt. He promised the Fed would shrink its balance sheet once the crisis passed. At the time, Peter said it was impossible. He said even if the Fed tried to normalize rates and shrink its balance sheet, it would fail.

Everything the Fed said about their ability to normalize rates and shrink the balance sheet was wrong. I said they were wrong as they were saying it. They never were able to normalize interest rates. They never came close to returning the balance sheet to pre-crisis levels.”

In Q4 2018, the Fed abandoned rate hikes at about 2.5% – not even close to normal. They called off quantitative tightening. By 2019, the Fed was back to rate cuts and the launched QE, all the while claiming it wasn’t QE. The Fed told us the pivot back to loose monetary policy was only temporary, calling it a “midcourse correction.” But Peter said we were going back to zero and that’s exactly what happened.

And here we are today with the central bank running QE infinity and saying rates will stay at zero for years.

We are now the banana republic that Ben Bernanke assured us we would never become.”

Peter said he went through the history of Fed failures to make a point that should be pretty obvious.

The Federal Reserve has never been right. Everything they have said about the efficacy of their policies, what their policies would create, and their ability to reverse them or unwind them, has been wrong. And it’s amazing how consistently wrong they have been.”

And now they are pushing toward the logical conclusion.

We are headed for a US dollar crisis and a sovereign debt crisis. The magnitude of this crisis will be unlike anything we’ve ever experienced. Because this is not just mortgages blowing up. This is the credit of the United States government. This is the risk-free asset becoming the most toxic asset on the planet. And it’s not just US Treasuries that are going to collapse, but it’s the entire US-denominated bond market which is built on top the foundation of US Treasuries. So, Treasuries go — it all goes — corporate bonds, muni bonds, mortgages. Any debt instrument that is denominated in US dollars is going to collapse.”

So where will people run?

Gold.

The world is going to return to gold-backed paper money.”

via ZeroHedge News https://ift.tt/2HIQH7k Tyler Durden

{kind=link}

{kind=link}