Last Wednesday, the Federal Reserve announced the latest decision concerning monetary policy which contained three primary components:

A cut of 25bps

Stopping balance sheet reductions (or Quantitative Tightening or Q.T.)

An outlook suggestive this may be the only rate cut for a while.

While stocks dropped on disappointment they Fed may not cut further; it didn’t take long for bullish commentators to start suggesting why the cuts were supportive of higher asset prices. To wit:

“Given today’s Fed decision and guidance, we remain comfortable with our view that the Fed will provide two more 25bp cuts this year (September and October),” – Bank of America.

Simply, cutting rates, and stopping Q.T., is the return of “accommodative policy” for the markets and the “ringing of Pavlov’s bell.” Via CNBC:

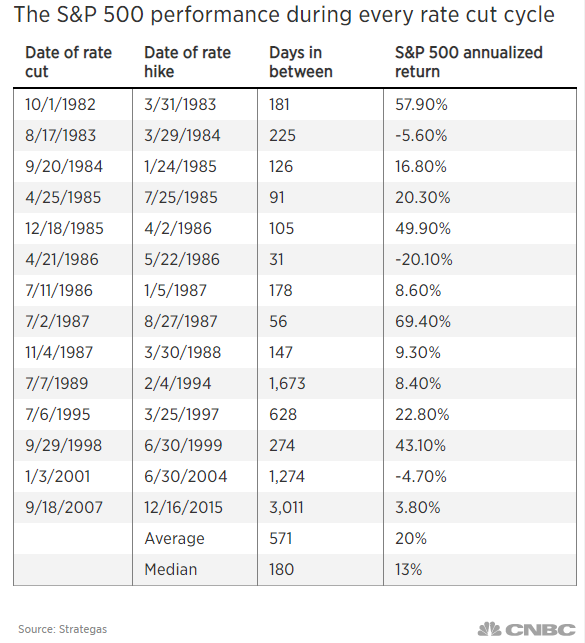

“The old investing mantra ‘don’t fight the Fed’ stands the test of time for a reason. Going back to 1982, the average annualized return for the S&P 500 between the first rate cut and the next hike has been 20%, while the median increase has been 13%, according to Strategas. The data show investors would do well if they invest in a way that aligns with the Federal Reserve’s policy direction, rather than against it, hence ‘don’t fight the Fed.’”

This is an interesting premise because when the Fed started hiking rates at the end of 2015, it also was bullish. Via Forbes:

“Early in a rate increase cycle, however, higher rates are actually good for the stock market. This is because rising rates, early on, signal an improving economy, and the faster growth more than compensates for higher rates.”

So, exactly “when” are Fed actions are “not bullish?”

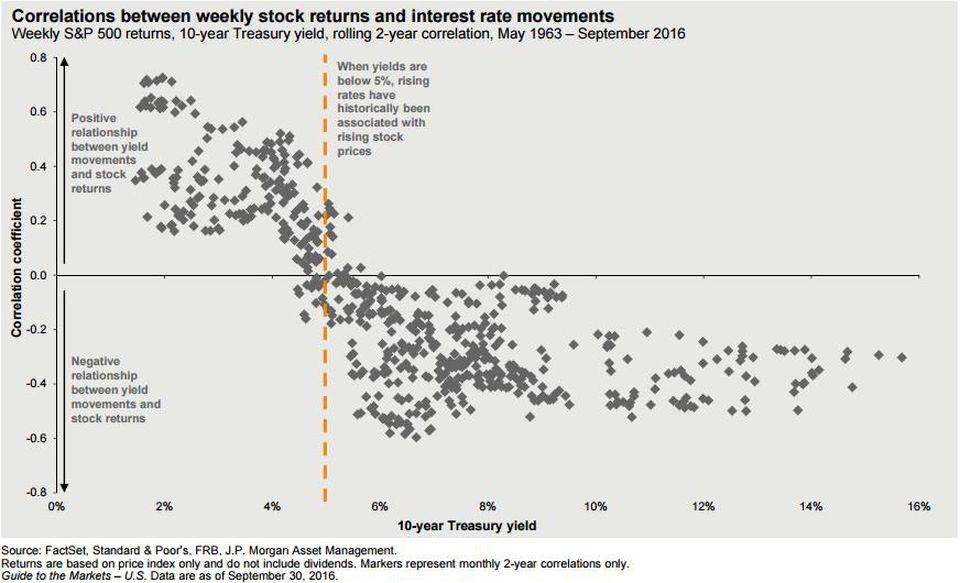

“Lower rates have less impact on the ‘economy,’when the monetary transmission system is weak. This is evident from the fact that surging asset prices have left 80% of the population behind in terms of higher levels of prosperity. This also is why tax cuts failed to work as intended. After a decade of low rates, and excess liquidity, the ability to ‘pull-forward’ demand has become limited.”

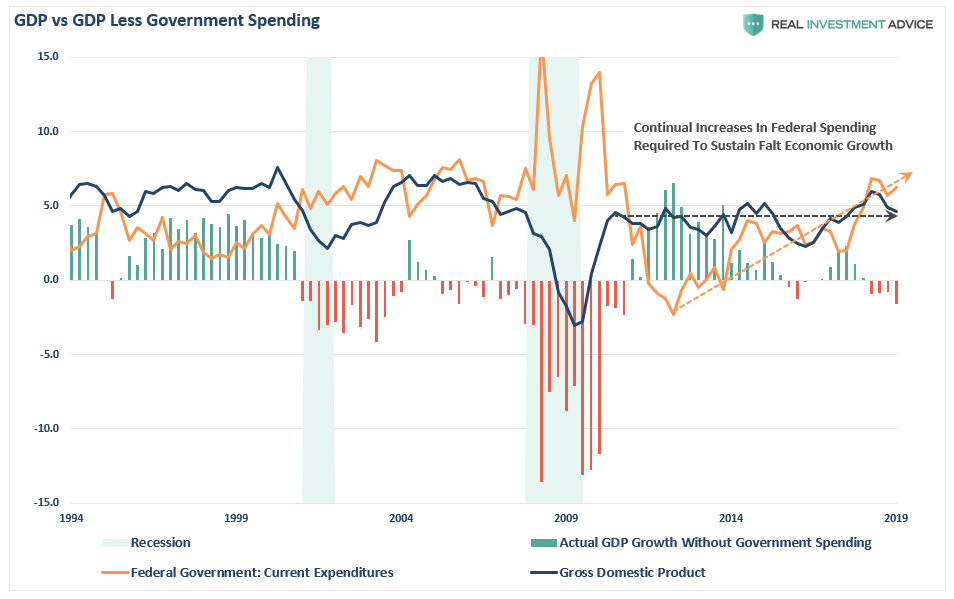

While, in the short-term, it may seem that whatever the Fed does is “bullish,” as the performance of the stock market since 2009 would seem to support, it has been a function unbridled fiscal largesse. As shown in the chart below, the Fed’s actions have been supported by a massive amount of Government spending as noted last week:

“As shown in the chart below, since 2010 it has taken continually increases in Federal expenditures just to maintain economic growth at the same level it was nearly a decade ago.”

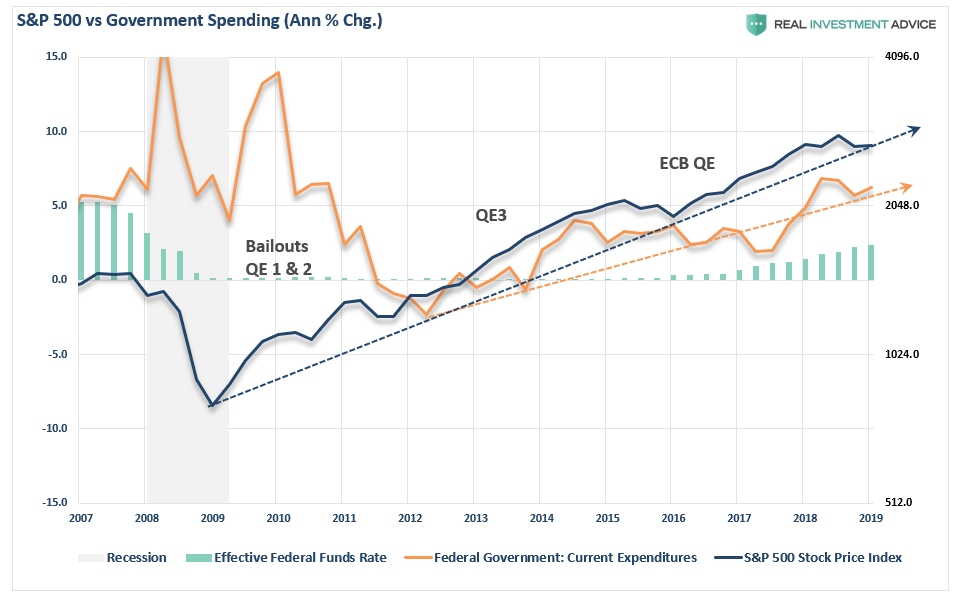

But let’s modify that chart to compare the Fed’s actions plus government expenditures to the S&P 500.

With that much liquidity sloshing around, it had to go somewhere. Not surprisingly, as the Fed suppressed interest rates, it forced investors to chase yield.

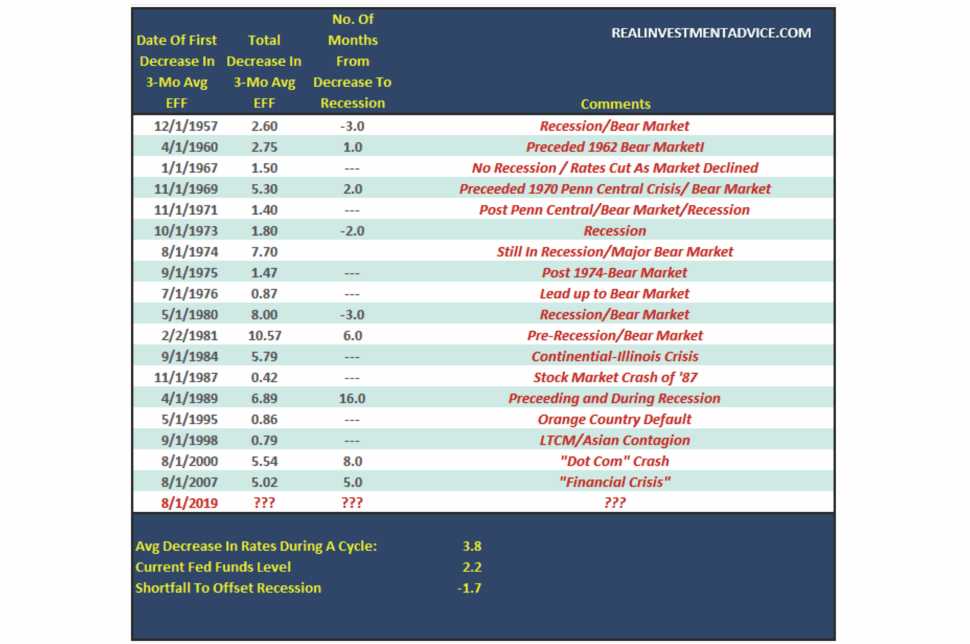

The problem with the table from CNBC above, as it only tells you what happens immediately after the Fed cut rates the first time. By the time the Fed is starts cutting rates, the markets are well entrenched into a bullish trend. Stocks aren’t beginning a bull run, but rather are being carried higher by existing momentum which has typically been a hallmark of a late-stage bullish cycle. In every case, there was an eventual negative outcome following Fed rate cut cycles. (The table below uses the 3-month average of the effective Fed Funds rate.)

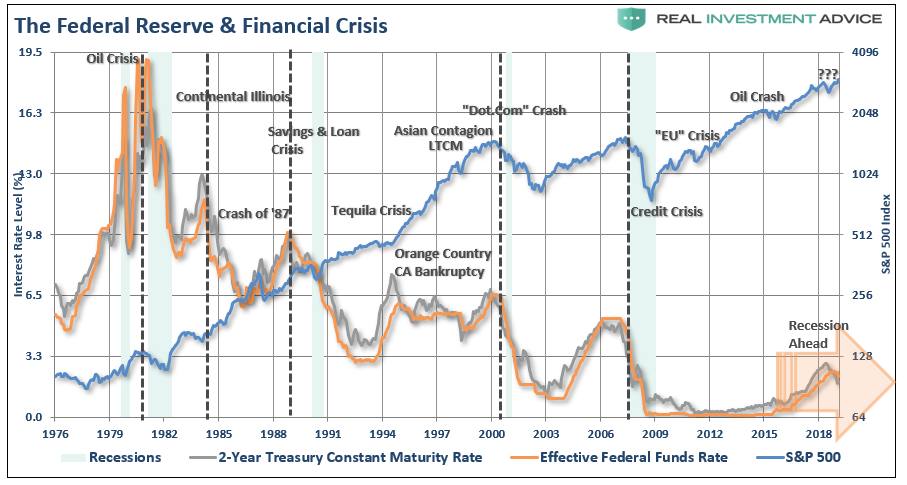

The chart of the effective Fed funds rate and the S&P 500 tells the story. (The vertical dashed lines marked the initial cuts, and you can see where subsequent crisis and declines occurred.)

The one exception was the initial rate cut in 1995 following the Orange County Bankruptcy, an “insurance cut,” despite both a strong market and economy at the time. As recently noted by J.P. Morgan:

“The late 1990’s rate cuts were used as insurance against Mexican and Russian default and collapse of hedge fund Long-Term Capital Management at the time, bolstered the equity market. The only other time the S&P 500 saw stronger performance following a rate cut was in 1980.”

The early 1980s are NOT comparative to the current cycle.

The U.S. economy was just coming out of back-to-back recessions

Valuations were extremely low

Dividends were high; and,

Inflation and interest rates were in double-digits.

President Reagan had just passed tax reform

The banks were deregulated; and,

Inflation and interest rates were beginning a 40-year secular decline.

Household debt was only about 60% of net worth and just starting a 40-year “leveraging cycle” .

In other words, there was nowhere for the market to go but up.

Clearly, such is not the case today, as deflation, debt, and demographic shifts loom large.

But What About 1995?

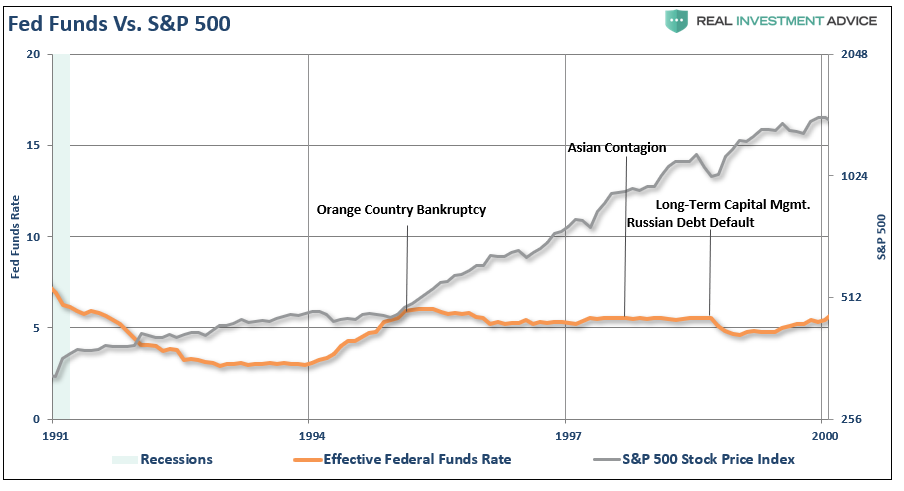

The mid-late 1990’s rate cuts was also another anomalous market environment. The Fed began a rate hiking campaign in 1993 as the economy began to stretch its legs post the 1991 recession. However, the Fed cut rates slightly in 1995, and again in 1998, to offset the risk imposed from three major market-related events. Ironically, it was the Fed’s tightening of monetary policy which contributed to those events.

Another critical point is that rates were relatively stable post the 1991 recession rather than the rather sharp increase we have seen over the last couple of years. Also, economic growth, as I showed last week, was running at an average of 3.5% on an inflation-adjusted basis, versus 2%-ish today.

Importantly, the markets sharp advance in the late-1990’s was due to a period of “market nirvana” as the internet became mainstream changing the way information was accessed, utilized, and institutionalized.

Mutual funds were a virtual “Hoover vacuum” sucking up retail assets and lofting asset prices higher.

Pension funds were finally allowed to invest in stocks, rather than just Treasuries, which brought massive buying power to the markets.

Foreign flows also poured into Wall Street to chase the raging bull market higher.

Lastly, “internet trading” hit the internet, which further opened the doors of the “WallStreet Casino” to the masses.

Yes, for a brief moment, the markets raged as “irrational exuberance” prevailed. Of course, while the rate cuts in 1995 didn’t slow the growth of the “bubble” immediately, it wasn’t long before all the gains were wiped out by the “Dot.com” crash.

Timing, as they say, is everything.

This Isn’t 1995

A quick comparison between 1995, and today, also elicits many other concerns about the markets ability to dramatically extend its current cycle.

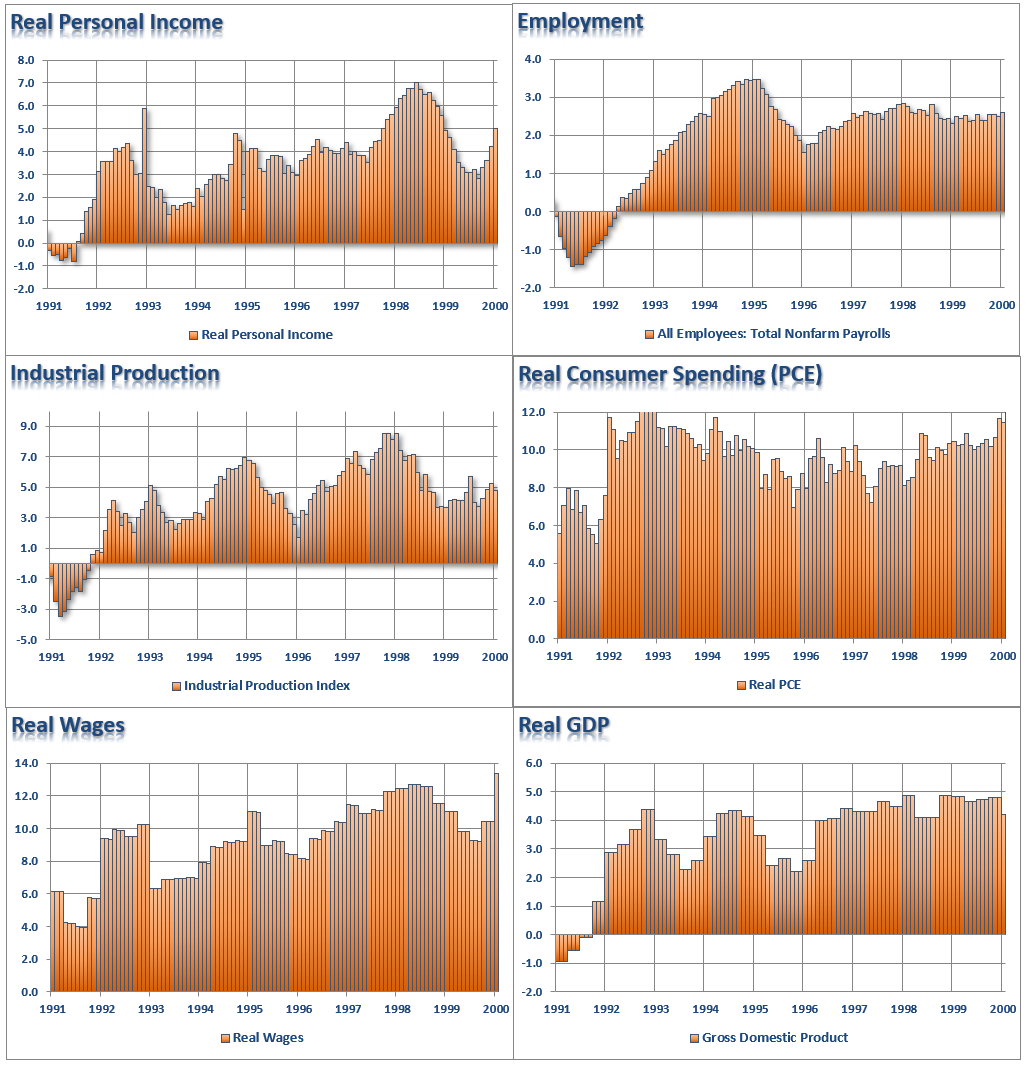

From 1991-2000 (10-Years)

Personal Incomes averaged 4% and were rising to 5% on an annual rate

Employment averaged a 2.5% annual growth rate and was solid heading into 2000.

Industrial Production averaged about 5% annual growth and was rising at the end of 1999.

Real Consumer Spending averaged a nearly 12% annual growth rate heading into 2000.

Real Wages were climbing steadily from 1991 to 1999 and hit a peak of almost 14% in 1999.

Real GDP was running at more than 4% annually in December of 1999.

NOTE: There was NO SIGN of RECESSION in late 1999.

Compare the chart above with the one below.

There is a vast difference between the strength of the economy today versus 1999; particularly we are already in a longer economic expansion than we were then.

Personal Incomes currently average about 2% versus 4% in 1995

Employment is averaging about a 1.5% annualized growth rate versus 2.5% in 1995.

Industrial Production has averaged about 2% annual growth vs 5% previously.

Real Consumer Spending has averaged about 4% annual growth versus 8-10% in 1995.

Real Wages have averaged about a 3.5 annual growth rate versus 8-10% in 1995.

Real GDP has averaged about 2% annual growth over the last decade versus 3% previously.

There is also one other significant difference.

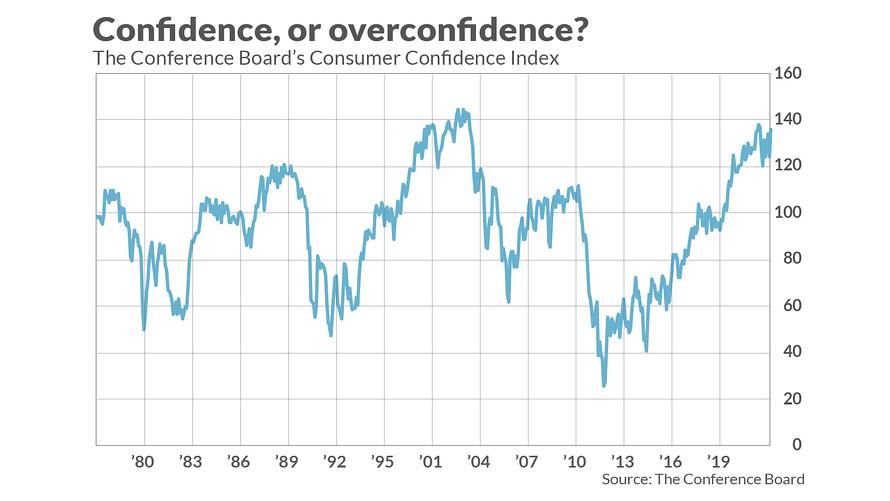

In 1995, Consumer Confidence was at about 100 on its way to 140.

Today, it is likely not possible to get more optimistic than consumers are currently.

It’s All Bullish

“We could get more volatility in the coming days, but as we settle into August you’ll see equities start to perk again. My assumption is that we could start to see a buy-the-dip mentality, created by the easy money move and the need to chase returns.” – Yousef Abbasi, INTL FCStone

“Low rates will continue to support a higher-than-average valuations for the S&P 500. At the same time that corporations are growing revenue at a healthy clip and appear set to avoid the earnings recession that many investors had been fearing this year.” – Brad McMillan, CommonWealth

Not surprisingly, since the Fed’s announcement, the financial media and Wall Street have been pushing the bullish narrative. Just as they did in 1999 and 2007, as there was “no recession in sight,” then either.

The problem is financial media, or Wall Street, is they never tell you when to sell.(They don’t make money when you are in cash.)

Currently, the risk to the market is elevated.

Confidence is at highs, not lows.

Economic growth is at a cycle peak

Earnings growth is beginning to weaken, and corporate profits are on the decline.

Valuations are elevated

Leverage is at records

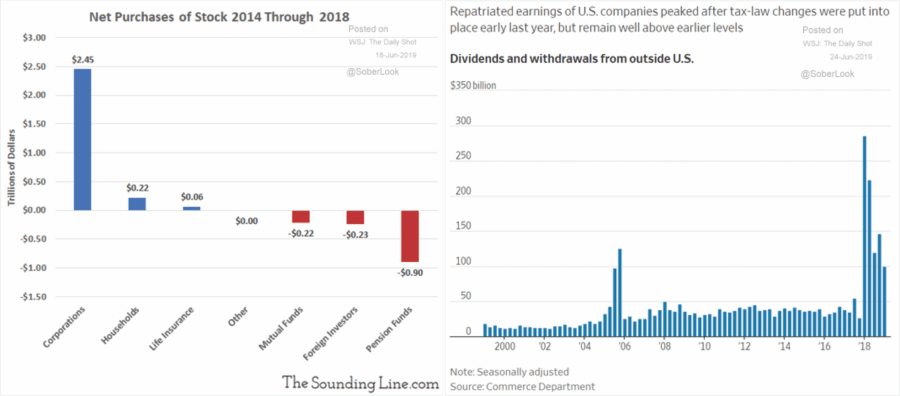

Stock buyback activity is slowing (As we noted previously, since 2014, buyback activity has accounted for nearly 100% of net equity purchases in the market and is now slowing).

While it is certainly possible for equities to push higher over the short-term, seemingly to confirm the “bullish calls,” don’t forget your time horizon is substantially longer than 6-12 months.

No one will ring a bell at the eventual top, the media won’t tell you to “sell,” and the mainstream financial advice will tell you that if your only option is to “buy and hold.”

If history is any guide, the next mean reverting event will likely wipe out of the bulk of the gains made over the last 5-7 years at a minimum.

If you are close to retirement, it should be clear that risk outweighs the reward currently.

Not everything the Fed does can be bullish.

via ZeroHedge News https://ift.tt/2T8SkN8 Tyler Durden

The situation in Hong Kong is rapidly deteriorating, with violence breaking out in seven locations Monday afternoon as the citywide strike continues.

White shirted ‘triad’ members beat protesters (via SCMP)

What were supposed to be peaceful sit-ins in different districts turned into riots, “with Wong Tai Sin and Harcourt Road seeing the most intense confrontations as protesters kneel instead of flee, to shield themselves while tear gas rounds and sponge grenades rain on them,” according to SCMP.

VIDEO: 🇭🇰 Hong Kong police launch rounds of tear gas and try to clear pro-democracy protesters who had gathered near a police dormitory in the working-class district of #WongTaiSin#HongKongProtestspic.twitter.com/GkuCBM0DCV

Protesters threw a suspected gasoline bomb at police after first being attacked by bricks.

20:00 A suspected gasoline bomb was thrown by protesters to the police who were resting on Tai Po Tai Wo road near the crossroad with Nam Wan Rd. The police were attacked suddenly first by bricks from the protesters and then the bomb. #antiELABpic.twitter.com/hyv8YLhKxH

Riot police used crowd control measures in at least five locations – targeting those filing the streets. 82 people were arrested for offences including rioting, unlawful assembly, assaulting a police officer, obstructing police and possession of offensive weapons.

Fighting broke out between protesters and local residents, while reports of ‘white shirted’ men believed to be triad gang members began beating protesters as the evening devolved.

Here’s the aftermath. Protesters chased the men with sticks up the hill and broke the windows of a residential building. To clarify, unclear if men with sticks are residents. Overheard some speaking in Cantonese and some speaking Mandarin. #HongKongpic.twitter.com/aN0bFZoaHH

In response to the unrest, Cathay Pacific airlines canceled over 150 flights and urged passengers to postpone non-essential travel according to CNN.

Cathay Pacific urged customers not to flyMonday and Tuesday, and said it would waive fees for rebooking. Shares in Cathay plunged more than 4% during trading Monday.

The airline is the city’s flagship carrier. It flies about34 million passengers every year and serves nearly 200 cities around the world from its hub at Hong Kong’s international airport.

Hong Kong Airlines, a smaller carrier, said it has canceled 32 flights. United Airlines said its flights were unaffected.

More than 2,300 aviation workers took part in the strike, including 1,200 Cathay cabin crew and pilots, according to the Hong Kong Confederation of Trade Unions.

Service was suspended for more than an hour Monday morning on the Airport Express, which is a line that zips people between the airport and the city center in under 25 minutes. –CNN

Carla Neems, a month shy of turning seven, was scootering home from school when she was hit by a garbage truck and killed.

A two-year inquest was held. Last week, the coroner, Tim Scott, finally issued his report. He blamed the parents, saying it was “unacceptable” that the girl was allowed to get home without them—because every heart-wrenching child tragedy, no matter how unpredictable or rare, must be deemed the fault of a bad mom or dad.

So here’s the story. It took place in New Zealand. Carla was coming home from school, which is about half a mile from her home. She had done this daily with her sisters, who are eight and ten, for a year. On May 2, 2017, she was with an older friend until the very last bit of the trip, which she made by herself. When she scootered in front of the truck, less than a block from her home, the driver didn’t see her. He has been acquitted of reckless driving.

The parents are not getting off that easy.

Coroner Scott declared, “I do not accept that it was acceptable for Carla to go to and from school in the care of her older siblings—and part of the way home alone. The siblings were too young to be vested with that responsibility. Sadly the confidence that Mr. and Mrs. Neems had about Carla’s road safety was misplaced and flies in the face of what happened.”

The problem is this: In the wake of any tragedy, it’s easy to say, “If only X hadn’t happened, we wouldn’t be mourning today.” That can make it feel as if “X” is so inherently and (in retrospect) inevitably dangerous that it should never be allowed. When the coroner says the parents’ trust in Carla “flies in the face of what happened,” he is saying they should have known this was going to happen.

This is a cruel twist of the knife. It is also wrong. If a child falls down the stairs and dies, does that “fly in the face” of parents who thought it was okay to raise kids in two-story houses? Would the coroner call them reckless? If a child slips in the tub, does that “fly in the face” of parents stupid enough to believe it was okay for their child to take a bath?

There is no such thing as a completely risk-free life. It is unfair and cruel to blame parents for trusting the odds—for not living every second as if an anvil was about to fall on their heads.

Maybe Scott could have found more compassionate words to comfort a grieving family; maybe he felt a need to draw a line in so much unnecessary death and shock people out of their complacency.

Who is complacent when it comes to the death of a child? In fact, we are so completely shaken by this development that we have to immediately turn it into a lesson so that we don’t have to stare into the abyss that is cruel fate. And that is exactly how the Stuff editorial proceeds: “Carla’s death is not meaningless; it has inspired an honest assessment of risk that will hopefully save many lives.”

In one sense—the design of garbage trucks—that may be true. Assessors came to realize the trucks have a blind spot and have since worked to eradicate it. They’ve also made the trucks even more visible. This is great news. But a coroner stating that children should not be allowed to venture outside on their own until age eight or nine, even when parents believe they should be allowed to do so, is alarming. It’s a hallmark of paranoia, not prudence.

At Let Grow, we believe in teaching kids to take care on the streets, to stop, look, and listen, and to check both ways. We also love reflectors, and lights and bells on bikes. But when it comes to blame, we believe in mourning with the Neems, rather than cruelly pretending this was their fault.

from Latest – Reason.com https://ift.tt/2yEHRiZ

via IFTTT

Earlier this year, following the Christ Church mosque attack, New Zealand briefly totally blocked access to several websites.

Yesterday, two men allegedly killed 30 people at a store in Dayton Ohio, and a mall in El Paso Texas.

Today 8chan has been totally shut down.

If you don’t know what 8chan is, well it’s like 4chan but without the sense of decency. If you don’t know what 4chan is, it’s like reddit went off its medication.

Both places could be, can be, kinda gross. But they could – can – also be amazing. Insightful. Useful. Free speech is like that. Sometimes beautiful, sometimes ugly. If you cut off the ugly parts it’s not “free speech” anymore. This is something we all know, but the media is trying to force us to forget.

Hell, going by this absurd definition of “death count” – meaning, apparently, “someone who allegedly posted there, allegedly committed a crime” – then all Facebook and twitter have staggering “death counts”.

Known war criminals use twitter every single day.

The alleged Christ Church shooting was live-streamed on Facebook (but it was 8chan that got blocked).

The Guardian itself published an opinion piece, a week ago, written by Alastair Campbell. A man with a body count 50,000x higher than the Texas shooting. That’s an El Paso every day for 137 years.

This isn’t about hate, they’re fine with hate. This isn’t about blood, they love blood.

8chan was no more hateful or bloody than any website on that list, so what was the real problem with it?

It was anonymous, fringe and uncontrollable.

It was free. Now it’s not. Any one of us could be next.

via ZeroHedge News https://ift.tt/2YGxOVj Tyler Durden

Last Friday, when describing the period which he called “the most manic 36 hours of trading in my 18 year career“, Nomura’s Charlie McElligott hit the nail on the head as to the two main reasons why risk assets are tumbling today alongside the dramatic spike in the VIX:

Dealers were clearly “Short Gamma” in Index / ETF at the start of the month, and

Dealers are clearly “Short Vol” in-bulk, thanks to the “50 Cent” VIX upside flows which have been trading in SIZE over the past few weeks.

In addition to dealers being off side, McElligott cautioned that systematic VIX Roll-down players in recent weeks had also reapplied significant size to the “Short Vol” trade, as per VIX futures positioning—thus, with the curve again “inverted,” they will be forced / unemotional hedging of these front-end shorts in UX1 and UX2 (none of this is surprising to those who read our piece from last weekend which found that, contrary to conventional wisdom, stocks were actually massively overbought across the board, according to JPMorgan data).

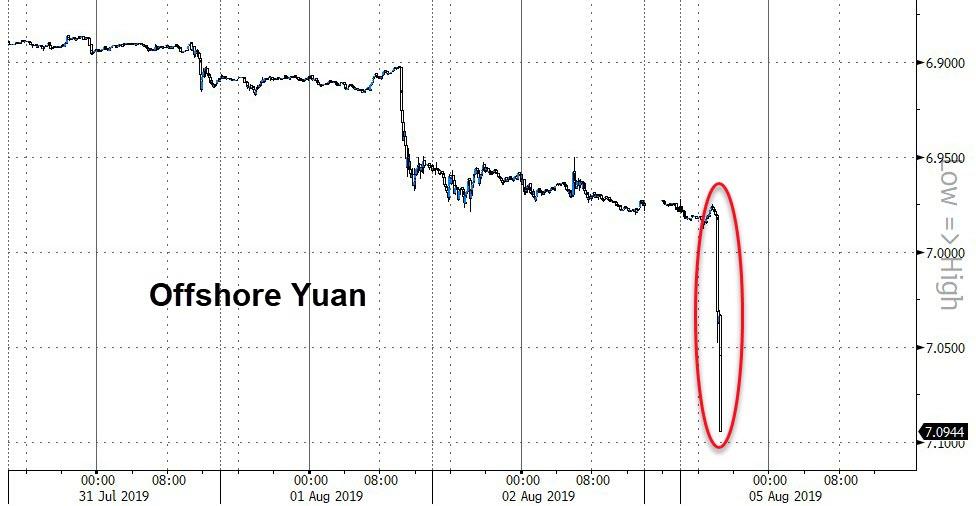

So fast forward to today, when after a hectic weekend, Charlie can soon tack on another 24 hours to “the most manic period”, because as he writes in his blitz post-mortem this morning, risk and safe haven assets are undergoing “extreme moves”, following the Chinese retaliation “double-whammy”, which initially spooked markets on the Sunday reopen, as reports stated that 1) Beijing had asked state-owned firms to suspend US crop purchases and 2) allowed the Yuan to plunge to the weakest level in more than a decade (offshore currently at 7.084)—both direct spites to the US administration, as the agricultural purchases and currency management were top priorities for the White House

While there has been debate whether the PBOC engineered or merely encouraged the overnight devaluation, semantics aside, the Nomura quant notes that the Yuan freefall has reinvigorated the “worst fears” of outright currency warfare across global CBs in “beggar thy neighbor” fashion (Japanese MoF official Takeuchi said he is watching FX markets “with a sense of urgency,” while S.Korean FX authority called the USDKRW moves “excessive, abnormal”), with the Yuan in-and-of-itself capable of triggering a global disinflationary impulse (Iron Ore in Singapore tumbled -7.0% overnight).

Looking ahead, McElligott expects the PBoC to use fixings, capital controls and potentially FX swaps with local banks (deter USD buying) in order to manage the Yuan and prevent full-fledged capital outflows / market breakdown, while at the same time try to minimize the depletion of FX reserves (as opposed to ’15 – ’16), although judging by the surge in cryptos this morning, Beijing’s bitcoin firewall has some very serious holes in it.

Further, as the Nomura quant points out, MNI has a PBoC “advisor sources” piece out stating that that the central bank may allow Yuan to weaken further if the US continues to play tough in trade negotiations; However, depreciation should be limited for now as authorities would step in to to limit heavy selling should it pose a threat to financial markets or trigger capital outflow.

There was a modest improvement in risk sentiment around at 530am ET, following headline reports from Chinese state TV that:

CHINA SAYS U.S. ACCUSATION ON NO FARM GOODS PURCHASE UNTRUE: TV

CHINA STATE PLANNER SAYS 2 MLN TONNES OF U.S. SOYBEANS DESTINED FOR CHINA WILL BE LOADED IN AUGUST – STATE MEDIA

And while Bloomberg since clarified that it was private purchasers who stopped buying US soybeans over uncertainty in the China – US trade relationship, the “risk-off” wave has returned, oblivious of any attempt to mitigate the selloff as all eyes are now solely on the USDCNH which continues to rise, and was last trading at 7.08, leaving the PBOC with little ammo to fix the USDCNY below 7.00 on Tuesday.

As a result, the “risk-off” was extreme and as Nomura notes, has largely held:

10Y UST nominal yields plunged to near 3-year lows;

Red Eurodollars exploded higher once-again as the cross-asset hedge of choice (Z0 +17bps at the highs of the session, largest cumulative 3d upside move since 11/01/11 @ +3.5SD);

Receiving across the board in Swaps via Banks- and Gamma Hedgers- as we broke-out to new multi-year levels;

Yen and Swiss Franc power ‘bid’ as the best performing G10 FX;

And as US Real Yields collapsed and the Yuan cratered, we saw Gold- and Crypto- rip higher overnight—as there is no central bank on the other side to devalue

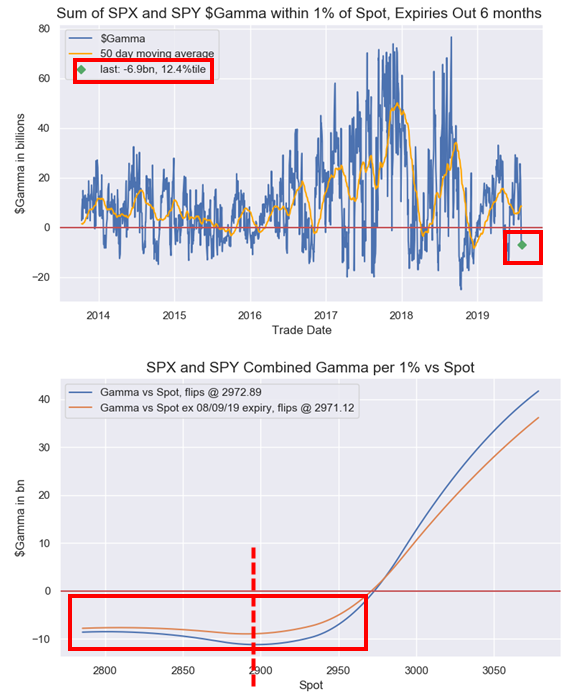

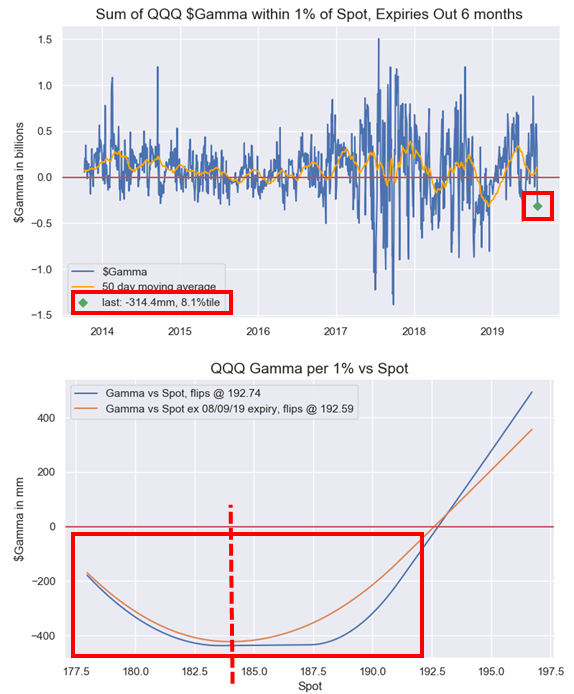

And here comes the bad news for the dip buyers who are hopeful that the ES slide below 2,900 will form a floor to risk: as McElligott cautions, from the key risk-sentiment bellwether that is US Equities, not only did Dealer options positions in S&P- and Nasdaq- both shift “Short Gamma” by midweek (each now EXTREME with Negative $Gamma percentile rank for SPX @ just 12th %ile and QQQ @ 8th %ile), but the feedback loop on the gap lower has now triggered CTA Trend model deleveraging in each as well.

In short, that massively overbought position that we – and BofA over the weekend – warned about, is now being massively sold, which in turn is causing even more selling in a feedback loop as margined positions are force-stopped out, or as those deeply versed in trading vernacular call it, we are having a breakout of “negative gamma”:

The CTA model’s S&P position below 2946 (spot currently WELL-through at 2900) sees a signal cut from +100% to +66%, triggering deleveraging; the next “sell” level is at 2830, where the model would flip “Short” at a -59% position, and “Max Short” under 2714

The Nasdaq position already reduced on Friday below 7732 to see the signal decline from +100% to +66%; the next “sell” level is7375 where we would flip to outright “Short”

Russell is already -59.4% Short, more selling under 1515 to get to get to “Max Short”

Internationally, HSI CH and Nikkei are both back “Short” already, while Eurostoxx will deleverage & “flip Short” under 3308

And visually, this is what the extreme negative gamma that McElligott has been warning about looks like:

No wonder that Charlie picked the following title for his note today: “Never get caught “short gamma” in August.”

via ZeroHedge News https://ift.tt/2Yo780d Tyler Durden

President Trump has escalated his rhetoric against China’s interventionsit lack-of-intervention, blasting “China dropped the price of their currency to an almost a historic low. It’s called ‘currency manipulation’…”

Then Trump added – clearly pushing Powell to do more: “Are you listening Federal Reserve? This is a major violation which will greatly weaken China over time!”

China dropped the price of their currency to an almost a historic low. It’s called “currency manipulation.” Are you listening Federal Reserve? This is a major violation which will greatly weaken China over time!

Recently, some new situations have emerged in the international economic situation and trade frictions, and market expectations have also undergone some changes. Affected by this, many currencies have depreciated against the US dollar since August, and the RMB exchange rate has also been affected to some extent. This fluctuation is driven and determined by the market.

As a responsible big country, China will abide by the spirit of the G20 leaders’ summit on the exchange rate issue, adhere to the market-determined exchange rate system, not engage in competitive devaluation, and not use the exchange rate for competitive purposes. Use the exchange rate as a tool to deal with external disturbances such as trade disputes. All along, the People’s Bank of China is committed to maintaining a stable and balanced RMB exchange rate at a reasonable and balanced level. This effort is believed to be obvious to all.

At present, China’s economy is stable and progressing, and its economic growth ranks among the top in the major economies, showing great resilience, potential and room for maneuver. The balance of international payments is balanced, foreign exchange reserves are sufficient, and there are more and more hedge enterprises in the foreign exchange market. The spread between China and major developed economies is in a suitable range and can support the basic stability of the RMB exchange rate.

The People’s Bank of China and the State Administration of Foreign Exchange will maintain the stability and continuity of foreign exchange management policies and guarantee the legitimate and legitimate use of foreign exchange by market players such as enterprises and individuals. We will deepen reform and opening up in the foreign exchange sector, further enhance the level of liberalization and facilitation of cross-border trade and investment, and serve the development of the real economy and the new pattern of comprehensive national opening up.

Whether it is from the fundamentals of the Chinese economy or from the balance of market supply and demand, the current RMB exchange rate is at an appropriate level. Although the RMB exchange rate has fluctuated due to recent external uncertainties, I am confident that the RMB will continue to be a strong currency. The People’s Bank of China has full experience and ability to maintain the smooth operation of the foreign exchange market and keep the RMB exchange rate basically stable at a reasonable and balanced level.

When China devalues the yuan (or allows the market to devalue the yuan), it exports deflation to the rest of the world which is the ominous threat that central banks have been so vigorously attempting to fight.

Pretty clear to everyone – currency wars begun they have – as this feedback loop pressures Powell and The Fed to cut rates further to weaken the dollar.

via ZeroHedge News https://ift.tt/2ZyBr0F Tyler Durden

Following this weekend’s series of mass shootings that left roughly 30 people dead, President Trump on Monday suggested passing new gun control legislation, which could be tied to immigration reform, in a reversal from his previous stance on gun control.

“Republicans and Democrats must come together and get strong background checks, perhaps marrying this legislation with desperately needed immigration reform” Trump tweeted

We cannot let those killed in El Paso, Texas, and Dayton, Ohio, die in vain. Likewise for those so seriously wounded. We can never forget them, and those many who came before them. Republicans and Democrats must come together and get strong background checks, perhaps marrying….

In a third tweet, Trump seemed to blame the “Fake News” media for the “anger and rage” that has led to these mass shootings.

The Media has a big responsibility to life and safety in our Country. Fake News has contributed greatly to the anger and rage that has built up over many years. News coverage has got to start being fair, balanced and unbiased, or these terrible problems will only get worse!

On Saturday, a gunman killed 20 people and wounded dozens more during an attack at a Walmart in El Paso. Less than a day later, another gunman killed at least nine people and wounded another two dozen in a Dayton, Ohio shooting. The shootings aren’t believed to be linked. And while the first gunman was quickly exposed as a right-wing extremist, the second has been revealed to be a leftist supporter of Bernie Sanders and Elizabeth Warren. The disturbed young man also revealed in his social media profiles that he was a satanist and a member of the Democratic Socialists of America.

Democrats are renewing their calls for the Senate to take up the universal background check bill that the House passed earlier this year, and by the looks of it, President Trump appears to now support that measure.

via ZeroHedge News https://ift.tt/2yGcSmS Tyler Durden

Democratic socialists earned some ridicule this weekend after video clips from their annual convention—which showed attendees objecting to clapping, disruptive chatter, and the use of gendered language on grounds that all of these things were triggering—appeared online.

One person took to the podium to thank his fellow comrades for waving their hands in the air instead of clapping, since sudden, loud noises can be harmful for the easily perturbed members of the audience.

“We have a lot of disabled comrades,” he said. He reminded everyone to “avoid hissing, avoid waving banners, there’s all sorts of things.”

It’s difficult, of course, to impose total silence on a political action conference. At one point, a convention delegate interrupted another person’s speech about “defeating capitalism” to make a “quick point of personal privilege.” This delegate began by reminding the audience that he uses “he/him” pronouns, and then implored: “Guys… please keep the chatter to a minimum,” because he is “very prone to sensory overload.” Immediately after this plea, another attendee shot back with their own point of personal privilege: “Please do not use gendered language to address everyone.” This person objected to the previous speaker’s use of the word “guys.”

It is not at all uncommon to see the DSA sidetracked by infighting over unreasonable requests related to language and disability status. In my book about modern activism—Panic Attack: Young Radicals in the Age of Trump—I describe how the DSA’s Medicare-for-All campaign was criticized by the DSA’s disability caucus, whose members claimed that they should have ultimate authority over issues pertaining to health and wellness. It is widely believed within progressive circles that the oppressed are the sole experts on their own oppression and that deference should be given to the most marginalized groups. In practice, this creates some weird standoffs. From my book:

Since disabled people are especially affected by health care policy, the Medicare for All group had essentially failed to let disabled people be the experts on their own oppression—an intersectionality no-no.

Amber A’Lee Frost, a Medicare for All proponent and prominent DSA member known for co-hosting the left-wing Chapo Trap House podcast, hit back, accusing her critics of trying to sabotage the movement with their “pathological anti-social behavior.” This made matters much worse: The comment was perceived as an attack on the autistic community.

Frost had committed ableism. Several dozen DSA members signed a petition demanding that she “immediately remove herself from any involvement, official or unofficial, with DSA’s Medicare for All campaign, and should she not, that she be removed.” This was necessary, because intersectionality means casting suspicion on organizing efforts if these efforts do not make the marginalized the center of attention.

No one should come away from the coverage of the DSA convention with the idea that attendees did nothing but call-out each other’s pronouns, though. Listening to the livestream I heard heated discussions about significant policy issues: criminal justice reform, supporting the presidential campaign of Sen. Bernie Sanders (I–Vt.), and combating “Lex Luthor–esque scumbag Jeff Bezos.” Of all the various factions of progressive activism, the DSA is by far the most organized, and the least likely to be derailed by culturally woke signaling.

from Latest – Reason.com https://ift.tt/2KqDQnZ

via IFTTT

U.S. equity futures slumped, European stocks tumbled and Asian markets were in freefall on Monday, after China finally struck back in its trade dispute with America, letting its currency plunge below the key psychological level of 7 vs the USD.

This unexpected escalation by Beijing, which sent the Yuan to a level last seen in 2008, spooked a selling panic across global risk assets, sending the S&P below 2,900, and world markets in a sea of red…

… as Treasuries, gold – and yes, cryptos – led a global bond rally as investors dashed to safer assets.

“Markets had not been expecting the latest US-China trade talks to conclude with any significant breakthrough last week, but very few expected President Trump to slap 10% tariffs on $300 billion worth of Chinese goods,” said Hussein Sayed, chief market strategist at FXTM.

In addition to the yuan devaluation, Bloomberg reported that China asked state buyers to halt their US agriculture imports. China’s US Ambassador said on Friday that if the US wants to talk about trade, then so will China, and if the US want to fight, so will China, while he added that new tariffs are an irrational and irresponsible act which Beijing will take new adequate countermeasures against. The Ambassador also commented on Hong Kong protests which he said are turning out to be violent as well as chaotic and should no longer be allowed to continue.

MSCI’s All Country World Index was down 0.7% on the day. That put it down almost 2% including Friday’s loss.

European stocks tumbled to a two-month low, suffering the biggest two-day sell-off in more than three years. The Stoxx Europe 600 Index fell as much as 2.1%, bringing the combined loss with Friday to the worst since June 2016 according to Bloomberg. An index tracking European basic resources stocks slumped as much as 3.8%, erasing its gains for the year, as iron ore and copper prices take a hit amid increasing U.S.-China trade tensions. The STOXX Europe 600 Basic Resources declines as much as 3.8%, before trimming loss to 2.9% at 8:30am in London, the region’s worst-performing sector on Monday.

Ahead of Monday’s plunge, European equities had already fallen 2.5% on Friday, the most since December, after the White House dangled the prospect of new tariffs over Chinese goods. Tensions escalated further today after China responded by letting the yuan tumble and asking state-owned companies to suspend imports of U.S. agricultural products.

Earlier in the session, Asian shares suffered their steepest daily drop in 10 months, with MSCI’s broadest index of Asia-Pacific shares outside Japan sinking 2.5% to depths not seen since late January. Japan’s Topix tumbled 1.8% to lowest close since Jan. 4 as the yen surged. Hong Kong’s Hang Seng Index lost 2.9% after protesters moved to shut down the city with a general strike. The Philippines’ benchmark was the region’s worst performer, dropping 3%. Investors moved to risk-off mode as the U.S.-China trade war escalated after U.S. president Donald Trump ratcheted up rhetoric by saying that he could boost levies on China to a “much higher number.” To counter the threat, China asked state-owned enterprises to suspend imports of U.S. agricultural products. South Korea’s Kospi Index declined 2.6% as the won weakened below 1,200 to the greenback for the first time since Jan. 2017.

And with S&P futures were down 1.4%, sliding below 2,900, the VIX index rose to 21.2%, its highest since May 9, while Europe’s equivalent hit its highest since early January.

“We reiterate our view to scale back equity positions to strategic allocations after strong gains year to date, amid the ongoing trade-related uncertainties,” Credit Suisse analysts wrote in a note to clients.

Meanwhile, China’s headaches persisted elsewhere, as protests continued in Hong Kong in which police fired tear gas into protesters, while Hong Kong authorities expect flight cancellations and other transport disruptions as 500k protesters plan a city-wide strike. Hong Kong Chief Executive Lam said protests have brought Hong Kong to the edge and protesters are pushing it to an extremely dangerous situation, while she added she will remain in her job to try and restore order.

The good news: Hong Kong Police said there is no chance of deploying People’s Liberation Army (PLA) officers in protests… at least for now. Most recently, reports that Beijing are to announce ‘something new’ regarding Hong Kong on Tuesday, an official has stated that Beijing’s position is largely unchanged., SCMP citing a source

Looking at the carnage in currencies, the biggest mover was of course the yuan, which fell past the key level of 7 to the dollar as Chinese authorities – expected to defend the currency at that level – allowed it to break through to its lowest in the onshore market since the 2008 global financial crisis. The offshore yuan fell to its weakest since international trading of the Chinese currency began. Headed for its biggest one-day drop in four years, it was last down 1.4% at 7.0744 in offshore markets.

“Over the past couple of years, China has kept the renminbi stable against the basket, but with the renminbi TWI (trade-weighted index) now testing the lower end of the range in play since 2017, investors may turn nervous, introducing another dose of volatility,” Morgan Stanley strategists wrote in a note to clients.

The currencies of other Asian economies closely linked with China’s growth prospects also dropped: a gauge of emerging-market currencies headed for its biggest drop in about a year. South Korea’s won tumbled 1.4$, its biggest one-day loss since August 2016, while India’s rupee and Mexico’s peso felt the brunt of the pain.

Developing-nation stocks fell for a ninth day, the longest streak of losses since December 2015. “There is probably more pain to come for EM currencies” given the unwinding of carry trades, reduction in growth exposure through equities and build-up in speculative wagers, Jason Daw, the Singapore-based head of emerging-markets strategy at Societe Generale SA, wrote in a report. “The strong policy signal by China has put the renminbi back in the driver’s seat; it will be a leader in the global currency cycle for the foreseeable future.” Sterling hovered near 2017 lows at $1.2117, pressured by concerns about Britain exiting the EU without a trade deal in place.

On the other side, the Japaness yen saw its traditional safe haven bid, rising 0.7% to its highest since a January flash crash. The Swiss franc was also boosted by safe-haven demand, despite intervention by the SNB seeking to keep appreciation minimal. Trump is also eyeing tariffs on the European Union, but has yet to make a formal announcement. The euro was 0.3% higher to the dollar at $1.1137.

Meanwhile, the stock of negative yielding debt hit new record highs as Dutch 30-year government bond yields turned negative for the first time as euro zone yields sank further amid concerns about U.S.-China trade and a no-deal Brexit. U.S. 10-year Treasury yields dived 7 basis points to 1.77%, while Germany’s 10-year bund yields fell to -0.53%. The three-month to 10-year U.S. yield curve was at its most inverted in 11 years.

In geopolitical news, Iran seized an Iraq oil tanker that was allegedly smuggling fuel in the Gulf, although the Iraq Oil Minister denied any links to the tanker. Turkey plans to carry out an operation east of the Euphrates in Syria, while US and Russia have been notified.

Finally, oil extended losses with U.S crude down 1.55% at $54.8 and Brent down 1.55% at $60.92. Gold prices jumped more than 1% to their highest in more than six years, with spot gold prices up 1.1% to $1,456.51 per ounce.

US President Trump is to address the nation on Monday (10:00 ET) and suggested that more gun control may be needed following a mass shooting incident in El Paso, Texas in which 20 were killed, while there was also a mass shooting in Dayton, Ohio. Other expected data include PMIs. Linde and Marriott International are among companies reporting earnings.

Market Snapshot

S&P 500 futures down 1.3% to 2,894.00

STOXX Europe 600 down 2% to 370.54

MXAP down 2% to 152.42

MXAPJ down 2.5% to 491.47

Nikkei down 1.7% to 20,720.29

Topix down 1.8% to 1,505.88

Hang Seng Index down 2.9% to 26,151.32

Shanghai Composite down 1.6% to 2,821.50

Sensex down 1.4% to 36,616.90

Australia S&P/ASX 200 down 1.9% to 6,640.30

Kospi down 2.6% to 1,946.98

German 10Y yield fell 2.2 bps to -0.517%

Euro up 0.3% to $1.1140

Italian 10Y yield fell 3.9 bps to 1.19%

Spanish 10Y yield fell 2.2 bps to 0.224%

Brent futures down 1.3% to $61.11/bbl

Gold spot up 1.2% to $1,457.46

U.S. Dollar Index down 0.2% to 97.87

Top Headline News from Bloomberg

China responded to Trump’s tariff threat with another escalation of the trade war on Monday, letting the yuan tumble to the weakest level in more than a decade and asking state-owned companies to suspend imports of U.S. agricultural products. Trump criticized Beijing for managing its currency unfairly and failing to keep promises to buy more U.S. crops

The yuan plunged beyond 7 per dollar for the first time since 2008 amid speculation Beijing was allowing currency depreciation to counter Trump’s latest tariff threat. PBOC says it’s able to keep yuan stable at a reasonable and balanced level

Hong Kong leader Carrie Lam warned of a “very dangerous situation” as protesters moved to shut down the Asian financial hub with a general strike on Monday after a ninth straight weekend of unrest in opposition to China’s tightening grip

HSBC Holdings Plc confirmed its plans to eliminate jobs, axing more than 4,000 posts and warning that senior executives will be a focus of the cutbacks. “We expect this year to have $650 million to $700 million of severance costs; that involves less than 2% of our workforce,” CFO Ewen Stevenson said in a call with analysts

Boris Johnson has dramatically boosted public spending since taking office, fueling speculation the U.K. prime minister is preparing not only for Brexit by Oct. 31, but a general election as well. The two are likely to be linked

India has revoked the special constitutional status of Kashmir in a move that’s drawn protests in parliament and risks deepening the deteriorating security relationship with rival Pakistan in the disputed region

Turkish banks approached the Treasury about swapping some of its local-currency bonds maturing early next year with longer-dated debt as the two sides discuss ways to soften the blow of a looming financing hump, according to four people with knowledge of the matter

Spanish King Felipe VI said it’s best for the nation to resolve the current political deadlock before holding new elections, newspaper El Pais reported Sunday

Iron ore has gone from high-flier to sinking star in a matter of weeks. Copper drops to two-year low as the latest U.S. tariffs on China fueled a global market sell-off

Asian equity markets were lower across the board as the stock rout resumed from last week’s tariff announcement by US President Trump and with retaliation from China in which it asked state-run purchasers to halt US agriculture imports, while a collapse in the CNH through the 7.00 handle also exacerbated the risk averse tone. ASX 200 (-1.7%) weakened with the trade sensitive sectors such as tech and materials front-running the declines, although gold names bucked the trend on the precious metal’s safe-haven status, while Nikkei 225 (-1.7%) was pressured by a firmer currency and several disappointing earnings including Kobe Steel and Yahoo Japan. Hang Seng (-2.8%) and Shanghai Comp. (-1.6%) also slipped amid the escalation of trade tensions with underperformance in Hong Kong as protests continued and with a 500k-strong city-wide strike said to be planned which disrupted public transport and saw more than 130 flights cancelled, while the latest Hong Kong PMI data printed at a decade low due to the impact from the ongoing disorder and trade dispute. Furthermore, a miss in Chinese Caixin Services PMI added to the glum, with the selling exacerbated after the PBoC weakened the reference rate which pressured CNH to a record low against the greenback past the 7.0000 level seen by some to be a sticking-point for China and in turn, raised concerns of China weaponizing its currency. Finally, 10yr JGBs were underpinned as the widespread risk averse tone spurred safe-haven buying which saw 10yr JGB futures post a record high and the 10yr yield drop to its lowest in 3 years at around -0.2%, while T-notes also found support overnight and the BoJ were present in the market today under its massive bond buying program.

Top Asian News

India Seeks to Revoke Special Autonomy to State of Kashmir

China’s Bond Market Leverage Ratio Falls on Lower Liquidity

Macau’s Gaming Regulator Clamps Down on Use of AI in Casinos

Philippines Central Bank Chief Sees 50bps Rate Cuts Rest of Year

Major European bourses have begun the week firmly in negative territory [Euro Stoxx 50 -1.4%] following on from a downbeat Asia-Pac handover after market sentiment took a hit from dwindling trade hopes as China asked state-run purchasers to halt US farm goods imports. Additionally, the collapse of the CNH to 7.0+ status vs. the USD also added further jitters to the trade-sensitive sentiment. Indices are firmly in the red but have crawled off lows in recent trade after China State Planner dismissed President Trump’s accusation that China has not bought US farm goods, adding that US and China agreed to China will purchase 14mln tonnes of soybeans from the US, with 2mln to be loaded in August. Sectors are in the red across the board with some mild resilience in defensive sectors. To the downside, miners fare the worst amid the freefall in base metal prices due to a bleaker demand outlook in the sector as protectionism ramps up. Thus, ArcelorMittal (-4.5%), Antofagasta (-3.3%), Rio Tinto (-2.4%), and Anglo American (-3.5%) have all fallen to the foot of their respective bourses. However, Fresnillo (+4.0%) bucks the miners’ trend as the Co. benefits from the safe-haven surge in gold prices. European luxury names and the auto sectors are also bearing the brunt of the US-China trade spat with LVMH (-2.9%), Kering (-2.1%), Volkswagen (-2.7%), Daimler (-2.5%), BMW (-2.4%) and Peugeot (-3.1%) all lower as a result. In terms of individual movers HSBC (-1.0%) shares opened lower due to the surprise stepping-down of CEO Flint, despite improvements in its metrics and the announcement of a share buyback program.

Top European News

U.S. Imposes More Sanctions on Russia for Chemical Agent Use; Russia’s Ruble Bucks EM Rout With Sanctions More Bark Than Bite

U.K. 10-Year Bond Yield Slides to Record Low on Haven Buying

Ascom Slumps to Six-Year Low as CEO Quits, 1H Hit by Poor Demand

Euro-Area Growth Momentum Slides as Industry Pain Overwhelms

In FX, the Aussie has been hit particularly hard by the Yuan’s slide through 7.0000 vs the Greenback on and offshore after the PBoC raised its official mid-point fix to 6.9225 overnight from 6.8996 last Friday. However, the sharp Cny and Cnh depreciation was sparked by reports that China has halted US agricultural produce purchases in retaliation to President Trump’s fresh tariff threat, with a softer than expected Caixin services PMI not helping as the composite PMI hit a 5 month low and Hong Kong’s headline print plunged to 42.8. All this undermining broad risk sentiment and base metals like iron or, with Aud/Usd dipping under 0.6750 at worst in the run up to the RBA policy meeting overnight with options pricing in a 50 pip break even that could expose the early January 0.6715 flash crash low if the Bank firmly flags more easing after a widely anticipated pause this time round – see the headline feed and/or Research Suite for a full preview.

NZD/CAD/GBP – Also victims of heightened risk aversion amidst rising US-China trade tensions, with the Kiwi down though 0.6500 at one stage vs its US peer, but holding up a bit better than the Aussie ahead of Wednesday’s RBNZ rate decision that is unanimously forecast to result in the OCR being cut by a further 25 bp to 1.25%, mainly due to supportive cross-winds as Aud/Nzd reverses through 1.0400 again. Meanwhile, the Loonie is back below 1.3200 against the backdrop of retreating crude prices and with trading volumes impaired by Canada’s Civic holiday, but the Pound has gleaned some support from another UK PMI beat and by a greater margin in services compared to manufacturing and construction. Indeed, Cable has bounced from close to 1.2100 and Eur/Gbp stopped just shy of 0.9200, though remains elevated on persistent no deal Brexit concerns.

CHF/JPY/EUR – In stark contrast to the above, and to the overall detriment of the US Dollar (DXY losing more post-NFP momentum and sub-98.000) the Franc, Yen and Euro are all outperforming on safe-haven grounds, with Usd/Jpy probing through 106.00 and beneath a key Fib (106.06) that could be crucial on a closing basis. Usd/Chf is under 0.9750 and Eur/Usd has rebounded firmly to 1.1150 from 1.1105 even though Eur/Chf has fallen further below 1.0900 towards 1.0850 amidst mixed Eurozone services PMIs and a bleak Sentix survey.

EM – Regional currencies are generally weaker vs the Buck on the aforementioned risk-off environment, but once again the Try is holding up better than rivals within a 5.5490-6175 range as the Lira responds favourably to Turkish inflation data that was not as strong as expected, plus the CBRT’s RRR moves that will culminate in a net Usd2.1 bn liquidity drain.

CBRT says RRR for FX deposits/participation fund have been increased by 100bps for all maturity brackets, remuneration rate for USD-denominated RR,Reserve options and Free Reserves held at the CBRT had been decreased by 100bps. (Newswires)

In commodities,WTI and Brent futures are on the backfoot due to the prospect of lower global demand amid the seemingly widening gap between US and China in trade, in turn souring sentiment. WTI now straddles north of the USD 55/bbl mark while its Brent counterpart has just reclaimed USD 61/bbl after finding a base below the round figure. Looking ahead, tomorrow sees the release of the EIA Short-Term Energy Outlook, followed by the IEA Monthly Oil Report on Friday. Elsewhere, metals markets were rattled by the latest developments in the US-China saga with spot gold jumping over 1% to a peak of 1459/oz, the highest level in six years. Meanwhile, copper prices slumped to a 2-year low, but have since crawled off lows, with the red metal increasingly threatening USD 2.5/lb to the downside. Finally, Dalian Iron ore futures hit limit down after crumbling over 6% after declining below USD 100/tonne amid demand woes from the aforementioned US-China fallout, which was exacerbated by rising stockpiles of the raw material.

US Event Calendar

9:45am: Markit US Services PMI, est. 52.2, prior 52.2; Markit US Composite PMI, prior 51.6

10am: ISM Non-Manufacturing Index, est. 55.5, prior 55.1

1:30pm: Fed’s Brainard Speaks on the Payment System

DB’s Jim Reid concludes the overnight wrap

Friday was very nearly the last Early Morning Reid ever. I finished up writing it early as usual, got on my bike to the station and on route got hit by a car and was flung in the air and off my bike. The guy didn’t stop at a roundabout and took me out while I was nearly exiting it. What saved me was that I was so far round the roundabout that he bashed me at an angle and into the curb and didn’t run over me. I’ve got a lot of scrapes, a sprained ankle and a heavily bruised coccyx (I hope only) from my landing. Oh and a ripped pair of GAP chinos. A van behind had a dashcam so the footage is available so you can all see for yourselves how lucky I was and judge the quality of the car driving!! I’ve put the link to the clip on my Bloomberg header or let me know and I’ll send it to you.

So I feel fortunate to see this coming week in markets. Hopefully the zen feeling of just being glad to be here carries on for a while yet! After last week’s high-octane news flow, you would naturally think things will calm down from here but markets will struggle to relax given all that’s going on. Indeed the breaking news this morning that the onshore and offshore Chinese Yuan have broken through the key level of 7.0 has caused a mini shockwave through markets already in Asia and goes to show that last week’s fallout will very much continue to dictate markets in the near term. August can be quite a difficult month as negative news flow can also be exaggerated by a lack of liquidity. So be warned. Our asset allocation team led by Binky Chadha have been raising red flags of late suggesting that the S&P 500 is still well above the 2700 or so level implied by current growth indicators. The US 10y yield is pretty much in line ( link ). However as they point out, leading indicators of growth continue to point to further slowing to come, even before taking the impact of the latest escalation into account. In their view, a resolution of the trade war, and not Fed easing, is the key for a turn-up in growth. See their latest from Friday night here ( link ). There’s also an interesting piece on how systematic strategies have been the key marginal drivers of the US market, and how their equity allocations are currently very elevated.

Back to Asia where as mentioned all the focus this morning is on the moves in the FX market. Both the onshore CNY and offshore CNH have weakened to 7.0274 and 7.0772 respectively as we go to print, moves of -1.25% and -1.45%. The PBoC have said that the moves are due to tariff expectations and protectionism and that the central bank will fight against short-term speculation on the Chinese currency and stabilize market expectations. There’s been plenty of debate as to whether China would let the currency weaken past 7.0 so this is a very significant move especially as authorities had explicitly capped a move past 7.0 following the May 5th breakdown in talks. The question for the market now is what will be the response of the US administration and will they argue for currency manipulation in offsetting the impact of the tariffs.

The significance of the moves are certainly not to be underestimated and we’re already seeing a fallout at a broader asset level in markets. The biggest falls in equity markets have been for the Hang Seng (-2.89%) and Nikkei (-2.28%) while the CSI 300 and Shanghai Comp are down -1.03% and -0.81% respectively. The Kospi is also down -2.10% and ASX -1.64% while futures on the S&P 500 and NASDAQ have dropped -1.23% and -1.58% respectively. In rates, 10y JGBs immediately dropped -2.0bps to -0.197% while Treasuries have rallied a fairly incredible -7.2bps to 1.773%. Rarely have we seen such a big move in Treasuries on a Monday morning. The short end hasn’t quite rallied as much meaning the 2s10s curve is 2.7bps flatter at 13.4bps. The market is also now pricing in 59bps of cuts by the Fed by the end of this year. Meanwhile Gold is up +0.82% while the likes of WTI oil is down -1.22%. In the rest of FX the Yen (+0.55%) and Swiss Franc (+0.38%) are the notable perceived safe-haven outperformers while the likes of the South Korea Won (-1.33%) and Mexican Peso (-0.87%) have dropped. Indeed South Korea have called the move in the Won “excessive” and “abnormal” while Japan have stated that they are watching moves in the FX market “with urgency”.

It’s worth noting that this morning China also asked state-owned companies to suspend imports of US agricultural products which is clearly adding to the negative circle of newsflow while China’s Caixin services PMI was reported as dropping 0.4pts in July to 51.6 and below expectations for 52.0.

So, no time to recover from last week and already plenty to consider and in terms of events outside of the trade war this week we’ve also got US/European earnings season continuing, albeit at a reduced pace, while data highlights include the important global services PMIs (today), German factory orders (tomorrow – after the steepest fall since Sept ‘09 last month), Q2 GDP from Japan and the UK (both Friday), Chinese trade balance for July (Thursday), and China CPI/PPI (Friday). We’ll also get monetary policy decisions from the Reserve Bank of India (Wednesday) and the Reserve Bank of Australia (Tuesday) which will be important given the ratcheting up of the trade war.

In terms of other central bankers, we’ll see the return of Fed speakers after their blackout period and last week’s FOMC. St Louis Fed President Bullard will be speaking tomorrow, followed by Chicago Fed President Evans on Wednesday. Meanwhile on Thursday, the ECB will release their latest Economic Bulletin.

Earnings season continues, although at a slower pace than last week, with 62 S&P 500 companies reporting, along with a further 78 in the STOXX 600. The highlights this week include HSBC and Linde today; Walt Disney on Tuesday; Unicredit, AIG, Commerzbank, Glencore and Booking Holdings on Wednesday; Deutsche Telekom, Zurich Insurance Group and Aviva on Thursday; and Novo Nordisk on Friday. The day by day week ahead is at the end as usual.

To recap last week, equity markets sold off following a perceived disappointing Powell FOMC press conference and the escalation of the trade war, with President Trump announcing that 10% tariffs would be placed on a further $300bn of Chinese imports from September 1st.The S&P 500 declined every day last week to finish down -3.10% for the week (-0.73% Friday), while the NASDAQ fell -3.92% (-1.32% Friday) as both indices experienced their worst week of the year so far. The Dow Jones had a slightly smaller fall however, down -2.60% (-0.37% Friday). European markets were also reeling on Friday as they reacted to Thursday evening’s tariff news, with the STOXX 600 having its worst day of the year so far, losing -2.46% on Friday, bringing its losses for the week to -3.22%.

Fixed income rallied however, as investors flocked to safety and hoped for further monetary stimulus. 10yr Treasury yields fell for a 6th consecutive session on Friday, ending the week down -22.5bps (-4.8bps Friday) to their lowest level since President Trump’s election, while ten-year bund yields fell -11.9bps (-4.6bps Friday) to a fresh all-time low. German 30-year yields fell -20.4bps last week to close at +0.5bps, and at one point intra-day on Friday actually yielded negative for the first time ever. Pretty crazy really. Other safe havens also rallied last week, with gold ending the week up +1.55% while the Japanese Yen strengthened by +1.95% against the dollar, its biggest weekly appreciation since February 2018. Credit spreads widened considerably however, with indexes of cash HY spreads in the US and Europe up +26bps and +27bps respectively (+7bps and +23bps Friday). Meanwhile, in a sign that central bank easing doesn’t seem to be persuading markets on inflation expectations, or that trade wars/growth fears outweigh them, five-year forward five-year inflation swaps fell in the US and Europe last week, down by -10.6bps (-1.7bps Friday) and -13.3bps (-8.2bps Friday) respectively to reach 2.01% in the US and 1.22% in Europe.

The other main event on Friday was the US jobs report, which came almost exactly in line with expectations at +164k (vs. +165k expected), though the prior two months were revised down by -41k. The three-month average also fell to 140k, the lowest since September 2017. Earnings rose slightly above expectations at +3.2% (vs. 3.1% expected) while the unemployment rate remained at 3.7% (vs. 3.6 expected). In more positive news, the broader U6 measure that includes those underemployed fell to 7.0%, the lowest since December 2000. From Europe, the main data release was Eurozone retail sales for June, which rose by +1.1% mom in June (vs. 0.3% expected), the strongest mom gain since November 2017. The move brings the yoy change to +2.6% (vs. +1.3% expected).

via ZeroHedge News https://ift.tt/2YIWVe8 Tyler Durden

Democratic socialists earned some ridicule this weekend after video clips from their annual convention—which showed attendees objecting to clapping, disruptive chatter, and the use of gendered language on grounds that all of these things were triggering—appeared online.

One person took to the podium to thank his fellow comrades for waving their hands in the air instead of clapping, since sudden, loud noises can be harmful for the easily perturbed members of the audience.

“We have a lot of disabled comrades,” he said. He reminded everyone to “avoid hissing, avoid waving banners, there’s all sorts of things.”

It’s difficult, of course, to impose total silence on a political action conference. At one point, a convention delegate interrupted another person’s speech about “defeating capitalism” to make a “quick point of personal privilege.” This delegate began by reminding the audience that he uses “he/him” pronouns, and then implored: “Guys… please keep the chatter to a minimum,” because he is “very prone to sensory overload.” Immediately after this plea, another attendee shot back with their own point of personal privilege: “Please do not use gendered language to address everyone.” This person objected to the previous speaker’s use of the word “guys.”

It is not at all uncommon to see the DSA sidetracked by infighting over unreasonable requests related to language and disability status. In my book about modern activism—Panic Attack: Young Radicals in the Age of Trump—I describe how the DSA’s Medicare-for-All campaign was criticized by the DSA’s disability caucus, whose members claimed that they should have ultimate authority over issues pertaining to health and wellness. It is widely believed within progressive circles that the oppressed are the sole experts on their own oppression and that deference should be given to the most marginalized groups. In practice, this creates some weird standoffs. From my book:

Since disabled people are especially affected by health care policy, the Medicare for All group had essentially failed to let disabled people be the experts on their own oppression—an intersectionality no-no.

Amber A’Lee Frost, a Medicare for All proponent and prominent DSA member known for co-hosting the left-wing Chapo Trap House podcast, hit back, accusing her critics of trying to sabotage the movement with their “pathological anti-social behavior.” This made matters much worse: The comment was perceived as an attack on the autistic community.

Frost had committed ableism. Several dozen DSA members signed a petition demanding that she “immediately remove herself from any involvement, official or unofficial, with DSA’s Medicare for All campaign, and should she not, that she be removed.” This was necessary, because intersectionality means casting suspicion on organizing efforts if these efforts do not make the marginalized the center of attention.

No one should come away from the coverage of the DSA convention with the idea that attendees did nothing but call-out each other’s pronouns, though. Listening to the livestream I heard heated discussions about significant policy issues: criminal justice reform, supporting the presidential campaign of Sen. Bernie Sanders (I–Vt.), and combating “Lex Luthor–esque scumbag Jeff Bezos.” Of all the various factions of progressive activism, the DSA is by far the most organized, and the least likely to be derailed by culturally woke signaling.

from Latest – Reason.com https://ift.tt/2KqDQnZ

via IFTTT

{kind=link}