Pigs At The Trough: Amtrak Is Latest Company Begging For Bailout As Ridership Plunges 92%

Welcome to the latest episode of our ongoing “Pigs At The Trough” series, documenting how companies who have taken zero financial precautions over the last decade are now rushing to Uncle Sam and the American taxpayer for their “do-overs”.

Next up on the list is Amtrak, who is now apparently banking on a $1 billion bailout, according to the Wall Street Journal.

Like other major businesses, everybody staying home has had a profoundly and disproportionately negative affect on Amtrak, which has seen its ridership plummet. And it apparently comes just before the railroad was going to eek out a profit for the first time in its 50 year history.

That’s a shame. Perhaps the company should have focused on turning a profit at some point over the last 5 decades a little quicker?

But we digress. Bookings on the company’s Acela have fallen 99% through the end of last week as total ridership has fallen 92% across the national railroad system.

CEO Richard Anderson said: “There’s really no one riding the Acela. There’s no point operating empty trains.”

High speed service between Boston and Washington has been shut down, along with 40% of the railroad’s capacity on the Northeast Corridor. The company is running just 14 trains per day on the Northeast Corridor.

Anderson said on Friday the company needs $1 billion in addition to its annual operating subsidy and that the company is now projecting an $840 million loss for the year ending September 30. That loss will come despite expense reductions of $110 million to $150 million.

Those expense cuts include corporate matching of 401(k) contributions being suspended and the top three bands of management taking pay cuts of 20% or more. Workers are also being asked to take voluntary unpaid leave, as layoffs inevitably loom.

Anderson said: “It’s as dramatic a falloff as you’d see in any business. So we are working very hard to make up $1 billion in cash right now.”

Mark Kenny, the general chairman of the union representing Amtrak engineers said: “We are still a long way from getting back to any degree of normalcy, and things are very likely to deteriorate further before getting better.”

The company is reportedly working with congress to deal with an ”unprecedented reduction in demand and ridership, our ongoing service adjustments and our future financial needs so that we come out of this crisis ready to continue serving the nation.”

A bill making its way through congress right now includes $1.018 billion for Amtrak.

Amtrak spokeswoman Christina Leeds said: “Additionally, it is vital that we continue to advance capital projects that are critical to the safety and long-term operation of passenger rail.”

Meanwhile, DJ Stadtler, the railroad’s chief administrative officer told employees last week: “Amtrak doesn’t have the funding to cover pay and benefits for almost 19,000 employees for an indefinite period of time, during a crisis that is going to cause the company to lose hundreds of millions of dollars. It doesn’t feel good to say that, but this is the hard reality that we and most other employers are facing now. “

A World Health Organization expert has come forward warning that lockdowns and economic depression are not going to stop this virus. Michael Ryan, who heads the WHO’s Health Emergencies Program, urged world governments to take further tyrannical measures in combating the coronavirus.

But his solution is complete global totalitarianism.

Ryan wants governments to do things such as identifying people with the virus and quarantining them, forcibly if necessary. Forced quarantine with a gun to your head.

“What we really need to focus on is finding those who are sick, those who have the virus, and isolate them, find their contacts and isolate them,” Ryan told the BBC on Sunday, according toReuters.

“The danger right now with the lockdowns… if we don’t put in place the strong public health measures now, when those movement restrictions and lockdowns are lifted, the danger is the disease will jump back up,” Ryan said.

“Once we’ve suppressed the transmission, we have to go after the virus. We have to take the fight to the virus.”

Yet other experts, such as Johns Hopkins senior scholar Dr. Amesh Adalja says the coronavirus is here to stay, and it will now be a part of our seasonal illnesses such as the flu and the common cold. Because of that, we should work hard to treat it and save the lives of those who do get sick, much like we do with the flu.

“It’s going to become a part of our seasonal respiratory virus family that causes disease,” Adalja said on “Squawk Box.”

Adalja compared the coronavirus to the 2009 H1N1 swine flu outbreak, which is now seen as a regular flu virus. Eventually, we’ll have to deal with this virus just like we do all the others.

Goldman On Gold: “Time To Buy The Currency Of Last Resort”

A month ago, Goldman Sachs suggested there is more to come for precious metals as with rates getting closer to their lower bound, gold looks increasingly like the safest haven.

At the start of March, Goldman’s head of commodity strategy said there is one commodity that will be safe: gold“which – unlike people and our economies – is immune to the virus.”

And now, Jeffrey Currie and Mikhail Sprogis are saying The Fed’s “open ended” QE reverses funding stresses and will offset the negative impact from lower EM demand:

“We are likely at an inflection point [for gold] where ‘fear’-driven purchases will begin to dominate liquidity-driven selling pressure as it did in November 2008.”

As such, Goldman raises both the near and long-term gold outlook, saying they are “far more constructive,” reaffirming their 12-month target of $1,800/oz.

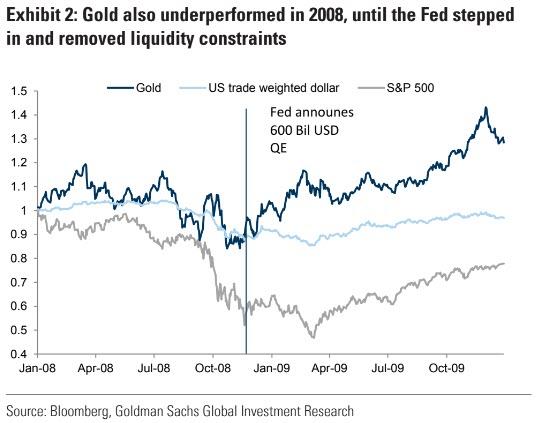

In 2008, the turning point for bullion was the announcement of $600b QE in November, after which gold began to climb despite further weakness in equities and commodities.

A similar pattern is emerging as gold prices stabilized over the past week and rallied as the Fed introduced new liquidity injection facilities.

Goldman’s full note below:

1) We have long argued that gold is the currency of last resort, acting as a hedge against currency debasement when policy-makers act to accommodate shocks such as the one being experienced now.

So why has the gold price fallen? The answer is the world is short dollars.

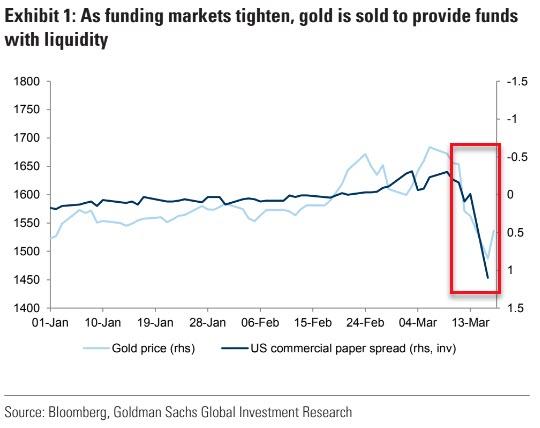

First, both physical and financial market participants face severe funding constraints; they have been forced to sell liquid positions which include gold and other commodities to generate dollars for other funding needs (see Exhibit 1).

Second, large falls in the price of oil have created dollar shortages for emerging market (EM) economies. This has become particularly apparent with the Russian central bank in the past several weeks as the oil price decline shifted Russia from a net buyer of gold to a possible net seller.

We believe that yesterday’s announcement from the Fed for ‘open ended’ QE reverses these funding stresses and offsets the negative impact to EM wealth and are recommending buying December 2020 gold.

2) Gold has been severely impacted by liquidity issues, correcting by $120 (-7%) from its peak.

The situation resembles 2008, when gold also failed to act as safe-haven asset initially, falling by around 20% due to dollar strength and a run into cash. In 2008, the turning point was the announcement of $600bn QE in November, following which gold began to climb despite further weakness in equities and commodities (see Exhibit 2).

We are beginning to see a similar pattern emerge as gold prices stabilized over the past week and rallied the last two days as the Fed introduced new liquidity injection facilities with this morning’s announcement.

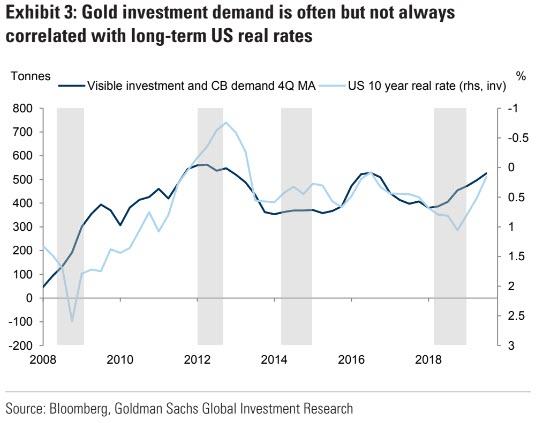

3) We analyze gold through the prism of our ‘Fear and Wealth’ framework, where ‘Fear’ of currency debasement is the primary driver of developed market (DM) investment demand while ‘Wealth’ is the primary driver of EM purchases.

Debasement ‘Fear’ is often, but not al ways, correlated with US long-term real rates (see Exhibit 3).

With funding stresses likely eased, focus will likely shift to the large size of the Fed balance sheet expansion, increase in fiscal deficits in DM economies as well as issues around the sustainability of the European monetary union.

We believe this will likely lead to debasement concerns similar to the post GFC period. Accordingly, we are likely at an inflection point where ‘Fear’-driven purchases will begin to dominate liquidity-driven selling pressure as it did in November 2008. As such, both the near-term and long-term gold outlook are looking far more constructive, and we are increasingly confident in our 12-month target of $1800/toz.

4) While ‘Wealth’ is likely to continue to be a headwind for gold, particularly in the near term as oil prices, EM growth and EM currencies remain under pressure, China and other parts of Asia are showing reassuring signs of recovery.

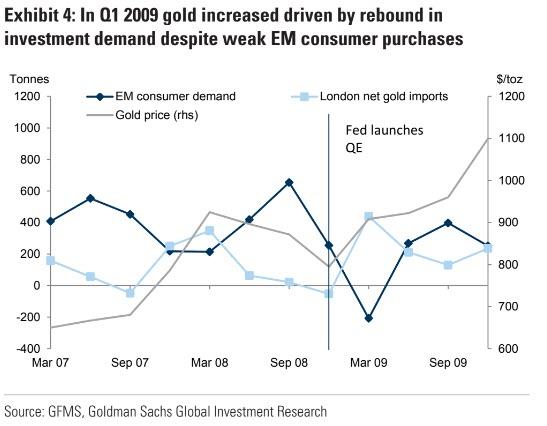

Last week we reduced our 6-month gold price target by $50/toz to $1700/toz to reflect the impact of lower EM ‘Wealth’, and we believe this has already been reflected in current gold pricing. Continuing to draw on the 2008 parallel, we believe that the increase in ‘Fear’-driven investment demand is likely to trump the negative ‘Wealth’ shock in the near term (see Exhibit 4).

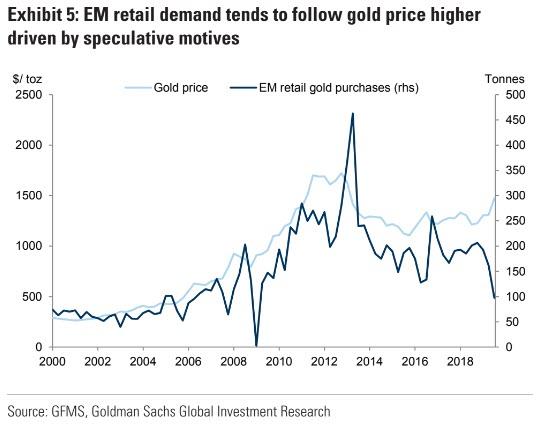

As gold demand can be deferred as opposed to permanently lost like energy demand, we expect as Asian EM economies stabilize, EM gold demand will rebound strongly as consumers make up for missed purchases, particularly for speculative purposes as they have done in the past when chasing a trending market (see Exhibit 5).

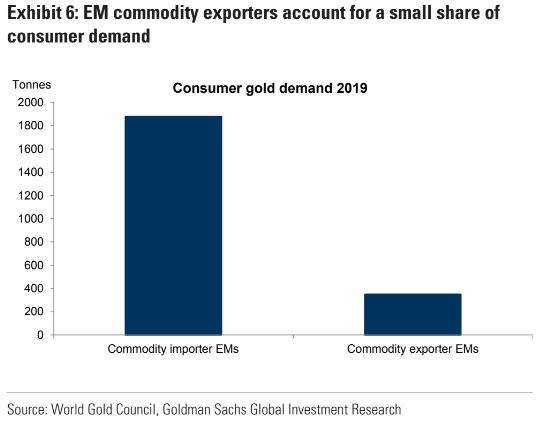

5) However, the wealth outlook for commodity-rich EMs is not as optimistic in the near term, but their demand for gold is not as large as that from the Asian EMs.

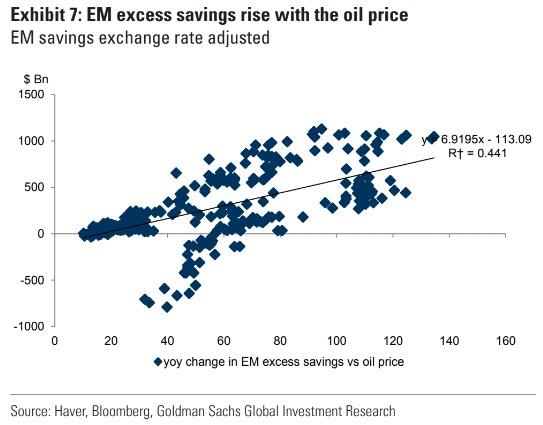

So while we are comfortable being long gold, it doesn’t mean that our FX strategists believe that the dollar shortages are behind us or that we would want to be long other commodities. As we have argued in the past, given the size of the global oil market, a drop in the oil price of recent magnitudes accentuates dollar shortages as oil and commodity prices are highly correlated with the accumulation and dissipation of EM excess savings (see Exhibit 7).

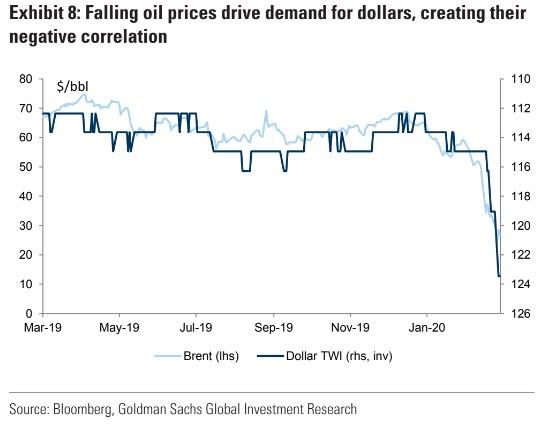

Financial markets normally transform these excess savings into greater global liquidity, supporting asset valuations and improving credit conditions globally. Hence, when weak commodity prices create a draw on EM savings they act as a drag on financial conditions and a headwind on gold prices as dollars become more scarce. Accordingly, the negative oil-dollar price correlation has been re-established (see Exhibit 8).

6) Ultimately, once their GDP stabilizes, EM consumers should help prolong the current ‘Fear’-driven bull market in gold.

Drawing one last parallel to 2008, while EM wealth continues to be under pressure due to the reasons cited above, once the COVID-19 crisis abates, we see potential for sequential improvement in Asian EM growth to lead DM out of the crisis as it did in 2008/09. This China-driven growth will likely give rise to inflationary concerns given the sharp expected contraction in oil and other commodity supply like agriculture and livestock. Combined with the fiscal nature of the current policy response to COVID-19, we believe physical inflationary concerns with the dollar starting near an all-time high will for once dominate financial asset inflation that was a feature of the past decade. Such inflationary concerns should further support gold prices as the currency of last resort.

… is according to Goldman the last thing and only thing that might store value, namely “the currency of last resort and avoids the concern that paper currencies could be a medium of transfer for the virus. As a result, gold has outperformed other safe haven assets like the Japanese Yen or Swiss Franc” a trend Goldman sees continuing as long as uncertainty around the full impact of COVID-19 remains, which will be the case for a long time, and is also why gold is currently the best performing asset class YTD, a “once in a decade event” as the last time this happened was back in 2010.

Before analyzing the emergency plans that the global economy needs, we must remember that, as in the past, the prudence and responsibility of the civil society and businesses will help us to get out of this crisis.

In the face of an unprecedented crisis, we have to be realistic, responsible and cautious.

This is a supply shock added to a mandatory shutdown of the economy. As such, a serious response must be supply-side driven. It is ludicrous to try to stimulate demand with printed money and public spending in a forced lockdown where any extra demand will not drive supply up, even may drive it down.

A mandatory shutdown due to a supply shock is not solved with government spending or demand-side measures. Printing money and lowering rates help the already indebted and governments with already historic-low bond yields, deficits are already going to soar due to automatic stabilizers, so governments need to work on three things:

First, make sure that once there is a tested and approved vaccine, the production, distribution, and healthcare networks are going to be adequately prepared to respond to the population requirements.

Second, make sure that businesses don’t collapse due to working capital build in a domino of bankruptcies that leads to mass unemployment.

Third, eliminate all unnecessary spending to effectively use all fiscal space to mitigate the crisis effects and allow the economy to breathe and recover.

Governments that overspent in growth times, massively increased debt and ignored the pandemic risks only to then create a widespread lockdown cannot present themselves as the solution.

Small and medium enterprises do not need a government to incentivize demand, because this is not a demand problem, the shutdown is imposed by law due to a health epidemic that lawmakers preferred to ignore.

We cannot fall into the trap of believing that what the economy needs is more monetary easing when it fails, and if it does not work then we must try even more monetary insanity.

Monetary insanity is not the solution to monetary excess and lunacy.

It is our duty to warn of the risks of falling into irresponsible optimism, precisely so that we can get out of this crisis sooner and better.

What recovery will there be?

Estimates of economic growth are plummeting at breakneck speed . The closure, albeit temporary, of economic activity, transport and trade, will mean an inevitable recession. The biggest mistake policymakers can make is to believe in a V-shaped recovery. All governments should prepare for an L-shaped recovery. If I am wrong, economies will be stronger anyway, but if I am right, massive stimulus implemented only three weeks after a market all-time high and immense deficit spending policies at the very beginning of a pandemic crisis will cripple the economy to an irreparable situation.

Leading economies have a great capacity to face a shock like this. This is not the case in Italy or Spain. Calculations for the United States indicate that unemployment will skyrocket to 6.5%, in the case of the United Kingdom to 7% and in Germany to 6%. In weak and highly intervened economies, the combination of already high unemployment, high debt, and high government spending can lead to a Greece-style crisis when the measures to address a forced shutdown come from more government intervention.

In the Eurozone, most of the plans announced by governments are based on three important flaws:

Ignore that many countries were already close to a recession in 2019,

assume a low-impact parenthesis and

estimate a rapid and exponential recovery that will inflict no real damage on employment or public and private accounts.

In the eurozone, Germany, France, Italy, and Spain’s fourth-quarter GDP already reflected a significant slowdown, so the European Commission, ECB and governments’ responses start from the wrong diagnosis: that the problem we are facing is one of demand and access to credit and not of sales collapse due to an imposed lockdown, with an accumulation of tax liabilities and fixed costs.

The United States must avoid making the mistakes that the eurozone nations are already starting to make.

Deadlines

European governments are unwillingly creating a worse long-term impact on the economy by giving citizens unrealistic small doses of negative information and extending lockdowns in fifteen days periods. This is leading to massive cash flow problems all over the economy because businesses find that the support mechanisms only last for a few days while the extension of losses destroys cash flow and balance sheets. Businesses are seeing current invoices delayed or unpaid while orders for November and December are being canceled.

Few will deny that it is necessary to take measures to close airspaces and cities, but in that same understanding, governments should allow solutions to real problems. By the time the developed economies’ government plans have completed its period of application, cities, and airspaces in other countries in the world will begin to close, creating a ripple effect. The collapse in activity that today affects mostly China and Europe, is likely going to spread to Latin America and India with a month lag.

Of course, a vaccine will be created, there are already great news from Seattle and twenty possible vaccines being tested, but it will take up to 18 months to approve it and, most importantly, it will take more months to manufacture those vaccines on a global scale. This cost is underestimated.

The vast majority of companies do not face a problem of access to credit (there is ample liquidity and credit supply on solvent demand and at very low rates), they face complete closure and layoffs due to cessation of activity. Zero income, but fixed costs and accumulated taxes. Many businesses will find that delaying tax payments or provide loans doesn’t solve anything.

Most businesses problem is not one of loan guarantees, but of the impossibility of requesting a loan. We are not in a crisis due to lack of access to credit, but rather a crisis due to the disappearance of activity.

The private contribution

Governments expect banks to provide massive relief through more loans, ignoring the fact that banks in the eurozone still have billions of non-performing loans and face a massive increase in delinquencies in Europe but also in their growth subsidiaries, mostly in Latin America and Asia.

Banks are going to face an increase in default on existing assets both in Europe and abroad. Banks can cope with this situation and they have done it well, but they are not going to be able to increase risk by tens of billions while helping their current clients to come out of the crisis Most Europen governments assume a balance sheet strength in private agents that is neither evident in large companies nor is it existent in SMEs (small and medium companies).

Additionally, Europe’s large companies already have high levels of indebtedness, although it has decreased admirably in recent years. Net debt to EBITDA in non-financial companies is already likely to soar due to the downgrades in earnings and cash flow.

Credit, liquidity and short-term aid measures are suitable for those who would have survived anyway before these new central bank and government measures. Liquidity was immense, rates were low and the banks did everything possible to lend.

The losers from this crisis will likely be those who have done their homework and live month by month, without large assets to cover a loan and without muscle to face months of zero income. And those, the ones who are going to suffer the most these months, were already drowned in taxes last year.

My proposals

Some politicians have mentioned the concept of “war economy”. And I think it is a correct one. For a war economy, there can be no bull-market administration.

The first thing that the Government should announce in the face of this challenge is a drastic reduction to zero of all the non-essential items of the budget, unnecessary subsidies, duplicate expenses, and a reduction in ministries and senior officials according to the moment.

The second is to work with the private sector to guarantee that, once a vaccine is available, all production and distribution channels are well organized so that it can reach the population quickly and efficiently.

The third is a complete tax exemption during the crisis period for companies, families and the self-employed. Zero income, zero tax. This will allow, together with liquidity lines at no cost, to survive the lockdown.

Governments are already going to consume all the fiscal space they have and more. The idea is that this enormous liquidity at negative real rates may be used for something effective for once, not to increase structural imbalances in current spending.

This is not asking the state to intervene, it is asking the government to stop intervening so much, stop the tax burden machine during an unprecedented business cataclysm, and unite in responsibility and austerity with those who are fighting every day to survive.

If governments and central banks decide to multiply the previous mistakes adding larger ones, like direct monetization of spending or helicopter money, they will add a monetary crisis to a mandatory supply shock. A mistake is not corrected doing the same but more aggressively.

We must ask the government to stop intervening so much, not to exploit an unprecedented business cataclysm to increase interventionism.

If governments insist on maintaining the few tax revenues they can scratch from the wreckage they will jeopardize the receipts of 2020 and those of 2021 and 2022, because of the massive increase in unemployment and closure of businesses.

Keeping the tax wedge system in a crisis of this magnitude generates a double negative. The domino of business failures and job losses will take years to recover, and with it, tax bases and receipts. Second, the potential growth is curtailed because of disproportionately high regulatory taxation, making it even more difficult to attract the little investment that could come after the recovery.

You cannot do war economics considering that everyone has margin except the enormous administration and political structure.

A widespread economic closure shock is not solved with demand measures or using the private sector balance sheet to add debt and accumulate risk, but with urgent supply measures that respond to the reality of businesses and, with them, of workers and families.

The US and the world will rise from this crisis. What the government has to do is allow it. The government is there to facilitate, not to pick winners and losers.

“The Recession Poised To Hit The Global Economy Will Be Unlike Any Other In History”

Authored by Ian Lyngen and Jon Hill of BMO Capital Markets

Service PMIs across the globe cratered during the month of March; Japan, Germany, France, and the UK all experienced dramatic declines in business sentiment as the coronavirus pandemic began to unfold. The dismal reports on the service side underperformed even the estimated weakness – hinting of a market which is struggling to gauge just how bad this will all be for the real economy. On the flipside, manufacturing PMIs came in better than anticipated as a theme – although it’s worth reiterating the context that all PMIs were sub-50 and decidedly in contractionary territory. Risk assets appear to be bouncing at the moment; this is occurring despite the inability of Congress to advance a stimulus bill to address the fallout from Covid-19 – still waiting.

We’ve offered the observation Italy is being viewed as the archetype for the pandemic in terms of speed of contagion and mortality – as imperfect of an estimate as it might ultimately prove. With this backdrop, stock futures hit the limit-up overnight and Treasury yields were modestly higher as the most recent Italian coronavirus stats indicated the growth of new cases might be slowing. In keeping with the theme of ‘moving on’ for parts of the world impacted, transportation to Wuhan is scheduled to resume on April 7 – after new infections fell to zero on March 19. We’ll be the first to suggest there is no obvious roadmap to recovery from this outbreak, although the experience (and response) of other areas has provided at least partial and imperfect information to aid in the domestic reaction.

The dueling concerns of containing the virus and limiting the economic fallout are the obvious driving force behind President Trump’s comments that “America will again, and soon, be open for business. Very soon. A lot sooner than three or four months.” This was also perhaps in response to Bullard’s suggestion the government should shut down the economy for three months; the odds of James replacing Jay anytime soon have been materially lowered. Just an observation.

In contemplating the next several months (of captivity), many have suggested the recession poised to hit the global economy will be unlike any other in history. We’ll sidestep challenging the actual validity of this claim and instead concede it will have a decidedly unique character versus anything experienced in the modern era. Unlike during armed conflicts, when the industrial machine has stepped up production and overshadowed the retrenchment of consumption, there is no real offset to plummeting economic activity. There is a case to be made that the medical equipment and home delivering industries will be booming – however (again using the Wuhan timeline), if the full course of the outbreak/shutdown is 2-3 months, by the time the extra capacity comes on line, consumers will once again be venturing into the great outdoors.

Sure, there have been plenty of predictions made about how the pandemic will forever change society and the way US workers participate in the labor market – home offices will overtake the ‘collaborative workspace’ as the new must-haves (even more bad news for WeWork). Perhaps, but we’ll argue this outlook has a much better probability of coming to fruition if the domestic economy is shutdown for 9-10 months versus 9-10 weeks. This is a challenging stance to take at what appears to be the eye of the hurricane (as it were). We’re reminded that it’s always darkest before the lights go completely out. Alas, we digress.

Instead, what’s currently underway is a test of financial reserves on pretty much every level. Liquidity reserves on the part of central bankers globally, cash reserves for businesses hoping to remain ongoing, and of course households – which could benefit from an additional injection from the Federal government to weather to economic storm. The extent to which the reserves are drawn upon (or completely exhausted) will dictate how much lingering economic damage and social/work-style changes ultimately come to pass. Just food for thought as stocks continue to bounce and Treasury yields define the range

China Lied, Released Infected COVID-19 Patients Ahead Of Xi Visit To Wuhan: Doctor

China lied about the number of COVID-19 patients in Wuhan, ground zero for the global pandemic, ahead of a visit for President Xi Jinping’s March 10 visit to the region, a local doctor told Kyodo News.

The same day China’s health authorities reported no new cases of coronavirus in Wuhan, several symptomatic patients were released early from quarantine, while health officials suspended a portion of testing, according to the report as relayed by the Japan Times.

According to the doctor – who works at a quarantine facility – the government figures “cannot be trusted,”as the number of patients under treatment is being deliberately reduced to show the CCP’s ‘success’ in getting the epidemic under control.

The doctor, in his 40s, whose responsibilities include determining whether a patient is discharged from a hospital expressed strong concerns that if the truth remains hidden from the public, another outbreak could occur.

Guidelines from the National Health Commission stipulate that patients must test negative for the virus twice and be cleared for pneumonia via a computerized tomography scan before being discharged.

But according to the doctor, from around the time of Xi’s visit, even though his patients still exhibited signs of pneumonia, the patients were released from quarantine at the discretion of a “specialist” from the epidemic prevention and control authority. –Japan Times

After the government specialist began releasing patients, the criteria for discharge was altered – and a “mass release of infected patients began,” he said.

Meanwhile, interview questions for people exhibiting symptoms were similarly simplified, while a blood test to detect antibodies produced during infection was discontinued – resulting in suspected patients being released back into the community.

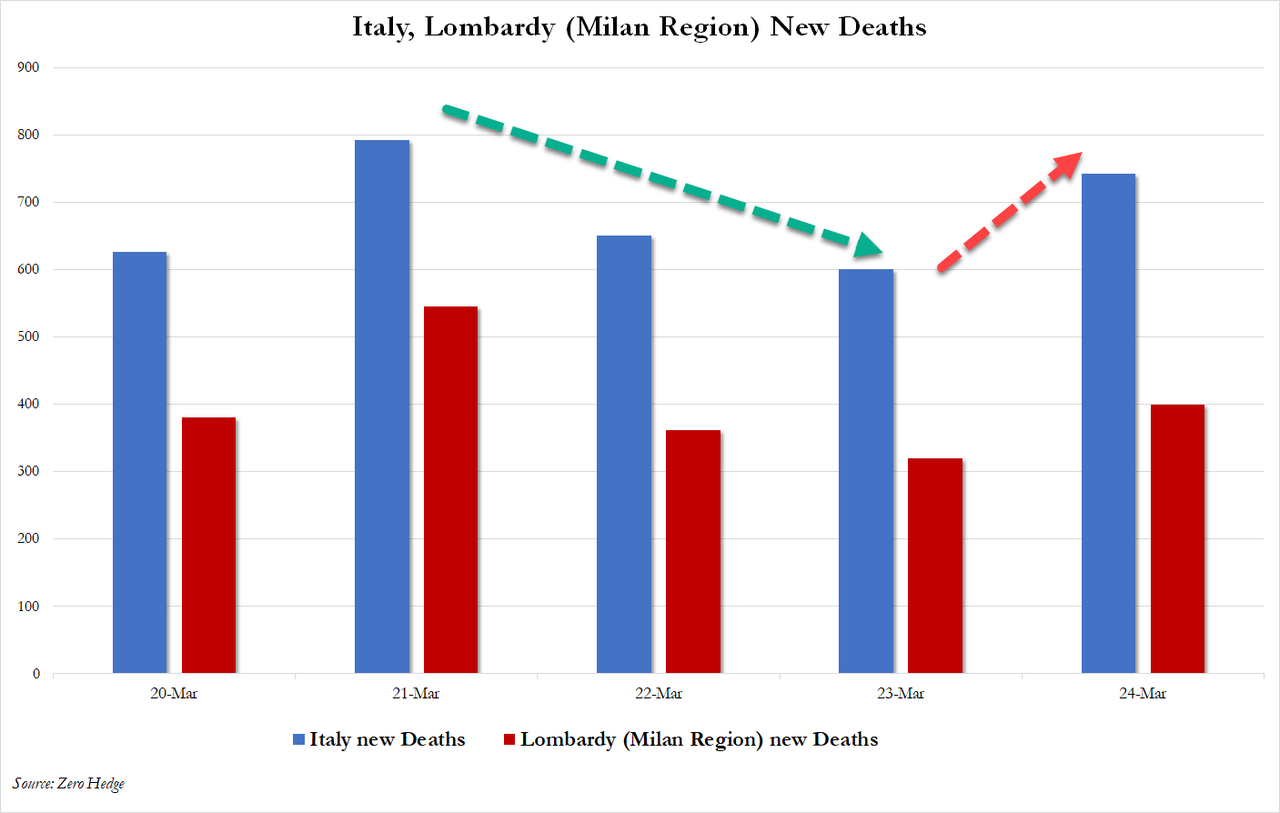

Stock Surge Stalls As Italy Admits 2nd Deadliest Day Of Outbreak

Dow futures have fallen back below 20,000, although still up dramatically on the day, as yesterday’s hopes that Italy had turned a corner in its virus-death-count are dashed after they reported 743 deaths overnight – the second worst count since the outbreak began.

New Cases re-accelerated…

And deaths re-surge to their second worst day of the outbreak…

Stocks faded (as Italy dashed the optimism of a two-day streak of declining totals)…

And bonds were bid…

But hope remains of the stimulus bill rescuing everything.

Foreign Buyers Flood 2Y TSY Acution Which Prices At Lowest Yield Since Feb 2014

In what may be one of the last normal Treasury auctions before the US has to prefund trillions and trillions in stimulus funds, moments ago the Treasury sold $40BN in 2 year paper, at a yield of just 0.398%, far below the 1.189% last month and the lowest since Feb 2014 when the US was back at ZIRP, and ahead of the Fed’s failed experiment at renormalizing.

The high yield of 0.398% tailed the When Issued 0.39% by 0.8bps, the third consecutive tail, and was a whopping 80bps below the February 2020 auction.

The Bid to Cover dropped to 2.362 from 2.454, the lowest since Dec but generally in line with the recent range.

Meanwhile, the internals were stellar with Indirects suring, and taking down 55.20%, up sharply from 46.2% and the highest since September, and as Directs dipped modestly from 9.31% to 8.55%, Dealers ended up taking down 36.3%, down from 44.5%.

Like we said, this is one of the last “normal” auctions as the next few months will see an unprecedented ramp up in new Treasury issuance as all those trillions in bailout funds have to paid somehow, and very soon it will not only be the Fed printer that does “brr”, but so will the US Treasury which will be printing debt just as fast.

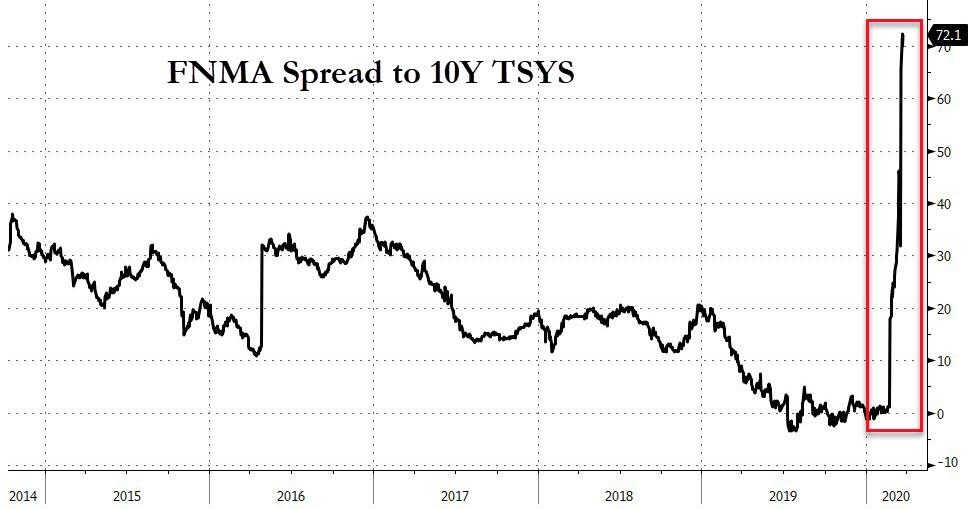

$14 Billion Commodity Broker Facing Crushing Margin Calls After Mortgage Hedges Go Terribly Wrong

We warned last week that, despite The Fed’s unlimited largesse, there is trouble brewing in the mortgage markets that has an ugly similarity to what sparked the last crisis in 2007.

For a sense of the decoupling, here is the spread between Agency MBS (FNMA) and 10Y TSY yields…

At that time, WSJ’s Greg Zuckerman reports that the AG Mortgage Investment Trust, a real-estate investment trust operated by New York hedge fund Angelo, Gordon & Co., is among those feeling pressure, the company said, and, in the latest sign of turmoil in crucial areas of the credit markets, is examining a possible asset sale.

“In recent weeks, due to the turmoil in the financial markets resulting from the global pandemic of the Covid-19 virus, the company and its subsidiaries have received an unusually high number of margin calls from financing counterparties,” AG Mortgage said Monday morning.

Well, they are not alone.

As Bloomberg reports, the $16 trillion U.S. mortgage market – epicenter of the last global financial crisis – is suddenly experiencing its worst turmoil in more than a decade, setting off alarms across the financial industry and prompting the Fed to intervene. But, as we previously noted, it is too late and too limited (the central bank is focusing on securities consisting of so-called agency home loans and commercial mortgages that were created with help from the federal government).

And the aftershocks of a chaotic rush to offload mortgage bonds are spilling over to regional broker-dealers facing mounting margin calls.

Flagstar Bancorp,one of the nation’s biggest lenders to mortgage providers, said Friday it stopped funding most new home loans without government backing. Other so-called warehouse lenders are tightening terms of financing to mortgage providers, either raising costs or refusing to support certain types of home loans.

One prominent mortgage funder, Angel Oak Mortgage Solutions, said Monday it’s even pausing all loan activity for two weeks. It blamed an “inability to appropriately evaluate credit risk.”

Things escalated over the weekend, according to Bloomberg, when some firms rushed to raise cash by requesting offers for their bonds backed by home loans.

“I ran dealer desks for over 20 years,” said Eric Rosen, who oversaw credit trading at JPMorgan Chase & Co., ticking off the collapse of Long-Term Capital Management, the bursting of the dot-com bubble some 20 years ago, and the 2008 global financial crisis. “And I never recall a BWIC on a weekend.”

And now, commodity-broker ED&F Man Capital Markets has been hit with growing demands to post more capital to cover souring hedges in its mortgage division, according to people with knowledge of the matter.

The requests are coming from central clearinghouses and exchanges, forcing the firm to put up almost $100 million on Friday alone, the people said, asking not to be identified because the information isn’t public.

ED&F, whose hedges exceed $5 billion in net notional value, has been in discussions with the clearinghouses and has met all the margin calls, one of the people said.

As a reminder, ED&F Man Capital is the financial-services division of ED&F Man Group, the 240-year-old agricultural commodities-trading house.

It has about $14 billion in assets and more than $940 million in shareholder equity, according to the firm’s website.

Concern about losses in mortgage bonds could feed turmoil in the overall mortgage market that ultimately drives up borrowing costs for consumers looking to buy homes and refinance. Mortgage rates have risen in recent weeks, despite a fall in benchmark rates.

“The Fed is going to do whatever it takes to restore normal functioning in the market,” said Karen Dynan, a Harvard University economics professor who formerly worked as a Fed economist and senior official at the Treasury Department.

“But we need to remember that the root of the problem is that financial institutions and investors are desperately seeking cash, so in that sense the Fed’s announcement is not everything that needs to be done.”

All of which sounds ominously similar to July 2007, when two Bear Stearns hedge funds (Bear Stearns High-Grade Structured Credit Fund and the Bear Stearns High-Grade Structured Credit Enhanced Leveraged Fund) – exposed to mortgage-backed securities and various other leveraged derivatives on same – crashed and burned and started the dominoes falling…

Boeing, Which Demands A $60BN Taxpayer Bailout, Refuses To Give US An Equity Stake

Here is a snapshot of America’s bailout culture: beggars, and those demanding bailouts, can not only be choosers, but can dictate under what terms they are bailed out.

With populist anger growing in response to Boeing’s demands for a taxpayer-funded bailout (or the employees get it) after it spent over $40BN on buybacks making its shareholders and management richer while burying the company and rank and file employees under a record $25BN in debt, many have asked what form the Boeing bailout will take, and whether the US taxpayers will also be entitled to some or all of the upside in the company they will soon be asked to bailout. In other words, will the US get an equity stake?

We got the answer moments ago, when the company’s new CEO Dave Calhoun confirmed that the disgraced airplane maker – which until recently was best known for making airplanes that were “designed by clowns, who in turn are supervised by monkeys”, at least until it came crawling and demanding a non-recourse bailout -said Boeing does not want the U.S. government to take a stake even as the planemaker seeks assistance to grapple with effects from the new coronavirus.

“I don’t have a need for an equity stake,” Calhoun said in an interviewTuesday with Fox Business. “I want them to support the credit markets, provide liquidity. Allow us to borrow against our future.”

And just in case it wasn’t clear that Boeing is confident it has all the leverage, he added “If they force it, we just look at all the other options and we’ve got plenty of them.”

Well of course he doesn’t want to give equity to those who bail Boeing out: that would cripple his comp for years which would be determine by some Treasury clerk. Instead, what Boeing really wants is to repackage a bailout with no loans and lots of grants (i.e., direct investments) as merely “providing liquidity.”

Note, again, this is the same company that blew $50 billion in “liquidity” repurchasing its stock so that management, which includes Mr. Calhoun, could cash out of their options at record high prices, and pocket millions. And now that the pillage is over, it’s time for a bailout, one where taxpayers inexplicably end up with… nothing?

But nobody wants to see Boeing in Chapter 11, and Calhoun said that if there is “no government support” in the credit markets, Boeing’s cash burn will accelerate. And if this goes on for 8 months, well, that could be a problem, Calhoun said during a separate interview Tuesday on CNBC.

In any case, we now wait to see what form that Boeing bailout will take. Congress has struggled to come to terms on a massive stimulus package to aid businesses and individuals struggling with the economic fallout of the outbreak, although House Speaker Nancy Pelosi said Tuesday she was confident a deal would be reached.

Boeing, which is seeking $60 billion in “aid” – whatever that means – for the aerospace industry, said Monday that it would shut down its Seattle-area manufacturing hub for two weeks after a worker died of coronavirus complications. The company suspended stock buybacks and dividend payments only late last week, while Calhoun and Chairman Larry Kellner have given up all pay until year-end. It is unlcear why Clahoun and Kellner shouldn’t have all their bonuses paid during years they were repurchasing stock clawed back.

Boeing shares surged 16% to above $123 on Tuesday as the market rallied on signs that Congress was near agreement on a stimulus bill. Boeing plunged 68% this year through Monday, the worst performance on the Dow Jones Industrial Average.