American Fishing Vessels Spooked As Russian Nuclear Submarine Surfaces Near Alaska Tyler Durden

Fri, 08/28/2020 – 09:35

Though American and its European allies are quite used to by now Russian drills occurring in places like the Black and Baltic Seas, and even in the Eastern Mediterranean off Syria’s coast, on Thursday into Friday the Russian navy conducted military games near Alaska, in a first such instance since the Soviet Union.

The military games took place in the Bering Sea and surprisingly involvedover 50 warships and some 40 aircraft. The significant size given the location will surely be seen as a provocation by Washington, in a region which over the past year has seen multiple NORAD jets scrambled to intercept Russian long-range bombers coming too near Alaska’s coast.

Illustrative file image, via TASS

“We are holding such massive drills there for the first time ever,” Russia’s navy chief, Adm. Nikolai Yevmenov said in an official statement.

The AP reports that the timeline of the exercises remains unclear, and they could be ongoing possibly through the weekend. It’s broadly part of a Russian military initiative to better secure the Arctic region and to “protect its resources,” as the AP notes.

The HQ of @NORADCommand and @USNorthernCmd are closely monitoring the Russian submarine that surfaced near Alaska today. We closely track vessels of interest, including foreign military naval vessels, in our area of responsibility.

“We are building up our forces to ensure the economic development of the region,” the Ministry of Defense statement said. “We are getting used to the Arctic spaces.”

Interestingly and certainly provocatively both the Omsk nuclear submarine and the Varyag missile cruiser took part in the games, reportedly launching cruise missiles at targets as part of the exercises.

A Russian submarine surfaced near Alaska on Thursday during a Russian war game exercise, U.S. military officials said. https://t.co/AoimcCdu5f

NORAD says it’s closely monitoring as is the US Coast Guard, the latter which was actually tipped off by US fishing vessels which were stunned to apparently observe military activity.

The Moscow Times also confirms that area fishing vessels actually witnessed a Russian nuclear submarine surfacing – something highly unusual:

A Russian nuclear submarine has surfaced near Alaska during navy exercises, spooking American commercial fishing vessels in the area, the U.S. military said early Friday.

Russia’s Defense Ministry announced Thursday that its nuclear-powered cruise missile submarine Omsk and missile cruiser Varyag fired at targets in the Bering Sea as part of its “Ocean Shield 2020” drills. Alaskan media reported that local pollock fishermen had a close encounter with the Russian vessels.

File image via Trident Seafoods

The ultra-rare event of the Omsk nuclear sub surfacing is something that even NATO intelligence is not often able to observe and document.

“We were notified by multiple fishing vessels that were operating out the Bering Sea that they had come across these vessels and were concerned,” a US Coast Guard statement said Thursday.

via ZeroHedge News https://ift.tt/2FWQGeT Tyler Durden

“Ce qu’il y a de certain c’est que moi, je ne suis pas Marxiste.”

(“What is certain is that I myself am not a Marxist.”)

– Karl Marx, 1882

Summary:

The bullish narrative of aggressive retail call buying driving markets higher conceals an important market dynamic of decreasing liquidity and an increasing mismatch between buyers and sellers as option volatility selling strategies, like call overwriting, retreat in the aftermath of poor performance. These dynamics drive a scenario of increased fragility that raises prospects for extreme moves in both directions.

This is going to be short, but sweet.

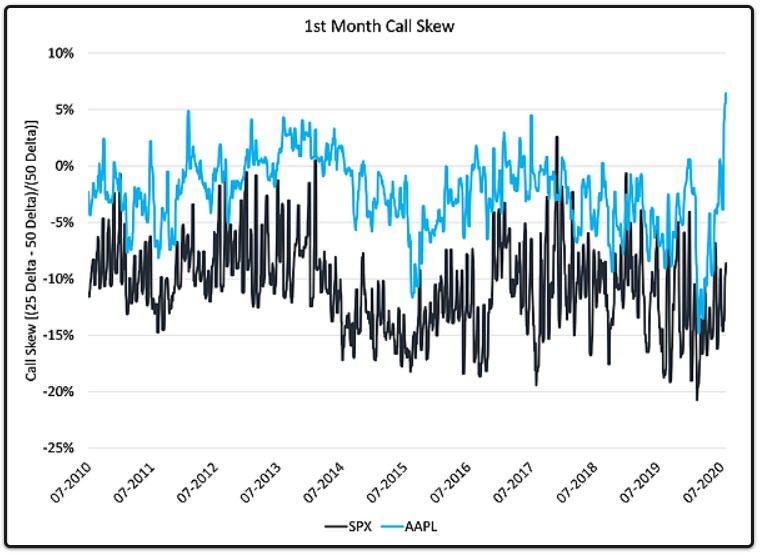

Over the past few weeks, media chatter has been steadily increasing with breathless comparisons to the DotCom bubble as many of the momentum favorites have churned higher and higher, and alongside their relentless rise, a consistent rise in the pricing of their Out Of The Money (OTM) call options.

For starters, it is important to emphasize that this is a single stock rather than an index phenomenon. As a simple example, Apple (AAPL) 25 delta – 50 delta front month call option implied volatility skew has risen to decade highs while the S&P’s is hanging out in normal territory.

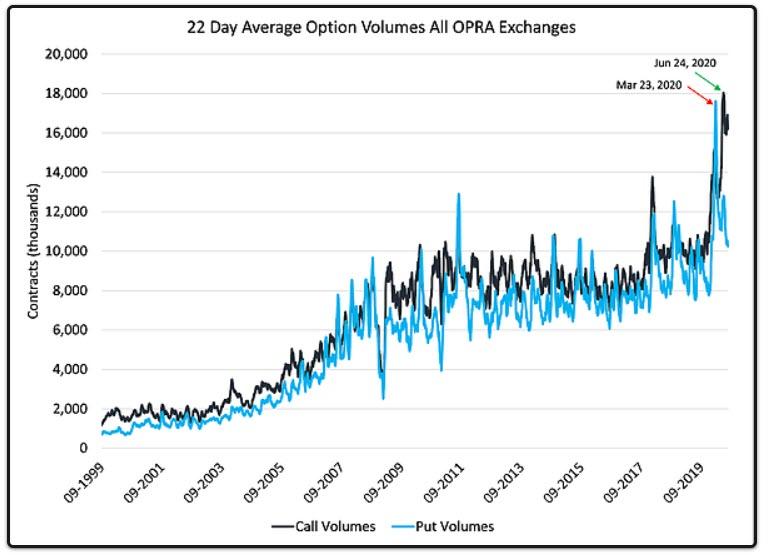

Concurrently, a chart has been making the rounds highlighting explosive call option volumes. While this is true, what is not represented is that just a few months ago we experienced record high put volumes. This market has truly been an equal opportunity offender in just the span of a few months. Given the extraordinary moves we have seen in stocks like AAPL, the obvious question becomes “Are we seeing a replay of DotCom mania?” Well, “yes, but…”

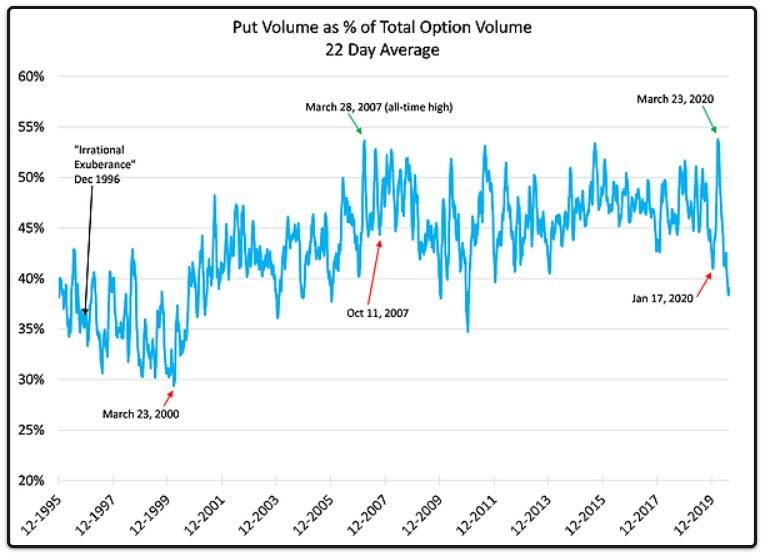

If we utilize a longer time frame to compare the current exuberance for calls to the heady DotCom era, we come nowhere close. The current fraction of option volume for calls, at 62%, remains below the average of 65% for the entire period from Greenspan’s “Irrational Exuberance” speech to the crashing of the Nasdaq on March 23, 2000. What does appear unusual is the near record share of puts as a fraction of option volumes (53.7%) on March 23, 2020(the day before the recent trough in equity prices and almost exactly 20 years to the day from the record low reached in the DotCom cycle when only 29% of option volume went to puts).

The unfortunate answer appears to be that the behavior we are seeing is not tied to massive speculation in calls, but rather a predictable dynamic driven by increased dealer hedging costs given an in increasingly illiquid market.

This is the source of the subtitle of this piece – the well-known disclaimer by Marx that if he were to listen to the Marxist rants of his followers, he would not consider himself to be a Marxist. At the core of the error in Marxism is the belief in the Labor Theory of Value; that cost determines price. This is only true in a monopolistic environment, which could only happen if option market making were becoming increasingly dominated by a few large players. We have seen no evidence of this. (Narrator: there is evidence for this)

via ZeroHedge News https://ift.tt/34FF2zx Tyler Durden

Russia, India Plan Partnership To Mass Produce Vaccine As Merkel Warns Germans COVID-19 Outbreak Will Worsen: Live Updates Tyler Durden

Fri, 08/28/2020 – 09:05

Summary:

Russia cases top 980k

Merkel warns Germans outbreak will get worse

India suffers biggest jump in new cases

Indonesia suffers 2nd straight record jump

Japan announces plan to stockpile vaccine as Abe resigns

South Korea extends social distancing restrictions

China reports 9 new imported cases, 12th day with no domestic infections

* * *

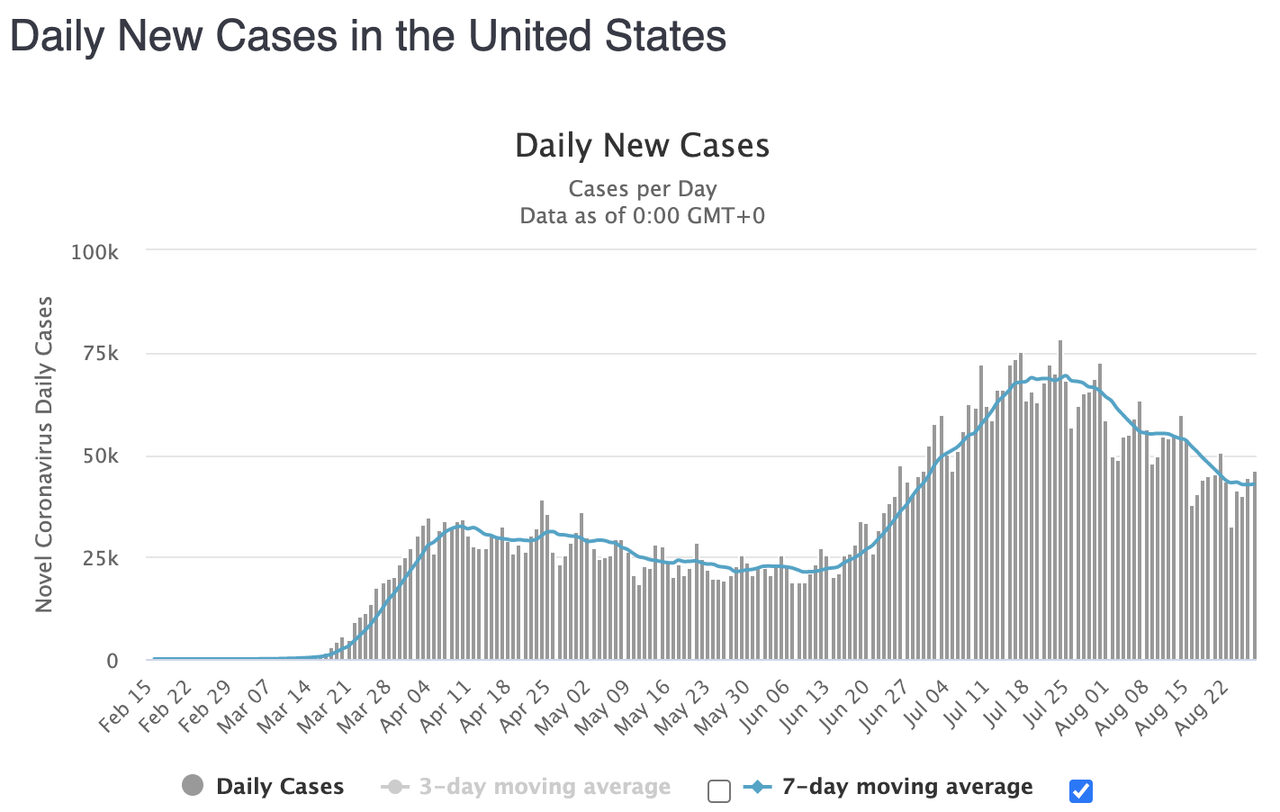

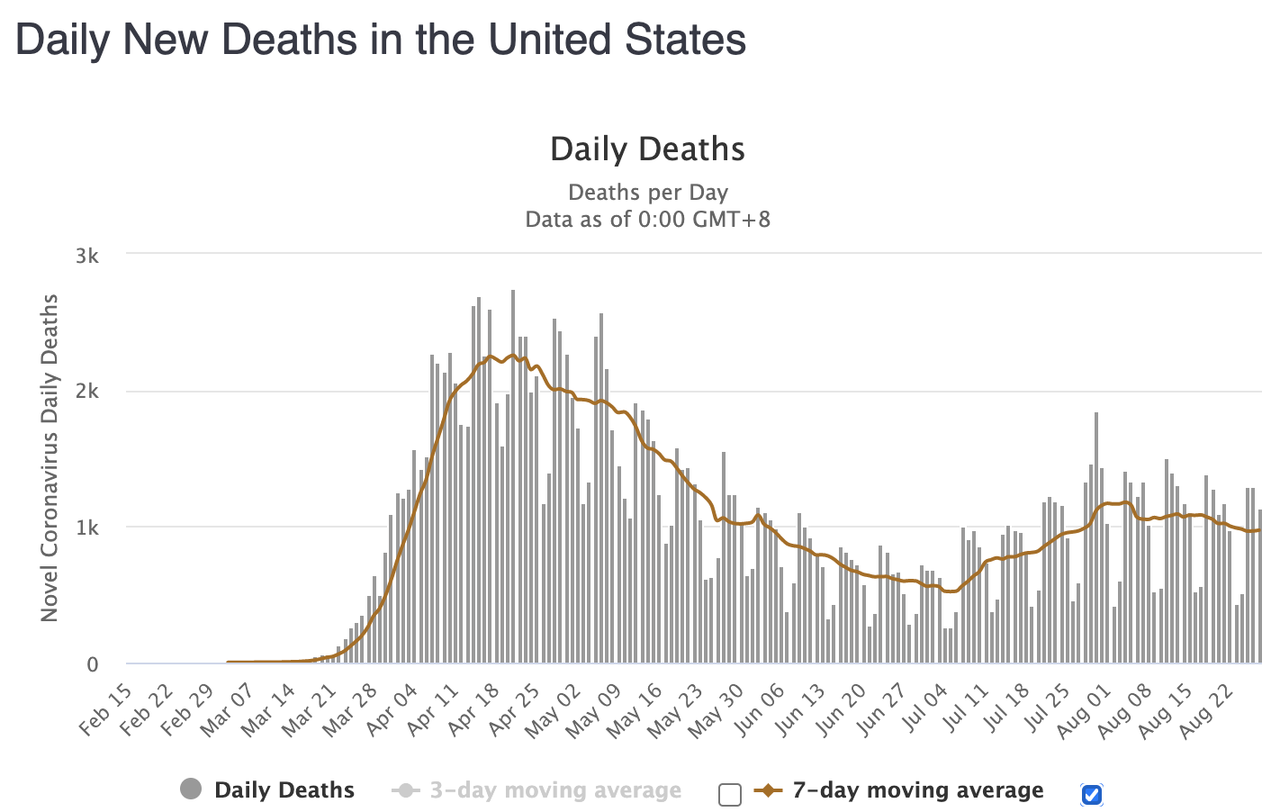

As we reported last night, the US surpassed 180,000 coronavirus-related deaths last night, by far the largest death toll in the world. Only one other country – Brazil – has a death toll in the six-figure territory. But on Friday morning, Russia’s coronavirus cases surpassed 980,000 after the country reported 4,829 new cases over the past day, cementing its status as the fourth-largest outbreak in the world.

Russia’s coronavirus taskforce added 110 deaths to the official death toll, bringing its total to 16,914, a total that some experts claim has been deliberately suppressed by the government.

Circling back to the US, the country has added 931 new coronavirus deaths in the past 24 hours, bringing the country’s total death toll to 180,527, along with an additional 42,859 new confirmed cases, bringing its overall caseload to 5,860,397.

In Japan, the big news overnight was that PM Shinzo Abe announced his plans to resign as soon as his party, the Liberal Democrats, elects a new leader. Abe leaves Japan with a parting gift: an initiative to stockpile vaccine doses ahead of next summer’s Olympics. Japan is aiming to secure COVID-19 vaccinations for all citizens by the first half of 2021, said Prime Minister Shinzo Abe, who announced the measures to beef up Japan’s vaccine stockpiles ahead of the upcoming flu season, even as he heads for the exits.

In other vaccine, Moderna shared some more procedural news about its clinical trials, while the European Commission said it had signed a contract with British drugmaker AstraZeneca, which is working with Oxford on a vaccine candidate, for the supply of at least 300 million doses of its as-yet-unproven vaccine. It is the first contract signed by the EU with a vaccine maker, and follows the US, UK and Japan in the race to secure supplies of a vaccine.

India reported yet another single-day record jump of 77,266 cases, pushing the country’s total to 3.39 million with the death toll rising to 61,529, up 1,057 since Thursday morning. With the COVID situation still pretty dire, Indian Health Secretary Rajesh Bhushan affirmed Friday that the country is considering manufacturing and testing Russia’s Gameleya Institute-developed vaccine, known as “Sputnik 5”.

“As far as Sputnik V vaccine is concerned, both the countries are in communication,” Indian Health Secretary Rajesh Bhushan told reporters this week when asked whether New Delhi had been formally approached by Moscow over manufacturing the vaccine.

“Some initial information has been shared [with India, and] some detailed information is awaited,” he said, without providing further details, according to Nikkei.

India has plenty of capacity for manufacturing generic drugs and vaccines, plus a massive population upon which to test the vaccine, which is probably why Russia is seek such a partnership.

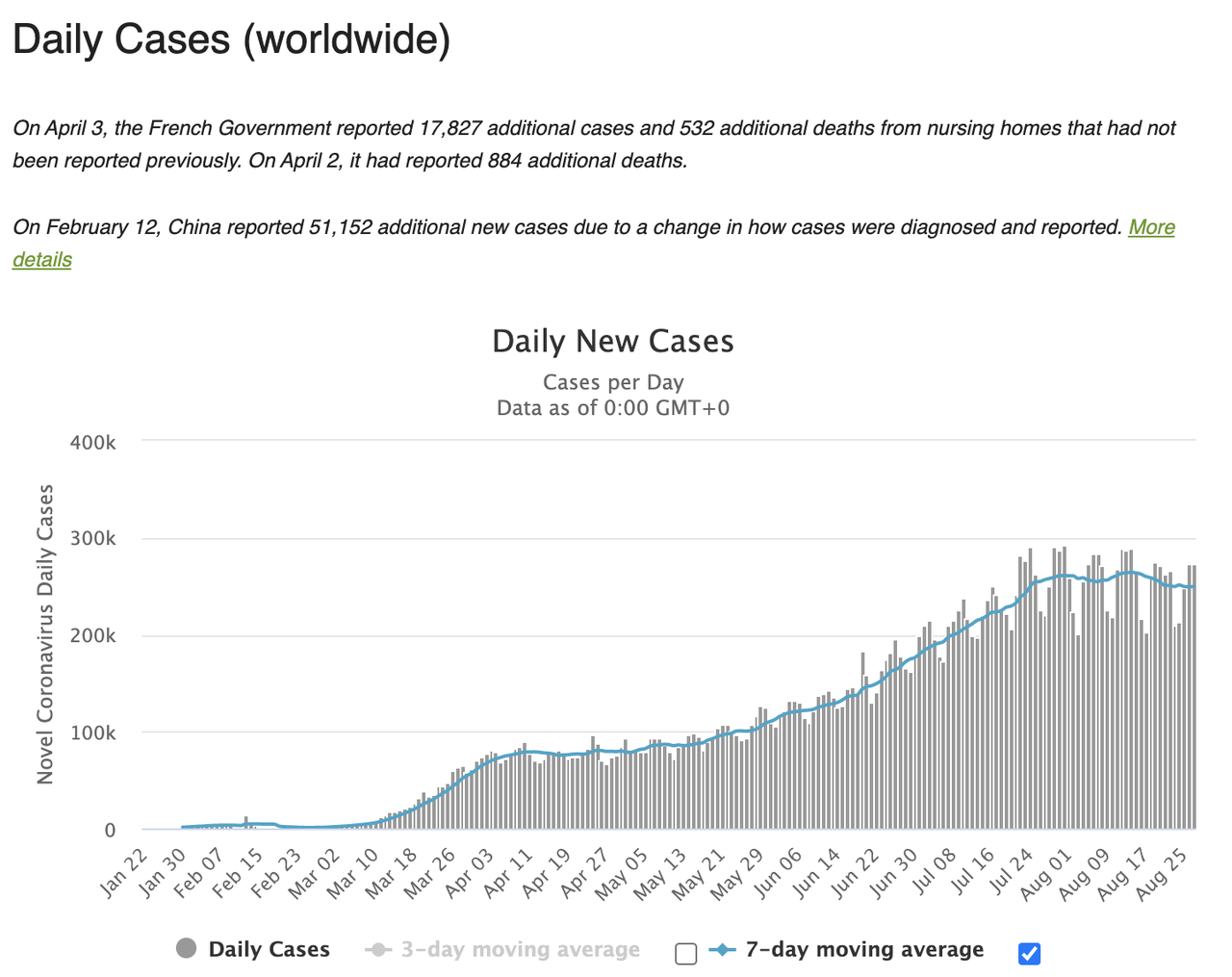

Globally, cases continued to slow with just under a quarter million reported yesterday.

South Korea extended the current Phase 2 social distancing measures in the Seoul area for at least another week, though the government stopped short of a threatened return to “Phase 3”. South Korea confirmed 371 cases on Friday, down from 441 a day ago, bringing the country’s total to 19,077 with 316 deaths.

China reported nine new cases on Friday, all of them imported, compared with eight a day earlier. It marked the 12th straight day with no domestic transmission.

President Donald Trump promised to “crush” the coronavirus pandemic with a vaccine by the end of the year during his speech accepting the Republican nomination last night.

“We are marshalling America’s scientific genius to produce a vaccine in record time,” Trump said. “We will have a safe and effective vaccine this year and together we will crush the virus.”

Indonesia’s daily new cases notched a new record high for a second consecutive day at 3,003 on Friday. Another 105 new deaths were slso recorded. Indonesia has clocked 165,887 cases and 7,169 deaths, while Jakarta cases have also set a new daily record at 869.

The Philippines confirmed 3,999 additional infections, up from 3,249 a day earlier, bringing the country total to 209,544. It also reports 91 more deaths, pushing the total to 3,325.

As Germany’s new daily COVID-19 numbers continue to climb, Chancellor Angela Merkel told Bloomberg that the coronavirus crisis represents a serious challenge to Germany’s financial health, largely because the virus could be with us for “a long time.”

Which is why it’s so important for Europeans to work together and to use the emergency financing mechanisms that have been set up.

“That is why a large part of the money will certainly go toward what we have already set out to do in the economic stimulus program and what has not yet been fully financed,” she said. During what was one of her final summer press briefings, Merkel warned Germans to buckle up, because cases will likely continue to climb in the coming months as more schools and businesses reopen, since returning to a lockdown isn’t an option, life probably won’t return to normal until a vaccine is in use, Merkel said.

Even though Germany isn’t expected to fully repay debt incurred by these relief measures until 2058, such stimulus measures are essential as the economy could not be allowed to grind to a halt in the meantime, she said.

“This is a serious matter, as serious as it’s ever been, and you need to carry on taking it seriously,” she told a news conference. And even once this is all over, “not everything will be like it was before,” Merkel added.

via ZeroHedge News https://ift.tt/2YFFyK8 Tyler Durden

“The Fed Has Become An Awful Echo Of The End-Days Of The Former Soviet Union” Tyler Durden

Fri, 08/28/2020 – 08:45

By Michael Every of Rabobank

As flagged yesterday, the Fed came, they saw,…and the Fed did even less than most had expected. After an exhaustive round of “The Fed listens” exercises, after teams of its economists and heavy thinkers got together to find a solution, the multi-year strategic policy framework review came up with…a shift to targeting inflation averaging 2% over the long term rather than the medium term and even greater tolerance for low unemployment.

That’s it. Not even yield curve control. Not even nominal GDP targeting. Nada.

This makes a mockery of those hoping for substantive change after such an exhaustive process. It makes a mockery of those expecting any substantive improvement in the future economic outlook. It makes a mockery of the army of Fed economists and their models and assumptions. As I said yesterday, it’s all political-economy…on which note please see here.

Yesterday was like a hunter-gatherer coming home to his starving tribe after yet another unsuccessful hunt for wild boar —because he uses a spear with no sharp flint on the end— and saying: “Don’t worry! After a policy review I am sticking with the spear, but will now catch more boar over the long run, so you will all get enough to eat.” This as winter approaches and it’s berries, berries, and berries on the menu again for those shivering round the fire.

Another way of looking at it, and one I’ve flagged before, is an awful echo of the end-days of the former Soviet Union. There were some planet-sized brains among the apparatchiks running that place. The problem was that the entire system didn’t work, and any tinkering with it could never achieve anything: the political-economy had to change, or nothing did. As a result, time after time, committee after committee of technocrat PhDs would meet, debate…offer up more agitprop jargon, and decide to build a new statue of Marx or Lenin.

Allow me to excerpt from the superb note on this latest Fed debacle from our Fed whisperer Philip Marey. First, he notes that the FOMC announced a 2% inflation target back in January 2012; the FOMC minutes of the October 2014 meeting then made clear this was symmetrical, and that over or under 2% was seen as problematic. The policy shift we saw yesterday has been in the pipeline since then. “During the Q&A at the Kansas City Fed event Powell said the Fed intends to do this kind of monetary policy review every 5 years. Does this mean that we have to wait 5 more years for the next negligible progress?”

Philip goes on to note: “The much deeper problem for the US economy is the asymmetric impact of Fed policies on households and businesses. The Fed’s monetary and regulatory policies have contributed to a form of capitalism where the rewards are going to the 1% and the risks are borne by the 99%. The current crisis response has made it painfully clear again that the Fed’s policies benefit high income individuals and large corporations, while small businesses and low income individuals bear the burden. While the Fed likes to see itself as part of the solution to America’s economic problems, it should ask itself whether it is also part of these problems.”

The market took a while to digest what it thinks this Fed move means. The end result was US 10-year yields jumping 12bp intra-day and sitting at 0.77% as I type, steepening the yield curve. Even the 5-year shot up from an intra-day low of 0.26% to a high of 0.31% and is at 0.32% at time of writing. In other words, it would appear that somebody seems to think that this will work and that there is now a moderately higher chance of higher inflation further down the line.

Really? By doing nothing for longer against a post-Covid-19 structural backdrop that is far, far worse than it was when the Fed’s policy review began, the odds of it meeting its future goals have improved? That’s an interestingly Panglossian view: perhaps we should all do more of nothing more often!

Meanwhile, even as the market is pushing US yields higher, the USD is on the back foot once again. Presumably, someone must be thinking that the Fed doing even less than was expected of the kind of policy that the more of which you do, the less success you get, is going to mean that the US government has to do more. Indeed, another new fiscal stimulus package, which is still not on the horizon in DC according to public statements, is being presented as the next trigger for USD selling. Movement in that direction might not have been accelerated by anything the Fed did, but it likely will be on the back of reports that a major US credit card firm is cutting consumer credit limits.

Well, let’s see how the rest of the world likes the same higher long yields the US is dragging them all towards: 10-year Aussies are now over 1% again, for example. Let’s see how their wobbly economies can cope with that, and how long before they too have to inject new monetary or fiscal or fiscal-monetary stimulus. Let’s see how much global demand there will be for those currencies when that inevitable happens.

For example, Tokyo CPI, which leads the national, was 0.3% y/y today vs. 0.6% expected, and -0.3% ex fresh food vs. 0.3% consensus, and -0.1% ex energy too, vs. 0.4% consensus. A whole lot more Japanese stimulus of the kind we know doesn’t work, and which the Fed is studiously copying, must surely be in the works?

Meanwhile, certainly putting the political in economy, Japanese PM Abe is stepping down for health reasons. This is a major development given under Abe Japan has seen political continuity, when the previous tradition was a rotating door of prime ministers. Will the new PM continue Abenomics? Will they actually implement the third arrow of structural reform (i.e., political-economy)? And how about the geopolitical implication given Abe has been pro-US and building up a regional alliance with Australia and India? The knee-jerk reaction has been a fall in the Nikkei and risk-off JPY buying.

More uncertainty. Indeed, the only certainty we have is the one that the Fed is providing – of the wrong kind.

via ZeroHedge News https://ift.tt/3hxJ7t4 Tyler Durden

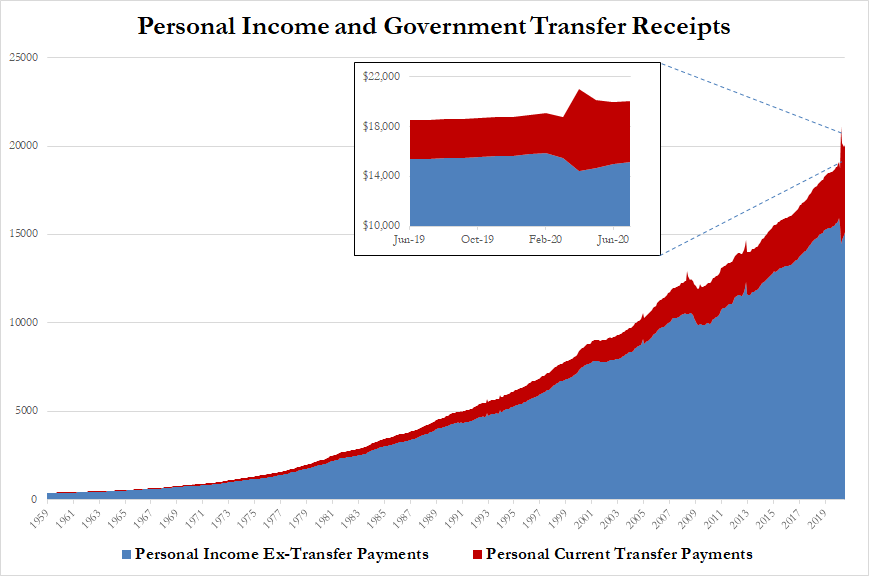

Americans’ Income & Spending Rose More Than Expected In July (Before Handouts Stopped) Tyler Durden

Fri, 08/28/2020 – 08:39

Analysts expected the trend of the last two months to continue in July with personal spending rebounding (though at a slower pace) and personal incomes shrinking back, but both surprised to the upside with a +0.4% MoM rise in incomes and +1.9% MoM jump in spending ( vs -0.2% and +1.6% respectively).

Source: Bloomberg

Incomes (thanks to govt transfers) are still up 8.2% YoY while spending remains down 2.8% YoY…

Source: Bloomberg

Private workers’ pay fell less than government workers’ pay in July on a YoY basis:

Private sector wages dropped -1.2% Y/Y, better than -2.7% last month

Government worker wages dropped -1.3%, better than -1.3% last month

Overall spending is back to Nov 2017 levels, but “V”-ing nicely off the 2012 lows…

Source: Bloomberg

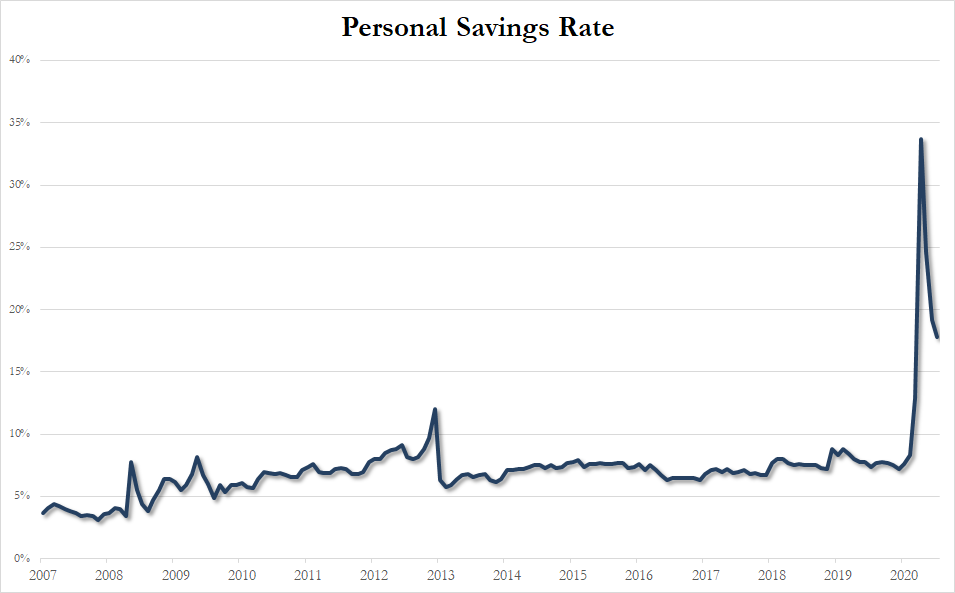

Sending the savings rate lower (from 19.2% to 17.8%)…

Finally we note that The Fed’s favorite inflation indicator – Core PCE Deflator – re-accelerated in July, but at 1.3% remains well below any old or new mandate-driven level…

Bear in mind that this data – from July – was before the big handouts all stopped!

via ZeroHedge News https://ift.tt/3hDgGtJ Tyler Durden

As the California attorney general pursues its lawsuit against these ride-sharing companies, to force them to comply immediately with the state’s virtual ban on using contractors as workers, the firms had announced last week that they would temporarily leave the state as they retool into smaller operations.

The courts gave them a last-minute reprieve, but their long-term plans here remain uncertain. Sadly, state officials had been intent on punishing these companies—even before voters have a say. At the very least, the state should have waited until the public decides on the matter in the Nov. 3 election via Proposition 22. That measure would carve out a contracting exemption for independent drivers and provide them with health-care and other benefits.

If voters reject Proposition 22, these groundbreaking services might really go away. Their crime? They’ve been too successful at serving consumers and providing flexible employment opportunities for hundreds of thousands of California workers. That has provoked the state’s politically muscular unions, which see a threat to their preferred work model—an antiquated system of inflexible 9-to-5 schedules, factories, offices and union shop stewards.

The unions can’t compete, so they must destroy what others have freely chosen. It reminds me of economist Walter Williams’ well-known quotation: “Prior to capitalism, the way people amassed great wealth was by looting, plundering and enslaving their fellow man. Capitalism made it possible to become wealthy by serving your fellow man.” These companies serve us, but the Legislature prefers looting and plunder.

I’m a slow adapter to technology, so I still recall my amazement when a friend introduced me to a cool alternative to slow, grimy, and pricey taxicabs. We were waiting to go to dinner while at a convention. Within minutes, an Uber driver showed up in a comfortable, clean, and late-model car, and inexpensively took us to our destination.

No big deal, right? But this simple system, which we now take for granted, is the result of amazing creativity, private investments, and voluntary arrangements. That’s how free markets work. Someone comes up with a better mousetrap and, as long as the government stays out of the way, the companies rise or fall based on their success attracting customers.

Think of how transportation services have improved lives. Elderly people have newfound mobility. They can easily get to doctors’ appointments and whatnot. Drivers deliver almost everything to our front door, from groceries to auto parts. After Austin, Texas, banned Uber and Lyft, drunken-driving arrests reportedly increased. As Williams noted, companies succeed by serving us.

I talk to drivers all the time—and they express satisfaction with their work arrangements. By the way, no one has forced them to take these jobs. The vast majority work limited hours, as they earn extra cash between other opportunities. Many independent workers of all types earn more piecing together various gigs than working only for one company.

We know what’s best for ourselves, even if Assemblywoman Lorena Gonzalez, the San Diego Democrat who authored the contracting-ban legislation (Assembly Bill 5), thinks she knows better. Her Twitter jabs at freelancers who have lost their jobs – they’re “not good jobs to begin with”—display an almost comical caricature of a “let them eat cake” legislator. Yet think about what happens if—or when—these services go away. Since January, when the law went into effect, companies have been eliminating bushel-loads of freelance jobs or shifting them to workers in other states.

Sorry, but one can’t create high-paid jobs by legislative fiat. The market does a remarkably good job of improving the lot of workers. It obviously has a better track record at doing this than the California Legislature. In the market economy, consumers come first—but workers’ fortunes rise in the process.

Look at Gonzalez’s home city of San Diego. As I’ve reported here before, prior to ride-sharing, residents were dependent on taxis. A 2013 report from the Center on Policy Initiatives found that “taxi drivers earn a median of less than $5 an hour” and “virtually no drivers have job-related health coverage or workers’ compensation insurance.”

Drivers spent their time paying off cab owners’ inflated permit fees—and had little chance of becoming owner-operators because government only issued a restricted number of “medallions.” By contrast, a recent study about ride-sharing in Seattle from Cornell University found Uber drivers earned an average of $23.25 an hour, which is close to the city’s median wage and is nearly 50 percent more than taxi-driver earnings.

Killing ride-sharing will not improve the plight of drivers. Still, the fundamental issue doesn’t center on worker benefits. It’s about the freedom to pioneer technologies and the ability of consumers to benefit from them. I don’t believe the future of any industry ought to be dependent on a popular vote, but at least California voters still have a chance to save these services.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/2Qx8vTV

via IFTTT

As the California attorney general pursues its lawsuit against these ride-sharing companies, to force them to comply immediately with the state’s virtual ban on using contractors as workers, the firms had announced last week that they would temporarily leave the state as they retool into smaller operations.

The courts gave them a last-minute reprieve, but their long-term plans here remain uncertain. Sadly, state officials had been intent on punishing these companies—even before voters have a say. At the very least, the state should have waited until the public decides on the matter in the Nov. 3 election via Proposition 22. That measure would carve out a contracting exemption for independent drivers and provide them with health-care and other benefits.

If voters reject Proposition 22, these groundbreaking services might really go away. Their crime? They’ve been too successful at serving consumers and providing flexible employment opportunities for hundreds of thousands of California workers. That has provoked the state’s politically muscular unions, which see a threat to their preferred work model—an antiquated system of inflexible 9-to-5 schedules, factories, offices and union shop stewards.

The unions can’t compete, so they must destroy what others have freely chosen. It reminds me of economist Walter Williams’ well-known quotation: “Prior to capitalism, the way people amassed great wealth was by looting, plundering and enslaving their fellow man. Capitalism made it possible to become wealthy by serving your fellow man.” These companies serve us, but the Legislature prefers looting and plunder.

I’m a slow adapter to technology, so I still recall my amazement when a friend introduced me to a cool alternative to slow, grimy, and pricey taxicabs. We were waiting to go to dinner while at a convention. Within minutes, an Uber driver showed up in a comfortable, clean, and late-model car, and inexpensively took us to our destination.

No big deal, right? But this simple system, which we now take for granted, is the result of amazing creativity, private investments, and voluntary arrangements. That’s how free markets work. Someone comes up with a better mousetrap and, as long as the government stays out of the way, the companies rise or fall based on their success attracting customers.

Think of how transportation services have improved lives. Elderly people have newfound mobility. They can easily get to doctors’ appointments and whatnot. Drivers deliver almost everything to our front door, from groceries to auto parts. After Austin, Texas, banned Uber and Lyft, drunken-driving arrests reportedly increased. As Williams noted, companies succeed by serving us.

I talk to drivers all the time—and they express satisfaction with their work arrangements. By the way, no one has forced them to take these jobs. The vast majority work limited hours, as they earn extra cash between other opportunities. Many independent workers of all types earn more piecing together various gigs than working only for one company.

We know what’s best for ourselves, even if Assemblywoman Lorena Gonzalez, the San Diego Democrat who authored the contracting-ban legislation (Assembly Bill 5), thinks she knows better. Her Twitter jabs at freelancers who have lost their jobs – they’re “not good jobs to begin with”—display an almost comical caricature of a “let them eat cake” legislator. Yet think about what happens if—or when—these services go away. Since January, when the law went into effect, companies have been eliminating bushel-loads of freelance jobs or shifting them to workers in other states.

Sorry, but one can’t create high-paid jobs by legislative fiat. The market does a remarkably good job of improving the lot of workers. It obviously has a better track record at doing this than the California Legislature. In the market economy, consumers come first—but workers’ fortunes rise in the process.

Look at Gonzalez’s home city of San Diego. As I’ve reported here before, prior to ride-sharing, residents were dependent on taxis. A 2013 report from the Center on Policy Initiatives found that “taxi drivers earn a median of less than $5 an hour” and “virtually no drivers have job-related health coverage or workers’ compensation insurance.”

Drivers spent their time paying off cab owners’ inflated permit fees—and had little chance of becoming owner-operators because government only issued a restricted number of “medallions.” By contrast, a recent study about ride-sharing in Seattle from Cornell University found Uber drivers earned an average of $23.25 an hour, which is close to the city’s median wage and is nearly 50 percent more than taxi-driver earnings.

Killing ride-sharing will not improve the plight of drivers. Still, the fundamental issue doesn’t center on worker benefits. It’s about the freedom to pioneer technologies and the ability of consumers to benefit from them. I don’t believe the future of any industry ought to be dependent on a popular vote, but at least California voters still have a chance to save these services.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/2Qx8vTV

via IFTTT

Top Beijing Official Warns: Chinese Consumers Will ‘Abandon’ iPhones If US Bans WeChat Tyler Durden

Fri, 08/28/2020 – 08:24

In a rare comment about potentially boycotting American products, China’s foreign ministry spokesman warned Friday if the Trump administration goes ahead with a ban on the popular messaging app WeChat, from mid-September on, then it would result in Chinese consumers ditching iPhones and other Apple products.

“If WeChat is banned, then there will be no reason why Chinese shall keep iPhone and apple products,” Foreign Ministry spokesman Zhao Lijan tweeted.

If WeChat is banned, then there will be no reason why Chinese shall keep iPhone and apple products. pic.twitter.com/qkKuMNQ87f

President Trump’s executive order banning WeChat in the coming weeks would not just stoke further tensions between both superpowers, but also could lead to a massive hit for the world’s most valuable company, Apple.

Lijan said, “many Chinese people are saying they may stop using iPhones if WeChat is banned in the U.S.” He accused Washington of “systematic economic bullying of non-US companies” by targeting the popular messaging app.

The comments of a top Chinese official addressing a potential boycott of American products, nevertheless, ones from Apple, sheds light on the spillover of tensions from the blame of the virus pandemic to lack of buying under the Phase One Trade deal to the rapid increase in military activity in the South China Sea.

T.F. International Securities’ Ming-Chi Kuo laid out in a note, the potential impact on Apple sales if a WeChat ban was seen. He said the hit would be absolutely devastating for Apple, resulting in a possible 25-30% annual decline in global phone shipments.

“Because WeChat has become a daily necessity in China, integrating functions such as messaging, payment, e-commerce, social networking, news reading, and productivity, if this is the case, we believe that Apple’s hardware product shipments in the Chinese market will decline significantly. We estimate that the annual iPhone shipments will be revised down by 25–30%, and the annual shipments of other Apple hardware devices, including AirPods, iPad, Apple Watch, and Mac, will be revised down by 15–25%,” Kuo said in an early August note.

Asia Times quoted Weibo users who said upon a WeChat ban – they would unanimously ditch their iPhones:

“I use Apple, but I also love my country,” one Weibo user said. “It’s not a conflict.”

“No matter how good Apple is, it’s just a phone. It can be replaced, but WeChat is different,” another user said. “Modern Chinese people will lose their soul if they leave WeChat, especially business people.”

While the Trump administration is gung ho about decoupling American and Chinese economies, the American Chamber of Commerce in Shanghai recently warned of an “enormous negative impact” on U.S. companies with international exposure to WeChat’s more than 1.2 billion active users if a ban was seen.

via ZeroHedge News https://ift.tt/32xHEgf Tyler Durden

Last week we put out a succinct mid-quarter update in which we highlighted 9 negative inputs into a tactical equity framework. This post builds upon that by calling out 7 rather conspicuous divergences that are developing in the financial markets.

The VIX index is rising while stocks are rising. Typically, implied volatility (what is measured by the VIX) tracks realized volatility. Realized volatility almost always falls when stocks rise.

Since mid-August, however, what we are seeing is realized volatility fall while implied volatility rises. It’s an odd configuration that suggests options investors are pricing in higher probability of a selloff than equity investors. The current divergence between these two series is by far the largest it’s been all year.

The headline S&P 500 index keeps going up, but on fewer and fewer participating stocks. Typically, breadth in the equity market tracks the price level of the headline index.

But that hasn’t been the case since mid-August. Since then, the S&P 500 has tacked on almost 100 points while Bloomberg’s cumulative breadth measure has fallen by 2%. Almost all of the rise in the S&P 500 has been due to a few large companies driving the gains. That usually isn’t a sustainable setup so we need to see breadth catch up for the correction risk to recede.

Small stocks are trending down while large stocks are at new highs. It’s not unusual for small stocks to outperform large stocks, but our antennae are piqued when small stocks are falling while the larger stocks are handily making new highs.

The US dollar has stopped falling against developed market crosses. The US dollar has moved in lock step with the S&P 500 since the March low. That is, the USD has fallen while stocks have risen.

A falling USD is a consequence of stimulus and reflation of the economy. But, since August 18th, the USD has stopped rising all together. This suggests there may be emerging tightness in the liquidity environment. Such a scenario would be disadvantageous for stocks if it persists.

Emerging market currencies are falling again. EM currencies are excellent indicators of the liquidity environment. When they fall, it suggests liquidity is tightening.

EM currencies have been falling since June and are contradicting the recent breakout of large US stocks.

High yield corporate credit spreads aren’t keeping up with stocks anymore. HY spreads have tracked stocks tightly all year. But, those spreads peaked out back in early August as the S&P 500 accelerated higher.

This suggests credit investors are pricing in less future improvement in the economy than are equity investors. We need to keep our eye on this indicator because the correction risk will get even stronger if HY spreads break back above 5%.

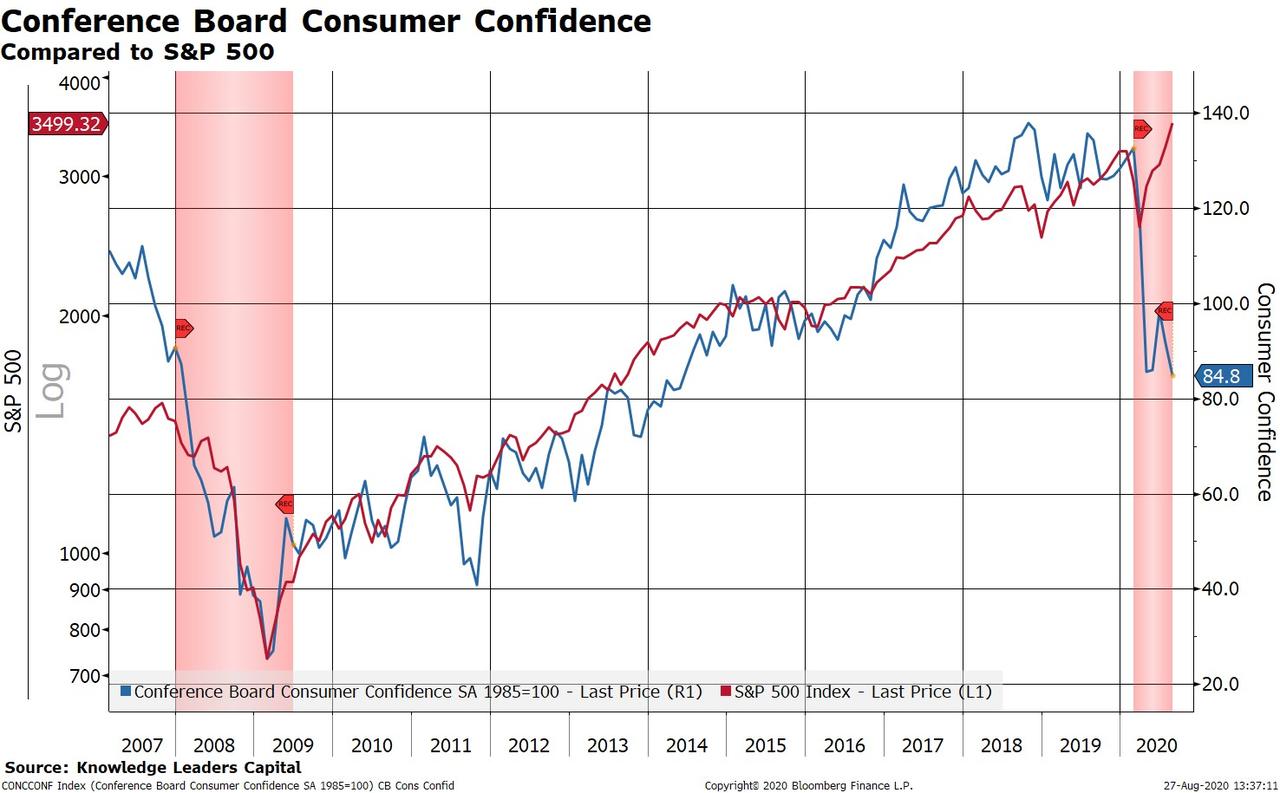

Consumer confidence is outright falling while US large stocks make new highs. Consumer confidence is highly correlated with equity prices for obvious reasons. But recently consumer confidence has taken a nosedive.

This is in part due to reduced unemployment benefit levels since the end of July combined with still high unemployment.

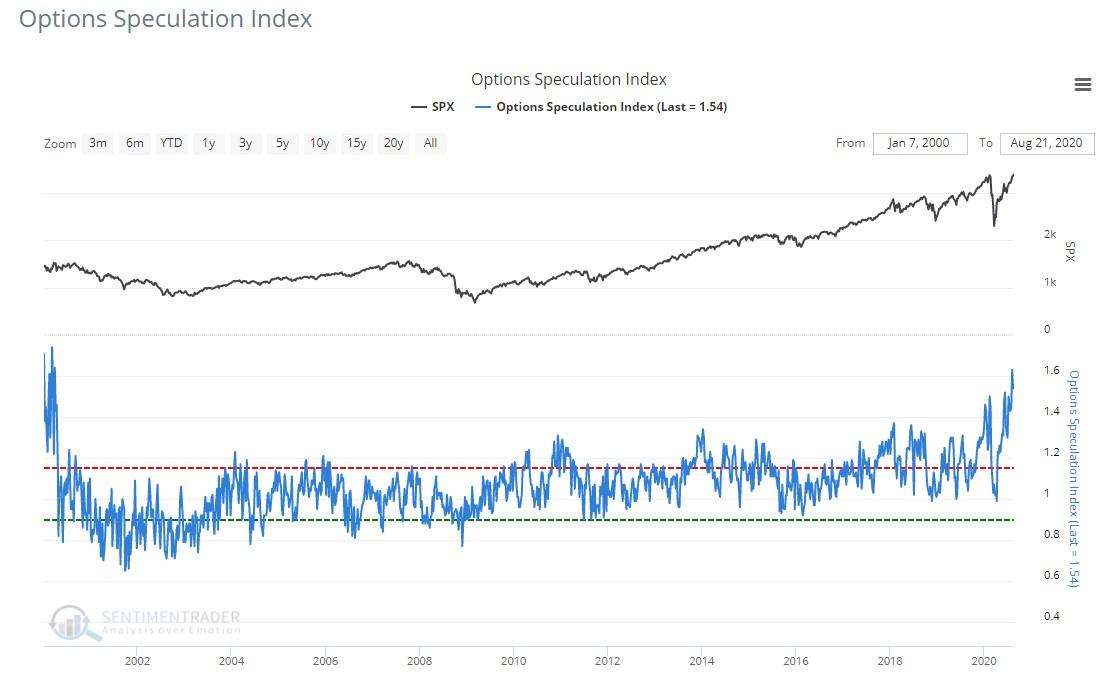

Bonus Chart

And then there is this. The option speculation index compares bullish and bearish options trades placed at the market open. Currently, option activity is skewed as heavily toward bullish strategies (buying calls or selling puts) as it was during the last days of the dotcom blowup.

To be clear, a repeat of that scenario seems rather unlikely, perhaps just as unlikely as option speculation remaining at these levels.

via ZeroHedge News https://ift.tt/34HXdEv Tyler Durden

S&P Futures Hit Record Above 3,500 As Dollar Tumbles To 27 Month Low Tyler Durden

Fri, 08/28/2020 – 07:53

After sprinting out of the gates and surging as high as 3,509 during Trump’s acceptance speech, the E-Mini S&P future faded some of its gains even as it remained green for a seventh straight day as investors worried about a lack of detail in the U.S. Federal Reserve’s policy shift which assured super low interest rates for years to come. Despite continued US levitation European and Asian markets were mixed, while Japanese markets were roiled as Prime Minister Shinzo Abe resigned for health reasons (again) sending the Yen surging. The dollar was headed for its worst daily decline in a month.

Futures initially jolted higher as investors bet interest rates would remain low for longer and more stimulus was likely. But markets have since been choppy, with some traders disappointed that the Fed did not reveal more details about how the new framework will work or provide any clues as to what it will do at its next policy meeting.

“It’s not so much about what to do about inflation when it comes but about getting inflation above target. The challenge is to get inflation up to target and not very much was said about that,” said Colin Asher, a senior economist at Mizuho.

The S&P 500 and the Nasdaq are on track for their fifth consecutive week of gains, but the Dow is still about 3.6% from its February all-time high. The Fed on Thursday unveiled a new policy aim for 2% inflation on average so that too low a pace would be followed by an effort to lift inflation “moderately above 2% for some time” and to restore the economy to full employment. In the previous session, the Dow briefly turned positive on the year, while the S&P 500 closed at a record level even as the U.S. economy struggles to recover, forcing the Fed to adopt an unprecedented policy of accepting inflation overshoots for an unknown period of time.

In further proof that technology companies are booming in the pandemic, business software provider Workday jumped 11.2% in premarket trading after raising its annual subscription forecast. Dell Technologies gained 4.5% after reporting quarterly profit that beat expectations as remote working and online learning boosted demand for its notebooks and software products. Cosmetics retailer Ulta Beauty Inc ULTA.N jumped 15.1% after posting quarterly profit ahead of market expectations.

The Euro Stoxx 50 recovered from earlier losses and was last up 0.03%, while Germany’s DAX slid 0.49%. Britain’s FTSE 100 was 0.4% higher.

Earlier, Asian stocks were little changed, with communications falling and finance rising, after falling in the last session. Asian shares outside of Japan limped higher, with the MSCI’s broadest index of Asia-Pacific shares outside Japan gaining 0.19%. Markets in the region were mixed, with Shanghai Composite and Singapore’s Straits Times Index rising, and Australia’s S&P/ASX 200 and Japan’s Topix Index falling. The Topix declined 0.7%, with TerraSky and Airtrip falling the most. Japanese shares dropped, with the Nikkei 225 down 1.4%. Abe resigned on Friday because of a chronic health condition, saying he would stay as prime minister until a new leader was appointed.

“This is a negative for Japanese stocks because it raises questions about what polices come next. We do see the familiar pattern of falling stocks pushing up the yen,” said Junichi Ishikawa, senior foreign exchange strategist at IG Securities in Tokyo. The yen, seen as a safe-haven currency to buy in times of uncertainty, surged to 105.32, gaining 150 pips on the session.

The Shanghai Composite Index rose 1.6%, with Western Superconducting and Whirlpool China posting the biggest advances.

In rates, Treasuries pared overnight losses as the US session gets underway after bear-steepening during Asia session, extending the response to Fed Chair Powell’s comments Thursday. A selloff in Aussie bonds weighed initially, with impact fading during European morning as U.S. stock futures pulled back from record highs. Treasuries remain cheaper by more than 1bp at long end while yields out to 10-year are richer on the day; bunds lag by ~1bp while gilts keep pace. The 5s30s curve steepened as much as 5.5bp to 125bp, highest since June 5 when it reached 128.5bp, steepest since 2006; 2s10s peaked at 62.5bp, steepest since June 9.

In FX, the dollar slumped 0.6% against a basket of other currencies, dropped to a more than two year low. The greenback has fallen sharply since June as many analysts are predicting more pain ahead given U.S. rates are likely to stay low for longer and the political uncertainty before the U.S. presidential election in November.

Residual or more month end rebalancing could be a factor behind the renewed Greenback weakness, though the aforementioned Yen revival has certainly contributed to the dollar reversing further from Thursday’s post-Fed chair policy revelation recovery highs to lower lows. The DXY index is now 100+ ticks down at 92.279 and the ytd trough looms (92.124) amidst broad and increasingly heavy losses across the board, as US stock futures continue to rally or consolidate near record peaks. The euro seized on the dollar’s weakness to gallop another 0.7% higher and was last at $1.1905, close to a more than two-year high it recently touched. The yen soared to 105.35 yen per dollar on news of Abe’s resignation.

On the back of dollar weakness, China’s yuan was on pace for a fifth weekly advance, the longest run since November last year, as the greenback stays weak. The currency traded onshore has risen 0.8% over the past five sessions, taking the climb since July 24 to 2.2%. The yuan jumped as much as 0.48% to 6.8612 a dollar on Friday to trade at its highest since January.

In commodities, Crude oil prices dipped as a massive storm raced inland past the heart of the U.S. oil industry in Louisiana and Texas without causing any widespread damage to refineries. Brent crude fell 0.47% to $44.88 a barrel. U.S. West Texas Intermediate crude dropped 0.49% to $42.83 per barrel. Gold prices bounced 1%, with the spot price at $1,949 an ounce. The precious metal tends to perform well when the dollar is weak and the U.S. central bank sends a dovish message on the future path of interest rates.

Expected data include wholesale inventories and personal income and spending. Big Lots is reporting earnings.

Market Snapshot

S&P 500 futures up 0.4% to 3,500.00

MXAP up 0.05% to 173.56

MXAPJ up 0.2% to 577.53

Nikkei down 1.4% to 22,882.65

Topix down 0.7% to 1,604.87

Hang Seng Index up 0.6% to 25,422.06

Shanghai Composite up 1.6% to 3,403.81

STOXX Europe 600 down 0.3% to 369.59

German 10Y yield rose 2.1 bps to -0.386%

Euro up 0.8% to $1.1917

Italian 10Y yield rose 0.3 bps to 0.894%

Spanish 10Y yield rose 0.4 bps to 0.393%

Sensex up 0.9% to 39,453.11

Australia S&P/ASX 200 down 0.9% to 6,073.81

Kospi up 0.4% to 2,353.80

Brent futures down 0.2% to $44.98/bbl

Gold spot up 1.4% to $1,956.80

U.S. Dollar Index down 0.7% to 92.35

Top Overnight News from Bloomberg

Abe announced he plans to step down for health reasons, after eight years at the head of Japan

The Jackson Hole symposium is set to continue after Fed Chairman Powell’s speech on Thursday shook the dollar and longer-dated treasuries overnight

The number of Americans killed by Covid-19 exceeded 180,000, while the resurgence continues in Europe, with Germany reporting a daily increase in cases close to a four-month high

Snapshot of key global markets courtesy of NewsSquawk:

Asian bourses eventually traded mixed as markets digested the Fed’s shift to an average inflation targeting framework, which briefly lifted the S&P 500 to the 3500 level for the first time ever and the Nasdaq to a fresh record intraday high during Wall Street hours. Some of the moves were then reversed as the dust settled and the recent big tech rally stalled – which dragged the Nasdaq into the red, although US equity futures have since caught a second wind overnight with E-mini S&P taking its turn to breach the 3500 milestone. As such, Nikkei 225 (-1.4%) was initially lifted as exporters benefitted from currency weakness, but plunged heading into the cash close amid reports that Japanese PM Abe is planning to resign due to worsening health conditions, while the Hang Seng (+0.6%) and Shanghai Comp. (+1.6%) were supported after this week’s liquidity efforts resulted to a net weekly injection of CNY 200bln and amid a deluge of earnings including blue-chip names PetroChina, and China Vanke, whose shares all traded higher despite posting varied results. Conversely, ASX 200 (-0.9%) bucked the trend as weakness in Australia’s tech and miners spearheaded the declines in the index, with sentiment not helped by the continued deterioration in ties with its largest trading partner China after Canberra’s move to veto the Belt & Road Initiative agreement, while China also suspended imports of beef from Australia’s John Dee after finding a banned substance. Finally, 10yr JGBs were lower amid spill-over selling from USTs which were heavily pressured as participants contemplated over the Fed’s tolerance for overshooting inflation, to push the US 10yr yield to its highest since mid-June, while the unprecedented levels seen in the E-mini S&P and a tepid BoJ Rinban announcement added to the dampened mood for bonds.

Top Asian News

New Zealand Deploys Spy Agency as Hackers Hit Stock Market

Goldman Pays Malaysia $2.5 Billion; Funds to Repay 1MDB Debt

Xiaomi’s Stock Surge a Big Reversal After Post-IPO Struggles

SoftBank Group to Sell $12.5 Billion of Wireless Unit Stock

European stocks see choppy price action, although bourses ultimately trade mixed/subdued (Euro Stoxx 50 -0.5%), as the region came under pressure after the cash open and subsequently nursed some of this downside – with little initial follow-through for European bourses from surprise reports that Japanese PM Abe will be stepping down from his position due to ill health. Participants must be wary of month-end rebalancing, although UBS suggests that this August flows are likely to be considerably less eventful than in July; “This month has seen lower levels of dispersion in global equity markets so far, with the model showing only CAD and NZD expected to see tangible buying pressure at month-end as local equity markets have underperformed SPX.” Overall, Core European bourses see little by way of under/outperformers, although peripheries, i.e. Spain’s IBEX (+0.7%) and Italy’s FTSE MIB (+0.2%) stand as the winners aided by their exposures to the financial sector – which is seeing clear outperformance in Europe amid the high yield environment. Overall, European sectors are mostly lower with no clear risk profile to be extrapolated, although tech resides as the laggard following a week of firm gains. In terms of individual movers; Bayer (-3.3%) sees losses after a judge overseeing the Roundup dispute remarks that they may consider lifting the ban on litigation proceedings as a consumer lawyer says Bayer are not abiding by the USD 11bln settlement, according to sources. Enel (+0.2%) is propped up by reports that Macquarie is reportedly working on a binding offer for the Co’s 50% stake in Open Fiber, according to Il Sole 24.

Top European News

European Equities Set for Pain if Euro’s Advance Nears $1.30

Apartment Prices Surge in Russia, Raising Fears of a Bubble

World’s Biggest Wealth Fund to Publish All Vote Plans by 2021

Sweden’s Historic Crisis Plan Exposes Central Bank’s Limits

In FX, the yen was in focus after Japanese PM Abe announced that he will stand down before his official term ends due to a recurring health problem. In response, Japanese stocks and bonds have fallen on concerns that his brand of expansive policy may not be replicated by the next leader, while the Yen has rebounded firmly with Usd/Jpy sub-106.00 ansd testing support/underlying bids ahead of 105.50 from almost a big figure above and the headline pair decisively through decent option expiry interest between 106.50-60 (1 bn) in advance of the NY cut.

DXY – Residual or more month end rebalancing could be a factor behind the renewed Greenback weakness, though the aforementioned Yen revival has certainly contributed to the Buck reversing further from Thursday’s post-Fed chair policy revelation recovery highs to lower lows. Indeed, the index is now 100+ ticks down at 92.279 and the ytd trough looms (92.124) amidst broad and increasingly heavy losses across the board, as US stock futures continue to rally or consolidate near record peaks. Ahead, PCE price metrics may well take on greater importance given the switch to average inflation targeting with flexibility, but from a more timely activity perspective Chicago PMI and any big revision to final Michigan sentiment will also be worth watching.

AUD/NZD/EUR/GBP/CHF/CAD – Understandably, all benefiting from their US rival’s demise, albeit to varying degrees. The Aussie has breached 0.7300 and the Kiwi is edging closer to 0.6700, while the Euro has rotated over 360 degrees again only this time from the low 1.1800 area to 1.1900+. Similarly, Cable is nudging nearer 1.3300 from under 1.3200 at one stage and setting minor new 2020 highs in the process, regardless of latest negative sounding Brexit news like senior EU sources claiming a 2 week ultimatum for UK PM Johnson to salvage post-transition trade and security negotiations. Elsewhere, the Franc is eyeing 0.9000 compared to 0.9100 at the other extreme following a significantly better than forecast Swiss KOF leading index and the Loonie has pared more recent declines to trade circa 1.3060 in the run up to Canadian Q2 GDP.

SCANDI/EM – The Sek and Nok have resumed bullish trajectories regardless of Euro strength elsewhere, with the former encouraged by Swedish Q2 GDP contracting a tad less than envisaged, while EM currencies are taking advantage of Usd depreciation almost across the board, as the Zar recovers alongside Gold and even the Try regroups with some assistance from an improvement in Turkish consumer sentiment.

In commodites, WTI and Brent front month futures trade relatively flat in early European hours, with some earlier downside coinciding with losses in stocks in what seems to be a sentiment-driven move; albeit, the magnitude of the price action across the oil complex has been minimal. Focus has now shifted away from developments in the Gulf of Mexico as Hurricane Laura is downgraded to a Tropical Storm and production starts coming back online. Aside from that, news flow for the complex has remained light, with participants eyeing the weekly Baker Hughes Rig Count as the only crude-related scheduled release. WTI October trades on either side of USD 43/bbl, contained within a tight USD 0.3/bbl range, whilst its Brent counterpart similarly oscillates around USD 45/bbl having printed a current 0.4/bbl range. Elsewhere, spot gold and silver gain impetus from the JPY-led USD declines. The yellow metal has reclaimed a USD 1950+/oz status (vs. low 1923/oz), whilst silver eyes USD 27.50/oz to the upside from an overnight base of USD 26.82/oz. Meanwhile, Shanghai copper prices rose 1% and London prices remain supported by the weaker Dollar. Finally, Dalian iron ore futures closed higher by 1.4% amid a softer Buck alongside expectations for firm demand from the steel industry.

8:30am: Retail Inventories MoM, est. -1.05%, prior -2.6%; Wholesale Inventories MoM, est. -0.85%, prior -1.4%

8:30am: Personal Income, est. -0.25%, prior -1.1%; Personal Spending, est. 1.6%, prior 5.6%

8:30am: Real Personal Spending, est. 1.3%, prior 5.2%

8:30am: PCE Deflator MoM, est. 0.4%, prior 0.4%; PCE Deflator YoY, est. 1.0%, prior 0.8%

PCE Core Deflator YoY, est. 1.23%, prior 0.9%; PCE Core Deflator MoM, est. 0.5%, prior 0.2%

9:45am: MNI Chicago PMI, est. 52.6, prior 51.9

10am: U. of Mich. Sentiment, est. 72.8, prior 72.8; Current Conditions, est. 82.4, prior 82.5; Expectations, est. 66, prior 66.5

DB’s Henry Allen concludes the overnight wrap

Happy Friday and hope you’ve had a good week. Jim’s taken another day off ahead of the UK bank holiday on Monday, so I’m back again for the second time this week. In fact, with Craig about to go on paternity leave, there’s the chance we might get to talk even more over the coming months. Whether that’s good news or bad I’ll let you decide, but from what Jim was saying I figured that the best route out of this was having a baby. Given the parenting manual I read each day in this email however, I can’t say he’s made it sound attractive.

Speaking of manuals, the Federal Reserve released some changes to their own one yesterday as the US central bank announced a revision to their longer-run goals and monetary policy strategy. In terms of the two big changes that stand out, the first is that the FOMC will now look to achieve an inflation rate averaging 2% over time, so that if there’s a period as in recent years when inflation has undershot the target, policy can then aim for an inflation rate above the 2% target for the period afterwards. The other main change is with regard to the Fed’s maximum employment objective, where the new statement says that policy will now be informed by the FOMC’s “assessments of the shortfalls of employment from its maximum level”, as opposed to “deviations from its maximum level” as it previously said. That reflects an evolution of their view in recent years as the unemployment rate has fallen below the levels they had previously estimated it could without generating above-target inflation, particularly as low-income communities were among the biggest beneficiaries of the unemployment rate falling to such low levels.

Our US economists write that both of these dovish revisions were in line with their expectations. However, the release of the results now opens the door wider than previously to the chance of a modification of the FOMC’s rates guidance and balance sheet policy at the September meeting. Their view is that the Committee will reveal enhanced forward guidance next month and adjustments to their asset purchases, most likely in the form of an extension of duration. You can find their piece here for those wanting more depth.

In terms of the market reaction, Treasuries whipsawed between gains and losses after the announcement, with 10yr yields falling to an intraday low of 0.648% in the immediate aftermath. However, we then got a major reversal that saw yields move up by over 10bps to end of the session at a 2-month high of 0.752%, ending the day +6.4bps higher, and this morning they’re up a further +1.8bps at 0.770%. There was also a notable steepening of the yield curve, with the 2s10s curve up +5.6bps at a 2-month high.

Looking at other asset classes, the dollar saw some dramatic moves of its own as it fell to an intraday low of -0.63% following Powell’s announcement, before paring back its losses to close down -0.01%, while gold shed -1.28%. US equities continued to power forward however, and in a line we’ve repeated every day this week, the S&P 500 hit another record high as the index advanced +0.17%, even managing to surpass the 3,500 mark at one point in trading. That said, tech stocks unusually lagged yesterday, with the NASDAQ shedding -0.34%, but the S&P 500’s banks rose +2.50% as they benefited from Powell’s comments.

Updating our screens overnight, there’s every chance we could see yet another rise in the S&P 500 today, with futures up another +0.60% this morning. Meanwhile in Asia, equity markets have seen further advances, with the Nikkei (+0.52%), the Hang Seng (+0.87%), the Shanghai Comp (+0.51%) and the KOSPI (+0.80%) all moving higher. The strong move for the KOSPI came as the South Korean Prime Minister announced that the level 2 social distancing rules would be extended for another week, but stopped short of moving up to the stricter level 3 as the current flareup in new infections continues.

In the political sphere, there were also some further headlines from President Trump’s speech to the Republican National Convention, where he formally accepted his party’s nomination for president. Trump made a number of second-term pledges, including further tax cuts, the creation of 10m jobs in 10 months, as well as ending “our reliance on China”. Opinion polls continue to show Trump lagging behind Democratic candidate Joe Biden however, with the FiveThirtyEight polling average currently showing Biden with an 8.4pt lead over Trump.

With the plethora of headlines yesterday, the coronavirus got somewhat less attention than usual from investors, but the series of negative developments out of Europe continued. In terms of the numbers, multiple countries saw new cases at their highest levels in months, with Spain reporting a 4-month high of 3,781, Italy reporting a 3-month high 1,411, and the UK reported a 2-month high of 1,522. In France, where cases have also been rising recently, it was announced that masks would become compulsory throughout Paris from this morning in order to stem the spread, and comes as the country reported 6,111 cases in the most recent 24 hour period, in the worst day since late March. So definitely a situation worth keeping an eye on in the coming days in case further restrictions are imposed.

Amidst rising coronavirus cases, European equities took a rather different path to the US, with the STOXX 600 down -0.64%, as other European bourses including the DAX (-0.71%), the CAC 40 (-0.64%) and the FTSE 100 (-0.75%) also moved lower. For sovereign bonds however, it was a similar picture to the US as they pared back earlier gains to lose ground on the day. By the close 10yr bunds yields had risen +1.0bps, as they reached their highest level in nearly 2 months.

Over in the US, Hurricane Laura hit the coast of Louisiana yesterday with winds just over 240kmph, matching a record set in 1856. Thankfully the storm lost more than half of its power by midday and was downgraded down from hurricane status to tropical storm, but by that time it had caused major flooding throughout the region. The impacted area contains a number of chemical and liquid natural gas producers, though Brent crude (-1.21%) and WTI (-0.81%) oil prices fell back yesterday as the damage wasn’t as bad as some had anticipated. In our Chart of the Day yesterday, we looked at 170 years of hurricane data, and showed how this Atlantic hurricane season could end up rivalling the most severe on record in 2005, which included Hurricane Katrina. The 170 year average of named storms is just below 10 per season, however in the last 25 years we have only seen 3 years with fewer than 10 and an annual average of 15. The Atlantic has already seen 13 such storms and 5-13 all arrived at the earliest point in any year. See the link here for more.

Finally, in terms of yesterday’s data, the weekly initial jobless claims came in at 1.006m (vs. 1m expected) for the week ending August 22, which represented a fall from the prior week’s 1.104m but was still higher than the 971k the week before that. Meanwhile the continuing claims number for the week ending August 15 fell to a post-pandemic low of 14.535m, though this was also above the 14.4m expected. In somewhat better news, the Q2 contraction in GDP was revised to a shallower annualised decline of -31.7% (vs. -32.9% initial estimate), while pending home sales in July were up +5.9% (vs. +2.0% expected) to reach their highest level since 2005.

To the day ahead now, and the Jackson Hole symposium wraps up, with today’s proceedings including a speech from Bank of England Governor Bailey. Otherwise there are a number of data releases, including the preliminary French CPI reading for August and the final Q2 GDP reading. Meanwhile the European Commission will be releasing their final consumer confidence reading for August and Canada will be releasing their own GDP print for June. From the US, we’ll get July data on personal income and personal spending, along with the final University of Michigan sentiment reading for August, the MNI Chicago PMI for August and preliminary wholesale inventories for July.

via ZeroHedge News https://ift.tt/3jm7ZV9 Tyler Durden

{kind=link}

{kind=link}