Drought, Windstorm Plunge Iowa’s Corn Industry Into Chaos Tyler Durden

Sun, 08/30/2020 – 12:55

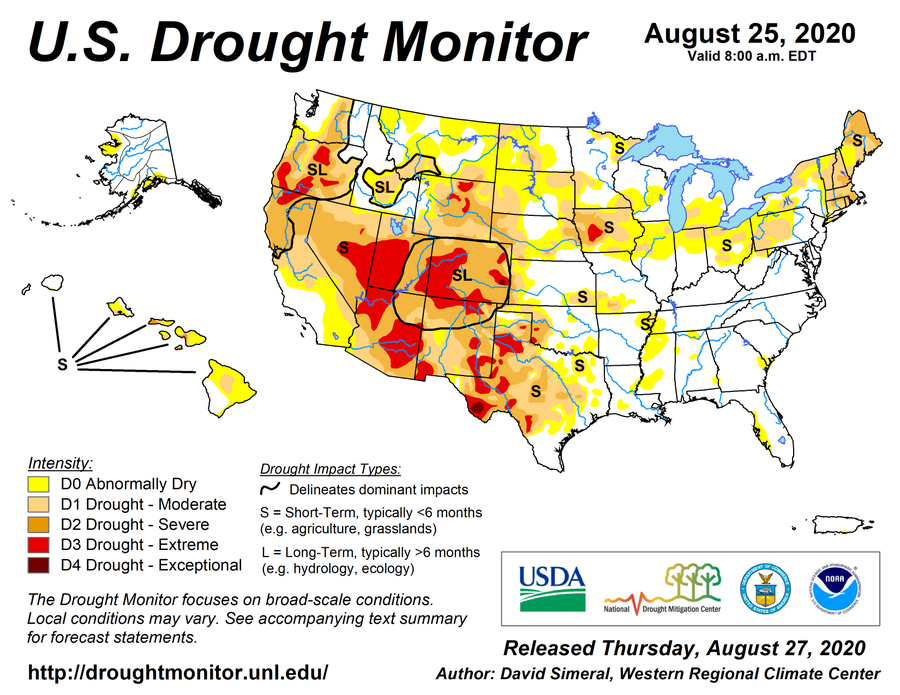

A “megadrought” could be forming across the West, parts of the Midwest, and in Texas, as the risks of a 1930s Dust Bowl-style event remain elevated.

The latest US Drought Monitor map shows nearly a third of the country is experiencing “severe drought” to “extreme drought” conditions.

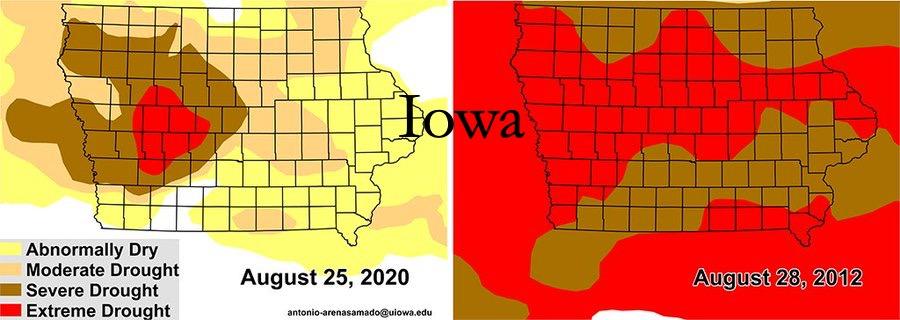

The lack of precipitation is so concerning that Iowa Secretary of Agriculture Mike Naig warned Friday that his state is facing the worst drought since September 2013.

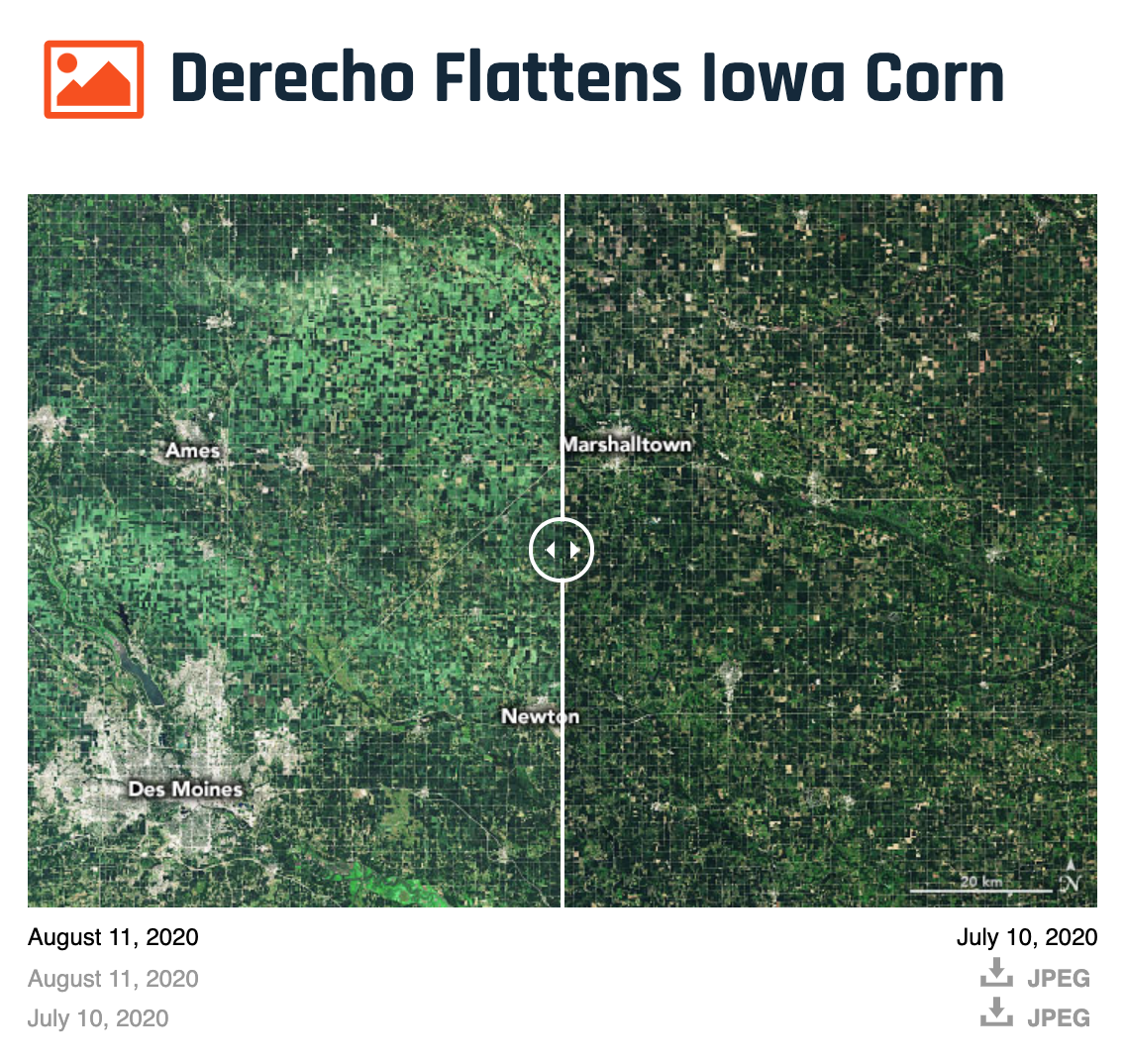

The drought in Iowa has caused severe headaches for farmers ahead of harvest, following high winds that flattened cornfields and destroyed silos in early August.

Iowa, the biggest US corn-producing state, is facing lower crop yields and deteriorating grain quality due to the recent volatility in the weather. This comes at an inopportune time as China increases purchases of US farm goods.

“The challenge here, and what’s unique, is that we’re dealing with adverse weather conditions over such a wide area in the state of Iowa,” Naig said.

He said, “this is the largest area of coverage of multiple problems that I’ve seen,” adding that crop yields could be much lower than estimates from months back.

Reuters noted the powerful windstorm on August 10, impacted 14 million crop acres, or about 57% of the state’s farms.

“We are starting to hear of some of those fields being declared a total loss and seeing farmers out destroying that crop,” Naig said.

US #Corn conditions down 5% on the week to 64% G/E

IOWA corn conditions down 9% on the week to 50% G/E… and now down 19% since the #derecho wind event

A confluence of events, in a short period, from drought to windstorm, has negatively impacted Iowa’s crop yield – as far as CBoT corn futures, well, they still remain on a low, following a bear market, or about a 23% drop post-signing of the Phase One Trade Deal with China in January.

Without the drought and windstorm, Iowa’s crop was forecasted to be large – further corn sales to China could push prices higher.

via ZeroHedge News https://ift.tt/2QErsUQ Tyler Durden

As an American, most of us strongly support the concept of peaceful protests. However, when things turn violent, when property gets destroyed, when buildings and cars are set on fire, and when businesses are looted, rational people can agree that this is wrong.

Unfortunately, a whole bunch of irrational people are being given microphones and they’re trying to tell us all why looting is not just okay, but actually awesome.

Looting is okay because it’s “reparations”

First, there was the woman who spoke after the Magnificent Mile in Chicago was looted so ferociously that Mayor Lori Lightfoot pulled the drawbridge open to keep people out of the downtown area. I recently wrote:

According to a Black Lives Matter activist and organizer, Ariel Atkins, it was just “reparations.” Atkins believes that anything the looters wish to damage or steal is owed to them. She made the radical statement at a solidarity rally in front of a Chicago police station, where people were gathered to support those who had been arrested.

“I don’t care if somebody decides to loot a Gucci’s or a Macy’s or a Nike because that makes sure that that person eats. That makes sure that that person has clothes,” Ariel Atkins said at a rally outside the South Loop police station Monday, local outlets reported.

“That’s a reparation,” Atkins said. “Anything they want to take, take it because these businesses have insurance.” (source)

At a time when more people than ever in the United States were willing to get on board and protest police brutality and racial violence, entitled statements like the one made by Atkins have served to return us to a place of absolute division. (source)

Atkin’s statement was made at a solidarity rally in front of a Chicago police station where people were gathered to support those who had been arrested for pillaging the Windy City.

Looting is okay if they “need” the item.

According to a document obtained by Red State News, Diana Becton, the district attorney of Contra Costa County, California, has changed up how looters are charged during a state of emergency.

Theft Offenses Committed During State of Emergency (PC 463)

In order to promote consistent and equitable filing practices the follow[ing] analysis is to be applied when giving consideration to filing of PC 463 (Looting):

1. Was this theft offense substantially motivated by the state of emergency, or simply a theft offense which occurred contemporaneous to the declared state of emergency?

a. Factors to consider in making this determination:

i. Was the target business open or closed to the public during the state of emergency?

ii. What was the manner and means by which the suspect gained entry to the business?

iii. What was the nature/quantity/value of the goods targeted?

iv. Was the theft committed for financial gain or personal need?

v. Is there an articulable reason why another statute wouldn’t adequately address the particular incident? (source)

Oh. Well. If you need those shoes and purses, then it’s totally different.

And yes, before the barrage of comments, I know that Red State News is biased. So is CNN. So is the New York Post. They’re all biased. If I could only use unbiased sources, I’d have maybe 3 articles on current events on this website. If you want to hear directly from District Attorney Becton, you can check out her opinion piece on Politico right here.

Rioting and looting are okay because they’re “joyous and liberatory”

Vicky Osterweil is the author of the book, In Defense of Looting. I’m sure it’s a super nice book despite that misleading picture of a crowbar on the cover.

Osterweil landed an interview with NPR to tout her opus and first provided a definition.

When I use the word looting, I mean the mass expropriation of property, mass shoplifting during a moment of upheaval or riot. That’s the thing I’m defending. I’m not defending any situation in which property is stolen by force. It’s not a home invasion, either. It’s about a certain kind of action that’s taken during protests and riots…

…It tends to be an attack on a business, a commercial space, maybe a government building—taking those things that would otherwise be commodified and controlled and sharing them for free. (source)

Then she continued to laud looting, almost poetically explaining the “number of important things” that looting does. (Emphasis mine)

It gets people what they need for free immediately, which means that they are capable of living and reproducing their lives without having to rely on jobs or a wage—which, during COVID times, is widely unreliable or, particularly in these communities is often not available, or it comes at great risk. That’s looting’s most basic tactical power as a political mode of action.

It also attacks the very way in which food and things are distributed. It attacks the idea of property, and it attacks the idea that in order for someone to have a roof over their head or have a meal ticket, they have to work for a boss, in order to buy things that people just like them somewhere else in the world had to make under the same conditions. It points to the way in which that’s unjust. And the reason that the world is organized that way, obviously, is for the profit of the people who own the stores and the factories. So you get to the heart of that property relation, and demonstrate that without police and without state oppression, we can have things for free…

…Looting strikes at the heart of property, of whiteness and of the police. It gets to the very root of the way those three things are interconnected. And also it provides people with an imaginative sense of freedom and pleasure and helps them imagine a world that could be. And I think that’s a part of it that doesn’t really get talked about—that riots and looting are experienced as sort of joyous and liberatory. (source)

And also, if you’re worried about violence, don’t be as long as you don’t “feel” violent. (Emphasis NPR’s)

Ultimately, what nonviolence ends up meaning is that the activist doesn’t do anything that makes them feel violent. And I think getting free is messier than that. We have to be willing to do things that scare us and that we wouldn’t do in normal, “peaceful” times, because we need to get free. (source)

I suspect if you are aggressively defending your hard-earned property against looters, folks like Vicky Osterweil won’t give two hoots whether you felt violent or not.

If looting continues to be considered acceptable, okay, or even awesome, it’s not just going to continue – it’s going to increase. Our country’s economy has already been devasted by COVID and the subsequent shutdowns. Imagine being a small business owner who just managed to reopen your shop or restaurant, only to have your windows smashed in, your property stolen, and your fixtures destroyed by an entitled mob. While it’s great that riot damage is often covered by insurance, who’s going to cover your massively increased premiums when your policy renews? If you aren’t driven out of business now, you might be when that bill comes in.

Not only are businesses being forced to board up their windows and close, they’re going to have difficulty doing business in the longterm due to these looters.

Looting is NOT okay under these kinds of circumstances. As preppers, we talk sometimes about looting and scavenging. But that is something which would take place when no further business is likely to occur due to a systemic breakdown. This is something entirely different.

What happens when more business owners decide that if the police aren’t going to protect their property they’ll protect it themselves? What happens when they take away the “joyousness” of looting? What happens when the rational people of the United States of America say, “That’s enough” and back it up?

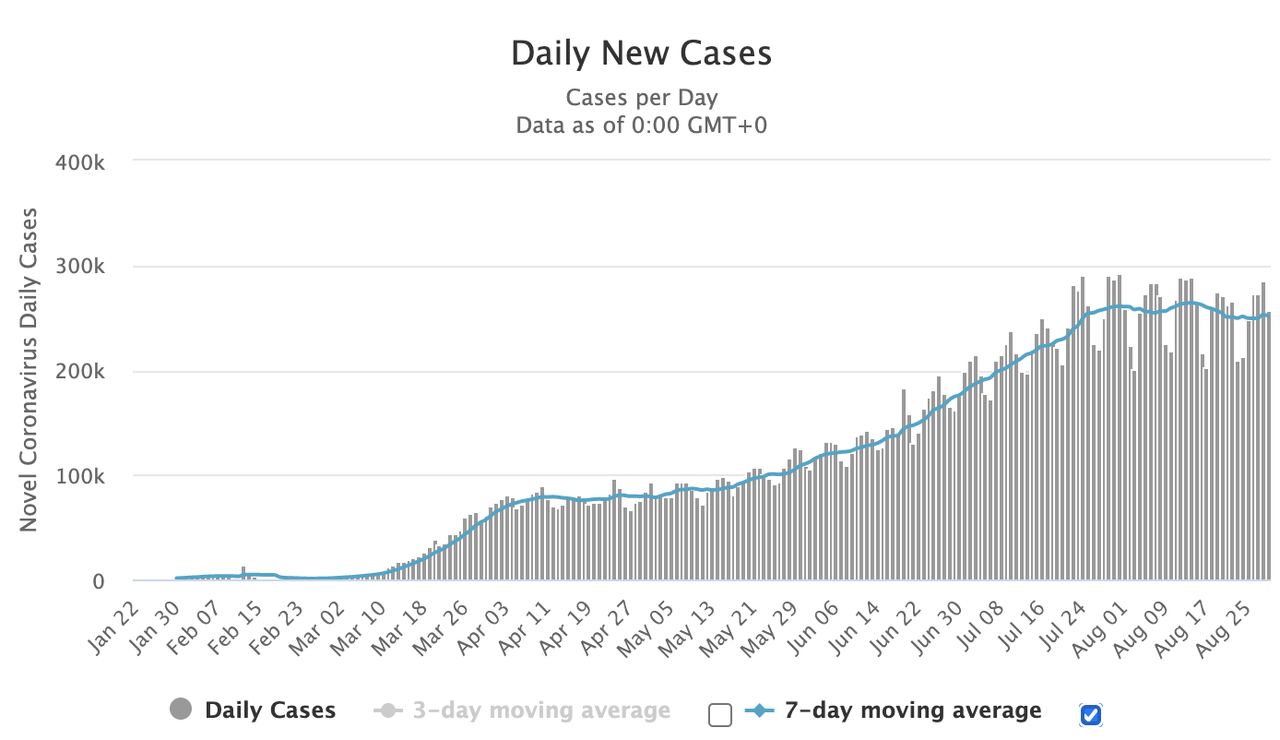

World Passes 25 Million Confirmed COVID-19 Cases: Live Updates Tyler Durden

Sun, 08/30/2020 – 12:14

Summary:

Global cases top 25 million

Deaths top 840,000

FDA director says vaccine can be fast-tracked

Dr. Fauci says vaccines could be proved ‘safe and effective’ by November

India tops 3.5 million cases

* * *

By mid-morning on Sunday in the US, the number of confirmed cases reported worldwide surpassed 25 million, a psychologically important milestone, even though millions more cases have likely gone undiagnosed.

Deaths, meanwhile, have topped 840,000.

In other news, Dr. Stephen Hahn, the FDA chief who caught flack, then apologized, for granting emergency-use approval to a blood plasma-focused COVID-19 treatment favored by President Trump, told the FT that he would be willing to “fast track” vaccine approval. This comes just days after he assured Bloomberg reporters that the agency would “stick to the science” and that any approval would be “data based”. Speaking to the Times of London, a different British broadsheet, Dr. Anthony Fauci reiterated his claims that the US should expect a vaccine by the end of the year, possibly sooner, and that we should know whether candidates are “safe and effective” by November.

Dr. Anthony Fauci, director of the National Institute of Allergy and Infectious Diseases, said this weekend: “The way the pace of the enrollment is going on and the level of the infections that are going on in the United States, it is likely that we’ll get an answer by the end of the year.” He added, “It is conceivable that we would get an answer before that.”

“I would say a safe bet is at least knowing that you have a safe and effective vaccine by November, December.”

That’s good news, because America’s colleges have reported one COVID-19 outbreak after the next since the new semester began earlier this month. But as student newspapers castigate universities for “putting students’ lives at risk” (calm down kids), Bloomberg reports that a consensus is building among public health experts that it’s better to keep university students on campus following a COVID-19 outbreak rather than send them home, as many schools are – inexplicably – doing.

It’s easier to isolate sick or exposed students and trace their contacts if they stay put, said Ravina Kullar, epidemiologist and spokesperson for Infectious Diseases Society of America. Sending them home creates obvious risks of further spread.

Over in Europe, Germany’s daily infections fell after a streak of rising numbers, but that didn’t stop its transmission rate – or “R” – from rising above the critical threshold of “1”. The Robert Koch Institute reported 709 new cases in the 24 hours through Sunday morning, pushing Germany’s total to 242,835, according to data from Johns Hopkins University.

That’s less than half of Saturday’s increase of 1,555. Germany registered more than 7,000 cases per day during the pandemic’s peak in the spring. Germany’s reproduction rate climbed to 1.04 from 0.94 the prior day.

After reporting another near-world record of new cases, India officially passed the 3.5-million case mark on Sunday, while its death toll exceeded 63,000. As India’s outbreak worsens, numbers in Brazil and the US continued to fall.

via ZeroHedge News https://ift.tt/2EEET4J Tyler Durden

Tanks Move Into Minsk As Police Hold Back Massive Protest At Gates Of Lukashenko Residence Tyler Durden

Sun, 08/30/2020 – 12:05

Defying a security services crackdown, tens of thousands of protesters demanding that Belarusian President Alexander Lukashenko step down engulfed the center of Minsk once again.

This time on the occasion of the now 66-year old leader’s birthday on Sunday, tens of thousands were seen marching on the presidential residence.

There he is again, its Sunday-Kalaschnikow-Time for Lukaschenko. Picture is from his office, released just now. pic.twitter.com/JG8ZD2pfEa

Riot police, armored vehicles, and even tanks were seen defending Lukashenko’s residence. Military tanks and personnel carriers were seen pouring into the area, based on activist footage on the ground.

#Belarus. There are numerous reports that infantry fighting vehicles are heading to the #Minsk city centre.People are now not far from the riot police cordon near Lukashenko’s residence. They are aboslutely peaceful. They brought birthday “gifts” that they leave near the cordon. pic.twitter.com/NNxomWOgon

Stunning video also showed a massive crowd being held off just outside the presidential compound by a wall of riot police, military, and armored vehicles.

A large crowd is massing outside Lukashenka’s residence in Minsk, blocked from going further by a phalanx of riot police. Video reports suggest tanks are heading to the residence, apparently to shore up its defenses. pic.twitter.com/4rZu7NT2Lk

Belarusian protests channels are posting a video of what look like infantry fighting vehicles heading into central Minsk. This could a serious escalation. https://t.co/qUkfA0deUgpic.twitter.com/eRMlOqYT2L

Reuters reports that despite the major show of force by state security, the demonstrations were relatively peaceful:

Protesters then converged on Lukashenko’s residence, which was guarded by security forces carrying shields, and water canon and prisoner vans. A column of armoured military vehicles was seen driving towards the city centre, Russia’s Interfax news agency reported.

Russia’s RIA news agency said at least 125 people were detained.

Security forces were seen detaining people in black unmarked police vans.

Violent scenes on independence prospekt where riot police have aggressively closed in protesters #minskpic.twitter.com/RU5pyEqoxA

In some cases, plain clothes officers were spotted arresting protesters, after rolling protests and nation-wide strikes have paralyzed parts of the country, especially the capital, since the Aug.9 disputed reelection of Lukashenko to a sixth term, which the opposition and people in the streets have denounced as “rigged”.

Reports of tanks and/or APCs moving through central Minsk now. Here’s one of several videos circulating. Video by @svabodapic.twitter.com/uM3eT89hzn

Meanwhile, citing external threats from NATO countries, Lukashenko has reportedly put up to half the army in ‘combat readiness’ mode, Reuters reports Sunday.

“(NATO) have launched exercises right by our borders. What am I supposed to do? I also rolled out some divisions, put half the army into combat preparedness mode. That’s not cheap,” Lukashenko announced.

via ZeroHedge News https://ift.tt/31GQIjJ Tyler Durden

Central banks are facing a serious predicament. After decades of ongoing accommodative monetary policy, the world is now sitting at record levels of debt relative to global GDP.

In our view, there has never been a bigger gulf between underlying economic fundamentals and security prices. We are in a global recession, but equity and credit markets still trading at outrageous valuations.

Markets are trading on a perverse combination of Fed life support and rabid speculative mania. Meanwhile, demand for gold and silver, which is fundamentally cheap, is starting to take off as central banks are engaged in new record easy monetary policies. Ongoing easy monetary policies in the face of today’s asset bubbles in stocks and fixed income securities has a high probability of leading to a self-reinforcing cycle that drives investors out of these over-valued asset classes and into under-valued precious metals.

Here are just some of the reasons Crescat is selling richly valued stocks at large and buying undervalued gold and silver including mining companies today:

The economy is now reaching credit exhaustion with record amounts of government and corporate debt relative to GDP worldwide.

The debt burden ensures weak future real economic growth.

Monetary debasement is the only way to reduce the debt burden. Fiat currencies are now engaged in a race to the bottom.

Global monetary base expansion to suppress interest rates creates a supercharged environment for gold and silver.

The global economy is in a severe recession with structural underpinnings beyond Covid-19.

Unemployment has spiked an historic 6.7% in just five months from 3.5% to 10.2% even after settling back from temporary 14.7% Covid-19 lockdown levels.

US equities today trade at truly record valuations, a full-blown mania. Ongoing policy rescue has perverted both free market accountability and price discovery creating a simultaneous zombie economy and stock market bubble which is unsustainable. Speculative asset bubbles are ripe for bursting.

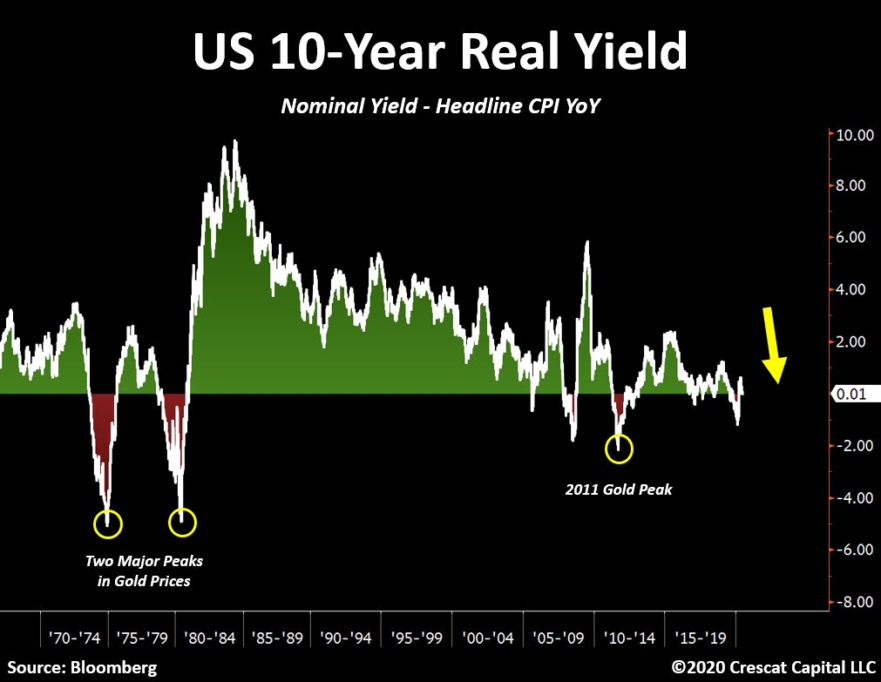

During the 1970s precious metals bull market, 10-year real yields got as low as -4.9%. We strongly believe we are headed in that direction and again with a long runway, especially with Jay Powell’s new signaling from Jackson Hole.

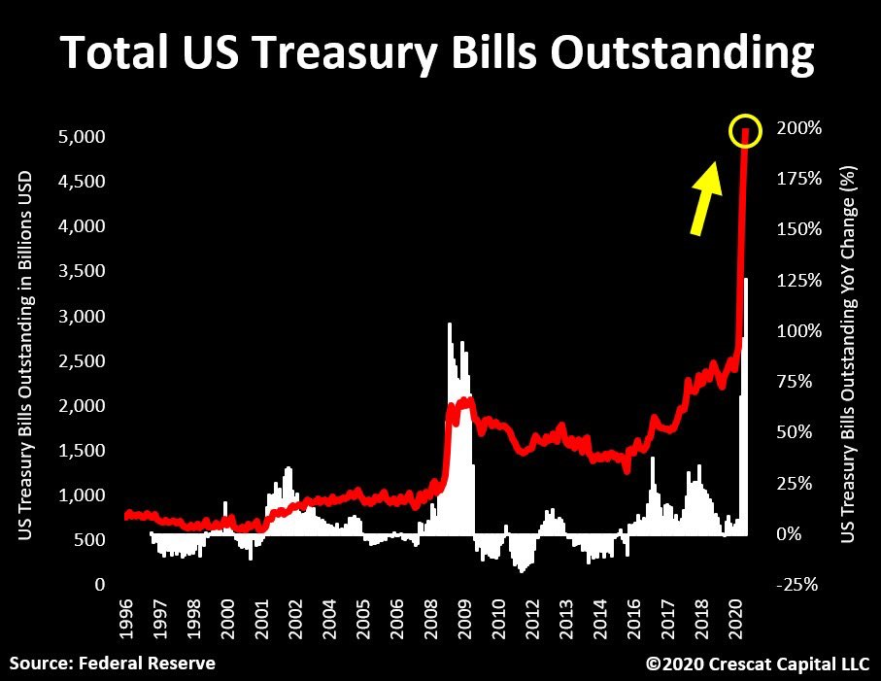

A colossal $8.5 trillion of US Treasuries will mature by the end of 2021 and will need to be refinanced. Our government’s own central bank, the Fed, is the only entity capable of swallowing its debt guaranteeing new record levels of money printing to top today’s already historic levels.

Precious metals became a forgotten class among large allocators of capital in the extended expansion phase of the last busines cycle.

With $15 trillion of negative yielding bonds, equities’ earnings real yields at a decade low, and corporate bonds near record prices, gold and silver are being rediscovered for their tactical as well as strategic risk reducing and return generating properties in prudently balanced portfolios.

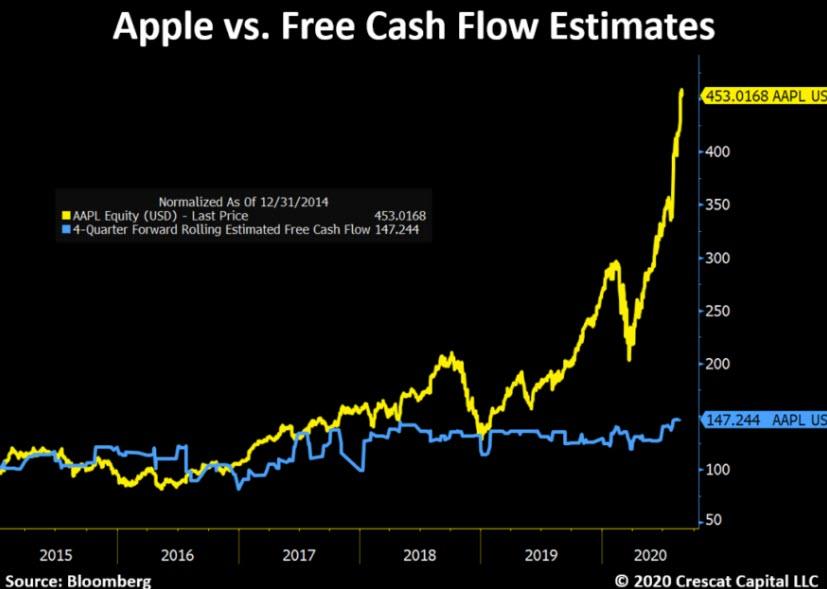

The precious metals mining industry is the one clear industry to directly benefit from this monetary and fiscal indulgence. The aggregate market value of this industry still is almost 3 times smaller than Apple’s market cap.

Precious metals are now trading at historically depressed levels relative to money supply; overall stocks, on the other hand, are the complete opposite.

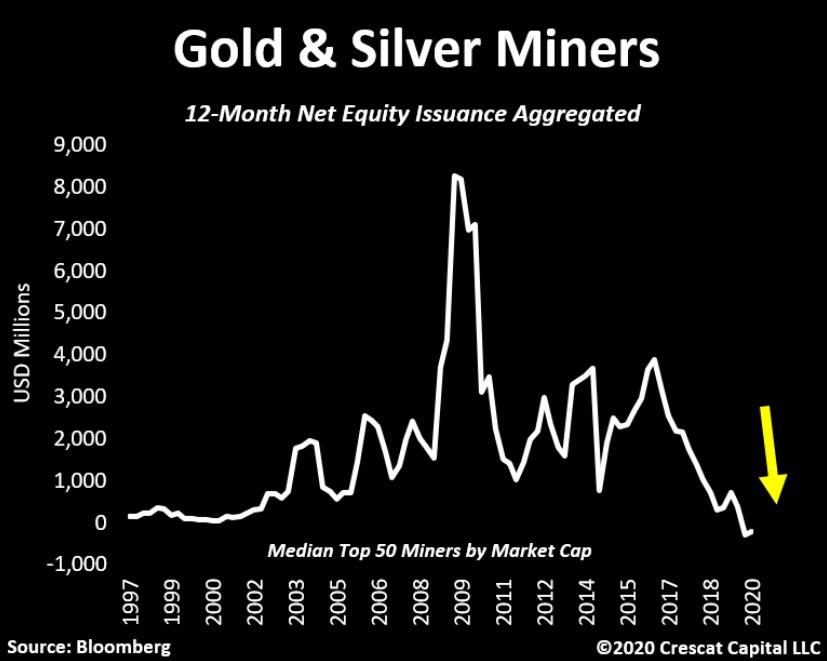

After a decade-long bear market, precious metals miners have been reluctant to spend capital. Now, they have historically low equity dilution, clean balance sheets, and record free cash flow growth.

The lack of investment in exploration and new gold and silver discoveries is setting up an incredibly bullish scenario for metals as supply is likely to remain constrained for an extended period at the same time while demand is poised to explode.

The year-over-year change in gold prices just broke out from a decade-long resistance. Last time we saw such strong appreciation was at the early stages of the 1970s gold bull market.

Financial markets simply cannot withstand higher interest rates. We believe the Fed has been forced into a new mandate, to suppress yields at all cost. This dynamic of expanding the monetary base to purchase assets and manipulate rates lower is an explosive mix for precious metals.

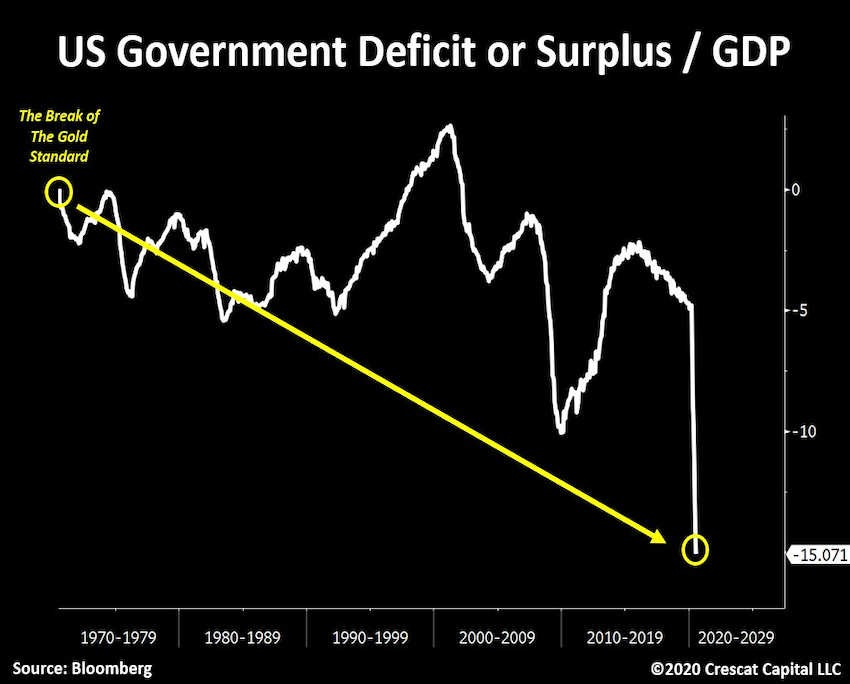

The break of the gold standard in 1971 was just as impactful as the Fed’s recent unlimited QE policy. Back then, it marked a period of lack of financial and fiscal discipline that triggered a frenetic 10-year bull market for gold. This time, we have arguably even stronger macro drivers for precious metals. As we show in the chart below, we have been in a clear trend of structurally increasing government deficits.

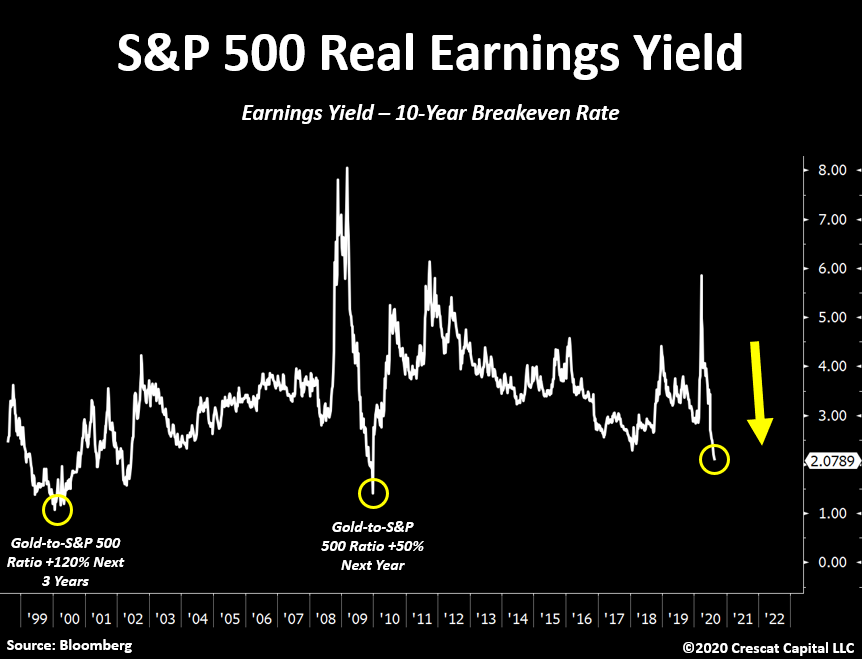

The S&P 500 real earnings yield is at its lowest level in a decade. Prior lows were also times that gold outperformed equities. In the early 2000s, for instance, the gold-to-S&P 500 ratio went up by 120% over 3 years. Even in 2010, a bull market for stocks, gold outperformed by 50%. The difference this time is that stocks have never been at record high valuations with fundamentals so severely depressed. We believe strongly this is the perfect time to buy gold and sell stocks. And when we say “buy gold”, we also include silver and precious metals mining stocks where there is even more upside exposure (both alpha and beta) to a macro move up in gold.

The debt quandary the US government faces also adds tremendously to our views on precious metals. From a funding perspective, 71% of all Treasuries issued in the past year matures in less than 12 months, resulting on Treasury Bills outstanding to surge to $5 trillion! The US Treasury is hoarding a record of $1.79 trillion of this cash. A similar buildup happened back in 2008-9. A major difference this time is the fact that Treasury Bills outstanding are almost $3.3 trillion higher than their cash balance. In such scenario, average maturity of government debt has dramatically declined to 64 months. As a result, there is a tsunami of $8.5 trillion of Treasuries that will be maturing by the end of 2021 ensuring astronomic levels of money printing in the near term.

Skeptics of Crescat’s long gold thesis often say real yields can’t move any lower. This is often because this are looking at the TIPS market which only dates back to 1997 and real yields are already at their lows for this time frame. Therefore, some investors assume interest rates when adjusted for inflation expectations have never been lower. That, unfortunately, fails to include one of the most important analogs to today’s set up, the decade of the 1970s. Back then, 10-year yields less inflation measured by CPI twice reach as low as about -4.9%. Those moments of large and declining negative real interest rates drove two of the US most significant surges in gold, silver, and precious metals mining stocks in US history. In today’s conundrum, corporations and governments are historically indebted and can’t take higher nominal yields, ensuring that strong monetary stimulus is here to stay to drive real yields lower, just like Jay Powell has promised.

A major narrative shift is underway. The old times of precious metals being perceived just as haven assets are probably over. With $15 trillion worth of negative yielding bonds, record overvalued stocks and a historically leveraged global economy, investors will likely begin to look at gold and silver, especially mining companies, with a fresh pair of eyes: growth and value. Precious metals miners are the only industry where we are seeing strong and sustainable growth in revenues and future free cash flow at still incredibly low valuations today. Investors are starting to take note. Silver mining stocks, for instance, have already started to outperform even the market darlings, tech stocks. We believe this is only the beginning of a new era for precious metals.

The mining industry built a reputation of being capital destroyers since it peaked in 2011. But today this skepticism is no longer warranted. It is mind blowing that gold prices have just hit record highs and the larger mining companies have barely engaged in share dilution. In aggregate, the top fifty gold and silver miners by market cap that trade in Canadian and US exchanges have only issued close to $266 million in equity in the last twelve months. That was the second lowest amount of 12-month equity issuance in the last 3 decades. These companies have also just paid down $200 million of debt in the last quarter.

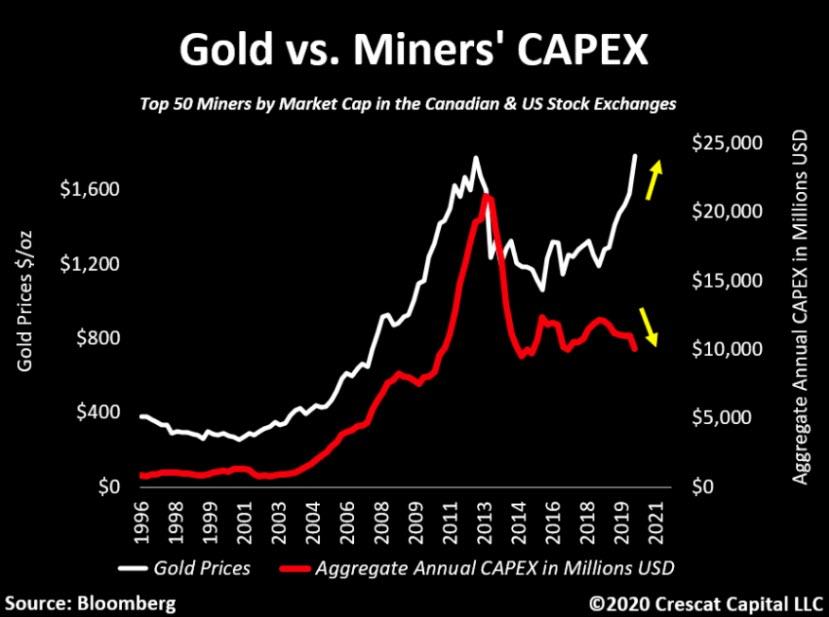

We have also noticed extremely conservative capital spending by miners. Throughout history, the CAPEX cycle for the industry tends to follow gold and silver prices incredibly close. Logically, this makes sense. As metal prices move higher, these businesses become more optimist and therefore focus on advancing their projects. This time, however, even though gold and silver prices have moved significantly higher, companies remain reluctant to spend capital. This level of divergence never happened in prior bull markets for precious metals. This is fundamentally bullish for entire asset class as we expect the supply of gold and silver to stay constrained for longer. It is also fundamentally bullish for Crescat’s activist investment strategy in the industry where we we can deploy capital into undervalued companies with big, highly economic projects that are ripe to move forward in current macro environment.

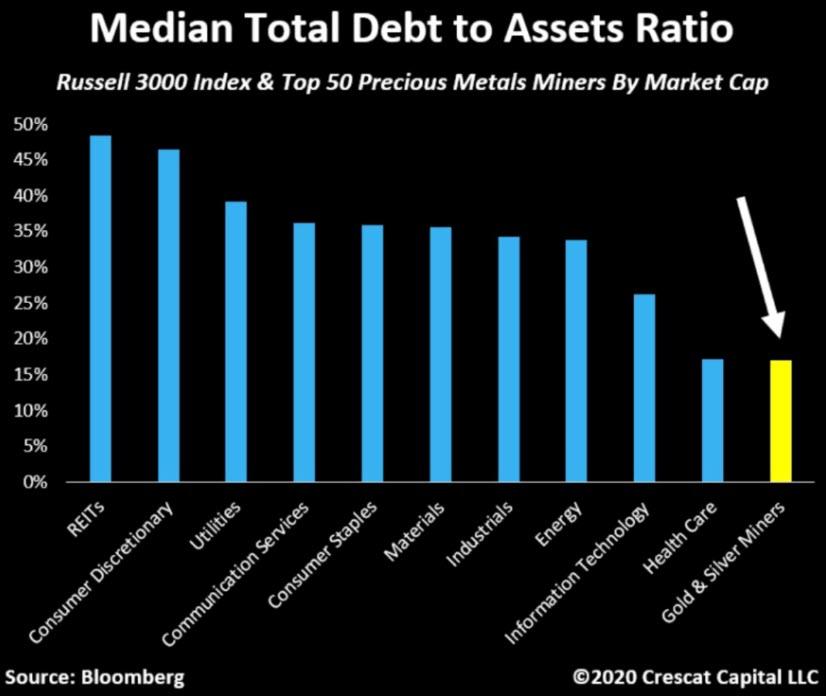

Precious metals miners have never looked so financially strong. If the industry were a sector, it would have the cleanest balance sheet among all sectors in the S&P 500. The median company in the S&P 500 today has historically high total debt to assets of 35%. Top miners, on the other hand, have only 12%. For such capital-intensive businesses, today’s healthy industry-wide capital structure is nice set-up to kick off a new secular bull market in precious metals mining.

We think it is important to get a sense of the both the value and growth opportunity today to see the incredible appreciation potential ahead of us. When we look at the ratio of gold and silver miners to global equities, it is still is near all-time lows and appearing to form a very bullish base, similar to what we saw back in early 2000s. Mining stocks meanwhile are about to become free cash flow growth machines. Juniors with a large scale, high grade new deposits, carry mind-blowing NPVs and IRRs. It is far and away the industry with the strongest combination of deep value and high growth opportunity for today’s macro environment.

In contrast to the value and growth prospects for miners, it is shocking to see Apple’s market cap still about 3.5 times the size of the entire precious metals industry. If anything, this reflects the level of skewness to the upside for gold and silver stocks in the near and medium term. This is the only industry to truly benefit from today’s world of unlimited QE and deficits.

As we show below, Apple’s stock price appreciated at a much faster growth rate than its underlying free cash flow on a rolling twelve-month, forward-looking basis. The stock price is way ahead of its fundamentals. Apple is just one the many poster children for the manic speculation and excess in today stock market at large. Stocks like Microsoft, Tesla, and Netflix show similar looking disconnect.

With stock market indices making new highs, the narrowing breadth is ominous, especially in the tech-laden NASDAQ Composite.

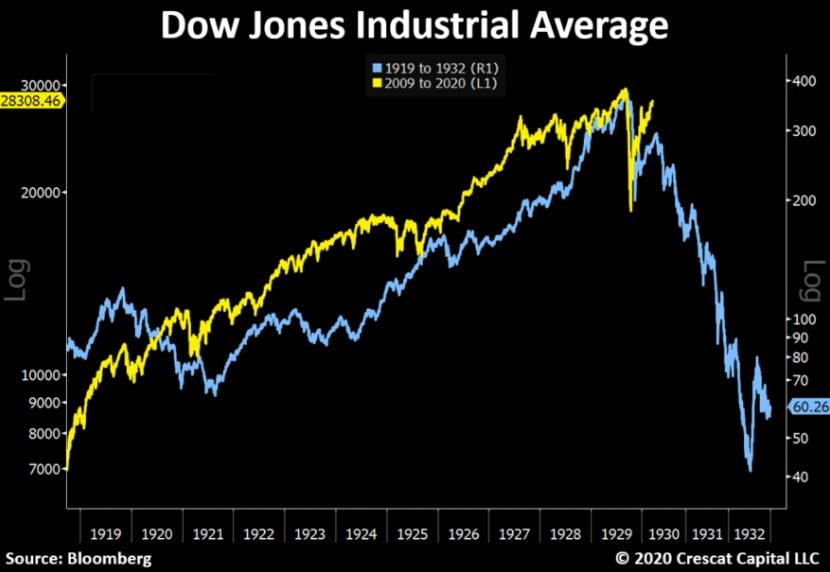

The valuation of US stocks at large based a combination of eight factors compiled by Crescat is the most over-valued ever. We believe that the stock market is more over-valued than in it was in 1929 and higher than 2000.

To think that the stock market does not have any downside risk because the Fed has its back is absurd. False hope in the Fed’s ability to sustain these market valuations is perhaps the sole remaining illusion holding this market up. If your are in the crowded investor camp that believes easy monetary policy can prevent a market crash this time around because the Fed is engaged in easy monetary policy unlike the Great Depression, do yourself a favor and look up what happened to stock prices and multiples during the 1973-1974 bear market.

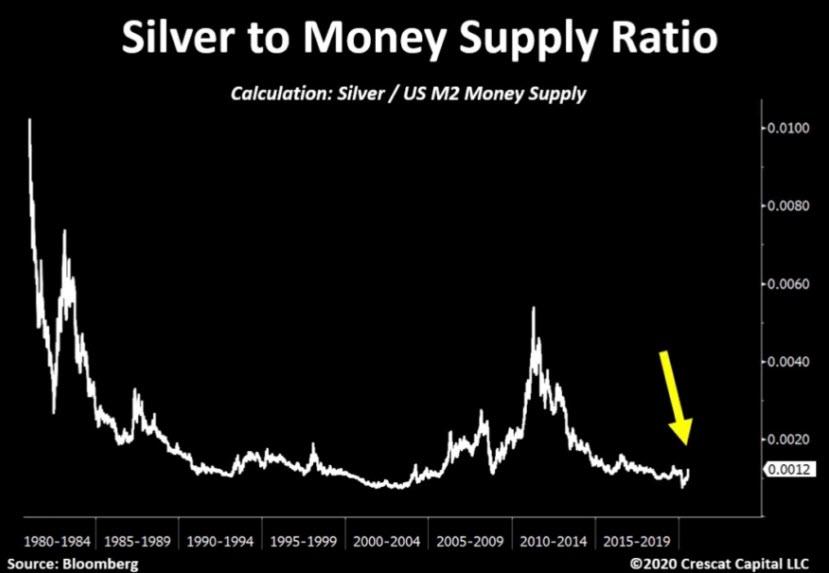

Easy monetary policies, as we have shown herein, are much more likely to drive investors out over-valued stocks and into under-valued precious metals. One precious metal that we are most excited about today is silver. Throughout history silver has played an important role in the monetary system. Its recent price surge made a lot of investors question the sustainability of this move, but in the grand scheme of things, silver remains near all-time lows relative to size of the US M2 money supply. The chart below is analytically important as it zooms out the still-early stages of what could be an incredible upsurge.

We have also recently noted that gold prices on a year over year basis just broke out from an over decade-long resistance. This is an important validation of our precious metals’ thesis. In our view, this looks a lot like the beginning of a late 70’s bull market.

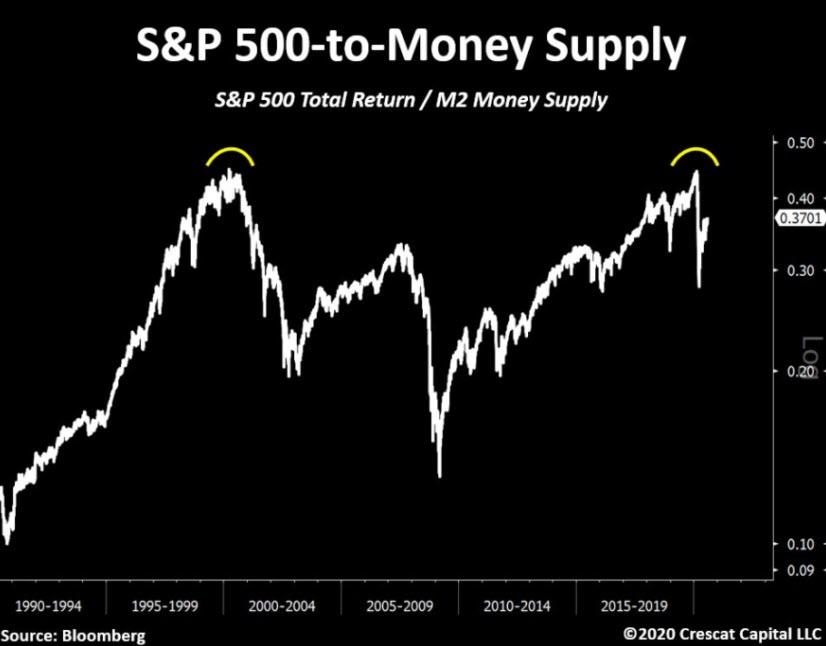

Even after the largest liquidity infusion seen in history, equity markets are not only overvalued relative to their fundamentals but also relative to money supply. On the chart below, the S&P 500-to-M2 money supply ratio recently formed a double top from the insane tech bubble levels. It also still it well above peak of the housing bubble. For investors looking for bargains, it is not in the stock market at large. In our view, precious metals are almost solely the place to be today.

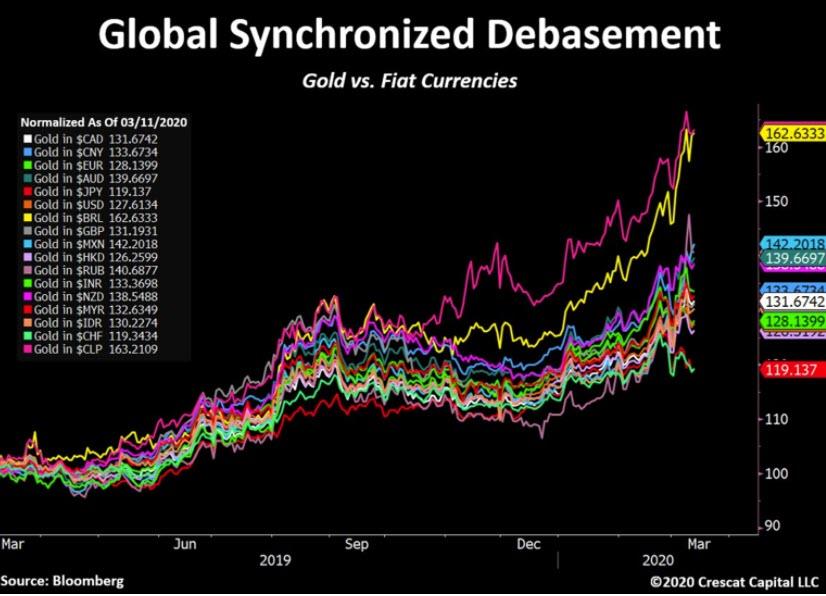

How does it all end? Colossal monetary dilution. None of us own enough gold. It is not just the US dollar that will be challenged. It is all the global fiat currencies of highly indebted countries. The Chinese yuan for instance is in an even worse predicament than the US dollar.

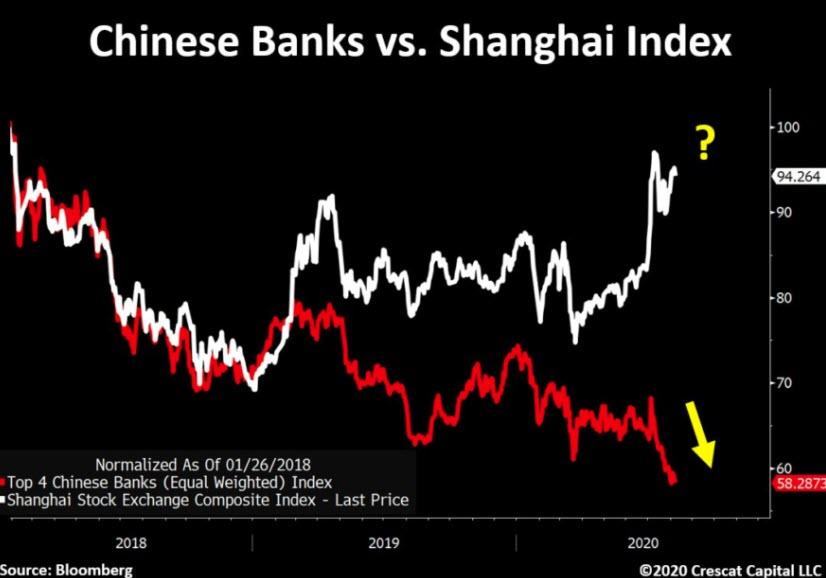

Chinese and Hong Kong banks are the most levered financial institutions in the global markets today. Chinese banks hold close to $43 trillion worth of highly inflated assets compared to China’s $14 trillion nominal GDP, an imbalance significantly greater than US and European banking imbalances that precipitated the Global Financial Crisis in 2008. Chronically troubled, the top four Chinese banks have been under pressure for years now and have significantly been diverging to the downside relative to the Chinese stock market at large, similar to US banks in 2007. We believe that China, formerly the growth engine of the global economy responsible for 60% of global GDP from 2009 to 2019, has finally reached credit exhaustion.

All fiat currencies are in a race to the bottom versus gold today.

The macro environment is one of global synchronized monetary debasement.

via ZeroHedge News https://ift.tt/3gI1Lxc Tyler Durden

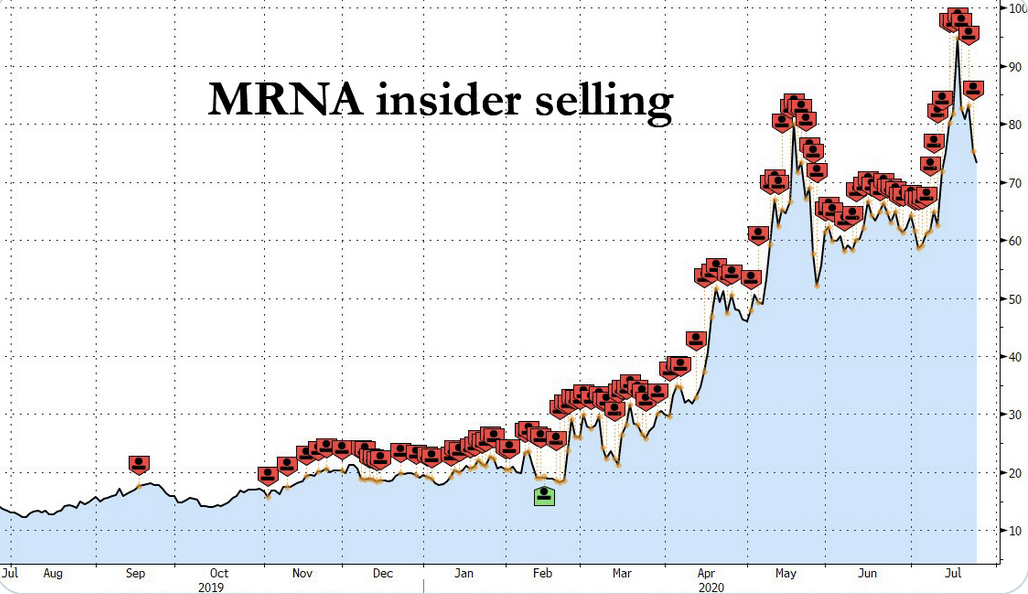

Moderna Neglected To Disclose Pentagon’s Financial Support In Applications For More Than 100 Patents Tyler Durden

Sun, 08/30/2020 – 11:15

Before the mainstream media transfigures Moderna founder and CEO Stephane Bancel into a corporate savior on par with Bill Gates, we’d like to remind investors (and the public) that Moderna and its insiders have demonstrated an eyebrow-raising affinity for pumping the stock with over-hyped press releases then cashing in shares or warrants (all insider stock sales were pre-scheduled divestitures, the insiders’ lawyers have argued).

Despite receiving nearly $1 billion in taxpayer money via “Operation Warp Speed”, the drugmaker is planning to charge as much as $37 for a single dose, or up to $60 for two courses, of its experimental mRNA COVID-19 vaccine. That’s far and away the highest price point disclosed yet.

And while we wait for more detailed data from the vaccine’s Phase 3 clinical trials, patent advocacy group KEI is taking Moderna and its executives to task for neglecting to disclose government funding received by the company during its early stages, before the coronavirus pandemic.

Despite receiving $25 million from the Department of Defense’s “Defense Advanced Research Projects Agency” – or “Darpa” – Moderna has never disclosed this, or any other, government funding in its applications for 126 patents and 154 patent applications. KEI has lodged a request with the DoD and Darpa to remedy this in patents.

As KEI points out, Moderna’s “failure” to disclose its government funding could have serious consequences for Americans hoping to get their hands on an affordable vaccine. The disclosures could affect everything from the US government’s worldwide royalty free license, to the public’s march-in rights, to obligations to make inventions available to the public on reasonable terms.

When approached by the FT, Darpa confirmed that Moderna was required in its contracts to disclose the funding in any patent applications that stemmed from research that the US government helped fund.

Now, Darpa is actively looking into which Moderna patents may have been produced with Darpa support, so the US government can take credit where credit is due.

“It appears that all past and present Darpa awards to Moderna include the requirement to report the role of government-funding for related inventions,” Darpa spokesman Jared Adams said in an emailed response to the Financial Times. “Further, Darpa is actively researching agency awards to Moderna to identify which patents and pending patents, if any at all, may be associated with Darpa support,” he said. Mr Adams declined to comment further, saying the investigation was continuing. US federal law required government funding to be disclosed in these circumstances, he noted.

Now, keep in mind that Moderna is trying to charge as much as $37 per dose for its vaccine, when the vaccine being developed by AstraZeneca and the University of Oxford is priced at about $3 per dose.

Maybe Moderna can make amends for these mistakes by cutting the price its charging the US government for a vaccine that it developed with the help of a massive infusion of government money?

via ZeroHedge News https://ift.tt/2QDMrqY Tyler Durden

Why, in the world’s richest country, is every metric of mental health pathology rapidly worsening?

THE YEAR 2020 has been one of the most tumultuous in modern American history. To find events remotely as destabilizing and transformative, one has to go back to the 2008 financial crisis and the 9/11 and anthrax attacks of 2001, though those systemic shocks, profound as they were, were isolated (one a national security crisis, the other a financial crisis) and thus more limited in scope than the multicrisis instability now shaping U.S. politics and culture.

Since the end of World War II, the only close competitor to the current moment is the multipronged unrest of the 1960s and early 1970s: serial assassinations of political leaders, mass civil rights and anti-war protests, sustained riots, fury over a heinous war in Indochina, and the resignation of a corruption-plagued president.

But those events unfolded and built upon one another over the course of a decade. By crucial contrast, the current confluence of crises, each of historic significance in their own right — a global pandemic, an economic and social shutdown, mass unemployment, an enduring protest movement provoking increasing levels of violence and volatility, and a presidential election centrally focused on one of the most divisive political figures the U.S. has known who happens to be the incumbent president — are happening simultaneously, having exploded one on top of the other in a matter of a few months.

Lurking beneath the headlines justifiably devoted to these major stories of 2020 are very troubling data that reflect intensifying pathologies in the U.S. population – not moral or allegorical sicknesses but mental, emotional, psychological and scientifically proven sickness. Many people fortunate enough to have survived this pandemic with their physical health intact know anecdotally — from observing others and themselves – that these political and social crises have spawned emotional difficulties and psychological challenges.

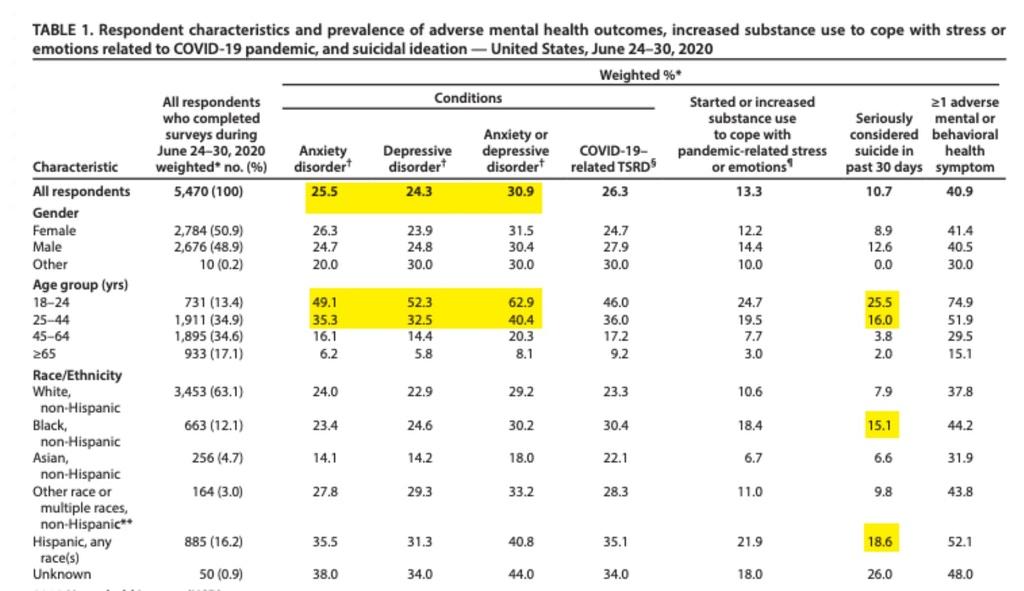

But the data are nonetheless stunning, in terms of both the depth of the social and mental health crises they demonstrate and the pervasiveness of them. Perhaps the most illustrative study was one released by the Centers for Disease Control and Prevention earlier this month, based on an extensive mental health survey of Americans in late June.

One question posed by researchers was whether someone has “seriously considered suicide in the past 30 days”— not fleetingly considered it as a momentary fantasy nor thought about it ever in their lifetime, but seriously considered suicide at least once in the past 30 days. The results are staggering.

For Americans between 18-24 years old, 25.5 percent — just over 1 out of every 4 young Americans — said they had. For the much larger group of Americans ages 25-44, the percentage was somewhat lower but still extremely alarming: 16 percent. A total of 18.6 percent of Hispanic Americans and 15 percent of African Americans said they had seriously considered suicide in the past month. The two groups with the largest percentage who said yes: Americans with less than a high school degree and unpaid caregivers, both of whom have 30 percent — or almost 1 out of every 3 — who answered in the affirmative. A full 10 percent of the U.S. population generally had seriously contemplated suicide in the month of June.

In a remotely healthy society, one that provides basic emotional needs to its population, suicide and serious suicidal ideation are rare events. It is anathema to the most basic human instinct: the will to live. A society in which such a vast swath of the population is seriously considering it as an option is one which is anything but healthy, one which is plainly failing to provide its citizens the basic necessities for a fulfilling life.

The alarming CDC data extends far beyond serious suicidal desires. It also found that “40.9% of respondents reported at least one adverse mental or behavioral health condition, including symptoms of anxiety disorder or depressive disorder (30.9%), symptoms of a trauma- and stressor-related disorder (TSRD) related to the pandemic (26.3%), and having started or increased substance use to cope with stress or emotions related to COVID-19 (13.3%).”

For the youngest part of the adult population, ages 18-24, significantly more than half (62.9 percent) reported suffering from depressive or anxiety disorders.

THAT MENTAL HEALTH WOULD SUFFER materially in the middle of a pandemic — one that requires isolation from community and work, quarantines, economic shutdowns, and fear of illness and death — is not surprising. In April, as the realities of isolation and quarantine were becoming more apparent in the U.S., we devoted a SYSTEM UPDATE episode to a discussion with the mental health experts Andrew Solomon and Johann Hari, both of whom described how “the traumas of this pandemic — the unraveling of our way of life for however long that lasts, the compulsory viewing of all other humans as threats, and especially sustained isolation and social distancing” — will exacerbate virtually every social pathology, including ones of mental health.

But what makes these trends all the more disturbing is that they long predated the arrival of the coronavirus crisis, to say nothing of the economic catastrophe left in its wake and the social unrest from this year’s protest movement. Indeed, since at least the financial crisis of 2008, when first the Bush administration and then the Obama administration acted to protect the interests of the tycoons who caused it while allowing everyone else to wallow in debt and foreclosures, the indicia of collective mental health in the U.S. have been blinking red.

In 2018, NBC News, using health insurance studies, reported that“major depression is on the rise among Americans from all age groups, but is rising fastest among teens and young adults.” In 2019, the American Psychological Association published a study documenting a 30 percent increase “in the rate of death by suicide in the United States between 2000 and 2016, from 10.4 to 13.5 per 100,000 people” and a 50 percent increase “in suicides among girls and women between 2000 and 2016.” It noted: “Suicide was the 10th-leading cause of death in the United States in 2016. It was the second-leading cause of death among people ages 10 to 34 and the fourth-leading cause among people ages 35 to 54.”

In March 2020, the New Yorker’s Atul Gawande published a survey of data from two Princeton economists, Anne Case and Angus Deaton, under the headline: “Why Americans Are Dying from Despair: the unfairness of our economy, two economists argue, can be measured not only in dollars but in deaths.” The decadeslong economic stagnation for Americans, the reversal of the American Dream, and the shockingly high mass unemployment ushered in by the pandemic are obviously significant reasons why these pathologies are rapidly worsening now.

Observing these trends is necessary but not sufficient for understanding their breadth and their impact. Why is virtually every metric of mental and spiritual disease — suicide, depression, anxiety disorders, addiction, and alcoholism — increasing significantly, rapidly, in the richest country on earth, one filled with advanced technologies and at least the pretense of liberal democracy?

One answer was provided by Dr. Laurel Williams, chief of psychiatry at Texas Children’s Hospital, to NBC when discussing the rise of depression:

“There’s a lack of community. There’s the amount of time that we spend in front of screens and not in front of other people. If you don’t have a community to reach out to, then your hopelessness doesn’t have any place to go.”

That answer is similar to the one offered by the brilliant book on depression and modern western societies by Johann Hari, “Lost Connections,” along with his viral TED Talk on the same topic: namely, it is precisely the attributes that define modern Western societies that are crafted perfectly to deprive humans of their most pressing emotional needs (a book by Hari on addiction, “Chasing the Scream,” and an even-more-viral TED Talk about it, sounds a similar theme about why Americans are turning in horrifyingly large numbers to serious problems of substance abuse).

Much attention is devoted to lamenting the toxicity of our discourse, the hate-driven polarization of our politics, and the fragmentation of our culture.

But it is difficult to imagine any other outcome in a society that is breeding so much psychological and emotional pathology by denying to its members the things they most need to live fulfilling lives.

Today’s SYSTEM UPDATE on The Intercept’s YouTube channel is devoted to exploring this unravelling of the social fabric: not just the data demonstrating that it is happening, but also what the causes are, and what the consequences are likely to be for our politics, our culture, our society generally. And the answers to the question prompted by all of this — where is the exit ramp to prevent these trends from worsening even further? — are as elusive as they are vital. It can also be viewed on the player below:

$16 Billion Ohio Police & Fire Pension Fund Approves A 5% Allocation For Gold Tyler Durden

Sun, 08/30/2020 – 10:40

Ohio’s $16 billion Police & Fire Pension Fund is following in the steps of Warren Buffett and making a big statement about owning gold. It has approved a 5% allocation to gold to help diversify the fund’s portfolio and to “hedge against the risk of inflation” according to Bloomberg.

The change was approved as “the first step” in an ongoing asset review that was presented to the fund’s board on August 26.

The fund was following the advice of its investment consultant, Wilshire Assocaites, in adding the gold allocation, according to Pensions & Investments. Additionally, the fund plans on adding the gold stake by borrowing; the fund is reportedly increasing its leverage from 20% to 25% to make the change.

“No new manager has been selected, and there currently is no timeline for implementing this change,” P&I reported.

Buffett’s move into gold has opened the door for fund managers to follow suit. Except, instead of playing in a hundred trillion dollar equity market, they are dealing with barely over $1 trillion in investable gold. This means that if the fund becomes a trend setter in the industry and if others follow suit, look out above.

Peter Schiff said on a recent podcast: “Warren Buffett seems to have a very good understanding of inflation. He doesn’t regard it as rising prices, he regards it as money supply. He’s talked about inflation as a hidden tax on savers. As a cruel tax. He understands the loss of value of money. He basically says that that’s inflation: the erosion of purchasing power of money. I think Buffett now has a much darker outlook on inflation than he did in the past.”

“Buffett is now of the opinion that inflation is going to be so high that gold is going to be particularly important to own, rather than just owning businesses,” he says.

You can listen to Schiff’s comments here:

If the inflation message starts to become clear to pension funds and main street asset managers, we could see a major sea change in psychology regarding gold as an investment.

Additionally, Rick Rule recently commented about exactly how under-owned gold was in the U.S.: “A major bank study, which I read, and I’ve quoted it before in interviews with you, says that between 0.3%-0.5% of savings and investment assets in the United States involve precious metals or precious metals securities.”

He continued: “That may have gone up because the denominator has declined the value, the Dow is an example, but the three decade-long mean was between 1.5%-2%. So gold is still very broadly under-owned, and I would suggest it’s even under-owned among people who are listening to this broadcast.”

But in plain English, another way to say it is that there simply isn’t enough gold available in the world for every pension fund to make the same 5% allocation.

Barbaric relic, pet rock, public enemy #1> Gold has begun a major transition> Buffett is attracted to enormous cash flow & dividend potential of Barrick, then Reserve Bank of India signals higher allocation, and now OHIO Police & Fire Pension approves a 5% allocation.

New Jersey Hikes Gas Tax By 22.5%, Bringing Total Increase Since 2016 To 250% Tyler Durden

Sun, 08/30/2020 – 10:25

Not content with driving out its wealthiest with yet another tax hike on millionaires, New Jersey just made life for all of its residents, including lower and middle classes, more expensive when it quietly decided on Friday to hike the state’s fuel tax.

Drivers filling up gas in New Jersey will pay 9.3 cents more per gallon, or a 22.5% increase, after the state announced a fuel tax increase that will take effect October 1, the Philly Voice reported. The rate increase will bring the state tax from 41.4 cents per gallon to 50.7 cents per gallon.

The NJ Treasury Department explained Friday that the decision was necessary because tax revenue has fallen with fewer people on the road during the coronavirus pandemic. And so, in all its brilliance, the Garden State plans to make gas even more expensive and guarantee that there will be even fewer people on the road because even before covid, New Jersey was the state with the most foreclosures not because its residents are swimming in money but, well, the opposite. So why not make everyone even poorer?

According to the Treasury, the increased tax revenue will support and ensure the solvency of the state’s Transportation Trust Fund, which was established in 2016 under former Gov. Chris Christie. The TTF requires that approximately $2 billion be contributed each year, with adjustments based on a model that assumes an increase of $50 million annually for every penny added to the fuel tax, according NJ.com.

“As we’ve noted before, any changes in the gas tax rate are dictated by several factors that are beyond the control of the administration,” State Treasurer Elizabeth Maher Muoio said in a statement Friday. “The law enacted in 2016 contains a specific formula to ensure that revenue is meeting a certain target. When it does not, the gas tax rate has to be adjusted accordingly in order for us to meet our obligation under the law and fully fund the state’s many pressing transportation infrastructure needs.”

The tax on diesel fuel also will rise by the same amount from 48.4 cents per gallon to 57.7 cents per gallon.

The last time the New Jersey tax was increased was in 2018, when Gov. Phil Murphy raised the rate by 4.3 cents per gallon. When the latest increase takes effect, the fuel tax in New Jersey will have increased by more than 250% since the TTF was established in 2016.

After the tax hike, New Jersey’s gas tax will be the fourth highest behind California, Pennsylvania and Illinois. The state currently has the 10th highest fuel tax in the U.S.

via ZeroHedge News https://ift.tt/3lwhF18 Tyler Durden

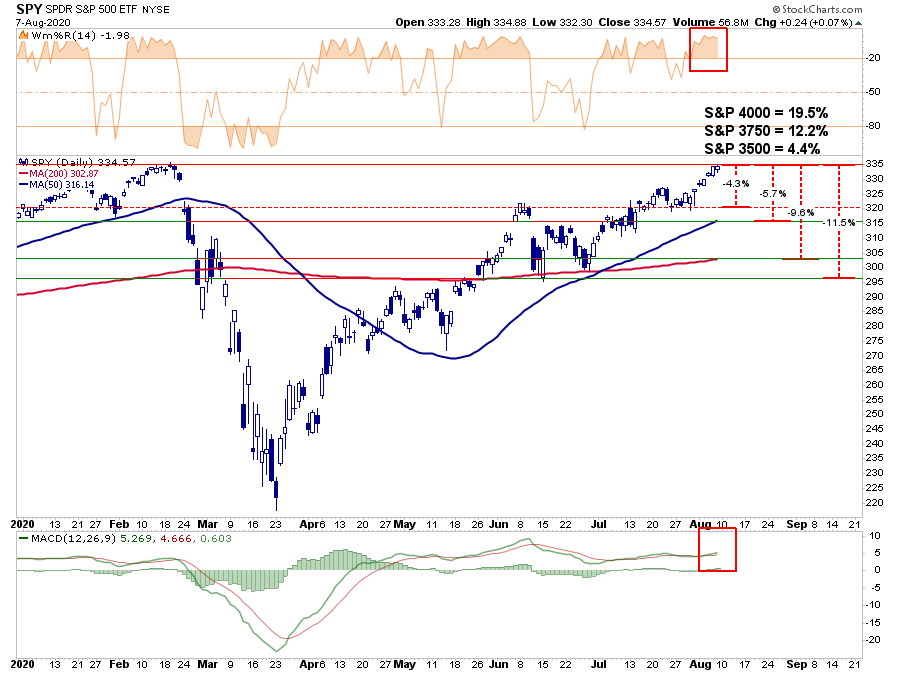

A couple of weeks ago, I wrote a wildly unpopular article laying out why, if the bulls could push the markets to new all-time highs, the next target would be 3750. With the market now at new all-time highs, and the bulls clearly in charge, is it “safe” for investors to become complacent? Maybe, not.

Technical analysis works well when there are defined “knowns” such as a previous top (resistance) or bottom (support) from which to build analysis. However, when markets break out to new highs, it pretty much becomes a “wild @$$ guess” or “WAG.”

However, we did previously attempt to establish some reasonable targets based on relative “risk/reward ranges,”

“With the markets closing just at all-time highs, we can only guess where the next market peak will be. Therefore, to gauge risk and reward ranges, we have set targets at 3500, 3750, and 4000 or 4.4%, 12.2%, and 19.5%, respectively.”

“Given there is no good measure to justify upside potential from a breakout to new highs, you can personally go through a lot of mental exercises. While there is certainly a potential the market could rally 19.9% to 4000, it is also just as reasonable the market could decline 22.2% test the March closing lows.

Just in case you think that can’t happen, just remember no one was expecting a 35% decline in March, either.”

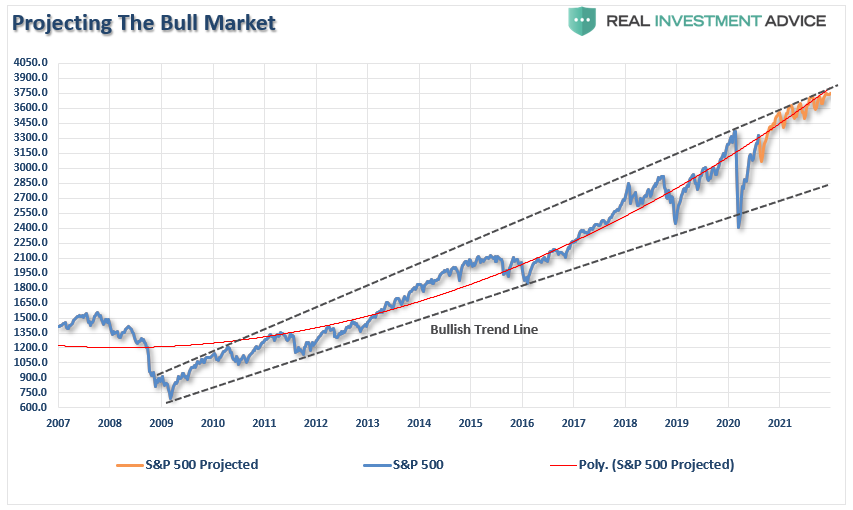

We then delved into establishing a targetusing the well-established trendlines from the 2009 lows. Given these trendlines have held for over a decade, we can only reasonably assume they will hold in the future. Therefore, since the upper bullish trend line coincides with the February 2020 market peak and the polynomial trend line, 3750 is the next reasonable target.

However, the most critical point of that article was the extreme deviation from long-term means. As noted, trend lines and moving averages tend to act as “gravity.” The further away the market moves from the trendline, the greater the pull becomes.

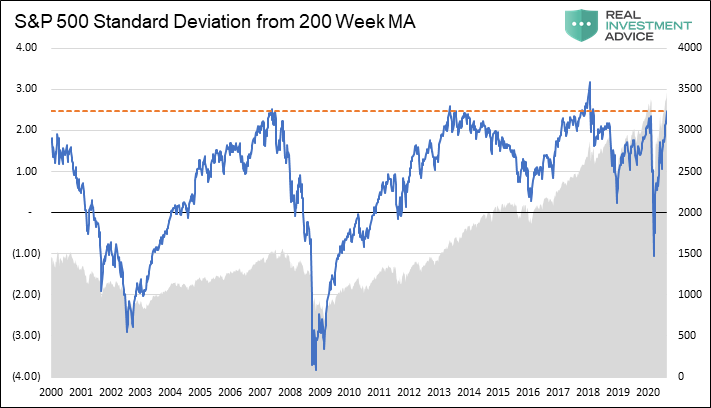

“Kyōki is the Japanese word for “insanity.” That was the word that came to mind when my co-portfolio manager, Michael Lebowitz, emailed me the following chart.”

“The chart is WEEKLY data, which smooths out some of the short-term volatility. What is displayed is the standard deviation of the market from its 200-WEEK (4-year) moving average.

Notably, each time of the 5-times previously, going back to 1999, where the market traded at 2-standard deviations or higher from the 4-year moving average, a reversion occurred. Those periods were 2000, 2007, 2014, 2018, February 2020, and now.”

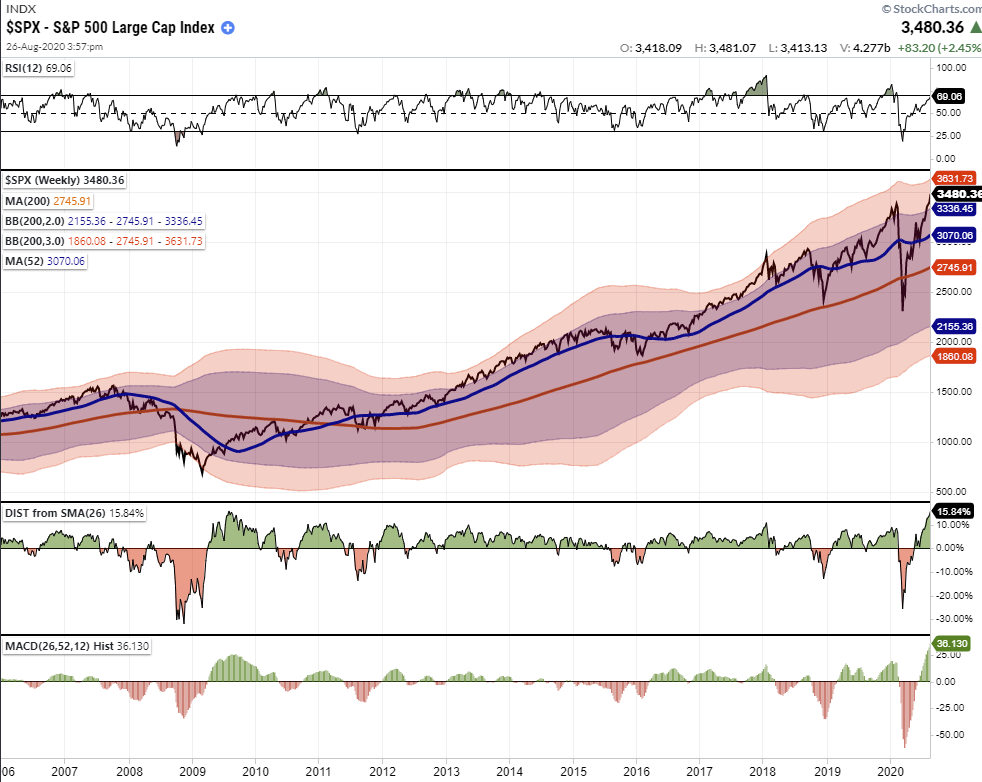

It is remarkable given the economic devastation; the S&P 500 is trading at not only at record highs, but at near-record deviations of the 4-year moving average and MACD readings. Historically, such deviations resolve through a correction or a full-fledged bear market.

“Like a rubber band that has been stretched too far – it must be relaxed in order to be stretched again. This is exactly the same for stock prices that are anchored to their moving averages. Trends that get overextended in one direction, or another, always return to their long-term average. Even during a strong uptrend or strong downtrend, prices often move back (revert) to a long-term moving average.”

More Signs Of Exuberance

While prices are clearly at historic extremes on many levels, we continue to see more numerous indicators showing extreme signs of “exuberance” in the markets.

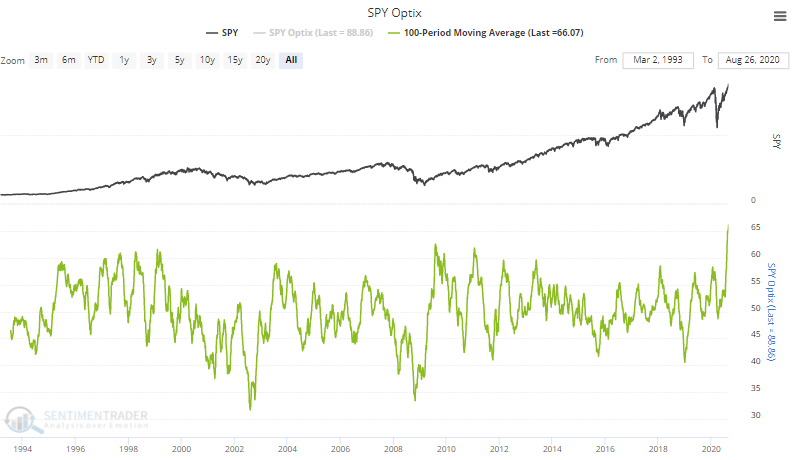

This tweet from Sentiment Trader summed it up best.

Speculative options trading reached the equivalent of 12% of NYSE volume last week.

Like some combustible combo of musical chairs, Russian roulette, and five finger fillet.

As noted in the weekly charts above, the S&P is also trading at extreme levels above its shorter-term daily moving averages as well.

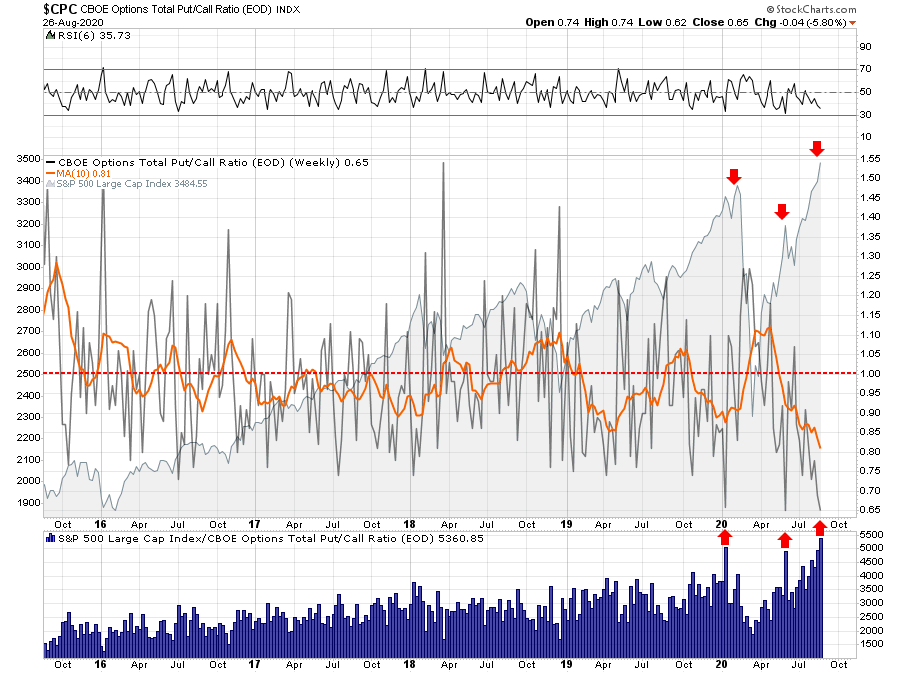

With “shorts” now at historically levels, market participants have given up hedging portfolios against a correction. Historically low put/call ratios have always coincided with short-term corrections or worse. It is one of the lowest levels since the peak of the market in 1999.

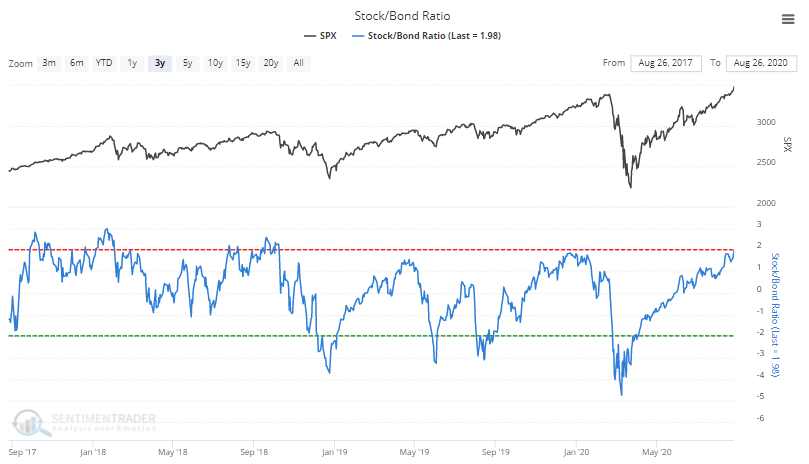

The stock/bond ratio has also reached levels more normally consistent with short-term market peaks and corrective actions.

The rise in the stock/bond ratio is not surprising, given the level of exuberance by retail investors.

None of this data means the market is about to crash.

What it does mean, as we discussed last week in “Winter Approaches,” is that a correction of 5-10% has become increasingly likely over the next few weeks to two months. While a 5-10% correction may not seem like much, it will feel much worse due to the high level of complacency by investors currently.

All of the data suggests that “Winter Is Coming.” Therefore, this is why we are adding “value” to our portfolios to prepare for colder weather.

Is There A Rotation To Value Coming

Why value?

As Michael Lebowitz, CFA previously noted:

“As a result of these behaviors, we have witnessed a divergence in what has historically spelled success for investors. Stronger companies with predictable income generation and solid balance sheets have grossly underperformed companies with unreliable earnings and over-burdened balance sheets. The prospect of majestic future growth has trumped dependable growth. Companies with little to no income and massive debts have been the winners.”

This underperformance of “value” relative to “growth” is not unique. What is unusual is the current duration and magnitude of that underperformance. Such underperformance was only seen previously in 1999-2000.

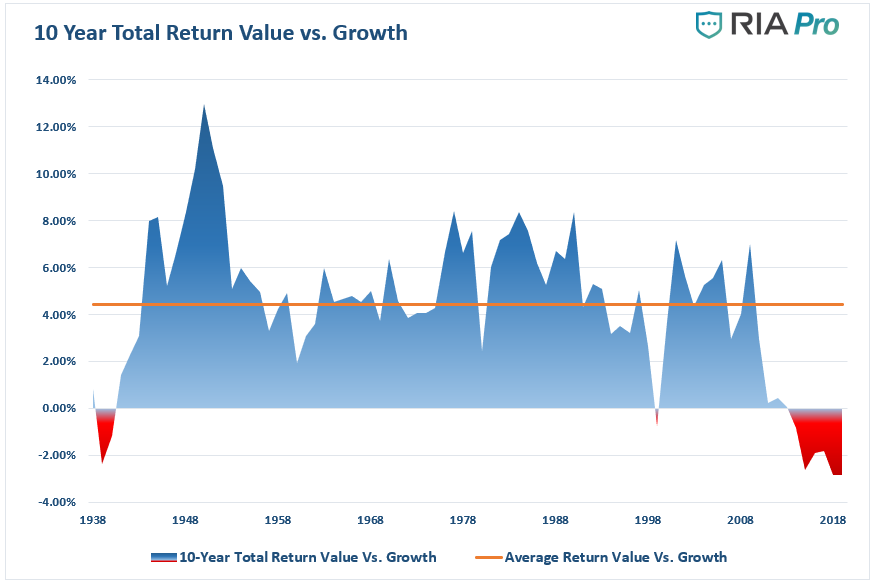

10-Year Total-Return Failure

The graph below charts ten-year annualized total returns (dividends included) for value stocks versus growth stocks. The most recent data point representing 2019, covering the years 2009 through 2019, stands at negative 2.86%. Suchindicates value stocks have underperformed growth stocks by 2.86% on average in each of the last ten years.

The data for this analysis comes from Kenneth French and Dartmouth University.

There are two critical takeaways from the graph above:

Over the last 90 years, value stocks have outperformed growth stocks by an average of 4.44% per year (orange line).

There have only been eight ten-year periods over the last 90 years (total of 90 ten-year periods) when value stocks underperformed growth stocks. Two of these occurred during the Great Depression, and the other spanned the 1990s leading into the Tech bust of 2001. The other five are recent, representing the years 2014 through 2019.

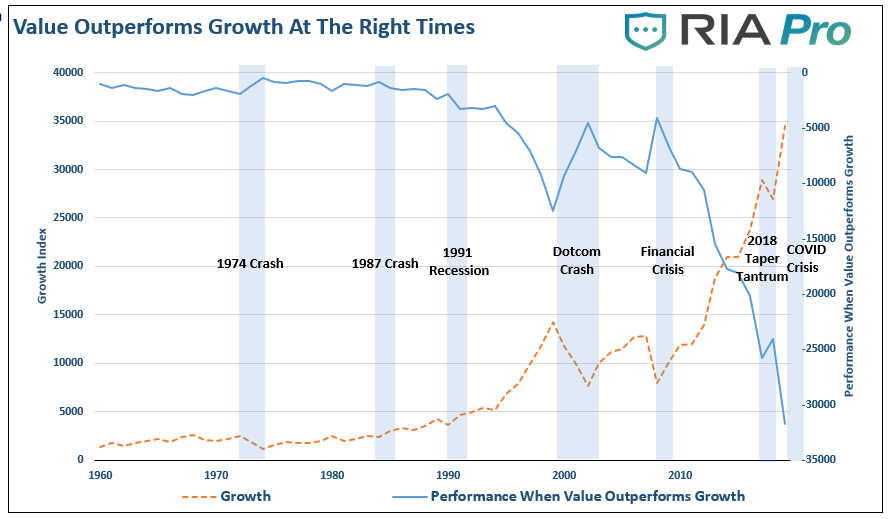

Mirror Opposites

The chart shows the difference in the performance of the “value vs. growth” index. The value and growth indices are each based on a $100 investment. While value investing always provides consistent returns, there are times when growth outperforms value. The periods when “value investing” has the most significant outperformance, as noted by the “blue shaded” areas, are notable.

The question is, what are the causes of this underperformance, and eventually, outperformance.

“The Fama–French value factor, and value investing in general, has suffered an extraordinarily long 13.3 years of underperformance relative to the growth investing style.The current drawdown has been by far the longest as well as the largest since July 1963.

An investment strategy, style, or factor can suffer a period of underperformance for many reasons.

First, the style may have been a product of data mining, only working during its backtest because of overfitting.

Second, structural changes in the market could render the factor newly irrelevant.

Third, the trade can get crowded, leading to distorted prices and low or negative expected returns.

Fourth, recent performance may disappoint because the style or factor is becoming cheaper as it plumbs new lows in relative valuation.

Finally, flagging performance might be a result of a left-tail outlier or pure bad luck.

If the first three reasons imply the style no longer works, and will not likely benefit investors in the future, the last two reasons have no such implications.

With today’s value vs. growth valuation gap at an extreme (the 100th percentile of historical relative valuations), it sets the stage for a potentially historic outperformance of value relative to growth over the coming decade.”

The reasons for underperformance are also the reasons for potential outperformance in the future. When something in the market ultimately goes “pear-shaped,” the return to value tends to be a swift event.

Such is the reason we are starting to add value to our portfolio. When “winter comes,” we have little doubt the value-growth relationship will revert to its long-term mean.

Our college recently penned a similar report for our RIAPro Subscribers:

While the current market advance seems to be unstoppable, such was always what investors believed at every prior market peak in history. As Howard Marks once stated:

“Rule No. 1: Most things will prove to be cyclical.

Rule No. 2: Some of the most exceptional opportunities for gain and loss come when other people forget Rule No. 1.”

The realization that nothing lasts forever is crucial to long term investing. To “buy low,” one must have first “sold high.” Understanding that all things are cyclical suggests that after significant price increases, investments become more prone to declines than further advances.

The rotation from “growth” to “value” is inevitable. It will occur against a backdrop of devastation for the majority of investors quietly lulled into the extreme sense of complacency years of monetary interventions have provided.

As Research Affiliates concludes:

“Overall, relative valuations are in the far tail of the historical distribution. If, as history suggests, there is any tendency for mean reversion, the expected future returns for value are elevated by almost any definition.”

The only question is whether you will be the buyer of “value” when everyone else is selling “growth?”

Portfolio Positioning

As we discussed last week in “Tending The Garden,” there is a good analogy between gardening and portfolio management. I put together a short video last week as a recap.

(We publish “3-Minutes” Monday-Thursday. Click here to subscribe to our YouTube channel for email notification of all of our video postings and live-streams.)

Such is where we are currently.

While we remain long-biased in our equity portfolios, we have begun to “harvest” some of our big winners (take profits), and do some “winter preparation” by adding to our defensive “value” oriented positions, and our risk hedges.

In the short-term, this will indeed provide some drag between our portfolio and the major market index. However, when the first “cold snap” washes across the markets, our preparation should protect our garden from “frostbite.”

We indeed remain “bullish” on the markets currently as momentum is still in play. However, just as any farmer is keenly aware of the signs “Winter” is approaching, we are just taking some precautionary actions. As noted last week:

“If you wait for the “blizzard” to hit, it will be too late to make much difference.”

via ZeroHedge News https://ift.tt/2ESh60L Tyler Durden