Futures Slump, Ignoring Korean Euphoria, After Iran Rejects Trump Enriched Uranium Demands

A steady rebound in US equities driven by peak insanity in Korea (where the two chip stocks that account for most of the market surged and sent the Kospi soaring more than 8% overnight) faded after a report that Iran’s Supreme Leader issued a directive that the country’s near-weapons-grade uranium must remain in the country, rejecting Trump’s key ceasefire demand, while oil and bond yields jumped as traders waited in mounting futility to see whether hopes of a peace deal in the Middle East would translate into tangible progress. As of 7:15am ET, S&P 500 futures fell 0.4% and Nasdaq futures slid 0.3% after otherwise very strong Nvidia’s earnings failed to ignite further strong gains in the artificial intelligence trade. Treasuries fell as Brent reversed earlier losses to climb 2% above $107 after Tehran’s response disappointed those hoping for de-escalation. JPMorgan CEO Jamie Dimon did not help, warning that interest rates may climb much further from current levels. Long-dated bonds around the world have tested multiyear highs in recent days on concern about an oil-driven spike in inflation and amid worries over government spending.

Yesterday’s Nvidia earnings proved to be a dud: Nvidia shares were unchanged (crushing both put and call buyers as the implied vol collapse) in US premarket trading after the AI chipmaker reported Q1 results and gave a forecast amid increased investor skepticism. While analysts were broadly positive, some also questioned the sustainability of growth, especially amid higher competition. Intuit sank 13% after the software company said it plans to reduce its workforce by about 17%. The shares of space exploration and satellite internet companies were broadly steady after Elon Musk’s SpaceX filed publicly for an initial public offering. Tesla advanced 1.6%, while other Mag 7 stocks were mixed (Amazon +0.6%, Alphabet +0.3%, Meta -0.2%, Apple -0.3%, Microsoft -0.3%).

- Aevex Corp. (AVEX) is up 8.5% after the drone maker reported first-quarter earnings. The company also announced that it was awarded $15.6 million in contracts by the US Air Force.

- Applied Digital (APLD) jumps 11% after the company signed a 15-year lease valued at about $7.5 billion with a US investment-grade hyperscaler for its Polaris Forge 3 campus.

- Elf Beauty Inc. (ELF) is up 9.9% after the cosmetics company beat the average analyst estimate on major profit and revenue estimates. Meanwhile, the company forecast adjusted earnings per share for 2027 that fell short of expectations.

- Intuit (INTU) sinks 13% after the tax-preparation software company reported third-quarter results that were seen as disappointing for its TurboTax business. It also said it is cutting about 17% of its staff, confirming an earlier Reuters report.

- Nebius (NBIS) is up 8.4% after partnering with Bloom Energy to deploy fuel-cell technology to power its AI infrastructure build-out in the US. Bloom rises 2.6%.

In other corporate news, Samsung reached a tentative last-minute deal with its union, averting a potentially crippling strike scheduled to start on Thursday at the world’s biggest memory firm.

Virtually all overnight gains in the S&P faded just after 6am when Reuters blasted the following two headlines which poured cold water on expectations of a quick deescalation in the Iran war

- *IRAN SUPREME LEADER SAYS URANIUM MUST STAY IN IRAN: REUTERS

- *IRAN SUPREME LEADER ISSUES DIRECTIVE ON URANIUM: REUTERS

Almost overshadowed by headlines related to AI-disrupter Anthropic and SpaceX, Nvidia’s results produced the expected high growth. Nvidia’s revenue growth shows that the momentum of the debt-fueled AI data-center buildout is accelerating. While analysts are broadly positive, some also questioned the sustainability of growth, especially amid higher competition. Some also pointed to the company’s compute revenue miss as an early warning sign, especially with Nvidia changing the way it reports revenue so it masks this weakness going forward. Nvidia’s price reaction was expected to be more muted compared to the last few years – call open interest has been drifting lower. While this suggests a cooling in the speculative chase that previously defined the popular AI trade, it isn’t dimming the price action of peripheral beneficiaries – a windfall for Asian chip makers.

“Investors remain relentless in pursuit of supernormal returns offered by AI,” said Emmanuel Valavanis, an equity sales specialist at Forte Securities, noting how narrow the market has become given a “laser beam focus on AI, the biggest tech infrastructure build-out of 21st century.”

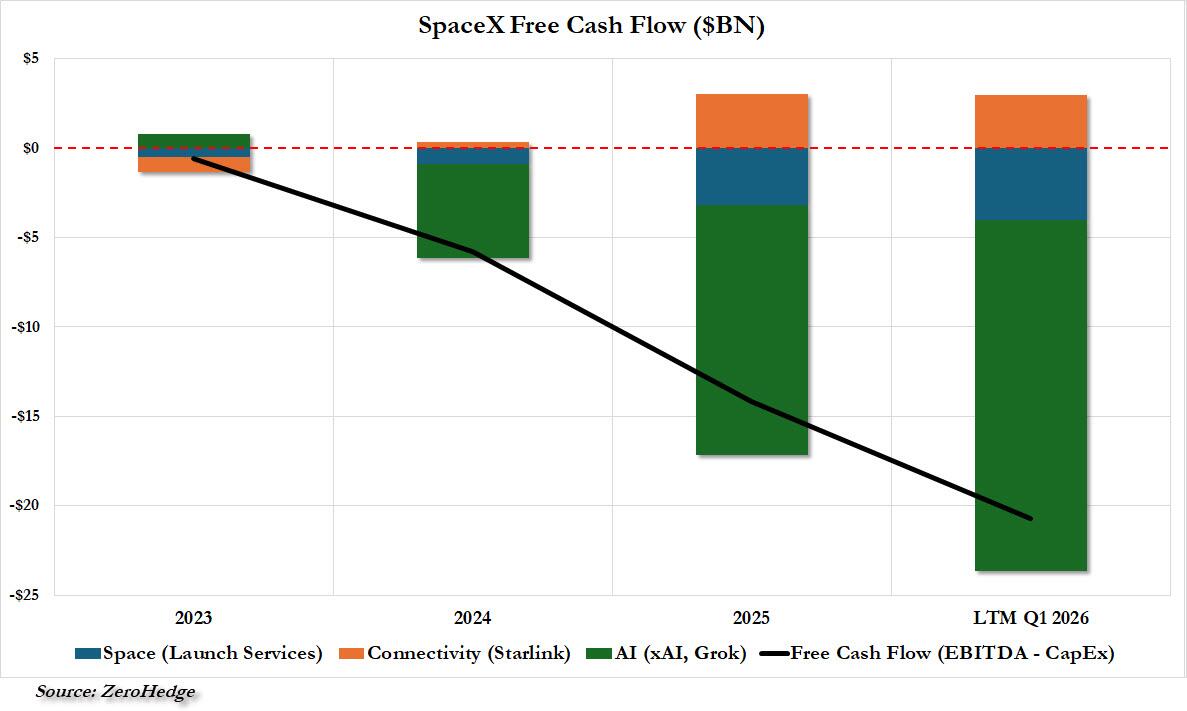

Shortly after the Nvidia results, SpaceX filed publicly for what stands to be the largest-ever IPO, revealing billions in losses and a super-voting share plan allowing Elon Musk to keep the company under his control. SpaceX had a net loss of $4.28 billion on revenue of $4.69 billion for the first quarter, compared with a net loss of $528 million on revenue of about $4 billion a year earlier, the filing shows.

While this will surely change, for now SpaceX is now a cash incinerating machine, with nearly $25BN in cash burn in the last 12 months.

“We believe that our current space efforts will catalyze transformative breakthroughs that could reshape terrestrial industries and lead to the emergence of new trillion-dollar markets on the Moon, Mars, and beyond.” Space Exploration said in its Form S-1.

Elsewhere Jamie Dimon said interest rates may climb much higher from current levels, while his firm will likely hire more AI specialists and fewer traditional bankers as the adoption of the technology accelerate.

The muted tone in US markets contrasted with buoyant optimism in Asia, where a key tech gauge jumped the most in six weeks.

Overnight Asia saw stock market fireworks with Korea’s LG Electronics and Hyundai Mobis both surging in Seoul after Nvidia CEO Jensen Huang touted new opportunities offered by robots and automated vehicles. SoftBank Group Corp. jumped 20% as two companies backed by the Japanese investor – OpenAI and SB Energy Corp. – were said to be preparing for initial public offerings. Regional chipmakers tracked Wednesday’s gains in US peers.

“The rally in Asia has been supported by very strong momentum in technology, particularly around the current reality of AI demand,” said Francisco Simón, European head of strategy at Santander Asset Management. “Looking ahead, investors also continue to see structural growth potential linked to the future evolution of AI, including companies that may emerge as leaders.”

European shares edged higher after early declines as investors digested earnings reports and purchasing managers’ index data from across the region. The Stoxx 600 rose 0.4%, British defense technology firm QinetiQ was among the top gainers after posting strong results and announcing a new share buyback programme, while Ubisoft slumped on weak bookings. Here are the biggest movers Thursday:

- QinetiQ shares jumped as much as 11%, the biggest daily rise in over a year, after earnings showed a profit beat and a buyback initiative.

- Investec rallied as much as 5.3% in London to its highest intraday level since April after the specialist lender reported net income for the full year that beat the average analyst estimate.

- Generali shares rose as much as 2.9%, the best performer on the Stoxx 600 Insurance Index, after the Italian insurer reported what analysts say are strong 1Q earnings.

- CSG shares rose as much as 5.9% after Oddo BHF upgraded the defense company to outperform from neutral, saying there is potential for significant re-rating after a short attack sent the stock plunging earlier this month.

- Naturgy Energy Group shares gained as much as 3.4%, trading at their highest level since 2022, after receiving upgrades from Morgan Stanley and BNP Paribas.

- Alfen rose as much as 25% after a Jefferies upgrade gives it a sole buy rating, with the energy-equipment company seen favorably positioned to capitalize on the energy transition theme, with double-digit growth in all end-markets.

- Greece’s Public Power rose as much as 6% to a record high after it concluded a share capital increase on Wednesday.

- Hexagon shares fell as much as 18% on Thursday, their first day of trading excluding rights to the company’s upcoming spin off of its subsidiary Octave.

- Ubisoft shares slumped as much as 19% on Thursday after the video game maker guided to a high single-digit percentage drop in net bookings for the coming fiscal year, well below expectations.

- Convatec shares dropped as much as 5.6%, worst performer in the Stoxx 600 Health Care Index on Thursday morning, after the medical products and equipment manufacturer provided an update for the first four months of 2026.

- MaaT Pharma shares plunge as much as 61%, the most on record, after the French biotech company said its experimental therapy Xervyteg for acute graft-versus-host disease is likely to be turned down by the European Medicines Agency.

- Autotrader falls as much as 4.8%, most since Feb. 3, after a soft earnings report which analysts said will weaken confidence in the online vehicle marketplace. The stock has lost about a fifth of its value this year.

- Elior slumped as much as 26%, the most since November 2024, after the French catering and food services company’s first-half results came in significantly below expectations and it lowered guidance for the full year.

Investors are also getting a reading into business activity in major economies against a backdrop of rising energy costs. The data compiled by S&P Global are closely watched as they arrive early in the month and are good at revealing trends and turning points. In the UK, businesses posted the first decline in output in over a year as the Iran shock and a mounting rebellion against Prime Minister Keir Starmer hit activity in the services sector. In the euro area, activity shrank at the quickest pace in 2 1/2 years.

Earlier in the session, Asian equities snapped a four-day losing streak, with a rally in tech shares and easing Middle East tensions helping lift sentiment. The MSCI Asia Pacific Index rose as much as 2.8%, the most over a month. South Korea’s Kospi surged more than 8% to lead gains in the region after Samsung Electronics reached a tentative deal with its labor union. Shares in Taiwan and Japan also jumped. Chip heavyweights contributed the most to the Asian benchmark’s gains. Meanwhile, SoftBank Group shares soared in Japan after reports said that two of the companies it backs are preparing to list in the US.

Walmart, Ralph Lauren and Deere are among companies expected to report results before the market opens. While confident in its ability to win market share, Walmart is unlikely to raise full-year guidance given persistent uncertainties from higher fuel and freight costs, Citi said. Numbers from Take-Two and Workday follow later in the day.

In commodities, Brent crude futures are up 2% to near $107 a barrel, erasing an earlier fall, after a report that Iran’s Supreme Leader has issued a directive that the country’s near-weapons-grade uranium should not be sent abroad. European stocks surrendered gains and turned red on the news, while US equity futures dropped. Precious metals extended declines.

Bonds also sold off, with the decline in Treasuries pushing US 10-year yields up 3 bps to 4.61%. European government followed suit, led lower by shorter dated maturities.

In FX, the Bloomberg Dollar Spot Index is up 0.2% while the Swedish krona and Aussie dollar slipped to the bottom of the G-10 FX pile, losing 0.4% each. While a resolution could put the dollar under selling pressure, conviction of a lasting peace deal is lower, ING strategists say. “The dollar’s contained reaction to Trump’s comments leaves a relatively larger scope for further downside if a deal is indeed about to be agreed,” they write in a note; “But it also confirms thinner market patience, and a new period of a stall in negotiations could end up taking DXY above the 99.50 mark even without any new military re-escalation.”” At the same time significant downside in the currency may be limited given hawkish FOMC minutes on Wednesday, strategists say

Looking at today’s calendar, we get Housing starts for April, Philadelphia Fed business outlook, and initial jobless claims through May 16 are due at 8:30 a.m. ET, followed by provisional PMI data for May at 9.45 a.m.

Market Snapshot

- S&P 500 mini -0.3%

- Nasdaq 100 mini -0.3%,

- Russell 2000 mini -0.3%

- Stoxx Europe 600 +0.4%,

- DAX +0.5%,

- CAC 40 +0.3%

- 10-year Treasury yield +2 basis point at 4.60%

- Bloomberg Dollar Index little changed at 1201.2,

- euro little changed at $1.163

- WTI crude -0.1% at $98.13/barrel

Top Overnight News

- Iran’s Supreme Leader has issued a directive that the country’s near-weapons-grade uranium should not be sent abroad, two senior Iranian sources said, hardening Tehran’s stance on one of the main U.S. demands at peace talks. RTRS

- Pakistan stepped up diplomatic efforts on Thursday to hasten U.S. and Iran peace talks, as Tehran said it was reviewing Washington’s latest responses and President Donald Trump suggested he could wait a few days for “the right answers” from Tehran but was also willing to resume attacks on the country. RTRS

- Tehran is studying the American text and has not yet submitted its response. Pakistan is working to bring closer the viewpoints between the US and Iran. Iran is in the process of responding to the text sent by the US and that “the sent text has reduced the gaps to some extent”, but requires guarantees: Al Arabiya and ISNA

- The US will open a new consulate building in Greenland, renewing concerns over Washington’s designs for the island. Protests are planned. BBG

- Beijing is holding up a proposed visit by the Pentagon’s top policy official as China pressures Donald Trump over a $14bn weapons package for Taiwan. FT

- The Trump administration is awarding $2 billion in grants to nine quantum-computing companies in deals that include U.S. government equity stakes. WSJ

- Anthropic’s revenue is set to more than double to $10.9 billion in the second quarter, an explosive rate of growth that will help it turn an operating profit for the first time. WSJ

- The RBI is considering all available options to stabilize the rupee, including an interest-rate hike, more currency swaps and raising dollars from investors overseas, people familiar said. BBG

- Euro-area business activity shrank at the quickest pace in two and a half years, adding to fears that the Iran war and surge in energy costs are dealing a severe blow to the economy. BBG

- The Fed proposed a new type of limited payment account to give fintech firms greater access to the US payments system. BBG

Iran

- Tehran is studying the American text and has not yet submitted its response, Al Arabiya reported citing sources. Pakistan is working to bring closer the viewpoints between the US and Iran. ISNA further reported that Iran is in the process of responding to the text sent by the US and that “the sent text has reduced the gaps to some extent”, but requires guarantees.

- “According to my sources in Tehran, Iran’s response hasn’t been handed to the Pakistani mediator. There’re ongoing deliberations, and serious efforts to reach a final draft,” according to Al Jazeera’s Hashem.

- “Pakistan’s mediation efforts between US and Iran are at a crucial stage where efforts are underway to secure an agreement or a framework for comprehensive talks which can eventually lead to a ‘deal’,” according to journalist Mallick.

- Pakistani source tells Al Jazeera the Army Chief is still in Pakistan and his visit to Iran depends on the outcomes of the interior minister’s visit, enriched uranium is the main sticking point in the US-Iranian negotiations.

- Pakistan’s Army Chief is to travel to Tehran on Thursday for negotiations and as part of mediation efforts between the US and Iran, ISNA reported.

- Pakistani political and media circles point to accelerated mediation efforts after Pakistani Interior Minister’s Tehran meetings, IRNA reported. The report adds that presenting a narrative that indicates that progress in negotiations between Tehran and Washington is likely.

- Iran’s Foreign Ministry spokesperson said Iran is pursuing talks “in good faith” but views US with “deep suspicion”, Press TV reported. Confirms multiple rounds of messages have been exchanged through Pakistani intermediaries based on the 14-point proposal.

- Iranian official said they are ready to use new weapons if the US makes an additional act of aggression again, while he said they have produced and advanced weapons inside the country that have not yet been used on the battlefield and have not yet been tested. Furthermore, the spokesman stated that in terms of equipment and defensive capabilities, they are not experiencing any shortages that would prevent the defence of the country, and this time, they do not intend to act with restraint.

- IRGC said forces are ready to respond to any enemy aggression and all armed forces are ready with fingers on the trigger, according to SNN and Tasnim.

A more detailed look at global markets courtesy of Newqsuawk

APAC stocks mostly rallied as the region took impetus from the gains on Wall Street, with global risk sentiment underpinned following a slide in oil prices due to increased optimism regarding a resolution to the Middle East conflict, after President Trump stated that they are in the final stages of talks with Iran. Furthermore, it was also reported that the Pakistani Army Chief may visit Iran today to announce the achievement of a final draft agreement, while the US side gave Iran a text through a Pakistani mediator after having received Iran’s 14-point text a few days ago. ASX 200 climbed higher with the gains led by outperformance in the real estate, mining and materials industries, while the index also shrugged off the weak flash PMIs and disappointing jobs data. Nikkei 225 surged higher amid the decline in energy prices and heavy buying in tech stocks, with SoftBank shares up around 20% following the earnings beat from NVIDIA, while there was a slew of data from Japan which were ultimately mixed, but included stronger-than-expected trade figures. KOSPI outperformed amid tech strength with SK Hynix surging by a double-digit percentage, while Samsung Electronics was boosted by an eleventh-hour tentative wage agreement with the labour union to avert an 18-day mass walkout. Hang Seng and Shanghai Comp lagged despite the increased liquidity effort by the PBoC, with price action rangebound and Chinese markets constrained amid weakness in energy stocks and automakers.

Top Asian News

- Japanese Finance Minister Katayama said Japan’s fiscal policy is proactive and not expansionary.

- Japan’s draft extra budget is reportedly around JPY 3tln, while it was also reported that Japan plans to spend JPY 500bln in reserve funds on energy measures.

- India is said to weigh options to boost the rupee, including a rate hike, with the RBI also considering options such as currency swaps and raising dollars from overseas investors.

- South Korea’s NPS may hike domestic stock holding target by 5 percentage points amid rises in domestic stock market, Maeil reported.

European bourses (STOXX 600 +0.3%) are entirely but modestly in the green, ex. FTSE 100 (-0.1%). Signs of an end to the Iran war seem to be emerging, with President Trump saying the US is in the final stages of negotiations with Iran, while Al Arabiya reported that Tehran is studying the American text. The source report added that Pakistan is working to bring closer the viewpoints between the US and Iran. Elsewhere, EZ flash PMIs disappointed, with commentary continuing to highlight stagflation worries despite ECB Lagarde’s persistence in moving away from the language. European sectors point to a positive bias. Autos (+1.2%) and Retail (+0.6%) top the sector pile while Energy (-0.2%) and Banks (-0.2%) underperform.

Top European News

- EU Commission downgrades 2026 GDP growth forecast to 0.9% (prev. 1.2%), 2026 inflation revised to 3.00% (prev. 1.9%).

- UK Chancellor Reeves is to announce cuts to food tariffs and children’s bus fares on Thursday in a cost-of-living push to win back voters. It was separately reported that Reeves will not announce a proposed voluntary cap on supermarket prices for essential groceries following strong backlash from the sector, according to Financial Times. Furthermore, Politico reported that Reeves is to announce a cut to agrifood tariffs on some products and a rise in mileage rates.

FX

- The Dollar index is unchanged on the day and returns to Thursday’s lows around 99.00 after chopping on geopolitics and soft EZ/French data. Action ultimately dictated by geopolitics, with reports recently sounding constructive and has outweighed the Dollar positive factors which incl. poor EZ PMI metrics and hawkish FOMC Minutes.

- EUR saw decent weakness on dismal French data, which heightened the possibility of EZ-US differentials widening. French PMIs marked the steepest contraction since late 2020. Services and composite were expected to be broadly unchanged from priors, though both slipped significantly further into contraction territory. The Manufacturing picture was better, though the metric still fell into contraction. The EZ figure was also poor but provided some reprieve for the single currency. EZ Manufacturing was resilient, though still fell below expected and previous, while composite and services fell further into contraction. As the French series was released, EUR/USD saw a move c.24 pips lower to a 1.1594 trough, though pared some downside as German/EZ figures were not as bad as feared according to the indications from France.

- JPY remains reluctant to deviate from the 159.00 mark despite hawkish remarks from BoJ’s Koeda. JPY fundamentals remain bearish amid reporting around the Supplementary Budget and terms of trade. Koeda’s remarks overnight, “BoJ needs to continue to raise the policy interest rate”, mark the second non-dissenting member to indicate willingness to tighten policy (Masu+Koeda). This shows that last meeting’s 6-3 vote split will be vulnerable in June’s meeting, with the aforementioned members’ remarks indicating a possible 5-4 vote split for a hike, where interest rate futures currently imply a 77% probability of such action.

Central Banks

- BoJ Board Member Koeda said the BoJ needs to continue to raise the policy interest rate in response to developments in economic activity and prices, as well as financial conditions, while she thinks the BoJ needs to continue examining the extent to which underlying inflation is anchored. Koeda said given the situation in the Middle East, she sees some possibility that underlying inflation may exceed 2% looking ahead, and noted it is reasonable for BoJ to raise the policy interest rate at an appropriate pace to address high inflation, whilst also considering the trade-offs for the economy. Furthermore, she warned that if real interest rates continue to deviate markedly in a negative direction from the natural rate of interest, unintended distortions could arise in future resource allocation, as well as stated that the BoJ should proceed steadily with normalising its balance sheet in a predictable manner, while ensuring flexibility.

- ECB’s Rehn said economy is moving towards the adverse scenario of projections; may need to raise rates to maintain credibility.

- Norges Bank Expectations Survey (Q2): 12-month ahead CPI 3.3% (prev. 2.8%), 2026 real wages 1.1% (prev. 1.3%).

Fixed Income

- USTs are off by a few ticks, but have been clambering off worst levels throughout the European session; currently towards the upper end of a 109-05 to 109-12 range. Wednesday saw sentiment lift amidst positive geopolitical newsflow, and this has continued into today’s session. Most recently, reports have suggested that Iran is in the process of responding to the text sent by the US, adding that it has “reduced the gaps to some extent”. This led to some pressure in the energy complex, in turn, lifting US paper.

- Bunds trade firmer today and towards the upper end of a 124.71 to 125.12 range. Strength today has been facilitated by a) geopolitical optimism (see above), and b) a dire set of PMI metrics. In brief, the French figures were awful, with Manufacturing surprisingly slipping into contractionary territory and Composite/Services also deteriorating; the German metrics also indicated the downbeat Manufacturing environment, but were more or less in line with expectations. The EZ-wide figure concluded that activity in the region is softening across both the Manufacturing and Services; “The survey data indicate that the euro area economy looks set to contract by 0.2% in the second quarter”. The report concludes by suggesting that price gauges suggest inflation is running close to 4%, which, alongside slowing growth, “creates a deepening dilemma for policymakers”.

- Gilts move higher alongside the pressure in the crude complex. The region had its own PMI metrics to digest. Manufacturing remained solid whilst Services surprisingly fell into contractionary territory. UK paper was choppy in reaction to the data, but ultimately little moved – perhaps as attention turns to Chancellor Reeves, who is due to speak at 11:30 BST. Reports suggest that she will announce targeted cuts to agrifood tariffs expected to save consumers more than GBP 150mln annually. She is also expected to announce free summer bus travel for children, and a GBP 400mln package for motorists and hauliers, including a postponed 5p fuel duty rise. Political analysts view her speech as an attempt to secure herself as the Labour Party’s long-term chancellor in the midst of recent political turmoil

Commodities

- In geopolitics, US President Trump said Iran talks were in the “final stages” but warned the US could get “a little bit nasty” if no deal is reached, while stressing sanctions relief would only come after an agreement. Iran said dialogue was continuing around its 14-point proposal, but rejected surrender, ultimatums or deadlines. Tehran is studying the American text and has not yet submitted its response.

- WTI and Brent crude futures are moving lower following the aforementioned constructive geopolitical headlines. WTI Jul briefly topped USD 100/bbl before returning under the level, currently in a USD 97.29-100.11/bbl range. Brent Jul resides in a 103.68-106.80/bbl parameter. Dutch TTF is now softer by over 1%, with downticks also seen in light of the constructive US-Iran commentary.

- Spot gold is contained to a USD 4,512-4,570/oz range, on a modestly softer footing intraday but off extremes as the yellow metal moves in lockstep with the USD, which is influenced by energy prices. Spot silver found intraday resistance at USD 77/bbl before printing a USD 74.67/oz low.

- Base metals are lower despite the broader optimism from the US-Iran relatively flat DXY at the time of writing, whilst PMI data in Europe pointed to an overall bleak picture, with the data pointing to contractions in the EZ and the UK. 3M LME copper resides in a USD 13,477.65- 13,713.40/t range.

- ADNOC said that while it can ramp up its oil production in a matter of weeks, it will take 4 months for oil flows through Hormuz to return to 80% of pre-war levels.

- China raises gas and diesel prices by CNY 75 and CNY 70 per ton, respectively, from May 22nd.

- UAE’s new pipeline that bypasses the Strait of Hormuz is reportedly around 50% complete.

- Goldman Sachs said global oil stockpiles fell at a record pace of 8.7mln bpd so far in May, while it added that physical markets continue to tighten with estimated oil exports through the Strait of Hormuz remaining at a very low 5% of normal.

Geopolitics

- Ukraine’s Drone Forces commander said Ukrainian drones attacked Russia’s Syzran oil refinery (147k-170k capacity) in the Samara region of Russia.

- US Defence Undersecretary Colby may visit China ahead of a possible trip by Pentagon chief Hegseth amid tension over Taiwan arms sales, SCMP reported.

- US deployed the USS Nimitz carrier strike group to the Caribbean in a show of force as President Trump pressures Cuba, according to NYT.

- US President Trump said on Wednesday he would speak with Taiwan’s President Lai in an unprecedented move for a US leader that could roil US relations with China, according to The Guardian.

- Beijing is reportedly holding up a proposed visit by a Pentagon top policy official as China pressures US President Trump regarding a USD 14bln arms sale to Taiwan, according to FT.

- Chinese President Xi may visit North Korea by as early as next week, according to Yonhap.

US Event Calendar

- 8:30 am: United States May 16 Initial Jobless Claims, est. 210k, prior 211k

- 8:30 am: United States May 9 Continuing Claims, est. 1786k, prior 1782k

- 8:30 am: United States May Philadelphia Fed Business Outlook, est. 17.8, prior 26.7

- 8:30 am: United States Apr Housing Starts, est. 1410k, prior 1502k

- 8:30 am: United States Apr P Building Permits, est. 1384k, prior 1363k

- 9:45 am: United States May P S&P Global US Manufacturing PMI, est. 53.8, prior 54.5

- 9:45 am: United States May P S&P Global US Services PMI, est. 51.2, prior 51

- 9:45 am: United States May P S&P Global US Composite PMI, est. 51.8, prior 51.7

Central Banks

- 11:20 am: United States Fed’s Goolsbee Speaks in Chicago Radio Interview

- 12:20 pm: United States Fed’s Barkin Speaks on the Economy

DB’s Jim Reid concludes the overnight wrap

Yesterday’s positive market mood has continued into Asian hours this morning, with the Kospi (+8.08%) and Nikkei (+3.58%) surging via a tech rally even as Nvidia’s eagerly awaited earnings drew a mixed response last night. This follows yesterday’s +1.08% gain for the S&P 500 on increased investor optimism that a US-Iran deal might materialise, leading to sharp declines for Brent crude (-5.63%) and a reversal in Treasury yields (-8.1bps on 10yr).

Starting with Nvidia, the chipmaker reported 85% yoy sales growth to $81.6bn last quarter and projected revenue of around $91bn in the current quarter (vs. $87.4bn est.). Despite the impressive growth and a 75% gross margin, that moderate sales guidance beat drew a lukewarm response from investors. Nvidia’s shares slipped by about 1% in post-market trading after a +1.30% gain yesterday that took it to a +19.8% gain YTD.

Futures on the Nasdaq and the S&P 500 are flat this morning following Nvidia’s results, but this comes after markets steamed ahead yesterday as the anticipation of good news on Iran brought oil prices and yields lower. The S&P 500 (+1.08%) rose for the first time in four sessions, with chipmakers and technology companies leading the way ahead of Nvidia’s results. The Philly Stock Exchange Index (+4.49%) rebounded strongly, with the Nasdaq (+1.54%) and the Magnificent-7 (+1.34%) also posting sizeable gains. European indices also rebounded, with the Stoxx 600 (+1.46%), CAC 40 (+1.70%), FTSE 100 (+0.99%) and DAX (+1.38%) all posting strong gains.

That positivity has carried over into Asian markets this morning. Japan’s Nikkei is up +3.58%, with Softbank surging +19.85% boosted by its roughly 13% stake in OpenAI as the WSJ reported that OpenAI is preparing to file an IPO in the coming days or weeks. Adrian Cox has written a quick note here on this overnight, putting the fundraising in some perspective. It would be double the previous largest IPO in history. Elsewhere, Korea’s KOSPI is soaring +8.08% with the likes of LG Electronics up +25.97% following Nvidia CEO Huang’s earnings call comments about the upside for physical AI and robotics. 8 stocks in the index are up by more than 15% as I type. Samsung (+5.35%) is also advancing strongly after reaching a tentative deal with its labour union to avoid a strike. The ASX is +1.63% higher but Chinese risk is broadly flat.

Before all that, it was rising optimism that the US and Iran might reach a deal that boosted markets yesterday. President Trump said that the US was in the “final stages” for a possible draft deal to end the conflict. Iran’s Tasnim news agency reported that Iran is reviewing the new draft US sent to Tehran in response to its 14-point proposal, while Axios reported that Trump and Israel’s Netanyahu had a tense call on Tuesday over the new peace proposal drafted by Qatar and Pakistan. That said, Trump did also threaten escalation, saying “We’ll either have a deal or we’re going to do some things that are a little bit nasty”. But overall investors jumped on potential, with Brent crude falling -5.63% to $105.02/bbl, whilst the 6-month ahead future fell -3.96% to $88.24/bbl. Brent is back up a modest +0.89% overnight.

The decline in oil helped Treasury yields retreat from Tuesday’s highs. The 10yr yield fell -8.1bps to 4.59%, though that still leaves it +23bps above where it was on May 8. The bond rally was led by breakevens, especially at the front-end, with the 1yr US inflation swap falling -13.9bps to 3.24%. Long-dated real yields also declined after the sharp repricing over the past week, with 30yr nominal (-5.8bps) and real (-5.7bps) yields retreating from post-GFC highs.

While the rates rally dominated the day, the minutes of this month’s FOMC meeting showed officials growing more open to the potential need to raise rates. In particular, a “majority of participants highlighted… that some policy firming would likely become appropriate if inflation were to continue to run persistently above 2 percent”, with “many” officials calling for the Fed to drop its easing bias as a result. As a reminder, three of the voting FOMC members had dissented in favour of dropping the bias.

European government bonds also saw significant relief, with yields on 10yr bunds down -9.6bps to 3.09%, while OATs (-11.2bps) and BTPs (-13.6bps) saw double digit declines amid the decline in oil prices. Those moves came as the final Euro Area April CPI was in-line with the flash reading at +3.0% y/y.

Here in the UK gilts outperformed after a big miss on April headline inflation (2.8% y/y vs 3.0% y/y expected). This was largely driven by weaker services inflation, which rose 3.2% y/y (vs 3.5% expected and down from 4.5% in March), though core CPI (2.5% y/y vs 2.6%) saw a more moderate downside miss. So combined with the global rally, that helped 10yr gilt yields to fall by -14.1bps to 4.99%, whilst the number of hikes priced in for the BoE in 2026 eased from 61bps to 47bps.

In overnight data, we’ve seen the first of the May flash PMI releases. The composite PMI declined in both Australia (from 50.4 to 47.8) and in Japan (from 52.2 to 51.1). Both manufacturing and services PMIs saw a deterioration, but it is services that led the decline, falling to 47.7 in Australia and a 14-month low of 50.0 in Japan. Meanwhile, Australia’s unemployment rate unexpectedly rose from 4.3% to 4.5% in April, marking its highest level since November 2021. The amount of further RBA hikes priced by year-end has declined from 34bps to 25bps following the data. In contrast, Japan trade figures were unexpectedly resilient in April, with +14.8% year-on-year export growth (vs. +9.2% expected) driving the economy to a third consecutive monthly trade surplus at ¥302bn, significantly outperforming expectations for a marginal deficit.

Flash PMIs will remain in focus later today, with the Eurozone, Germany, France, UK and US releases due. Other US data today includes weekly initial jobless claims (our economists expect these to edge slightly lower to 209k from 211k), the May Philadelphia Fed manufacturing survey, as well as April housing starts and building permits. In the Eurozone, we’ll also have May consumer confidence and the March current account data. Central bank speakers today include the ECB’s Villeroy and BoE’s Taylor. Notable earnings include Walmart and Generali.

Tyler Durden

Thu, 05/21/2026 – 07:38

via ZeroHedge News https://ift.tt/8KQGxYy Tyler Durden