Walmart Tumbles On Disappointing Guidance, Warns Low-Income Consumers Drowning

Extending concerns about US consumer weakness – now that the bumper OBBBA tax refund period is over – after yesterday’s earnings by Home Depot and Target, this morning Walmart reported Q1 earnings (the last big company to report, rounding out earnings season) and warned that fuel costs are squeezing the company’s bottom line and could lead to higher prices for shoppers.

In the latest quarter, the world’s largest retailer said comparable sales in US stores rose 4.1%, excluding fuel, in the latest quarter, slightly better than the 4.0% Wall Street analysts were expecting. That was the good news; the bad news is that Walmart also forecast adjusted profit for the second quarter that missed analysts’ expectations.

The results show that the company continues to gain market share across income levels with its focus on low prices, fast delivery and wide assortment. But the emphasis on affordability is facing pressure as inflation accelerates and the conflict in Iran drives up fuel prices.

Here is a snapshot of what WMT just reported, starting with the highlights:

- Revenue $177.75 billion, +7.3% y/y, beating estimates of $175.06 billion

- Walmart-only US stores comparable sales ex-gas +4.1%, estimate +4%

- Sam’s Club US comparable sales ex-gas +3.9%, estimate +3.59%

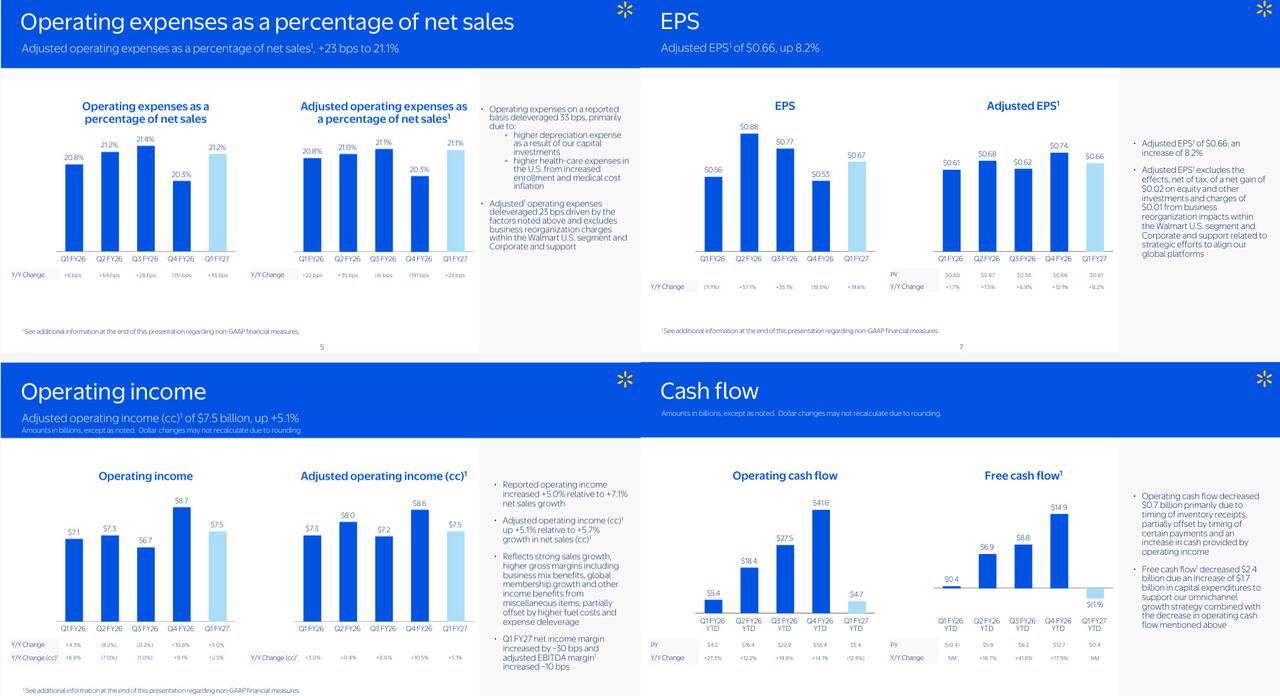

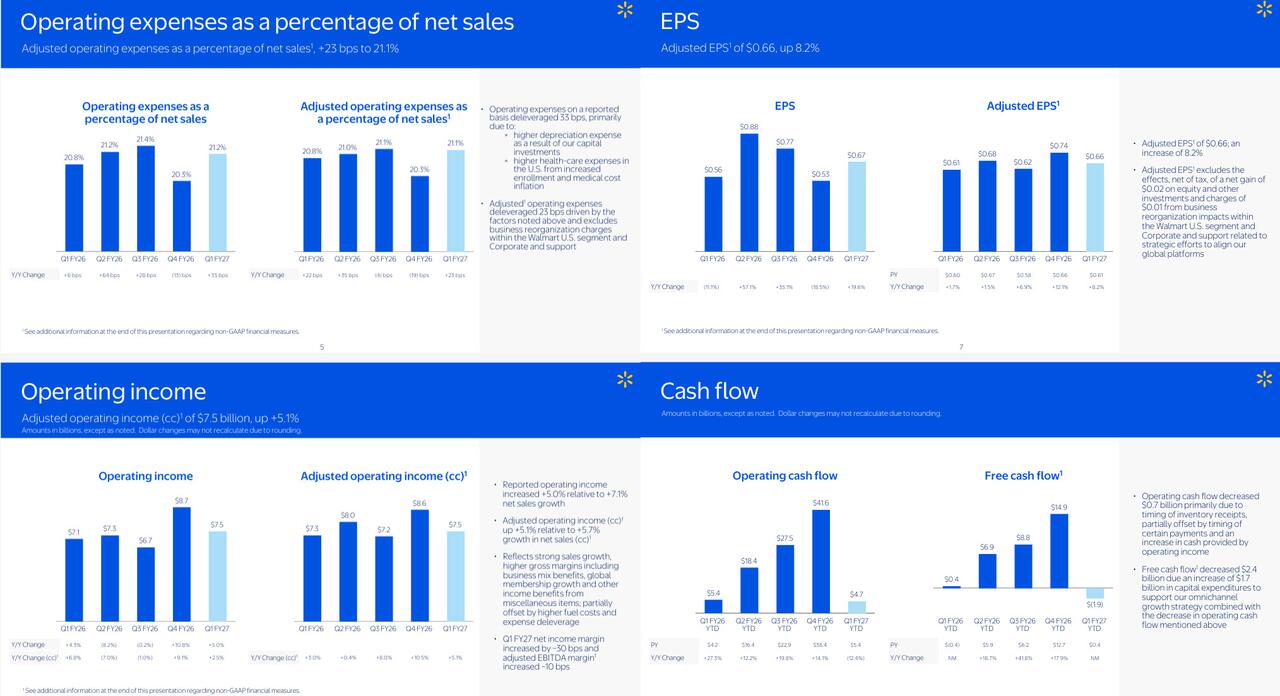

- Adjusted EPS 66c vs. 61c y/y, in line with exp. 66c

- Gross margin 24.3%, in line with exp. 24.3%

Going down the line:

- Change in US E-Commerce sales +26%, estimate +18.6%

- Operating cash flow $4.74 billion, -12% y/y

- Adjusted operating income $7.67 billion, estimate $7.69 billion

US e-commerce sales grew 26% during the quarter, fueling growth in the company’s biggest market. Sales of grocery and general merchandise rose mid single-digits. General merchandise, which consists of apparel, electronics and other discretionary items, gained the most share in five years.

Walmart also said that transactions at Walmart US rose 3%, while average ticket was up 1.1%, which means that WMT is still eating much of the input costs and making up for its with traffic. That however, will change very soon as the company revealed in its earnings call.

Walmart reported strong growth in grocery and general merchandise categories; partially offset by 100 bps headwind from maximum fair pricing legislation in pharmacy. Broad-based share gains across categories and income tiers led by upper-income households.

“The high-income consumer is spending with confidence in many categories, whereas the low-income consumer, we can tell, is more budget-conscious, trying to navigate certain financial distress,” Chief Financial Officer John David Rainey said in an interview with Bloomberg News. During the quarter, sales slowed somewhat in April after the Easter holiday. Higher tax refunds likely muted the impact of rising gas prices, though that’s abating, Rainey said. Prices rose 1.2% during the quarter and they could increase further if fuel prices stay where they are, he added, although that would surely lead to reduced traffic.

Translation: if it weren’t for upper income consumers, who are forced to trade down to discounters such as Walmart, earnings would have been a disaster.

And nowhere was this more obvious than in the company’s guidance, because while Q1 earnings were solid, the reason the stock is selling off sharply in premarket trading is the company’s disappointing forecast:

Second quarter forecast:

- Sees adjusted EPS 72c to 74c, both below the median estimate of 75c

- Sees net sales at constant currencies +4% to +5%

- Sees operating income at constant currencies up 7% to 10%

2027 full-year forecast

- Still sees adjusted EPS $2.75 to $2.85, below the median estimate $2.92

- Still sees net sales at constant currencies +3.5% to +4.5%

Walmart, which is viewed as an economic barometer due to its large size and footprint across the US and other markets, was the latest confirmation that the “lower half” of the K-shaped economy continues to sink, and it is only the upper half (that is increasingly shopping at WalMart) which is keeping the retailer afloat.

While spending has largely held up in recent years, consumers have become increasingly selective with their purchases. Good deals and unique products can still attract buyers.

But the biggest wildcard is that the higher tax refunds this year have given families some extra cash, but this benefit is now fading fast as we explained a month ago. While most prices of general goods haven’t risen as operators move existing inventory, this could change as the war drags on.

There’ more: fuel weighed on Walmart’s profit margin in the quarter, as the company absorbed “virtually the entirety” of the increases during the period, Rainey said. The company is prioritizing keeping prices low, with the number of discounts rising 20% from a year ago. That said, Reiney warned of potential higher retail price inflation in Q2 and H2 if the current elevated cost environment persists.

“It’s tough on very short notice to be able to navigate a cost headwind like that,” he said. While Walmart will be able to manage through it, he expects to see an equal or larger challenge related to fuel in the current quarter.

Rainey said that the number of gas gallons customers bought at Walmart stations fell below 10 for first time since 2022; he added that the decline in gas buying is sign of financial stress.

Walmart has consistently posted stronger results than many competitors, raising investors’ expectations and pushing the company’s forward PE to an insane 45x, a multiple that will soon get a painful reminder of what happens to multiples during consumer recessions.

Walmart’s cautious narrative echoes commentary from big-box peers Target Corp. and Home Depot which both signaled this week that consumers are staying resilient although purchases are slowing. Kraft Heinz, McDonald’s and other companies have also struck a cautious tone recently. The past year has been a roller coaster for consumer-facing companies, first with President Trump’s expansive, on-off tariffs, that in some cases roiled operations, and now with the ongoing geopolitical conflicts threatening to dampen demand.

The Bentonville, Arkansas-based retailer has said it seeks to gain market share during challenging economic times by focusing on value and essentials like groceries. Delivery and other online services have expanded Walmart’s base of clients to include wealthier shoppers. Advertising and other businesses are also contributing to profit growth and giving the company more room to further invest in lowering prices and improving store operations.

In particular, fast deliveries have been a growth engine, and the company’s efforts to make inroads into the fashion market are gaining traction. Walmart has also expanded the selection of merchandise on its marketplace of third-party vendors.

The company’s shares tumbled more than 3% in premarket trading in New York. The stock has risen 17% so far this year as of Wednesday’s close. Shares of Walmart’s peers, including Target and Kroger Co., also fell in premarket trading on Thursday.

Full Q1 investor presentation below (pdf link)

Tyler Durden

Thu, 05/21/2026 – 09:10

via ZeroHedge News https://ift.tt/3oraiEh Tyler Durden