Super El Nino: Famine Follows War?

Rory Green, TS Lombard’s chief China economist, is the latest Wall Street strategist to warn of the mounting macro and food inflation risks that a super El Niño could release on certain regions of the world.

In a note titled “Super El Niño: Famine Follows War?” Green warns that war-related disruptions to energy and fertilizer markets, compounded by adverse weather conditions, could create a perfect storm for global food prices.

Green said, “In general, El Niño raises temperatures and significantly exacerbates both drought and heavy rainfall. For global macro, it is an inflationary shock via the food price channel – a shock that will likely be compounded by existing war-related high fertilizer costs.”

He said within his coverage, “India is the most exposed to both growth and inflation risks, supporting our underweight Indian assets. Brazil and Mexico, too, will receive an inflation impulse.”

In recent weeks, the Japanese Meteorological Agency became the first major weather body to formally declare the onset of a super El Niño in the tropical Pacific.

If that forecast is correct, adverse climatic disruption could persist for 2 or more years, raising the risk of drought, flooding, lower crop yields, and higher food prices across key agricultural regions.

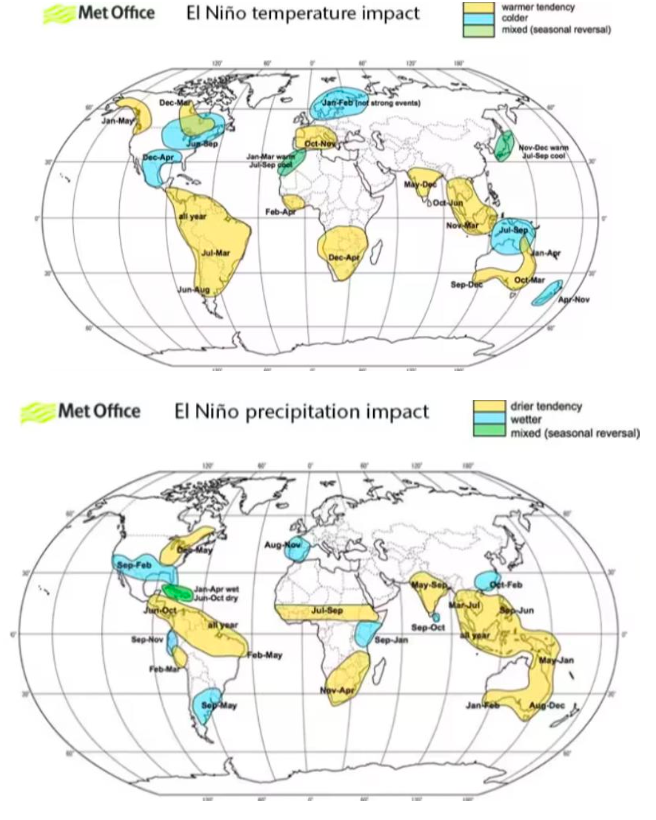

Green noted that El Niño has typically been associated with “hotter and drier conditions in India, parts of South and Southeast Asia, and Central America. But at the same time, it brings higher rainfall to parts of southern South America, the United States and Central Asia.”

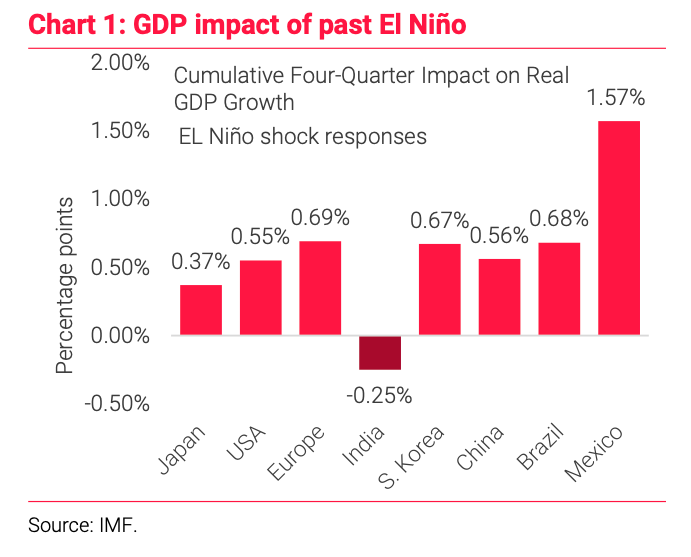

Chart 1: GDP impact of past El Niño

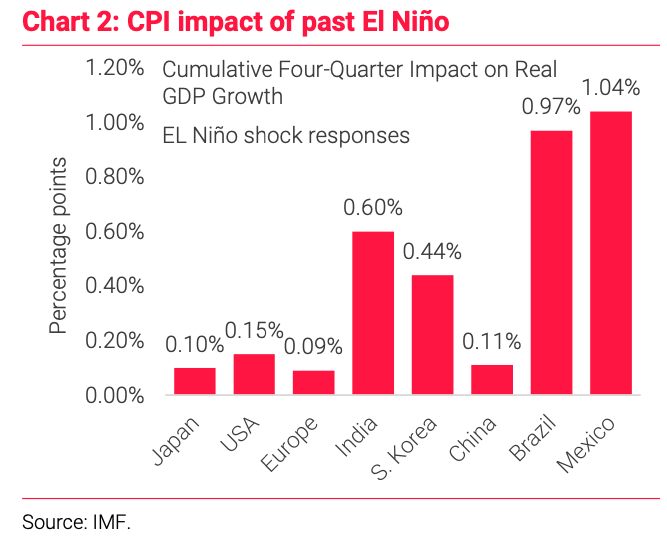

Chart 2: CPI impact of past El Niño

El Niño Impact Watch:

If it proves “strong” or “very strong”, the 2026 El Niño is likely to have a historically large impact on global food prices, given already elevated underlying inflation, existing supply-chain disruption and the current high cost of farm inputs. China, Korea and Taiwan are relatively well insulated from the shock. As are most DMs, with the exception of Australia, as the maps below and the charts above show. In our coverage, it is India and LatAm that are most exposed.

India Impact:

El Niño to hit prices, employment and potentially equities

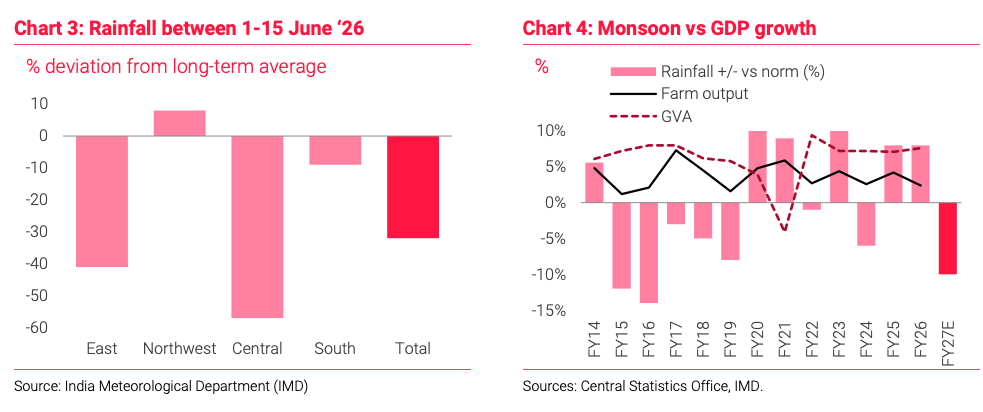

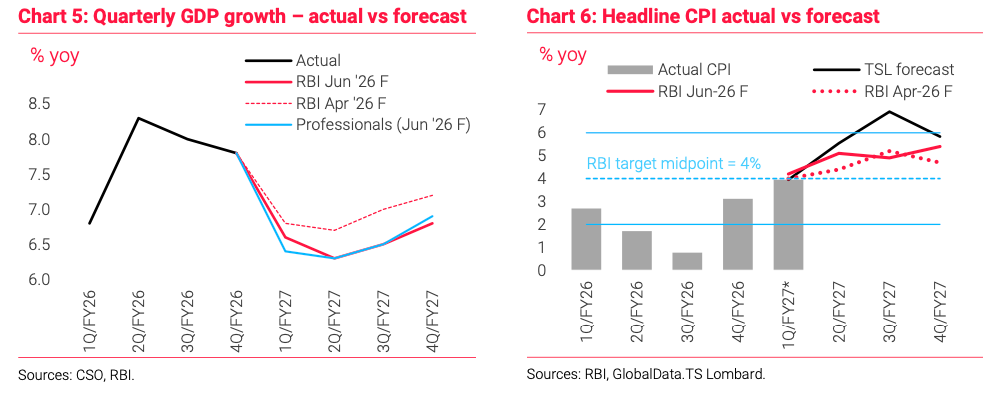

India’s Met Department recently warned that El Niño conditions will strengthen during the crucial monsoon season that accounts for ~75% of the annual rainfall the country receives. The Met Department (IMD) has forecast rainfall in the June-September monsoon to be 90% of the long-period average (LPA); if that projection bears out, India will face its worst monsoon since 2015. That year, the IMD had initially predicted below normal rainfall of 93% of the LPA, but the actual rainfall recorded was 86%, leading to drought-like conditions across many parts of India. Even though it is early days yet in this year’s season with the rains just about setting in over south peninsular India, indications are that the monsoon is off to a weak start. Rainfall in the first 15 days of June has already been far below normal, as Chart 1 below shows, and the progress of the monsoon across the subcontinent has stalled.

A weak monsoon will exacerbate headwinds to growth that India’s heavily energy import- dependent economy has been facing due to the surge in global oil prices. Damage to the summer-sown crop output is a risk to agricultural incomes and rural demand, as well as a potential inflation trigger. Rising food and fuel costs pushed headline CPI higher to 3.9% yoy in May, up from 3.5% yoy in April; May’s food price inflation rose at a faster pace to 4.8% yoy. We expect high commodity prices to spill over into broader inflation, and for headline CPI to breach the upper threshold of the Reserve Bank of India’s (RBI) 2-6% flexible target by 3Q/FY27. At its early June policy, the RBI revised up its inflation forecast for FY27 to 5.1% vs 4.6% previously, cautioning against upside risks to its projection. It cited further downside risks to its GDP growth forecast for FY27 that is cut to 6.6% (vs 6.9% previously) owing to supply shocks from both energy and weather-related factors.

The government has been taking proactive measures to combat the El Niño impact, including increasing stocks of rice and wheat in state-run warehouses. How the El Niño impacts the monsoon will be clearer by end-July, when the IMD issues its updated monsoon forecast. July is the key month for crop sowing as the rains typically cover the entire country by the start of the month. Last week, Agriculture Minister Shivraj Singh Chouhan said almost 200 districts (a quarter of India’s total) are “most vulnerable” to the impact of El Niño. The monsoon season’s impact on crops is determined not just by the quantity of rainfall but also its geographical distribution. The accumulation of water in reservoirs – critical for the winter-sown crop – is also important to track: as of early June, the level was a little lower vs a year ago but higher vs the LPA.

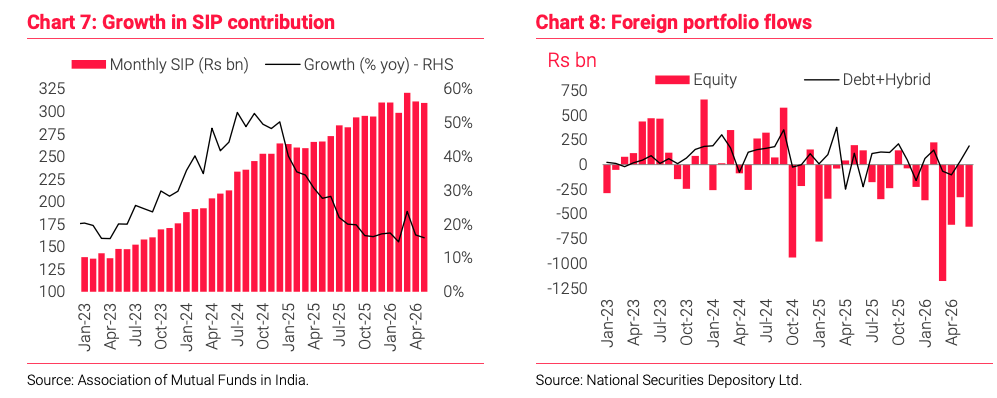

For now, the markets are rebounding after tensions in the Middle East eased, but the Indian economy’s resilience will be tested again soon if the monsoon fails: since 1951, 12 of 17 El Niño years have witnessed deficient rains. Foreigners remain net sellers in the equity market, although tax exemptions announced for overseas bond investors are pulling flows into local debt. Equities have been supported by local investors, but returns have been capped as momentum of domestic flows has been flagging recently

Brazil Impact

El Niño could weigh on power, food prices

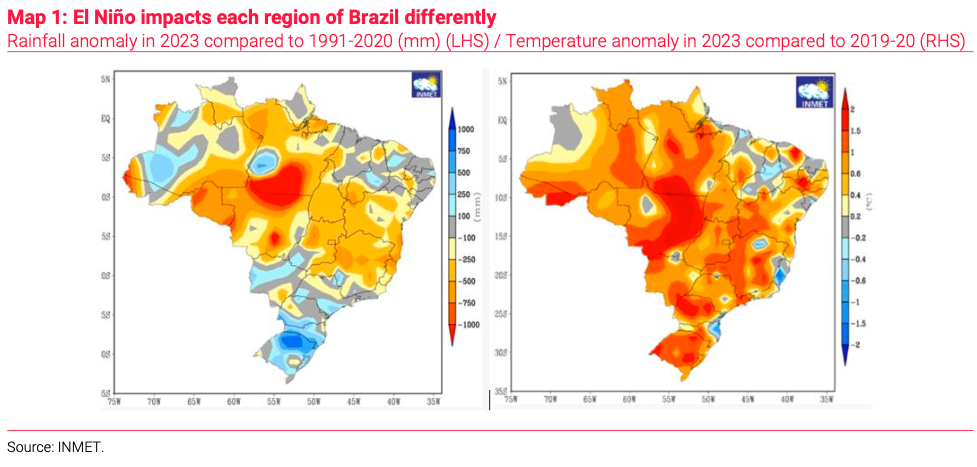

A ‘Super El Niño’ could push up inflation, but Brazil is more prepared for extreme weather than in the past. As a country that spans across the South American continent, El Niño has an uneven impact on regional weather patterns. In southern Brazil, overall precipitation, the number of heavy downpours and the severity of storms tends to increase, particularly in the spring. Northern Brazil, including parts of the Amazon basin, tend to have drier weather, as does the country’s northeast. While parts of the country’s populous southeastern region see a limited impact, key states – including Minas Gerais, tend to be drier than normal. Across the countries, average temperatures tend to rise, and the number of heatwaves tends to increase. These factors, coupled with the greater frequency of extreme weather already effecting the country because of climate change, mean that Brazil runs an even greater risk of severe events this year, similar to the record floods in Rio Grande do Sul state in 2024.

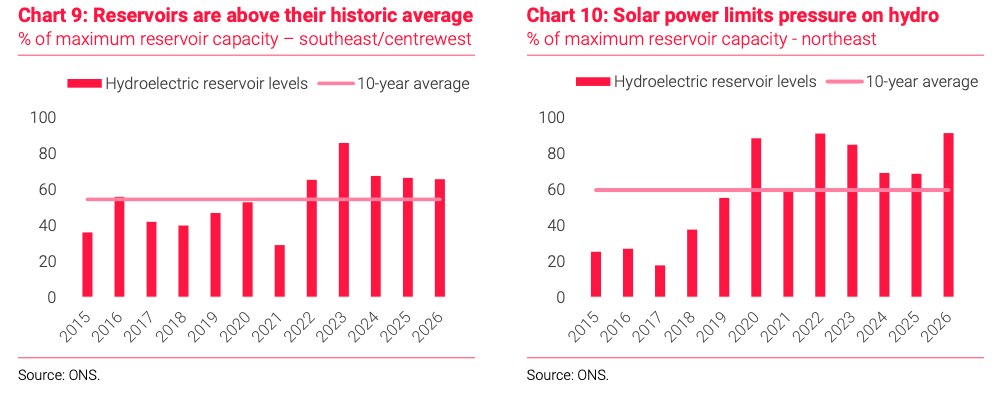

The El Niño adds another layer of uncertainty regarding the economic outlook. Although we do not expect the El Niño to play a decisive role in the direction of the economy in H1/26, it could exacerbate existing issues in the economy, including inflation. Electricity prices, which typically tick up during the dry season (April to October) could rise even more if dry weather has a significant impact on hydroelectric reservoir levels in south-central Brazil, which holds the lion’s share of the country’s generation capacity. This would force the National Systems Operator (ONS) to continue to maximize the use of high-cost thermoelectric plants to offset the reduction in hydroelectric generation. This would mean that electricity costs would increase in the coming months through the so-called tariff flag systems, which is imposed to cover the costs of thermoelectric generation. Likewise, energy consumption – and spot market prices – tends to increase during heatwaves, as more households use air conditioning. The positive news is that Brazil is entering the dry season, Brazil’s hydroelectric reservoirs are in a slightly more comfortable situation than in previous El Niño years, which could limit the impact of the weather phenomenon on power prices.

The El Niño could have an impact on food prices, but not in the short term. When temperatures exceed 40°C for prolonged periods, it generally takes three to four months for the hot, dry conditions to affect fruit and vegetable harvests. The effect on grain and oilseed crops takes even longer. Brazil has already harvested its summer soybean crop and the winter corn crop is in the ground and scheduled for harvest in August and September. At that point, farmers begin planting their summer crops. Even without the El Niño, there are already doubts regarding whether Brazil will manage to expand its soybean and corn crops in the upcoming 2026/27 season. This is because of unfavourable global prices, as well as higher input costs, which could force Brazilian farmers to reduce fertilizer use. While a modest decline in fertilizer application is unlikely to significantly affect yields in a single season, production costs for soybeans and corn will be higher for the 2026/27 season. This increase could influence the cost of meat and biofuels in the following year. In short, pressures from weather and fertilizer prices are present, but their impact on food prices is unlikely to be felt until early next year.

Mexico Impact

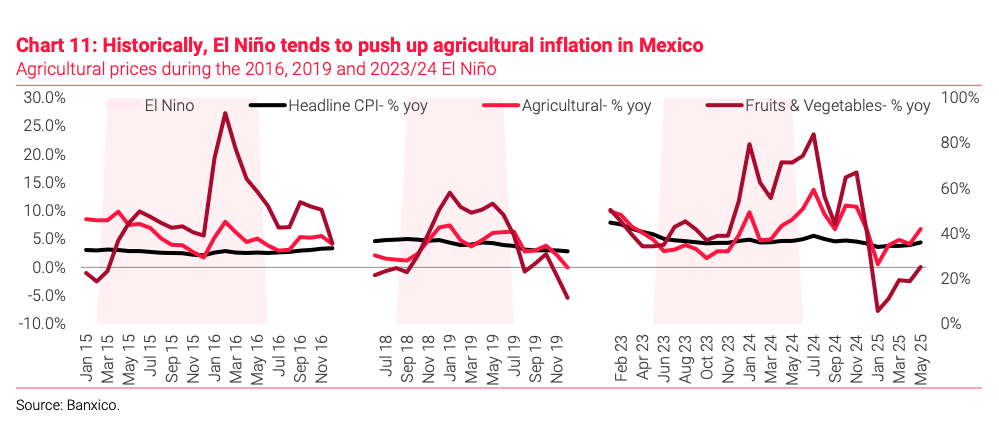

The most immediate impact is likely to come through agricultural prices. Adverse weather conditions have historically reduce agricultural output and, with a lag, feed into livestock prices as poorer pasture conditions and water scarcity raise production costs. Agricultural inflation hit 14.33% y/y during the 2023-24 El Niño, nearly three times the headline rate, with fruits and vegetables peaking at 25.69%. The 2026 starting point is no less uncomfortable. Fruits and vegetables spiked to 21.77% in March and, despite easing to 14.38% in May, remain well above headline, leaving the most weather-sensitive part of the CPI basket exposed to a renewed supply shocks. It’s worth highlighting that El Niño affects Mexico in distinct ways, with northern states tend to see higher precipitation in winter, which tends to benefit export crops. But the weather phenomenon also boosts the risk of unseasonal frosts and floods that damage, with potential implications for the tomato, wheat, and maize harvests. In the centre-south, El Niño reduces rainfall and coffee, sugarcane, maize, beans, and avocados are the most exposed crops.

Bad timing for Banxico. The central bank cut rates to 6.5% in May and signalled that the easing cycle had likely come to an end, citing weak activity and a resilient peso. We continue to view growth risks as outweighing inflation concerns and believe additional easing in Q3/26 remains possible. However, a moderate-to-strong El Niño would complicate that assessment by pushing up agricultural inflation through supply-side shocks that monetary policy cannot easily offset. This would make any further easing harder to deliver, even as growth concerns continue to mount.

El Niño also exposes structural vulnerabilities to more extreme weather. Along the Pacific coast, warmer sea surface temperatures fuel a more active hurricane season, raising the risk of storm damage to coastal infrastructure and export agriculture. At the same time, the phenomenon puts urban water supply under pressure. Cutzamala, which provides roughly a quarter of Mexico City’s water, fell to just 27% capacity during the El Niño. An exceptionally wet 2025 reversed much of that damage, bringing the system back to 67.7% by early June 202 – the highest level in the seasonal cycle in seven years. That buffer offers some protection, but a strong El Niño would still test it.

Green’s note builds on a UBS report published earlier this month, which warned that El Niño risks could send food inflation higher across Asia.

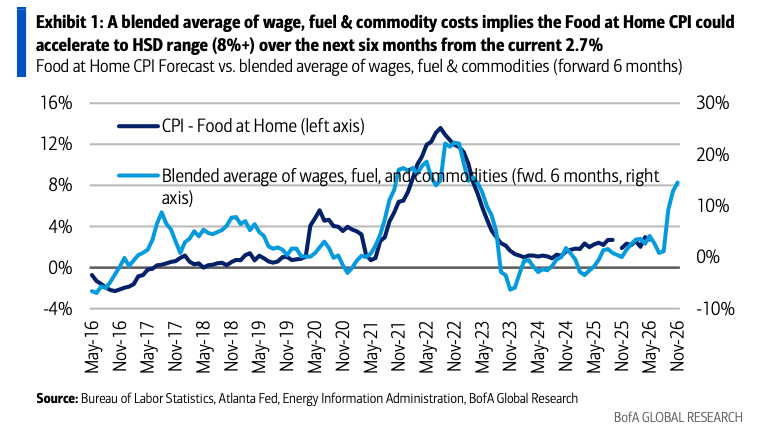

The U.S. is not out of the woods just yet. Bank of America analysts warn that the energy shock of the last several months could ultimately feed into food inflation later this year, with a lag (read the report).

Now there has been what Daryna Kovalska, a commodity strategist at BofA, described as an “aggressive positioning washout” in the agriculture trade. However, she believes that the selloff in soft commodities such as corn is well overdone.

Professional subscribers can read the full note here at our new Marketdesk.ai portal.

Tyler Durden

Mon, 06/22/2026 – 23:00

via ZeroHedge News https://ift.tt/AI6qQ2h Tyler Durden