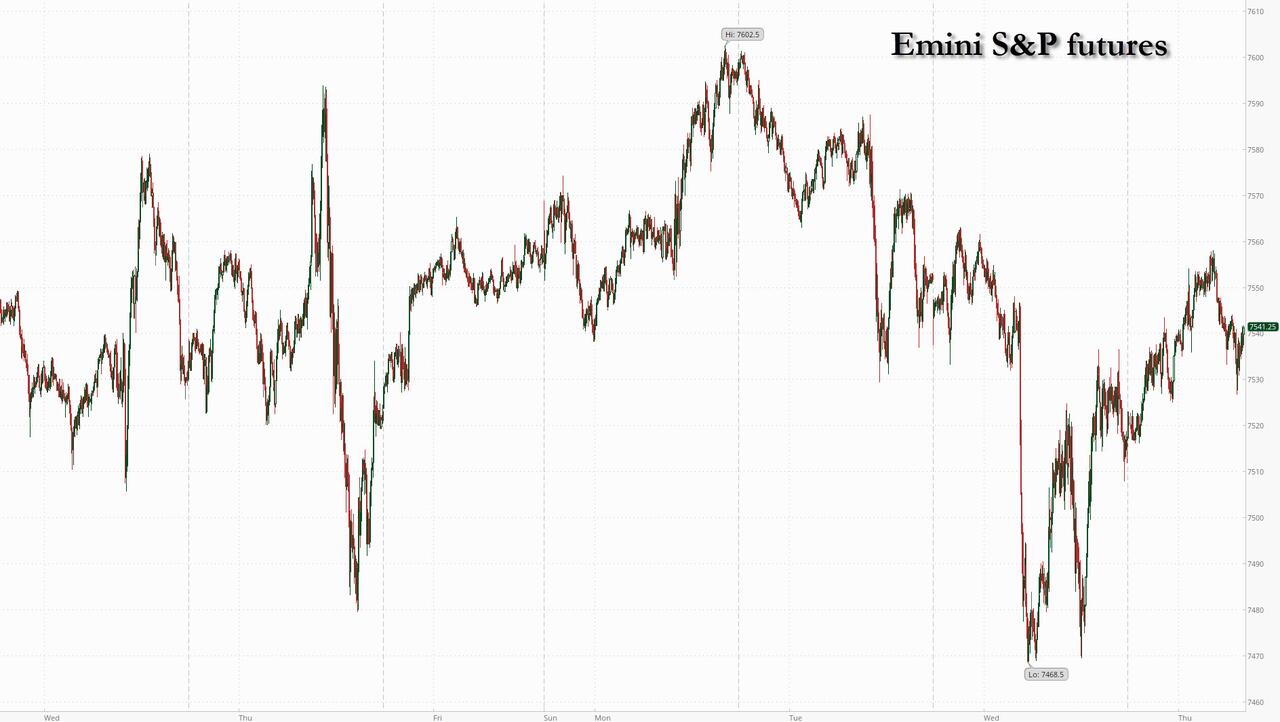

Futures Rise, Oil Drops As Markets Ignore Latest Middle East Airstrikes

Futures are higher (although off session highs), and oil erased overnight gains as the market moved past the latest Middle-East flare up which saw the US military strike 90 Iranian targets for a second day and Tehran retaliated against American allies in the Persian Gulf. And like during previous escalations, this time nobody believes it will last. As of 8:00am ET S&P 500 futures rose 0.2% and Nasdaq 100 contracts gained 0.6% as semiconductor stocks advanced in Asia, Europe and US premarket trading after SK Hynix drew strong demand for its offering of ADRs. Mag7 stocks are mixed, with META tumbling on a Reuters report the company has signed long-term contracts for memory, networking gear and flash storage, refuting the market’s expectation that the company is starting to ease back on capex spending. The FTSE 100 lags and is down 0.8% as AstraZeneca shares slump 9% after its Wainua drug failed to prevent heart problems. . Cyclicals, ex-Energy, are rebounding led by Fins and Industrials. Momentum is poised for another strong day, this time with Beta. Brent traded near $79 a barrel after swinging between gains and losses. Bond yields are down 2bps to up 1bps as the curve twists steeper ahead of today’s 30Y auction; the 10Y yield trades at 4.59%, near a one-month high. Commodities are weaker with Ags and Energy selling off but there is a bid to metals led by Precious. The Bloomberg Dollar Spot Index is also little changed. The kiwi is the strongest of the G-10 currencies, rising 0.6% against the greenback after some hawkish remarks from RBNZ Governor Breman. Precious metals advance along with Bitcoin. Today’s macro data focus is on jobless data and existing home sales with the macro focus shifting to next week’s CPI / PPI, Retail Sales prints as earnings season kicks off.

In premarket trading, Mag 7 stocks are mixed (Meta Platforms -0.1%, Microsoft -1%, Tesla +0.2%, Nvidia +0.2%, Amazon -0.6%, Apple -0.2%, Alphabet -0.3%)

- Ceco Environmental (CECO) rises 3% after JPMorgan initiated coverage of the air-purification equipment provider with a recommendation of overweight, citing its acquisition of Thermon.

- IBM (IBM) slips 3% as Starbucks is developing in-house tools with the help of artificial intelligence that could replace some software applications it now buys from the company.

- Ionis Pharmaceuticals (IONS) slumps 19%, while AstraZeneca falls in London, after a late-stage trial of the companies’ gene silencer drug Wainua showed a failure to help prevent heart problems in patients with a rare and potentially fatal disease of the organ.

- Developers of rival cardiomyopathy drugs gain: Alnylam Pharmaceuticals (ALNY) +17%, Bridgebio (BBIO) +13%.

- Levi Strauss (LEVI) falls 4% after after the apparel company’s increase to its forecast underwhelmed investors.

- Mattel (MAT) slips 2% after Goldman Sachs analyst Stephen Laszczyk cut his recommendation on the toy maker to sell from neutral, and cut his price target to a Street-low $12 from $15.

- Salesforce (CRM) falls 4% after KeyBanc downgraded the software company to sector weight, noting a lack of momentum in the the company’s Agentforce AI product.

- Simply Good Foods (SMPL) rises 13% after the packaged-food company reported adjusted earnings per share for the third quarter that beat the average analyst estimate.

In other news, PepsiCo narrowly missed estimated for second-quarter organic sales growth as the earnings season for the June quarter got underway. Bain Capital has sold its entire stake in flash memory chipmaker Kioxia. AstraZeneca and Ionis Pharmaceuticals’s gene silencer drug Wainua failed to help prevent heart problems in patients with a rare and potentially fatal disease of the organ, sending Ionis shares plunging in premarket trading. Porsche deliveries slumped 16% in the first half, dragged down by weak demand in North America and a decline in China.

The calmer mood in markets comes despite an escalation of violence in the Middle East that is threatening efforts to reach a permanent US-Iran peace deal. The US military hit about 90 Iranian targets Wednesday to degrade Tehran’s ability to attack commercial shipping in the Strait of Hormuz. Traders say that while the tensions reflect the fragile nature of the truce between the sides, neither government would want a full-scale return to war and that the parties would likely return to negotiations.

“This is the new status quo; it’s an uneasy equilibrium, but an equilibrium nonetheless,” said Geoff Yu, a senior macro strategist at BNY. “You just need to factor in the volatility in your asset allocation.”

Global bonds were modestly higher as two days of an oil-driven selloff came to an end. The yield on two-year Treasuries eased two basis points to 4.20%. The dollar was little changed.

After Wednesday’s minutes of the Federal Reserve’s June meeting showed that some committee members saw a case for a rate increase, traders will now wait for next week’s inflation data and Chair Kevin Warsh’s testimony to lawmakers for another steer on the path for interest rates. New York Fed President John Williams will take part in a moderated discussion later on Thursday.

“The only reason the July meeting wasn’t live was because oil prices were basically where they started the war,” Bob Elliott, chief investment officer at Unlimited Funds, told Bloomberg TV. “That’s changed. The conflict in Iran and the Hormuz problem has not really been resolved.”

In tech, SK Hynix’s US listing is said to be more than seven times oversubscribed, as the South Korean memory chipmaker prepares to price its offering later today. With its ADRs set to trade for the first time on Friday, arbitrage investors are without a historical benchmark for what constitutes a normal premium, making it far harder to judge when a spread is attractive or stretched. On the subject of memory, the knock-on effects of ongoing component price inflation could dampen hardware growth expectations, with Citi forecasting 2026 PC units to fall 15% in 2026, and smartphones to decline 12%.

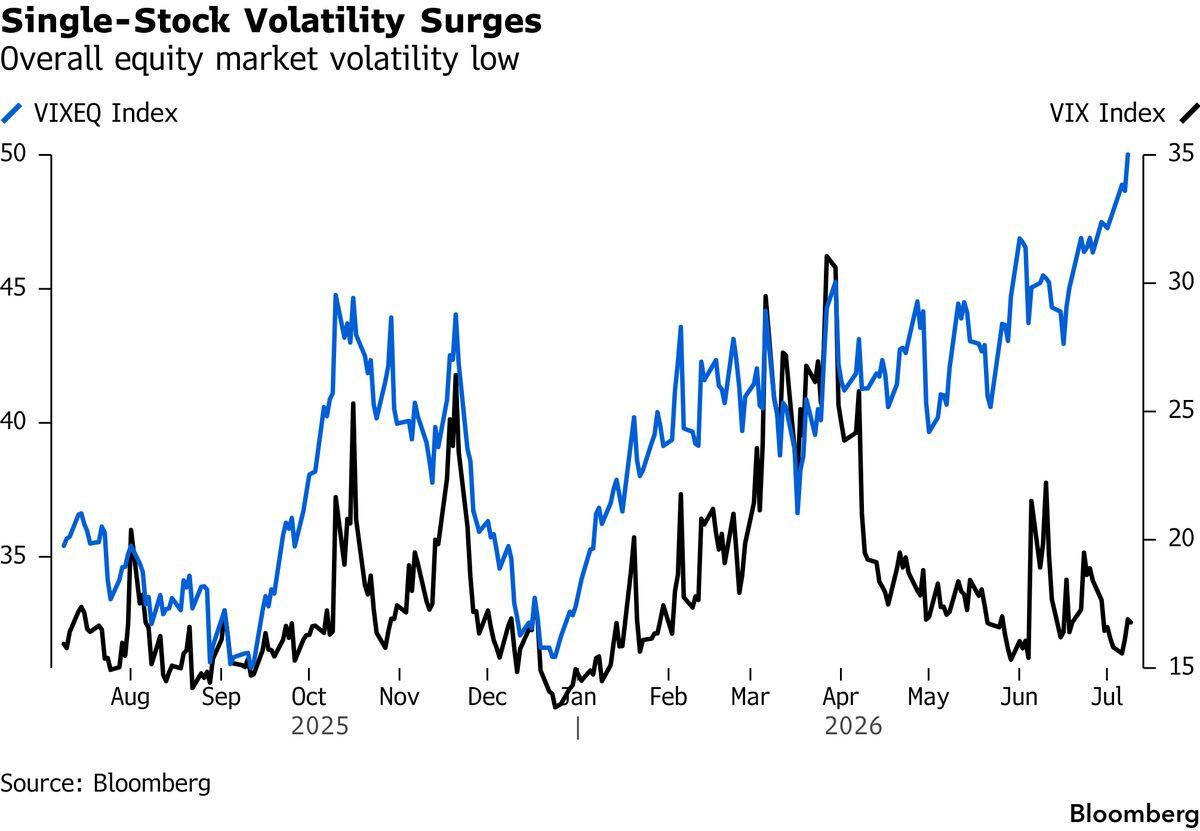

As Bloomberg notes, an interesting divergence is emerging under the surface of volatility. While the VIX Index continues to exhibit placid price moves, single stock volatility, expressed through the S&P 500 Dispersion Index, closed at a one-year high on Wednesday.

When it comes to AI, massive spending commitments are set to sustain the investment theme around the technology for two to three years, according to BlackRock Inc.’s Helen Jewell, even as tech giants gradually turn cash-flow negative and start raising debt to fund their buildouts.

“From an investment perspective, you lean into the AI theme, you do the secondary beneficiaries of that, but you need to diversify those portfolios,” Jewell told Bloomberg TV. “Healthcare, Latam, even the UK.”

Consumer stocks are in focus with Costco reporting a deceleration in June comps relative to May, while Levi Strauss is lower in premarket trading after a decent beat and raise report fell short of some expectations for a more punchy forecast. It follows BofA noting that clients had put the most money into consumer discretionary stocks ever last week.

In politics, Graham Platner suspended his Senate campaign in Maine following a sexual assault allegation that caused his support from fellow Democrats to collapse. And Democratic infighting is threatening to undermine the party’s midterm targets.

Europe’s Stoxx 600 rises 0.4% after its worst day since March. Miners and banks are the best performers while healthcare lags its sector peers.The FTSE 100 lags and is down 0.8% as AstraZeneca shares slump after its Wainua drug failed to prevent heart problems. Here are some of the biggest movers on Thursday:

- Glencore rises as much as 3.9% after Goldman Sachs raised the diversified miner to buy from neutral, citing commodity leverage, earnings upside and valuation support.

- Nordex shares gain as much as 5.2% after the German wind turbine maker said it recorded 3,054MW of orders in the second quarter, above expectations.

- Computacenter shares rise as much as 14% to a record high after the UK IT reseller tipped full-year results to be “comfortably ahead” of market expectations, showing it continues to benefit from US hyperscalers’ data center buildout.

- Admiral Group rallies as much as 2.2% after Goldman Sachs upgraded the car insurance provider to neutral from sell and set a Street-high price target, citing an upturn in UK motor market pricing.

- Schott Pharma shares jump by a record 22% after the company improved its guidance for the full year, prompting an upgrade at RBC Capital Markets. The stock is trading at its highest level since October.

- Wolters Kluwer shares rise as much as 7.3% as JP Morgan upgrades its rating on the IT firm to overweight from neutral and lifts its price target, citing a “compelling” valuation and the potential for interest from private equity.

- Sampo gains as much as 2.3% after the insurer was upgraded to buy from neutral at Goldman Sachs, which sees Nordic markets and an upturn in UK motor pricing driving operating earnings growth through 2029.

- Erste shares rise as much as 3.4% after Goldman Sachs resumed analyst coverage with a buy rating and a €150 price target.

- Deutz shares rise as much as 10% after the German engine manufacturer said it agreed to buy closely held military-vehicle maker FFG Flensburger Fahrzeugbau Gesellschaft.

- Pepco gains as much as 5.2% after the discount retailer reported acceleration of like-for-like sales during the 3Q period ended in June.

- Playtech shares rally as much as 20% after the maker of gaming software said its performance in the first half was materially ahead of expectations and lifted its full year guidance.

- Suedzucker shares rise as much as 4% after the German food company raised its revenue outlook for the year.

- AstraZeneca shares slump as much as 9.9% after a late-stage trial showed the gene silencer drug Wainua failed to help prevent heart problems in patients with a rare and potentially fatal disease of the organ.

- Capita shares plunge as much as 20% after the outsourcing company warned issues with a contract will hit 2026 profit, leading analysts at RBC Capital Markets to cut their forecasts and price target.

Asian stocks swung between gains and losses as concern over renewed Middle East tensions was countered by optimism toward the artificial intelligence trade. The MSCI Asia Pacific Index was 0.1% higher after earlier climbing as much as 1% and falling 0.5%. Most technology shares gained, with SK Hynix and Kioxia Holdings among the major contributors to the gauge’s advance. Mainland China’s CSI 300 Index jumped more than 2% as chip stocks advanced. Shares in Japan and South Korea also rose, while those in Hong Kong and Taiwan fell. Oil fluctuated as traders assessed the outlook for Middle Eastern crude supplies after fresh hostilities between the US and Iran, raising concerns for global energy supplies and posing a fresh challenge Asian economies that are mainly oil importers. Investors are reassessing the sustainability of AI-driven rally, as investors looked to earnings season for the next catalyst.

In FX, the Bloomberg Dollar Spot Index is also little changed. The kiwi is the strongest of the G-10 currencies, rising 0.6% against the greenback after some hawkish remarks from RBNZ Governor Breman.

In rates, treasuries are mixed with the curve steeper, pivoting around little-changed 10-year sector, as front-end tenors unwind some of their oil-driven losses of the past two sessions. Long-end tenors lag with WTI crude futures extending recent gains after IRNA report that the perimeter of Bushehr Nuclear Power Plant was hit by US projectiles. US front-end yields are about 2bp richer on the day, long-end yields 1.5bp cheaper, steepening 2s10s and 5s30s spreads by 2bp and 2.5bp respectively. 10-year, little changed around 4.58%, trails bunds and gilts in the sector by around 3bp. European government bonds rise with UK and German 10-year yields falling 2-3 bps each. US 10-year borrowing costs are flat.This week’s Treasury auctions conclude with $22 billion 30-year reopening at 1pm, following strong demand for Wednesday’s 10-year note sale; WI 30-year yield near 5.09% is 7bp cheaper than last month’s auction, which tailed by 1.2bp. Focal points of Thursday’s US session include weekly jobless claims data and 30-year bond reopening, on the heels of good demand for Wednesday’s 10-year note sale. .

In commodities, brent crude futures are little changed near $78 a barrel having erased earlier gains seen after the US military struck Iran for a second straight day. Precious metals advance along with Bitcoin.

US economic data calendar includes weekly jobless claims (8:30am) and June existing home sales (10am). Fed calendar includes Williams (9am) and Logan (1:30pm).

Market snapshot

Top Overnight News

- US, Iran Trade Airstrikes as Fears Grow of a Return to War: BBG

- The Iran War threatened a food crisis. The next Gulf conflict could do the same: RTRS

- The Red Flag That Led to Graham Platner’s Implosion Was Hiding in Plain Sight: WSJ

- Meta to put AI chip into production in September as it looks to double computing capacity, memo shows: RTRS

- An Impending IPO Boom Has Sparked FOMO Among San Francisco Home Buyers: WSJ

- China consumer price growth weakens in June while producer inflation rises to near 4-year high, squeezing manufacturers: RTRS

- U.S. Targets One of Cuba’s Last Lifelines: Its Army of Overseas Doctors: WSJ

- Ukraine’s Six-Part Strategy to Survive the Global Run on Patriot Missiles. Kyiv is trying to mitigate the shortage of missile interceptors that has left its cities exposed to Russia’s ballistic missiles: WSJ

- The US Senate committee will reportedly vote next week on a bill to toughen the US government ban on Chinese automakers from entering the US market.

- Counterfeit Air-Bag Parts Are Killing U.S. Drivers—and the Government Can’t Stop It: WSJ

- Trump said he is a bigger fan of SAVE America than the housing bill; Trump said he will be asking for a rehearing by the Supreme Court on birthright citizenship: Truth Social

Iran War

- US CENTCOM announced the completion of its most recent round of strikes against Iran, in which forces struck around 90 Iranian military targets. There were reports of fresh explosions in Bandar Abbas, Sirik and Hormozgan. There have also been reports of explosions in Abu Musa Island and Bushehr. Nour news reported that the attack on Bushehr did not cause any damage to the nuclear power plant.

- The IRGC later announced that two US bases in Kuwait and two base in Bahrain were attacked and threatened that response will be extended to other US bases in the region if the US repeats its attacks.

- Trump said Iran was just hit very hard and we have many ways to win. He added that he do not know if Iran will honor a deal but Iran wants to make a deal badly.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks initially proved resilient to the recent US-Iran strikes, with the majority of indices opening with decent gains. However, as the session progressed, market reversed, with the Nikkei 225 the only index printed gains. The reversal came without a clear driver, which highlights the extreme volatility in equity markets. ASX 200 began trade with losses and continued to trade in the red, however stabilised above 8,700. Energy was the sector outperformer, while Metals & Mining lagged for a fourth straight session.

Nikkei 225 was the only index printing gains, helped by gains in Kioxia, after Bain Capital announced the sale of its entire stake, and Tokyo Election, as it highlighted the ability to cut chip gear delivery times by 50%. KOSPI initially surged at the open, following on from the tech-led gains stateside, with Samsung and SK Hynix printing gains of over 5% at one point. However, the index reversed, driven by the losses in the two tech giants, highlighting the extreme volatility in the South Korean benchmark. The KOSPI volatility index currently stands at 87.41, compared to Nasdaq’s 27.86. Shanghai Comp. and Hang Seng opened with modest gains but gave back slightly. It was another day of IPOs for the Hang Seng, with the introduction of Luxshare Precision Industry, which didn’t start as hoped.

Top Asian News

- Japanese Chief Cabinet Secretary Kiara said they are watching markets with a high sense of urgency.

- China announces issuance of guidelines to promote the retail sector.

- South Korean official said Won weakness is temporary.

European bourses (STOXX 600 +0.6%) opened with gains as markets generally look through the geopolitical escalation. FTSE 100 is the laggard as energy majors pull back and AstraZeneca slumps, IBEX 35 is the clear outperformer after US-Spain trade-related underperformance on Wednesday. To briefly recap events overnight, tit-for-tat strikes were conducted by the US on around 90 Iranian targets, and the IRGC fired on military bases in Bahrain and Kuwait. Markets remain optimistic, focusing on remarks from US President Trump, who said he spoke with Iran, and that they want to make a deal. European sectors opened with a positive, risk-on bias and continue this way in quiet EU trade. Tech and Basic Resources outperform, while Energy and Utilities are the laggards. Stock specifics include: AstraZeneca (-9%) CARDIO-TTRansform Phase III trial did not meet the primary endpoint of efficacy around CV mortality; Deutz (5.5%), To acquire FFG Flensburger Fahrzeugbau Gesellschaft for EUR 1.6bln.

Top European News

- Andy Burnham has pledged to rebuild the country’s hard power by ensuring that billions of pounds of additional defence spending is focused on the UK rather than given to American or European companies, according to the Times’ Swinford.

FX

- In short, the USD is a touch softer at the expense of G10s across the board ex-CAD which has been hit by the energy pullback. Kiwi continues to lead post-RBNZ.

- NZD continues to climb, as high as 0.5739 against the USD, approaching the 22nd of June peak at 0.5741 and numerous levels thereafter. The narrative for the Kiwi is a continuation of the move seen following the RBNZ, and as the last session or two’s worth of energy action adds to, and arguably brings forward, the tentative hawkish guidance from the Bank. As a reminder, the statement said “While further OCR increases appear likely at upcoming meetings, their timing is highly uncertain.”

- CAD lags. USD/CAD at a 1.4188 peak and threatening to move higher despite energy lifting off lows, but with WTI and Brent still lower by around USD 0.40/bbl on the day. Numerous levels are in focus on either side, with the direction likely to remain firmly and almost exclusively at the whim of energy, barring a trade or similar development.

- EUR and GBP both benefit from the USD downside. EUR/USD as high as 1.1449 and Cable to 1.3431. However, the last 30 minutes or so have seen a bit of a bounce in energy, still in the red but only by around USD 0.40/bbl vs downside of c. USD 1.10/bbl at most. Action that has allowed the USD to fight back a touch, and weighed on peers with GBP/USD down to a 1.3413 low and EUR/USD back towards the overnight 1.1416 base. Given this, the DXY remains in the red and below 101.00, but only just and is eyeing a return into the green.

- For the EUR, we look to the ECB Minutes for June. However, the significant amount of developments on the geopolitical front since then mean the account is even more stale than typical. UK participants await the formal start of the Labour leadership process, though it is not expected to be a contest with just Burnham to enter.

- USD/JPY under modest pressure, broadly in-fitting with the action seen in other G10s as the USD dictates. At the mid-point of narrow 162.24-62 parameters. Specifics include Chief Cabinet Secretary Kihara saying they are watching markets with a high sense of urgency.

Fixed Income

- A firmer start to the day for fixed income, after a relatively rangebound APAC session on account of the lack of energy follow-through to the tit-for-tat strikes by the US and Iran overnight, with the narrative potentially being that the strikes are no more of an escalation than what we saw on Tuesday night.

- Overnight, USTs held around 108-30 and were near-enough flat, Bunds similar between 125.20-30, firmer by around 10 ticks. Thereafter, in the early European morning, US President Trump said Iran “called a while ago” and they “want to make a deal”, in-fitting with his overnight language; however, the indication that contacts, likely via mediators but unconfirmed, have occurred allowed energy to pull back and lifted fixed. This was enough to bring USTs to a 109-03+ peak. However, in recent trade, as the energy complex comes off worst levels US paper has flicked slightly into the red.

- Bunds as high as 125.40, firmer by 26 ticks at best but well shy of the week’s opening level just below 127.00. Specifics for the bloc light, aside from ECB Minutes for the June meeting, which are likely more stale than usual given the MoU and more recent flare up.

- Gilts opened with gains of 28 ticks, reacting to the early-morning pickup in peers. Since, it has extended to an 87.62 peak with gains of just over 50 ticks; albeit, as is the case with peers, the benchmark remains well shy of Monday’s 88.93 opening level. For the UK, BoE’s Breeden is on the docket and may well provide further insight on Gilt-related reform. Additionally, the Labour leadership nomination process formally opens, if as expected only Burnham contends then he will be PM around the 20th of July.

- Japan sold JPY 2.5tln 5-year JGBs; b/c 3.43x (prev. 3.11x), average yield 2.020% (prev. 1.905%). Lowest accepted price 99.88 (prev. 100.35). Weighted average price 99.91 (prev. 100.41). Tail in price 0.03 (prev. 0.06).

- China Interbank bond market regulator is to reportedly curb short-term bond issuance by local government financing vehicles.

- Australia sold AUD 150mln 0.25% November 2032 I/L AGBs: b/c 3.23x (prev. 4.42x), average yield 2.1808% (prev. 2.2373%).

Commodities

- Focus remains on the turbulent geopolitical situation. Overnight, the US struck various regions in Iran, aiming to degrade the IRGC’s ability to attack commercial ships. Iran responded with its own attacks on US bases in Kuwait and Bahrain.

- Following the strikes, US President Trump said that Iran called a short while ago, and that they want to make a deal. Details are light at this stage, and it remains to be seen whether a call actually took place, and whether Trump was truthful of Iran seeking a deal. For now, market sentiment is positive, with traders focusing in on: a) Trump’s deal comments, b) no large-scale war so far, c) the Strait remaining open. On the latter point, whilst ships continue to traverse the Strait of Hormuz, Reuters reported that that some war insurers advised shipowners to pause Hormuz voyages after the latest attacks.

- Crude benchmarks extended lower this morning, after trading with mild strength overnight. However, the complex now trades flat on the session, as markets digest the overnight strikes.

- Spot gold (+0.9%) trades slightly firmer this morning, thanks to the softer USD and lower energy prices. Currently holding above the USD 4.1k/oz mark, and trades within a USD 4,054-4,118/oz range. Elsewhere, base metals are entirely in the green, following the positive risk tone. 3M LME copper trades at the upper end of a USD 13,241-13,447/t range. Elsewhere, for Lithium markets, reports have suggested that Chile’s lithium exports have almost tripled Y/Y.

- Stavropol governor said a fire at the industrial site in Stavropol has intensified, reaching fuel tanks, Interfax reported.

- UK announces issuance of electricity supply warning as heat wave strains grid.

Trade/Tariffs

- US President Trump said a lot of good trade deals were made with Turkey; Spain was very generous today as they honoured a request for lots of payment.

- A US official said that the US Treasury will work with USTR and the Commerce Department to present President Trump with a menu of Spanish products that may be subject to a trade embargo in the coming days.

Central Banks

- BoJ Osaka branch manager said many companies in the region expect solid earnings and share the need for further wage increases to secure workers amid labour shortages; expect significant price rises ahead.

- BoJ maintains its assessment for all 9 of Japan’s regions. Many regions said the risk of sharp drop in exports and output has declined somewhat. Many regions said firms were maintaining robust capex plans, increasing chip equipment and chip orders due to expanding global AI demand. Many regions said firms, including smaller ones, offered high wage increases this year, though some said it could be difficult to keep a hiking pay.

- RBNZ Governor Breman reiterates that the neutral OCR range is centred around 3%, need to read the economy to assess where the neutral rate is.

- PBoC set USD/CNY mid-point at 6.8036 vs exp. 6.7978 (prev. 6.8077).

- BoK Governor Shin said they are in talks with other central banks all the time to discuss markets, sees a strong chance of a stronger KRW.

- Taiwan Central Bank Governor said concerns remain about the possibility of an AI bubble.

- BoK Governor Shin said interest rates need to be raised at an appropriate time.

- BoK said KRW weakness is sharper than other major currencies, will continue making market stabilising efforts, inflation seen exceeding target with demand-side pressure growing gradually.

Geopolitics: Overnight strikes:

- At the direction of the Commander in Chief, US Central Command forces have started conducting additional strikes against Iran to further degrade their ability to threaten freedom of navigation in the Strait of Hormuz. The United States is holding Iran accountable for recent unjustified aggression against commercial shipping and civilian crews freely navigating a vital international waterway.

- US military base in Kuwait was hit in an Iranian retaliatory attack, while explosions heard at the US Fifth fleet HQ in Bahrain.

- Iranian missiles targeted the Azraq base in eastern Jordan, Fars reported.

- Iranian opposition sources report that maritime industries, shipyards, and the Revolutionary Guards’ naval base in Bandar Abbas were attacked, report Kan News.

Geopolitics: US Commentary:

- US President Trump said Iran called a while ago, they want to make a deal.

- US President Trump’s frustration with Iran was due in part to his anger over the Strait not being fully open yet and that Iran hit ships transiting the Strait, CNN reported citing a US official. The official added that Trump is losing patience with the pace of negotiations, specifically Iran’s appearing to slow walk Washington on the nuclear talks.

- US President Trump posted “This is in retribution for yesterday’s bombing of ships by Iran. If it happens again, it will get much worse!”.

- US President Trump said Iran was just hit very hard, we have many ways to win; do not know if Iran will honour a deal but Iran wants to make a deal badly. Europe wants to help on Iran.

- A US official said the ceasefire with Iran has been halted, at least temporarily, CNN reported.

- “Everything depends on Iran’s response – if they continue to shoot, the night’s events could become a daily, weekly event. We are prepared,” i24News reported citing a US source.

- The length and severity of the new campaign depends entirely on Tehran’s next moves, Axios reported citing a US official; The White House is preparing for a multi-day or multi-week exchange of fire with Iran over the Strait of Hormuz.

- Israel has no connection to the US strikes on Iran, Al Arabiya reported citing an Israeli military source. Any attempt to target Israel will be met with a swift, decisive and strong response.

Geopolitics: Iran Commentary:

- Iran’s Bushehr Governor said that US attacks on a nuclear plant in the region are not true.

- Iran’s advisor to the Supreme Leader Rezaei said “martyr Khamenei taught us not to fear American and showed that falsehood will perish. Await the hard slap from the Iranians”.

- Iran’s IRGC said they will respond to the targeting of a bridge in Aqqala, Al Arabiya reported.

- Iran’s IRGC said two US bases in Kuwait and two base in Bahrain were attacked, response will be extended to other US bases in the region if the US repeats its attacks.

- Iranian Parliament Speaker Ghalibaf said America has not yet learned that bullying and breach of promise are no longer free, adds the Strait of Hormuz will only open with Iranian arrangements, not American threats.

- The US attack on Bushehr did not cause any damage to the nuclear power plant, Nour news reported citing a source.

Geopolitics: Lebanon:

- “The US ambassador in Beirut: Negotiations between Lebanon and Israel have moved to Rome for technical reasons”, via Al Arabiya. Preparations are underway regarding the start of work in the pilot areas.

- Israeli Defence Minister Katz said they will remain within the Lebanon security zone and will operate within it until Hezbollah is disarmed.

Geopolitics: Ukraine:

- Ukraine’s Military said it struck 12 Russian tankers in the Sea of Azov.

- Ukrainian President Zelensky said the military has struck Russian oil depots in the Tver and Stavropol Regions; also strikes on a Russian oil pumping Station in Ufa and oil terminal in the Rostov region.

- reported of explosions in Dnipro, Ukraine.

- A Russian official said two tankers were attacked by drones in the Sea of Azov.

- A Russian governor said a fire has occurred in one tank of the Tverskaya oil deposit enterprise as a result of a UAV attack and all districts of the Kershon region are partially or completely depowered, Interfax reported.

- Russian governor said a UAV raid caused a fire at an industrial facility in Stavropol, Interfax reported.

Geopolitics: Others

- EU reportedly puts trade ban with Israeli settlements on the table, Euronews reported.

- US President Trump said have not decided on pulling troops out of Greenland.

- Wednesday’s strikes were broader in scope than the strikes the day before, targeting IRGC coastal radars, anti-ship missile sites and air defence systems, Axios’ Ravid reported citing a senior US official.

US Event Calendar

- 8:30 am: Jul 4 Initial Jobless Claims, est. 217k, prior 215k

- 8:30 am: Jun 27 Continuing Claims, est. 1814k, prior 1814k

- 10:00 am: Jun Existing Home Sales, est. 4.2m, prior 4.17m

- 9:00 am: United States Fed’s Williams in Moderated Discussion

- 1:30 pm: United States Fed’s Logan Moderates Panel on Market Liquidity

DB’s Jim Reid concludes the overnight wrap

The US has now conducted a second consecutive day of strikes on Iran, reportedly targeting around 90 sites including air defence systems, missile and drone facilities, and coastal surveillance infrastructure. This marks a clear escalation, with Washington signalling it is prepared to sustain operations to protect shipping in the Strait of Hormuz. In response, Iran’s Revolutionary Guard has reportedly struck US-linked bases in the Gulf and warned of further retaliation, raising the risk of a broader regional conflict. President Trump said that he would not stop negotiations but that “I just don’t know if they’re worthy of making a deal. I don’t know that they’re going to honor the deal.”

Asian equity markets are mixed overnight, with the renewed US military action against Iran and higher oil prices (+1.03% at around $78/bbl but under yesterday’s peak above $80) weighing on risk appetite. Japan’s Nikkei (+1.55%) is the standout performer, supported by chip-related buying. Elsewhere, the KOSPI (-0.16%) is rebounding from an earlier drop of close to 2 percent even if it had moved positive when I started writing this paragraph! Chinese markets are mostly lower, with the Hang Seng (-0.78%) and Shanghai Composite (-0.89%) declining after soft inflation data. The S&P/ASX 200 is also down (-0.45%). S&P 500 (+0.17%) and Nasdaq (+0.18%) futures are up alongside Stoxx futures (+1.03%) which is being helped by a late US recovery last night after the European close.

Japan’s five-year government bond auction saw solid demand, supported by elevated yields. The bid-to-cover ratio came in at 3.43, above the previous auction’s 3.11 and the 12-month average of 3.35.

The US-Iran conflict and associated oil concerns had built up through the day yesterday, amidst growing fears that last month’s interim deal was coming apart. Oil prices immediately jumped in the London morning by around $2/bbl after President Trump said on the ceasefire that “For me, I think it’s over”. Then later on, Trump said that the US would “probably hit them hard again tonight”, and that “We may put it back, the blockade, and it’ll only be a blockade for Iran”. Meanwhile on the Iranian side, an aide to the Supreme Leader said in a post that “We have proven time and again that adventures will receive an immediate response”. So collectively it felt like the most serious escalation since the deal was agreed last month.

All that led to a clear reaction for oil prices, with Brent crude (+5.20%) posting its biggest daily gain since May 4th, peaking at $80.59/bbl but closing a couple of dollars lower. For reference, that’s still a long way beneath its recent peak in absolute terms, having approached $120/bbl during the initial phase of the conflict. But it’s a clear shift away from the downward trajectory for oil back in Q2, and the various headlines revived fears about a more persistent inflationary shock. Indeed, the 1yr Euro inflation swap surged +26.8bps yesterday to 2.14%.

With stagflation concerns back on the agenda, that led investors to price back in more rate hikes. For instance, the probability of a Fed hike as soon as this month was up +3.2bps to 30.5% by the close, and the amount of hikes priced by December was up +4.8bps on the day to 42.2bps. Meanwhile at the ECB, there was an even bigger hawkish repricing, with the amount of hikes by December up +12.7bps on the day to 39.5bps. And given the ECB already hiked in June, that pricing implies a growing chance that they might end up hiking 3 times by the end of the year.

Just like when the conflict began, yesterday’s re-escalation caused significant damage to sovereign bonds, particularly in Europe given the region’s exposure to the energy shock. So 10yr bund yields (+9.9bps) surged back up to 3.09%, marking its biggest daily jump since May. And over in France, there was an even bigger milestone, as the 10yr OAT yield (+13.5bps) closed at 3.93%, marking its highest level since 2009. Then in the US, the moves weren’t quite as aggressive, but the 10yr Treasury yield (+2.8bps) still rose to 4.58%, and the 10yr real yield (+2.4bps) closed at a 17-month high of 2.31%.

Later on, we also had the minutes from last month’s FOMC meeting, which was the first with new Chair Kevin Warsh. The minutes added further credence to the hawkish market pricing seen since the meeting last month. While much of the committee agreed that inflation would cool as energy prices fell and one-off tariff impacts subsided, there were some worries of persistent underlying price pressures. Artificial Intelligence and the corresponding build out seemed top of mind for the committee, as “many participants noted that ongoing strong demand for AI infrastructure would likely sustain upward pressure on prices for technology products and electricity.” There is also greater concern amongst the committee that consumers and businesses are increasingly expecting higher prices.

However, most Fed officials said in the minutes that they put more weight on financial market measures of inflation expectations rather than surveyed responses.

Given the stagflationary backdrop, this meant equities took a big hit on both sides of the Atlantic. So the S&P 500 fell -0.28%, with a broad-based decline that saw 78% of the index lose ground. Once again, the move in chip stocks was against the overall market as the Philly semiconductor index (+2.23%) outperformed. The outperformance was bolstered by two large news stories. First, SK Hynix’s US offering was more than seven times oversubscribed, with the ADR set to raise nearly $24.5bn and become the second largest debut for a foreign company after Alibaba ($25bn). Second, it was reported that China had plans to allow some domestic AI companies to purchase Nvidia’s H200 chips. Outside of the semiconductor rally, the only other S&P 500 industry groups to gain yesterday were Tech Hardware (+1.52%), Energy (+1.45%), and Consumer Staples (+1.15%) – the other 21 industry groups were lower on the day.

Over in Europe, those declines were even more severe, with Spain seeing the worst of the declines after Trump renewed his calls to end trade with Spain. This was at the NATO summit, where he said “Spain is a wasted cause” and that “We don’t want to do any trade business with Spain anymore.” Moreover, WSJ reporter Brian Schwartz posted that US officials would provide Trump a list of Spanish products that could be embargoed in the coming days. So that meant the IBEX 35 (-2.73%) posted a significant decline, sharply underperforming the Europe-wide STOXX 600 (-1.61%). That said, there wasn’t much good news anywhere in Europe, with the DAX (-2.23%), the CAC 40 (-2.18%) and the FTSE MIB (-1.22%) all posting significant declines as well.

Coming back to China, June inflation data revealed a diverging trend, highlighting uneven price pressures in the economy. CPI eased more than expected, rising +1.0% year-over-year (vs. +1.1% consensus) and slowing from May’s +1.2% reading. In contrast, factory-gate inflation (PPI) accelerated to a four-year high of +4.1% year-over-year, matching forecasts. On a month-over-month basis, however, producer prices fell -0.3%, the first such decline since July 2025.

Looking at the day ahead now, data releases include US existing home sales for June, and the weekly initial jobless claims. Meanwhile from central banks, we’ll get the ECB’s account of their June meeting, and hear from the ECB’s Escriva, the Fed’s Williams and Logan, and the BoE’s Breeden.

Tyler Durden

Thu, 07/09/2026 – 08:26

via ZeroHedge News https://ift.tt/3qaxbc8 Tyler Durden