Authored by Gail Tverberg via Our Finite World blog,

We live in a world where words are very carefully chosen. Companies hire public relations firms to give just the right “spin” to what they are saying. Politicians make statements which suggest that everything is going well. Newspapers would like their advertisers to be happy; they certainly won’t suggest that the automobile you purchase today may be of no use to you in five years.

I believe that what has happened in recent years is that the “truth” has become very dark. We live in a finite world; we are rapidly approaching limits of many kinds. For example, there is not enough fresh water for everyone, including agriculture and businesses. This inadequate water supply is now tipping over into inadequate food supply in quite a few places because irrigation requires fresh water. This problem is, in a sense, an energy problem, because adding more irrigation requires more energy supplies used for digging deeper wells or making desalination plants. We are reaching energy scarcity issues not too different from those of World War I, World War II and the Depression Era between the wars.

We now live in a strange world filled with half-truths, not too different from the world of the 1930s. US newspapers leave out the many stories that could be written about rising food insecurity around the world, and even in the US. We see more reports of conflicts among countries and increasing gaps between the rich and the poor, but no one explains that such changes are to be expected when energy consumption per capita starts falling too low.

The majority of people seem to believe that all of these problems can be fixed simply by increasingly taxing the rich and using the proceeds to help the poor. They also believe that the biggest problem we are facing is climate change. Very few are even aware of the food scarcity problems occurring in many parts of the world already.

Our political leaders started down the wrong path long ago, when they chose to rely on economists rather than physicists. The economists created the fiction that the economy could expand endlessly, even with falling energy supplies. The physicists understood that the economy requires energy for growth, but didn’t really understand the financial system, so they weren’t in a position to explain which parts of economic theory were incorrect. Even as the true story becomes increasingly clear, politicians stick to their belief that our only energy problem is the possibility of using too much fossil fuel, with the result of rising world temperatures and disrupted weather patterns. This can be interpreted as a relatively distant problem that can be corrected over a fairly long future period.

In this post, I will explain why it appears to me that, right now, we are dealing with an energy problem as severe as that which seems to have led to World War I, World War II, and the Great Depression. We really need a solution to our energy problems right now, not in the year 2050 or 2100. Scientists modeled the wrong problem: a fairly distant energy problem which would be associated with high energy prices. The real issue is a very close-at-hand energy shortage problem, associated with relatively low energy prices. It should not be surprising that the solutions scientists have found are mostly absurd, given the true nature of the problem we are facing.

[1] There is a great deal of confusion with respect to which energy problem we are dealing with. Are we dealing with a near-at-hand problem featuring inadequate prices for producers or a more distant problem featuring high prices for consumers? It makes a huge difference in finding a solution, if any.

Business leaders would like us to believe that the problem to be concerned with is a fairly distant one: climate change. In fact, this is the problem most scientists are working on. There is a common misbelief that fossil fuel prices will jump to high levels if they are in short supply. These high prices will allow the extraction of a huge amount of coal, oil and natural gas from the ground. The rising prices will also allow high-priced alternatives to become competitive. Thus, it makes sense to start down the long road of trying to substitute “renewables” for fossil fuels.

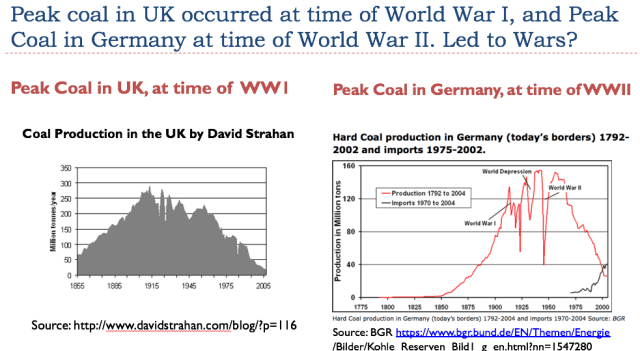

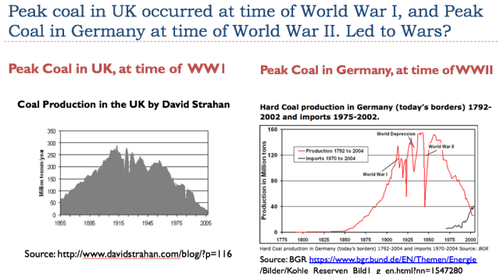

If business leaders had stopped to look at the history of coal depletion, they would have discovered that expecting high prices when energy limits are encountered is incorrect. The issue that really happens is a wage problem: too many workers discover that their wages are too low. Indirectly, these low-wage workers need to cut back on purchases of goods of many types, including coal to heat workers’ homes. This loss of purchasing power tends to hold coal prices down to a level that is too low for producers. We can see this situation if we look at the historical problems with coal depletion in the UK and in Germany.

Coal played an outsized role in the time leading up to, and including, World War II.

Figure 1. Figure by author describing peak coal timing.

History shows that as early coal mines became depleted, the number of hours of labor required to extract a given amount of coal tended to rise significantly. This happened because deeper mines were needed, or mines were needed in areas where there were only thin coal seams. The problem owners of mines experienced was that coal prices that did not rise enough to cover their higher labor costs, related to depletion. The issue was really that prices fell too low for coal producers.

Owners of mines found that they needed to cut the wages of miners. This led to strikes and lower coal production. Indirectly, other coal-using industries, such as iron production and bread baking, were adversely affected, leading these industries to cut jobs and wages, as well. In a sense, the big issue was growing wage disparity, because many higher-wage workers and property owners were not affected.

Today, the issue we see is very similar, especially when we look at wages worldwide, because markets are now worldwide. Many workers around the world have very low wages, or no wages at all. As a result, the number of workers worldwide who can afford to purchase goods that require large amounts of oil and coal products for their manufacture and operation, such as vehicles, tends to fall. For example, peak sales of private passenger automobile, worldwide, occurred in 2017. With fewer auto sales (as well as fewer sales of other high-priced goods), it is difficult to keep oil and coal prices high enough for producers. This is very similar to the problems of the 1914 to 1945 era.

Everything that I can see indicates that we are now reaching a time that is parallel to the period between 1914 and 1945. Conflict is one of the major things that a person would expect because each country wants to protect its jobs. Each country also wants to add new jobs that pay well.

In a period parallel to the 1914 to 1945 period, we can also expect pandemics. This happens because the many poor people often cannot afford adequate diets, making them more susceptible to diseases that are easily transmitted. In the Spanish Flu epidemic of 1918-1919, more than 50 million people worldwide died. The equivalent number with today’s world population would be about 260 million. This hugely dwarfs the 3.2 million COVID-19 deaths around the world that we have experienced to date.

[2] If we look at growth in energy supply, relative to the growth in population, precisely the same type of “squeeze” is occurring now as was occurring in the 1914 to 1945 period. This squeeze particularly affects coal and oil supplies.

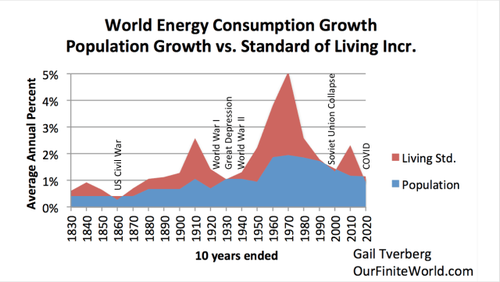

Figure 2. The sum of red and blue areas on the chart represent average annual world energy consumption growth by 10-year periods. Blue areas represent average annual population growth percentages during these 10-year periods. The red area is determined by subtraction. It represents the amount of energy consumption growth that is “left over” for growth in people’s standards of living. Chart by Gail Tverberg using energy data from Vaclav Smil’s estimates shown in Energy Transitions: History, Requirements and Prospects, together with BP Statistical Data for 1965 and subsequent years.

The chart above is somewhat complex. It looks at how quickly energy consumption has been growing historically, over ten-year periods (sum of red and blue areas). This amount is divided into two parts. The blue area shows how much of this growth in energy consumption was required to provide food, housing and transportation to the growing world population, based on the standards at that time. The red area shows how much growth in energy consumption was “left over” for growth in the standard of living, such as better roads, more vehicles, and nicer homes. Note that GDP growth is not shown in the chart. It likely corresponds fairly closely to total energy consumption growth.

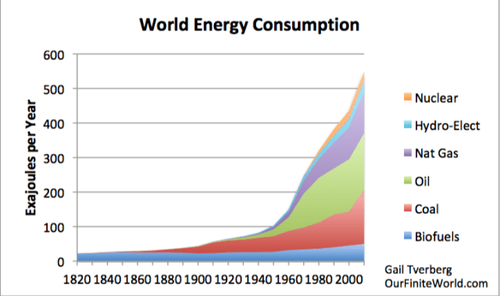

Figure 3, below, shows energy consumption by type of fuel between 1820 and 2010. From this, it is clear that the world’s energy consumption was tiny back in 1820, when most of the world’s energy came from burned biomass. Even at that time, there was a huge problem with deforestation.

Figure 3. World Energy Consumption by Source, based on Vaclav Smil estimates from Energy Transitions: History, Requirements and Prospects and together with BP’s Statistical Review of World Energy data for 1965 and subsequent years. (Wind and solar are included with biofuels.)

Clearly, the addition of coal, starting shortly after 1820, allowed huge changes in the world economy. But by 1910, this growth in coal consumption was flattening out, leading quite possibly to the problems of the 1914-1945 era. The growth in oil consumption after World War II allowed the world economy to recover. Natural gas, hydroelectric and nuclear have been added in recent years, as well, but the amounts have been less significant than those of coal and oil.

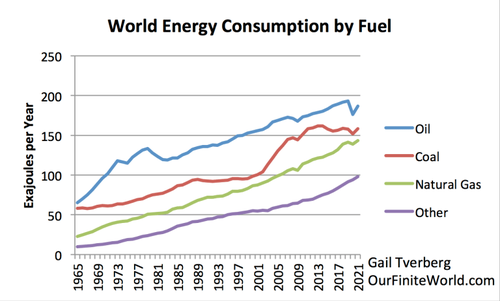

We can see how coal and oil have dominated growth in energy supplies in other ways, as well. This is a chart of energy supplies, with a projection of expected energy supplies through 2021 based on estimates of the IEA’s Global Energy Review 2021.

Figure 4. World energy consumption by fuel. Data through 2019 based on information from BP’s Statistical Review of World Energy 2020. Amounts for 2020 and 2021 based on percentage change estimates from IEA’s Global Energy Review 2021.

Oil supplies became a problem in the 1970s. There was briefly a dip in the demand for oil supplies as the world switched from burning oil to the use of other fuels in applications where this could easily be done, such as producing electricity and heating homes. Also, private passenger automobiles became smaller and more fuel efficient. There has been a continued push for fuel efficiency since then. In 2020, oil consumption was greatly affected by the reduction in personal travel associated with the COVID-19 epidemic.

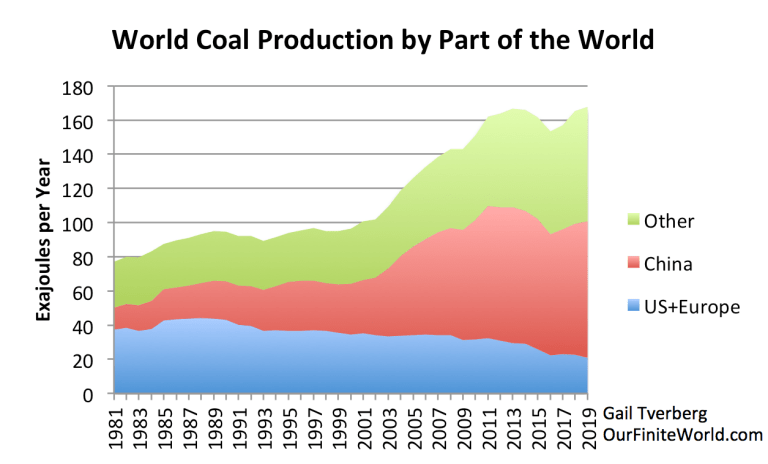

Figure 4, above, shows that world coal consumption has been close to flat since about 2012. This is also evident in Figure 5, below.

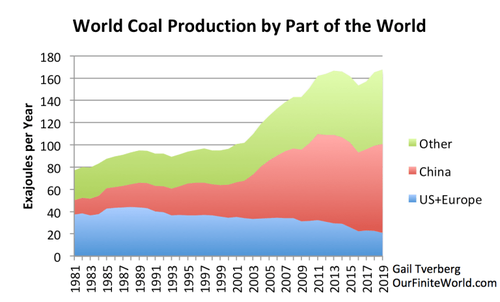

Figure 5. World coal production by part of the world, based on data of BP’s Statistical Review of World Energy, 2020.

Figure 5 shows that coal production for the United States and Europe has been declining for a very long time, since about 1988. Before China joined the World Trade Organization (WTO) in 2001, its coal production grew at a moderate pace. After joining the WTO in 2001, China’s coal production grew very rapidly for about 10 years. In about 2011, China’s coal production leveled off, leading to the leveling of world coal production.

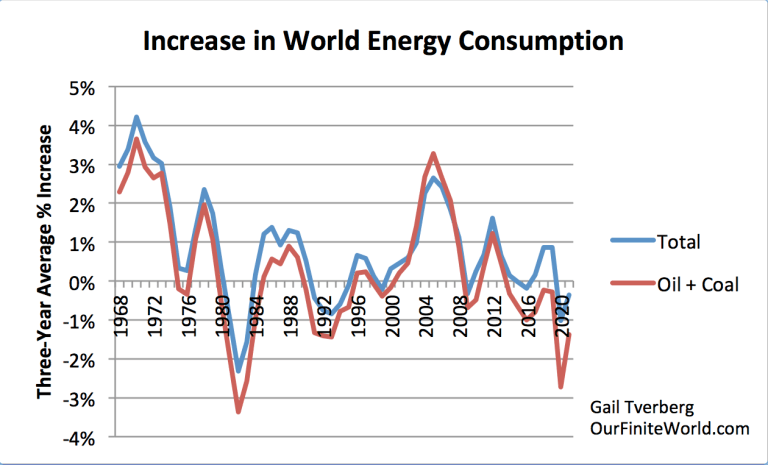

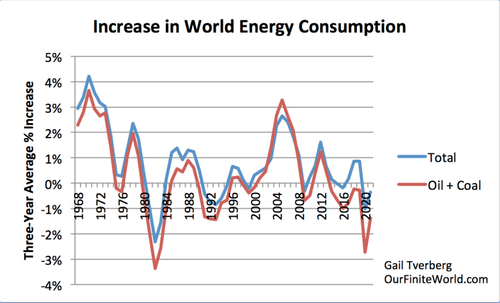

Figure 6 shows that recently, growth in the sum of oil and coal consumption has been lagging total energy consumption.

Figure 6. Three-year average annual increase in oil and coal consumption versus three-year average increase in total energy consumption, based on a combination of BP data through 2019 from BP’s Statistical Review of World Energy, 2010 and IEA’s 2020 and 2021 percentage change forecasts, from its Global Energy Review 2021.

We can see from Figure 6 that the only recent time when oil and coal supplies grew faster than energy consumption in total was during a brief period between 2002 and 2007. More recently, oil and coal consumption has been increasingly lagging total energy consumption. For both coal and oil, the problem has been that low prices for producers cause producers to voluntarily drop out of coal or oil production. The reason for this is two-fold: (1) With less oil (or coal) production, perhaps prices might rise, making production more profitable, and (2) Unprofitable oil (or coal) production isn’t really satisfactory for producers.

When determining the required level of profitability for these fuels, there is a need to include the tax revenue that governments require in order to maintain adequate services. This is especially the case with oil exporters, but it is also true in general. Energy products, to be useful, produce an energy surplus that can be used to benefit the rest of the economy. The way that this energy surplus can be transferred to the rest of the economy is by paying relatively high taxes. These taxes allow changes that aid economic growth, such as improvements in roads and schools.

If energy prices are chronically too low (so that an energy product requires a subsidy, rather than paying taxes), this is a sign that the energy product is most likely an energy “sink.” Such a product acts in the direction of pulling the economy down through ever-lower productivity.

[3] Governments have chosen to focus on preventing climate change because, in theory, the changes that are needed to prevent climate change seem to be the same ones needed to cover the contingency of “running out.” The catch is that the indicated changes don’t really work in the scarcity situation we are already facing.

It turns out that the very fuels that we seem to be running out of (coal and oil) are the very ones most associated with high carbon dioxide emissions. Thus, focusing on climate change seems to please everyone. Those who were concerned that we could keep extracting fossil fuels for hundreds of years and, because of this, completely ruin the climate, would be happy. Those who were concerned about running out of fossil fuels would be happy, as well. This is precisely the kind of solution that politicians prefer.

The catch is that we used coal and oil first because, in a very real sense, they are the “best” fuels for our needs. All of the other fuels, even natural gas, are in many senses inferior. Natural gas has the problem that it is very expensive to transport and store. Also, methane, which makes up the majority of natural gas, is itself a gas that contributes to global warming. It tends to leak from pipelines and from ships attempting to transport it. Thus, it is doubtful that it is much better from a global warming perspective than coal or oil.

So-called renewable fuels tend to be very damaging to the environment in ways other than CO2 emissions. This point is made very well in the new book Bright Green Lies by Derrick Jensen, Lierre Keith and Max Wilbert. It makes the point that renewable fuels are not an attempt to save the environment. Instead, they are trying to save our current industrial civilization using approaches that tend to destroy the environment. Cutting down forests, even if new trees are planted in their place, is especially detrimental. Alice Friedemann, in her new book, Life after Fossil Fuels: A Reality Check on Alternative Fuels, points out the high cost of these alternatives and their dependence on fossil fuel energy.

We are right now in a huge scarcity situation which is starting to cause conflicts of many kinds. Even if there were a way of producing these types of alternative energy cheaply enough, they are coming far too late and in far too small quantities to make a difference. They also don’t match up with our current coal and oil uses, adding a layer of time and expense for conversion that needs to be included in any model.

[4] What we really have is a huge conflict problem due to inadequate energy supplies for today’s world population. The powers that be are trying to hide this problem by publishing only their preferred version of the truth.

The situation that we are really facing is one that often goes under the name of “collapse.” It is a problem that many civilizations have faced in the past when a given population has outgrown its resource base.

Needless to say, the issue of collapse is not a story any politician wants to tell its citizens. Instead, we are told over and over, “Everything is fine. Any energy problem will be handled by the solutions scientists are finding.” The catch is that scientists were not told the correct problem to solve. They were told about a distant problem. To make the problem easier to solve, high prices and subsidies seemed to be acceptable. The problem they were asked to solve is very different from our real energy problem today.

Many people think that taxing the rich and giving the proceeds to the poor can solve our problem, but this doesn’t really solve the problem for a couple of reasons. One of the issues is that our scarcity issue is really a worldwide problem. Higher taxation of the rich in a few rich countries does nothing for the many problems of poor people in countries such as Lebanon, Yemen, Venezuela and India. Furthermore, taking money from the rich doesn’t really fix scarcity problems. Rich people don’t really eat a vastly disproportionate amount of food or drink more water, for example.

A detail that most of us don’t think about is that the military of many different countries has been very much aware of the potential conflict situation that is now occurring. They are aware that a “hot war” would require huge use of fossil fuel energy, so they have been trying to find alternative approaches. One approach military groups have been working on is the use of bioweapons of various kinds. In fact, some groups might even contemplate starting a pandemic. Another approach that might be used is computer viruses to disrupt the systems of other countries.

Needless to say, the powers that be do not want the general population to hear about issues of these kinds. We find ourselves with narrower and narrower news reports that provide only the version of the truth that politicians and news media want us to read. Citizens who have developed the view, “All I need to do to find out the truth is read my home town newspaper,” are likely to encounter more and more surprises, as conflict situations escalate.