Russia is uneasy over the destabilization of Tehran, and on other hotspots the powers’ positions are clear…

Even veiled by thick layers of diplomatic fog, the overlapping meetings in Sochi between US Secretary of State Mike Pompeo and President Putin and Foreign Minister Sergey Lavrov still offer tantalizing geopolitical nuggets.

Russian presidential aide Yury Ushakov did his best to smooth the utterly intractable, admitting there was “no breakthrough yet” during the talks but at least the US “demonstrated a constructive approach.”

Putin told Pompeo that after his 90-minute phone call with Trump, initiated by the White House, and described by Ushakov as “very good,” the Russian president “got the impression that the [US] president was inclined to re-establish Russian-American relations and contacts to resolve together the issues that are of mutual interest to us.”

That would imply a Russiagate closure. Putin told Pompeo, in no uncertain terms, that Moscow never interfered in the US elections, and that the Mueller report proved that there was no connection between the Kremlin and the Trump campaign.

This adds to the fact Russiagate has been consistently debunked by the best independent American investigators such as the VIPS group.

‘Interesting’ talk on Iran

Let’s briefly review what became public of the discussions on multiple (hot and cold) conflict fronts – Venezuela, North Korea, Afghanistan, Iran.

Venezuela – Ushakov reiterated the Kremlin’s position: “Any steps that may provoke a civil war in the country are inadmissible.” The future of President Maduro was apparently not part of the discussion.

That brings to mind the recent Arctic Council summit. Both Lavrov and Pompeo were there. Here’s a significant exchange:

Lavrov: I believe you don’t represent the South American region, do you?

Pompeo: We represent the entire hemisphere.

Lavrov: Oh, the hemisphere. Then what’s the US doing in the Eastern Hemisphere, in Ukraine, for instance?

There was no response from Pompeo.

North Korea – Even acknowledging that the Trump administration is “generally ready to continue working [with Pyongyang] despite the stalemate at the last meeting, Ushakov again reiterated the Kremlin’s position: Pyongyang will not give in to “any type of pressure,” and North Korea wants “a respectful approach” and international security guarantees.

Afghanistan – Ushakov noted Moscow is very much aware that the Taliban are getting stronger. So the only way out is to find a “balance of power.” There was a crucial trilateral in Moscow on April 25 featuring Russia, China and the US, where they all called on the Taliban to start talking with Kabul as soon as possible.

Iran – Ushakov said the JCPOA, or Iran nuclear deal, was “briefly discussed.”.He would only say the discussion was “interesting.”

Talk about a larger than life euphemism. Moscow is extremely uneasy over the possibility of a destabilization of Iran that allows a free transit of jihadis from the Caspian to the Caucasus.

Which brings us to the heart of the matter. Diplomatic sources – from Russia and Iran – confirm, off the record, there have been secret talks among the three pillars of Eurasian integration – Russia, China and Iran – about Chinese and Russian guarantees in the event the Trump administration’s drive to strangle Tehran to death takes an ominous turn.

This is being discussed at the highest levels in Moscow and Beijing. The bottom line: Russia-China won’t allow Iran to be destroyed.

But it’s quite understandable that Ushakov wouldn’t let that information slip through a mere press briefing.

Wang Yi and other deals

On multiple fronts, what was not disclosed by Ushakov is way more fascinating than what’s now on the record. There’s absolutely no way Russian hypersonic weapons were not also discussed, as well as China’s intermediate-range missiles capable of reaching any US military base encircling or containing China.

US Secretary of State Mike Pompeo, third right, meets Russian Foreign Minister Sergei Lavrov, center left, in Sochi on 14 May 2019. Photo: AFP / Russian Foreign Ministry Press Service / Anadolu

The real deal was, in fact, not Putin-Pompeo or Pompeo-Lavrov in Sochi. It was actually Lavrov-Wang Yi (the Chinese Foreign Minister), the day before in Moscow.

A US investment banker doing business in Russia told me:

“Note how Pompeo ran like mad to Sochi. We are frightened and overstretched.”

Diplomats later remarked: “Pompeo looked solemn afterwards. Lavrov sounded very diplomatic and calm.” It’s no secret in Moscow’s top diplomatic circles that the Chinese Politburo overruled President Xi Jinping’s effort to find an accommodation to Trump’s tariff offensive. The tension was visible in Pompeo’s demeanor.

In terms of substance, it’s remarkable how Lavrov and Wang Yi talked about, literally, everything: Syria, Iran, Venezuela, the Caspian, the Caucasus, New Silk Roads (BRI), Eurasia Economic Union (EAEU), Shanghai Cooperation Organization (SCO), missiles, nuclear proliferation.

Or as Lavrov diplomatically put it:

“In general, Russia-China cooperation is one of the key factors in maintaining the international security and stability, establishing a multipolar world order. . . . Our states cooperate closely in various multilateral organizations, including the UN, G20, SCO, BRICS and RIC [Russia, India, China trilateral forum], we are working on aligning the integration potential of the EAEU and the Belt and Road Initiative, with potentially establishing [a] larger Eurasian partnership.”

The strategic partnership is in sync on Venezuela, Syria, Iran, Afghanistan – they want a solution brokered by the SCO. And on North Korea, the message could not have been more forceful.

After talking to Wang Yi, Lavrov stressed that contacts between Washington and North Korea “proceeded in conformity with the road map that we had drafted together with China, from confidence restoration measures to further direct contacts.”

This is a frank admission that Pyongyang gets top advice from the Russia-China strategic partnership. And there’s more:

“We hope that at a certain point a comprehensive agreement will be achieved on the denuclearization of the Korean Peninsula and on the creation of a system of peace and security in general in Northeast Asia, including concrete firm guarantees of North Korea’s security.”

Translation: Russia and China won’t back down on guaranteeing North Korea’s security. Lavrov said:

“Such guarantees will be not easy to provide, but this is an absolutely mandatory part of a future agreement. Russia and China are prepared to work on such guarantees.”

Reset, maybe?

The indomitable Maria Zakharova, Russian Ministry of Foreign Affairs spokeswoman, may have summed it all up. A US-Russia reset may even, eventually, happen. Certainly, it won’t be of the Hillary Clinton kind, especially when current CIA director Gina Haspel is shifting most of the agency’s resources towards Iran and Russia.

Top Russian military analyst Andrei Martyanov was way more scathing. Russia won’t break with China, because the US “doesn’t have any more a geopolitical currency to ‘buy’ Russia – she is out of [the] price range for the US.”

That left Ushakov with his brave face, confirming there may be a Trump-Putin meeting on the sidelines of the G20 summit in Osaka next month.

“We can organize a meeting ‘on the go’ with President Trump. Alternatively, we can sit down for a more comprehensive discussion.”

Under the current geopolitical incandescence, that’s the best rational minds can hope for.

via ZeroHedge News http://bit.ly/2VGuSv2 Tyler Durden

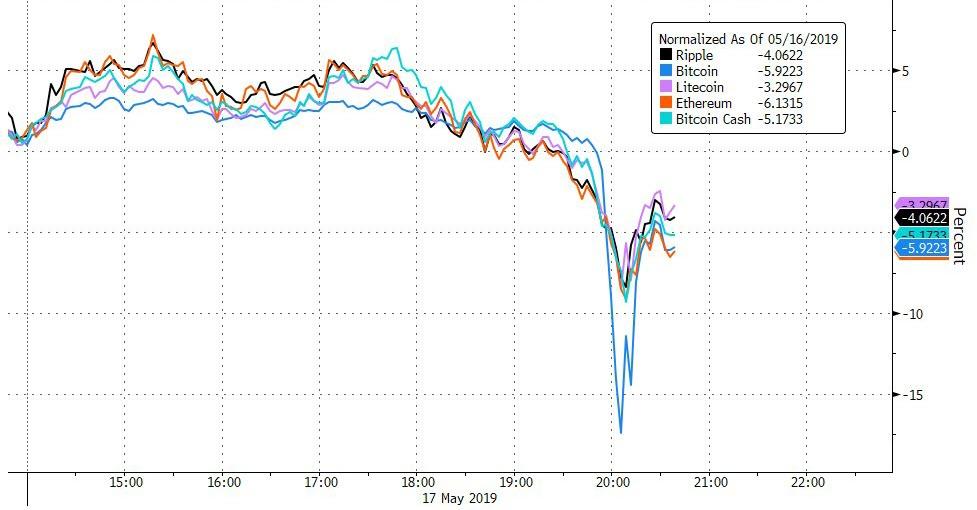

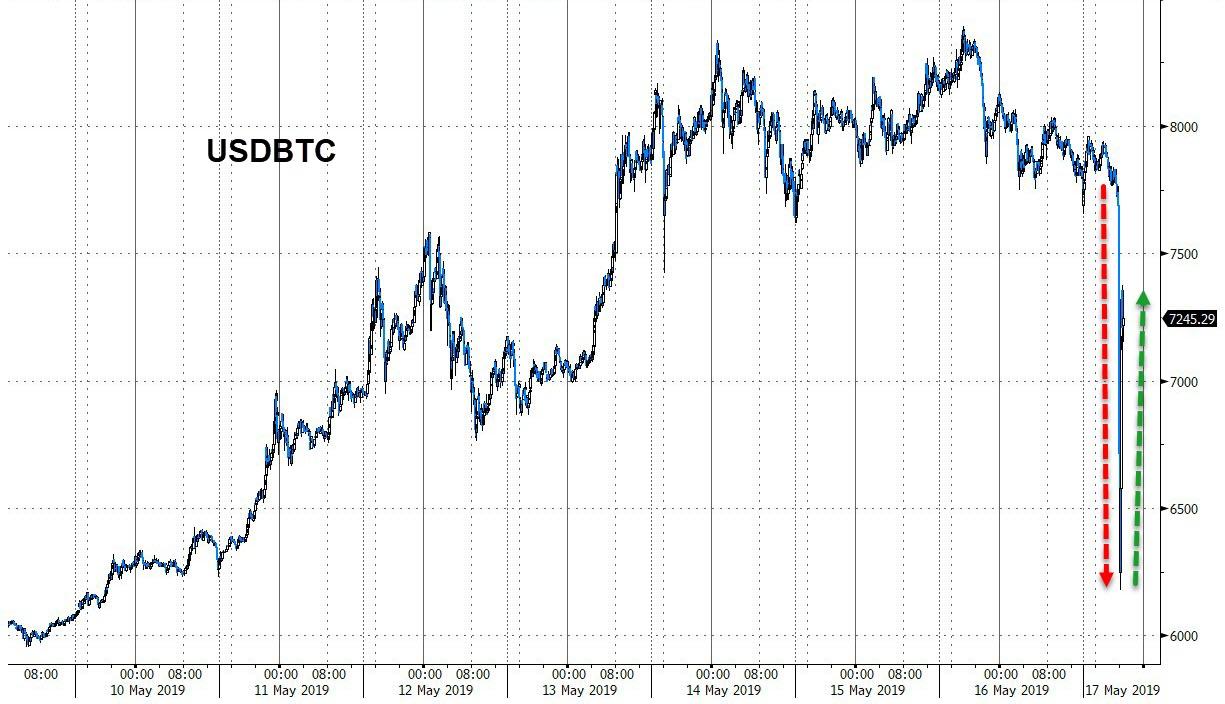

Shortly before 11pmET, cryptos suddenly jerked lower with Bitcoin flash-crashing over 15% before bouncing back…

Bitcoin was hit the hardest…

Bitcoin collapsed over $1500 before quickly ramping back higher…

No immediate catalyst for the moves in crypto but we note that China’s offshore yuan started to accelerate lower at the same time…

As did US equity futures…

After commentaries run by Chinese state media outlets on Friday suggest the nation has little no interest in continuing trade negotiations with the U.S. for now.

via ZeroHedge News http://bit.ly/2W8T6NZ Tyler Durden

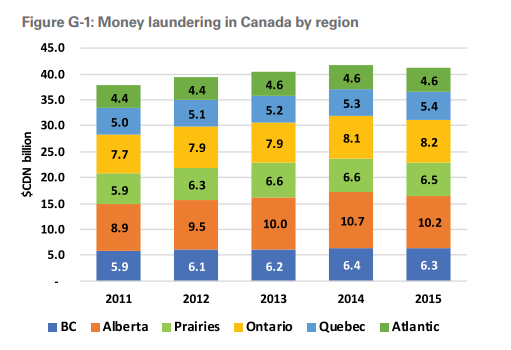

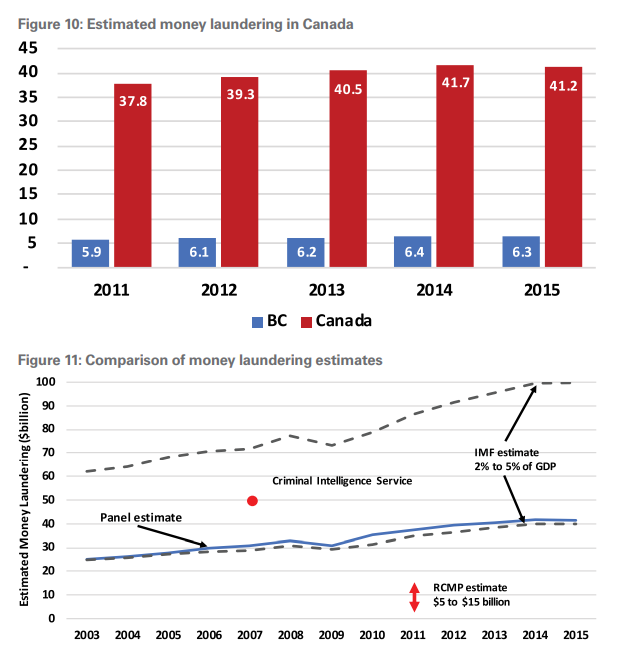

On the heels of a stunning report revealing over $7 billion in laundered money through British Columbia in 2018 (mostly in the form of Chinese oligarchs buying Vancouver real estate and using it to park money offshore), the province will finally hold a public inquiry into money laundering, according to CBC. The decision was announced by BC Premier John Horgan and Attorney General David Eby on Wednesday morning. They were joined by Finance Minister Carole James.

At the announcement, Horgan said: “It became abundantly clear to us that the depth and the magnitude of money laundering in British Columbia was far worse than we imagined when we were first sworn in, and that’s why we established the public inquiry today.”

Heading up the inquiry will be B.C. Supreme Court Justice Austin F. Cullen, who will be looking into real estate, gaming, financial institutions and the corporate and professional sectors. Eby claimed that the recent report formed the basis for the inquiry, while also noting that some individuals had refused to participate in voluntary reviews. Cullen has been given “significant” powers to compel witnesses, testimony, gather evidence and search and seize records with a warrant.

Eby also said that Organized Crime Reduction Minister Bill Blair assured him that the government would cooperate with the inquiry. Eby said: “We are done with asking nicely. Today, our government has given Justice Cullen the authority to do more than ask for voluntary participation.”

“If there is testimony that the commissioner needs to get to the bottom of this, he will compel that testimony. We’re not constraining the commissioner in any way,” Horgan said.

Earlier this week we discussed a report detailing the extent of money laundering in the Canadian province, which included more than $5.3 billion being laundered through the real estate market. The independent report released just days ago concluded that an astounding $7.4 billion was laundered in British Columbia in 2018, out of a total of $46.7 billion laundered across Canada throughout the same period. The report was published by an expert panel led by former B.C. deputy attorney general Maureen Maloney.

The reports come after the government commissioned them to try and shed light on laundering by organized crime in BC’s real estate market. This follows last June’s report on dirty money in casinos, which we also wrote about just days ago.

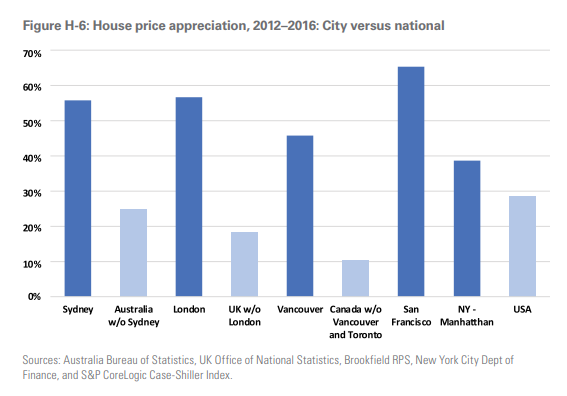

RCMP commissioner Peter German was commissioned to write the report on real estate, and he concluded that illicit money is what led to “a frenzy of buying” that caused housing prices to spike around Metro Vancouver. The report concluded that there are thousands of properties worth billions at high risk for money laundering.

An international anti-money laundering agency said last year that organized criminals were laundering about $1 billion per year in the province.

Green Leader Andrew Weaver had already called for a public inquiry: “Namely, that it would improve public awareness, play a crucial role in fault finding, and would help to develop full recommendations,” he said last week. In sum, the report made 29 recommendations, including for the entire province to launch a financial investigations unit.

Finance Minister Carole James said last week: “…all the recommendations look critical, but the government wants to ensure it’s prioritizing the most important ones, while also noting that action already underway in the legislature on some solutions.”

In late April, we highlighted measures that Vancouver casinos were taking against money laundering, noting that they were resulting in casinos taking a brutal hit to their bottom lines.

The final public inquiry report is expected to be delivered by May 2021 and an interim report is expected within the next 18 months.

via ZeroHedge News http://bit.ly/2WRhRLY Tyler Durden

For all practical purposes, the manner in which contestants have played “Jeopardy!” has not changed since Art Fleming provided the game show’s first “answer” 55 years ago. That is, until James Holzhauer took his place behind the podium earlier this year.

After winning 22 consecutive games by an astounding average margin of $64,913, one question must be asked: Had everyone of these contestants been playing this game the wrong way?

If this is indeed the case,“a professional sports gambler from Nevada” may have shown the world what’s possible when a template – never challenged or questioned over half a century – is blown up and replaced by another strategy that produces vastly superior results.

By now millions of Americans are familiar with James’s unorthodox “Jeopardy!” strategy. Unlike 99.9 percent of the game’s previous contestants, he starts at the bottom of the board and goes sideways.

“It seems pretty simple to me: If you want more money, start with the bigger-money clues,” Holzhauer explained in an interview with Vulture magazine. He told NPR “What I do that’s different than anyone who came before me is I will try to build the pot first” before seeking out the game’s Daily Doubles. He then “leverages” his winnings with “strategically aggressive” wagers (read: wagers far larger than any contestant before him was willing to make).

This strategy – along with the fact he’s answering 96.7 percent of the clues correctly – has allowed James to build insurmountable leads heading into Final Jeopardy. He can then be ultra-aggressive with his Final Jeopardy wagers, including one of $60,013. It was this wager that allowed James to establish his current single-game record of $131,016. (James now holds the Top 12 all-time records for one-game winnings).

In 22 episodes, James has earned $1.69 million. Given that each show takes about 24 minutes to play, James is averaging $192,045/hour.

How could a strategy that really is “pretty simple” – one that on a per-hour basis generates more income than any job in America – have been eschewed by approximately 25,000 previous contestants?

There are several possible answers to this question, none of which speaks particularly well of America, or Americans.

One is that most people are afraid to challenge “conventional wisdom.” If something’s been done the same way for decades by everyone, no one thinks that it can be done differently. And/or people have observed that those who do challenge the Status Quo (“Who is Galileo?”) aren’t always celebrated, at least in their own times.

Holzhauer’s contrarian approach to “Jeopardy!” has clearly rubbed many Americans the wrong way.

Washington Post columnist Charles Lane labeled Holzhauer a “menace” who is guilty of violating the “unwritten rules of the game,” a view endorsed by CNN host Michael Smerconish.

Other pundits accused Holzhauer of using tactics that are “unfair” or “bad for the game.” He’s been called divisive, polarizing and controversial, someone who has “destroyed the quaintness of the game” and given America “deadly dull television.” Some speculate he’s “gaming the system,” perhaps even cheating. Many message board posters have pledged to boycott the show until the “robotic” Holzhauer is defeated.

The opposite view – thankfully held by more Americans if message board posts are a gauge – is that James is a sensation whose accomplishments should be celebrated. According to one story, he’s the “man who solved ‘Jeopardy!’“

Another depressing possibility is that the overwhelming percentage of Jeopardy contestants (and, symbolically, the population writ large) is incapable of performing contrarian analysis, or of approaching a project or puzzle in a unique way. Americans have either known for decades that “Jeopardy!” was being played the wrong way but were too chicken to play it correctly, or James Holzhauer is the only American who figured the game out.

It’s too soon to tell if future contestants will emulate James’s strategy. For what it’s worth, over the past two weeks, 16 contestants have competed in Jeopardy’s “Teacher Tournament” and every contestant reverted to the game’s normal style of play. Such is the enduring power of conformity, of not challenging conventional wisdom.

But what if conventional wisdom is wrong? And how often is it wrong?

According to Washington Post columnist Robert Samuelson, the answer is “almost always.”

Indeed, Samuelson wrote an important if largely overlooked book on this very subject in 2001. The book’s title: Untruth: How The Conventional Wisdom Is (Almost Always) Wrong.

Samuelson’s thesis is that people or organizations with an “agenda” often create problems or a “crisis” that are exaggerated or not problems at all. The “solutions” policy makers give us typically make things worse.

One can take his premise and run with it … and it holds. A few conventional wisdom examples:

To protect our freedoms and save lives, America must invade, occupy or attack nation after nation, countries which pose great threats to our country and/or our freedoms.

Man-made climate change is the greatest threat to our planet and its inhabitants and can and must be reversed at all costs.

Donald Trump will never be elected president of the United States.

Donald Trump will drain the swamp.

Russia “hacked” an election.

There’s only one way to play “Jeopardy!”

Wrong. Wrong. Wrong. Wrong. Wrong. Wrong. Or, if not all wrong, at least not all sacrosanct.

Examples where conventional wisdom is often wrong could also be easily identified in the fields of science, health, economics and education. The point: if conventional wisdom really is “almost always wrong,” someone (or a lot of someones) need to expose this.

In the grand scheme of things, disproving the postulate that there’s only one way to play “Jeopardy!” might not seem like a big deal. It could be, however, if a rare “eureka!” moment opened the floodgates of independent thought among more Americans, a development that might qualify as a tectonic shift in any quest to shatter a sub-optimal Status Quo.

As I was researching James, I learned the fascinating identify of one of his sources of inspiration.

“Do you follow hot-dog eating?”

This out-of-left-field question came after a reporter with Vulture asked James to respond to the charge he had “broken” Jeopardy.

“No. Can’t say I do,” the interviewer responded.

James: “About a decade ago, nobody ever thought someone could eat more than, like, 25 hot dogs in ten minutes. But this guy named Takeru Kobayashi came along and he shattered the record by so much that people realized there was a new blueprint to do this.”

Here I was looking (in vain) for sports analogies to compare James’s paradigm-shifting strategy and it’s James himself who (of course) had the answer.

It wasn’t Secretariat winning by 31 lengths, or Bob Beamon breaking the long-jump record by almost 22 inches, or Wilt Chamberlain scoring 100 points in an NBA game who transcended what everyone thought was possible. These athletes were simply doing the same things they’d always done, just far better, at least on one occasion.

The example that caught James’s attention – and gave me my perfect analogy – was the story of a 130-pound Japanese man with the goal of eating a mind-boggling number of hot dogs.

Freakonomics Radio – an outfit that appreciates what’s possible when a puzzle is looked at in novel ways – did a podcast on the great Kobayashi.

Through intense study and trial-and-error experimentation, Kobayashi discovered that if he ripped the hot dog in two, squeezed each piece into a ball, dipped the balls in water (thereby breaking down the starch), squeezed out the excess water and tossed each ball into his mouth his stomach could tolerate many more dogs. These simple innovations helped Kobayashi double the existing record his first time out.

But here’s the kicker, one that offers hope for the world. Once Kobayashi smashed the record, his fellow competitors didn’t quit. They didn’t demand the rules be changed. They simply adapted their techniques and raised the level of their game. Today, an American once again holds the hot-dog-eating record – 72 wieners in 10 minutes!

The lesson is as obvious as Kobayashi’s bulging abdomen. When someone does think outside the box, when someone proves that performances once thought impossible are in fact easily obtainable, new levels of excellence become possible.

Back to James: “… So I’d be interested to see if there was a new paradigm in (‘Jeopardy!’). If someone comes along and breaks my record, and attributed it to my style, that would be really great,” he told Vulture.

When someone finally cures cancer, my wager is it will be someone like James Holzhauer, or Takeru Kobayashi. It will be someone who looks at all the work that’s come before him and says, “This doesn’t make sense. There’s a better way to approach this.”

Over the last two months James Holzhauer has been trying to teach Americans that eye-opening accomplishments are possible if one ignores or rejects conventional wisdom that is, in fact, wrong. The more Americans who absorb this lesson the better. But really it might take just one future James Holzhauer to improve our world. Let’s hope he or she’s been watching.

via ZeroHedge News http://bit.ly/2EdszVu Tyler Durden

As the international hand-wringing continues over whether there is an actual heightened “Iran threat” with American troops in the cross hairs, and as some US allies – notably Spain, Germany, and The Netherlands – actually withdraw their forces from US operations support in the region, we must ask at this point, what do we actually know in terms of Bolton’s original intelligence cited earlier this month which sparked the ongoing crisis?

Aside from knowing much or all of the intelligence was reportedly provided to the administration by Israeli Mossad, we have the piecemeal explanations of both top admin officials and regional allies. Secretary of State Mike Pompeo told Iraqi officials during his unplanned stopover in Baghdad last week that “U.S. intelligence showed Iran-backed militias moved missiles near bases housing American forces,” according to Fox.

Iranian weaponry and military equipment exhibition in Tehran on February 2, 2019. Image source: AFP

According to that report, a senior Iraqi source relayed of the US message: “They said if the U.S. were attacked on Iraqi soil, it would take action to defend itself without coordinating with Baghdad.” So the crisis appears focused on potential Iranian proxy actions in Iraq – apparently enough to take the very rare step of evacuating all non-emergency US personnel from the US embassy in Baghdad (a move that hadn’t even been done at the height of ISIS’ offensive across western and northern Iraqi).

However, US allies even disagree on this point. For starters, the deputy head of the US-led coalition, British Army Maj. Gen. Christopher Ghika, caused an almost unheard of row among allies when earlier this week he flatly stated: “No – there’s been no increased threat from Iranian-backed forces in Iraq and Syria,” in a videolink briefing at a Pentagon press conference.

Furthermore, Iraqi Prime Minister Adel Abdul Mahdi said on Tuesday that the Iraqis had no information showing “movements that constitute a threat to any side,” but added that his government “is doing its duty to protect all parties.”

So is the new “threat” which warranted the latest US military build-up, which has caused Iran’s military to warn “We are on the cusp of a full scale confrontation with the enemy” — all based on either Iran or Iran-backed “popular mobilization units” in Iraq moving around a few missiles? If so, it would be nothing new.

All the way back in August of last year we reported, based on Reuters, “Iran Stuns Enemies By Moving Ballistic Missiles To Iraq – Within Easy Striking Distance of Tel Aviv.” It was known at that time that Iran had transferred short-range ballistic missiles to Shia proxy forces in Iraq for “months” prior, according to Western and Iraqi intelligence sources. This is why a number of prominent Middle East watchers and military analysts have shrugged, “nothing new… nothing to see here” in response to the “new” vaunted White House intelligence. This also appears to be the attitude of Britain’s chain of command within the joint “Operation Inherent Resolve” coalition.

And enter the New York Times, which in a report published late Wednesday citing three defense officials, found that: “The intelligence that caused the White House to escalate its warnings about a threat from Iran came from photographs of missiles on small boats in the Persian Gulf that were put on board by Iranian paramilitary forces.”

Secret satellite photos of Iranian missiles in Persian Gulf ignites heated debate among White House, Congress, allies and the public over new threats from Iran https://t.co/F1i3G39Jt0

Overhead imagery showed fully assembled missiles, stoking fears that the Islamic Revolutionary Guards Corps would fire them at United States naval ships. Additional pieces of intelligence picked up threats against commercial shipping and potential attacks by Arab militias with Iran ties on American troops in Iraq.

The NYT also noted that some top lawmakers are seeking to ensure that Congress is consulted before taking any military action against Iran. Speaker Nancy Pelosi reportedly “criticized the administration’s lack of transparency on the intelligence” in a closed-door meeting involving House Democrats.

Pompeo’s latest statements presented in the earlier Fox report seems to confirm the new NYT report. US allies in the region have also reportedly dismissed the “satellite evidence” of the Iranians moving missiles as mere usual defensive posturing.

And then there’s the possibility that all of this bluster and heated war rhetoric and build-up could have merely originated from Iran’s moving or assembling missiles on their own soil or in their own territorial waters in the Persian Gulf.

via ZeroHedge News http://bit.ly/2Efe17Z Tyler Durden

U.S. policy through the Bush and Obama administrations was to soft-pedal questionable Chinese trade practices, pirating technology and theft of intellectual property in return for cheap manufactured goods and China’s willingness to finance trillions of dollars of U.S. government debt.

Now Trump has changed the rules of the game. He’s said lost jobs in the U.S. are not worth the cheap goods and cheap financing. He bet that China had no alternative but to keep producing those goods and keep buying our debt, even if the U.S. imposes tariffs to help create manufacturing jobs here.

President Trump and President Xi had been on a collision course involving issues of trade, tariffs, and currency manipulation, which are coming to a head.

It’s important to understand that China’s economy is not just about providing jobs, goods and services. It is about regime survival for a Chinese Communist Party that faces an existential crisis if it fails to deliver. It is an illegitimate regime that will remain in power only so long as it provides jobs and a rising living standard for the Chinese people. The overriding imperative of the Chinese leadership is to avoid societal unrest.

Once the Chinese job machine stalls out, popular unrest could emerge on a scale much greater than the 1989 Tiananmen Square protests. This is an existential threat to Communist power.

If China encounters a financial crisis, Xi could quickly lose what the Chinese call, “The Mandate of Heaven.” That’s a term that describes the intangible goodwill and popular support needed by emperors to rule China for the past 3,000 years.

If The Mandate of Heaven is lost, a ruler can fall quickly.

China has serious structural economic problems and its internal contradictions are catching up with it. Economies can grow through consumption, investment, government spending and net exports. The “Chinese miracle” has been mostly a matter of investment and net exports, with minimal spending by consumers.

The investment component was thinly disguised government spending — many of the companies conducting investment in large infrastructure projects were backed directly or indirectly by the government through the banks.

This investment was debt-financed. China is so heavily indebted that it is now at the point where more debt does not produce growth. Adding additional debt today slows the economy and calls into question China’s ability to service its existing debt.

China is now confronting an insolvent banking system, a real estate bubble, and a $1 trillion wealth management product Ponzi scheme that is starting to fall apart.

Up to half of China’s investment is a complete waste. It does produce jobs and utilize inputs like cement, steel, copper and glass. But the finished product, whether a city, train station or sports arena, is often a white elephant that will remain unused.

Chinese growth has been reported in recent years as 6.5–10% but is actually closer to 5% or lower once an adjustment is made for the waste. The Chinese landscape is littered with “ghost cities” that have resulted from China’s wasted investment and flawed development model.

What’s worse is that these white elephants are being financed with debt that can never be repaid. And no allowance has been made for the maintenance that will be needed to keep these white elephants in usable form if demand does rise in the future, which is doubtful.

Essentially, China is on the horns of a dilemma with no good way out. On the one hand, China has driven growth for the past eight years with excessive credit, wasted infrastructure investment and Ponzi schemes.

The Chinese leadership knows this, but they had to keep the growth machine in high gear to create jobs for millions of migrants coming from the countryside to the city and to maintain jobs for the millions more already in the cities.

The two ways to get rid of debt are deflation (which results in write-offs, bankruptcies and unemployment) or inflation (which results in theft of purchasing power, similar to a tax increase).

Both alternatives are unacceptable to the Communists because they lack the political legitimacy to endure either unemployment or inflation. Either policy would cause social unrest and unleash revolutionary potential.

China has hit a wall that development economists refer to as the “middle income trap.” Again, this happens to developing economies when they have exhausted the easy growth potential moving from low income to middle income and then face the far more difficult task of moving from middle income to high income.

The move to high-income status requires far more than simple assembly-style jobs staffed by rural dwellers moving to the cities. It requires the creation and adoption of high-value-added products enabled by high technology.

China has not shown much capacity for developing high technology on its own, but it has been quite effective at stealing such technology from trading partners and applying it through its own system of state-owned enterprises and “national champions” such as Huawei in the telecommunications sector.

Unfortunately for China, this growth by theft has run its course. The U.S. and its allies, such as Canada and the EU, are taking strict steps to limit further theft and are holding China to account for its theft so far by imposing punitive tariffs and banning Chinese companies from participation in critical technology rollouts such as 5G mobile phones.

My view is that a crisis in China is inevitable based on China’s growth model, the international financial climate and excessive debt. A countdown to crisis has begun. Geopolitical issues will make the economic issues even harder to resolve.

Yes, headlines are dominated by the trade war. That escalating confrontation is a big deal, but it’s not the only flash point in U.S.-China relations, and not even the most important. China is as much concerned about a military confrontation in the South China Sea as it is about the economic confrontation in the trade wars.

China dredged sand surrounding useless rocks and atolls in the South China Sea and converted them into artificial islands and then built out the islands to include naval ports, air force landing strips, anti-aircraft weapons and other defensive and offensive weapons systems.

Not only are the Chinese militarizing rocks, but they are trampling on competing claims by the Philippines, Vietnam, Brunei, Malaysia and other countries surrounding the sea.

The world has developed rules-based platforms for resolving these issues without military force. The U.S. is guaranteeing freedom of passage, freedom of the seas and the territorial rights of allies such as the Philippines.

So far, the U.S.-Chinese confrontation has been about naval vessels passing in close quarters and surveillance aircraft being harassed by fighter jets. The risk of such tactics is an accidental collision, a rogue shot fired or a command misunderstood.

Any such incident could lead to retaliation, and there’s no telling where it might stop. Trump is not someone to back down, and Chinese leadership does not want to appear weak before the U.S.

That’s especially true at a time of great economic uncertainty. China does not want war at this time. But diverting the people’s attention away from domestic problems toward a foreign foe is an old trick leaders use to unite the people in times of uncertainty. Rallying the people around the flag is a tried and true method to garner support.

If China’s leadership decides that the risk of losing legitimacy at home outweighs the risk of conflict with the United States, the likelihood of war rises dramatically.

I’m not predicting it, but wars have started over less. This is a very dangerous time.

Be sure to hold cash, gold, silver, land and other assets that will cushion you against a market crash.

via ZeroHedge News http://bit.ly/2HmIYch Tyler Durden

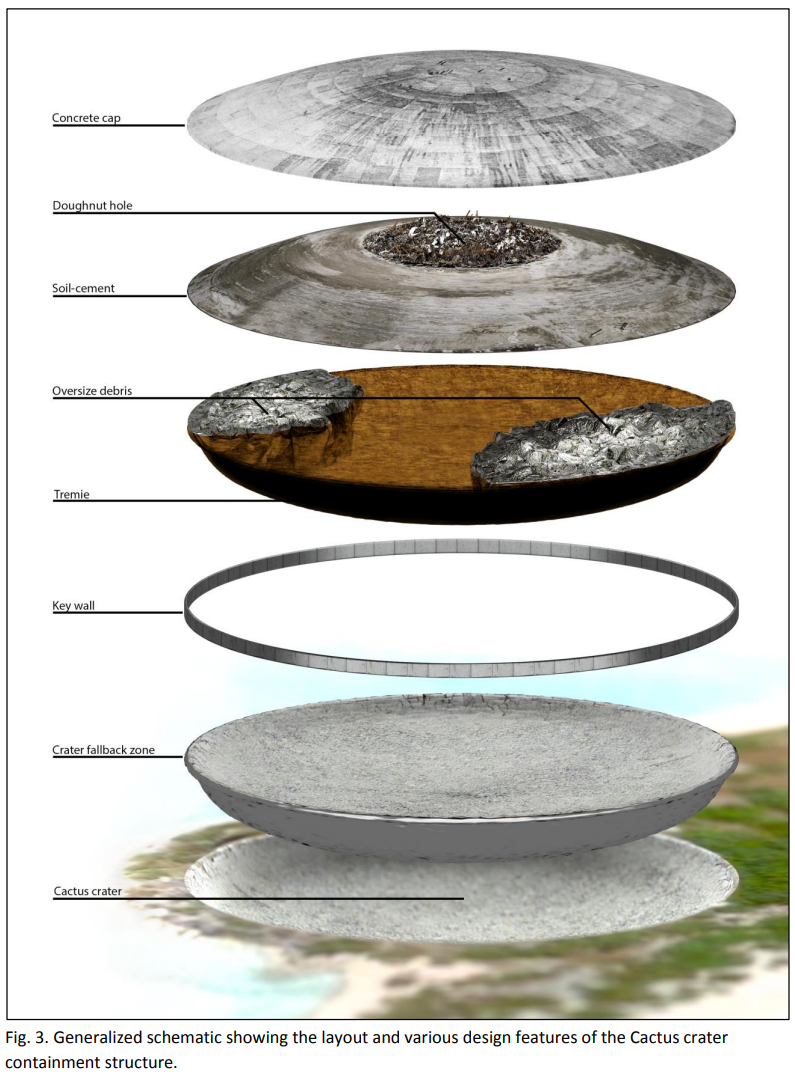

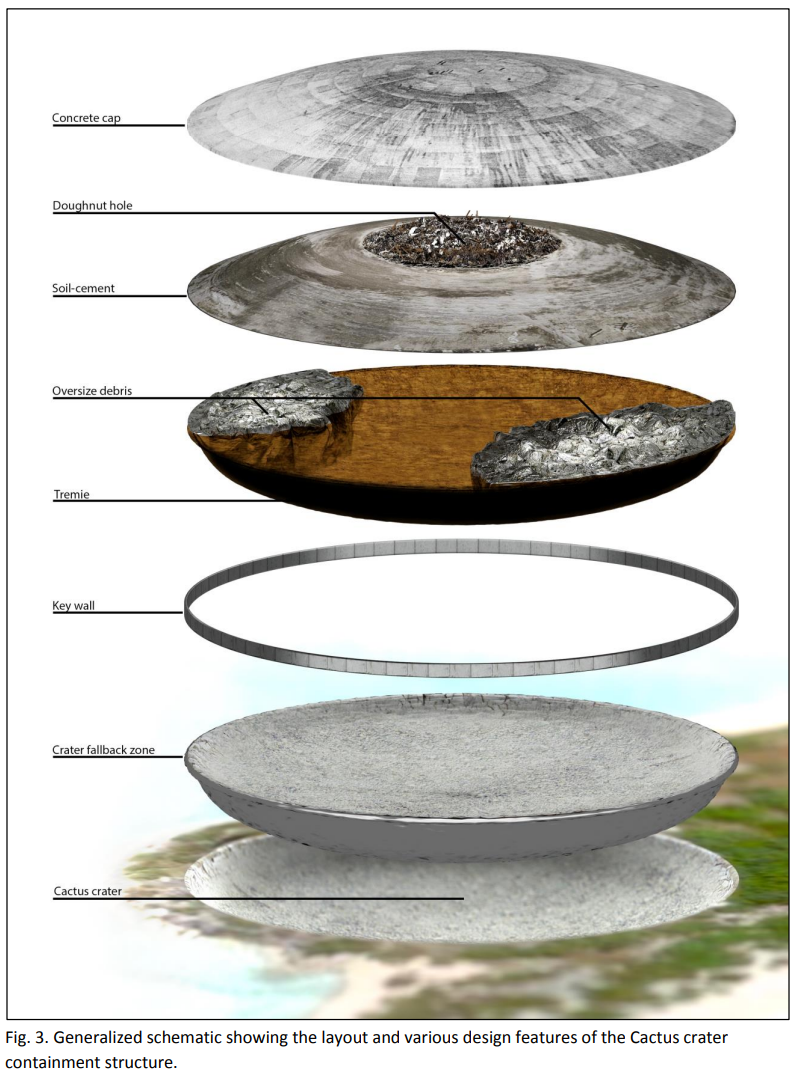

UN Secretary General Antonio Guterres has sounded the alarm over a giant concrete dome built 40 years ago in the Marshall Islands to contain radioactive waste from Cold War-era atomic tests.

According to Guterres, the dome – which houses approximately 73,000 cubic meters of debris on Runit island, part of the Enewetak Atoll – may be leaking radioactive material into the Pacific Ocean, as the porous ground underneath the 18″ thick dome was never lined as originally planned. It was constructed in the crater formed by the 18-kt Cactus test.

“The Pacific was victimised in the past as we all know,” Guterres told students in the island nation of Figi while on a tour of the South Pacific. “I’ve just been with the President of the Marshall Islands (Hilda Heine), who is very worried because there is a risk of leaking of radioactive materials that are contained in a kind of coffin in the area.”

DoE report, 2013

Residents of the Islands were relocated from their ancestral lands shortly after the United States began what would become 67 nuclear weapons tests from 1946 – 1958 at Bikini and Enewetak atolls. Despite US efforts to move people to safety, thousands of islanders were exposed to radioactive fallout from above-ground tests conducted before a moratorium was enacted in 1958.

The tests included the 15 Megaton Castle Bravo on the Bikini Atoll, which was detonated on March 1, 1954. It was the most powerful ever detonated by the United States – and around 1,000 times bigger than the bomb dropped on Hiroshima just nine years before.

The effort to clean up the region in the 1970s included approximately 4,000 US servicemen in what was known as the Enewetak Radiological Support Project.

Cracks are visible in the dome’s surface, and the sea sometimes washes over its surface during storms, according to ABC.

View from atop of Runit Dome showing the beach configuration on the north end of Runit Island at low tide (Reference Photo, May 2013).

“The United States Government has acknowledged that a major typhoon could break it apart and cause all of the radiation in it to disperse,” said Columbia University’s Michael Gerrard.

That said, a 2013 DoE report found that the soil outside of the dome is more contaminated than its contents – as the 1970s cleaning operation only removed an estimated 0.8 percent of the total nuclear waste in Enewetak atoll.

Guterres did not propose a solution, however he said that “a lot needs to be done in relation to the explosions that took place in French Polynesia and the Marshall Islands,” adding “This is in relation to the health consequences, the impact on communities and other aspects.”

And of course, reparations; “there are questions of compensation and mechanisms to allow these impacts to be minimised,” Guterres added.

via ZeroHedge News http://bit.ly/2HmHXRv Tyler Durden

President Trump has declared he will extend tariffs of 25% on all America’s imports of Chinese goods. China is responding with tariff increases of its own. The consequences of this action and reaction will be to kick-start higher monetary inflation in America and an economic slump. This article explains how an overdue credit crisis will be made considerably worse by trade protectionism. It could become the credit crisis to end all credit crises and undermine the whole fiat currency system.

Introduction

Following President Trump’s imposition of 25% tariffs on all Chinese imports, it is time to assesses the consequences. Already, we have seen a contraction in US-China trade of 20% in the first three months of 2019 compared with the same quarter last year, and also compared with the average outturn for the whole of 2018. This contraction was worse than that which followed the Lehman crisis.

In assessing the extent of the impact of Trump’s tariffs on the US economy, we must take into account a number of inter-related factors. Clearly, higher prices to US consumers will hit Chinese imports, which explains why they have dropped 20% so far, and why they will likely drop even more. Interestingly, US exports to China fell by the same percentage, though they are about one quarter of China’s exports to the US.

These inter-related factors are, but not limited to:

The effect of the new tariff increases on trade volumes

The effect on US consumer prices

The effect on US production costs of tariffs on imported Chinese components

The consequences of retaliatory action on US exports to China

The recessionary impact of all the above on GDP

The consequences for the US budget deficit, allowing for likely tariff income to the US Treasury.

These are only first-order effects in what becomes an iterative process, and will be accompanied and followed by:

Reassessment of business plans in the light of market information

A tendency for bank credit to contract as banks anticipate heightened lending risk

Liquidation of financial assets held by banks as collateral

Foreign liquidation of USD assets and deposits

The government’s borrowing requirement increasing unexpectedly

Bond yields rising to discount increasing price inflation

Banks facing increasing difficulties and the re-emergence of systemic risk.

We can expect two stages.

The first will be characterised by monetary expansion will little apparent effect on price inflation. Putting aside statistical manipulation of price indices, this is the current situation and has been since the Lehman crisis.

It will be followed by a second phase, following an acceleration of currency debasement. It will be characterised by increasing price inflation, and ultimately the collapse of purchasing power for unbacked fiat currencies.

The trade framework

The simple accounting identity at national level linking trade with changes in the quantity of money and credit is comprised of three factors: the budget deficit, the trade deficit, and changes in total savings. They are captured in the following equation:

In other words, a trade deficit is the net result of a shortfall in the combination of a savings surplus over industrial investment and the budget deficit. For a detailed explanation as to why this is so, see Trade wars – a catalyst for economic crisis. The equation tells us that it is the expansion of money and credit which gives rise to trade imbalances, which is why when there is no change in the savings rate and in the absence of other factors the twin deficits arise. Otherwise, monetary inflation would lead directly into price inflation, the effect in a closed economic system.

Mainstream economists often disagree with this point, having discarded Say’s law. Say’s law explains the division of labour. It maintains that we specialise in our own production to buy all the other things we require and desire, and money is just the intermediation between our production, consumption and deferred consumption (savings). It was the iron rule of pre-Keynesian classical economic theory and allowed no latitude for state-issued money that was inflated into the system. Keynes had to disprove it (he did not – his definition was deliberately misleading) in order to develop his inflationist theories and create an economic role for intervening governments. It was this fundamental error of post-Keynesian economics that has led to successive economic crises, despite the ability of ordinary economic actors to adapt to government interference.

Understand this, and it follows that money and credit not earned through production can only lead to the importation of products from exogenous sources, or alternatively, fuel a rise in prices to reflect the increased quantity of money circulating between consumers and domestic producers. Free trade, the ability to substitute lower-priced goods from abroad for domestic equivalents, reduces the price impact of monetary inflation. If it wasn’t for the availability of foreign substitutes, price inflation would be far higher, which is why tariffs on imported goods only serve to push up price inflation.

Unintended consequences

Obviously, being a tax on imports, tariffs benefit the Treasury’s finances; a fact which President Trump continually boasts about. To be precise, a 25% tariff on all Chinese imports in the remaining five months of the current fiscal year (based on the first quarter of 2019) can be expected to raise $45bn, which reduces the Office of Management’s budget deficit estimate of $1,092bn for fiscal 2019 to $1,047bn. The tax benefit is therefore relatively minor, and likely to be more than offset by the recessionary consequences of higher tariffs on government tax revenues and welfare costs. This article will go into more detail why this is so.

If for a moment we assume there will be a limited impact on consumer demand from increased tariffs, the effect on prices at the margin would be to drive them sharply higher for all consumer goods in the product categories where Chinese supply is a factor, with some spill-over into others. Price inflation would simply begin to escalate. But given the indebtedness of the average American consumer, the ability to pay higher prices is obviously restricted, suggesting that overall demand must suffer, not just for imported Chinese goods, but for domestically-produced goods as well. It is therefore likely there will be both an impact on price inflation and a fall in consumer demand.

Besides the effect on consumers, manufacturers relying on part-manufactured Chinese imports and processed commodities now face cost pressures from tariffs which they may or may not be able to pass on to consumers. The cost pressures on manufacturers are bound to lead to a reassessment of their business models. This will be communicated to their bankers as increased lending risk, and they in turn will almost certainly restrict credit availability. The credit cycle would then move rapidly into a contractionary phase as both businesses and their bankers take fright.

Anyone who has analysed post-war credit cycles will be familiar with these dynamics. We are probably not there yet, despite the warning shot from financial markets in the fourth quarter of 2018. For now, the initial softening of consumer demand has led to a general assumption that monetary policy will ease sufficiently to prevent little more than a mild recession, benefiting capital values. Government bond yields have eased, and arbitrage across bond markets has ensured investment grade corporate bond yields have declined as well. Since end-November when the central banks began to ease monetary policy, the effective yield on investment grade corporate bonds, reported by Bank of America Merrill Lynch, has fallen from 4.8% to 4%. This is hardly an assessment of increasing lending risk.

As well as bond markets, equity markets are also expecting monetary easing, instead of a gathering crisis, and have rallied along with bonds. Clearly, financial markets have not noted the seriousness of trade protectionism, having become complacent while trade restrictions have generally eased in recent decades. However, market historians will note that this brief recovery phase was also the pattern in stock markets between October 1929, when the Smoot-Hawley Tariff Act was passed by Congress, and April 1930, two months before President Hoover signed it into law. If the correlation with that period continues, equities could be in for a substantial fall (in 1929-32 it was 88% top to bottom).

In the Wall Street Crash, equities fell as collateral was liquidated into falling markets. Non-financial assets, such as property, similarly lost value and productive assets (plant, machinery etc.) failed to generate anticipated cash flows. This nightmare was famously described by Irving Fisher, and has continued to frighten economists ever since.

While debt was a problem in 1929, it was generally confined to corporate borrowers and speculators. Today’s context of Fisher’s nightmare is in record levels of government, corporate and consumer debt. The potential disruption from the unwinding of the credit cycle is therefore worse today. Trump’s trade protectionism so far is targeted at one country, unlike Smoot-Hawley which was across the board. At first glance, Smoot Hawley was more dangerous, but it is the lethal combination of tariffs and the end of the expansionary phase of the credit cycle which should concern us.

The credit cycle with its periodic crises is both a given and overdue. The addition of trade tariffs will act as a catalyst to make things worse. Inflation and unemployment will rise, and as unemployment rises, government welfare costs will too. Being mandated, it will be impossible for the US Government to reduce them without revising the law. We can only guess the effect on the borrowing requirement, but with the Office of Management’s forecast deficit for fiscal 2019 at $1,095bn, perhaps over $1,200bn might be closer to the mark. The full impact is likely to be felt in 2020, when it could top $1500bn.

The cost of borrowing will escalate

With government borrowing already escalating, the interest rate burden on the government will become a very public issue. The following chart becomes the baseline for the government’s future borrowing costs.

Interest costs are already running away, before the addition of two other factors; a more rapidly accelerating borrowing requirement (as discussed above) and higher interest rates. After an initial round of monetary easing, higher interest rates can be expected to arise from a combination of three further factors. The most obvious is the increased rate paid by a borrower placing ever-greater demands on the bond market as the recession deepens.

With a gathering US and therefore global slump developing, foreigners will also become sellers of dollars and US Treasuries, simply because they do not need and cannot afford to run substantial dollar balances and investments. A foreign corporation may not like its home currency compared with the mighty dollar, but when costs and losses at its operating base need covering it has no option but to sell its dollars. Foreigners selling dollars and US Treasuries put all the funding onus on US residents, in conditions which, thanks to tariffs, are leading to increasing prices.

The impact of rising price inflation is bound to lead to higher nominal interest rates. While domestic investors can be expected to buy US Treasuries at supressed yields while recessionary fears persist, their appetite for guaranteed losses will be strictly limited. Commentators who have foreseen this difficulty expect quantitative easing to be reintroduced to guarantee affordable funding for the government. The argument in favour of more QE accords with the likely monetary response to collapsing consumer demand. It resolvs both the capital needs of hard-pressed banks and government funding demands.

Therefore, ahead of the next credit crisis, QE is the logical planners solution to stabilising an economy. It worked in the wake of the Lehman crisis. The inflationists are ready to try it again. Attention is even being paid to modern monetary theorists, the ultimate inflationists, who argue that increased government spending, so long as it is not inflationary at the price level, is good for the economy. It is the inflation assumption that could unwind it all.

Inflation will become the most important issue

Inflation is a more complex issue than presented by modern monetary theorists and other post-Keynesians. The root of price inflation is found in a combination of monetary inflation and the public’s changing preferences for holding money. An increase in the money quantity can be neutralised by an increase in the public’s preference for holding money relative to goods. Equally, if the public rejects money as a medium of exchange entirely, whatever the quantity, its purchasing power will vanish.

Modern economists take the view that monetary inflation does not appear to be a problem, citing Japan’s relationship between monetary expansion and prices. It appears that monetary expansion has not led to expected price inflation in the US, but here there is an issue with the statistics under-recording the price effect. Very few economists pay attention to relative preferences between money and goods.

In a credit crisis, it should be obvious that these preferences will change. Foreigners will reduce their relative preferences for dollars and will be a source of dollar liquidation to be absorbed by domestic US financial and non-financial sectors. A lower dollar in terms of its purchasing power of commodities will be the consequence.

For US residents the situation is more complex. Initially, banks will try to reduce outstanding credit obligations to the private sector, leading to deflationary pressures. Lending for working capital will be curtailed, and cash will also be raised from asset sales. Instead, banks will be buyers of US Treasury bills and short-maturity Treasuries. The Fed will reduce interest rates to zero again, and possibly even introduce negative rates in an attempt to counter credit deflation and reduce the cost of the government’s funding.

As mentioned above, the government’s budget deficit will increase due to a combination of falling tax revenue and increasing welfare costs. Initially, funding the deficit will not be a problem because banks will be keen to avoid private sector credit risk. Furthermore, the Fed will want to reintroduce QE as part of a stimulus package. With an embarrassment of funding options, government spending will escalate even more, justified as a fiscal stimulus by the inflationists. The scene will then be set for a second stage, where the banks, underwritten by the Fed, start expanding credit again in favour of the government.

Unfortunately, a weakening dollar combined with trade protectionism is likely to push up consumer prices, despite falling demand. It is not only foreigners who are overweight in dollars, but domestic holders are as well, which will become an issue when the credit crisis threatens the banks. Despite the banks’ efforts to de-gear their lending to businesses and individuals, a systemic crisis in a fractional reserve system cannot be avoided. Whether it starts in America or elsewhere (such as in the fragile Eurosystem) is immaterial. The only solution for the authorities, of course, is to chuck yet more money at the problem. They will have no alternative to accelerating the debasement of the currency to protect the banks.

The budget deficit widens even further

A broken economy with a collapsing currency forces a government to increasingly rely on monetary inflation as its principal source of revenue. The gap between a government’s spending and tax revenues widens even further. This returns us to the accounting identity described towards the beginning of this article: in the absence of savings, a budget deficit leads to a trade deficit.

With the budget deficit widening, so will be the tendency for the trade deficit. But we are now in a world where politicians feel they have no option but to discourage imports with even more trade protectionism. It is easier to tell the public that nasty foreigners are profiting from their economic misery than admit the fault lies squarely on the shoulders of the government’s excess spending.

The consequences for other fiat currencies

With the dollar being the world’s reserve currency, rising dollar interest rates and price inflation will affect almost all the other fiat currencies. We can argue over the fundamentals for various currencies, but what truly matters is which foreign currencies everyone owns. It should be noted at the outset that Americans own very little foreign currency liquidity, their currency being the reserve currency, and also because the dollar’s recent strength has reflected liquid inward flows.

It will be foreigners liquidating their excess dollars who call the shots. It is a myth that foreigners are short of dollars, perpetuated by those who seem to think that foreign loan obligations need cover for repayment. They don’t, and many of them will not be repaid anyway. More pressing is the problem of contracting global trade, requiring lower dollar balances and the liquidation of portfolio assets which will be falling in price, reflecting the slump. Call it the “Great Unwinding”, reflecting decades of inward investment since the end of Bretton Woods.

The combination of trade protectionism and the turning of the credit cycle threatens to result in an economic slump of severe proportions. The experience of Smoot-Hawley in the 1930s was that America’s trade protectionism rapidly led to a worldwide depression. Since the dollar was on a gold standard, commodity and food prices fell heavily. This time, with no gold backing, it will be currencies that lose purchasing power, at least to the extent they neutralise contracting demand, that being de facto monetary policy already. Therefore, there could be for a short time the appearance of price stability in other currencies, giving central banks the leeway to maintain their price inflation targets.

This will simply encourage central banks to run the loosest possible monetary policies, hoping for a controlled devaluation to stimulate demand. For a time, the only evidence of the true effect of these policies will not be rising commodity prices, but a rising gold price. Gold will be reflecting what is truly happening to prices while the balancing act between falling demand and fiat devaluation plays out.

The monetary planners will give themselves firepower to manage currencies through enhanced swap arrangements, and whatever other means they cook up. But it will always be inflationary. Consequently, they will lose control over prices, and will resort to other more direct means, such as price controls. It always happens that way, and they only hasten the end.

via ZeroHedge News http://bit.ly/2W9GBlk Tyler Durden

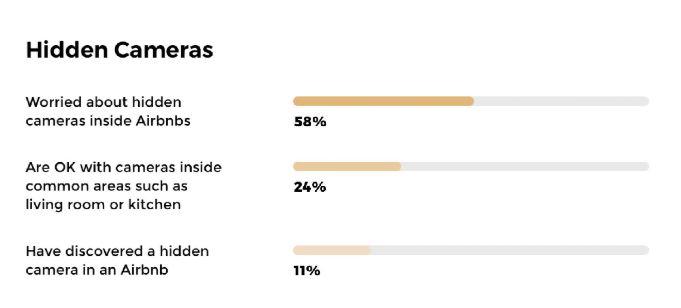

As we have documented in the past, Airbnb – which is hoping to become one of the next hot Silicon Valley startups to IPO later this year – has a hidden camera problem.

While the company’s rules allow hosts to place cameras outdoors, in living rooms or in common areas, bathrooms and bedrooms are considered off limits. But that hasn’t stopped some hosts – motivated either by perversion or an intense paranoia – from going ahead and placing cameras there anyway.

Though the company has said it’s working to address the issue, one recent survey suggests that it might be more widespread than previously believed.

IPX surveyed 2,023 Americans about their views and opinions on Airbnb, and discovered that a staggering 11% of them reported having discovered undisclosed hidden cameras in their rentals.

That’s a huge problem, because nearly 60% of Airbnb users say they’re worried about hidden cameras.

Hopefully the company can find some way to reassure customers and investors that it has the tools for addressing this problem – or it could create huge problems down the road.

via ZeroHedge News http://bit.ly/2JpDBvj Tyler Durden

Whether it is blowing up the Hanoi Summit with a memo, embarrassing the US abroad by backing a Venezuelan coup which fizzled out or getting American forces into a potential war with Iran based solely on non-specific Israeli intelligence the National Security Advisor has shown himself to be unable to help President Donald Trump deliver on campaign promises but adept at creating a mess. Since assuming his position in April 2018, Bolton has dragged Trump, who ran on a platform of non-intervention and a re-haul of American foreign policy strategies, into a myriad of problems that have caused him to contradict his own agenda. This is the result of extreme incompetence if not outright sabotage.

With Trump reportedly growing frustrated with Bolton, a new candidate for the job should be suggested. The President ought to consider retired Army Colonel Douglas Macgregor.

Macgregor has an anti-establishment flair that causes him not to get along with the bureaucratic class who Trump popularly clashed with in the 2016 US Presidential election. He was the squadron operations officer responsible for directing US troops on the ground in the legendary Battle of 73 Easting during the Gulf War where American armored vehicles defeated a much Iraqi detachment. But his dislike for gamesmanship and blunt demeanor meant that Macgregor did not thrive in the military despite his ability to innovate on the battlefield. A perfect match for Trump, who prefers officials that are not liked by the herd.

“Make Donald Trump Great Again” is Macgregor’s mantra. It is much needed in an administration where the President often seems to be the only one who still champions foreign policy objectives like the border wall that originally caught the attention of his base. While Bolton lives eternally in the Cold War, Macgregor’s focus is on the problems afflicting a United States that is struggling without grace to find its place in the modern world. He rightly calls out Bolton’s insistence on an “all or nothing” approach to negotiations with North Korea that have prevented a peace deal and rages about constant attempts by Washington insiders to induce Trump to backtrack on policy announcements that him look weak and self-contradictory in the process.

The strategy pursued by Bolton and his contemporaries seeks to return the United States to the unipolar era of the 1990’s when America’s dominance was secured by a ruined Russia and a still-developing China. They have not learned from the lessons of the USSR, which collapsed because it was simply unable to keep up with the expenses of running a global empire that an economically dominant United States could once handle.

America’s shifting role in the world is very much on the mind of Macgregor. It is reflected in his skepticism of NATO, his calls for reform of the military and his criticism of America’s wars that drag on for years but no longer result in victories. His distaste for foreign wars that sap a nation’s global power and do not meaningfully help America achieve its foreign policy objectives is a refreshing change from the hawkish behavior of Bolton, who is currently drawing the United States dangerously close to a conflict with Iran. Macgregor compares Bolton to Don Gaspar de Guzmán, the advisor to Spain’s King Philip IV who crashed the debt-ridden Spanish empire by engaging it in sporadic and unhelpful foreign interventions. Philip IV is notorious for this failure while Guzmán is now long forgotten. If Trump does not release Bolton soon his legacy will likely suffer the same fate.

America cannot afford the foolish council of those who are unable or unwilling to see the crisis that the country currently sits in. Take a chance on someone who goes against the grain.

via ZeroHedge News http://bit.ly/2JN7k0C Tyler Durden

{kind=link}

{kind=link}

{kind=link}