The Islamic Republic of Iran is looking for new ways to link their capital, Tehran, with Syria’s Damascus and Iraq’s Baghdad. One of the proposed actions they are taking to make this a reality is the construction of new highways and rail systems that would link Syria with Iran via Iraq.

Iran’s Vice President Eshaq Jahangiri in statements this week underlined his country’s determination to build new roads and railways in order to link the Persian Gulf states to Syria and the Mediterranean region.

Image via AMN News.

“Iran which understands the political and economic conditions and developments believes that the necessary capacities for cooperation in transferring power and electricity, building roads and etc. will be provided and we hope that obstacles will be removed through the presence of the private sector,” Jahangiri said, addressing the joint Iran-Iraq economic-trade forum in Tehran on Sunday.

He noted that building the Shalamcheh-Basra railway was one of the agreements made during the recent visit by the Iraqi delegation to Iran.

Jahangiri stressed the importance of developing a cross border highway between the two countries in order to boost trade and commerce, while also protecting their interests in the region.

“We will connect the Persian Gulf from Iraq to Syria and Mediterranean via railway and road,” Jahangiri said.

The Shalamcheh-Basra railway project is said to cost around 2.22 billion rials and once implemented, it will link the Iranian railway to Syria through Iraq.

For years since the start of the war in Syria, analysts have speculated what the so-called “Shia land bridge” or Iran-Iraq-Syria corridor to the Mediterranean would look like:

Director General of the Railway and Technical Structures Department at the Islamic Republic of Iran Railways (RAI) Mohammad Moussavi said in December that Iran was to build a movable railway bridge over the Arvand River as part of the 35-kilometer Shalamcheh-Basra railway project for linking Iran-Iraq railway network.

In addition to their railway and highway projects, Iran is also rumored to be planning to build a naval base in Syria’s western coast.

While this is still rumor, the idea that Iran could have access to the Mediterranean could trigger more airstrikes from Israel.

via ZeroHedge News http://bit.ly/2WV3Kom Tyler Durden

Actress Helen Mirren has had enough of Netflis, and she’s letting the world know.

The actress, who is most famous for roles in in “The Queen” and “Gosford Park,” recently said on stage in Las Vegas: “I love Netflix, but fuck Netflix. There’s nothing like sitting in a cinema.” She recently spoke at an event to promote her new film “The Good Liar” at the CinemaCon conference. She was looking to rile up a relatively friendly crowd of theater owners who attend the conference.

After Netflix’s “Roma” nearly won an Academy Award for best picture, the company has been in the crosshairs of industry traditionalists, who believe it undermines the industry’s longstanding practices. “Roma” was the first nominee that was a digital release. If it had won, Netflix would have been the first tech company to win the award.

The controversy stems from movies being put out on Netflix being considered for awards without traditional theater runs.

Mirren isn’t the first to speak out on the issue, either. Steven Spielberg has claimed that streaming movies shouldn’t be considered for Oscars unless they are shown in theaters.

“Steven feels strongly about the difference between the streaming and theatrical situation,” a spokesperson from Amblin, Spielberg’s production company, told IndieWire earlier this month. Spielberg helps set policy for the organization as one of the three Academy governors of the directors branch.

And what would any stupid and meaningless controversy be without the government’s involvement?

The DOJ weighed in to warn the Academy that if rule changes hurt Netflix, they may violate anti-competition laws. According to Bloomberg, Makan Delrahim, head of the agency’s antitrust division, sent a letter to Academy Chief Executive Officer Dawn Hudson on March 21, expressing concern about the way new award rules might be written.

via ZeroHedge News http://bit.ly/2Kkxfi0 Tyler Durden

This year marks the 70th anniversary of the founding of NATO, but the question is, is this a happy birthday for a lively meaningful organization or time for us to pull the plug on a Cold War dreg that has lived well past its purpose?

After WWII it was inevitable that there would be a conflict between the Liberal Capitalist world and the growing Red Communist one. Perhaps if the Soviet Union would have resigned itself to being the only Communist nation rejecting any form of proselytization and rebranding itself as some kind of Democracy B as a mild alternative to the West’s Democracy A then the Cold War could have been avoided.

But this did not happen and was very unlikely to do so. The motto of the Soviet Union on its seal was “Workers of the World Unite!”. That was workers of the “world” not “only Russia”. So it is not surprising that the West took a preemptive move and formed NATO to gang up on the USSR.

However now the Soviet Union is dead and gone. NATO fulfilled its mission a little after turning 40. Sadly rather than phasing out and riding off into the sunset it had a midlife crisis, bought a Camaro and continued to not only exist but expand and bomb. But should it exist? Why is this organization still around at 70 years old posing as if we are still living in some sort of Cold War dynamic where if we don’t bomb Libya back to the stone age somehow Belgium and Greece will fall to evil ideologically different invaders.

NATO relies heavily on the idea that the weakest members benefit from being treated as “equals” in the security organization. Many tiny nations would be militarily helpless otherwise. At first this logic makes sense. Little nations need a boost to help them maintain a stable defense.

For example, the smaller nations who allied with Nazi Germany in/before WWII avoided their Deutsch wrath via submission. By NATO logic they were made vastly “stronger” by being part of the Axis/Tripartite Pact. The Nazis did have arguably the best military in the world at that time which would bump up weaker allies for sure. But in turn could weak Bulgaria and Romania really make any demands from Germany? Could Germany get their allies to do what the Reich wanted?

Weak members of an alliance are never equal members with a voice, they are merely submissive states who fear the whip of their masters who are more benevolent than some other potential master, and this is what we see in many NATO members today who have absolutely neither an economy nor military of any worth to offer allies.

Interestingly, NATO seems to acknowledge that some people might be baffled as to why it continues to exist and by making a video about the very topic they somewhat subconsciously confirm the doubters’ beliefs.

So NATO in its own PR declares that its current missions, which are too big for any one nation to handle, are the following…

Protect against an “assertive” Russia.

Deal with the “deteriorated” security situation in Africa and the Middle-East which cause migration and terror attacks.

Promoting “international efforts” (whatever that means) to project stability and strengthen security outside of NATO territory.

Dealing with WMD’s, Cyber Attacks, and threats to Energy Supplies and deal with Environmental Challenges with “security implications”.

So let’s evaluate these points to see if NATO should shoot for for an 80th birthday and beyond.

Protecting Against an Assertive Russia

During the 90’s Russia would have been willing to join NATO. Russia is very powerful but still a distant third on the world stage. Furthermore, in a world of mutually assured destruction, Russia is only capable of maybe retaking lost friendly territory that those in power in America cannot find on a map or helping foreign nations help themselves win wars like they did in Syria.

Russia as it is today is not very assertive and always plays a reactive role to the West. An assertive Russia would have taken the majority of the Ukraine which it considers to be an inherent and ancient part of Russia itself. Only being able to take the Crimea reveals that Russia still has far to go before becoming a “threat” to Europe again. In terms of the grand chessboard of the former USSR, Russia is usually spending its turns escaping from being in check.

The Deteriorated Security Situation in Africa and the Middle-East

This has been caused by NATO itself committing regime changes in stable nations. If NATO had disbanded in 1991 the security situation in these regions would be exponentially better.

Promoting International Efforts” to Project Stability and Strengthen Security Outside of NATO Territory.

Projecting Stability is just coded language for terrifying others into submission. This is a normal part of human history and NATO like all militaries should do this, however they should be more honest about it. If one is to act like the Romans or Mongols and put the fear of God into their enemies with the threat of war then they could at least do so boldly.

The key words here that raise eyebrows are “outside of NATO territory”. Meaning that an organization founded for the “defense” of its members must by its own officially stated objectives work outside of its own territory proving that their mission is not defense but a form of preemptive offense.

Dealing with WMD’s, Cyber Attacks, Threats to Energy Supplies and Environmental Challenges with “Security Implications”.

Every powerful military has WMD’s. If they mean getting them out of the hands of Non-State actors then NATO should try to not allow any of its members to sell weapons to non-member entities. Why does defense against cyber attacks require NATO? Threats to energy supplies is coded language for wars for oil. Dealing with the environment militarily is just stupid but it sounds trendy and caring, so why not?

As you can see none of the official arguments for the continued existence of NATO is particularly convincing. By their own logic NATO exists to deal with the problems it causes by itself, fight against an assertive enemy that backs down from fighting it, terrify foreigners outside its borders into submission as a form of collective defense and deal with vague issues and security threats to the environment vaguely.

These arguments are not convincing to anyone, and probably not even to the member states of NATO themselves. As we blow out the 70 candles on the NATO cake everyone knows that this organization is a farce living on via historical inertia alone. The only real purpose it has is to keep much of Europe under the Washington yoke which means that in all likelihood it will outlive us all. Happy Birthday!

via ZeroHedge News http://bit.ly/2KidJTj Tyler Durden

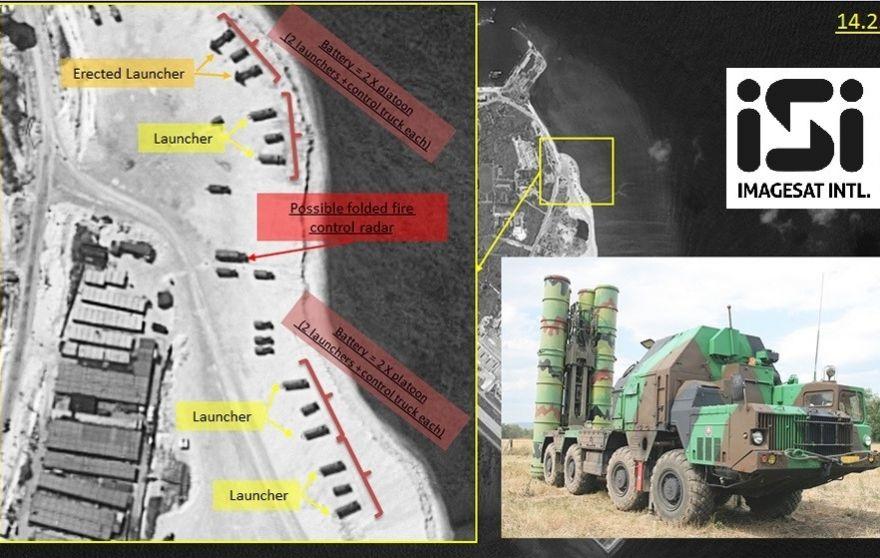

Spotlight Zimbabwe has reported that China is preparing to station elite special forces in Zimbabwe, as Beijing increases military cooperation with Harare, amid concerns that the Asian powerhouse is set to construct a secret underground military base in the country.

The new report comes one year after Spotlight Zimbabwe revealed that China installed next-generation surface-to-air missiles (SAM) in the country, the same ones that are deployed to the South China Sea on Woody Island.

China’s new military base is set to protect its large diamond claims and gold mines across the country, where some of its SAM launchers are already located.

According to a former minister of ex-leader President Robert Mugabe’s administration, China has been planning on sending their special forces to the country since 2014 “to offer technical assistance and support” to the Zimbabwe National Army (ZNA). However, Mugabe called off the plan several years ago, after accusing the Chinese of corruption, and the plunder of natural resources in Marange.

“They (China) have been itching to set a permanent military presence in this country, to protect their vast economic interests here but Mugabe was resisting the overtures,” said the former cabinet minister. “Although the cover argument was around offering technical assistance and support to our armed forces, it later became clear that Mnangagwa had his own agreement and arrangements with China. This infuriated Mugabe, and it was also during the same period Mnangagwa had first traveled to China as vice president, holding high-level meetings which his boss had not fully been briefed on. The incident increased Mugabe’s political mistrust for Mnangagwa, whom he suspected was presenting himself to President Xi Jinping, as the best political actor to secure China’s investments in Zimbabwe after he steps down. The rest is history. Mnangagwa has since invited China back to mine diamonds in Marange, and their special force has received the greenlight from vice president Rtd General, Constatino Chiwenga, to find a station in the country. Now there is every reason to believe that Mugabe’s November 2017 ouster, could have been a result of China viewing his stay in power as a threat to their economic investments, especially after having stripped them of diamond mining rights.”

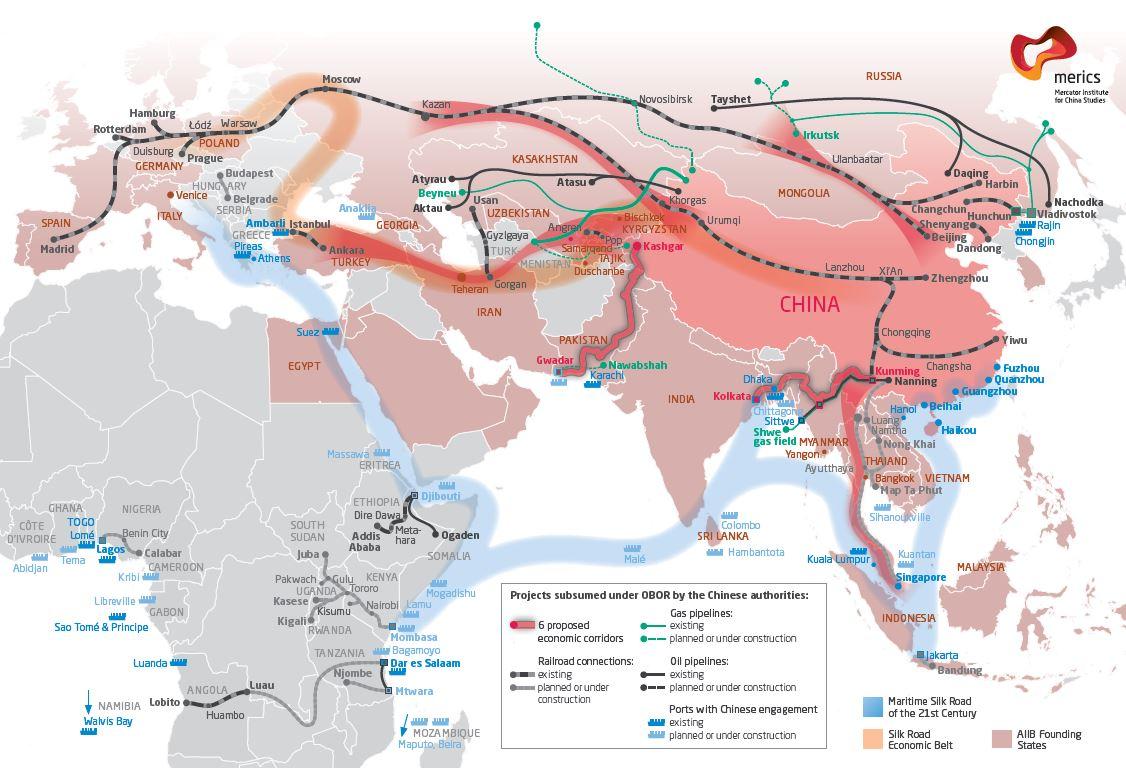

Zimbabwe has seen billions of dollars of Chinese investments over the last few years, mainly in critical economic sectors of mining, agriculture, and telecommunications. The investments are part of the Belt and Road Initiative (BRI), an ambitious effort to improve regional economies on a trans-continental scale. It aims to strengthen infrastructure, trade, and investment between China and 65 other countries that collectively account for 30% of global Gross Domestic Product (GDP), 62% of world population and 75% of known global energy reserves.

President Emmerson Mnangagwa said last month that BRI is a significant improvement of the old Silk Road.

“In the past, there was the Silk Road, and that to a greater extent did not embrace the entire continent. Zimbabwe was only lucky to the extent that 800 to 1000 years ago there was trade between the Munhumutapa Kingdom and China when we imported porcelain and silk from here and in turn you got our ivory.

“But today the Road and Belt Initiative has taken everybody on board so that our economies can talk to each other, so that our economies can help each other modernize and mechanize. We are getting connected and benefiting from each other.

“If you look at the current FOCAC meeting, there are 10 issues that we are going to deal with and these issues are really primary issues that show developing countries like Zimbabwe.

“The issue of transportation, the issue of infrastructure development in our countries . . . we believe that with this relationship under FOCAC where the rest of Africa is making conversations with China, and China helping Zimbabwe and Africa to go up. And when that happens it creates the integration of marketing in China and Africa so we are happy that we are part of this global vision,” he said.

China has indicated that it will invest in Africa with the Agenda 2063 of the African Union, the 2030 Agenda for Sustainable Development of the United Nations, as well as the development strategies of individual African countries.

However, in Zimbabwe’s case, Chinese BRI investments have been followed by a permanent military presence. Now, allegedly, a secret underground military base for special forces is set to be constructed, a move that will certainly anger Washington.

via ZeroHedge News http://bit.ly/2VwBXKz Tyler Durden

America’s designation of the Iranian Revolutionary Guard Corps (IRGC) as a terrorist group is an example of taking a good idea — sanctioning Iranian entities for malign behavior — one step too far.

A former State Department counterterrorism official said of the designation, “The future ramifications of this decision will be profound.” He’s right about that, but “profound” may cut both ways.

In 2007, the U.S. designated the Guard’s overseas operations arm, the Quds Force, for support of terrorist organizations, so the new sanctions will hit the parent organization which is already under sanctions for ballistic missile development and supporting the Bashar Assad regime in Syria.

An Iranian lawmaker responded to the news by saying Iran would regard the U.S. military as no different than the Islamic State, echoing the 2017 statement by the commander of the Guards, Major General Mohammad Ali Jafari, that the Guards would “consider the American army to be like Islamic State all around the world.”

The Department of Defense (DOD) and the CIA reportedly opposed the move, and no wonder: Officials at the National Security Council and the Treasury Department are safe in Washington, D.C., State Department officers in Baghdad labor under restrictive security rules which limit their movements, which leaves the U.S. military and CIA officers exposed.

DOD has opposed this idea for a long time. When it was considered in 2007, the representative of the Joint Chiefs of Staff told his civilian counterparts, “The United States has always carefully avoided declaring military officers engaged in activities sanctioned by their governments as terrorists to avoid the same being done to us.” It could be applied to American special forces officers, who frequently operate clandestinely and have provided military assistance and training to insurgents.

Encounters between the American and Iranian military and security services can go one of three ways:

Proxy war: Iraqi militias supported by Iran killed at least 608 American servicemen.

Let’s-get-this-over-with: Iran quickly released the U.S. Navy crews who were captured by the IRGC Navy when they wandered into Iranian waters in early 2016.

The Beirut option: In the 1980s, the CIA’s Beirut station chief William Buckley and U.S. Marine colonel William Higgins were kidnapped by Iran’s Lebanese Hezbollah allies and died under interrogation. Former FBI agent – and CIA contractor – Robert Levinson disappeared in Iran in 2007, and the FBI, then led by Robert Mueller, was reduced to asking Vladimir Putin’s most loyal oligarch, Oleg Deripaska, to fund his (unsuccessful) rescue.

And the designation won’t just discomfit Americans; Iraqi officials regularly encounter Guards officers whether they want to or not. Quds Force commander Qasem Soleimani regularly visits Iraq, and the last three Iranian ambassadors to Baghdad have been Quds Force officers, so Iraqi officials can expect to be put on notice by the Americans to avoid “terrorists.” Iran is active economically in Iraq, so the designation may be bad for Iraq’s economy. One near-term effect may be to scuttle an effort to import electricity from Iran, badly needed as the country still suffers from power shortages.

America’s timing is bad, as Iran’s “resistance economy” is dragging, and the government has been criticized for its lackluster response to the recent widespread, deadly flooding. These sanctions will just give the mullahs an excuse for their economic mismanagement.

Given the Guard’s penetration of Iran’s economy, new sanctions might enrich it even more. If the economy becomes radioactive to outside investors because the due diligence is too hard, the IRGC could buy the remaining assets at cut-rate prices. If, in the future, the Guard is neutered and sanctions are relaxed, unwinding the sanctioned businesses will take years and will require the approval of the U.S., which will move at the speed of government. This will hobble the post-mullah regime which will be under pressure to improve the lives of newly-free Iranians.

The current U.S. practice of targeting specific people and economic entities for sanctions allows the U.S. to fine-tune its actions and tells the Iranians the U.S. knows who is doing what. Given the Guards economic ubiquity, the terrorist designation is a blanket sanction with unknown consequences, though one might be increased power for the Guards.

The last time a military formation of a sovereign state was declared a criminal organization was when Nazi Germany’s Waffen-SS was condemned for its involvement in war crimes and crimes against humanity. Designating the IRGC a terrorist entity may sound great after that third beer, but is IRGC commander Major General Jafari as bad as Himmler? No.

Terrorism sanctions on Iran’s Revolutionary Guards promise something for everyone, all of it bad: More American hostages, and more money for the Guards. The Americans should ignore the bright, shiny object of terrorism sanctions and remember firm, consistent pressure is the way to win the contest with Iran.

via ZeroHedge News http://bit.ly/2D4FVTL Tyler Durden

About a 60-minute drive northeast of Washington D.C., the city of Baltimore is on the verge of collapse.

Thousands of people are fleeing the city each year as total population plummets to 100-year lows. There are about 46,000 vacant rowhomes scattered throughout the area, or roughly 15% of the housing stock is dormant. On a per capita basis, the city has the highest rate of homicides per 100,000 in the country. Opioids from Johns Hopkins and the University of Maryland Medical Center continue to flood the poorest of neighborhoods, leaving the African American communities in a perpetual state of addiction, along with the need for constant government assistance programs. With the local economy basically a black market, gangs roam the streets like a third world country.

The outlook for Baltimore is rather bleak. We have covered the great implosion of Baltimore over the years. The accelerated deterioration restarted after 2015 Baltimore riots. Ever since, the slope of decline has been far steeper than ever seen before.

There is new evidence that verifies our coverage on Baltimore, and we must say – the report doesn’t give hope that a turn around in the city is happening anytime soon.

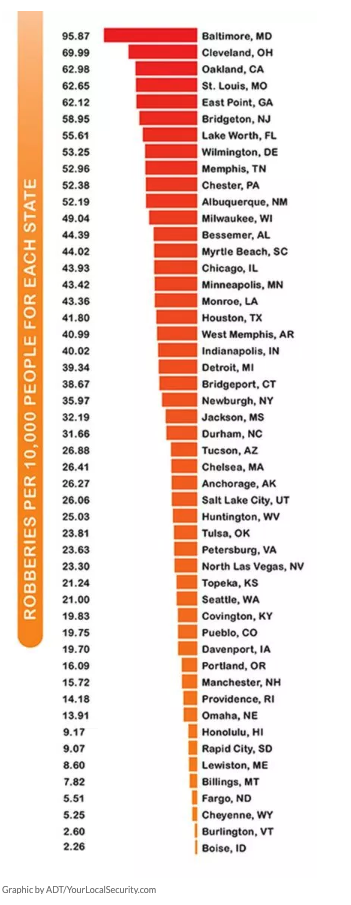

Baltimore had the most significant number of robberies per capita – 95.87 for every 10,000 people.

ADT’s analytic analysts “looked at the FBI’s annual crime data [for 2017] for robbery rates to discover which city in each state experienced the most robberies.”

While robberies worsened in Baltimore, they declined nationwide, dropping by 28% between 2008 and 2017.

Some of the safest streets in America are in Boise, Idaho where 2.26 people are robbed per 10,000 people.

Here’s the rest of the most dangerous cities:

Cleveland, Ohio

Oakland, California

St. Louis, Missouri

East Point, Georgia

Wilmington, Delaware ranks no. 8, Chester, Pa. is no. 10.

via ZeroHedge News http://bit.ly/2FZe1cd Tyler Durden

Libya has been in a state of the constant chaos since the NATO intervention in 2011. After the fall of the government of Muammar Gaddafi, the country fell into the hands of warrying armed factions, many of which were linked to radical Islamist groups. Al-Qaeda and then ISIS strengthened and expanded their presence in the country. The erupted humanitarian crisis has never been fully overcome. A high level of violence, crime and unsolved humanitarian issues turned Libya in one of the key hubs of arms, drugs and even trafficking. A large number of the refugees moving to Europe uses Libya as a transfer point.

NATO contributed very little efforts to change this situation, defeat terrorism and restore the order. One of the reasons is that the Western-backed Government of National Accord (GNA), based in Tripoli, is itself largely linked to radicals. Groups that declared their support to the GNA control a part of northwestern Libya. The only real anti-terror effort undertaken by pro-GNA forces and their foreign backers took place in 2016, when they moved to chuck ISIS out of the coastal city of Sirte. Despite this, ISIS cells kept a notable presence in the county. The GNA receives support from the US, various EU states, Qatar and Turkey.

The southwestern part of the country is controlled by local Tuareg and Tabu militias. Central, northeastern and southeastern Libya is in the hands of the Libyan National Army (LNA) and the allied to it House of Representatives based in the city of Torbuk.

Over the past few years, the LNA under the leadership of Field Marshal Khalifa Haftar has consolidated control over a major part of the country, sometimes by forming pacts and alliances with local communities like in the south and sometimes by defeating radical militant groups by force. The LNA has also carried out a successful operation against militant and criminal groups in southern Libya. This effort was officially coordinated with the governments of Niger and Chad. Egypt, the UAE and France are often mentioned as the LNA backers. An interesting fact is that wilde media speculations about Russian mercenaries, Special Forces and, if we take into account the British mainstream media, even military bases allegedly deployed and created to support the LNA are barely linked with the reality on the ground. The real Kremlin involvement in the conflict has so far been mostly limited to diplomatic contacts with representatives of at least formally constructive local forces.

On April 4, Field Marshal Haftar officially announced a start of counter-terrorism operation in the area of Tripoli. In the following days, the LNA has made a series of advances capturing large areas south of the city, including Tripoli International Airport, and reached the vicinity of the city. According to local sources, over 40 people were killed or injured in clashes between the LNA and pro-GNA forces. The sides even employed their existing air forces in order to deliver strikes each against other.

However, a coalition of pro-GNA forces, which includes the al-Nuasi Brigade, the Tripoli Revolutionaries Brigade, the Special Deterrence Force, the al-Mahjub Brigade, the 33rd Infantry Brigade, the Abu Obeida al-Zawia Forces, the al-Halbus Brigade and the Usama al-Juwayli Forces, appeared to be able showing some resistance to the LNA only when Haftar-led forces reached the city’s vicinity.

On April 7, the U.S. Army Africa Command (AFRICOM) announced that it had evacuated its troops from the Libyan capital “in response to the evolving security situation” there. This means that Washington expects clashes in the city itself.

The LNA claims that its move to capture Tripoli is not a part of political struggle, but an operation against terrorists who are hiding there. Nonetheless, it’s clear that the LNA advance is another move made in the framework of the previous LNA attempts to put an end to the division of the country into feods controlled by local warlords and to consolidate the governmental power, including the right of use of force, in one hands. In the event of success, it will allow to restore a kind of order in the major part of he country and to crack down on local militant and criminal armed groups that operate freely in the existing power vacuum.

On the other hand, the LNA advance faced a wide criticism on the international level. Foreign powers use the collapse of Libya to exploit its territory and energy resources in own favor are opposing the LNA actions under the banner of the need to defend democracy and prevent humanitarian crisis.

In the event of their success the humanitarian and security situation in Libya will likely continue to deteriorate creating a room for the further expansion of radical groups, first of all ISIS and al-Qaeda, in and contributing to the continuing flow of migrants to Europe.

via ZeroHedge News http://bit.ly/2D6GA6X Tyler Durden

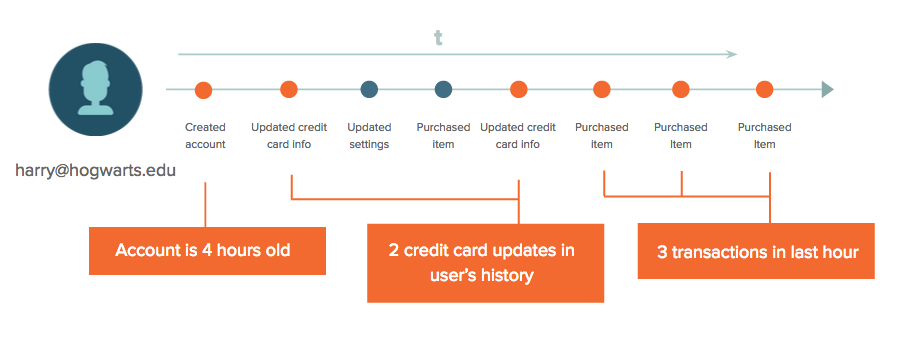

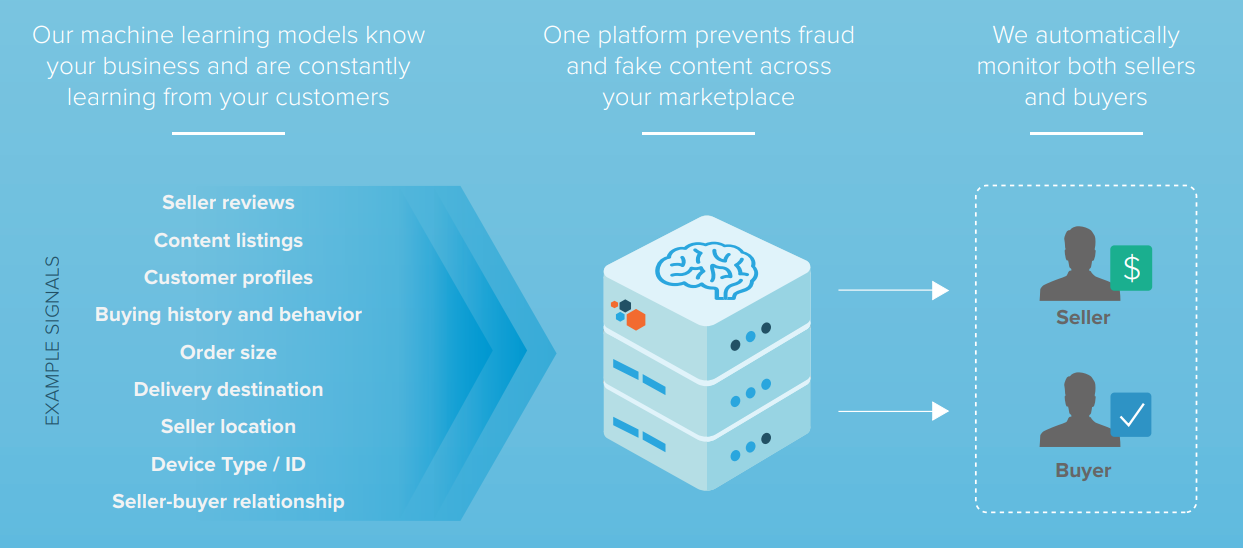

Nearly everything we buy, how we buy, and where we’re buying from is secretly fed into AI-powered verification services that help companies guard against credit-card and other forms of fraud, according to the Wall Street Journal.

More than 16,000 signals are analyzed by a service called Sift, which generates a “Sift score” ranging from 1 – 100. The score is used to flag devices, credit cards and accounts that a vendor may want to block based on a person or entity’s overall “trustworthiness” score, according to a company spokeswoman.

From the Sift website: “Each time we get an event — be it a page view or an API event — we extract features related to those events and compute the Sift Score. These features are then weighed based on fraud we’ve seen both on your site and within our global network, and determine a user’s Score. There are features that can negatively impact a Score as well as ones which have a positive impact.”

The system is similar to a credit score – except there’s no way to find out your own Sift score.

Factors which contribute to one’s Sift score (per the WSJ):

• Is the account new?

• Are there are a lot of digits at the end of an email address?

• Is the transaction coming from an IP address that’s unusual for your account?

• Is the transaction coming from a region where there are a lot of hackers, such as China, Russia or Eastern Europe?

• Is the transaction coming from an anonymization network?

• Is the transaction happening at an odd time of day?

• Has the credit card being used had chargebacks associated with it?

• Is the browser different from what you typically use?

• Is the device different from what you typically use?

• Is the cadence of the way you typed out your password typical for you? (tracked by some advanced systems)

Sources: Sift, SecureAuth, Patreon

The system is used by companies such as Airbnb, OpenTable, Instacart and LinkedIn.

Companies that use services like this often mention it in their privacy policies—see Airbnb’s here—but how many of us realize our account behaviors are being shared with companies we’ve never heard of, in the name of security? How much of the information one company shares with these fraud-detection services is used by other clients of that service? And why can’t we access any of this data ourselves, to update, correct or delete it?

According to Sift and competitors such as SecureAuth, which has a similar scoring system, this practice complies with regulations such as the European Union’s General Data Protection Regulation, which mandates that companies don’t store data that can be used to identify real human beings unless they give permission.

Unfortunately GDPR, which went into effect a year ago, has rules that are often vaguely worded, says Lisa Hawke, vice president of security and compliance at the legal tech startup Everlaw. All of this will have to get sorted out in court, she adds. –Wall Street Journal

In order to optimize scoring “Sift regularly evaluates the performance of our models and tries to minimize bias and variance in order to maximize accuracy,” according to a spokeswoman.

“While we don’t perform audits of our customers’ systems for bias, we enable the organizations that use our platform to have as much visibility as possible into the decision trees, models or data that were used to reach a decision,” according to SecureAuth Vice President and chief security architect Stephen Cox. “In some cases, we may not be fully aware of the means by which our services and products are being used within a customer’s environment.”

Not always right

While Sift and SecureAuth strive for accuracy, sometimes it’s difficult to decipher authentic purchasing behavior from fraud.

“Sometimes your best customers and your worst customers look the same,” said Jacqueline Hart, head of trust and safety at Patreon – a site used by artists and creators to allow benefactors to support them. “You can have someone come in and say I want to pledge $10,000 and they’re either a fraudster or an amazing patron of the arts,” Hart added.

If an account is rejected due to its Sift score, Patreon directs the benefactor to the company’s trust and safety team. “It’s an important way for us to find out if there are any false positives from the Sift score and reinstate the account if it shouldn’t have been flagged as high risk,” said Hart.

There are many potential tells that a transaction is fishy. “The amazing thing to me is when someone fails to log in effectively, you know it’s a real person,” says Ms. Hart. The bots log in perfectly every time. Email addresses with a lot of numbers at the end and brand new accounts are also more likely to be fraudulent, as are logins coming from anonymity networks such as Tor.

These services also learn from every transaction across their entire system, and compare data from multiple clients. For instance, if an account or mobile device has been associated with fraud at, say, Instacart, that could mark it as risky for another company, say Wayfair—even if the credit card being used seems legitimate, says a Sift spokeswoman. –Wall Street Journal

A person’s Sift score is constantly changing based on that user’s behavior, and any new information the system gathers about them, according to the spokeswoman. From Sift:

We learn in real-time, which means Scores are constantly being recalculated based on new knowledge of fraudulent users and patterns. For example, when someone logs in, we’ve found out a lot of information in the meantime about suspicious devices, IP addresses, shipping addresses, etc., based on the activity of other users. Add this to the fact that there may have been some new labeled users since their last login, and the scores can sometimes have a significant change. This is also more likely if the user hasn’t had much activity on your site. –Sift.com

While Sift judges whether or not one can be trusted, there’s no file with your name on it that it can produce for review – because it doesn’t need your name to analyze your behavior, according to the report – which seems like total BS.

“Our customers will send us events like ‘account created,’ ‘profile photo uploaded,’ ‘someone sent a message,’ ‘review written,’ ‘an item was added to shopping cart,” says Sift CEO Jason Tan.

It’s technically possible to make user data difficult or impossible to link to a real person. Apple and others say they take steps to prevent such “de-anonymizing.”Sift doesn’t use those techniques. And an individual’s name can be among the characteristics its customers share with it in order to determine the riskiness of a transaction.

In the gap between who is taking responsibility for user data—Sift or its clients—there appears to be ample room for the kind of slip-ups that could run afoul of privacy laws. Without an audit of such a system it’s impossible to know. Companies live under increasing threat of prosecution, but as just-released research on biases in Facebook ’s advertising algorithm suggest, even the most sophisticated operators don’t seem to be fully aware of how their systems are behaving. –Wall Street Journal

“I would argue that in our desire to protect privacy, we have to be careful, because are we going to make it impossible for the good guys to perform the necessary function of security?” asks Anshu Sharma – co-founder of Clearedin, a startup which helps companies avoid falling victim to email phishing attacks.

His solution? Transparency. When a company rejects a potential customer based on their Sift score, for example, it should explain why – even if that exposes how the scoring system works.

via ZeroHedge News http://bit.ly/2uWwktI Tyler Durden

Some students at George Mason University continue to put pressure on campus leaders to fire U.S. Supreme Court Justice Brett Kavanaugh from his new post as a visiting law professor.

Kavanaugh was hired in January by GMU’s Antonin Scalia Law School and is set to co-teach a class this summer called “Creation of the Constitution” in Runnymede, England, where the Magna Carta was sealed.

Despite the fact that Kavanaugh is teaching over 3,500 miles away from the Virginia campus, several students took to the podium at the Board of Visitors meeting last Wednesday to say they feel unsafe having Kavanaugh teach the class.

Exclusive video recorded by The College Fix shows several students, a few who say they are sexual assault survivors, address the campus leaders to tell them students’ mental health is threatened by the Kavanaugh hire.

“As a survivor of sexual assault this decision has really impacted me negatively,” one female student said.

“It is affecting my mental health knowing that an abuser will be part of our faculty.”

Another female student gave similar comments to the board:

“As someone who has survived sexual assault three times I do not feel comfortable with someone who has sexual assault allegations like walking on campus.”

A third female student told the board “we are fighting to eradicate sexual violence on this campus. But the hiring of Kavanaugh threatens the mental well being of all survivors on this campus.”

A fourth female student echoed similar sentiments, noting her sister is a sexual assault victim.

“I’ve seen what it does to a person,” she said. “I’ve seen what these cases can do to people.”

The comments were made during the meeting’s public comment section. The students represent a relatively new group on campus called “Mason 4 Survivors,” launched in recent months.

A student petition created by “Mason 4 Survivors” demands that the university “terminate AND void ALL contracts and affiliation with Brett Kavanaugh at George Mason University.” So far nearly 3,300 have signed it.

After the students spoke, Rector Tom Davis and GMU President Angel Cabrera said they were proud of the students and appreciated that they spoke up and acted as engaged citizens.

Later in the meeting, Cabrera suggested steps to continue to eradicate sexual assault on the campus, stating “one case of sexual assault is one too many.” The board agreed to learn more about sexual assault on campus and steps underway to combat the problem.

The next day, students continued their protest by marching around campus chanting “cancel Kavanaugh” and “take Kavanaugh off campus.” Some had blue tape over their mouths. The group delivered their petition to fire the Supreme Court justice to Merten Hall, an administration building.

The demonstrators also defaced a statue of George Mason, putting blue tape on his mouth and attaching anti-Kavanaugh signs to it, using it as a prop in their protest.

— Mason For Survivors GMU (@Mason4Survivors) April 4, 2019

We really out here doing the damn thing. Sharing my story has been so empowering and healing for me, I am so amazed by the support from students, faculty, and community members ❤️ #chacelkavanaughGMUpic.twitter.com/aF0gV0mEZ5

— Mason For Survivors GMU (@Mason4Survivors) April 4, 2019

University spokesman Michael Sandler told The College Fix“we allow students to dress up the statue, so this doesn’t violate any policies that I’m aware of.” He said the university “strongly supports freedom of expression and this would seem to fall into that category.”

As to Kavanaugh’s fate at George Mason University, some members of the Faculty Senate may believe they have the right to investigate Kavanaugh independently despite the U.S. Senate’s determination. They called for as much at their meeting last Wednesday.

But President Cabrera has stated that Justice Kavanaugh’s appointment was approved by the law school faculty in January and he stands behind that decision.

via ZeroHedge News http://bit.ly/2P0Hln0 Tyler Durden

In yet more confirmation that US sanctions don’t fundamentally punish or weaken regimes they seek to bring down, but hurt the common population America feigns to be helping, a new report finds that relief efforts in the wake historic floods which have created a disaster zone in Iran are being hindered due to Washington’s sanctions.

The Middle East’s main regional emergency response and humanitarian aid arm, the Red Crescent, says that US sanctions have prevented the bulk of badly needed external emergency relief from getting through after record rains have caused the worst floods in nearly a century in multiple provinces across Iran, killing at least 70 and displacing many tens of thousands.

The worst flooding in 70 years has hit Iran over the past 3 weeks, via the AP.

“No foreign cash help has been given to the Iranian Red Crescent society. With attention to the inhuman American sanctions, there is no way to send this cash assistance,” the Red Crescent said in a statement, cited by Reuters.

In all, international humanitarian groups say up to 90,000 have sought emergency shelter amid response efforts which are faltering due to lack of external help.

The floods began on March 19, and produced surreal scenes coming out of the country involving flash floods sweeping away cars and whole towns over the past three weeks.

Poldokhtar is among the cities hit hard, via Sky News

The US has acknowledged the crisis, with US Secretary of State Mike Pompeo pledging the US government was prepared to help through the Red Cross and Red Crescent.

However, in rhetoric that sounded similar to his tough talk on Venezuela amid ongoing economic and infrastructural collapse there, he blamed Iran’s woes on “mismanagement in urban planning and in emergency preparedness” due to the inept and corrupt leadership of Iran’s Ayatollah and other leading clergy.

Surreal scenes of entire towns being swept away by flash floods have come out of Iran over the past weeks.

The level of international attention to #Iran‘s unprecedented #floods is surprisingly low. People of Iran are in need of help and attention, regardless of international politics.

Will be on today’s @BBCNewshour at 20:30 (& 21:30) GMT, going over floods in Iran with @BBCTimFranks. pic.twitter.com/ffMIZZWehf

— Kaveh Madani | کاوه مدنی (@KavehMadani) April 2, 2019

But Iranian Foreign Minister Mohammad Javad Zarif in statements last week pointed the finger at Washington for imposing an economic blockade by seeking to prevent European and other international companies from doing business with Iran: “Blocked equipment includes relief choppers: This isn’t just economic warfare; it’s economic TERRORISM,” he said on Twitter.

.@realDonaldTrump ‘s “maximum pressure”—flouting UNSC Res 2231 & ICJ ruling—is impeding aid efforts by #IranianRedCrescent to all communities devastated by unprecedented floods. Blocked equipment includes relief choppers: This isn’t just economic warfare; it’s economic TERRORISM. pic.twitter.com/EEKTMiXLEi

Over the weekend sustained rains continued to unleash floods in the southwest of the country, and new evacuation efforts are underway for towns along the Iraq border, near rivers and dams already bulging under the strain.

Meanwhile the head of the Iranian Red Crescent Society, Ali Asghar Peyvandi, in fresh statements slammed the US for blocking the Society for Worldwide Interbank Financial Telecommunication (SWIFT).

Iran – Lorestan

The flood has reached the roof of the houses and destroys them in Pol-e Dokhtar in Khorramabad city . The Citizens don’t have any government assistance.

April 1,2019#IranFloodshttps://t.co/M4eumQ52I6pic.twitter.com/Jd5WvnAktX

Peyvandi said: “We used a number of bank accounts connected to SWIFT, which we used for receiving international aid. But at the moment these accounts are subject to sanctions.”

Six cities along the Karkheh River in southwestern Khuzestan province were ordered evacuated over the weekend. Image source: Tasnim News/AFP

“It’s impossible to transfer cash from other countries as well as the International Federation of [Red Cross and] Red Crescent Societies,” he added.

Thus far it’s unclear just how the US State Department plans to help, other than send funds through the Red Cross and Red Crescent organizations; however, that would ironically run the risk of violating Washington’s own sanctions against Tehran.

via ZeroHedge News http://bit.ly/2G9CBZb Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}