Two Years After Handing It The Biggest Ever Bailout Loan, IMF Finds Argentina Debt Levels Are “Unsustainable”

Back in the summer of 2018, when the IMF handed Argentina an unprecedented $56 billion bailout loan, the largest in IMF history, some warned that this is a case of deja vu similar to the 2001/2002 precedent when Argentina eventually defaulted on its foreign creditors, while humiliating the IMF which had signed off on Argentina’s economic policies that ended up in bankruptcy court. The IMF, however, was confident that this time would be different, and rushed – under now-ECB head Christine Lagarde – to hand to Argentina the greatest amount of money the IMF had ever disbursed to a struggling nation.

It turned out that this time wasn’t different, and after completing a week of meetings in Argentine, the IMF – which so generously handed out other people’s money to prop up the crumbling, corrupt Latin American nation less than two years aqo – finally threw in the towel and admitted that Argentina’s debt load is unsustainable, paving the way for the government to ask private bondholders to take on losses as it prepares to renegotiate its obligations.

The last time IMF officials commented on Argentina’s debt was in the fourth review of the credit line in July 2019, when they called it “sustainable, but not with a high probability.”

Oops. But it gets better.

A “meaningful contribution” will be necessary from private bondholders to restore the country’s debt sustainability, the IMF wrote in a statement Wednesday following talks with Argentine officials during its first technical mission in Buenos Aires under Alberto Fernandez’s presidency.

“The primary surplus that would be needed to reduce public debt and gross financing needs to levels consistent with manageable rollover risk and satisfactory potential growth is not economically nor politically feasible,” the Fund said, in what may be the most embarrassing moment in the Fund’s history.

Why embarrassing? Because as Hector Torres, a former executive director at the Fund who represented South American countries, said last summer, “The IMF has put a lot in — not just money, but prestige,” to avoid a default. “The fact that the arrangement is not performing well right now is an embarrassment,” he said. Little did he know just how embarrassing it would get.

As discussed previously, Fernandez is seeking to renegotiate billions of dollars in debt with private creditors, including the infamous $56 billion loan with the Washington-based organization.

Argentina’s record IMF loan has been on hold since August after Fernandez pulled off a shock upset of incumbent Mauricio Macri in a presidential primary vote, sending markets reeling.

“IMF staff emphasized the importance of continuing a collaborative process of engagement with private creditors to maximize their participation in the debt operation,” according to the statement. Meanwhile, Argentina’s economy has collapsed, the currency has plunged, bonds prices have been in freefall and debt rose to nearly 90% of GDP at the end of 2019, the Fund said.

But the biggest pain now await bondholders, some of whom were so dumb to actually buy 100 year bonds from Argentina. Guzman warned investors (or at least their replacement since those who made the original investment were surely summarily fired) last week they’ll probably be frustrated with negotiations, which he intends to wrap up by the end of March. South America’s second-largest nation owes over $38.7 billion to bondholders just this year, and payments peak in May. There is no way it can make those payments without magic.

Submitted by Micro Hive; authored by Dominique Dwor-Frecaut is a macro strategist based in Southern California. She has worked on EM and DMs at hedge funds, on the sell side, the NY Fed , the IMF and the World Bank. She publishes the blog Macro Sis that discusses the drivers of macro returns.

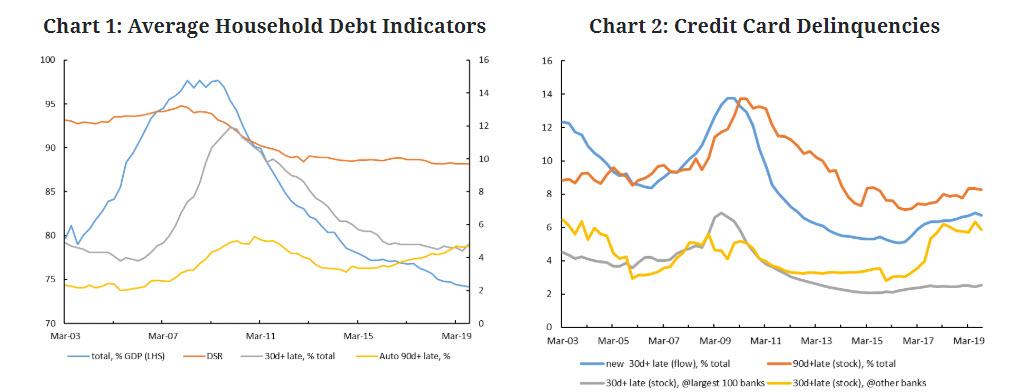

US credit scoring is facing a revamp. Fair Isaac (FICO) recently announced changes to consumer credit scoring that will raise the credit core of highly-rated borrowers and lower that of lower-rated consumers. While lenders have a choice of ratings methodologies and could take time to adopt the new FICO scoring, Fed surveys show a gradual, but steady, tightening of consumer loans standards is already underway. With household balance sheets starting to show signs of strain, this trend could have a negative and significant impact on consumption, the main, and already-slowing, engine of US growth.

Healthy consumer balance sheets are often cited as one of the strengths of the US economy. Average household leverage ratios look good: relative to the crisis peak, debt is down by more than 20 percentage points of GDP and continues to slide lower (chart 1). The debt service ratio is lower than before the crisis and default rates are back to their pre-crisis levels. The one–well known– exception to this positive picture, is auto loans, about 9% of total household debt, where delinquencies are nearly back to their crisis peak.

Yet, a detailed look at consumer finances shows cracks starting to appear. While average mortgage delinquencies are still falling, credit card delinquencies have been rising since 2016 (chart 2).

At small banks, accounting for about 20% of consumer lending, credit card delinquencies are now well above their crisis peak. In addition, Discover, the US largest independent credit card network, has seen a 10% decline in its stock price caused by investor concerns over its classification of compromised loans. The performance of Fintechs, small but fast growing, could also come under pressure. Fintechs offer mainly unsecured personal loans, the fastest growing segment of the consumer credit market, that are used largely to repay or consolidate other debts, especially credit card debt. Lastly, personal bankruptcy filings increased in 2019 for the first time since 2010. These weaknesses are puzzling in view of the decline in unemployment to a 50-year low.

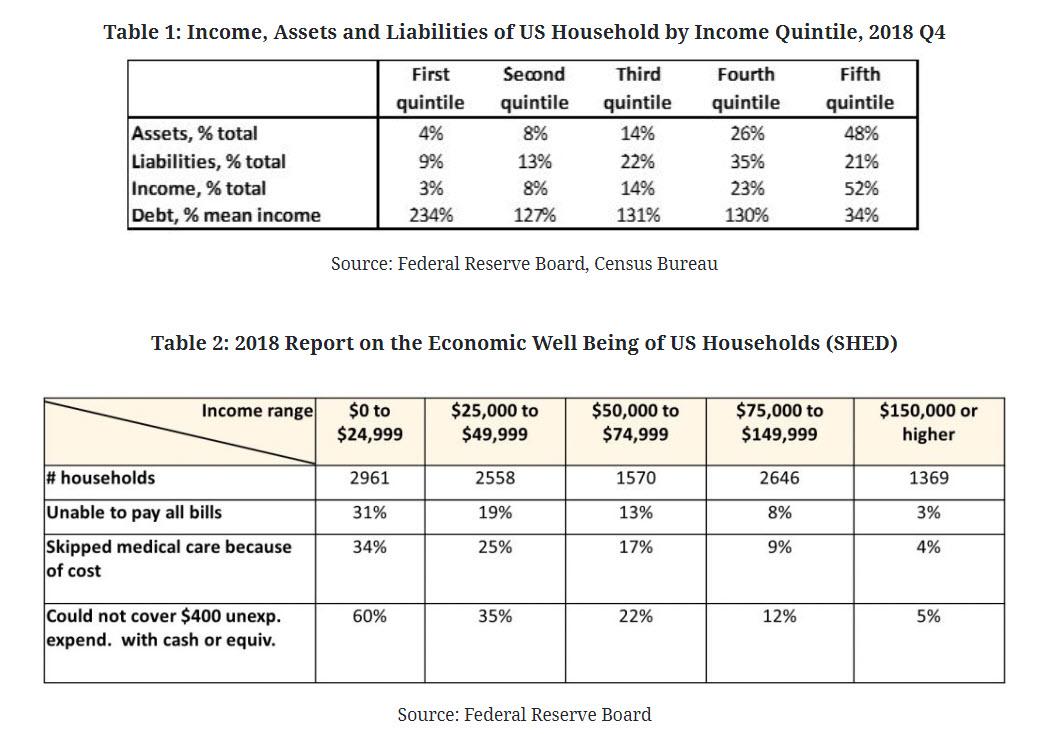

Raghuram Rajan, Chicago professor and former Governor of the Reserve Bank of India, who famously predicted the crisis, asserts that widening income inequalities were a major driver of the unsustainable leveraging of low-income US households before the crisis. Since then, income inequalities have increased, with most of the income and wealth gains accruing to higher-income households (table 1).

Indeed Federal Reserve and Census Bureau data on income and debt distribution show that a large share of American households cannot cover their basic expenses out of income (table 2). For instance, one-third of Americans in the lowest income quintile cannot pay all their bills, even after skipping needed medical care. This income shortfall could explain low income households high leverage.

Of course, relative to the crisis the scale of bad consumer debt seems much more limited. In addition, regulatory tightening since the crisis has pushed risk out of the banking sector. Risks however are more likely to have been displaced than eliminated altogether. It may well turn out that consumer credit risks are now concentrated in fintechs. In any event, those are less systemically important than large deposit taking institutions.

The cracks in household balance sheets are still likely to add to downside risks to growth. The pre-crisis household debt overhang and subsequent deleveraging were major causes of the recession and weak recovery. This time around, while the debt overhang is smaller, it also seems concentrated within low income households that have a higher propensity to consume. Against this backdrop, a continued tightening of consumer credit standards could force low income households to increase their savings. Consumption growth, that is already slowing and is the US economy main growth engine, could slow further and bring GDP growth below potential.

Turkey Threatens “Imminent” Large Scale Invasion Of Idlib To Halt Syrian-Russian Advance

New threats related to Idlib this week could see the Russian and Turkish armies on a direct collision course.

Turkey’s President Recep Tayyip Erdogan on Wednesday threatened a full-scale military invasion of the war torn province after the Syrian Army and its Russian ally refused to halt their ongoing offensive.

“An operation in Idlib is imminent,”Erdogan told Turkish parliament of preparations for NATO’s second largest army. “We are counting down, we are making our final warnings”.

Turkish tank in the town of Binnish in Syria’s northwestern province of Idlib, via AFP.

“Turkey has completed preparations for the implementation of its plan on Idlib, just like we did with previous operations. Frankly speaking, an operation in Idlib is only a matter of time,” Erdogan said.

He further emphasized that Turkey “is determined to pay any price to ensure security in both Idlib and Turkey.” The Syrian and Turkish armies have been engaged in sporadic fierce clashes for the past two weeks in Idlib, resulting in scores dead and wounded on each side, though specific numbers are disputed. Turkey has acknowledged at least 13 of its national troops killed.

“We will not leave Idlib to the [Syrian] regime, which does not understand our country’s determination, and to those encouraging it,” said Erdogan. Turkey has thus far sent limited deployments of troops and armored convoys into the northwest Syrian province to support and defend a dozen observation posts.

The Kremlin was quick to respond to such a threat of major escalation, pointing out that any Turkish offensive against Syrian forces in Idlib would be the “worst case scenario”.

“If it will be an operation against terrorist forces in Idlib, that would certainly be within the spirit” of Russia’s agreements with Turkey, Kremlin spokesman Dmitry Peskov said before adding: “But if it is about an operation against legitimate Syrian armed forces, that would certainly be the worst case scenario.”

The IDPs break into one of the humanitarian supplies warehouses as they are fed up waiting for 6 hours in-line with so little being distributed. #Syria#Idlibpic.twitter.com/OTRyoyN7QH

Talks between Turkish and Russian officials earlier this week related to Idlib failed to reach any agreement. This after Erdogan and Trump held a phone call wherein both leaders agreed the Syrian-Russian offensive must be halted “immediately”.

Mainstream media has also begun to again put Idlib coverage front and center as hundreds of thousands of civilians are said to be fleeing. Erdogan has long expressed fears that a million or more refugees could flood across the Turkish border, adding to the already some three million Turkey says it’s hosting.

UN figures state that at least 700,000 people have been displaced in Idlib since fighting was renewed in early December.

2 ‘Diamond Princess’ Passengers Die Of Coronavirus

As Japanese health officials begin the second day of offloading passengers and crew from the ‘Diamond Princess’ cruise ship that has been under quarantine in Yokohama for the last two weeks, the Japanese press is reporting that two passengers from the ship have died.

The report cites unidentified government officials.

Even as roughly 600 passengers disembarked on Wednesday, Japanese officials announced 79 more confirmed cases aboard the ship on Wednesday, bringing the total number of infected to 621 – the largest outbreak outside mainland China.

In the US, the CDC has questioned the wisdom of Japanese officials, and accused them of failing to properly quarantine the ship, particularly after 14 passengers found to be carrying the virus were allowed onto a US evacuation flight.

All of the passengers leaving the ship have reportedly been tested for the COVID-19, according to the cruise line. Several hundred other passengers who aren’t taking repatriation flights to their home countries are expected to leave the ship on Thursday, and it’s unclear what will happen to them after that. Most of the passengers will be ferried back to their home countries, where they will face another two weeks of quarantine.

Japanese health officials are expected to begin offloading more passengers shortly (since it’s already mid-morning on Thursday in Tokyo). It’s not clear how these deaths will affect the process, if at all.

These are the first deaths since Hong Kong reported its second death and Iran reported two virus-related deaths. It brings the death toll ex-China to 9. They marked the second and thirds deaths in Japan, respectively.

One event is taking center stage in the world that affects not only basic survival for millions of people, but the health of the global economy overall.

Of course, I’m talking about the coronavirus outbreak currently playing out before our eyes in China.

China’s economy was slowing substantially before the outbreak of the highly contagious and deadly virus last fall.

This slowing was the predictable result of excessive debt levels, Trump’s retaliation in the trade wars, and China’s encounter with what development economists call the “middle-income trap.”

Developing economies can grow at double-digit rates as they move from low-income (about $3,000 annual per capita income) to middle-income (about $10,000 annual per capita income).

The main requirements are limits on corruption, a large pool of available labor, and an attractive legal environment for foreign direct investment. Once investment is used for infrastructure and labor is mobilized, large-scale basic manufacturing can commence.

This powers growth and the accumulation of hard currency reserves from export earnings.

The difficulty begins when an economy tries to move from middle-income to high-income (about $18,000 annual per capita income). That move requires more than cheap labor and infrastructure investment. It requires applied technology to produce high-value added products.

Only Taiwan, South Korea and Singapore have made this transition, (excluding Japan after World War II, and oil-exporting nations).

This explains why China has been so focused on stealing U.S. intellectual property.

Trump has been closing that avenue. China cannot generate the needed technology through its own R&D. China is stuck in the middle-income trap and a slowdown in growth is the inevitable result.

The story gets worse for China.

As of Friday, the total reported number of people infected by the coronavirus was 64,435. And the death toll was up to 1,383, including three people outside of China.

Those figures are official statistics released by China and other countries around the world where the virus has spread.

However, there is substantial medical, anecdotal, and model-based evidence that the actual infection rate and death rate may be ten to twenty times higher than those official statistics.

Over 60 million Chinese in several major cities are under “lock-down” where individuals are confined to their homes and may only leave once every three days to buy groceries.

Streets are empty, stores are closed, trains and planes are not moving, and factories are shut. The Chinese economy is slowly grinding to a halt.

This not only affects China’s economy as a whole, but the contagion filters down into individual companies that are dependent on China both for supply chain inputs and final sales.

And it will have a rippling effect on the U.S. economy also. This story has a long way to run.

Ayatollah Tweets “Wealthy Zionists” Control America Amid Push To Get Him Banned From Twitter

Iranian Supreme Leader Ayatollah Khamenei has marked the latest national event commemorating the death of IRGC Quds Force commander Qasem Soleimani by tweeting a deeply provocative statement asserting that “wealthy Zionists” control America.

The United States has reached the “peak of arrogance,” and is controlled by “wealthy Zionists and their corporate owners,” which makes it a “manifestation of oppression, abhorred by the world,” he said further, as reported in The Jerusalem Post.

Now deceased Iran’s Quds Force commander Qassem Soleimani (left) with Iranian Supreme Leader Ali Khamenei, via Times of Israel/Wiki Commons.

The statement comes after the Islamic Republic’s top cleric and head of the regime previously slammed Trump’s Mideast peace plan “Deal of the Century” as “satanic” because it ultimately represents the “Jewishization” of Jerusalem and the suppression of Islamic identity.

“To the dismay of US politicians, the satanic, evil US policy about Palestine — the so-called Deal Of The Century— will never bear fruit, by the grace of God,” Khamenei wrote on his official Twitter account in late January.

Such inflammatory and religiously charged rhetoric will likely only fuel an ongoing initiative of hawkish Republican Senators to get Khamenei and other top Iranian leaders banned from Twitter and other US social media platforms.

We are against the rule of oppression and arrogance. This is what we mean by “America.” Today, the peak of arrogance is the US, which is controlled by the wealthy Zionists & their corporate owners. The US is a manifestation of oppression. Thus, they’re abhorred by the world.

Earlier this month the group of Republicans including Ted Cruz (Tx.), Tom Cotton (Ark.) Marsha Blackburn (Tenn.) and Marco Rubio (Fla.) wrote in the letter to Twitter: “While the First Amendment protects the free speech rights of Americans — and Twitter should not be censoring the political speech of Americans — the Ayatollah enjoys zero protection from the United States Bill of Rights.”

“And, as the leader of the world’s leading state sponsor of terrorism — directly responsible for the murder of hundreds of U.S. citizens — the Ayatollah and any American companies providing him assistance are entirely subject to U.S. sanctions laws,” they added.

Twitter has long defended its position of never banning heads of state from the platform, given the need to publicly articulate a country’s positions.

Israeli media has carefully documented Khamenei’s recent history of lashing out at “Zionists and Jews” on Twitter; however, as The Jerusalem Post notes, he’s long underscored a distinction between political Zionism and adherents of the Jewish religion:

Last year, the ayatollah said Iran is not antisemitic and that Jews live safely in Iran. In June 2019, he contrasted Iran’s treatment of Jews with “certain old Arab leaders who believed Jews should be thrown into the sea.”He says Iran is only opposed to the “Zionist” regime.

Regardless, American politicians and pundits typically view any and all disparaging remarks about ‘Zionists’ – especially coming out of Iran or the Islamic world in general – as an anti-Semitic trope.

Historically, Russia goes to great lengths to hide or disguise its strategic intentions but it clearly feels empowered enough in the Middle East to very obviously stake its claim in the region – excluding, for the time being only, Saudi Arabia – by stating that a slew of Russian companies are to spend up to US$20 billion on oil projects in Iraq in the near term.

“Since [U.S. President Donald] Trump outlined the new U.S. foreign policy of not engaging in conflicts abroad unless they were directly aligned with U.S. interests [October 2019], and then effectively withdrawing from Syria and from supporting the Kurds, Russia and China have felt that they can bring forward their plans to bring Iraq within their geopolitical arc of influence,” a senior source who works closely with Iraq’s Oil Ministry told OilPrice.com last week.

“They know that provided that they do not impinge on Saudi Arabia and, at a pinch the UAE and Kuwait, or launch attacks against U.S. personnel, then they can basically do whatever they want anywhere else, hence this announcement from Russia last week,” he added.

Before this announcement – which specifically mentioned Zarubezhneft, Tatneft, and Rosneftegaz as companies interested in pursuing specific but as yet unnamed projects, in addition to those Russia companies already active in the country (including Lukoil, Bashneft, and GazpromNeft) – Russia had adopted its usual stealth approach to building up its presence in Iraq.

“It is incremental colonialism, beginning one day with one relatively small contract being taken up by some Russian company nobody has heard of, then more Russian companies turn up in the same place under ‘contractor’ terms having been engaged by the company you gave the original contact to, then security companies turn up to guard all of the personnel, and suddenly you have a major Russian occupation of part of your key oil and gas infrastructure,” the Iraq source underlined.

The oil and gas prize for the Russians in Iraq is, of course, huge, but many in the industry do not realise that it is still underestimated. The official figures for oil are that Iraq has around 149 billion barrels of reserves (18 per cent of the Middle East total and 9 per cent of the global total) and is currently the second-largest oil supplier in OPEC, after Saudi Arabia. All of this oil coming at a mean average ‘lifting cost’ per barrel in Iraq of US$2 to US$3 per barrel, according to the IEA, at least as competitive as Saudi Arabia. For gas, the official figures are slightly less impressive, but they are likely even more underestimated than the oil figures, with Iraq having about 135 trillion cubic feet of reserves (the 12th largest in the world), mostly associated at the moment with oil fields in the supergiant fields in the south of the country. However, despite the occasional increase in reserves estimates over the past few years – extremely modest by the standards of its neighbours, incidentally – much of Iraq still remains unexplored or under-explored compared with other major oil-producing countries.

According to the International Energy Agency (IEA), and derived from the landmark United States Geological Survey (USGS) 2000 assessment and subsequent updates, the level of ultimately recoverable resources at that time was around 232 billion barrels of crude and natural gas liquids. Even this, though, might prove on the low side, added the IEA, as a detailed study by Petrolog around that time reached a similar figure but did not include the parts of northern Iraq in the KRG area or examination of the geological anomalies prevalent in the central and western regions of the country. Even using the much more conservative USGS number, Iraq had just a decade ago only produced around 15 per cent of its ultimately recoverable resources, compared with 23 per cent for the Middle East as a whole at that time. At that point, of the 530 potential hydrocarbon-bearing geological prospects identified by – only – geophysical means in Iraq only 113 had been drilled, with oil being found in 73 of them, a success rate of 65 per cent. Although more of these geophysically-identified sites have now been drilled many more new ones have arisen due to identification by more sophisticated analysis of seismic and historical data.

“The Russians have done their own testing of potential oil and gas reserves over the years and they think it is about double the current official estimates on both of those [oil and gas],” the Iraq source told OilPrice.com last week.

This is one of two key reasons why Russia has exploited every opportunity to expand its footprint in the north and south of Iraq. In the north it has been extremely successful so far in using its corporate proxy, Rosneft, to gain control over key elements of the region’s oil and gas infrastructure while in the south it had been forced by the U.S.’s own former ambitions to tread more stealthily. Although it has always been able to rely on being able to use Iran’s political and military over Iraq for its own purposes, these had to be sidelined for a while, at least whilst the real power in Iraq – Moqtada al-Sadr – was getting settled in to his power-broking role. As this was initially founded on the ultra-nationalist message (‘Iraq for the Iraqis, with no undue foreign influence’, in essence) of his election-winning ‘Sairoon’ power bloc, Moscow was able to tinker only the edges.

In such strategies, though, Russia is a master, and the influence it can ultimately wield starting from such a tiny access point is absolutely extraordinary. The most recent example of this – and a template for such strategies for any aspiring superpower, frankly – was the ‘awarding’ of a hitherto unknown development block in the middle of a wasteland by a hitherto unknown Russian company at a time when no one else was aware that anything was due to be awarded. As highlighted in-depth by OilPrice.com at the time, Russia’s Stroytransgaz (an almost unknown Russian oil and gas company – except by the U.S. whose Office of Foreign Assets Control extensively sanctioned it in 2014) signed a preliminary contract with the oil ministry in Baghdad for oil and gas exploration in Anbar province (a wasteland as far as Iraq’s oil and gas sector development goes). On the face of it, there was – and is – no real prospect of any substantial amounts of oil or gas being recovered from its Block 17 and additionally stationing any normal oil and gas workers there would be perilous to say the least, as it is an area torn by warring tribal communities, which even Islamic State avoided where possible.

The key to this, though – and vital in understanding the purpose behind the announcement of a doubling (possibly tripling) of Russian overt investment into Iraq – is that the area is critical in Russia fortifying its presence in the central Middle East and being able to secure a warm water multi-layered military presence in the Mediterranean.

“Russia risked full-on military confrontation with the U.S. to get a full-scale Black Sea port [Sevastopol] with access into the Mediterranean when it annexed Crimea in 2014, so there’s nothing it won’t do to build out its foothold in Syria and in the transit and supply route to Syria, which includes Iraq,” said the Iraq source.

In this context, then, Block 17 in Anbar – and the US$20 billion investment announced last week – makes perfect sense for the Russians, as it intends to secure what the U.S. military used to call ‘the spine’ of Islamic State where the Euphrates flows westwards into Syria and eastwards into the Persian Gulf. Along the spine running from east to west are the historical ultra-nationalist and ultra-anti-West cities of Falluja, Ramadi, Hit and Haditha, and then there is Syria, with its key strategic ports of Banias and Tartus. By happy ‘coincidence’ both Banias and Tartus are also extremely close to the massive Russian Khmeimim Air Base and the S-400 Triumf missile system. Although the base only came in to operation in 2015 supposedly to help in the fight against Islamic State, Russia appears to have changed its tactical plans for it, having also signed a 49 year lease on it, with the option for another 25 year extension. A short flight away is Russia’s Latakia intelligence-gathering listening station.

Watch Live: Bernie Battles “Billionaire” Bloomberg In Critical Las Vegas Debate

Americans will get a glimpse of the great ‘revolutionary class war’ over the soul of the Democratic Party Wednesday night as Democratic Primary frontrunner Bernie Sanders, a self-proclaimed “Democratic Socialist” who once proposed that no American be allowed to earn more than $1 million per year, faces off against latecomer Mike Bloomberg.

Bloomberg has shot up in the polls in recent weeks after leveraging his $62.8 billion fortune to build a massive campaign operation and finance a deluge of ad buys. The former NYC mayors participation in tonight’s debate is controversial: He only qualified yesterday, and his name isn’t even on the ballot in Nevada.

After skipping the first four contests, Bloomberg won’t officially enter the running until March 3 – better known as “Super Tuesday” – where it looks like he has a strong shot at winning several delegate-heavy states.

Bloomberg campaign manager Kevin Sheekey said in a statement Tuesday that the candidate is “looking forward to joining the other Democratic candidates on stage and making the case for why he’s the best candidate to defeat Donald Trump and unite the country. The opportunity to discuss his workable and achievable plans for the challenges facing this country is an important part of the campaign process.”

Polls aren’t the only arena where Bloomberg has recently clocked a major advance: Ahead of the debate, online betting markets also placed Bloomberg in second to Sanders via the odds.

But, as Bernie has soared into the bookies’ odds lead, so the odds of a Trump win has surged…

If Bloomberg performs well tonight, parrying Sanders’ ad hominem attacks and slanders about billionaires, perhaps he’ll win over the rest of the doubters from his fellow moderates, and solidify his position as one true alternative to Sanders, especially as the Biden campaign implodes, Warren drops behind Klobuchar (with neither garnering much support) and Pete Buttigieg still can’t seem to convince much of the public that he’d be a trustworthy keeper of the nuclear codes.

Bloomberg will walk onto Wednesday night’s debate stage with a target on his back as a result of his ascendance in the polls. The forum will give voters a new view of Bloomberg, who has not yet been on a debate stage this cycle and has given only a few sit-down interviews since announcing his candidacy. The self-funded candidate is set to make the stage in Nevada after the Democratic National Committee dropped a previous donor threshold. The biggest attacks Bloomberg has received from the Democratic field this cycle have been from Sanders. The senator has repeatedly accused Bloomberg of looking to buy his way into the Democratic nomination after spending hundreds of millions of dollars on ads. The war of words escalated further on Monday when Bloomberg accused Sanders of not doing enough to call out the behavior and rhetoric of a segment of his supporters. Biden and Klobuchar have both also signaled their eagerness to hit Bloomberg on the debate stage, including over comments the former New York City mayor made about stop-and-frisk policing and housing policy for low-income buyers. “I am also an advocate for him coming on the debate stage. I know that I’m not going to be able to beat him on the airwaves, but I can beat him on the debate stage,” Klobuchar said.

How will Sanders fend off attacks on ‘Medicare for All’?

Sanders’s Medicare for All proposal, a hallmark of his campaign, came under fire in Nevada last week after the state’s powerful Culinary Union warned that the plan would “end culinary health care” by replacing private plans with government-run insurance. Klobuchar, Buttigieg and Biden have all questioned how Sanders would pay for his Medicare for All plan. Warren faced similar questions earlier in the race. The recent developments regarding the Culinary Union, which ended up not endorsing a candidate, have put a newfound scrutiny on Sanders’s proposed plan. “It is striking that there’s been no explanation of how this is supposed to work when it could be one of the biggest things done to the American economy in a generation,” Buttigieg said, referring to Sanders’s plan, in January. Sanders has argued that health care costs will be more expensive over the next decade without a Medicare for All system. Sanders also came under pressure after the Culinary Union denounced the candidate’s supporters for “viciously” attacking union members online. Sanders urged supporters of all campaigns to stop online attacks, saying “harassment of all forms is unacceptable to me.”

Can Biden and Warren have their debate moment?

Biden and Warren were both seen as front-runners earlier in the race but have both seen a decline in support in the polls after less-than-stellar performances in Iowa and New Hampshire. Critics say Biden’s debate performances have been weak, which could be an impediment to him on Wednesday as he looks to revamp his campaign. Biden is banking on the support of Latinos and African Americans in Nevada and could use Wednesday’s debate stage as an opportunity to tout his ties with those communities across the country. Warren, who has had a number of strong debate performances, will also be looking for a breakout moment as she looks to hit the reset button on her campaign. The senator will likely be looking to reclaim her spot as the race’s top progressive from Sanders, while also looking for opportunities to hit Bloomberg. Klobuchar showed this month that strong debate performances matter after a good showing by the Minnesota senator ahead of the New Hampshire primary was widely seen as having contributed to her better-than-expected third-place finish in the Granite State.

How will Buttigieg, Klobuchar pitch to a more diverse electorate?

Buttigieg and Klobuchar have emerged from contests in Iowa and New Hampshire with momentum, but they will be addressing a vastly different audience in Nevada. The two Midwesterners have struggled throughout the campaign to appeal to voters of color, which threatens to hurt them in Nevada. The two have also not spent as much time in Nevada compared to Iowa and New Hampshire, so Wednesday could be critical in terms of making their case to voters. Buttigieg and Klobuchar will likely have to answer questions about their past careers as a mayor and prosecutor, respectively, and how they affected minority communities in their roles. Buttigieg has come under scrutiny for his handling of the aftermath of a police-involved shooting of a black man, as well as questions about the disproportionate arrests of black people for marijuana possession during his mayoral tenure and the firing of a black police chief. Klobuchar has come under fire for prosecuting a black teenager who was found guilty of murder in 2002 despite a number of flaws in the case uncovered by an Associated Press story. The senator has called for all evidence in the case to be reviewed.

Which candidates besides Bloomberg are most likely to clash or take fire?

Aside from Bloomberg, there are a number of other candidate clashes that could take place on Wednesday night. Buttigieg and Sanders have gone head-to-head over their differences in policies, often showcasing the division between moderates and progressives within the party. Biden also attacked Buttigieg over his experience as the former mayor narrowly won more delegates in the Iowa caucuses, effectively replacing Biden as the standard-bearer for the moderate wing of the party. Klobuchar could see dividends in attacking Sanders, billing herself as the more pragmatic candidate. However, she could also look to go after the moderates on stage in an effort to break further out of the crowded centrist lane. Warren, whose attacks on Sanders have fallen flat in the past, could also set her sights on the moderates in the race in an effort to contrast her more progressive ideas.

Reportedly, according to campaign officials, Bloomberg will not be standing on a box for the duration of the debate.

Watch the debate live below. It begins at 9 pm ET:

Could the coronavirus act as a catalyst for a new global economic crisis? It certainly has that potential – but how would the crisis proceed?

In the December 2018 issue of our Q-Review, we laid out the likely scenarios of an approaching global economic collapse. But, like most things in life, such a dramatic event is unlikely to proceed in a linear fashion. There will be different stages within it.

In December 2019 we outlined these stages, which are likely five: the onset, counter-attack, flood, calamity and recovery. Here, we briefly define the characteristics of each.

The onset

Currently, there seems to be two possible ignition points for the collapse: the credit market and the European banking sector.

At the onset, stresses that have been building in the credit markets since the summer of 2019 will explode, shrinking if not eliminating entirely the exits from many parts of that market. Downgrades of corporate debt in the U.S. and peripheral sovereign debt in the Eurozone will push large fixed-income investors, including pension funds, into higher-rated bonds, leading to large-scale selling of lower-rated bonds, forcing wider spreads and even more selling.

Panic will build first in the junk bond market, then in the “investment-grade” corporate bond market, and then rapidly metastasize to engulf the stock market. A frantic retreat to ‘safe-haven’ assets, including U.S. Treasuries, German Bunds and U.K. Gilts as well as cash and precious metals will commence.

Cascading banking troubles in Europe will have the same destabilizing effects on the global stock and bond markets.

The counterattack

The second phase of the collapse will be the desperate efforts of authorities to stop the crisis by a counterattack.

These are likely to include the restarting and acceleration of QE-programs and other market support programs, gigantic fiscal stimulus, increasing trade protectionism and possibly even calls for direct debt monetization (see Q-Review 3/2019 for an explanation).

However, the plummeting yields on safe-haven bonds will make reflexive central bank QE-programs utterly ineffective, while any central bank stock purchase programs will provide little relief from the panic gripping investors. Central banks will also be unable to ameliorate a massive reduction in market liquidity.

Most of the governments of the Eurozone are too indebted to engage in any meaningful stimulus, especially when confronted with cascading bank problems and eventual failures. China will desperately try to enact even more fiscal stimulus, but due to the collapse of global economic demand and the probable implosion of the housing and financial system bubbles in China, such attempts will be wholly inadequate. The Chinese economy will slam to earth in a hard landing.

The flood

The crack-up in the credit and stock markets will be followed by a flood of corporate bankruptcies.

So-called “zombie” corporations, faced with collapsing economic demand and exploding interest rates—due to the banking crisis and crashing credit markets—will fail on a scale unseen in decades. The value of the holdings of pension funds, charitable endowments, trust funds, insurance company variable accounts, and stock and bond mutual funds will crash in short order. Even lowly money-market funds may be at risk, just as they were in the Financial Crisis.

If the European banking sector has not ‘cracked’ by this point, this tsunami of corporate bankruptcies will wash it over the edge. As Europe holds the largest concentration of Global Systemically Important Banks, or G-SIBs, the European banking crisis will “go global” in an instant.

Massive global deflation will follow, led by an ugly chain of bank and corporate failures. Global liquidity will collapse. An utter economic crash will follow.

The calamity

Due to both crashing capital markets and banking sector bankruptcies, joblessness and poverty are likely to explode. Simultaneously, government tax revenues will collapse as incomes retreat and capital gains evaporate. As governments spending skyrockets in an orgy of Keynesian counter-cyclicality, national deficits will hit all-time highs on both an absolute and relative basis.

Governments will try to save critically-important banks, which will require large-scale funding many countries—such as those in the Eurozone—cannot afford and will not be able to finance in paralyzed capital markets. This economic reality makes depositor bail-ins the only, if politically-unpalatable option.

Confronted by new and harsh fiscal realities, pensions and other social security programs are likely to face serious cutbacks by desperate governments. An economic calamity sets in.

The recovery

We expect the global depression to last 4-5 years. The initial collapse is likely to be over within three years.

The path to recovery will depend crucially on how far the ‘cleansing’ of the economy, markets and financial sector is allowed to go. If the banking sector implodes completely, the economic deficit will naturally be made much deeper leading to a systemic crisis.

However, if the essential functions of the banking sector are sustained, especially in Europe, we would avoid the deepest malaise. Moreover, if unsound banks and “zombie” corporations are allowed to go-under or are wound-down methodically, it will clear much of the malinvestment from the economy, creating the foundation for a strong and sustained recovery.

So, if we manage to return to the principles of the market economy including, most crucially, a return to undistorted price discovery in the capital markets, we are likely to see one of the most powerful recoveries in global economic history. It would be led by robotization and general technological innovation, which hard economic times tend to foster.

However, debt monetization, Modern Monetary Theory (“MMT”) and other money-conjuring schemes would corrupt the economy further making a sustained recovery impossible (see more from Q-Review 4/2019).

Moreover, with the governments and the central banks assuming a much bigger role in the economy and society in this darker scenario, some form of fascism (which is, by definition, the merger of state and corporate power) would be the likely end-result of these developments.

We can do nothing more than hope that wise, courageous and far-sighted political leadership will spare us from that horrible fate.

When?

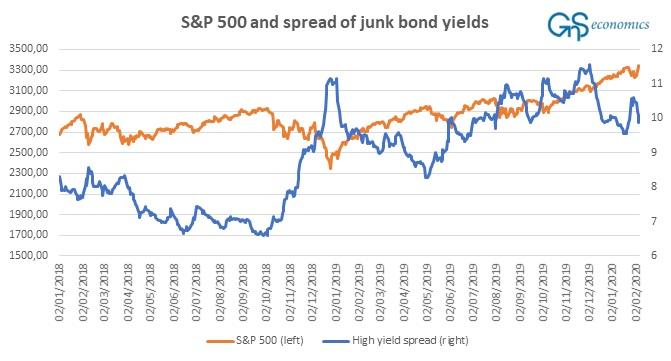

After the Fed launched its desperate repo-market bailout operations in September and October of last year, stresses in the credit markets eased-up and stock markets rallied. Following the coronavirus outbreak, junk bond yield-spreads shot-up, but they were quickly tamed by the massive support operations launched, once again, by major central banks (see Figure 1).

It’s truly interesting to see, how long the artificial liquidity can keep the stock markets up, when the economy slows.

Figure 1. The daily closing value of the S&P 500 index and the option-adjusted spread of the ICE BofAML US corporate C index over the spot Treasury curve. Source: GnS economicss, Fed St. Louis, Yahoo Finance

Now, everything depends on China, and the impact of the coronavirus. How bad will the situation get? Do we anticipate a global pandemic, which at this point appears increasingly likely? Can China restore production quickly, which currently looks unlike?

The virus is so hazardous for the Chinese economy, because the virus itself and the draconian measures adopted to contain it disrupt production and the incomes of millions of highly-indebted firms and households. The longer that this broad economic stress continues, the higher the likelihood of corporate defaults and bankruptcies.

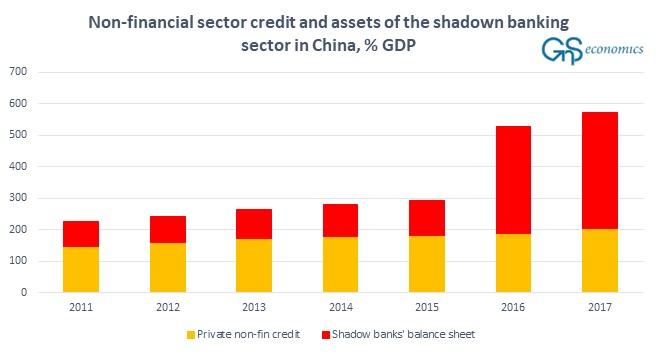

China’s banking system is extremely levered (see Figure 2). As we explained in Q-Review 4/2019, China’s banking system will be unable to cope with any longer slowing down of growth, not to speak of a recession.

Large-scale defaults and bankruptcies caused by the reasons just discussed would hit the Chinese banking sector especially hard. The virus can in this way easily act as a catalyst for a deep and severe banking crisis in China. It would guarantee a global recession.

Figure 2. Asset of the shadow banking sector and the credit issued to the non-financial sector in China. Source: GnS Economics, PBoC, BIS, Fed St. Louis

Most importantly, if the coronavirus pushes the Eurozone into a recession within the next few months, which seems very likely, our weak banking sector is unlikely to be able to cope with that (see Q-Review 4/2019 for a detailed explanation). And, that would imply the beginning of a global banking crisis, as explained above.

This is to say that by summer, we may be at the onset.

Israel To Step Up “Offensive Action” – Will Turn Syria Into “Iranian Vietnam”: Israeli Defense Chief

After over two years of sporadic Israeli air and missile attacks inside Syria, which Syria’s military has been more aggressive in responding to of late, Israel has issued a rare statement revealing its medium to long-term strategy, saying it will soon step up “offensive action” in the country to ensure Iranian fighters depart.

Speaking to Ynet News on Wednesday the new Israeli Defense Minister, Naftali Bennett said, “We will go from preventive action to offensive action — the only measure that guarantees us the expulsion of Iran out of Syria.”

“We are warning them (the Iranians), we will turn Syria into an Iranian Vietnam, and you will continue to bleed until the last Iranian soldier leaves Syrian territory,” the nation’s defense chief threatened.

Prime Minister Benjamin Netanyahu and Defense Minister Naftali Bennett visit Golan Heights base overlooking Syria last year. Image source: GPO/Haaretz

Israel’s latest attack on Damascus occurred last Thursday, which resulted in heavy damage at the Syrian capital’s international airport, which media reports claim was used for Iranian weapons storage. Satellite imagery analysis source ImageSatsaid one of the more severely damaged buildings was “probably used for storing ammunition or [surface-to-air missiles].”

Syrian opposition media claimed that four members of Iran’s elite Islamic Revolutionary Guard Corps (IRGC) and three Syrian soldiers were killed in the airstrikes. Israel has throughout the war often conducted attacks from over Lebanese airspace, targeting what it claims are Iranian assets inside Syria. Israel almost never provides confirmation it was behind these attacks, with Netanyahu quipping to reporters when asked about it: “I don’t know what happened at night. Maybe it was the Belgian air force.”

With the final battle for Idlib province now underway in the northwest, Assad has clearly emerged victorious in the war, making Tel Aviv increasingly anxious about Iran’s continued entrenched presence in support of its ally.

In separate prior comments delivered on Tuesday, Defense Minister Bennett said Iran is changing its thinking inside Syria. “I can tell you that we are seeing the initial indications of Iran weakening and considering a new tack in Syria,” he told a military technology conference in Tel Aviv.

“[The Iranians] are sending forces in order to establish a presence there to exhaust us, but we are turning this disadvantage into an advantage. We have intelligence and operational superiority, and we are telling the Iranians clearly: Get out of Syria. There’s nothing for you here.”

“We are moving from a defensive position to an offensive position — to weaken, to exhaust, to tire and wear out the head of the octopus in order to weaken its arms,” Bennett said, using an analogy he employs frequently.

He also said recent anti-government demonstrations in Iran were a sign that the Iranian people were growing tired of the Ayatollah’s “foreign adventurism” in places like Syria, and that they are telling their leaders “Stop wasting money and our blood on adventures”.

{kind=link}

{kind=link}

{kind=link}