Now a teenager in France has triggered a debate over its plunge into speech crimes and regulation after characterizing Islam as “a religion of hate.” She can now be criminally investigated for hate speech under the notorious French speech law.

On a January 18th live broadcast on her Instagram account, Mila, 16, was called a “dirty lesbian” by a Muslim commenter. She responded by saying “I hate religion. The Koran is a religion of hate” and using vulgarity against the religion. She added “I am not racist. You cannot be racist towards a religion. I said what I thought, you’re not going to make me regret it.”

Despite receiving death threats and being forced to forego school, she refused to back down and said that she “wanted to blaspheme”. She apologized if she was vulgar and said that she did not want to insult people who practice their religion “in peace,” but “I have absolutely no regrets about what I said, it was really my thought.”

When French justice minister Nicole Belloubet denounced this as an attack on religion and was “an attack on freedom of conscience”.

This is the inevitable result of speech codes and speech crimes. There is an insatiable appetite to use the criminal justice system to punish those who hold opposing views.

These laws criminalize speech under vague standards referring to “inciting” or “intimidating” others based on race or religion.

For example, fashion designer John Galliano has been found guilty in a French court on charges of making anti-Semitic comments against at least three people in a Paris bar. At his sentencing, Judge Anne Marie Sauteraud read out a list of the bad words used by Galliano to Geraldine Bloch and Philippe Virgitti. “He said ‘dirty whore’ at least a thousand times,” she explained out loud.

In another case, the father of French conservative presidential candidate Marine Le Pen was fined because he had called people from the Roma minority “smelly”. A French mother was prosecuted because her son went to school with a shirt reading “I am a bomb.”

As I have previously discussed, the sad irony of France leading efforts to curb free speech is powerful.

Once the bastion of liberty, France has now become one of the greatest international threats to free speech. It even led a crackdown on the free press with criminal investigations. Mila has vividly shown how France has replaced its rallying cry for liberty with a demand for conformity. Perhaps this teenager will awaken enough citizens to the scourge of speech codes and crimes.

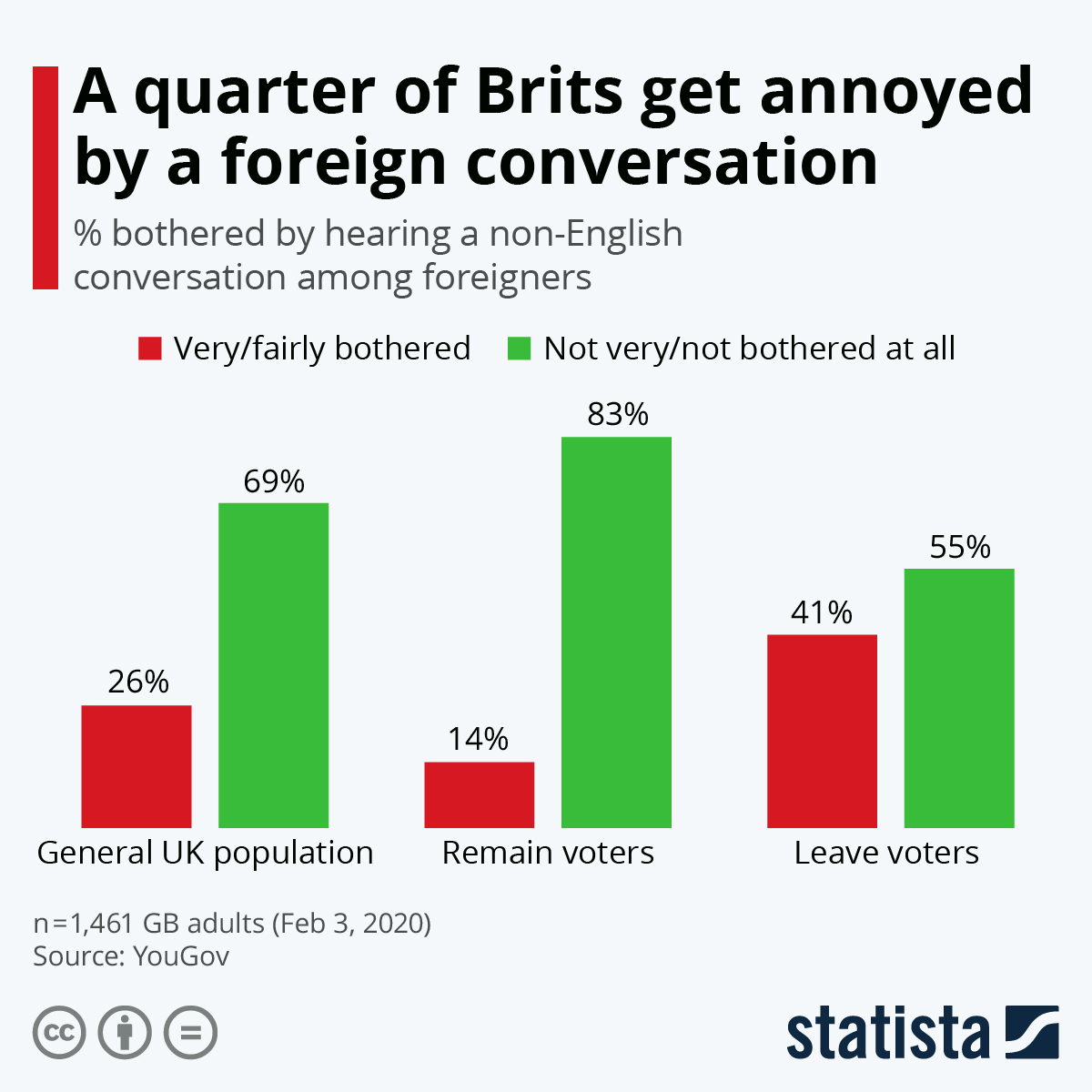

The survey involved 1,461 adults and, as Statista’s Niall McCarthy notes, it found that more than a quarter of them would be very or fairly bothered by hearing people from a non-English speaking country talking to each other in their own language.

Among those who voted to remain in the EU, 14 percent would be bothered in some fashion by conversation in a foreign language while 83 percent couldn’t care less.

Intolerance is high among leave voters, however, with 55 percent of those polled stating that a foreign conversation would get on their nerves while 41 percent would not be bothered by it.

The European Union has lost one of its most important member states. The United Kingdom accounted for around one-sixth of the EU’s population and economy. Without it, the EU will still be one of the world’s premier economic powers, but it will suffer a loss of dynamism.

Still, there is hope for a fruitful, cooperative EU-UK relationship. The first step is to negotiate a trade agreement. But it would be a mistake to concentrate too much on the details of those talks. Trade is important to both sides, but the minutiae of the UK’s trading relationship with Europe will not determine its economic fate. The most likely outcome is a deal that eliminates tariffs for both sides, but even a return to standard World Trade Organization rules would not be the end of the world. While a better trade deal might prevent the loss of a few percentage points of GDP over the next decade, other variables, such as the quality of education, investment, and domestic regulation, are ultimately more important for growth.

In any case, the EU is much more than a market. It has its own currency and has abolished fiscal-policy frontiers across a massive geographic area. The UK did not participate in either of these key areas of integration and would not have done so anytime soon. As such, the EU has actually lost only a “one-third” member. The relationship with the UK needs to be managed properly. But the fact is that European leaders and policymakers have much more pressing issues to address. Brexit is now a sideshow.

Chief among the EU’s priorities is the European Green Deal, which is an area where the UK could continue to participate, given its shared concerns about climate change. In the long run, however, the EU’s efforts to complete the eurozone and the Schengen area of passport-free travel will put it and the UK on diverging paths.

Economists will continue to debate whether the euro was ever a good idea, with Anglo-Saxons sticking to the line that, “It can’t happen, it is a bad idea, it won’t last.” The euro crisis did seem to vindicate the UK’s skepticism. And yet opinion polls over the past few years show that the European population has moved beyond the academic debate. By the latest count, close to 80% of Eurobarometer respondents think the euro is “good for the EU.”

For younger generations that have never known any other currency, the very question of whether they would prefer some newly introduced national currency is nonsensical. There is a reason why Euroskeptic parties and candidates have consistently lost elections in which they have explicitly advocated an exit from the eurozone. Even an arch-populist like Matteo Salvini of the League party in Italy has abandoned the “No Euro” slogan on which he once ran.

Similar political dynamics apply to passport-free travel. The Schengen area is still a work in progress, but the direction of its evolution is clear: rather than retreating on the principle of freedom of movement, member states are gradually reinforcing the EU’s external border. Over time, that will give voters confidence that they do not need permanent controls or fences between member states. True, there are still some internal controls left over from the 2016 refugee crisis, but these are exceptions that prove the rule. In most cases, however, Europeans enjoy passport-free travel on the continent.

In the UK, these advances have been dismissed as part of the much-derided quest for “ever closer union,” which the British electorate never embraced. Nonetheless, EU integration will continue among the remaining 27 members, leading to further projects that the UK probably would not have supported anyway. The most conspicuous (and long-term) of these projects is European defense. Ironically, while the UK was in the EU, it always opposed proposals for a joint defense force. But now that it is on its own, it supports the idea, because it will facilitate EU-UK defense cooperation.

The UK has already become accustomed to playing second fiddle in its “special relationship” with the United States, so it is not unreasonable to think that it could accept a similar relationship with the EU. In most cases, the UK would inevitably follow Europe’s lead, while maintaining its sense of cultural superiority at home. British diplomats would be able to revive their pre-membership tradition of remaining aloof and mystified by European polyglots’ impractical schemes.

Of course, for such an arrangement to work, the EU will have to make a good-faith effort to consider the UK’s legitimate interests. That will require overcoming some bad habits. In its dealings with other neighbors, including the Balkan countries, Ukraine, and even Norway and Switzerland, the EU tends to behave like an acknowledged hegemon, often assuming a “take it or leave it” position.

To be sure, in economic terms, the EU’s relative size speaks for itself. But it is the UK that will be stronger in many other areas, not least security and intelligence, where the EU has limited capacity, while most individual member states have almost none at all.

Given these broader considerations, the EU would be mistaken to exploit its economic advantage when the trade talks start at the beginning of March. Brexit could ultimately lead to a productive special relationship in which the UK remains a close partner of the EU and makes a valuable contribution to Europe’s peace and prosperity.

On Friday November 29, 2019, an Islamist terror attack took place in London. Two young people, both recent Cambridge University graduates, Jack Merritt (25) and Saskia Jones (23), were stabbed and killed by a single attacker. It was a terrible and unnecessary loss of life.

The special irony about Jack and Saskia’s deaths is that they (and a colleague) had been involved with Cambridge University’s Learning Together prison-rehabilitation program, similar to the US version known as Inside-Out, both of which bring prison inmates together with students to learn together. The British programme is run by Cambridge University’s Institute of Criminology, from which both Merritt and Jones had received M.Phils in criminology.

On that Friday, the fifth anniversary of the program, they were attending a conference on offender rehabilitation. The event, dedicated to work on reintegrating prisoners after their release, took place in the stately Fishmongers’ Hall at the north end of London Bridge. It was attended by a mix of academics, students, graduates and former prisoners, some with tags.

Just after lunch, at 12.58 p.m., the conference erupted into chaos when one of the participants threatened to blow it up. A man, later identified as Usman Khan, revealed that he was wearing what appeared to be a suicide vest. It is not clear what he planned to do, given that the vest was a fake and could not have served in any attack. However, he did have two knives taped to his wrists. When he left the Hall and went down to the bridge, it was indeed with these weapons that he killed Merritt and Jones and injured several others, some badly.

Remarkably, instead of running for their lives, many of the conference participants, including some prisoners, tackled Khan. One was a convicted murderer on day release. Two of these heroes were Merritt and Jones, who paid for their bravery with their own lives.

That Khan was there at all almost beggars belief. He was out on licence from prison, where he had served just half of a 16-year prison sentence for engaging with others in plans for what could have led to a major terrorist atrocity. He was at the conference because it was believed he was working towards his own deradicalization. Quite obviously, he had not been deradicalized.

Nine years earlier, when he was 19, Khan had been a leading member of a terrorist outfit inspired by al-Qa’ida.The members were arrested and put on trial in 2012, when Khan and two others were handed undetermined sentences; Khan was classified as never to be released. They had never carried out an attack, but they had ambitious plans, distributing letter bombs in the post, and setting off pipe bombs in toilets and pubs. There was also a handwritten target list belonging to the group which listed the names and addresses of the then London mayor, Boris Johnson, the Dean of St Paul’s Cathedral, two rabbis, the US embassy in London and the stock exchange.

There were nine accused in all, but Khan and two others were described by the judge who sentenced them, Justice Alan Wilkie, to have been “more serious jihadis than the others.” Wilkie had also warned that Khan should not be released from prison early:

In my judgment, these offenders would remain, even after a lengthy term of imprisonment, of such a significant risk that the public could not be adequately protected by their being managed on licence in the community, subject to conditions, by reference to a preordained release date.

That warning was not heeded when it came to a reconsideration of Khan’s situation.

At an appeal hearing in 2013, Khan was given a determinate sentence of 16 years in gaol. He had served about five years of this when he was released on licence while wearing a GPS ankle bracelet.According to a BBC investigation:

During his time in prison, Khan completed a course for people convicted of extremism offences and after his release went on a scheme to address the root causes of terrorism.

The first course Khan went on, the Healthy Identity Intervention Programme, was piloted from 2010 and is now the main rehabilitation scheme for prisoners convicted of offences linked to extremism.

There was, however, a flaw in these schemes: they had not been fully tested or evaluated. The BBC’s home affairs correspondent, Danny Shaw, remarked:

Last year, the Ministry of Justice published the findings of research into the pilot project which found it was “viewed positively” by a sample of those who attended and ran the course.

However, the department has not completed any work to test whether the scheme prevents reoffending or successfully tackles extremist behaviour.

There has also been no evaluation of the impact of the Desistance and Disengagement Programme, which Khan took part in after his release last year.

It need hardly be said that Khan’s attack is evidence that such schemes are inherently unstable and, in a certain percentage of cases, likely to fail.

Actually, the failure rate had already been predicted by Ian Acheson, a British expert on prisons who is currently a senior advisor to the US-based Counter Extremism Project. In 2015, Britain’s Justice Secretary, Michael Gove, appointed Acheson, aided by a small expert team, to conduct an independent review of Islamist extremism in the prisons and probation system in England and Wales. A summary of the main findings of Acheson’s final report has been made available online by the UK government.

On December 1, however, Acheson himself wrote an article for the London Times entitled “London Bridge attack: I told ministers we were treating terrorist prisoners with jaw-dropping naivety. Did they listen?”

In it, he revealed that his survey was originally opposed by the CEO of Britain’s Prison and Probation Service, who had to be overruled by Gove. He goes on to write that “What we found was so shockingly bad that I had to agree to the language in the original report being toned down. With hindsight, I’m not sure that was the right decision.” He continues with a deeply worrying account of what he and his team found:

There were serious deficiencies in almost every aspect of the management of terrorist offenders through the system that are relevant to Usman Khan. Frontline prison staff were vulnerable to attack and were ill-equipped to counter hateful extremism on prison landings for fear of being accused of racism. Prison imams did not possess the tools, and sometimes the will, to combat Islamist ideology. The prison service’s intelligence-gathering system was hopelessly fractured and ineffectual.

The rest of the article should be read in full, for it is a damning indictment of the way Islamic extremism and deradicalization of terrorists are handled within the UK’s prison network. At one point, he writes:

What has this got to do with Khan? Many of the recommendations I made related to what I saw as serious gaps in the management of terrorist offenders into custody and “through the gate”. There was a lack of expertise and appropriateness in the arrangements for probation supervision of these most potentially lethal offenders.

The questions Acheson proceeds to ask are detailed and well informed. Perhaps the government agencies responsible for incarceration and deradicalization of terrorists and would-be jihadists will listen to him and others who are deeply informed about the problem and will introduce some at least of the many reforms he calls for.

Tragically, that may not happen. As he himself admits, he is likely to be persona non grata within the service and perhaps the Ministry of Justice:

Moreover, there are legitimate questions to ask about the qualifications of the key people in this highly sensitive role and how they were appointed. HM Prison and Probation Service, where I spent nearly a decade working, is a notoriously closed shop when it comes to the advancement of its senior leadership, whatever the public relations person says.

To make life even harder for prison officials at every level, a study published by the Ministry of Justice in May 2019, has revealed that radical Muslims in gaol in the UK are almost out of control to the point where they rule prisons. Entitled “Exploring the Nature of Muslim Groups and Related Gang Activity in Three High Security Prisons: Findings from Qualitative Research”, the study paints a disturbing picture that could have been a script for a violent TV drama.

There is a useful summary of the UK situation by Patrick Dunleavy, a former Inspector General for the New York State Department of Corrections. Dunleavy has testified as an expert witness before the House Committee on Homeland Security about the threat of Islamic Radicalization in the U.S. prison system.

In his summary dated June 19, 2019, Dunleavy identifies a group of radicalized Muslims who function as a gang in UK prisons, taking control of territory and exercising influence over existing and new Muslim prisoners, even where the latter do not enter gaol as extremists or terrorist supporters. Dunleavy sums up the influence of this broad “gang”:

Obedience is achieved by violence and intimidation carried out by members of the group known as enforcers. “Those who had committed terrorist crimes often held more senior roles in the gang,” the study found, “facilitated by the respect some younger prisoners gave them.”

Leadership gives the orders for all acts of violence. No member acts on his own. If he does, one inmate said, he is taken aside by a leader….

The study described the leaders as manipulative, dominating, and outspoken and yet found they were able to portray themselves to prison staff as compliant and polite. In other words, “jail wise.”

A similar situation exists in the United States, where Muslim radicals also form gang-like structures of mutual reinforcement and coercion. Dunleavy draws on his own direct experience of US prisons:

I was assigned to “Operation Hades” at the time, a multifaceted investigative group of federal, state, and local agents, analysts, and law enforcement officers tasked with exploring the level of radical Islamic recruitment in the prison system.

The study found that terrorist groups such as al-Qaida did not see prison as an obstacle. Quite the opposite, they viewed it as an opportunity to organize and expand.

In prison, terrorists designed an organizational structure providing specific roles for each member, roles identical to what was just found in the UK; leaders, recruiters, enforcers, foot soldiers. The intelligence report also said that terrorists would operate their group in prison like a “brotherhood,” and that recruitment would thrive because they had a large “pool of vulnerable people” from which to draw.

However, in Dunleavy’s opinion, American prison and counter-terrorism authorities have handled these matters better than their counterparts in the UK:

The United States seems to have fared better curbing radical Islamic groups organizing in the prison system than our UK and EU counterparts. This may be due in part to the Correctional Intelligence Initiative program operated by the FBI’s Joint Terrorism Task Force (JTTF), which continues to build on the recommendations of the 2002 report.

If there is one shortcoming, it is in the area of post-release supervision of convicted terrorists.

As we have previously reported, more terrorists are being released from custody with no viable de-radicalization program or monitoring system in place.

Where they live or work, as well as any social media involvement after their release, needs to be strictly monitored. Any important intelligence gleaned from this should be shared across the board with participating agencies. International travel should also be restricted.

Usman Khan’s trajectory confirms Dunleavy’s uneasy concern about the “post-release supervision of convicted terrorists”. Is any form of deradicalization possible at all? It is no secret that hundreds of former Islamic State/Da’esh fighters may have returned or hope yet to return to their countries of origin in Europe:

Jürgen Stock, Interpol’s chief, who is also a criminologist and law enforcement officer from Germany, said: “We could soon be facing a second wave of other Islamic State linked or radicalised individuals that you might call Isis 2.0.”

“A lot of these are suspected terrorists or those who are linked to terrorist groups as supporters who are facing maybe two to five years in jail. Because they were not convicted of a concrete terrorist attack but only support for terrorist activities, their sentences are perhaps not so heavy.”

Many such fighters are already in custody under Turkish control. A recent report from Ankara indicates that the Islamist Turkish government is threatening to release them and send them into Europe. If that happens, handling such an influx could become an intense and possibly irresoluble headache for the prison, security, and counter-terrorism authorities everywhere.

In Part II, we shall examine what the Western states will have to do and should already be doing to quash this menace.

* * *

Postscript. Just as this article finished editing, a grim event, once more in London, took place in an eerie replica of Usman Khan’s November terrorist attack on London Bridge. On February 2, a young Muslim, Sudesh Amman, stabbed two passers-by in Streatham, a London district. Ten days earlier, he had, like Khan, been released from prison halfway through his sentence for terror offences in 2018. He too was shot dead by armed police, and in his case neither of his victims died.

Amman was one of the top five terrorist risk people in the country and was known still to possess extremist views, yet his parole board did not assess him before setting him free to go onto the street, take a knife from a shop, and attack two innocent people. This, despite the fact, as we shall see in part two, that the government had earlier announced plans to tighten up sentencing and end halfway release for terrorist prisoners.

Just A Little Sloppy Record-Keeping? The Pentagon’s $35 Trillion ‘Accounting Black Hole’

Over the past two weeks of coronavirus headlines and heightened global anxiety, along with impeachment coverage and after over the Super Bowl weekend Americans huddled in living rooms in blissful oblivion, a story which in more normal times would be front and center has gone largely unnoticed. To be sure, the Pentagon couldn’t be happier that this bombshell has taken a back burner in global headlines:

The Pentagon made $35 trillion in accounting adjustments last year alone— a total that’s larger than the entire U.S. economy and underscores the Defense Department’s continuing difficulty in balancing its books.

The latest estimate is up from $30.7 trillion in 2018 and $29 trillion in 2017, the first year adjustments were tracked in a concerted way, according to Pentagon figures and a lawmaker who’s pursued the accounting morass.

It sounds more appropriately news out of The Onion or Babylon Bee given this is *Trillions* and not just billions — though that itself would have been remarkable enough. Naturally, the first and only question we should start with is: how is this even possible?

After all, $35 trillion is about one-and-a-half times the size of the entire US economy. Not to mention that the figure easily dwarfs the GDP of the entire combined nations of the European continent. Consider too that the current actual US budge for defense-related funding is $738 billion.

“Within that $30 trillion is a lot of double, triple, and quadruple counting of the same money as it got moved between accounts,” Todd Harrison, a Pentagon budget expert with the Center for Strategic and International Studies, told Bloomberg in a recent report.

But are we really to believe that mere “combined errors, shorthand, and sloppy record-keeping by DoD accountants” — as another analyst was quoted as saying — can explain a $35 Trillion accounting black hole?

The Defense Department acknowledged that it failed its first-ever audit in 2018 and then again last year, when it reviewed $2.7 trillion in assets and $2.6 trillion in liabilities. While auditors found no evidence of fraud in the review of finances that Congress required, they flagged a laundry list of problems, including accounting adjustments.

With tax season now fast approaching, it’s not too comforting to know the Pentagon enjoys over half of all discretionary domestic spending for its global war machine in maintenance of our humble Republic Empire .

Bloomberg attempted to get a handle on it further in explaining, “The military services make adjustments, some automatic and some manual, on a monthly and quarterly basis, and those actions are consolidated by the Pentagon’s primary finance and accounting service and submitted to the Treasury.”

“There were 546,433 adjustments in fiscal 2017 and 562,568 in 2018, according to figures provided by Representative Jackie Speier, who asked the Government Accountability Office to investigate,” the report added.

Spokeswoman for the Pentagon’s inspector general, Dwrena Allen, downplayed what to most Americans will sound like the makings of an explosive scandal. “In layman’s terms, this means that the DoD made adjustments to accounting records without having documentation to support the need or amount for the adjustment,” she said.

“It means money that DoD moved from one part of the budget to another,” Clark explained to Task & Purpose. “So, like in your household budget: It would be like moving money from checking, to savings, to your 401K, to your credit card, and then back.”

However, $35 trillion is close to 50-times the size of the Pentagon’s 2019 budget, so that means every dollar the Defense Department received from Congress was moved up to 50 times before it was actually spent, Clark said.

“Trillions” explained away by a little benign neglect of simple documentation?

Of course, in the real world outside the halls of government and of largely unchecked power, a mere single trillion would be enough send people to jail. Here we’re talking $30+ trillion and it appears this gaping accounting black hole bigger that most of the world’s past and future economies will itself be memory holed and explained away as being but the minor errors of some DoD pencil-pushers, apparently.

“The brutal reality is that a predator doesn’t have to be in the same room, building, or even country to abuse a child. And that’s what they’re doing – subjecting children to psychological and sexual abuse.”

What can we do to protect America’s young people from sexual predators?

That’s the question I keep getting asked by people who, having read my article on the growing danger of young boys and girls (some as young as 9 years old) being bought and sold for sex, want to do something proactive to stop these monsters in their tracks.

It is estimated that the number of children who are at risk of being trafficked or have already been sold into the sex trade would fill 1300 school buses.

While those who seek to buy young children for sex come from all backgrounds, races, ages and work forces, they do have one thing in common: 99% of them are men.

This is not a problem with an easy fix.

That so many children continue to be victimized, brutalized and treated like human cargo is due to three things: one, a consumer demand that is increasingly lucrative for everyone involved—except the victims; two, a level of corruption so invasive on both a local and international scale that there is little hope of working through established channels for change; and three, an eerie silence from individuals who fail to speak out against such atrocities.

Sure, there are things that can be done to catch those who trade in young flesh: police need to do a better job of training, identifying and responding to these issues; communities and social services need to do a better job of protecting runaways, who are the primary targets of traffickers, and educating parents and young people about the dangers; legislators need to pass legislation aimed at prosecuting traffickers and “johns,” the buyers who drive the demand for sex slaves; and hotels need to stop enabling these traffickers, by providing them with rooms and cover for their dirty deeds.

However, these are reactive responses to a menace that grows more sophisticated by the day.

We need to be preemptive and proactive in our understanding of the threats and smarter and more sophisticated in our responses, as well.

What we are dealing with is a culture that is grooming these young children, especially young girls, to be preyed upon by men.

There are usually six stages to grooming by a sexual predator:friendship (targeting and gaining trust); relationship (filling the child’s needs); gauging the level of protection surrounding the child; exclusivity (isolating the child from others); sexualization (desensitizing the child to sex talk and activities); and abuse.

All of those screen devices being passed along to children at ever-younger ages? They have become the sexual predator’s primary means of gaining access to young people, and it’s primarily happening online. As The New York Times reports:

Indeed, video games such as Minecraft and Fortnite, social media apps such as TikTok and Instagram, and online chat forums have become “hunting grounds” for sexual predators.

One Bark investigator, Sloane Ryan, a 37-year-old woman who poses as an 11-year-old girl online in order to better understand predation and help those who are fighting it, wrote a chilling account of the kinds of solicitations she received after merely uploading a generic photo (of her 11-year-old self) to Instagram.

“By the end of two-and-a-half hours, I’ve had seven video calls, ignored another two dozen of them, text-chatted with 17 men (some who had messaged her before, gearing back up in hopes for more interaction), and seen the genitalia of 11 of those,” notes Ryan.

This is the new face of how predators are grooming young girls (and boys) to be trafficked, molested and raped. However, it starts much earlier, with a culture that has brainwashed itself into believing that sexual freedom amounts to a Super Bowl half-time show in which barely-clad women spend 20 minutes twerking, gyrating (some of it on a stripper pole) and showing off sexually provocative dance moves.

This is part and parcel of the pornification of American culture.

As commentator Dixie Laite writes for Bust magazine:

Sex sells. Madonna knew it when she crawled the VMA stage very much not “Like a Virgin”. Rihanna, Beyonce, Britney and countless others have climbed that ladder to fame… Last time I looked, we as a nation absolutely adored this so-called slutty behavior. I see people voting with their dollars and their attention to Playboy’s Bunnies, Victoria’s Secrets, strippers, people who dress like strippers, and girls who’ve gone wild.

This foray into porn culture—the increasing acceptability and pervasiveness of sexualized imagery in mainstream media—is where pop culture takes a dark turn. “Visual images and narratives of music videos clearly have more potential to form attitudes, values, or perceptions of social reality than does the music alone,” notes author Douglas A. Gentile in his book Media Violence and Children. In fact, music videos are among the worst culprits constantly bombarding young people today with sexual images and references.

Screen time has become the primary culprit for the oversexualization of young people.

As Jessica Bennett notes in “The Pornification of a Generation” for Newsweek:

“In a market that sells high heels for babies and thongs for tweens, it doesn’t take a genius to see that sex, if not porn, has invaded our lives. Whether we welcome it or not, television brings it into our living rooms and the Web brings it into our bedrooms… All it takes is one look at [social media] photos of teens to see examples—if they aren’t imitating porn they’ve actually seen, they’re imitating the porn-inspired images and poses they’ve absorbed elsewhere. Latex, corsets and stripper heels, once the fashion of porn stars, have made their way into middle and high school… Celebrities, too, have become amateur porn stars. They show up in sex tapes (Colin Farrell, Kim Kardashian), hire porn producers to shoot their videos (Britney Spears) or produce porn outright (Snoop Dogg). Actual porn stars and call girls, meanwhile, have become celebs. Ron Jeremy regularly takes cameos in movies and on TV, while adult star Jenna Jameson is a best-selling author.”

How we got to this place in time, where children are sexualized at an early age and trotted out as easy targets for all manner of predators is not really all that hard to decipher, but it requires a certain amount of candor.

First, there is nothing sexually liberating about young women—young girls—reducing themselves to little more than sex objects and prancing about like prostitutes.

Second, this is a dangerous game that can only end in tragic consequences: there are sexual predators out there only too eager to take advantage of any innuendo-laced sexual “invitations” being put out there, intentional or not.

Third, if it looks like porn, sounds like porn and imitates porn, it is porn, and it is devastating on every front, turning women into objects for male aggression.

Fourth, no matter what its champions might say about the First Amendment and women’s liberation, pornography in all its forms—whether overtly packaged as skin flicks and mags or more subtly disguised by pop culture as trendy music videos and precocious clothing—is about one thing only: money.

Fifth, parents: turn off your cell phones for a change and tune into what your kids are watching, reading, listening to, and whom they are emulating.

And finally, remember that the sexualization of young children is part of a larger continuum in America that runs the gamut from sexualized entertainment, the glorification of a pimp/ho culture, and a billion dollar sex industry built on the back of pornography, music, entertainment, etc., and ends with these same young people being bought and sold for sex. It is estimated that the porn industry brings in more money than Amazon, Microsoft, Google, Apple, and Yahoo.

That this issue continues to be treated with a shrug, especially by those who claim to care about the state of our freedoms, is not only surprising and unnerving but also dangerously oblivious.

Like so many of the evils in our midst, sex trafficking (and the sexualization of young people) is a cultural disease that is rooted in the American police state’s heart of darkness. It speaks to a sordid, far-reaching corruption that stretches from the highest seats of power (governmental and corporate) down to the most hidden corners and relies on our silence and our complicity to turn a blind eye to wrongdoing.

You don’t have to be a parent to care about what’s happening to our young people. Likewise, you shouldn’t have to subscribe to any particular political viewpoint to recognize and be alarmed by the authoritarian trajectory of the nation.

Those concerned about the emerging police state in America, which I detail in my book Battlefield America: The War on the American People, should be equally concerned about the sex trafficking of young girls (and boys) and the pornification of America: they are two sides of the same coin.

As Aldous Huxley explains in his introduction to Brave New World:

As political and economic freedom diminishes, sexual freedom tends compensatingly to increase. And the dictator (unless he needs cannon fodder and families with which to colonize empty or conquered territories) will do well to encourage that freedom. In conjunction with the freedom to daydream under the influence of dope and movies and the radio, it will help to reconcile his subjects to the servitude which is their fate.

States That Tax The Most Are Getting The Worst Results Per Dollar

Today in “more definitive proof that the government can’t spend your capital as well as you can” news, it should come as no surprise that states who spend less in taxes are getting better results, per dollar, than similarly sized states who collect far more in tax revenue.

At least that was the result of looking at the country’s four largest states: California, Texas, Florida and New York.

Aside from being the same size, the states differ greatly in politics and governance, the NY Post notes. California and New York are liberal hot beds dominated by Democrats who have put the nation’s highest and sixth highest marginal income tax rates.

Texas and Florida are the opposite: both states have been run by conservatives for years and offer the benefits of no income tax on workers while keeping spending on social programs much lower.

An analysis of these states reveals some stark differences, but mainly tells the tale that lower taxed states have excelled, on a per dollar basis, past those with heavy tax burdens in a number of areas.

Blue states show little ability to improve academic outcomes of their kids, while red states have been able to “foster more upward mobility and trust in government,” the Post writes.

New York spends about $23,000 per pupil on education – about twice the national average of $12,000. Florida and Texas spend about $9,000 per pupil. And the difference in outputs has been almost unnoticeable.

In 2017, the National Assessment of Educational Progress found that students in New York and Texas both scored around the national average in fourth and eighth grades, as did Floridians in eighth. Florida students in fourth grade scored above the national average, while California students in both grades scored below the national average.

In addition, minority students in Florida scored highest in the nation across the board. Black students scored 240 out of 500 on an average of the four tests used, which bests a 234 score average nationally. In New York, minority students scored above or around the national average of 236 for black students and 237 for hispanic students.

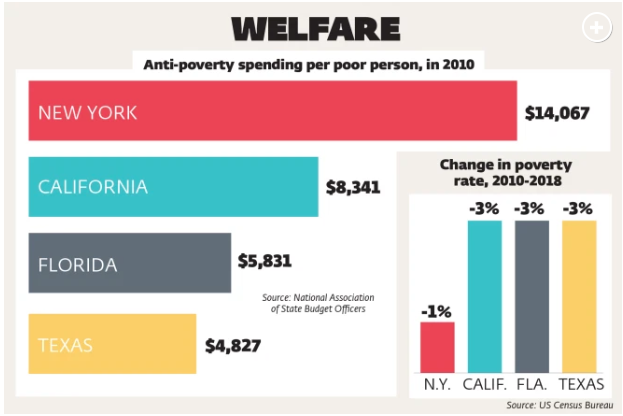

California and New York spend tons more on their anti-poverty programs than Texas and Florida. For instance, inclusive of Medicaid, California spent about $19,000 per person under the poverty line in 2017. New York spent over $21,000. Florida spent just $9,000 and Texas spent under $8,000.

But there’s no evidence that the extra spending is helping. The poverty rate fell 3% in California and 1.3% in New York from 2010 to 2018, while it fell 3% in Texas and 2.8% in Florida.

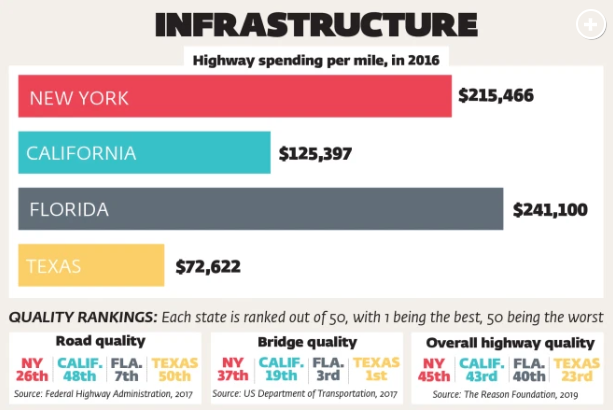

New York spends the most out of the four states on transportation, at $538 per capita. The national average is $476 while Florida, Texas and California spend $427, $399 and $339, respectively.

Per highway mile, Florida spends $241,000 and New York spends $215,000. This compares to $125,000 in California and $73,000 in Texas.

But the numbers find that there’s “no evidence” New York’s extra spending provides value to the people living there. Road quality in the state is ranked at 26th in the nation by the Federal Highway Administration, bridge quality is 37th and overall value of highways was 45th.

Florida is getting the better value for its dollar, yet again. Its roads rank 7th in the nation and its bridges rank 3rd. The Reason foundation has reported that overall, Texas taxpayers get the better value for their highways than the three other states.

Matt Gaetz Files Ethics Complaint, Criminal Referral Request Against Nancy Pelosi For Tearing Up SOTU Speech

Rep. Matt Gaetz (R-FL) has written a letter to the House Ethics Committee requesting an investigation into Speaker Nancy Pelosi’s decision to tear up a copy of President Trump’s State of the Union address, arguing that “Her unseemly behavior certainly warrants censure.”

Gaetz has also requested a criminal referral for Pelosi’s potential violation of 18 U.S. Code § 2071 (Concealment, removal, or mutilation of documents).

Pelosi, still steaming after House Democrats’ impeachment gambit only drove President Trump’s approval ratings to all time highs, sat through Trump’s Tuesday night address staring daggers into the back of Trump’s head and mumbling to herself – only to test, pre-rip, and then tear up her copy of Trump’s SOTU speech.

Here’s Pelosi testing to see if she could rip the speech before the speech even started. She was planning to do it from the start. pic.twitter.com/1gEMlYrNB7

According to Gaetz, President Trump delivered remarks “which received overwhelming (and frequently bipartisan) support,” that were an “uplifting celebration of the diversity of the American experience and the triumph of the American Spirit.”

Pelosi’s theatrics were “utterly dismissive of the President’s achievements, and, more importantly, the achievements of the American People.”

Gaetz argues that Pelosi’s actions appear to violate clauses 1 and 2 of House Rule XXIII, and does not “reflect creditably on the House,” or follow “the spirit and the letter of the Rules of the House.”

BREAKING: I’m filing an ethics complaint against @SpeakerPelosi for destroying @realDonaldTrump‘s State of the Union speech.

Her conduct was beneath the dignity of the House, and a potential violation of law (18 USC 2071).

US Army Developing Uniforms That Destroy Bioweapons In Minutes

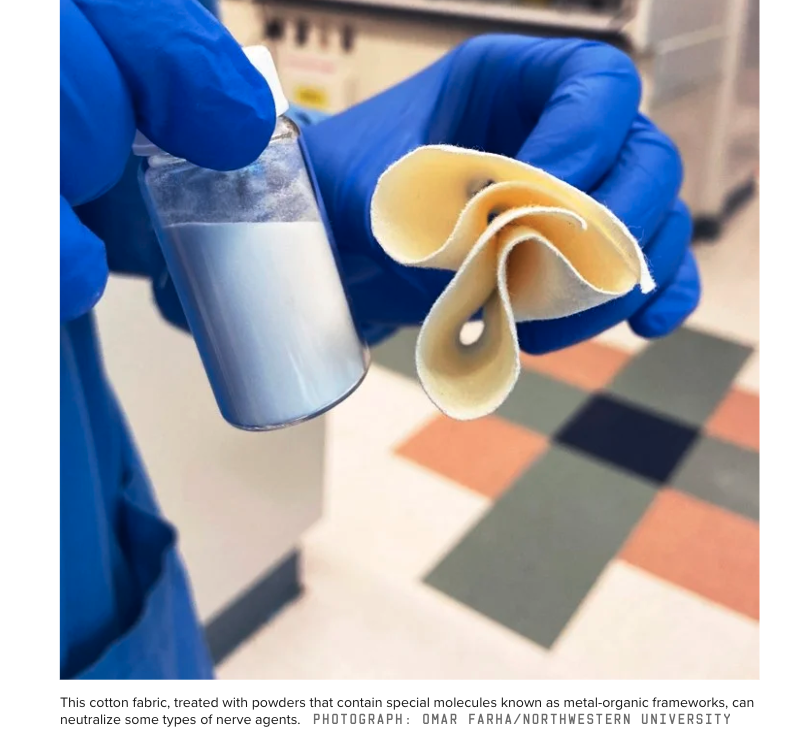

Chemists working with the US Army are developing new uniforms that can quickly break down toxic substances, protecting troops from bioweapons, according to Wired.

Omar Farha’s lab at Northwestern University is testing a fabric that can neutralize nerve agents.

The new fabric is part of a collaborative effort between the college and the Army, which might take upwards of a decade to test and then commissioned as the next-generation battle uniform.

The fabric can destroy nerve agents VX, soman, and sarin. These dangerous chemicals can be made in a Biosafety Level 4 laboratory (BSL-4), like the one found in Wuhan, China.

The Wired noted, the Army already has uniforms to protect troops from nerve agents, but there are no uniforms that can also destroy the toxins.

Jared DeCoste, a researcher with the Army who isn’t involved in the project, said the military has been searching for uniforms that can shield troops from bioweapons and, at the same time, destroy the chemicals.

According to Farha, the important ingredient in the new fabric is a crumpled crystalline molecule called MOF-808:

“This molecule essentially harvests water from ambient air. Water vapor likes to condense onto MOF-808 molecules because of their shape and chemical properties. When MOF-808 makes contact with a nerve agent, the water attached to the molecule breaks down the toxin, while zirconium atoms that recur throughout MOF-808’s crystal serve as the catalyst, accelerating the nerve agent’s breakdown. As long as the fabric is worn in a place where the humidity level is at least 30 percent, it can collect enough water to break down nerve agents in minutes.”

Dr. Francis Boyle, the man who drafted the Biological Weapons Act, recently said in an explosive interview that the coronavirus outbreak in Wuhan likely came from a BSL-4 in the city.

He believes the virus is potentially lethal and an offensive biological warfare weapon or dual-use biowarfare weapons agent genetically modified with a gain of function properties.

The threats of biological warfare in the 2020s is undoubtedly a concerning matter for the Army, perhaps that’s why next-generational suits to repel and neutralize toxins will be standard issue by the end of the decade.

The investor George Soros objects that Facebook is doing what the U.S. Government allows it to do, but he doesn’t object to the U.S. Government’s allowing it. Yet, he claims to be opposing the Republican Government of Donald Trump, while he demands that the leadership of Facebook be replaced — supposedly for violating a law that the Trump Administration maybe isn’t enforcing. Is Soros really that incoherent? Or is there an ulterior motive here?

“I repeat and reaffirm my accusation against Facebook under the leadership of Mr. Zuckerberg and Ms. Sandberg. They follow only one guiding principle: maximize profits irrespective of the consequences. One way or another, they should not be left in control of Facebook.”

He cited, for blame in this, Section 230 of the Communications Decency Act, which allows passive online media – media that exercise no editorial control over what their users post online – to be not responsible for, and not subject to lawsuits for, whatever is posted to their sites.*

Soros noted that Facebook is not censoring posts to its site in a way that will help Democratic candidates, but instead in a way that will help Republican candidates. He apparently wants censorship, but it must be his type of censorship, not theirs.

He is clear about his support for some sort of censorship. But is he proposing that the Government will somehow force this change from a Republican Facebook to a Democratic Facebook, or instead that Facebook’s stockholders will, somehow, do this — get rid of their founder and two top leaders? Soros doesn’t respect his readers enough to so much as even just touch on that basic question in his presentation — is the Government to get rid of Zuckerberg and Sandberg, or are the stockholders supposed to do it?

Soros is addressing his commentary only to fools who don’t care about what case he’s trying to persuade them to believe. If his article were, at all, serious, it would have been less holier-than-thou against businesses that supposedly adhere to “only one guiding principle: maximize profits irrespective of the consequences,” and it would have outlined a proposal — and not just asserted “One way or another, they should not be left in control of Facebook.” But why shouldn’t they? He really doesn’t say. He doesn’t cite even a single concrete example. He presents no case, at all.

He didn’t object that by Facebook’s doing any censorship at all, Facebook doesn’t actually fit into Section 230 of the Communications Decency Act and Facebook is instead serving as an online publisher (a member of the press) and therefore is supposed to be legally responsible for what is being posted to their site — responsible for it in just the same way that the New York Times and Washington Post and NBC, CBS, ABC, Fox News, CNN, and MSNBC, are responsible for what they publish (responsible, that is, to civil suits, but not to any criminal laws). Soros isn’t hiring lawyers to present such a case against Facebook, which would be a serious case to present, holding Facebook liable for any libels that it has published; he is instead trying to smear the leaders of Facebook, without supplying facts, or, really, any case, at all.

He is not objecting to the Trump Administration’s prejudicially granting this non-enforcement to Facebook, the publisher — the Trump Administration’s treating them as if they weren’t being publishers, but just passive information-providers; treating them as if Facebook weren’t selecting what to transmit and what not to transmit on their networks, to their audience.

(Facebook, and other online media such as Twitter, don’t even hide the fact that they exercise censorship, while they claim to be only “passive” media and thus protected by Section 230. Like I said: this case against Facebook would be serious, if it were brought, because these online platforms really do censor-out whatever they wish to censor-out.)

Why did Soros object to Facebook’s controllers, Mark Zuckerberg and Sheryl Sandberg, instead of object to Donald Trump — who is granting this prejudicial treatment, to that publisher (allowing it to be treated in accord with the Section 230 exemption)? Is it because Soros is too stupid to know better, or to understand the difference?

Soros knows enough to be expressing his viewpoint in a partisan manner, as a Democrat who spends tens of millions of dollars each election-cycle in order to support conservative Democrats against progressive Democrats.

And, then, in the general election, Soros supports conservative Democrats (such as that same conservative liberal Clinton) against sometimes even more conservative Republican Party nominees, for the given federal office. (The idea that Soros pumps about himself, that he’s progressive, is one big fat lie: he’s nothing of the sort.)

Why would he not be objecting to Trump here — the Republican who will soon be running against whomever the Democratic Party chooses to be its nominee?

The reason is that Trump isn’t really his target here: this is not the season during which the President will be chosen, but is instead the season in which each Party is to be selecting its nominee to then run against the other Parties’ nominees. And, since Soros is addressing, really (and only), fellow Democrats, his agenda could reasonably be viewed as being to affect whom they will be voting for in the present primaries.

In other words, George Soros wants as free a hand as possible, as a Democratic Party mega-donor, in order to determine whom the Democratic Party’s nominee will be. He wants Facebook to be censoring his way, not their way. Then, later, if that nominee suits his purposes, Soros will donate funds proportionately, to that Democratic Party nominee, against Donald Trump. Perhaps right now Soros is using the opinion-page of the Democratic Party’s New York Times in order to warn Facebook to avoid using its censorship so as to favor and oppose ‘the wrong’ Democratic Party candidates. And, maybe, that newspaper favors and opposes the same candidates that Soros does, and so perhaps that’s why they published his tripe here, rather than higher-quality submissions they could have chosen instead to publish.

Google, during the 2016 election-cycle, was slanting its ‘news’ to favor conservative Democrats against progressive Democrats, and then to favor the Democratic Party nominees against the Republican Party’s nominees, whereas Facebook was slanting its ‘news’ to favor Republican Party nominees against Democratic Party nominees. Twitter censors-out whatever neither Party wants the public to know,such as that Julian Assange is being tortured awaiting his extradition to the U.S. — for a trial that will likely never happen — all of these years of his imprisonment, lately in solitary confinement moreover, and never once being tried in a court of law, for anything, at all.

Since George Soros is a Democratic Party billionaire, he is objecting against Facebook instead of against Google. Similarly, Republican Party billionaires (and the ‘news’-media that they control) attack Google and other pro-Democratic-Party media.

Thus, Soros says:

“Facebook can post deliberately misleading or false statements by candidates for public office and others, and take no responsibility for them”

instead of:

“President Trump is not enforcing federal laws that hold publishers liable for lies they publish.”

So, Soros knows, and understands, a thing or two about propaganda. And, of course, he knows that Julian Assange is his enemy, just as much as Assange is, say, an enemy of Google’s Eric Schmidt, and of Cambridge Analytica’s Peter Thiel (who supported Trump).

This is just a game that virtually all of the billionaires play, against democracy itself. They want to control the country. Ever since around 1980, they have been accustomed to doing so.

* * *

* The U.S. Constitution, in its First Amendment, prohibited any type of governmentally imposed censorship but allowed censorship by members of the privately owned “press.” Section 230 was written to exclude passive online providers from being referred to as being “press” or a “publisher,” but it was poorly written, by lobbyists for corporations in the same category as Facebook and Google, and has yet to be revised by lobbyists for their print and broadcast competitors, who might define more precisely Section 230’s key phrase “interactive computer service” so as to state explicitly that only passive ones are being referred to by that phrase. Right now, even the New York Times online could conceivably qualify as being not a “publisher” and therefore not liable as publishers have been in the past. A corrupt government writes laws corruptly (such as Section 230 is) so that the laws reflect little else than the contending mega-corporate interests; and Section 230 is an example of this (as are most of our laws). With a big enough budget for its lawyering, any mega-corporation or association of large corporations can get the laws, in a corrupt country, written so as to serve its interests. Of course, such a country is no democracy. (But a corrupt country will have a corrupt press so that the public will think it’s a democracy.) Under such circumstances, judges make the final decision in particular cases. There already do exist some legal precedents for interpreting “interactive computer service” to apply only to passive ones. However, most billionaires are probably similar to Soros in wanting the internet to continue being used so as to propagandize the public — shape people’s attitudes and beliefs — instead of to inform the public (which entails no censorship whatsoever and is therefore overwhelmingly disfavored by billionaires and their corporations and their PACs and their lobbyists). Julian Assange is an example of the way a billionaires-controlled world treats leading anti-censorship activists. America is becoming a bastion of censorship, as one would expect of any dictatorship. This is certainly not what the people who wrote the U.S. Constitution had intended or even expected. After 9/11, it has become a seemingly permanent police-state. It’s what one would expect from a country that’s controlled by its billionaires. The 2020 U.S. elections should be about this problem, but, of course, are not.