Higher education is often considered the first rung in the ladder of success.

That’s why thousands of students flock to top-tier universities around the world, hoping to translate their degrees into financial outcomes. After all, a degree from specific institutions can often mean that a wealthy and secure future is in the books.

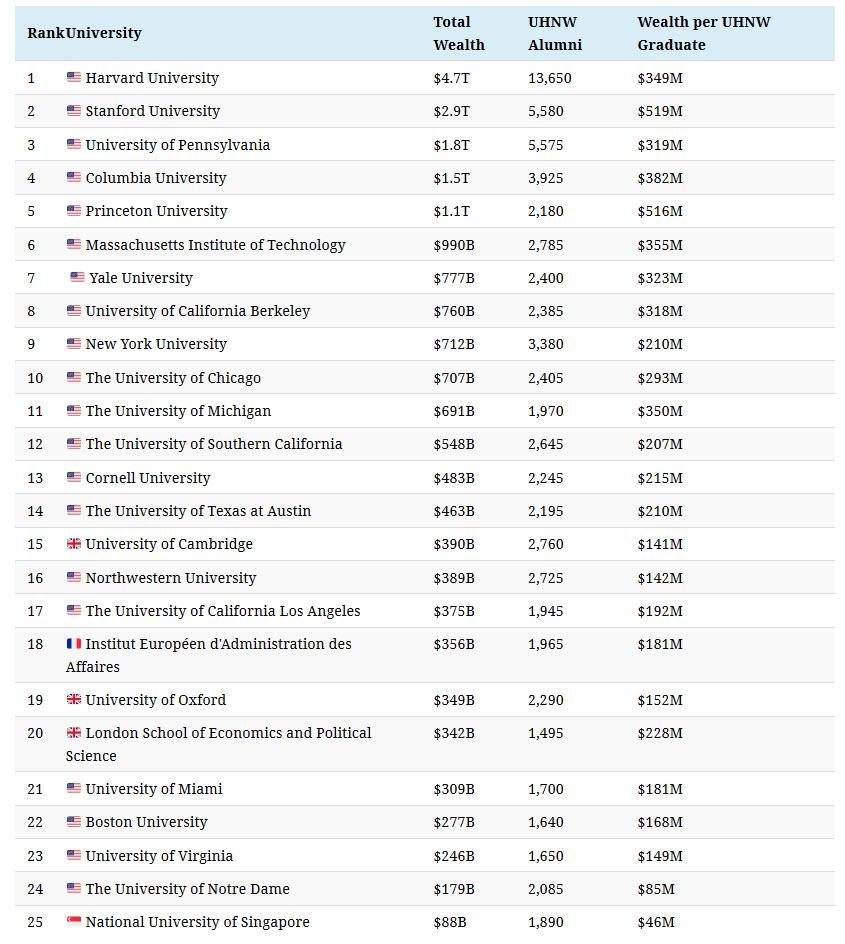

With a new fall term just around the corner, today’s chart relies on the third annual Wealth-X report ranking of global universities with the most ultra-high net worth (UHNW) alumni. We’ve also tracked their combined wealth, and how much each UHNW alumni makes on average.

Analyzing UHNW Riches

The Wealth-X database defines ultra-high net worth alumni as those who own at least $30 million in assets. In addition, the alumni figures are based on the actual known UHNW individuals from each university, then projected based on the sample size to predict total alumni within the global UHNW population.

One caveat to note is that both bachelor’s and master’s degree-holders have been considered, while UHNW individuals who may have attended more than one university have been counted twice. With that in mind, let’s dive in.

Upholding a Stellar Reputation

It’s immediately noticeable that a majority of universities on the list are located in the United States, with a high concentration on the East Coast—including the elite Ivy League.

Established in 1636, Harvard dwarfs all its Ivy League counterparts for the richest graduates. Its 13,650 UHNW alumni is double that of second-place Stanford (5,580 UHNW alumni), with twice the total wealth to boot.

One way that Harvard falls short is when average UHNW alumni wealth is considered in this chart, with Stanford beating it by a difference of $170 million per graduate. Regardless, it’s clear Harvard graduates go on to have a significant impact on the world. Notable alumni include political leaders such as former U.S. President Barack Obama, and billionaires such as Michael Bloomberg.

Interestingly, Princeton climbs the charts for total alumni wealth ($1.1 trillion), despite a lower UHNW alumni count of just over 2,000—but this also puts its wealth per graduate at a high of $516 million. Notable alumni from Princeton include Jeff Bezos and Steve Forbes. Meanwhile, Brown and Dartmouth are the only Ivy universities that don’t make the list at all.

Excellence Outside the U.S.

Zooming out, private universities dominate most of this list of richest graduates. In the United Kingdom, Cambridge, Oxford, and the London School of Economics and Political Science (LSE) have over 6,500 UHNW alumni combined. This represents a total of $1.08 trillion in wealth, an average of $174 million per UHNW grad.

Notable alumni and achievements from these institutions include:

Cambridge: Isaac Newton, Charles Darwin, Stephen Hawking

Oxford: 69 Nobel prize winners, Stephen Hawking, JRR Tolkien

LSE: 18 Nobel prize winners, including political leaders

*LSE’s label has been misrepresented in the original report as #26 instead of the actual #25.

Nearby in France, the graduate business school Institut Européen d’Administration des Affaires (INSEAD) has a total of 1,956 UHNW alumni and $356 billion in combined wealth—contributed by CEOs of companies like Credit Suisse, Royal Dutch Shell, Ericsson, and Lego.

It’s impressive that the National University of Singapore (NUS) enters the list, with 1,890 UHNW alumni and an average of $46.6 million to their name. Graduates from NUS have gone on to become Singaporean prime ministers and presidents, as well as high-ranking officials in the WHO and UN Security Council.

Here are the full statistics for the top 25 universities worldwide—does yours make the cut?

Where’s the Money, Really?

According to the report, a majority of UHNW alumni from these universities are “self-made” millionaires, who became successful through their own efforts rather than relying on family fortune or social status.

Of course, the name of a university is one step to climb on the ladder. What’s often glossed over is how steep the tuition fees at private institutions are, which can rack up significant student debt over time.

Graduates from Boston University, Columbia University, and Northwestern University relied the most on inheritance for their wealth, between 10-12%. A combination of both self-made and inherited wealth sources are also common for UHNW alumni—and it’s not a stretch to say that it helped them pay off debts before focusing on their wealth creation.

via ZeroHedge News https://ift.tt/34cVqoo Tyler Durden

The Dutch coalition government is reportedly considering a EUR 50 bn investment fund to support economic growth, to be financed by borrowing at negative rates

Many details are yet to be determined, but the Netherlands should have sufficient fiscal space to finance additional investment spending on this scale in the years ahead

This represents a notable shift from the debt-averse political consensus in the Netherlands and it could increase pressure on Germany to use fiscal policy to support growth.

News leaked last week that the Dutch coalition government is considering setting up a fund for investing in economic growth. Details are scarce, but media reports suggest a fund of up to €50 bn that would most likely be announced along with the rest of the Dutch budget in mid-September. It could be financed by borrowing from the market and spent on growth-friendly initiatives in areas such as infrastructure, innovation and education. Policy makers appear keen to capitalize on negative rates along the entire Dutch state yield curve.

Despite potential new borrowing, Dutch state debt levels would still be modest compared to other European countries and below the 60% Maastricht debt limit. The degree to which the fund actually results in additional investment and whether this will help growth, will depend on the governance around it.

From an international perspective, the idea of a government investment fund could impact the debate about the role of fiscal policy in supporting growth, in particular the special role of investment (in contrast to spending on (re-)current items). With limited space for additional ECB stimulus, the central bank has called on countries with available fiscal space to use their budget to support growth. The central bank’s policies have also made negative yields possible, giving governments an opportunity to finance such policies. The Netherlands has always been seen as squarely in the debt-averse camp, along with Germany. So this initiative could increase pressure on Germany to use its fiscal policy more actively, especially as the need for investment in infrastructure and digitalisation are seen as more acute there

Government investment fund: more questions than answers

The investment fund was initially reported by the Dutch newspaper De Telegraaf and later confirmed by other sources. The headline figure of EUR 50 bn remains indicative. Other details are also missing, probably because they remain to be worked out. But the main idea is clear: the government should make use of negative interest rates on Dutch government bonds to invest in things “such as” infrastructure and innovation. Apparently outlines of an idea were discussed between the coalition partners in the run-up to the state budget (to be released on 17 September) and were favourably received.

Since then there has been a widespread discussion on the topic in the Dutch media. The majority of responses have been supportive, based on the need to boost productivity growth in the Netherlands and the opportunity to borrow at negative rates. But there were also critics who felt that this was a distraction from the more immediate need to spend on income policies for the middle class or who cited earlier unsatisfactory experiences with a similar investment fund financed by natural gas income. Nevertheless, if the reports were a trial balloon to gauge the support for such a plan, there seems to be plenty of scope for the government to explore the idea further. And indeed, there is still much to be worked out and how the scheme is designed will be crucial for its impact and success. Open questions include the following …

What is the fund for?

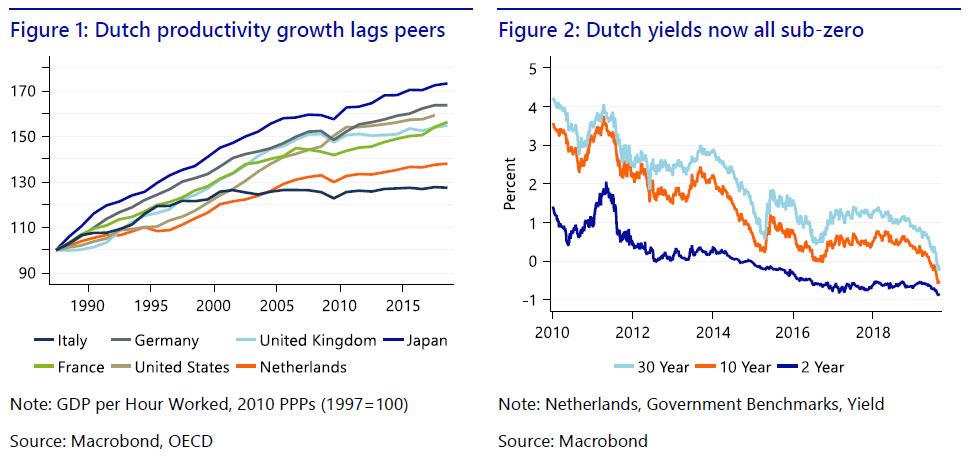

Generally reports suggest that the focus of the fund should be on supporting the long-term growth potential of the economy. This is a welcome goal, as productivity growth has been slow in developed countries in general and in the Netherlands in particular (Figure 1).

It is not quite clear what types of projects would be funded. Infrastructure, innovation, education and green energy have been named. Since the idea of a fund was reported, proposals like moving Schiphol, the national airport, into the North Sea (to circumvent spatial and environmental growth constraints at its current location) and building a high speed railway line to the north of the country have also been revived.

Should the fund be purely focussed on long-term investment or can it also play a role in stimulating the economy during a recession? Many press reports cited the possibility of an imminent recession as a motivation for the fund. However, the set of projects that make sense from a cyclical stimulus perspective – things like “shovel-ready” infrastructure projects – is smaller than the set that could support long-run growth.

How and when will it be financed?

The idea of the fund came shortly after the entire Dutch government yield curve, including the 30 year rate, moved below 0 percent (Figure 2). The possibility of borrowing money from the market and getting paid for the privilege has captured the imagination of the Dutch public and politicians alike. Some reports suggested the fund might be immediately stocked by borrowing from the market. Perhaps this reflects a sense that this opportunity to borrow at negative rates is a fleeting aberration. However, tasking the DSTA with prefunding this vehicle appears fanciful. First of all, it would undermine the Dutch State’s long-held policy of being a steady and reliable issuer. Furthermore, negative rates are a double edged sword. They may be an effective subsidy for borrowers, but are also a penalty for those looking to invest in liquid assets. As such, it makes better sense to raise capital as and when projects require financing.

Who will decide that the fund invests?

Should the “fund” be financed on-the-go then one might wonder, what’s the point? Dutch governments could easily invest in long-term growth projects using the regular budget. Establishing a separate fund should probably be seen as a commitment device to making the necessary investments, not just for the current governments but also for those in the future.

The Netherlands has an experience with a similar setup and several Dutch economists have cited this experience as a reason to be sceptical of this new idea. Natural gas revenues were supposed to be allocated separately from the rest of the budget on investments that would “strengthen the economic structure” of the Netherlands. However, it appears that the investment spending from the fund merely substituted for investment out of the regular budget. Furthermore, part of the fund was raided to finance regular state spending. It also lacked a strong strategic investment framework.

Without clear rules on what the new fund can spend its money on an who decides what counts as an appropriate investment, a repeat of these earlier experiences seems likely. An independent government agency with an investment spending mandate would be the most effective way to avoid this, but it is far from clear this will be politically feasible.

Fund unlikely to break the budget

Regardless of the exact structure, a fund of the scale proposed is likely to fit within the fiscal space the Dutch government has. We do expect that spending under the fund would fall under the EMU budget rules and that the Dutch government would be keen to stick to them. However, according official (CPB) estimates the EMU surplus will be 1.2% of GDP this year and the debt ratio will be 49% of GDP. Investments spending of EUR 50 bn, which is about 6% of GDP, could be easily accommodated if it were spent over several years and would still see debt stay below the 60% Maastricht threshold. Given the ongoing demand for safe-haven bonds in line with the elevated level of geopolitical tension, and with the ECB widely expected to soon wade in and further reduce the de facto supply of such bonds, an incremental funding programme for the proposed investment vehicle is also unlikely to weigh on spreads. As stated, we consider that a wholesale market-based prefunding of the fund, as speculated about in certain corners of the press, looks to be a flight of imagination.

Growth-effect depends on how wisely money is spent

Investment spending from a government fund like this could have both a short-term and a long-term growth impact.

In the short term, extra investment spending would boost GDP-growth directly and through a multiplier effect through private sector spending. The size of this effect depends on the state of the economy. Currently, the government is finding it difficult to implement its existing investment plans due to the tight labour market. However, as the economy weakens we expect unemployment to rise and there to be more space for this type of spending. More slack in the economy should also result in a stronger multiplier effect and reduce the risk of crowding out private sector investment. Indeed, if many of the risks facing the Dutch economy currently come to pass, the extra spending would be welcome stimulus.

The long term effect on growth (and thus indirectly on debt-sustainability) will depend on how wisely the government invests these funds. Investment in infrastructure, research and education could all benefit long-run economic growth. However, there are also strong cases to be made for investing in expanding the housing supply and in making growth more climate friendly. The social returns on such investments would justify their (negative) funding costs, but wouldn’t translate into higher growth of potential GDP.

Is this what the ECB had in mind?

The ECB has called on countries in the euro-zone with fiscal space to do more to stimulate growth. The ECB might thus welcome the plans from the Netherlands. However, it does not look like the Dutch government has classic stimulus measures in mind, that would boost aggregate demand in the short term. Not to mention, that the Netherlands is too small to influence overall Eurozone GDP enough to factor into the ECB’s calculus by itself.

It is also doubtful that the ECB’s call for more fiscal support to the economy has influenced Dutch politicians. Rather than seeing this as a question of fiscal-monetary policy coordination, another way to look at it would be to see it as part of the monetary policy transmission channel. The ECB has helped to create, at first low and now negative yields on Dutch government bonds through its negative deposit rate, its bond purchases and by stoking expectations of more easing to come. Due to deep-seated political preferences the Dutch government has so far not responded much to these incentives, but sub-zero rates are apparently a game-changer for Dutch politicians.

Pressure on Germany to invest more could increase

A Dutch investment fund would in itself not change much for the rest of the euro-zone. It could have an influence, however, on the debate regarding German fiscal policy. The Netherlands and Germany have always seen to be in the same club of countries that support conservative fiscal and monetary policy. An investment fund in the Netherlands could increase the pressure from other EU countries, the European Commission, the ECB and the IMF on Germany to do more. It could also play a role in the debate in Germany itself. Already there are signs that the political mood in Germany is shifting towards more investment (and possibly this has influenced the mood in the Netherlands as well). A long-term investment fund or program would arguably also be more politically palatable in Germany than straightforward stimulus. It would also be more welcome, given the consensus that Germany lags behind in digitalisation and needs more infrastructure investment. While from the perspective of the ECB and the euro area as a whole, coordinated investment across the currency union, targeting projects with the highest potential returns in regions with high unemployment, could be considered optimal policy. But that would require an even bigger shift in attitudes about fiscal policy.

via ZeroHedge News https://ift.tt/2UmgkNy Tyler Durden

The reason for persistent strength in the price of gold can be found in the changing relationship between time preference for monetary gold, and a new round of interest rate suppression for the dollar. Evidence mounts that the forthcoming recession is likely to be significant, even turning into a deep slump. Bullion bank traders are waking up to the possibility that dollar interest rates are going to zero and that pressure is likely to be put on the Fed to introduce negative rates. The laws of time preference tell us bullion banks must urgently cover their short bullion positions in anticipation of a dollar rate-induced permanent backwardation for gold, silver and across all commodities.

This article dissects the moving parts in this fascinating story.

Introduction

For some time now, I have maintained the wheels are likely to fall off the global economic wagon by the year-end. Furthermore, for many of my interlocutors, the recent rise in the gold price is just evidence of an impending cyclical crisis, anticipating and discounting the certain inflationary response by central banks. But in this, we are describing only surface evidence, not the underlying market reality.

In the combination of trade protectionism and an emerging credit crisis we face a problem upon which almost no formal research has been done, so it is not something that even far-thinking analysts have considered. To my knowledge, no mainstream economist has pointed out the lethal mix these two dynamics together present. Very few even recognise the existence of a credit cycle, traditionally called a trade or business cycle. Not even the great von Mises called it a cycle of credit, having identified and described it with great accuracy in his The Theory of Money and Credit, first published in 1912. But a spade must be called a spade: it is in its fundament a credit cycle.

There are many Austrian economists who fully understand the credit cycle. But to it we must add the destructive synergy of American trade policy aimed at China. Much economic research has been conducted on the causes of a credit cycle, trade cycle, business cycle, whatever it may be called. Much research has also been conducted on the economic consequences of trade tariffs. But nowhere is there to be found any research or commentary on the destructive power of combining the two.

Yet, these were precisely the conditions in October 1929, when Wall Street awoke to the certainty that Congress would vote in favour of the Smoot-Hawley Tariff Act at the end of that month. The shock of a 35% top to bottom fall in the Dow in October 1929 was only a prelude to an extended collapse following President Hoover signing it into law the following year. The economic research that followed the subsequent depression was conducted almost entirely by inflationists promoting reflation, so the destructive synergy between a credit crisis and trade protectionism has been ignored.

We cannot know the future with certainty, but we can point to the empirical evidence following Smoot-Hawley and draw an alarming parallel with today’s events. Thus alerted, we can then develop a convincing theoretical case for its repeat. Every week, reports of the global economy stalling now hit the headlines, drawing the parallel even closer. Yet, with equity markets close to all-time highs, little more than a mild recession, easily batted away with a little more monetary inflation, is the general expectation.

But our knowledge tells us there is almost certainly a large unanticipated shock ahead of us, and we should proceed in any analysis with that expectation. This article postulates how early evidence from the rising price of gold suggests the shock is closer than even perennially bearish analysts expect. We shall now take the inflationary consequences of an unexpected slump as a given in order to predict the changes in the relationship between physical gold and fiat dollars; a relationship that has for the last four decades led to a massive expansion of gold derivatives. To understand that relationship, and why it now appears to be reversing requires a working knowledge of time preference, the basis of interest; and more specifically the changing relationship of gold’s time preference to that of dollars.

Interest and time preference

One’s own bookcase provides the perfect illustration of time preference, which is the greater value of possession over non possession. There will be books bought on a whim which just clutter a bookshelf and have no value. Next time there’s a clear-out, they are destined for the charity shop: there’s no difference in time value, being worthless to the owner today and in the future.

Then there are the first editions, which have a commercial value. Books in this category will have a high current value to you compared with their non-possession. But perhaps the books with the highest personal value are the ones that have little value to anyone else: that battered copy of Wren’s Beau Geste, or the translation of Hoffmann’s Struwwelpeter read to you when you were a child. You may have even visited the museum in Frankfurt dedicated to Hoffmann and his famous book of moral tales for children. The value of these books in possession is far greater than their absence, even though you rarely open their pages.

This is the basis of time preference: the greater value placed on possession than non-possession. The books with sentimental value will have very little value to anyone else, other booklovers having their own favourites. Everyone’s time preferences are different. In economic terms, we express these varying values in terms of the difference between a current value in possession and the value of non-possession, but the certainty of repossession at a future time. The discounted value of the future possession is normally expressed as an interest rate on the monetary value today.

Assuming free market prices, in theory nearly everything of value has a time preference, an interest rate. That is, anything people value more in their immediate possession than the promise of ownership at some stage in the future. A future value, with very few exceptions, is always less than that of current ownership, and it is the difference between the two that is given to a current owner in one form or another to part with possession for a defined period of time.

The only examples that go against time preference are special cases. For example, an individual might forgo a decent salary today, in order to study so that he or she can earn more after passing a professional exam. In this case, the value of a current earnings stream is rejected in favour of potentially better prospects later. Or the philanthropist, who lends artworks for free to a public gallery so that a wider audience can appreciate them (but perhaps he does have a reward – to be thought of as a generous philanthropist and pillar of society).

The proxy for valuing time preference on goods is money, and the way it is normally expressed is as a money-rate of interest, often termed the originary rate. The originary rate of interest can be specific, assessed and applied in a single transaction such as obtaining the temporary use of a machine for a defined time. It can be a consolidated rate through the application of savings, reflecting the time preferences of the many goods and services whose possession is temporarily deferred by the saver.

Time preference is just the core consideration behind an interest rate. There will be other interest elements in addition, such as the trustworthiness and financial record of the borrower. But for the individual who has sacrificed the immediate satisfaction of spending the money put aside as savings, the time preference element will reflect the discounted future values of the goods and services that otherwise would have been purchased.

As well as time preferences reflecting baskets of specific goods and services, individuals will personally have different time preferences as well, as illustrated with the example of a personal library. But as is the case with any value, it is the marginal rate which is usually accepted as the market rate of interest, and therefore indicates the overall value of time preference within it. In addition, an interest rate must be greater than the sum of the originary rate and the compensation for all perceived lending risks, in order to create savings flows to feed investment.

This being the case, why is it that in financial markets, the forward price of something at a future date is usually higher than the present? The answer is simple: forward prices are not for possession, but for extending non-possession. Instead of being obliged to pay for possession today, a futures or forward price allows an individual to hang on to money for longer, rather than part with it now. And, assuming free markets set interest rates, with money’s time preference being greater than that of the average consumer item (in order to create savings flows referred to above), plus the addition for financial risk compensation, it should always be higher than the pure time preference applied to the underlying commodity, item or even just a title to ownership.

Therefore, higher prices for future deliveries of commodities and titles to ownership in financial markets are principally a reflection of money’s time preference, plus the risks associated with change of its ownership. To this should be offset the specific time-preference for individual commodities, but so long as they are in adequate supply, they will not be relatively significant compared with that of money.

This means the financial representation of time in a futures or forward contract in a properly functioning market is normally a positive cost. This condition is termed contango. We must also allow for the relative demand and supply characteristics of the underlying security between Date 1 and Date 2, which may temporarily lift a commodity’s time preference above that of money. If demand characteristics are such that the value of an immediate delivery overrides money’s time preference, then we have a backwardation. For example, there may be an acute shortage currently but supplies of the commodity in question are expected to be more plentiful at a future date. Backwardation is a temporary condition, and not the normal situation in financial markets.

To summarise so far, time preference tells us, except in a few specific cases, that the underlying or originary interest rate on money, which represents the time preference in all goods and services, must always be positive and include an extra margin to ensure savings flows occur. Furthermore, this is the basis for all pricing in financial markets for deferring delivery or settlement, which is called contango. In normal markets, backwardations are always unnatural and temporary, reflecting an excess of demand over supply for an earlier date over a later, but is never a general condition.

The reason it is vital to grasp the meaning and implications of time preference is to show that negative interest rates are unnatural, and do not accord with human action. It might not be obviously disruptive to financial markets when a central bank, whose currency is not the reserve currency, imposes a relatively minor negative rate on its commercial banks’ reserves. After all, a commercial bank will still charge its borrowers a positive rate, even though it may have to be imaginative when it comes to keeping depositors happy. But this is beginning to change, with both governments and large corporates now being able to issue bonds at negative rates. As we have seen from our discourse on time preference, this is a significant distortion from normality, indicating bond markets expect yet deeper negative rates in the currencies concerned.

In managing interest rates, the assumption central bankers make is that interest is the price of money. This is wrong for the reasons argued above. But instead of realising that deeper negative rates will not promote economic recovery in accordance with a cost of money approach to economic management, central banks’ economic models predict deeper negative rates are necessary in the event that a significant recession materialises.

However, this is new territory for policy makers, and they are naturally cautious about the prospect of deeper negative rates. Deeper negative interest rate policies will almost certainly be preceded or accompanied by quantitative easing, which allows a central bank to anchor term rates and government bond yields at the zero bound or even in negative territory. If the world faces a global recession, monetary expansion is likely to be the only course of action open to central banks, and deeper negative rates will become central to monetary policy if a recession persists.

With the expansionary phase of the credit cycle demonstrably running out of steam, history tells us that not only are we overdue a crisis in bank credit, but the tariff war between China and America will probably synergise with the cyclical downturn in the credit cycle to trigger a slump on a scale not seen since the early 1930s.

That being the case, under our assumptions for economic prospects, deeper negative rates will become unavoidable. The first to explore this dangerous territory are likely to be the ECB, the Swiss National Bank and the Bank of Japan. So far, lending rates at the Fed and the Bank of England are still in positive territory, but faced with an economic slump, that may not persist. The Fed’s interest rate is particularly important, because international financial markets price everything in dollars. And unless the Fed is prepared to see a dollar being strengthened by deepening negative rates elsewhere, the Fed may have little option but to follow.

If the Fed introduces negative dollar rates, then distortions of time preference will take a catastrophic turn. All financial markets will move into backwardation, reflecting negative rates imposed on dollars. Remember, the only conditions where backwardation can theoretically exist in free markets are when there is a shortage of a commodity for earlier settlement than for a later one. Yet here are backwardation conditions being imposed from the money side. It leads us to one conclusion: if negative rates for the dollar are imposed on financial markets, they will almost certainly lead to a flight out of the dollar where deposits become taxed with negative rates, not into other currencies, but into all commodities and future claims upon them. The current situation, where since the 1980s derivatives have inflated commodity supply, thereby suppressing prices, will be reversed. The purchasing power of dollars will be undermined by an attempted flight out of money. And it is unlikely to be long before the difference between negative time preferences between dollars and mildly positive ones for everyday items promotes a similar flight out of retail bank deposits.

That is the black and white of it. But there is a grey area of close to zero rates, when they are less than the implied rate of interest on gold, because of its time preference. Here it should be noted that gold’s interest rate when sterling was on the gold standard generally varied between two and four per cent, using the yield on British Consols as proxy. The Fed fund rate is already testing the lower boundary for monetary gold’s historic time preference, and markets are now expecting the FFR to go lower still.

Negative dollar interest rates and gold

This leads us to consider how a negative dollar interest rate will affect the price of gold. Gold is different from other commodities, because it is also a medium of exchange. And while it may not be commonly used as such in capital markets, it is widely retained by central banks and diverse parties as a monetary store of value.

Gold has a monetary time preference of its own, in accordance with time preference theory. And when gold was money, expressed as such through money substitutes, we know from the British experience in the nineteenth century, gold’s time preference usually held above two per cent, and that was still roughly the case reflected in gold’s lease rate since the 1980s.

In the 1980s gold was increasingly used as the collateral for a carry trade, leading to an explosion in business for the London bullion market. The underlying position was that central banks had accumulated bullion as part of their monetary reserves, and the gold price was generally falling. As bullish conditions died, gold’s time preference fell. Central banks and government treasury departments added to this trend, being prepared to lease their gold in large quantities to specialist banks in the bullion market.

At that time, a bullion bank could lease gold from a central bank and use it as collateral to invest in US Treasury bills. Gold’s time preference was reflected in a lease rate of typically 1.5-2% (though there were some spikes to 3-5%). Lease rates rhymed with evidence of gold’s originary rate established in the nineteenth century.

Meanwhile, 6-month UST bills yielded about 6% or more, giving bullion banks a fat profit over the lease rate. While figures were never published, Frank Veneroso, at that time a leading independent gold analyst, gave a speech in Lima in 2002 estimating central bank gold leases and swaps were between 10,000 and 15,000 tonnes. In other words, up to half of all central bank gold was out on lease or swapped.

Since those days, the London forward market has continued to grow. Bullion banks extended their operations to offer bullion accounts for wealthier individuals around the world, almost entirely on an unallocated basis. Unallocated accounts allow a bullion bank to own the gold deposited with it and to leverage its use as collateral for carry trades and other opportunities of interest rate arbitrage. This market became so developed that insiders have postulated that for every ounce of physical bullion in the possession of bullion banks there could be a hundred of paper liabilities.

We have no way of knowing the true level of paper gold leverage today. A working assumption that actual gearing is closer to between ten or twenty times seems more realistic, given Bank for International Settlements statistics of OTC swaps and forwards and LBMA vaulting statistics, allowing for ETF and other custody holdings, segregated from bullion bank ownership. To this must be added the banks’ unallocated customer account liabilities which go unrecorded. In any event, we can be certain that in recent decades a positive gold lease rate led to a substantial systemic uncovered position, likely to be still institutionalised, given the evidence from the LBMA’s daily clearing statistics.

The dollar interest rate that matters today is the wholesale market rate, USD LIBOR of a term that matches a gold lease. At the time of writing, 12-month USD LIBOR shows at 1.949%. The gold 12-month forward rate is roughly the same, implying the lease rate is zero. Clearly, with gold lease rates reflecting no time preference for gold, its supply into wholesale markets is being severely restricted. Look at it from a central bank’s point of view: if a lease is coming due, there is no incentive to renew it, particularly given the unquantifiable counterparty and systemic risks that may arise in the current global economic climate.

We can conclude that the basis for highly geared interest rate arbitrage by borrowing gold is running into a brick wall. Not only is there no incentive for lessors but also there is also a diminishing appetite for lessees, because the opportunities are vanishing. Synthetic gold liabilities are being gradually reduced, not only by ceasing the creation of new obligations, but by buying bullion to cover existing ones. This will have been particularly the case when the USD yield curve began to invert in recent months (itself a backwardation of time preference), and was the surface reason, therefore, that the gold price moved rapidly from under $1200 to over $1500.

Bullion banks are now faced with the prospect that the Fed will reduce interest rates to zero again, even without a systemic crisis such as Lehman. Traders, who are not often deeply analytical, will almost certainly link gold’s move in the wake of the Lehman crisis, once dollar liquidity concerns subsided, from under $750 to over $1900, with dollar rates being suppressed at the zero bound. If rates return there and LIBOR remains positive, that will be a reflection of systemic risk, not time preference. Meanwhile, gold’s time preference will almost certainly be increasing as markets attempt to discount a new wave of base money expansion when the Fed attempts to stabilise the US economy and manage government finances.

Bullion bank traders can see therefore, the day has arrived when gold’s time preference exceeds that of the dollar by an increasing margin. Furthermore, there is the growing threat of negative dollar rates, as economic conditions deteriorate. Putting other considerations aside, the switch in time preferences suggests a bullion bank’s future trading strategy should be the polar opposite of their current position. Instead of holding a small stock of gold to finance a large dollar position, logically they should maintain a small reserve of dollars to finance a larger position in physical gold.

It is for this reason that not only is the gold price rising, but is likely to continue to rise, appearing to defy all expectations. It is impossible to quantify the extent to which the gold price will rise as the bullion banks scramble to unwind or even reverse their habitual short positions, but if there is a surprise it is likely to be on the upside.

The consequences

As well as being modified by its specific supply and demand conditions, Gold’s time preference is essentially for its moneyness, represented by its use as a medium of exchange and store of value. The moneyness aspect links it to its exchange value for all commodities, and it is this aspect of gold’s qualities that should warn us that a backwardation in gold, emanating from negative dollar interest rates, will herald a general backwardation in commodities as well.

We must not forget that markets anticipate events where they can, so with a recession threatening to turn into a slump and with a looming credit crisis in the wings the prospect of negative rates will be increasingly priced into the relationship between commodities and fiat dollars. Assuming economic prospects darken because of the coincidence of American tariffs and the emerging crisis stage of the credit cycle, it will be check-mate for central banks. They were never appointed nor are they technically equipped to save the currency at the expense of widespread bankruptcies, not just in the private sector, but of their governments as well. And that is what markets will be faced with.

The current situation has striking similarities with the 1930s, and the prospects for the global economy are driven by the same broad factors. With the gold standard then and not now the price effects are already showing differences. Nor was there a bubble of hundreds of trillions of outstanding derivatives then as there are today. This time, the monetary sins since the ending of the Bretton Woods agreement seem set to come home to roost all of a sudden, even if dollar rates are lowered towards zero and only stay there. But if they go negative and the more below zero that they go, the greater the backwardation on the whole commodity complex. The more rapidly commodities will be bought so the dollar, taxed with negative rates can be sold, and the quicker market actors will devalue the currency.

With all other fiat currencies referenced to the dollar, it will mark the start of a process that is likely to collapse the entire fiat currency system. Bullion banks which are too slow to recognise the change and have not shut down their gold obligations will be forced to steal their customers allocated gold, or go to the wall, adding to the disruption. All commodity derivatives will face a period of rapid contraction of open interest, in lockstep or one pace behind those of gold.

Instead of central banks stabilising the system by monetary easing, the easing itself will guarantee the crisis. The development of a problem in gold markets, driving the gold price rapidly higher while some banks are caught napping, is likely to anticipate a wider financial and systemic crisis. Therefore, with gold’s sudden move higher coupled with its persistent strength we can reasonably certain that we are seeing the start of the dismantling of the dollar-based monetary system, and that gold has much further to go.

via ZeroHedge News https://ift.tt/2Zsm1PI Tyler Durden

Protesters in Hong Kong returned to the streets in what Bloomberg has called “one of the city’s most violent days in its 13th weekend of social unrest,” after several top organizers were arrested and then released, including Joshua Wong, Agnes Chow and Andy Chan.

Hong Kong police fired tear gas and sprayed protesters with blue dye from pepper-spray filled water cannons, while charging other protesters with shields and batons.

Tens of thousands participated in an unauthorized demonstration – many of whom threw objects and gasoline bombs over barriers at the government’s headquarters. After initially retreating in response to the crowd control measures, protesters returned to a nearby suburb and set fire to a wall on Hennessy Road in the city’s Wan Chai district.

While others marched back and forth elsewhere in the city, a large crowd wearing helmets and gas masks gathered outside the city government building. Some approached barriers that had been set up to keep protesters away and appeared to throw objects at the police on the other side. Others shone laser lights at the officers.

Police fired tear gas from the other side of the barriers, then brought out a water cannon truck that fired regular water and then colored water at the protesters, staining them and nearby journalists and leaving blue puddles in the street. –AP

Several people were arrested and tossed into police vans.

“Violent protesters continue to throw corrosives and petrol bombs on Central Government Complex, Legislative Council Complex and Police Headquarters,” said the police in a statement. “Such acts pose a serious threat to everyone at the scene and breach public peace.”

TEAR GAS: Police fire tear gas at #antiELAB protesters outside Hong Kong’s Legislative Council offices#HongKongProtests#香港

Protesters in Hong Kong returned to the streets in what Bloomberg has called “one of the city’s most violent days in its 13th weekend of social unrest,” after several top organizers were arrested, including Joshua Wong, Agnes Chow and Andy Chan. Hong Kong police fired tear gas and sprayed protesters with blue dye from pepper-spray filled water cannons, while charging other protesters with shields and batons. Water cannons fired blue dye pic.twitter.com/U8YAR1PsrQ — Tiffany May (@nytmay) August 31, 2019 Tens of thousands participated in an unauthorized demonstration – many of whom threw objects and gasoline bombs over barriers at the government’s headquarters. After initially retreating in response to the crowd control measures, protesters returned to a nearby suburb and set fire to a wall on Hennessy Road in the city’s Wan Chai district. this fire has gotten much bigger after 20 minutes. the street is full of dark smoke. #hongkongprotests#HongKong Clashes Escalate as Water Cannons, Firebombs Are Used https://t.co/JtIZo9EhGJ @bpolitics pic.twitter.com/pxdhcV0iRc — Fion Li (@fion_li) August 31, 2019 While others marched back and forth elsewhere in the city, a large crowd wearing helmets and gas masks gathered outside the city government building. Some approached barriers that had been set up to keep protesters away and appeared to throw objects at the police on the other side. Others shone laser lights at the officers. Police fired tear gas from the other side of the barriers, then brought out a water cannon truck that fired regular water and then colored water at the protesters, staining them and nearby journalists and leaving blue puddles in the street. -AP #HongKong police used water cannons to disperse rioters near Causeway Bay. The water contains pepper. pic.twitter.com/A0aSgzTTea — Global Times (@globaltimesnews) August 31, 2019 The protesters were undeterred. protesters aren’t deterred by rounds of tear gas outside Sogo department store at all. what a scene in causeway bay. #hongkongprotests#HongKong Clashes Escalate as Water Cannons, Firebombs Are Used https://t.co/JtIZo9EhGJ @bpolitics pic.twitter.com/SOPyI4ZIzu — Fion Li (@fion_li) August 31, 2019 Several people were arrested and tossed into police vans. “Violent protesters continue to throw corrosives and petrol bombs on Central Government Complex, Legislative Council Complex and Police Headquarters,” said the police in a statement. “Such acts pose a serious threat to everyone at the scene and breach public peace.” TEAR GAS: Police fire tear gas at #antiELAB protesters outside Hong Kong’s Legislative Council offices#HongKongProtests #香港 More @business: https://t.co/MmE4GkqhtD pic.twitter.com/9ZnKPDCTUA — Bloomberg TicToc (@tictoc) August 31, 2019 Protesters asked US President Donald Trump to take action and help the activists, who originally took to the streets to protest a controversial extradition bill which would have allowed China to bring suspects to the mainland to face trial in PRC courts. This #antiELAB protester tells us why he’s urging Trump to take action on #HongKongProtests #香港 More @business: https://t.co/6KN3YO371w pic.twitter.com/55ZzVNpdqW — Bloomberg TicToc (@tictoc) August 31, 2019 Acting on orders from Beijing, Hong Kong rejected an application by the Civil Human Rights Front for a march to the Chinese government office. While previous marches have begun peacefully, police say that they have increasingly devolved into chaos and violence towards the end.

Protesters asked US President Donald Trump to take action and help the activists, who originally took to the streets to protest a controversial extradition bill which would have allowed China to bring suspects to the mainland to face trial in PRC courts.

Acting on orders from Beijing, Hong Kong rejected an application by the Civil Human Rights Front for a march to the Chinese government office. While previous marches have begun peacefully, police say that they have increasingly devolved into chaos and violence towards the end.

via ZeroHedge News https://ift.tt/32gEyeB Tyler Durden

Recent unprecedented airstrikes on Iraq widely believed to have been carried out by either Israeli drones or stealth jets have been acknowledged by Prime Minister Benjamin Netanyahu, who on Friday gave belated confirmation that the Israeli military has been active there.

He said during a Facebook live stream event to political supports that “I am doing everything to defend our nation’s security from all directions: in the north facing Lebanon and Hezbollah, in Syria facing Iran and Hezbollah, unfortunately in Iraq as well facing Iran. We are surrounded by radical Islam led by Iran.”

Image source: The Times of Israel

Over the past six weeks there’s been three significant airstrikes on Iraqi paramilitary forces bases — at least one of which US officials have confirmed Israeli responsibility for. All of them targeted Iran-backed Shia paramilitary units.

The ‘mystery’ attacks, two of which came in August and one in July, have renewed calls from Iraqi parliament for a complete US troops withdrawal from the country, especially given the demise of the Islamic State and now with no official justification for American forces to be there.

The political and diplomatic firestorm resulting from the Israeli strikes and violations of sovereign Iraqi airspace have resulted in an awkward Pentagon statement saying the US had no role or foreknowledge of the attacks; however the statement stopped short of naming Israel or alleging who was behind them.

AP image of one of the recent airstrikes on an Iraqi munitions depot and paramilitary base.

Last week while on a state visit to Kiev, Netanyahu told reporters, “Iran has no immunity, anywhere”. He was responding to a specific question about the mystery attacks on Iraq.

“We will act — and currently are acting — against them, wherever it is necessary,” he declared.

via ZeroHedge News https://ift.tt/32hwSZx Tyler Durden

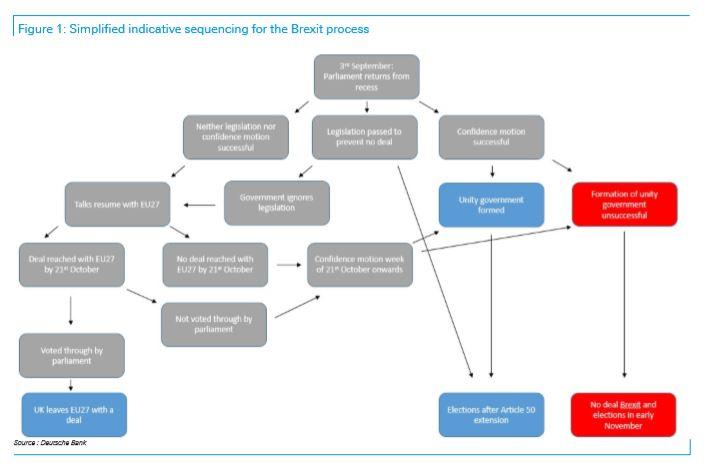

MPs who oppose a no-deal Brexit have joined together across party lines to try and stop Prime Minister Boris Johnson from ‘proroguing’ (a fancy term for suspending) Parliament. And as several legal challenges to Johnson’s plan make their way through British courts, Wall Street analysts are trying to parse the most likely outcomes.

One team of analysts at Deutsche Bank, who have been closely following the increasingly convoluted Brexit process for more than a year, has updated their odds for various Brexit outcomes, along with a “simplified” flow chart that is almost comical.

According to the latest ‘Brexit Update’, entitled “Constitutional Warfare,” the team, led by Macro Strategist Oliver Harvey, examined several potentialities for how the Brexit process might play out between now and ‘Brexit Day’ (Oct. 31).

Should all of the legal challenges to proroguing fail, MPs could opt to pursue a vote of no confidence in the government, or legislation to prohibit a ‘no deal’ exit. But if the past is any guide, the legislative approach would likely take too long, leaving the motion of no confidence and the formation of a government of national unity as the more likely option.

But an all-out rebellion against Johnson carries its own risks. For example, picking a leader for a national unity government could become a serious sticking point, as anti-no-deal Tories would vehemently oppose installing Labour leader Jeremy Corbyn as interim prime minister.

Already, several opposition MPs have ruled out supporting Corbyn as interim Prime Minister, leaving the question open as to who could lead the interim government. And there is also disagreement about whether the interim government should request an Article 50 extension from the EU27, as well as whether the UK should seek to revoke Article 50 altogether, effectively cancelling Brexit.

While most observers have effectively given up on the possibility that the withdrawal agreement might be renegotiated, DB believes there’s still a chance. “In our view, there is room for compromise on the backstop. The EU27 would be willing to entertain additional guarantees concerning the backstop, including possibly a time limit,” the analysts wrote.

However,if Johnson remains in power, the political consequences for a last-minute compromise with the EU27 on the backstop are clear. Should Johnson do a 180-degree turn on the backstop, he faces the prospect of possible defections to the Brexit Party from his own MPs, raising the prospects of another general election where the conservatives lose a sizable number of MPs to the BP, led by former UKIP leader and Brexit architect Nigel Farage.

Circling back to the odds of various outcomes mentioned above, the breakdown looks something like this:

Successful no confidence motion before 10th September or in late October: 50% probability.

Of which, unity government formed, followed by elections: 30% probability.

Of which, no unity government formed, followed by no deal Brexit: 20% probability.

Johnson administration completes a no deal Brexit on 31st October followed by snap election: 30% probability.

Johnson administration completes successful renegotiation with EU27 and ratifies Withdrawal Agreement by end October: 10% probability.

Parliament passes legislation to prevent no deal and Johnson government requests Article 50 extension: 5% probability.

Parliament passes legislation to prevent no deal and Johnson government calls election before Oct. 31: 5% probability.

When it comes to what the market will be focused on in the near term, that will depend on what anti-no-deal MPs do next week: That is, whether they decide to try and legislate away the prospects for ‘no deal’, as MPs tried to do under Theresa May or whether they opt for a no confidence motion.

If MPs successfully pass legislation seeking to prohibit a ‘no deal’ exit, the ball will be back in the government’s court, the DB analysts wrote. Johnson could choose to ignore the legislation – in which case MPs could opt for the no confidence motion and unity government route.

But there’s always the possibility that Johnson might succeed in negotiating a new deal with the EU. After all, as we’ve explained in the past, despite the EU’s insistence that the backstop is a non-negotiable part of the withdrawal agreement, the fact remains that it is completely unenforceable. By insisting that it be discarded, Johnson has effectively called Brussels’ bluff. If they finally acquiesce, Johnson just might walk away with the ‘holy grail’ of Brexit talks: a reworked withdrawal agreement that he could sell to Parliament.

via ZeroHedge News https://ift.tt/30NU1CH Tyler Durden

According to the MBA, the benchmark 30-year fixed mortgage rate broke below the 4% level in August, repeating what’s occurred three other times since 2012; in the first two episodes, purchase applications jumped by double-digits while in the third and current, activity slowed

Consumer expectations for lower interest rates spiked to a ten-year high in August; though falling rates have flowed through to a bump in new and existing home sales, the lack of urgency communicated in falling rate expectations will likely pressure housing activity

In Q2, ‘tappable’ home equity rose to a record $6.3T suggesting refinancing activity, up 167% over the last year, should continue to benefit; while refinancing bolsters consumption, a six-month low in perceived job availability and the trade war could crimp home sales

“Something is rotten in the state of Denmark,” is one of the most recognizable lines of all time. What’s key is that Shakespeare wrote this line into Hamlet, but it was not spoken by Hamlet. Marcellus said it to Horatio after the ghost of Hamlet’s father appeared and Hamlet exited stage left with his dear old floating dad. The iconic phrase called out political corruption, a subtlety that high school students must glean from their required reading. Or, if you prefer the obvious, it flags something that’s gone awry.

Today, something really is negative in the State of Denmark. As per this CNBC headline: “Danish bank offers mortgages with negative 0.5% interest rates – here’s why that’s not necessarily a good thing.” On Monday, August 5, Jyske Bank A/S, Denmark’s third-largest bank, announced that big carrot on a 10-year mortgage. Banks offering negative mortgages are willing to take a smaller loss compared to lending at higher interest rates where they risk less creditworthy borrowers that may not be able to pay them back in the future.

The good news? Something is positive in the State of America. Positive mortgage rates are still all the rage in the good ole U.S. of A. That doesn’t make lenders any less nervous. According to the latest weekly report from the Mortgage Bankers Association (MBA), in August, the benchmark 30-year fixed rate made its fourth foray into sub-4% territory. The only three other periods where 30-year mortgages dabbled in 3-handles occurred from May 2012 to May 2013, January 2015 to April 2015 and February 2016 to October 2016.

Was ‘3’ a magic number for mortgage brokers? In the first two instances, mortgage loan applications to purchase homes ignited, growing by double digits on a year-over-year basis. In the third episode, growth slowed from double digits to single digits.

The jury is still out on the here and now. We fear the law of diminishing returns is at play. Over the last three weeks, purchase applications have slowed by more than 5% even as mortgage rates fell from 4.01% to 3.94%.

We know this short span does not constitute a trend, but homebuyers might be holding out for even lower rates. As you can see above, in August, consumer expectations for lower interest spiked to a ten-year high. Why lock in today when you’ll get “paid” to wait for an even lower rate?

This lack of urgency implies disappointing home sales. To that end, through July, we’ve had three consecutive misses in new home sales. Despite this, new home sales are still up 13% thus far this year. Meanwhile, existing home sales broke their losing streak, rising by 0.6% over the prior year for the first time since February 2018.

Pending home sales’ track record has been more mixed in recent months and we’ll know more this morning with the release of July’s data. For context, commitments to buy homes have risen by a tenth since bottoming in December 2018.

These developments smell like a turning point. Enter Richard Curtin’s take on consumer interest rate expectations from the August University of Michigan consumer survey:

“The main takeaway for consumers from the first cut in interest rates in a decade was to increase apprehensions about a possible recession. Consumers concluded, following the Fed’s lead, that they may need to reduce spending in anticipation of a potential recession. Falling interest rates have long been associated with the start of recessions.”

The silver lining for lenders and households alike will be refinancing. Fresh data from Black Knight finds that the equity homeowners can pull from their homes rose by $355 billion to a record $6.3 trillion in the second quarter, a quarter more than the mid-2006 $5 trillion prior peak. The money to cushion household budgets as the economy slows is there for the taking — of the 45 million with excess equity, half have mortgage rates north of 4.25%. Little wonder, refinancing activity is 167% above its year ago level.

While this will help boost consumption, it’s new digs that drive the economy. With households’ perceptions of job availability at a six-month low, the risk is rising that home purchases will be postponed despite falling mortgage rates, frustrating policymakers at the Federal Reserve. With rates so low, and precious little in the way of easing capacity at the Fed, re-booting residential real estate could prove futile in the current easing cycle.

That brings us back to what is rotten in the State of America. What started here – the trade war – has already transitioned into rising costs among employers. As these drag on topline growth, labor cost cuts will increasingly be in focus threatening to enflame households’ growing anxiety about the sky-high expense of putting a roof over their head.

via ZeroHedge News https://ift.tt/2HBlWOO Tyler Durden

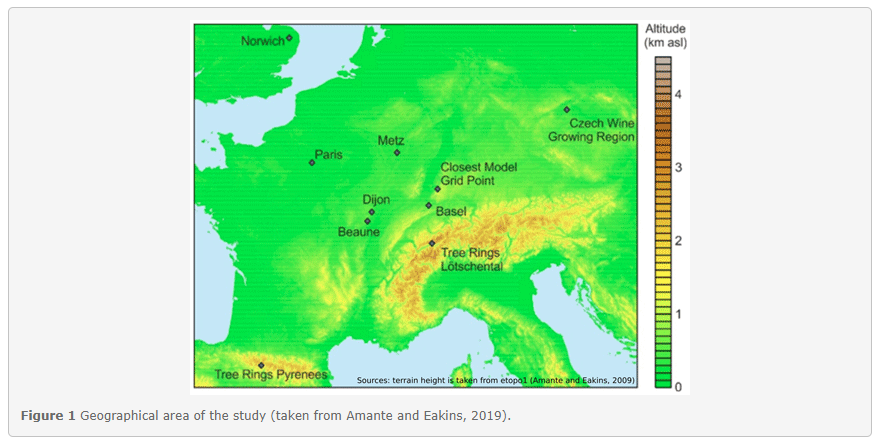

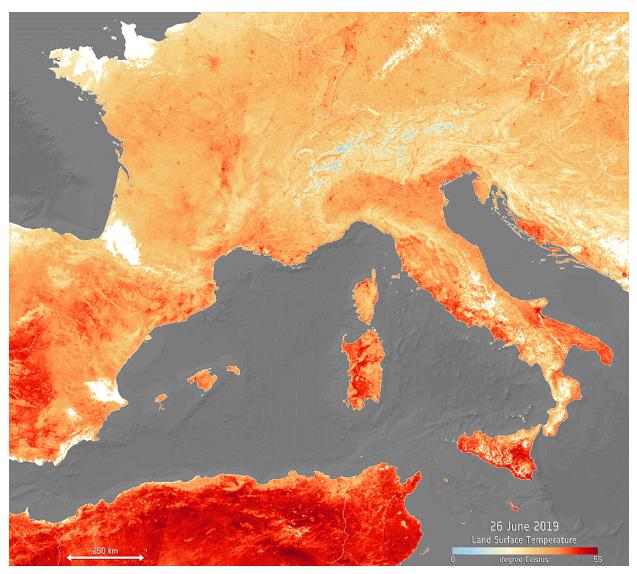

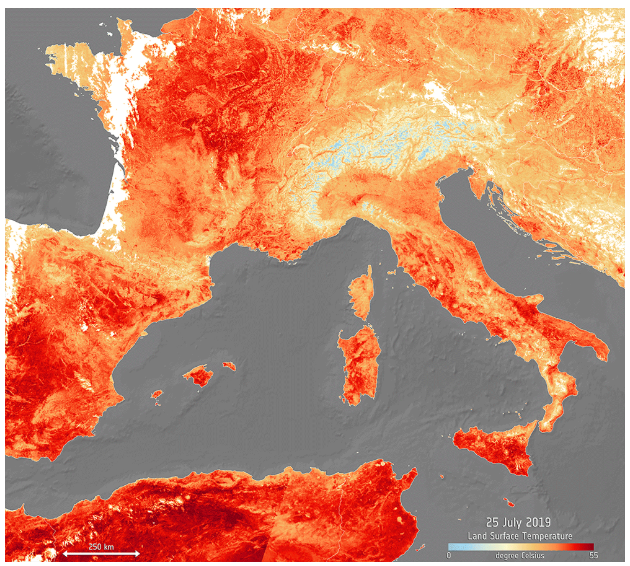

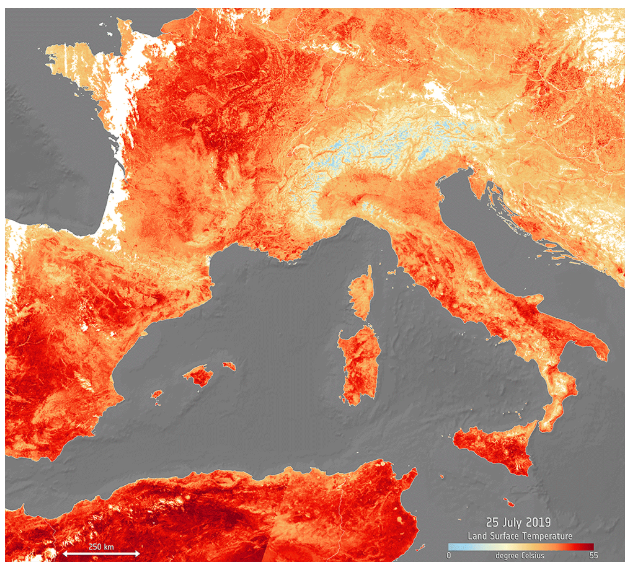

Vintners in France haven’t seen such a succession of hot weather and dry harvest since the 14th century, during a time called “the Black Death”, according to Bloomberg. Has a nice ring to it, doesn’t it?

Though these weather extremes may seem normal to those under the age of 30, they are unprecedented by historical standards, going all the way back to when Europe was recovering from the pandemic that trounced its population. This is the conclusion of researchers who examined temperature, grape harvest and wage data dating back to 1354.

In their paper, the authors led by Thomas Labbe conclude:

“Outstanding hot and dry years in the past were outliers, while they have become the norm since the transition to rapid warming in 1988. Hotter temperatures over the last three decades have resulted in Burgundy grapes being harvested on average 13 days earlier than they were over the last 664 years.”

The study underscores how the effects of climate change are forcing some populations to adapt to new cycles.

Comparing land surface temperatures from June to July 2019

The hotter temperatures have an effect on Burgundy’s farmers tending to their vineyards, itinerant harvesters, merchants and consumers.

Through looking at about 300 documentary weather reports, the researchers looked at the legendary hot summer of 1540 that dried up the Rhine River. That year, workers harvested grapes that looked like “withered raisins” and “yielded a sweet sherry-like wine which made people rapidly drunk.”

Doesn’t sound that bad to us…

Regardless, Hugh Johnson, a well known wine critic, said tasting the 1540 vintage was “one of the most memorable moments of his career”.

High temperatures don’t necessarily guarantee quality harvests, according to the research, which notes that the duration of ripening and winemaker styles are also important inputs.

via ZeroHedge News https://ift.tt/2Ztk3yg Tyler Durden

Facing a Parliamentary majority opposed to a hard Brexit – a crashing out of the EU if Britain is not offered a deal she can live with – Boris Johnson took matters into his own hands.

He went to the Queen at Balmoral and got Parliament “prorogued,” suspended, from Sept. 12 to Oct. 14. That’s two weeks before the Oct. 31 deadline Johnson has set for Britain’s departure.

The time his opposition in Parliament has to prevent a crash out of the European Union has just been sliced in half. His adversaries are incensed.

The speaker of the House of Commons called Johnson’s action “a constitutional outrage.” Johnson’s Tory Party leader in Scotland resigned. Labor Party Leader Jeremy Corbyn said Parliament will start legislating Tuesday to block Johnson.

There is talk of a no-confidence vote in the Tory government.

One recalls the counsel Benjamin Jowett, Master of Balliol, gave his students: Never retract, never explain, just do it and let them howl! For Johnson has done what he was chosen, and pledged, to do.

Though he lacks a majority for a “no-deal Brexit,” his suspension of Parliament keeps faith with the hardline Tories who put their trust in him — that he would honor his commitment to get done by October’s end what the British people voted to do in 2016.

Whatever may be said of him, Johnson has shown himself as a man of action, a risk-taker, a doer, like Trump, who has hailed Johnson for the suspension. And leaders like Johnson are today shouldering aside the cookie-cutter politicians to dominate the world stage.

Matteo Salvini, interior minister, leader of the League party, and the most popular political figure in Italy, brought down his own government to force new elections he felt he would win. His ambition is to take the leadership not only of Italy but of the European populist right.

Salvini’s boldness backfired when the League’s ex-partner in the government, the leftist Five Star Movement, joined the Democratic Party to form a new government from which the League is excluded.

Yet Salvini, too, is in the mold of Trump and Vladimir Putin, who, when he saw a U.S.-backed coup take down the pro-Russian president in Ukraine, seized Crimea, home port of Russia’s Black Sea fleet since the 18th century.

These leaders are men of action not words. And their countrymen are cheering their decisiveness.

India’s Narendra Modi is in the mold. After reelection, he revoked Article 370 of India’s constitution that guaranteed special rights to the Muslim-majority in Kashmir, a state over which India and Pakistan have fought two wars. To effect the annexation of Kashmir, Modi sent thousands of troops into the disputed territory, imposed a curfew, shut down the internet and arrested political leaders.

When Prime Minister Imran Khan asked Trump to intervene on Pakistan’s behalf, Trump, meeting with Modi at the G-7, called it a matter between the two countries.

While autocrats appear ascendant, there is another phenomenon of our time: popular uprisings and mass demonstrations as shortcuts to political change.

These began to flourish with the Arab Spring in Tunisia and Egypt in 2011, the latter of which brought down President Hosni Mubarak after 30 years in power. The Cairo revolution and subsequent election brought to power Mohammed Morsi of the Muslim Brotherhood. This was intolerable to the Egyptian army, which executed a coup that led to new elections and the installation of the present ruler and former general Abdel-Fattah el-Sissi.

In 2014 came the protests in Maidan Square that led to the ouster of the pro-Russian government in Kiev and loss of Crimea.

This year saw mass demonstrations in Puerto Rico bring down the government in San Juan. In France, the Yellow Vest movement, rebelling against a fuel tax Emmanuel Macron imposed to cut carbon emissions, flooded the streets for months, demonstrating, rioting, even vandalizing the heart of Paris to get it repealed.

Then there is Hong Kong, a city of 7 million claimed by a China of 1.4 billion, where scores of thousands, even millions, have protested, blocked streets, shut down businesses and closed the airport.

The Hong Kong demonstrators are demanding what the 13 colonies demanded: freedom, liberty, independence. But as Xi Jinping is very much an authoritarian autocrat, the protesters are pushing their luck.

What motivates the democratic protesters and what propels the rise and welcome reception of the autocrats, the men of action, is not all that dissimilar.

It is impatience, a sense that the regime is out of touch, that it does not reflect or respond to what people want, that it is torpid and cannot act decisively, that it does not “get things done,” that it is tedious and boring.

Part of Trump’s appeal to his base is that people sense he feels exactly as they do. And they readily understand why Trump would not want to sit down at a G-7 gathering and gas endlessly about climate change.

via ZeroHedge News https://ift.tt/2ZC2XgV Tyler Durden

You won’t find any shallow hashtags at the former concentration camp, just quiet, powerful reality…

Right now, someone in the media is finding another excuse to proclaim that Trump is Hitler, America is Germany 1933, and detention centers on the southern border are concentration camps.

Recently I went to Dachau, just outside of Munich, to see a real concentration camp.

The first thing you notice is the irony. The people who, in too loud voices, mill around the station entrance asking “Is this the train to Dachau?” and then the conductor’s announcement calling out the name as if it were just another stop. The mediocre station has a McDonald’s. The bus stop sign for the shuttle you need to take has “Concentration Camp” written in English. Everyone around you is on vacation, dressed for it and chattering like it. You arrive at a visitor’s center, and there’s a rush for the toilets and the snack bar. Which way to the camp, Dad? Can we see the crematorium? Can we?

A hundred steps outside the snack bar, the world changes. The road turns gray even though the light playing through the poplars is out of a postcard. They’ve changed the entrance location from a few years ago so that you now enter through the former SS barracks and come to the gate. It really says Arbeit Macht Frei (“Work Will Set You Free”) on the iron bars and you walk through just like they did. The gate only swings one way; you will leave today, but it wasn’t originally designed that way and you can tell. There may be a hundred people with you but it is completely silent as you enter.

It is too small. You see the administrative buildings to the right, the reconstructed prisoner barracks to the left, the assembly ground in front of you. You see the fences and walls on all four sides, walkable in a few minutes at an easy pace on a gorgeous day. It is too small to have held all those people, too small for all that happened, too small to be the symbol of Nazi power it was then. You expect something more substantial, with the distant site lines obscured, like at Disney World, where tricks of the eye make things seem grander.

It is too familiar. It takes only a few minutes to get your bearings. You’ve seen photos before, and there are many posted, populating the place with buildings and people once here and forever gone. It is unlike, say, an art museum on the scale of the Met or the Uffizi, where, after hours of circling corridors, you have no idea where you’ve been. You know Dachau.

The museum unfolds in the order that new prisoners were processed. The early days of National Socialism are explained where the inmates were once assigned numbers. The seizure of power by Hitler is documented in the room where people were stripped and deloused (subtlety is missing when the backdrop is Nazism). And you exit into the campgrounds awkwardly after reading about their liberation by the 45th Infantry Division.

You think, after all that reading and those museum exhibits (and it is a thorough education, much more than an Instagram collection of artifacts and, oh look, a real prisoner’s uniform, honey!), you understand something. But not yet. You have really just arrived, and in front of you is Dachau itself, the ground, the air—the same ground they saw and air they breathed—and you have a choice. Many visitors turn back towards the snack bar, falsely satiated after an hour, thinking they’ve seen Dachau and anxiously trying to remember when the shuttle bus runs back to the station.

If you wait for them to leave, you can see Dachau.

Most of the place is empty, acres of crushed stone with flat markers showing where the now-missing barracks were. The trees lining the central road bisecting the camp are old. They were here when Dachau was working. You can match up an individual tree from a 1942 photo with the one in front of you and touch it. The sun is warm; it’s a beautiful late summer afternoon with those wonderful tickles of early fall all around. A day to be alive, grandpa would have called it. There must have been days just like this one in 1942.

There is some minor archaeological excavation work going on. An archaeologist stands over a hole about three feet deep and explains that he’s looking for evidence of the original fence line, the border of the camp before it was expanded in 1937. He’s found some wooden post fragments and some barbed wire. So the bottom of that hole is 1937, I ask? Yes, he says, the dirt and stones piled here haven’t seen sunlight since then. I ask if I can take one of the stones with me as a keepsake, and he explains that is not allowed, even as he looks away just long enough. Doing the right thing is hard enough elsewhere, never mind in Dachau.

A sign states simply that the area in front of you is where the barracks used for medical experiments on live humans once stood. Another denotes the punishment barracks, where the SS concocted even darker methods of retribution. You see where the bodies were stacked like cordwood but you know that wood is strong and straight and the images you are recreating show corpses floppy and tangled in their piles. Now you are seeing Dachau, here in the deeper waters.

Dachau does not believe in your tears. This is not a sentimental place. It is not clean. A universe of victims died here but there is no acknowledgement of victimhood, or raising of awareness, or giving of voice, or trafficking in of shallow hashtags. Dachau is here to declare what happened and charge you with doing something on the scale and with the accuracy that are required.

See, by coming here, it is now handed to you, that obligation. Hitler and his Dachau did not emerge from an election that frowned on a favored candidate. Following World War I, Germany was purposefully humiliated and saddled with war reparations that were not payable. An economic crisis unrolled. Inflation drove the nation to starvation. With no history of democracy, Germany was willed into a republic as unprepared as two virgins in an arranged marriage. Both across the border and at home, powerful communist forces threatened. Hungry people weren’t tricked into a strongman because of Facebook or some Electoral College fluke; they demanded one.

Within three months of taking office, Hitler gave himself the right to amend the constitution, ended representative government, created special political courts, made criticism of the government a capital crime, and established Dachau. Two months after that, Jews were fired from government positions, political parties and unions were prohibited, opponents were murdered, and books were burned. There was no slippery slope. It was not incremental; it was inevitable.

There is obviously more to this story than a travelogue about an interesting day trip out to Dachau by train from nearby Munich. To say that Trump is Hitler, America is Germany in 1933, and a grimy detention facility is a concentration camp means you have never been to Dachau.

The presentation at Dachau is very un-2019, where everyone vies for adopted victimhood and chosen trauma. Dachau is cold because only its facts matter.

Tweets childishly mocking political opponents and regulations preventing a small number of self-declared trans people from joining the Army have nothing to do with Dachau. To cite 2019 border facilities or exaggerate the historical impact of a march in Charlottesville is to turn Dachau relative, the dial jiggered to magnify some other event. It makes people numb; it dumbs down discussion; it is cheap, inaccurate, and exploitative. It demands mighty outrage from a partial set of facts. Both butterflies and elephants have legs, but no one should claim a butterfly is an elephant.

Propagandists have always used ignorance to manipulate. Yet while CNN works to convince viewers that silver mylar blankets instead of comfy quilts for migrants means there are concentration camps in America, Dachau reminds us that physicians here dissected human beings alive as part of medical experiments. Just as is taught in beginning writing courses, truth comes from showing, not just telling. For those who call Trump a Nazi, there is Dachau to visit. For the record.

via ZeroHedge News https://ift.tt/2LaMacO Tyler Durden

{kind=link}

{kind=link}

{kind=link}