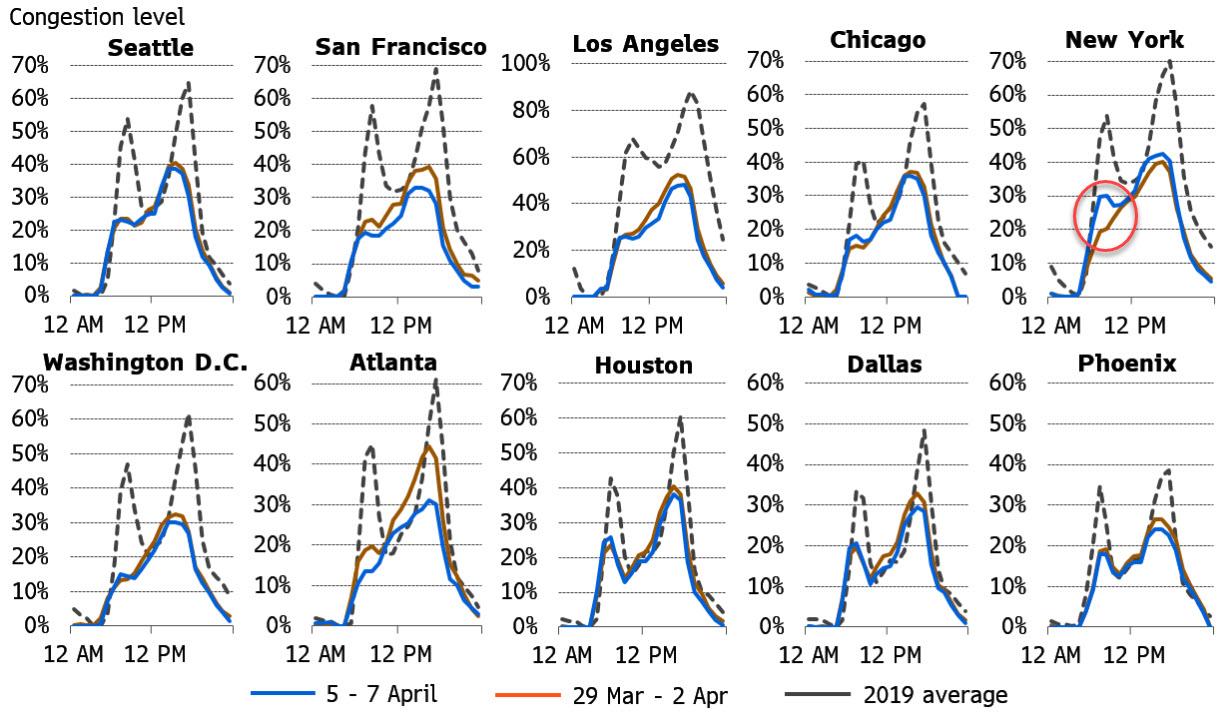

Morning Traffic Congestion Is Returning To New York

Things are slowly getting back to normal in the Big Apple (or they would be, if any rich people still wanted to live there after Cuomo is done pushing their tax rate near triple digits).

While peak congestion remains mostly unchanged across the U.S, the morning peak appears to be slowly re-emerging in New York City as commuters begin to return to offices, according to an analysis from Bloomberg.

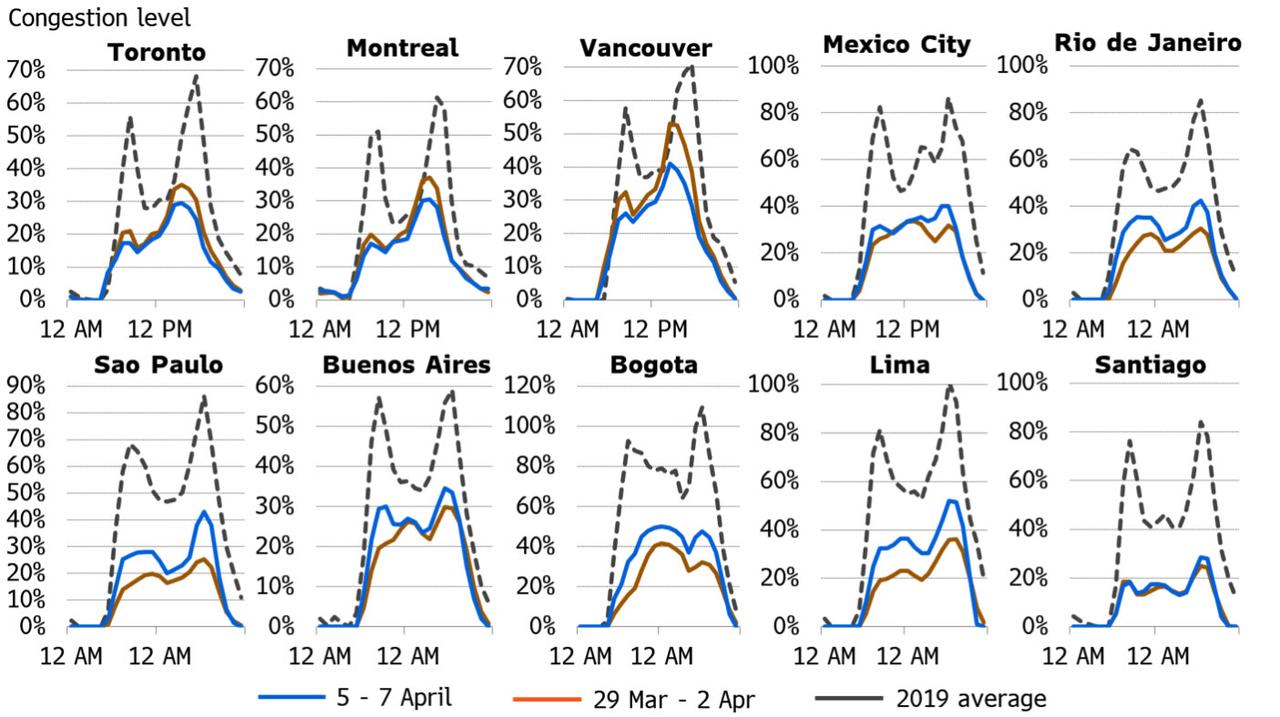

Elsewhere across North America, traffic levels remain around half of normal levels while outside the U.S., congestion levels have ticked higher across South America, in particular in Sao Paulo and Lima.

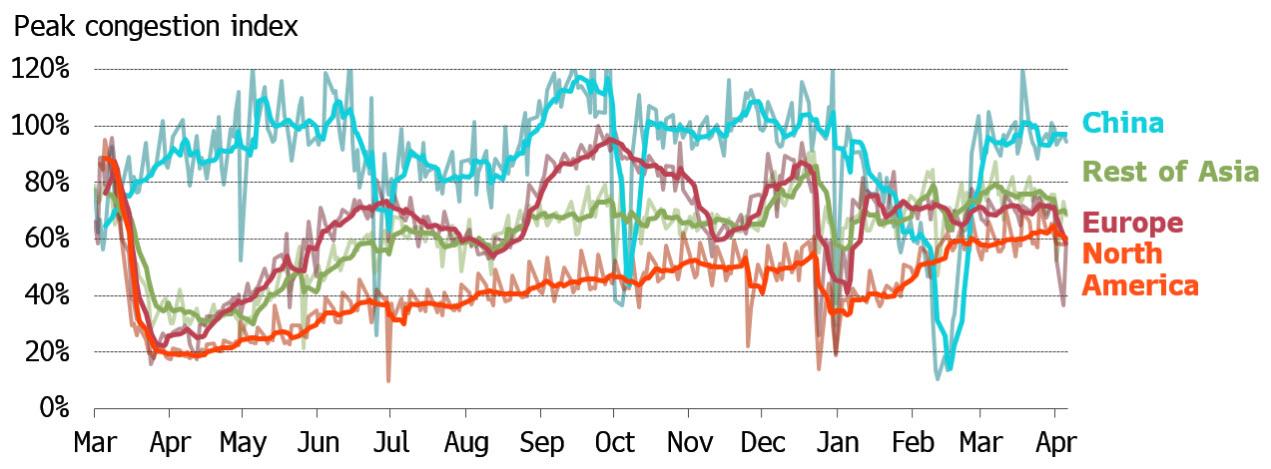

It’s a different story in China, where average hourly peak congestion on a five-day rolling average basis in the major Chinese cities (Beijing, Shanghai and Guangzhou) remains close to pre-pandemic levels, with peak morning traffic in Beijing and Shanghai exceeding normal levels, while the recovery remains incomplete only in Guangzhou. At the same time, the recovery is advancing in many parts of South and South East Asia, with the re-emergence of the morning peak in many cities signaling that commuters are returning to offices.

Looking at Europe, the current impact of the latest round of lockdowns across Europe is difficult to discern due to the Easter public holiday affecting normal mid-week travel patterns. As Bloomberg notes, lockdowns of varying stringency remain in force across Italy, France, the U.K., parts of Scandinavia, Iberia and Greece, although the recovery appears to be underway in Spain and Portugal.

It’s a report on Federal Heritage Minister Steven Guibeault’s ongoing vendetta against non-conforming political speech on the internet, in which he’s calling for censorship of “hurtful” comments against politicians and implementation of an internet killswitch to facilitate it.

Federal Heritage Minister Steven Guibeault

Blackrocks is behind a paywall, permit me to quote it here:

‘Federal internet censors should target hurtful words against politicians, says Heritage Minister Steven Guilbeault. The Minister added pending regulations may include an internet kill switch to block websites deemed hurtful, but called it a “nuclear” option.

“We have seen too many examples of public officials retreating from public service due to the hateful online content targeted towards themselves or even their families,” said Guilbeault. “I have seen firsthand alongside other Canadians the damaging effects harmful content has on our families, our values and our institutions. As a dad and a stepdad to six kids, I know more can and should be done to create a safer online environment.”

Guilbeault made his remarks in a podcast sponsored by Canada 2020, an Ottawa think tank affiliated with the Liberal Party. Legislation to censor internet content will be introduced shortly, he said.

“I am confident we can get this adopted,” said Guilbeault. “Once the legislation is adopted, clearly creating a new body, a new regulator like that in Canada, would take some time.”’

The goal is obviously to silence non-conforming analysis

Coincidentally or not Guilbeault has been relentlessly pursuing the recommendations of the Canada’s Broadband Telecom Legislative Review (BTLR), which I wrote about last year and tabled a petition to the House of Commons to kill it. Then the whole pandemic thing broke out, and we entered this “New Normal”.

For a political cabinet minister to seriously push forward new rules silencing free speech directed against politicians is quite rich, having just last week been publicly attacked and mocked by a senior advisor to Premier Doug Ford (my transgression? Raising the issue of small business bankruptcies under lockdowns with my MPP).

(Cue up Jacobs, who will probably come barrelling in here and call me a moron because Guilbeault is Federal and he’s provincial, so I’ll save him the trouble to say: it’s all one political class)

These are the last gasps of our political overlords

This global, near ubiquitous ham-fisted reaction to the global pandemic has ushered us into an era of hypernormalization. That’s simply defined as when the mental fatigue and psychic stress of pretending to believe demonstrably false and often contradictory narratives begins to manifest in a kind of mass neurosis.

Being brainwashed or coerced into accepting ideologies that have been decided by oligarchs and billionaire Sith Lords are an additional antagonizing factor.

Sooner or later a tipping point will be reached and the public will simply abandon what they see as an increasingly non-functional system, one where the entire might of the state is arrayed against their own interests.

When this happens it can channel into populism, deteriorate into (arguably deserved) demagoguery, or perhaps more hopefully a type of mass opt-out of the current system into the next iteration of human organization and governance.

We’re in the early innings of an inexorable transition from the age of nation states into network , or crypto states (“crypto populism”?). How that looks is often the topic of discussion on our AxisOfEasy podcasts, it can be chilling, as in if the Network State is Facebook, or Google. Or it can be liberating, like a decentralized mosaic of Hanseatic Crypto States. That’s a choice we, as people and citizens actually can participate in, right now, today.

But these cocooned, self-serving elites running these dilapidated nation states? They’re just rigging a game that’s increasingly irrelevant. It doesn’t really matter because their era is over.

No matter which trajectory things pursue, one thing is certain: the next step is a cascading loss of institutional and political legitimacy, such as what happened in 1989 with the implosion of communism and the Warsaw Pact states. A year earlier, not one geo-political strategist, let alone party apparatchik would have forecasted the coming collapse. Eighteen months later, it was all over.

I think we’re headed for a similar period over the next few years, and it’s the current leadership and the incumbent elites who brought us here.

New Neuralink Video Purportedly Shows Monkey Playing Video Games Using Its Mind

The man who can’t seem to keep his cars (or his recent spaceships) from spontaneously combusting now claims that his mind-machine interface company, Neuralink, can allow a monkey to play video games using only its mind.

Neuralink released footage this week that purports to show a monkey named Pager, who is nine years old, playing video games in exchange for a banana smoothie delivered through a straw. Pager was hooked up to a Neuralink system six weeks ago, according to RT.

The video shows links recording activity from more than 2,000 electrodes implanted in the monkey’s motor cortex. The activity is then wirelessly fed to a machine-learning algorithm, which “sensed modulations in the monkey’s neurons and allowed the system to predict intended hand movements via a mathematical model of neural activity and the corresponding joystick movements.”

Researchers calibrated the system, the report says, by monitoring Pager’s brain waves as it manipulated a joystick. Then, they disconnected the controller without telling the monkey, who wound up playing pong using only its brain, sans the joystick.

And what would an inch of progress be without Elon Musk taking a mile? Musk quickly took to Twitter to proclaim that Neuralink’s first product would “enable someone with paralysis to use a smartphone with their mind faster than someone using thumbs”.

“Later versions will be able to shunt signals from Neuralinks in brain to Neuralinks in body motor/sensory neuron clusters, thus enabling, for example, paraplegics to walk again,” Musk wrote.

Later versions will be able to shunt signals from Neuralinks in brain to Neuralinks in body motor/sensory neuron clusters, thus enabling, for example, paraplegics to walk again

We think it must be capital raising time for Neuralink. Either way, it’s starting to smell like the Neuralink SPAC – or perhaps the Neuralink/SpaceX merger, or something equally as heinous – is just right around the corner.

Section 230 of the Communications Decency Act is one of the most important pieces of legislation in American history. Passed into law in 1996, it has overseen the entirety of the consumer Internet’s development. Its premise is simple: Internet service providers and platform operators are not responsible for civil damages that result from user-generated content that they host or manage. These protections are why the United States is the first choice for hosting any digital service. Without them, the entire world would suffer a less free Internet.

I have operated a controversial website called the Kiwi Farms for 8 years and was featured in ZeroHedge in 2019 after telling New Zealand police I would not be surrendering my user’s information to them. My website thrives and doubles in size each year, primarily thanks to Section 230. I can allow my users to say almost anything they want without having to worry about being sued for what they say. Without these essential protections, I would not be able to host in the United States.

Unfortunately, Section 230 has been defamed as the reason Facebook, Twitter, Google, et al behave the way they do. This is not true. These businesses censor because they have personal motivations to do so. More importantly, they have financial motivations to do so.

I hope to convince a reasonable person that:

Payment networks must be regulated to give fair access.

Section 230 is essential and modifying it harms online speech.

Big tech does not need Section 230, but you do.

You should learn how to use cryptocurrencies right now.

The payment networks are more powerful than big tech.

Without the consent of all four major payment networks to stay in business, even mighty tech giants are vulnerable to lose billions of dollars in revenue. The various agreements enforced by the four major payment networks (MasterCard, Visa, Amex, and Discover) impose rules that any business wanting to exist in the digital economy must obey. Not all these rules are written.

The big payment networks like to stay out of the public eye. They avoid attention by using blacklists which they claim only banks can add to, but which they manage and share. You also never deal with the payment network directly. An eCommerce site passes your credit card information to a “payment gateway”, which is plugged into a “payment processor”, and that payment processor handles communications with the payment networks. Each of these are usually different companies. When you get banned from processing payments, you are told so by your payment gateway or payment processor, but the decision can come from much higher up. If it were, you’d be lucky to find out.

Consider a company like Patreon. They are an online crowdfunding service which handles donations from many supporters to many online content creators. Patreon has its own rules, uses Stripe as a payment gateway and payment processor, agrees to Stripe’s terms of service, and then Stripe coordinates with all major payment networks which each have their own set of agreements. That means every creator on Patreon must obey six different sets of rules. If the gateway were its own company, it would be seven. It is no wonder so many people get banned, as only the most tepid and inoffensive content creators could hope to meet so many different standards!

Patreon must keep Stripe happy to stay in business, and Stripe must keep all four payment networks happy to stay in business. If any one of MasterCard, Visa, Amex, or Discover pass a rule, then it affects the entire downstream ecosystem. If Discover (5% of the market) says an industry or behavior is prohibited, then Stripe must enforce that rule on all the merchants on their service (even merchants who do not process Discover). If Discover were to cut ties with Stripe, then Stripe would lose at least 5% of their transactions over night and any merchants who do want to process Discover cards. That is a large and dramatic blow to any company operating on small margins.

I do not claim it is MasterCard’s fault that Twitter banned Trump. I am sure Twitter makes many stupid decisions all on its own. The problem is that these rules—how they are enforced, the secrecy in which they are enforced, and unappealable finality of these decisions—stifle competition. Startups like Gab quickly find themselves told they are not allowed to make money. This problem has never existed before on the scale that it does now.

This phenomenon transcends the type of startup. All alt-tech is trodden upon equally. Patreon competitor New Project 2 was first banned from a payment processor at the demand of Discover, then after finding a new payment processor was put on MATCH (the MasterCard blocklist), prohibiting the company from ever finding another payment processor. If Dick Masterson (the owner of NP2) made a new company to try and get around MATCH for the purpose of continuing NP2, he would very likely find his person on that blocklist directly, ending all his businesses at once.

These blocklists, and the risk management factors which decide who goes on them, are “trade secrets” and you cannot even sue to figure out why you were added to them. New Project 2 was blacklisted for “Violation of Standards”, which prohibits it from even using so-called high-risk processors. Nobody knows what “Violation of Standards” means. Dick only found some details of New Project 2’s blacklisting because he called the banks and annoyed the right people for days until they reluctantly admitted who was actually at fault. Payment networks claim they do not add merchants to the blacklists, and that only partner banks can, but they will call these banks and tell them to do it on their behalf, and the banks are not in any position to refuse.

PayPal has not been mentioned so far, but rest assured they are one of the most egregious and will drop you first. BitChute, a video platform competing with YouTube, was banned from PayPal. ZeroHedge itself is banned from using PayPal. To this day, because of my association with the Kiwi Farms, I cannot use the Uber app to get a taxi because Uber uses PayPal to process credit cards and I am banned from PayPal.

Before we regulate the Internet, why don’t we try to regulate the payment networks?

Give the market a fair chance at competing with tech giants by enforcing fair access to credit and debit card processing!

The Office of the Comptroller of Currency proposed new regulation which would require banks (and the services they run, including payment networks) to stop industry blacklisting and require specific examples of risk to ban a merchant from processing cards. It was called Fair Access to Financial Services (OCC-2020-0042-0001).

These “fair access” rules were finalized on January 14th, 2021. They were set to take effect on April 1st. Placing this on April Fool’s Day was a bit too prescient, because the Chairman immediately resigned after passing this rule, and the fair access rule was formally put on an indefinite pause on January 28th, 2021 – one week after Biden assumed office.

This rule was politicized as a way for Republicans to force poor, innocent multinational trillion dollar banking institutions to do business with ‘evil’ industries like oil drilling and the NRA. The Chairman of the OCC made note that it should be an act of congress to regulate those industries, not unilaterally enforced by nameless risk management committees behind closed doors.

It is unlikely that payment network regulation will find bipartisan support. The payment networks do a good job of picking their targets. Controversial but left-leaning organizations like Nation of Islam appear to have no issue processing cards, despite their virulent antisemitism rivaling anything found on Gab. Perhaps if Planned Parenthood suddenly needed cash upfront to perform abortions things would change. Until then, free speech will be clustered alongside weapons and Alaskan oil prospecting as an industry that is safe to punch down at.

So, if bankers are above regulation for now, why not regulate social media?

We have already amended Section 230 and it sucked.

There are holes poked into Section 230 protections already. When Section 230 was first passed in 1996, Congress effectively legalized piracy. Platforms were immunized even from copyright infringement damages. So, if pirates could stay anonymous, there was no one to sue for distributing copies of movies.

To patch the piracy loophole, in 1998, we passed the DMCA. This act created the process for the copyright takedown system that is infamous on websites like YouTube. Rights Holders can now take down copyrighted content and sue the services directly if they refuse to comply. Unfortunately, the process created is so sloppy and awful it is a continuous nightmare for a host like me (and everyone on YouTube) to deal with.

For one, there is no recourse for flagrant or malicious DMCA takedowns. There is no requirement that the person sending the DMCA prove they own the copyright, to have a copyright ID, to be an attorney, or anything to that effect. I routinely receive copyright complaints that I must take seriously for content they don’t even own. OnlyFans (a Grand Cayman company) makes it clear in their Terms of Service that they do not own the content they host. Despite that, OnlyFans routinely sends me DMCA takedown notices for their 3rd party content through a man out of California who is not an attorney. This is a total farce, and there is nothing I can do. I still must reply with a counter notice, but they never take it to court and I never even hear back. I have no legal recourse against this abuse.

This will be everything online if further loopholes were carved into Section 230. Imagine if defamation was handled the same way the copyright system is. Random trolls could issue takedowns for your Tweets and Facebook posts. You would have to send a legal counter notice with your real name and address to the troll to reinstate your messages. There would be no validations in place. Your speech would be at the mercy of the whims of insane people online.

In this environment where platforms could be held liable for things said on their websites, only the richest of them could afford survival. I am currently dealing with two lawsuits. They are completely baseless, insane ramblings from insane people, but they will still cost a lot of money to deal with. There is no way to get fees from them because they have nothing to take. Without Section 230, I would lose a layer of protection enabling me to deal with these lawsuits for much less than it would if we had to take it to trial. It would destroy the site, especially since I cannot charge cards normally to generate consistent revenue to fund my defenses with.

President Trump and people in general seem desperate just for revenge. The rabble directed towards Section 230 is out of anger. “If only this blow were delivered and 230 were repealed,” they think, “Twitter would be plunged into financial ruin overnight.” Maybe a Samson Option is what we need?

Unfortunately, it is not so simple. Twitter would adapt and become more censorious to reduce its civil liabilities. All US search engines would have their results curated by anyone willing to complain about defamation—including, and perhaps especially, by public figures with something to hide. The smaller and less profitable sites hosted out of the US (Gab, Parler, 4chan, 8kun, Kiwi Farms, Encyclopedia Dramatica, thousands of small, federated services and communities) would either be destroyed outright, forced go private, or driven out of the United States. It would be a total disaster for the little guys.

Jack Posobiec made a comment recently that Justice Clarence Thomas had ruled Section 230 was unconstitutional. This is not true. The opinion he cited as ‘sauce’ was not case law, but rather an opinion in the strictest sense. Thomas did not even claim Section 230 was unconstitutional. This misinformation was seen hundreds of thousands of times and further defamed the public perception of a law we rely on to even conduct these conversations about Section 230 online.

So, if we can’t regulate the banks and Section 230 is actually good, what can we do?

What Clarence Thomas actually suggested was that we might have to regulate the supermassive tech companies as ‘common carriers’ or utilities. Regulating only the largest social media networks could work. You can either be a monopoly, or you can be unregulated, you cannot be both. I maintain that regulating payment networks first would be ideal, but that will not happen.

There is some hope that FedNow, an atrociously named US answer to SEPA, could offer some relief to this payment network bottleneck on speech. I am not optimistic for it, but it is good for more people to know it is supposedly in development.

Cryptocurrencies bypass the payment network bottleneck now.

The more people who know how to transact in cryptocurrency, the freer the Internet will be. Sites like buybitcoinworldwide.com (not an affiliate url) contain simple guides on how to get into the ecosystem regardless of your country. You do not have to invest any money in. Just learn how crypto works, how to get it, and how to send it. That knowledge cannot be taken away from you—and it might prove useful, sooner rather than later.

Top Carbon-Credit-Seller Launches Internal Probe After Selling “Worthless” Offsets To JPMorgan, Disney

Back in December, Bloomberg published a sweeping expose that raised serious questions about the ESG investing craze sweeping the world. In the piece, Bloomberg detailed how the Nature Conservancy, the world’s biggest environmental group and a prominent seller of carbon offsets, had sold “worthless” credits to JPMorgan, Disney and BlackRock as the corporations sought to finance the protection of carbon-absorbing forest land to absolve them of their sins tied to fossil fuel usage.

Carbon credits and so-called “green” bonds are some of the most popular ESG-focused products that are being purchased by corporations, or ESG investment funds. But as Bill Blain pointed out in his Morning Porridge a couple of weeks back, it looks like the ESG craze is already becoming too ‘woke’ for its own good, as companies and institutional investors are chiefly concerned with virtue signaling, and less concerned with whether the products they’re buying are actually making a difference in the fight against climate change.

Fast forward to Monday, and Bloomberg is reporting that the Nature Conservancy is launching an investigation into its procedures for selling carbon credits to try and address the criticisms raised by Bloomberg.

The self-examination follows a Bloomberg Green investigation last year that found the world’s largest environmental group taking credit for preserving trees in no danger of destruction. The internal review is a sign that it’s at least questioning some practices that have become widespread in the environmental world, and could carry implications for the broader market for carbon credits.

While the Nature Conservancy declined to answer specific questions about the review, it said in a statement that it aims to meet the highest standards with its carbon projects and that the inquiry will be led by scientists and a “team of experts with deep project knowledge.”

Selling credits for well-protected trees potentially undermines the sustainability efforts of some of the world’s biggest companies. Each carbon offset is supposed to represent the reduction of one ton of planet-warming emissions that would have otherwise spewed into the atmosphere without intervention. Around the world, a wide variety of offset projects do everything from protect mangrove forests to destroy heat-trapping gases from landfills and coal mines. But offset payments channeled to already safe ecosystems don’t fundamentally change the amount of carbon dioxide in the atmosphere.

Considering the investing public’s growing interest in ESG, with talk of an ESG boom driving EV stocks higher (while companies like Deliveroo flop on concerns about governance issues and the outlook for more restrictive labor laws for “gig economy” firms), the details about the market for carbon offsets aren’t well understood. As Bloomberg explains, every carbon offset project is measured against a “baseline scenario”, an estimate of what would have happened if preservation efforts weren’t undertaken. When the project involves a forest, the manager of the project calculates the difference between the existing ‘preserved’ trees, and the “baseline scenario”, and uses that to determine the amount of carbon credits that can be sold.

Since there’s virtually no oversight or review of these calculations by a third party, carbon-credit producers have carte blanche to make up the rules as they go along. Project developers can make unlikely claims about the huge numbers of well-protected trees that were supposed to be cut down, and in that way produce a surfeit of credits.

In this case, the Conservancy claims the forest land it protects would have been aggressively harvested if it weren’t for carbon payments. But while this allows the nonprofit to earn more money by selling more credits, those credits aren’t actually offsetting pollution. “In a sense, you’re giving a polluter a license to emit a very large quantity of pollution based on these things,” says Charles Canham, a forest ecologist at the Cary Institute of Ecosystem Studies and a longtime board member of a local chapter of the Conservancy who has acted as a whistleblower, repeatedly and publicly criticizing the Conservancy’s tactics, telling BBG that “the way the Nature Conservancy has gone about this is unconscionable.”

For its part, the Conservancy claims its projects have been vetted by third parties and comply with nonprofit registries that supervise offsets. “As our understanding of climate change science and policy evolves, changes, and grows, we strive to ensure our projects do the same so we can achieve our goals for a low-carbon future,” the group said.

Since megacorps like Amazon, Google-owner Alphabet and Microsoft (along with some of the West’s biggest banks, like JP Morgan, have vowed to achieve “net zero” emissions within a few decades. To accomplish this, carbon credits will be essential (because not even the most dedicated uranium bull expects the US to go all-in on nuclear power in the foreseeable future). In 2020, carbon offset sales increased by roughly one-third vs. the prior year.

Carbon offsets have become an increasingly popular method way for corporations looking to reduce their emissions, as some aim to achieve “net zero” emissions in the not-too-distant future.

In 2020, companies purchased more than 93 million carbon credits, equivalent to the pollution from 20 million cars in a year. That’s a 33% increase over 2019, according to clean-energy research firm BloombergNEF. The market is poised to grow sharply in the coming years as heavy emitters such as Royal Dutch Shell Plc, Delta Air Lines Inc., and JetBlue Airways have vowed to negate pollution by acquiring more carbon offsets. Mark Carney, the former Bank of England governor who is an organizer of this year’s COP26 climate talks in Glasgow, Scotland, has said that the global market for carbon offsets can be expected to grow to $100 billion in the decades ahead.

But the biggest problem facing governments, regulators etc. seeking to ensure carbon credits have the intended environmental impact is this: they must ensure that the activities that carbon projects take credit for weren’t already occurring. The biggest sin committed by the Conservancy is it essentially sells too many credits backed by the same patches of “preserved” forestland – although the organization has protected more than 125M acres since it was founded 70 years ago, before carbon credits were even a twinkle in the eye of environmental activists.

“Carbon offsets are not a donation to a nonprofit group, it’s a purchase of a product,” says Eli Mitchell-Larson, a University of Oxford climate researcher and co-author of the Oxford Offsetting Principles, which provides guidance for how offsets should be used by companies with zero-emission targets. “The purchaser is getting the ability to say they’ve neutralized one ton of their emissions.”

While Mitchell-Larson applauds conservation groups for protecting and restoring lands, he says they hinder the world’s response to climate change when they sell offsets on land that was going to be preserved anyway. “One of my frustrations is the slowness of some conservation groups to take seriously the credibility of carbon claims they are making,” he says.

To be sure, the Conservancy isn’t the only well-known environmental group selling carbon credits against land that was already set to be preserved. Bloomberg cited some examples of the National Audubon Society using similar tactics.

The Conservancy isn’t the only environmental group selling offsets from acreage it didn’t intend to harvest. For instance, in the swampy tidal region of South Carolina, the National Audubon Society has been preserving an ancient forest since 1970. Some of the towering cypress trees have stood for more than 1,000 years. On its website for the sanctuary, known as Beidler Forest, Audubon describes a “pristine ecosystem untouched for millennia.”

In 2013, Audubon began selling carbon credits from this natural sanctuary, with the project’s documents describing a rapacious baseline scenario of “clearcuts and thins.” The majority of its trees would have been felled within 25 years in the absence of carbon payments, stated the documents.

In reality, nothing of the sort would have happened, according to Norman Brunswig, who helped launch the carbon project and managed the sanctuary for Audubon for decades before retiring a few years ago. “We never intended to cut that forest,” he says.

Retrofitting American infrastructure with more emissions-friendly materials and technologies is a major theme from President Biden’s “American Jobs Plan”. Biden and his team have set a goal for the US to reach “net zero” emissions by 2050. Part of the plan will harness the largess of the federal budget is to build charging ports for electric vehicles, electric heat pumps for residential heating and advanced nuclear reactors. But there’s little doubt that, for most companies and governments, achieving “net zero” will be impossible without the purchase of offsetting credits. Expect scrutiny of the space to intensify in the coming years.

While Japan last month marked the 10th anniversary of the devastating 2011 Tohoku earthquake and tsunami with solemn ceremonies, the government has also been stressing the successes of its recovery efforts in the country’s northeast.

In truth, however, the country is still coping with the aftermath of the Fukushima Daiichi disaster, which has already cost Japan trillions of yen and whose exclusion zone will require up to 40 more years to fully rehabilitate.

And with contaminated water continuing to build up at the ruined Fukushima Daiichi Nuclear Power Plant, Prime Minister Yoshihide Suga says that the government must finally begin dumping it into the Pacific Ocean.

With nuclear waste and fuel rods still contaminating the area, over one million tons of radioactive waste water continue to seep from the facility, according to The Japan Times, forcing authorities into what Suga describes as the “unavoidable” position of having to dump the water.

Officials claim that the water would be purified to the maximum extent possible, but environmentalist groups like Greenpeace warn that the water contains hazardous material that could damage human DNA and the health of marine life.

#Fukushima water release could change human DNA, Greenpeace warns: a “major contributor to collective human radiation dose and has the potential to damage human DNA.” https://t.co/S0864I4Vns

Fishermen also fear that consumers will refuse to buy fish caught in contaminated waters, worsening their plight amid a restriction of imports from Fukushima prefecture imposed by 15 countries and regions.

Regardless, authorities argue they must deal with the cards that have been dealt.

“What to do with the [treated] water is a task that the government can no longer put off without setting a policy,” Japanese trade minister Hiroshi Kajiyama said on Wednesday.

Suga is expected to formally decide on the course of action by next Tuesday. If he proceeds, authorities will dilute tritium to 2.5 percent of the maximum concentration allowed by the country before it is dumped.

But while Japanese officials say that the water will be safe, it remains an open question whether people will trust their word.

Melvin Capital Down Another 7% In March, Brings Q1 Loss To 49%

Just two questions: i) is Melvin Capital still short Gamestop and ii) how does it still have any clients left?

That’s what we would like answered first and foremost after Bloomberg just reported that Gabe Plotkin’s notorious Melvin Capital Management, best known for being blown up by a bunch of WallStreetBet redittors over its Gamestop short, and which lost billions of dollars requiring a $2.75BN bailout from Ken Griffin and Steve Cohen, ended the first quarter down 49% after dropping another 7% last month.

The sharp drop – which “mysteriously” coincided with a sharp surge in Gamestop stock in March – reversed a gain of almost 22% in February – when Gamestop plunged after its historic January surge, which caused Melvin to lose a record 53% of AUM.

Another firm which was also caught in the cross hairs of the GameStop saga – Maplelane Capital – which we first profiled here, is reportedly “starting to recover” after losing 45% in January. The fund rose 6.5% in February and 2.1% in March, according to people familiar with the matter, and ended the first quarter with a loss of 39.5%.

The fund benefited from its long and short wagers on technology and consumer-focused companies, a Bloomberg source said. It also appears that unlike some others who claimed the opposite, Maplelane actually did close out its Gamestop short.

Still, after such historic and furious plunges, it’s amazing that anyone is still an LP in either of the two funds, which will take many months if not years of high aggressive – and flawless – performance to recover the January losses. In fact, it’s far more likely that the two funds will lose everything as they aggressively double down with Archegos-style leverage to recover their record losses.

As for our first question of whether Melvin is still short GME, we will have to wait until mid-April when its 13F hits. Assuming the fund is still around by then and hasn’t been converted into a Credit Suisse-special family office.

So how did everyone else do? Well, Senvest – which orchestrated the entire Gamestop squeeze and made a killing on it – remains the top performing hedge fund according to HSBC, with a bunch of familiar names rounding out the top 20 including Odey Europe, Maverick, Glenview, Mudrick and the perfectly titled Tulip Trend fund. On the other side, there are quite a few systematic hedge funds in addition to the public-facing Renaissance fund, RIEF B, which continues to suck unlike its “friends and family only” cousin, Medallion.

While the S&P 500 keeps rallying and hitting new records, the spectacular collapse of Archegos family office brought a sharp reminder of the consequences of excessive leverage in the financial system.

As always, Warren Buffet had already warned us: “Having a large amount of leverage is like driving a car with a dagger on the steering wheel pointed at your heart. If you do that, you will be a better driver. There will be fewer accidents but when they happen, they will be fatal.”

I do not know what the worst part of that story is. Whether it is the fact that Bill Hwang had a criminal record. Or that Archegos used the same collateral to enter contracts with up to seven banks boosting leverage as high as 500%. Or if it is Nomura’s reaction, saying basically that whatever happens central banks will rescue banks if needed. Nothing seems to matter anymore for a system accustomed to perpetual bailouts since the LTCM failure.

But beyond those ethical considerations, the Archegos collapse has taught a few interesting things about US capital markets.

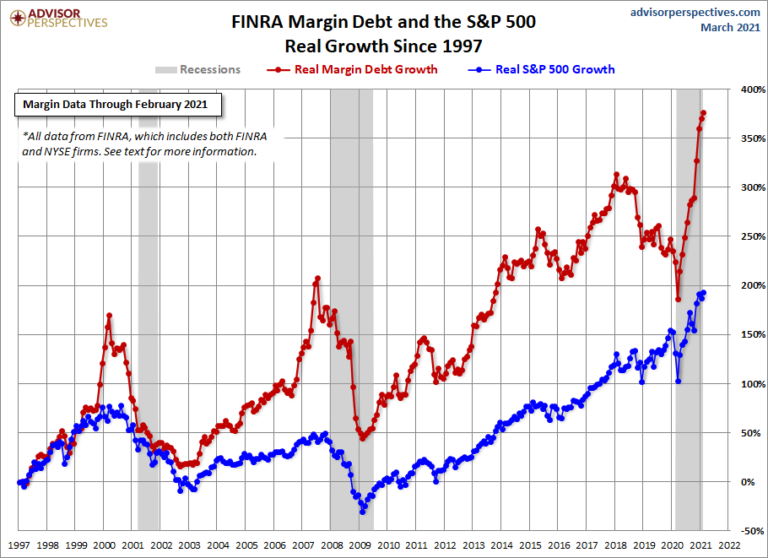

The first lesson for investors is the fact that years of lose monetary policy have laid the ground for moral hazard and very risky bets, as evidenced by the record of margin debt. And the higher the leverage ratio, the bigger the vulnerability to unexpected moves.

The subprime crisis was a perfect illustration of that issue, as it “only” took a 11% drop of US home prices and a 1.5 expansion of the delinquency rate on mortgages to funnel the global banking industry toward the cliff in September 2008. In a highly leveraged system, you do not necessarily need a violent crash to generate significant losses and trigger a bigger crisis.

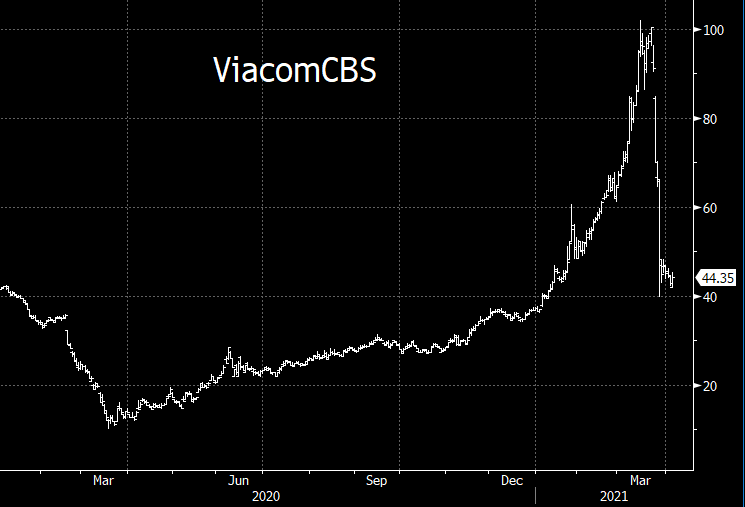

Using debt to go all-in on stocks on like ViacomCBS which had already started to move vertically was not the smartest thing to do in my opinion, as such technical patterns often signal imminent ruptures. It is hard to believe that professionals who managed those amounts of money got caught in such an absurd situation, but I do think that other players will exhibit similar losses sooner or later, as most participants have caved to the mania and have assumed that equities cannot go down anymore.

More and more participants display “Gaussian-like behavior,” meaning that they tend to unconsciously underestimate the probability of occurrence of large volatility spikes (i.e. significant drawdowns). And I am not only talking about retail investors. The whole market has turned extremely bullish, and everyone believes that “the Fed has our backs” and that there will always be someone to bid if necessary.

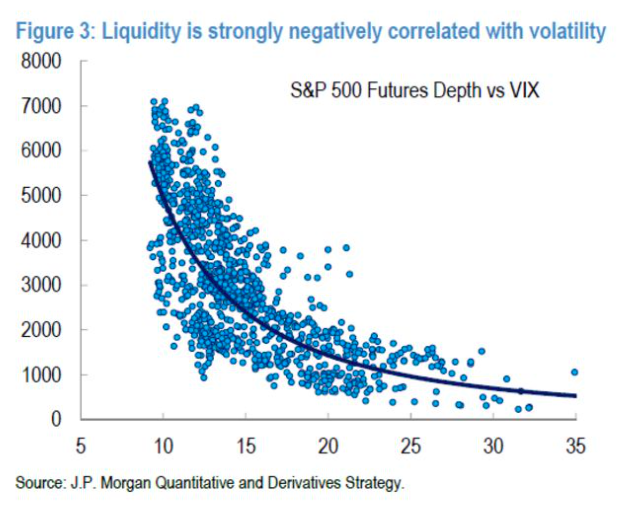

That brings us to the second lesson of the Archegos collapse, which is how illiquid can assets suddenly become when a big seller comes out.

The concept of liquidity can be very misleading, as past trading volume is no guarantee of future liquidity. Indeed, the convexity of the order book means that if the selling flows become too big, then there may be no bid unless the price adjusts significantly to the downside (I recommend the following thread on Twitter by @FadingRallies).

In fact, there is a nonlinear and negative relationship between depth and instantaneous volatility, meaning that the liquidity of equities is likely to shrink whenever the VIX spikes. Therefore, the idea that there will always be someone to bid and to buy the dip, even on large cap shares, can be proven wrong.

As the S&P 500 is trading above 4k, it is important to bear in mind that any unexpected situation leading to forced selling could trigger a problematic situation. And even though people tend to naturally display “Gaussian-like behavior,” everyone should remember that volatility spikes are distributed following some form of power law (see my paper on that topic), meaning that extreme fat-tail events occur more frequently than what the general public thinks.

And in my opinion, there is not much the Fed can do about it.

Red Queens Narratives

I often say that financial markets are all about intersubjective narratives. Thus, I have created this second section to analyze the narratives at play.

The past months have been characterized by a once-in-a-lifetime buying frenzy, with millions of retail investors entering the market as wannabee gurus like Dave Portnoy kept saying that “stocks ony go up.” The corollary of this phenomenon has been the “you only live once” philosophy (YOLO), justifying any risky trade by the idea that nothing really matters anymore on markets.

For months, we have seen people chasing stocks like Tesla, Virgin Galactic, Zoom, or Peloton, whatever the price. Then, we have seen them rushing to purchase out-of-the-money call options to maximize their profits, leading to the so-called “gamma squeeze.”

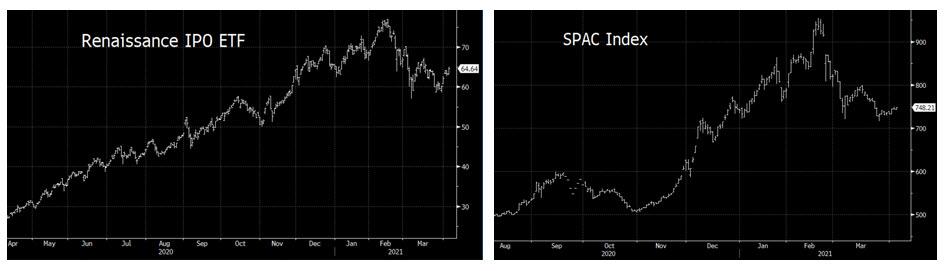

However, while everyone expected Americans to massively spend their second check on the market, the YOLO trade has started to exhibit signs of weakness recently. And as already mentioned in a previous post, the launch of the Buzz ETF may have coincided with the top of the retail mania (see Whale Beaching).

But beyond the lower volume on equity call options, it is worth highlighting the recent disappointing performance of indices tracking IPOs or SPACs (see charts below).

The thing is, there has been a record level of equity issues, and most of them were YOLO names. And not only on the stock market, as there have also been record amounts issued on the convertible bonds segment, most of the issuers being companies like Beyond Meat, Airbnb, Peloton, etc.

After all, maybe the market is reaching its digestive limits.

Even if the Nasdaq managed to bounce back to mid-February levels, the recent moves have been characterized by negative internals, meaning that US tech indices have been mainly driven by FAANGs, while many YOLO stocks have struggled to recapture the powerful trend of the past months.

Does it mean that the party is over? I have learned to be careful about calling the top, but I do believe that a bubble is all about a narrative, and thus when the dominant narrative starts to weaken, it is time to seriously question the validity of the bull thesis.

While the Biden-Harris administration continues to insist there’s ‘no border crisis‘ (as they take over seven hotels near the US-Mexico border), the departure of ‘Border Czar’ Roberta Jacobson, suggests otherwise.

Jacobson, a former US ambassador to Mexico who criticized the White House for sending ‘mixed messages‘ to asylum seekers over whether they should head for the border (which Biden absolutely implied during the 2020 election), is stepping down after less than three months on the job.

Suggesting her services were no longer needed (as ICE commandeers seven border-area hotelsbecause government facilities have run out of space), National Security Adviser Jake Sullivan said on Friday that Jacobson’s departure was “consistent with her commitment at the outset to serve in the Administration’s first 100 days,” according to the New York Post.

The move comes as the Biden administration is reportedly considering sending cash payments to Central Americans in a bid to prevent them from making the trek north and as Vice President Kamala Harris, tapped by Biden to handle the crisis, still has yet to visit the border.

Meanwhile, migrant parents already in the United States say they are not being given regular — if any — updates about the location or well-being of their children in federal custody. And it’s reportedly costing US taxpayers more than $60 million a week to care for 16,500 unaccompanied migrant teenagers and children now in federally run shelters. -NY Post

Despite thousands of migrant children sitting in US Border Patrol detention facilities – White House officials have maintained that there’s no crisis – because to do so would mean Biden sparked the crisis when he presented himself as an immigrant-friendly antithesis to President Trump – who he now blames for the border surge.

Biden’s Press Secretary Jen Psaki can’t name any “numerical” or “tangible” goal or measure that the Biden Administration has in dealing with the border crisishttps://t.co/VVMfLCBVsgpic.twitter.com/6ftE9rZu9P

Last month White House press secretary Jen Psaki accidentally referred to the “crisis at the border,” only to correct herself when pressed – calling them “challenges on the border.”

On April Fool’s Day, CNN ran an “analysis” of Joe Biden’s presidency:

Will JRB take his place alongside FDR and LBJ?

CNN explained “JRB” had just unveiled a $2 trillion infrastructure plan “to boost ordinary working Americans rather than the wealthy,” a program that together with his $1.9 trillion Covid rescue doubles “as a bid to lift millions of Americans out of poverty.”

That this high-flown language came on the heels of Biden’s people whispering F.D.R. comparisons in the ears of reporters for weeks, and Biden himself calling his plan “a once-in-a-generation investment in America,” seemed not to bother anyone. We live in a time when a president can be said to have “sharply cut poverty” the moment he signs a relief bill, so why not say, as CNN editorialists Stephen Collison and Caitlin Hu did, that this new bill’s passage would immediately allow Biden to “lay claim to a spot in the Democratic pantheon alongside Franklin Roosevelt and Lyndon Johnson?”

This would only be natural, they said, since “Scranton Joe” has long despaired over the silver spoon inequities of Donald Trump’s trickle-down economy:

The President complained as he unveiled his plan in Pittsburgh — the kind of gritty blue-collar city he loves — that the top 1% saw their wealth rise by $4 trillion during the pandemic while millions of Americans lost jobs. “Just goes to show you how distorted and unfair our economy has become,” Biden said. “Wasn’t always this way. Well, it’s time to change that.”

Left unmentioned was that the same gritty, blue-collar president oversaw the TARP bailout, which resulted in a similar Trumpian windfall for the 1%. The richest saw their share of America’s wealth increase from 30% in 2010 to 39% in 2016. Median household net worth fell 34% from a peak in 2007 to the end of the Obama-Biden presidency, while banks in 2009 had the best year they would have until 2020, that “unfair” bailout year Biden complained about.

Pundits have long been working on revising that history. By last summer, the Atlantic was writing this about Biden’s management of the other bailout:

Critics on the left faulted him and Obama for not making the stimulus package bigger (though keeping it below $1 trillion was the price of winning necessary Republican votes for its passage in the Senate).

With a partisan divide wedded to a hyper-concentrated landscape, commercial media companies can now sell almost any narrative they want. They can disappear the past with relative ease, and the present can be pushed whichever way a handful of key decision-makers thinks will sell best with audiences.

In the case of Biden, we’ve seen in the first few months that the upscale, cosmopolitan target audiences of outlets like CNN, the New York Times, and the Washington Post want to believe they’re living through a “radical,” “transformative” presidency, the political antidote to the Trump years. The same crowd of West Wing power-tweeters was leading the charge against “purity” in politics about eight minutes ago.

In fact, in the 2019-2020 primary season, Bernie Sanders was regularlylambasted by the same blue-leaning press outlets for trying to re-imagine F.D.R. through programs with names like the “Green New Deal.” Proposal after proposal that had been directly inspired by F.D.R. was described as too expensive, unrealistic, or a political non-starter heading into a general election.

Now that the real version of that brand of politics has been safely eliminated, a new PR campaign is stressing that Democrats did elect F.D.R. after all. Moreover, a legend is being built that crime-bill signing, PATRIOT-Act inspiring, Iraq-war-humping Joe Biden wanted all along to be a radical progressive, but was held back by the intransigence of the evil Republicans. Is that even remotely true?

Observe, for instance, the hilarious Ezra Klein editorial that just ran in the New York Times, called “Four Ways to Look at the Radicalism of Joe Biden” (someone actually wrote that headline!):

Before Biden, Democratic presidents designed policy with one eye on attracting Republican votes, or at least mollifying Republican critics. That’s why a third of the 2009 stimulus was made up of tax cuts, why the Affordable Care Act was built atop the Romneycare framework, why President Bill Clinton’s first budget included sharp spending cuts…

Over the past decade, congressional Republicans slowly but completely disabused Democrats of these hopes. The long campaign against the ideological compromise that was the Affordable Care Act is central here…

The result is that Obama, Biden, the key political strategists who advise Biden and almost the entire Democratic congressional caucus simply stopped believing Republicans would ever vote for major Democratic bills.

Question for Ezra: did Obama also accelerate the drone program, expand the surveillance state, and abandon enforcement of white-collar crime to a degree that made John Ashcroft look like Eliot Ness, in a similar effort to reach across the aisle? Or were those Executive Branch behaviors just expressions of unrequited love?

Obama as a presidential candidate in 2008 contrasted himself with Hillary Clinton by insisting he would be the guy to stop kowtowing to special interests. On health care, he was incredibly specific: he would green-light drug re-importation from Canada and allow Medicare to negotiate bulk pharmaceutical prices, insisting also he was a “proponent” of single-payer.

Obama went so far as to do an ad blasting former Louisiana congressman Billy Tauzin, who went from helping write the ban on Medicare bargaining to going to “work for the pharmaceutical industry making two million dollars a year” at the lobbying group PhRMA.

“Imagine that,” said Obama. “That’s an example of the same old game‐playing in Washington. I don’t want to learn how to play the game better. I want to put an end to the game‐playing.”

The year after this ad ran, Obama was meeting with that same Billy Tauzin in, ironically, the Roosevelt Room of the White House (Tauzin would end up visiting a dozen times). There, they hammered out a deal: Tauzin’s group, PhRMA, would fund a $150 million ad campaign boosting Obama’s health care program, in exchange for the Obama White House agreeing to kill the reimportation idea and leave the ban on Medicare negotiation in place.

Tauzin later described the deal, saying it had been “blessed” by the White House, and emails later released showed a union official who was part of health care bill negotiations explaining how Obama’s White House planned on paying for its PR campaign: “They plan to hit up the ‘bad guys’ for most of the $.”

Obama in other words won a contentious primary against Hillary Clinton by snowing reporters like me into hyping him as the clean hands guy who’d push aside Clintonian transactional politics. Then he turned around a year later and passed his signature program with help from the worst industry actors, paying for it by killing the progressive parts of the plan.

This history — important history — is now being rewritten by people like Klein as an “ideological compromise” inspired by the Obama/Biden White House’s misguided desire to govern with Republican votes. The fact that the Affordable Care Act passed with a grand total of zero such votes is apparently irrelevant, as was Biden’s ignored and erroneous (do we only say “lie” in some cases?) insistence as a candidate last year that he found “Republican votes” for “Obamacare.”

Something like Obama’s PhRMA one-two is happening again, and predictably, it’s not getting much press. A hundred countries have formally asked the World Trade Organization to waive intellectual property laws that only allow companies like Pfizer, Moderna, and AstraZeneca to make Covid-19 vaccines. Favoring the waiver: Sanders, Elizabeth Warren, and hundreds of millions of poor and mostly nonwhite folks in other countries who are nervous about the whole dying thing.

Opposing (drumroll, please): that same PhRMA lobbying group, which says such waivers would “undermine the global response to the pandemic, including ongoing effort to tackle new variants.” Meaning, industry will stop developing vaccines now, and certainly won’t develop any the next time, if you don’t let it cash in.

Without the ability to make generics, countries like Mexico have to be grateful for handouts of some of the tens of millions of excess vaccine doses we have sitting in storage. In fact, in what the New York Times called a “notable step into vaccine diplomacy,” Biden agreed to send 2.5 million doses to Mexico in return for Mexico promising to increase patrols on its southern border with Guatemala.

To recap: while waffling on patent waivers, Biden traded 2.5 million doses of vaccine to Mexico for a promise to crack down on the Central American migrants who have become a pain in this administration’s public relations tuchus. Perhaps Biden eventually will push for the patent waivers, but for now, does anyone even have to ask what the headlines describing that kind of lives-for-fewer-immigrants deal would have looked like if Trump brokered it?

This has so much been the story of Biden’s presidency, which is certainly less chaotic than Trump’s and does have some clearly different ambitions, but in many ways represents continuity with both his predecessor and his predecessor’s predecessor.

What would we have said if Trump promised to stop wall construction, then went ahead and kept building it anyway? Candidate Biden promised not to build “another foot of wall,” and although it is true that he’s frozen Defense Department funding for Trump’s project, his Homeland Security Secretary Alejandro Mayorkas said the decision left “room” for the administration to “make decisions” about “areas of the wall that need renovation and “particular projects that need to be finished.” So F.D.R. is building more wall.

Others have made plenty of hay about the discrepancies in covering unaccompanied child detainees now, versus a few years ago. Agencies from the AP to the Washington Post are using the word “challenge” instead of “crisis” or “horror.” It’s of course only a coincidence that this is the word Press Secretary Psaki started using back on March 18th (correcting the use of “crisis”).

The cries of hypocrisy about the non-use of the term “kids in cages” is, I think, overblown, because separating children from families was an intentional aim of the Trump administration — remember, Trump officials were hoping for a lot of media coverage about separated kids, with the specific aim of producing a “substantial deterrent effect.” That was substantially more deranged than any Biden policy. That doesn’t make it not ridiculous that the Washington Post called the following structures “migrant facilities”:

When pressed on the absurdity, the Post noted that it hadn’t necessarily said what was happening at the border was a good thing, even quoting activists saying it was a “huge step backward.” The Post hastened to add that the same activist said of the Carrizo Springs, Texas facility, “I consoled myself with the fact that it was considered the Cadillac of [migrant child] centers.”

Again, is it hard to imagine what the response would have been if anyone, inside or outside the Trump administration, had tried to sell us on the idea that immigrant kids were staying in the “Cadillac” of detention centers? The “Cadillac cages” and “Cadillac concentration camps” jokes would have written themselves.

The dull truth about Biden is that he’s governed, domestically, as a slightly more progressive version of the Obama administration, with a more ambitious bailout, while his foreign policy is a notch or two more hawkish — a wash, overall, though most of the stories about policy continuity from Afghanistan to Iran to Ukraine and beyond, don’t get headlines.

During the recent all-consuming furor over the Major League Baseball all-star game, for instance, news that the federal defense budget under Biden will likely remain at the same astronomical levels they reached under Trump went mostly unnoticed. A few outlets that paid attention used the common defense industry talking point that the numbers actually represented a cut, since the increase was smaller than the rate of inflation. Same with Biden’s continuation of the storied presidential tradition of punting on withdrawal of support for Israel’s occupation of Palestine territories, reported via headlines like, “Joe Biden is not planning to solve the Israeli-Palestinian conflict.”