“You’re Bull*hit Beto!” O’Rourke Flattened By Female Trump Supporter In Viral Pro-Gun Rant

Democratic presidential candidate Beto (Robert Francis) O’Rourke was taken to task by an angry Trump supporter in Newtown, Connecticut – who slammed the former congressman for trying to ‘hijack this town’ and ‘make an issue out of getting guns out of good people’s hands.”

“This is bullshit,” said Rebecca Carnes – a vocal Trump supporter who says she’s a “third-generation” resident of Newtown – where the Sandy Hook elementary school shooting took place in 2012. “It’s about mental health and it’s about this war on boys and masculinity,” she added. “You’re bullshit by being here, shame on you Beto.”

“Why don’t you debate me?“

Here are the top five reactions to Beto’s beatdown on Fox 61‘s YouTube channel, in order of popularity:

“Bitchy Beto can’t say shit cos it’s not Anderson Cooper who’s asking him the questions.”

“It would have great to have seen Beto’s face after that dress down.”

“In Beto’s defense, it is important to remember that Epstein did not kill himself.”

“I’d say that she probably has more testosterone in her system than Beto O’Dork, but I think most women probably do.”

“Good for her.

More people need to be made aware that Newtown has voted more for the republican candidates, in many of the recent local and general elections.

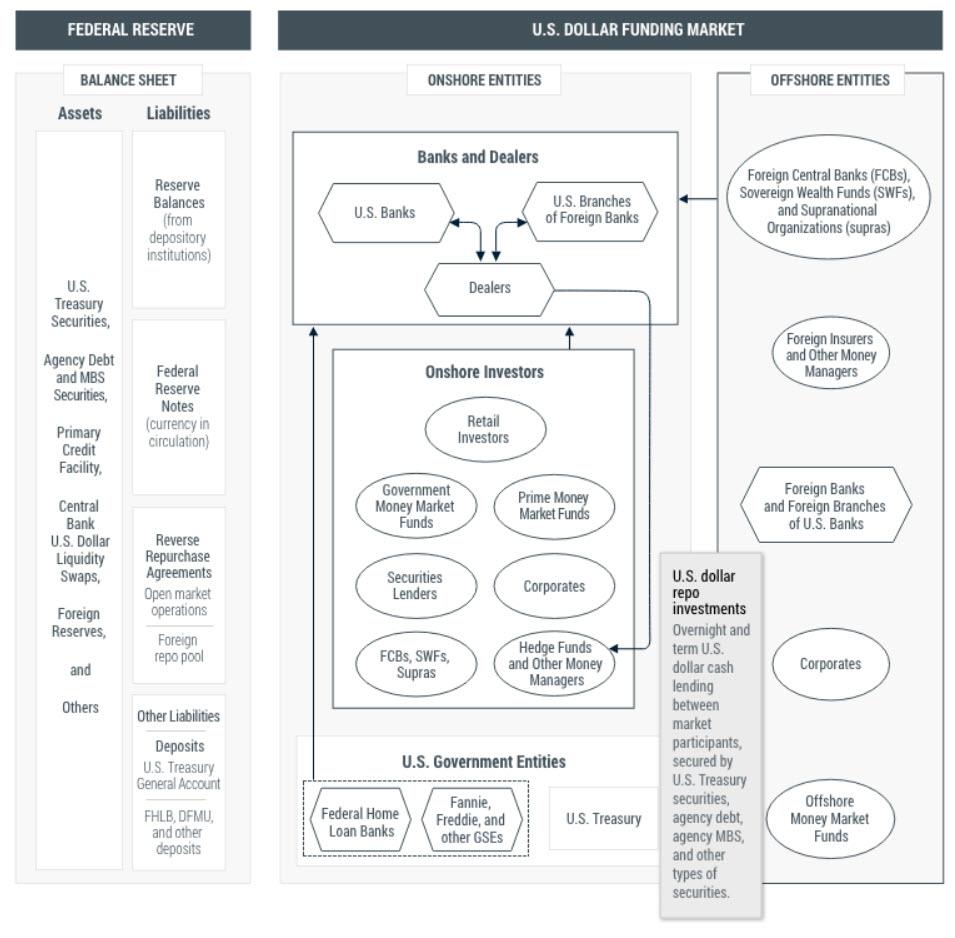

The Federal Open Market Committee cut the target for short-term funds another quarter point last night, raising the question as to whether the central bank can actually defend the 1.75% upper bound of the new policy range. Fact is, demand for short-term funding is pulling rates higher as the year draws to a close.

Ray’s Camp, The Flowage, Princeton, Maine

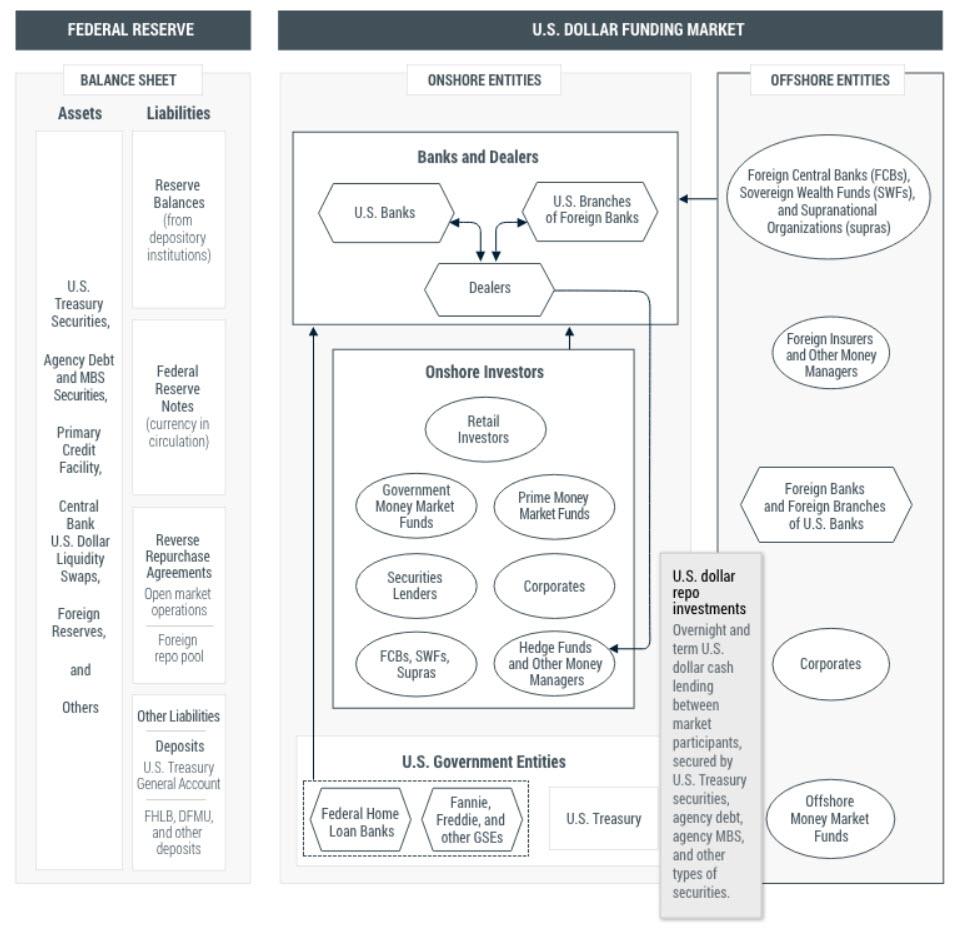

We got to dine with the risk committee this week, revealing new aspects of the recent repo kerfuffle that deserve mention. Chief among them was the idea of competition and, indeed, even conflict between the retail bank side of the house and the capital markets component inside the Fed’s primary dealers.

It seems that when the Federal Reserve Board was caught napping in mid-September, the bank treasury side of one of the largest US banks basically took a line from the 1990 Martin Scorsese film “Goodfellas” and told the bank’s capital markets side: “Fuck you, pay me.”

Under Regulation W, which implements what we traditionalists know as Section 23A of the Federal Reserve Act, transactions inside the bank holding co do not count against the bank’s statutory allocation for transactions with affiliates. But when market rates spiked, the retail treasury representing a very large insured depository, essentially told the traders to pound sand when it came to price. Reg W requires transactions with affiliates to be at market on an arm’s length basis, even with risk-free collateral supporting the trade.

The lesson here is that regulators do not want the cash-rich retail bank to give carte blanche to the traders, either with respect to the amount of liquidity or the price. The regulatory system worked – but also caused a new problem. A rush of fully motivated capital markets banksters suddenly turned outward and sought funding in the broader market for federal funds.

A squeeze ensued on or around September 16th, needless to say. Risk free collateral went begging for funding. Effective rates to finance Treasury and GNMA collateral spiked to double digits. So then, ask not whether one aspect of federal prudential regulations or another caused the liquidity squeeze seen last December and in June and later in September.

Ask instead why the Fed and other regulators cannot cooperate to tweak the system and fix da plumbing. December is just a month away. The reality, as F.A. Hayek described in his classic 1988 essay “Fatal Conceit: The Errors of Socialism” is that fine tuning the markets is an impossibility. The Fed suffers from the “fatal conceit” that “man is able to shape the world around him according to his wishes.”

Happy Halloween

Softbank Denies WeWork Control??

Meanwhile in the world of finance, a couple of notable events and comments occurred that deserve comment. PIMCO announced that it is reducing allocations to corporate debt, another data point on our worry beads regarding corporate credit in 2020.

Our favorite was the blasé Street reaction to the announcement by Softbank that its 80% stake in the insolvent WeWork did not mean control. Hello?? Further, Masayoshi Son indicated that therefore the company would not be consolidated onto Softbank’s balance sheet. Really? If this transparent evasion of leverage disclosure does not qualify for securities fraud in the US, then we need to buy some new textbooks.

Several managers, ratings firms and former shareholders complained about a “lack of controls” at Softbank in a Wall Street Journal article by Phred Dvorak and Justin Baer, but when one man is in charge is this even up for debate? We have always viewed Softbank as an investor driven Ponzi scheme, but we suspect our readers already knew that.

Of note, we also were reminded over dinner that no less than Deutsche Bank AG (DB) has been the advisor and lender for much of Softbank’s issuance of securities. Would be funny were it not so very sad, especially for the credulous sovereign investors in Softbank. The whole vision thing strikes us as a grotesque speculation verging on outright fraud. On Wednesday, DB reported a third-quarter loss of $955.1 million or about 10% of total revenue, after reporting a profit in the same period a year earlier.

The Softbank strategy goes like this: Give me and lend me enough capital and I will corner the market for innovation or some such version of that theme. We recall that Jim Fisk and Jay Gould attempted a similar operation in the late 1860s. Their machinations resulted in Black Friday September 24, 1869, the first modern financial crisis. Their scheme to corner the gold market – and ensnare President Ulysses Grant in the operation — collapsed in spectacular fashion, leading the US into a credit crisis. Gold, after all, was money in those days.

DOJ/HUD Accord Reached

Hannah Lang of National Mortgage News reports that Department of Housing and Urban Development Secretary Ben Carson announced that HUD and the Department of Justice released a joint a memorandum of understanding, stating that HUD will deal with False Claims Act violations — involving Federal Housing Administration (FHA) lenders — mainly through administrative proceedings. This is a big deal for HUD and the mortgage industry, which has been brutally raped since 2008 to the tune of tens of billions of dollars by a succession of ambitious politicians.

One of the main reasons why Senator Kamala Harris (D-CA), who served as the state’s AG during the 2012 National Mortgage Settlement, won higher office was the billions she extracted from the shareholders of JPMorgan (JPM), Bank America (BAC) et al. And this is why a very angry Jamie Dimon publicly took Chase out of the FHA loan market immediately after, followed by hundreds of other banks.

Today only Wells Fargo & Co (WFC) and Flagstar Bank (FBC) remain as significant bank issuers and servicers of GNMA securities in the FHA/VA/USDA loan market. As former GNMA President Ted Tozer told us last week, without the bond market execution of GNMA-guaranteed securities the FHA/VA/USDA programs are moribund.

We salute Secretary Carson and FHA chief Brian Montgomery for getting this interagency understanding done, but the banks won’t come back to the FHA/VA loan market until 1) the cost of servicing GNMA securities is brought into line with the GSEs Fannie Mae and Freddie Mac and 2) profitability on origination of FHA/VA loans improves a lot more. GNMA MSRs should trade even yield to conventional mortgage servicing assets.

Perhaps the bigger challenge for HUD is convincing the Fed, OCC, FDIC and other prudential regulators to allow large banks to return to the FHA market. So long as the federal regulatory community sees small, low FICO, high LTV loans as being “unsafe and unsound,” the banks are unlikely to return fully to the GNMA market. Small loans are loss leaders. Would you rather service a $280,000 FHA loan for 32bs per year gross or a $3 million prime jumbo loan at 25bps per year?

Are ‘Green Bonds’ The “But It’s For The Children” Trojan Horse For MMT?

While still small, sustainable financing is growing. There’s been $165 billion of so-called “green”-bond issuance from companies and countries this year – more than double 2016’s total – according to data compiled by Bloomberg.

And, under pressure from ‘the people’ demanding policymakers “do something” to save the world from almost certain climate-driven doom, Bloomberg reports that central banks are putting their money-printing malarkey to work in sustainable financing, opening up a new source of demand for the budding asset class.

Most major central banks have signed on to promote sustainable growth, offering incentives that encourage green financing.

“Central banks are important institutional investors, and the fact that they are participating in this market, it gives the market almost like a seal of reliability and maturity,” said Christian Deseglise, global head of central banks and global sponsor of sustainable finance at HSBC Holdings Plc, the biggest underwriter of the bonds this year.

“It’s not so much about adding demand, because we already have demand,” he said. “It’s the quality of that demand that’s really important.”

The European Central Bank has been buying the debt as part of its asset repurchase program.

Hungary and France’s central banks have each created funds dedicated to ecological investments.

Now Peru is considering buying green bonds, too.

While the Federal Reserve, with nearly $4 trillion on its balance sheet, is notably absent from the Network for Greening the Financial System, regional branches have published research on the topic, and Chairman Jerome Powell maintains that it’s a “longer-run issue.”

However, as Bloomberg notes, pricing and liquidity are still limiting factors. As green bonds become more mainstream, investors are offered little additional incentive to buy them as they price comparably to non-green debt.

“As soon as the green-bond market becomes sizable you’ll see central banks investing more in green bonds,” according to Massimiliano Castelli, head of sovereign strategy at UBS Asset Management.

Of course, as most are aware, “green”-bonds are largely a marketing gimmick, and if central banks really do escalate their buying, then you don’t need a crystal ball to forecast that there will be a rise in companies’ “Greenwashing” their issuance – using green labels to spend on not so green things!

The Forest Resilience Bond (FRB) is a financial tool that enables private investment in forest enhancements on public land. The FRB promises to accelerate the pace and scale at which critical work to restore the health and functioning of the nation’s forested landscapes is undertaken.

It does so by engaging private capital to cover the upfront cost of activities to improve forest health and by bringing together stakeholders that benefit from this work to share in the cost of reimbursing investors over time. These beneficiaries sign contracts that jointly cover the project cost plus a modest return to investors, meaning that no one stakeholder shoulders the burden of repayment alone. The result is a collaborative finance model that yields clear ecological, social, and financial returns.

While perhaps less obvious, the FRB model also unlocks opportunities for positive social impact in rural communities across the country. In addition to the direct impact of job creation, FRB projects can catalyze infusions of capital into rural areas by sending signals to the market that there is a steady supply of raw material to fuel forest-based industries. Against a backdrop of declining rural prosperity, this article envisions how the FRB could play a role in assisting rural areas – especially those with historically forest-based economies – transition to a more resilient ecological and economic future.

…

What differentiates the Forest Resilience Bond (FRB) from other approaches is not only its use of investor capital to fund restoration quickly and at scale, but the collaborative model of cost sharing between beneficiaries.

This approach engages a range of stakeholders to split the cost of repaying investors and involves them in project development. As such, the FRB model encourages a collaborative systems-level response to forest health challenges that makes use of funds, experience, and expertise from a range of public, private, and civic stakeholders.

Or, put another way, it’s a public-private partnership that levers taxpayer funds to support ‘green’-led initiatives, without the need for voting (because the central banks are unelected!)

So, to summarize, the concept of “green”-bonds is becoming more and more mainstream – who cares if we don’t get any yield, at least we are signaling just how virtuous we are – and as various ‘wealthy’ western nations hit the monetary and fiscal policy wall, the rhetoric around “People’s QE” or a Modern-Monetary-Theory-driven (MMT) redistribution spreads positively among many (especially the socialism-supporting Millennials).

While common-sense destroys the radical concepts behind MMT, we would argue that “green”-bonds are the perfect trojan horse to create a narrative that monetizing debt “that’s good for the world” is something ‘no one’ can argue with… Let’s just hope not, for the sake of our children’s future loss of purchasing power.

“Central banks are already buying green bonds and they should be buying more,” said Ulrich Volz, director of the SOAS Centre for Sustainable Finance in London. “But at the end of the day we need a mainstreaming of responsible investing across all assets.”

Of course, we look forward to the issuers of “green”-bonds explaining how their bonds mature past the world’s apparent sell-by date in 10-12 years depending on which climate-extremist you ask.

Today, Oct. 31, marks eleven years since the publication of the Bitcoin white paper by the still-mysterious person or group pseudonymously identified as Satoshi Nakamoto.

Bitcoin: A Peer-to-Peer Electronic Cash System — published on Oct. 31, 2008 — outlined a tamper-proof, decentralized peer-to-peer protocol that could track and verify digital transactions, prevent double-spending and generate a transparent record for anyone to inspect in nearly real-time.

The protocol represented a cryptographically-secured system — based on a Proof-of-Work algorithm — in which Bitcoins (BTC) are “mined” for a reward by individual nodes and then verified by other nodes in a decentralized network.

This system contained the possibility of overcoming the need for intermediaries such as banks and financial institutions to facilitate and audit transactions — a major disruption to a siloed, monopolized field of centralized financial power.

Eleven years on, Bitcoin is consistently setting new records for its network hash rate — a measure of the overall computing power involved in validating transactions on the blockchain at any given time.

More power and participation establishes greater network security and attests to widespread recognition of the profitability potential of Bitcoin mining.

As of the middle of this month, network data revealed that since the creation of the very first block on the Bitcoin blockchain on Jan 3, 2009 — known in more technical language as its “genesis block” — miners have received combined revenue of just under $15 billion.

The figure includes both block rewards — “new” bitcoins paid to miners for validating a block of transactions — as well as transaction fees, which broke the $1 billion mark this week.

Bitcoin’s first-ever recorded trading price was noted on Mar. 17, 2010 — on the now-defunct trading platform bitcoinmarket.com, at a value of $0.003.

The cryptocurrency’s appreciation thus stands at a staggering 304033233% as of press time, with Bitcoin currently trading at $9,120.

As of this August, 85% of Bitcoin’s supply in circulation had been mined — leaving just 3.15 million new coins for the future.

Eleven years on, the mystery enshrouding the white paper’s author remains as impenetrable as ever.

Those both within and without the crypto community began attempting to determine Nakamoto’s identity as early as October 2011, just a few months after the mysterious figure first went silent.

What Ethics Violation? Katie Hill Blames Departure On Nudes Leaked “For The Sexual Entertainment Of Millions”

Democratic Rep. Katie Hill of California, who wrote the world’s lengthiest non-apology while resigning under a House Ethics Committee probe into allegations that she slept with an employee, gave her final swan-song on the House floor on Thursday, where she blamed leaked nudes and mysoginy (and not her own ethics violation) for her departure.

“I am leaving now because of a double standard. I am leaving because I no longer want to be used as a bargaining chip. I am leaving because I didn’t want to be peddled by papers and blogs and websites, used by shameless operatives for the dirtiest gutter politics that I’ve ever seen,” Hill said, adding that her nude photos were shared “for the sexual entertainment of millions.“

WATCH: Katie Hill believes her leaked nudes were the somehow the “sexual entertainment of millions.”

Explicit photos of Hill were published in the Daily Mail and other publications, while allegations that she and her husband had a separate relationship with an unnamed female campaign staffer resulted in the ethics investigation.

“I am leaving because of a misogynistic culture that gleefully consumed my naked pictures,” Hill added in her Thursday comments. “The forces of revenge by a bitter jealous man, cyber exploitation and sexual shaming that target our gender and a large segment of society that fears and hates powerful women have combined to push a young woman out of power and say that she doesn’t belong here.”

Not saying Katie Hill has a bit of an ego problem… just saying that in her resignation speech, she said that her nude photos were shared “for the sexual entertainment of millions.”

Hill then turned her ire to President Trump, saying it’s unfair that “a man who brags about his sexual predation, who has had dozens of women come forward to accuse him of sexual assault, who pushes policies that are uniquely harmful to women and who fills the courts with judges who proudly rule to deprive women of the most fundamental right to control of their own bodies, sits in the highest office of the land.”

We weren’t aware that President Trump was sleeping with employees.

Where is the line between “working class” and “middle class”? Maybe there isn’t any.

Defining the “middle class” has devolved to a pundit parlor game, so let’s get real for a moment (if we dare): the “middle class” is no longer defined by the traditional metrics of income or job type (blue collar, white collar), but by an entirely different set of metrics:

1. Household indebtedness, i.e. how much of the income is devoted to debt service, and

2. How much of the household spending is funded by debt.

3. The ability of the household to set aside substantial savings / capital investment.

4. The security of the households’ employment.

5. The dependence of the household wealth on speculative asset bubbles inflated by central bank policies.

6. The percentage of the household income that is unearned, i.e. derived not from labor but from productive assets.

7. The exposure of the households’ employment to automation, AI or offshoring.

8. How much of the household income is government transfers: benefits, subsidies, etc.

After writing about the middle class and America’s class structure in depth for over a decade, it seems to me the actual, real-world class structure is something along these lines:

1. No formal earned income, dependent on government transfers, possibly supplemented by informal “black market” income; no family wealth.

2. The Working Poor, those laboring at minimum wage or part-time jobs with few if any benefits. This class depends on government transfers to get by: EBT (food stamps), housing subsidies, school lunch subsidies, Medicaid, etc. Highly exposed to reductions in hours, tips, gigs, etc. and layoffs.

3. The “muddle class” which muddles through on earned income, much of which goes to debt service (student loans, auto loans, mortgages, credit cards) and skyrocketing big-ticket expenses: rent, healthcare, childcare, etc. Unable to save enough to move the needle on household capital, any net worth is dependent on speculative asset bubbles continuing to inflate. Highly exposed to layoffs or destabilizing changes in employment status: from full-time to part-time, loss of benefits, etc.

4. The Protected Class with secure income/earnings and benefits: this includes the nomenklatura of government employees, mid-level technocrat / managerial employees in academia, government-funded non-profits, etc., and retirees with Medicare, Social Security and other income (pensions, unearned investment income, etc.) and family assets (home owned free and clear, substantial 401K nest eggs, etc.)

5. “Winner Take Most” Corporate America / market-economy households: top managers and salespeople, entrepreneurs, successful business owners, speculators in financialization/asset bubbles, marketers, those earning substantial royalties, etc. Most work crazy-hard and make sacrifices, as per this article from The Atlantic: Why You Never See Your Friends Anymore: Our unpredictable and overburdened schedules are taking a dire toll on American society.

6. The wealthy and super-wealthy. Many continue working hard despite being worth tens of millions or hundreds of millions of dollars, as per this article from NYT.com: Why Don’t Rich People Just Stop Working?Are the wealthy addicted to money, competition, or just feeling important? Yes.

7. The upper reaches of this class constitute a Financial Aristocracy / Oligarchy / New Nobility, those who have leveraged mere wealth into political, social and financial power.

8. The Mobile Creatives Class, currently small but expanding, which essentially obsoletes the entire status quo of working for an employer (often to get benefits), going heavily into debt for a college degree, vehicle, house, wedding, etc., hiring employees and paying outrageous prices to live in an overcrowded, soul-destroying city, etc.

Where is the line between “working class” and “middle class”? Maybe there isn’t any. The old definitions of working and middle class were social more than financial–the middle class was better educated (school teacher, etc.) than the working class (factory worker, skilled tradesperson) but both could aspire to owning a home and giving their children a more secure life than they had started with.

The working class was not limited to the working poor: working-class jobs provided security and social mobility, just like white-collar middle class jobs.

What differentiates classes now is debt, employment security and the ability to build household capital that isn’t just a sand castle of speculative bubble “wealth.” The worker with tradecraft skills (welding, logger, etc.) has more security and earning power than a college graduate with few skills that can’t be outsourced or automated.

Many college graduates work in sectors that are highly exposed to layoffs and downsizing once the economy contracts: food and beverages, hospitality, etc.

All of which leads us to a highly verboten conclusion: both political parties and the corporate media have abandoned the 2/3 of the workforce that is working/middle class. The bottom 20% dependent on government transfers has more security than those earning just enough to disqualify the household for transfers, while the top 15% in the Protected Class are doing just fine unless they’re over-indebted.

The winner take most class and the wealthy dominate both political parties and the media which is now dependent on advertising that appeals to the top 10% of households that collect more than 50% of the national income.

The political parties take care of the government dependent class to keep the rabble from rebelling, and they keep the government gravy train flowing to the Protected Class (healthcare, national defense, academia, government employees) to insure their support at election time, but they take their marching orders from the Aristocracy / Oligarchy that fund their campaigns and enrich them with $100,000 speaking fees, seats on the board of directors, etc.

The Working/Middle Class gets nothing but lip-service, and that’s been the case for decades. The political parties and the media abandoned the Working/Middle Class long ago, buttering their bread with the soaring wealth of the Aristocracy / Oligarchy and relegating everyone outside the Protected Class who labors for their livelihood to the servitude of politically impotent tax donkey / debt-serfdom.

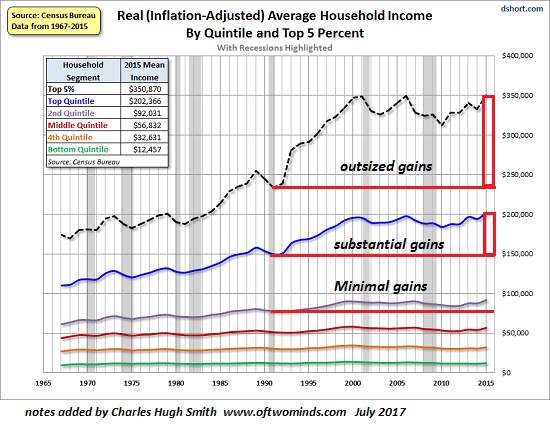

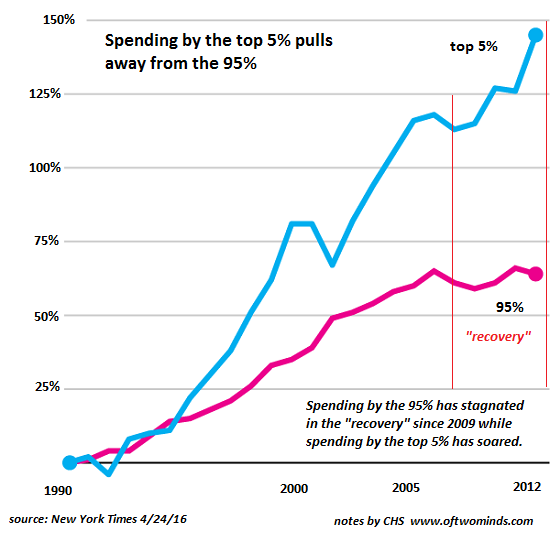

Please examine these charts closely. They look busy but show that income inequality has been rising for over three decades.

Here’s income by quintile. The top 5% have done extremely well, the Protected Class 15% below them have done just fine, and the bottom 80%, well, who cares about them as long as they’re politically passive and make their loan payments?

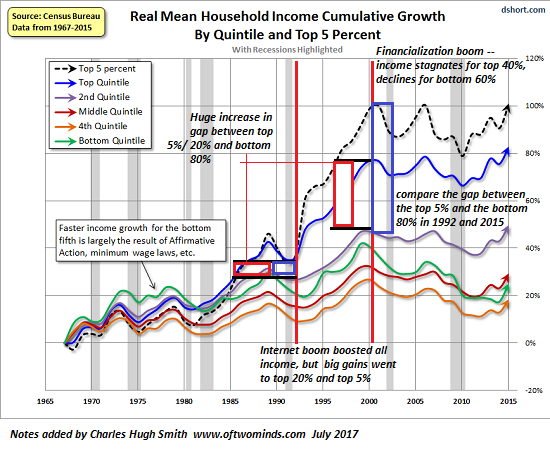

Cumulative income reveals the widening gap between the bottom 80% and the top 5%. The gap was not very big in the early 1990s, but look at it now:

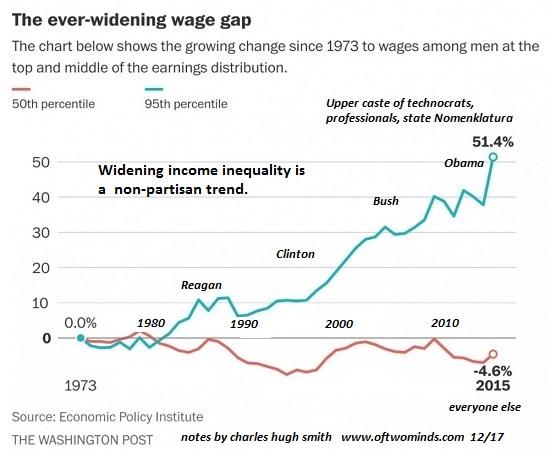

Another chart of the top 5% pulling away from the rest of us:

No wonder the media depends on luxury/aspirational advertising: the top 5% are the only ones with the money and credit to blow on status-signifying fripperies:

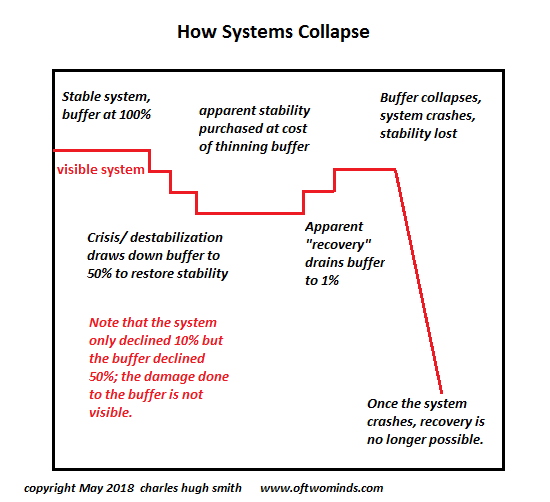

Where does this lead? To this–a collapse of buffers: debt is not income, and eventually the buffers of borrowing more to keep afloat thin and break down. When the financial buffers of the middle two-thirds of working / middle class households break down, the economy and the social-political order will break down, too.

Don’t think it won’t happen just because it hasn’t happened yet.

ISIS Spy Who Betrayed Al-Baghdadi Likely To Receive “All Or Part” Of $25 Million Bounty

The Islamic State militant who betrayed ISIS leader Abu Bakr al-Baghdadi was motivated by revenge, according to NBC News.

“I think he was under a lot of pressure from his family,” Gen. Mazloum Abdi – commander of the Kurdish-led Syrian Democratic Forces, said in a detailed account of how he spent months handling the spy inside the inner circle of the terrorist organization’s now-dead leader.

“His relatives were subjected to harsh treatment by ISIS and he no longer believed in the future of ISIS. He wanted to take revenge on ISIS and al-Baghdadi himself,” added Abdi.

“He was, you could say, a security official,” the general added. “A personal security official for al-Baghdadi himself, in charge of al-Baghdadi’s movements.”

Part of the informant’s job, Abdi said, was “securing the places” where al-Baghdadi would later hide.

This ISIS spy memorized the locations and layouts of al-Baghdadi’s safe houses and even stole samples of the world’s most wanted terrorist’s blood and clothing for DNA analysis, he said.

None of that was easy.

“Al-Baghdadi took his security precautions to the highest level,” Abdi said. “He never used high-tech communications at all. Any place he was in, was in a communications blackout, with exception of those who were directly responsible for his security, and that was a small group of people.” –NBC News

“His direct family, the children, his relatives, his siblings, they are formed a tight ring around him,” said Abdi, adding that the ISIS leader only allowed a small group of outsiders to meet with him – the spy being one of them.

What’s more, the spy is likely to receive some or all of the $25 million bounty for al-Baghdadi’s head according to the report.

“We confirmed that (al-Baghdadi) had been moved to Idlib in April of this year,” said Abdi – who wouldn’t reveal when or how his forces first made contact with the ISIS informant. Over the last five months, however, the relationship ‘deepend and expanded dramatically‘ according to the report.

Idlib was an unlikely place for the ISIS leader to hide. The province is largely controlled by other Islamist groups, including one linked to al Qaeda that is often called the Al-Nusra Front. The group has, at times, fought against ISIS. Abdi said al-Baghdadi was hiding among a pocket of supporters, in what was largely unfriendly territory.

“The idea that al-Baghdadi was in Idlib was completely unexpected,” Abdi said. “It was a surprise to everyone.”

Idlib is a large province with a varied terrain, including hills, canyons, olive groves, and several large towns and cities. Abdi said the spy’s meetings in Idlib were frequent but inconsistent. Kurdish intelligence officials said the spy could not approach the ISIS leader at will, but had to wait to be called for meetings. The face-to-face meetings — ostensibly to talk about security, movements, transportation and setting up future safe houses — would turn out to be critical. –NBC News

In order to determine where exactly al-Baghdadi was staying in Idlib province, the spy had to rely on his senses and memory according to Abdi. Bodyguards for the ISIS leader would pick him up in a car or taxi. Because of his trusted position, he was one of the few al-Baghdadi visitors who did not have to wear a blindfold on the journey. He was simply asked not to look out the car windows.

“When they approached the area, they would ask him to lower his seat so he can’t look around,” said Abdi. “They asked him to lie down, to lower the seat in the taxi.”

Even with the seat down, the spy was able to glean enough of the local topography to tell roughly where he was.

Once inside al-Baghdadi’s hideouts — and there were several, in close proximity to each other — the spy was able to look around freely, the general said.

He started memorizing the internal spaces and distinguishing structural features that could be seen from above, like a red water tank on a roof.

Those details, Abdi said, were fed constantly back to the Kurds and, through them, to American intelligence agencies, enabling U.S. aerial surveillance to pinpoint al-Baghdadi’s final hideout. The descriptions of the compound helped American commandos plan their assault.

“He provided information about the house itself, the shape of the house and things to do with the house, the specifications of the house,” Abdi said. –NBC News

“We learned that there was a tunnel in the house,” said Abdi. “We learned how many people in the house, how many guards were in the house. We learned the closest al-Nusra checkpoints near the house. We learned all the security details of the house.”

US intelligence required proof, however, that the informant wasn’t lying. In order to prove himself, the spy stole a pair of al-Baghdadi’s underwear and, later, a blood sample to compare with known samples of the ISIS leader’s DNA from when he had been in US custody in Iraq.

Abdi said the spy stole underwear roughly three months ago from a house al-Baghdadi had previously used and abandoned. He wouldn’t say how the blood was collected, only that it was taken about a month ago. Abdi said both DNA tests matched, proving the spy’s bona fides.

“After that, the CIA took this more seriously,” Abdi said. “They began to work hard and serious on the highest level.”

Meanwhile, President Trump’s decision to suddenly pull US troops out of northern Syria and Turkey’s subsequent invasion meant that Kurdish-led forces had to shift their focus on defending themselves.

At the same time, al-Baghdadi was preparing to move locations yet again.

“Al al-Baghdadi had prepared a new house for himself in a different place located in the area of Dera al-Fraat (Jarablus area),” said Abdi. “That house was ready. I assume that within 48 hours he would have left the house to the new house, and the new house was completely different and wasn’t known.”

And while the spy was at the compound when US Special Forces attacked, “He was there and he returned safely with the American forces,” according to Abdi.

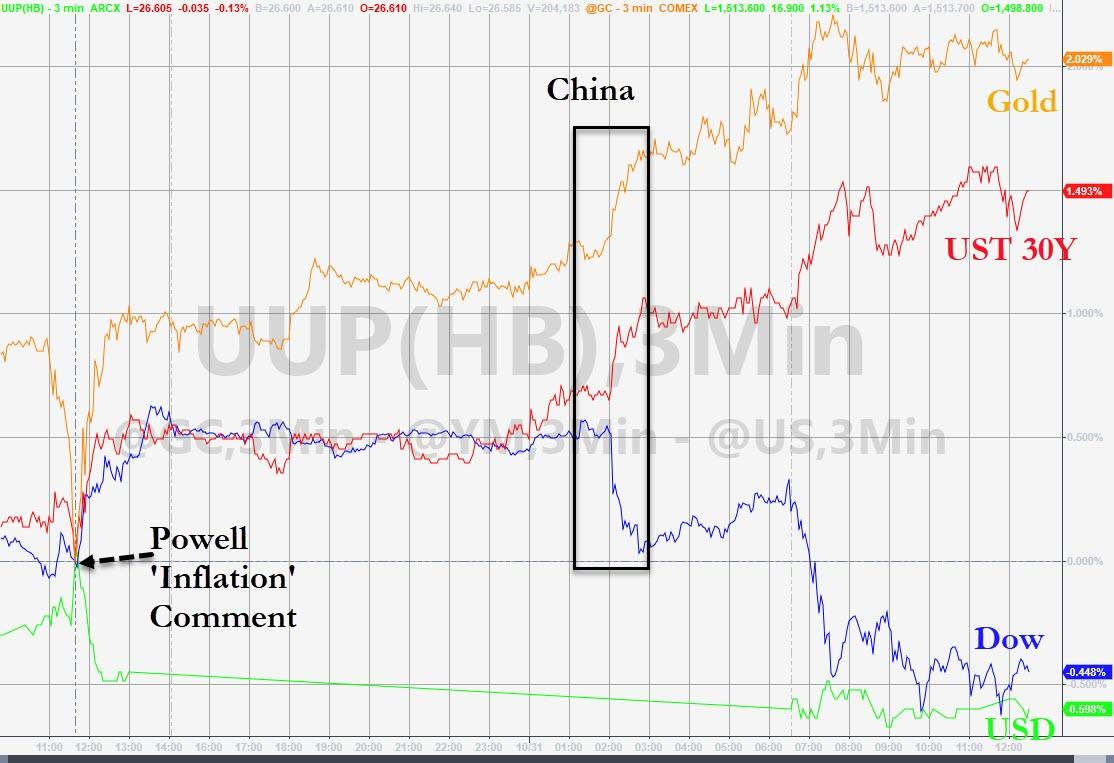

Stocks Slump, Gold Jumps On Powell-Pause, Trade-Turmoil, & Dismal-Data

October ended with the most disappointing macro-economic data since April 2017…

Source: Bloomberg

But stocks were holding up well until China blew it…

China chundered in the trade-deal punchbowl overnight, claiming that a deal was unlikely and despite Kudlow and Trump’s best efforts, the odds of a trade deal tumbled (but remain up on the month)…

Source: Bloomberg

And that crushed the gains in stocks that Powell had created…

Source: Bloomberg

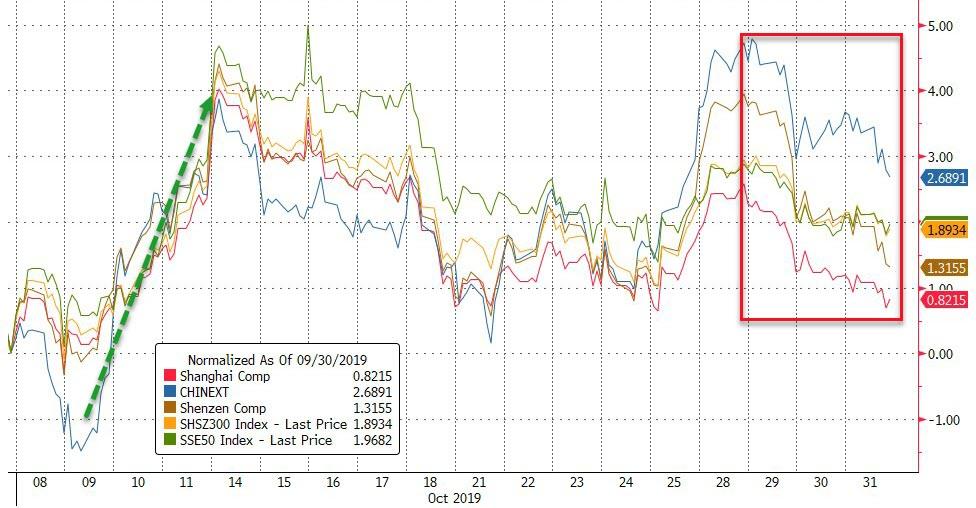

Chinese stocks managed to hold on to gains from post-Golden-Week buying but faded the last few days as reality of the non-deal trade-deal hit investors…

Source: Bloomberg

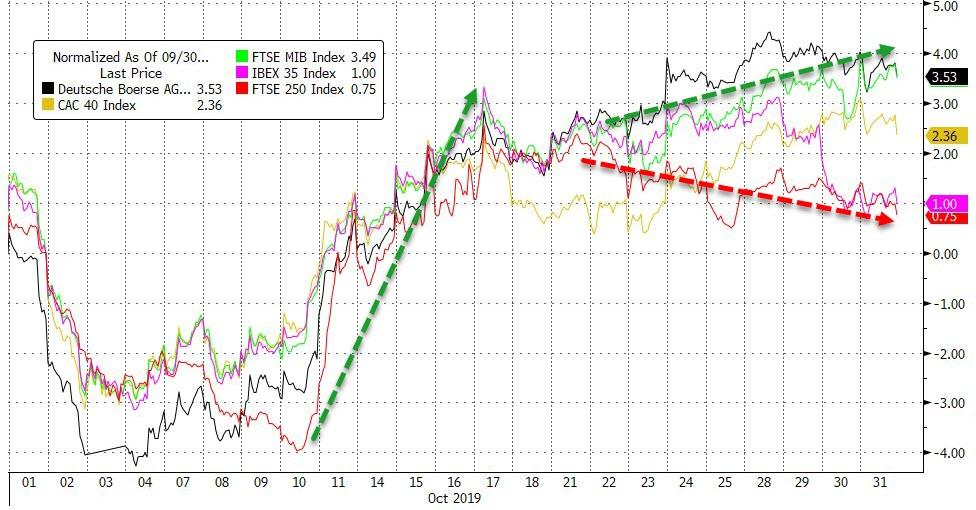

European Stocks ended October higher with UK’s FTSE lagging and Germany’s DAX leading…

Source: Bloomberg

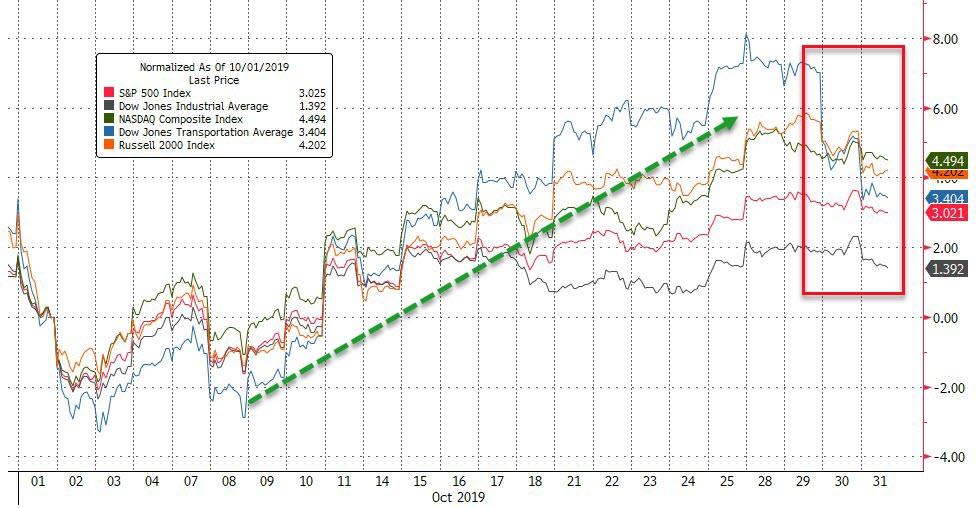

All major US Stock indices were higher in October, led by Nasdaq (Dow was a laggard) but the last few days has seen selling…

Source: Bloomberg

NOTE that US, Europe, and China all saw stocks rise once China returned from Golden Week

A daft end to the day…

US equity gains came on the back of an almost non-stop short-squeeze…

Source: Bloomberg

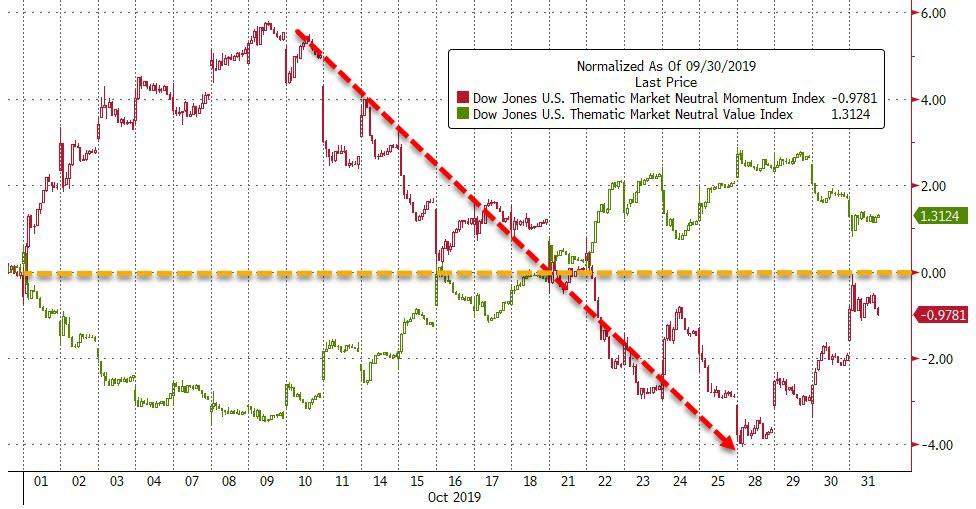

Momo ended October just in the red, after a big slide intramonth…

Source: Bloomberg

Defensives and Cyclicals were practically unchanged on the month, thanks to a surge in cyclical risk-taking mid-month…

Source: Bloomberg

Financials outperformed on the month but started to fall back in line with the yield curve in the last few days…

Source: Bloomberg

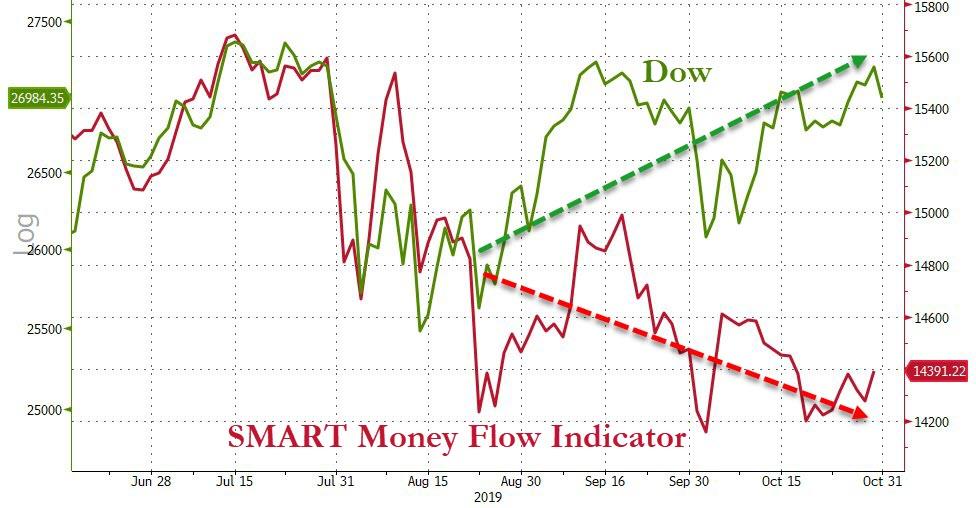

Smart Money has started to decouple from stocks…

Source: Bloomberg

Equity and credit protection costs collapsed in October…

Source: Bloomberg

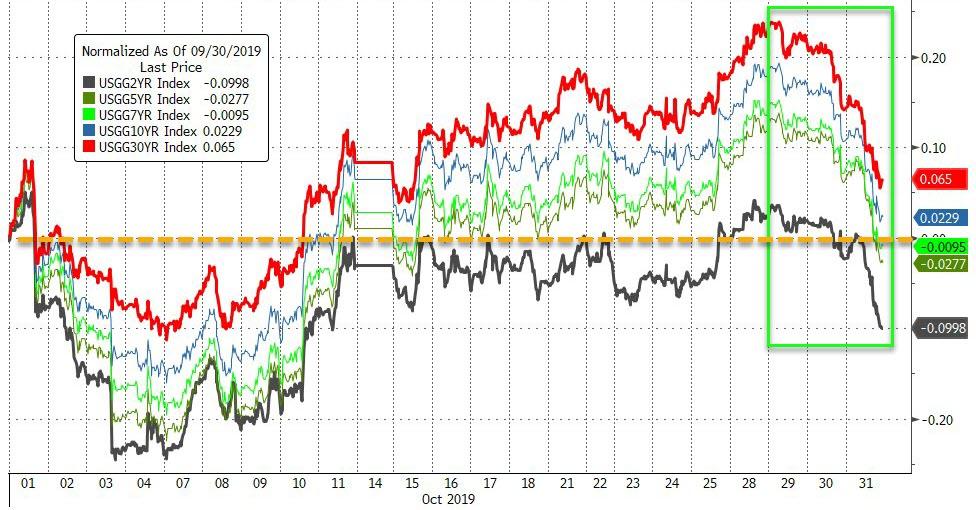

Treasury yields were mixed on the month with the short-end lower and 10Y/30Y higher by the end (despite a collapse in yields the last few days)…

Source: Bloomberg

This divergence meant that the yield curve (2s10s) soared in October – its biggest steepening since Dec 2016 (right after Trump elected)…

Source: Bloomberg

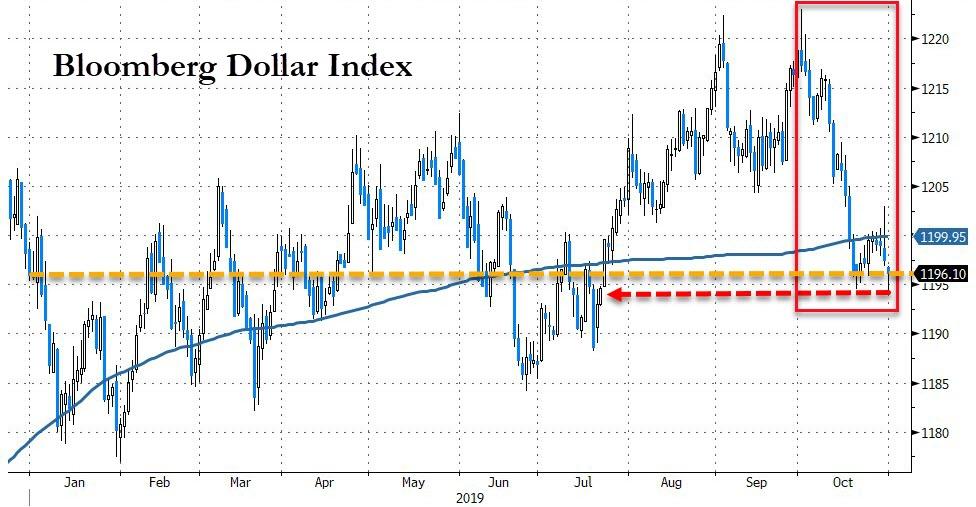

The Dollar Index dived in October (after 3 straight months higher), the worst month since Jan 2018, and back in the red for 2019 (back below 200DMA)…

Source: Bloomberg

While the rest of the world appears to be weakening vs the dollar, the dollar itself is losing notable ground against ‘money’…

Source: Bloomberg

Cable soared over 5% in October, the biggest gain since May 2009 (back above 200DMA)…

Source: Bloomberg

Offshore Yuan surged in October, its best gain since January 2019…

Source: Bloomberg

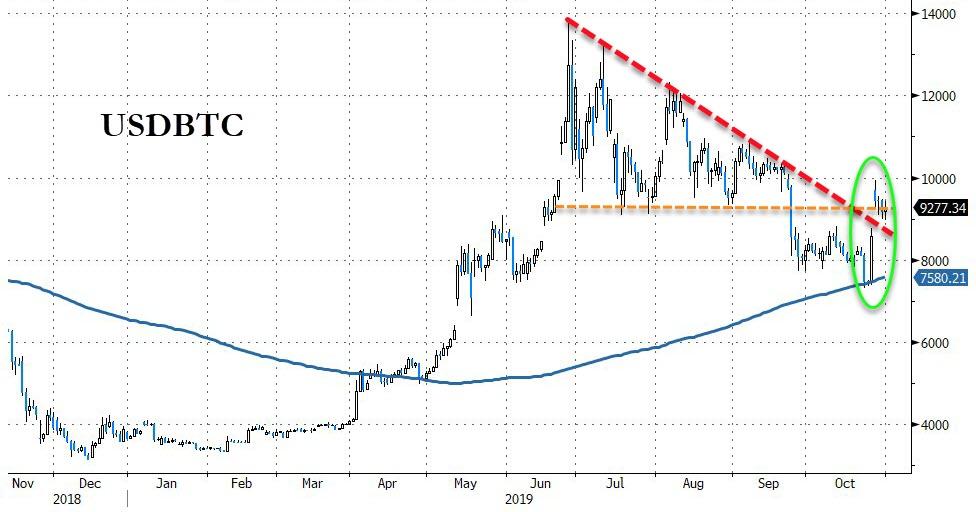

Despite an ugly puke late in the month, Cryptos ended October higher (after 3 down months), led by Bitcoin Cash…

Source: Bloomberg

Bitcoin bounced perfectly off its 200DMA during the month, roaring back above a key trendline…

Source: Bloomberg

Silver soared in October and while the dollar dived, crude ended lower…

Source: Bloomberg

This is silver’s 4th month higher in the last 5, ending back above $18…

Gold managed to end October higher (up 5 of the last 6 months) and back above $1500…

Silver’s outperformance of gold erased September’s relative gains…

Source: Bloomberg

WTI ended back below $55 after three big legs down this week…

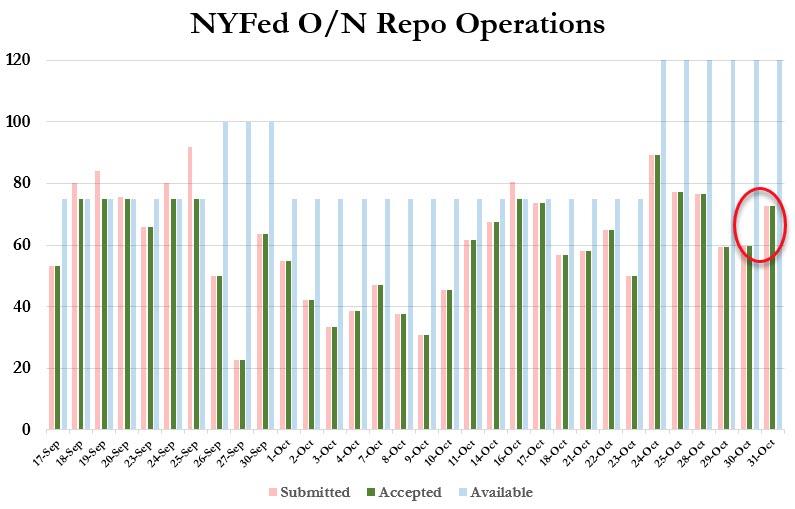

Finally, we note that the Fed’s liquidity spigot is wide open and shows no signs of being “fixed”…

Source: Bloomberg

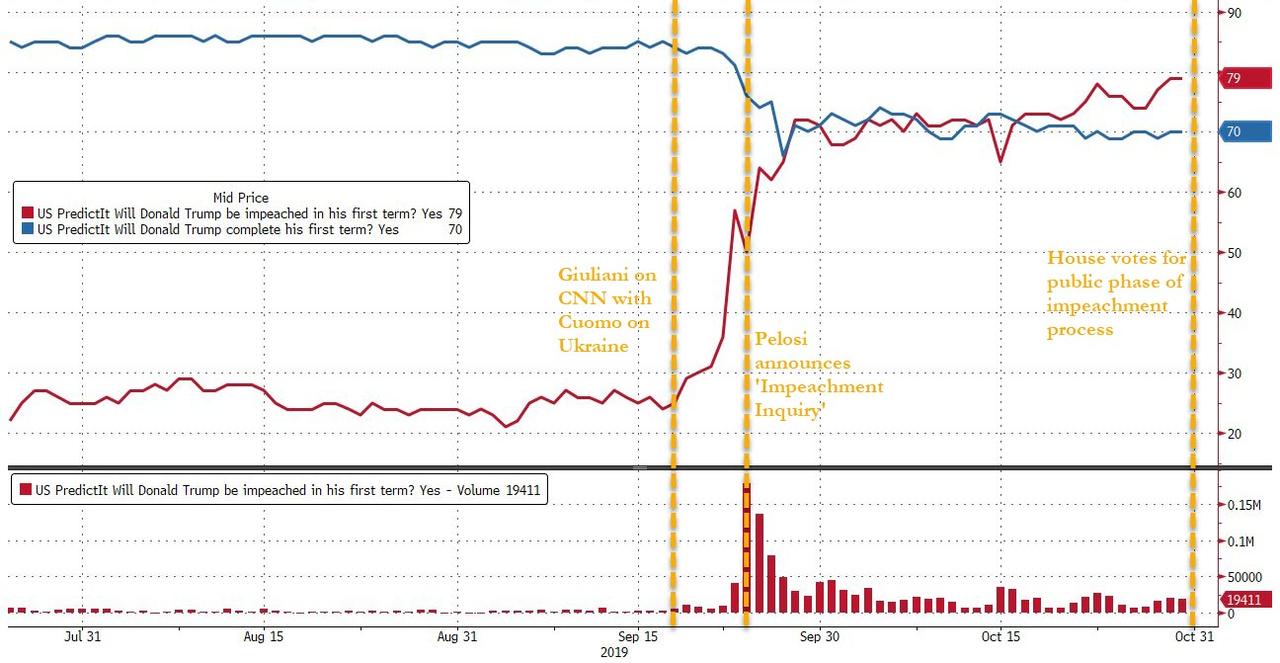

Additionally, after today’s vote to formalize the public phase of the House’s impeachment inquiry, odds of Trump being impeached by the House have risen to 79% BUT the odds of him completing his first term (i.e. a bet that the Senate will reject the impeachment) is at 70%…

Source: Bloomberg

And for those claim that global economic data is bottoming… it’s not!! (October was the worst month since May 2018)…

Source: Bloomberg

And what happens next, now that The Fed has shown their cards…

A Texas school district board has unanimously approved a proposal to introduce transgender education for children as young as 8-years-old.

The Austin Independent School District rubber stamped the new curriculum, which will for the first time will see students taught about “gender identity and sexual orientation.”

“The lessons will also help kids identify an adult they can trust; plus talk to them about options if they get pregnant, and seventh graders would learn how to use a condom,” reports KXAN.

The curriculum is being described as “controversial” given that it will teach children as young as eight about gay anal sex and transgender identities.

Two groups held dueling rallies outside the school district headquarters, including Informed Parents of Austin, a group which seeks to prevent “bullying” and enforce “equality” within the school district.

The usual answer to this kind of story is ‘homeschool your kids,’ but similar things are being inserted into homeschooling curriculums too.

Over in the UK, efforts to introduce similar LGBT curriculums into schools have been met with fierce protests, almost exclusively from Muslim parents.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

Hezbollah Fires Anti-Aircraft Missile At Israeli Drone Over Lebanese Airspace

A major incident has unfolded along Lebanon’s southern border with Israel on Thursday involving an Israeli drone. Hours ago Lebanese media reported that Hezbollah operatives shot down an Israeli aircraft, identified as an unmanned aerial vehicle (UAV), likely with an anti aircraft missile, specifically a MANPAD (or man-portable air-defense system).

Pro-Hezbollah media channels widely circulated footage of the purported shoot down; however, the Israeli Defense Forces (IDF) were quick to issue a statement denying that Hezbollah scored a hit on the aircraft, saying it was not damaged, but while confirming it was flying in Lebanese airspace.

“A short while ago, anti-aircraft fire was detected from Lebanese territory at an IDF unmanned aerial vehicle. The aircraft was not damaged,” the Israeli military said in a statement.

Footage taken near the southern border village of Nabatieh showed what appeared to be missile fire followed by an explosion, but Hezbollah later released a statement which confirms that while the group fired on the Israeli aircraft, it was not hit.

The Hezbollah statement reads as follows: “This afternoon at 2:05 pm, the Islamic Resistance confronted with the appropriate weapons an enemy drone in the skies of south Lebanon and forced it to leave the Lebanese airspace.”

A short while ago, an anti-aircraft missile was launched over Lebanese territory towards an IDF UAV. The UAV was not hit.

There are unconfirmed reports that Israel may have attempted to fire on Hezbollah in return following the incident.

Israeli incursions into Lebanese airspace have reportedly been a rarer occurrence since the August 25th incident which saw two Israeli reconnaissance drones downed over Beirut, outside of Hezbollah offices. That dangerous incident resulted in a significant exchange of fire between Hezbollah and Israeli troops on the southern border, with Hezbollah claiming a direct hit in a revenge attack on an Israeli vehicle.

Currently, Lebanon is on edge after two weeks of protests which have brought daily life and public institutions, including banks and schools, to a standstill. Hezbollah and Iran have accused foreign powers of fueling unrest in order to further destabilize the region and weaken the ‘Shia resistance group’ – further making its role in Lebanon uncertain.

{kind=link}

{kind=link}

{kind=link}