Futures swung from all time highs to losses during the European session and then rebounded again as Asian stocks hit their lowest this year on a third straight session of selling in Chinese internet giants, while real bond yields hit another record low ahead of earnings from the most valuable companies on Wall Street and in the run-up to the two-day Federal Reserve meeting. S&P 500 E-minis were down 5 points, or 0.11%, at 07:15 am ET. Dow E-minis were down 77 points, or 0.22%, while Nasdaq 100 E-minis were up 3 points, or 0.02%.

More than one third of the S&P 500 is set to report quarterly results this week, led by Apple, Microsoft, Amazon and Alphabet, the four largest U.S. companies by market value. Apple, Alphabet and Microsoft, which were largely flat in premarket trade, are set to report earnings after the market closes, while Amazon will report results on Thursday. U.S.-listed Chinese stocks extended their declines as fears over more regulations in the mainland persisted. Alibaba and Baidu lost about 3.6% and 4.9%, respectively (more below). Here are some of the biggest U.S. movers today:

- Chinese large cap stocks listed in the U.S. fall in premarket trading amid a deepening rout trigged by Beijing’s regulatory crackdown. Didi Global (DIDI) drops 4.4% and JD.com (JD) falls 6.4%, while Baidu (BIDU) declines 4.9%.

- Cryptocurrency-exposed stocks slumped in premarket trading after Bitcoin gave up some of the gains seen on Monday. Bit Digital (BTBT) sinks 18% and Riot Blockchain (RIOT) drops 5%, while Marathon Digital (MARA) falls 6.2%.

- ObsEva (OBSV) soars 34% after entering a pact for Organon to exclusively develop and commercialize ebopiprant, a treatment for preterm labor.

- Tesla’s (TSLA) second-quarter earnings beat and increased delivery outlook was well received by analysts, with the stock gaining 2.5% in premarket trading.

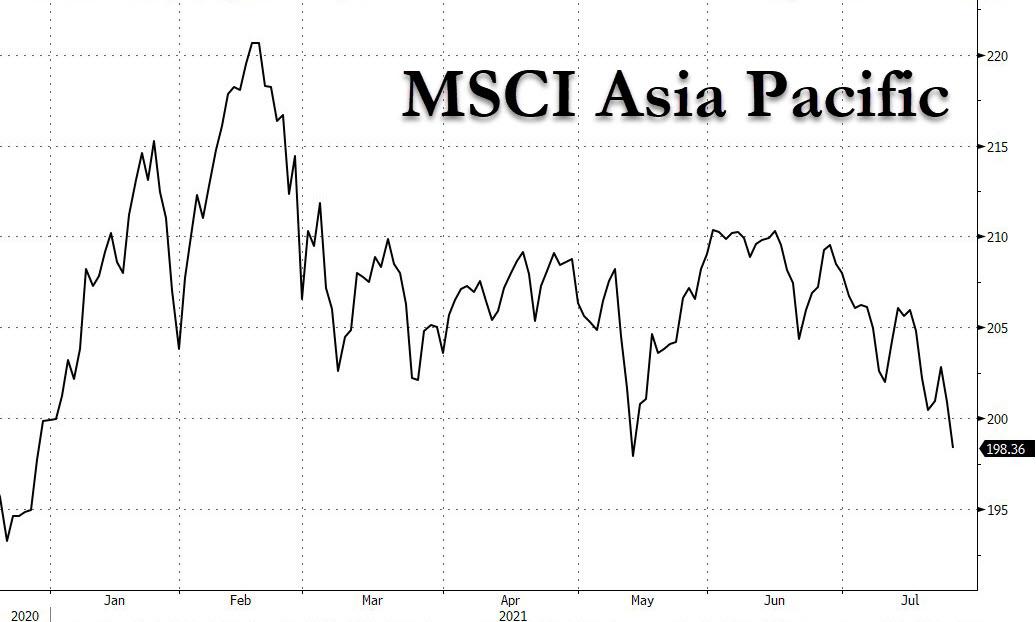

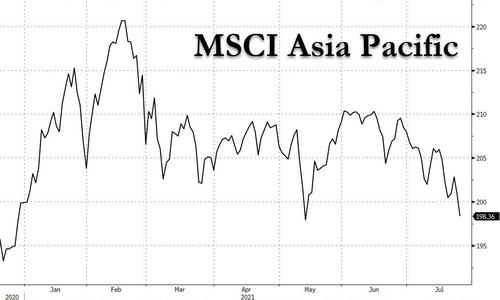

All eyes were on Asia, however, where equities dropped for a third day sliding to 2021 lows, as a selloff in Chinese tech shares deepened amid continued worries over Beijing’s regulatory crackdown. The MSCI Asia-Pacific index outside Japan fell 2.2% to its lowest level since end-December, having slid 2.45% the previous day.

The broader MSCI Asia Pacific Index fell as much as 1.4% after sliding 1.3% on Monday. The Hong Kong Hang Seng Index slid 4.2%, its third day of declines, as speculation swirled that U.S. funds are offloading China and Hong Kong assets. The Hang Seng Tech index slumped as much as 9.6% to its lowest since its inception in July 2020. It has fallen around 17% in three days and has lost 44% from a February peak.

Delivery giant Meituan plunged the most on record, while Tencent, Alibaba and JD.com also plunging. Fears over the government’s intensifying crackdown has shaken sentiment toward Chinese stocks, forcing investors like Cathie Wood of Ark Investment Management to dump shares of companies like Tencent Holdings and KE Holdings. Chinese bluechips dropped 3.53%, also hitting 2021 lows, thanks to regulatory crackdowns in the education and property sectors.

“The market seems to be uncertain whether there will be more policy changes for fintech, social media platforms, delivery platforms and ride hailing platforms,” said Iris Pang, chief economist for Greater China at ING. “Each has their own issue and faces different regulatory actions, so the market is looking for ‘which technology subsector will be next?’”

While it isn’t completely clear if the current selloff has follow-through, there are some indications it might, said Ilya Spivak, head of greater Asia at DailyFX. “Establishing a foothold below the 4,800 figure on the benchmark CSI 300 index would suggest that recent weakness is more than just a corrective pullback and speak to scope for downward follow-through.”

Not all was doom and gloom: Japanese equities climbed for a third day as investors looked for catalysts in earnings reports at home and abroad. Electronics makers and banks were the biggest boosts to the Topix, which rose 0.6%. Advantest and Recruit were the largest contributors to a 0.5% advance in the Nikkei 225. The market was also looking toward this week’s Federal Reserve meeting and reports from major Japanese companies including Fanuc and Canon. “As investors anticipate a recovery in the economic cycle and corporate earnings, stocks sensitive to business cycles such as autos are likely to be bought up,” said Ryuta Otsuka, a strategist at Toyo Securities Co. South Korean stocks also gained, along with equities in the Philippines and Vietnam.

Asian weakness weighed on European stocks, which fell 0.92%, moving further away from recent record highs. Britain’s FTSE 100 was down 1.23%. Here are some of the biggest European movers today:

- LVMH shares gain as much as 1.8% after the company’s 1H results beat analyst expectations, with luxury valuations hovering at near-record levels. The sector remains in focus with peers Kering and Moncler due to report later on Tuesday.

- Dassault Systemes shares rise as much as 4.8% to a record high after results, with Citi saying the software firm saw another “solid” execution performance against high expectations.

- Croda shares rise as much as 6.1%; Berenberg says results are “excellent,” analyst Sebastian Bray (buy) remains positive on shares.

- MorphoSys shares fall as much as 11.6% after Commerzbank downgrades to hold from buy and slashes PT to EU59 from EU105, with the broker saying it is losing confidence in the investment case turning positive.

- Reckitt shares sink as much as 10%, the most since the global financial crisis, after the U.K. consumer- goods company’s results disappointed analysts. Reckitt is the biggest decliner in the FTSE 100 Index and the second-worst performer in the Stoxx 600 Index on Tuesday.

- Randstad falls as much as 8.1%, the most since April 2020, after the temporary- employment services firm reported results. Jefferies (underperform) notes U.S. weakness and suspects operational gearing has peaked.

Looking ahead, 3 of the 5 FAAMGs, Alphabet, Apple and Microsoft, are set to publish quarterly results late on Tuesday, with Amazon.com Inc’s due later in the week. In addition, the Fed will begins its two-day meeting on Tuesday, with investors set to scrutinise a statement and press conference from Chair Jerome Powell due late Wednesday. They will be looking to see how the central bank will balance fast-rising prices with the complication of increased coronavirus infections.

“While we expect the Federal Reserve to prove more hawkish than expected…the negative impact on the equity market should be quite subdued as easy monetary policy is still there for quite a while,” said Sebastien Galy, senior macro strategist at Nordea Asset Management.

In rates, real bond yields in the United States and Europe have fallen to record lows and on Tuesday, the yield on 10-year Treasury inflation-protected securities (TIPS) hit -1.147%, down 4 basis points on the day. German inflation-linked bond yields also extended their recent falls, hitting a new low at around -1.747%. ING Bank strategist Antoine Bouvet said the fall in real yields could be explained by thin market liquidity and hefty central bank bond buying. “Of course there are macro worries, and the phase of growth acceleration of this cycle looks to be over, but this does not justify rates where they are,” he said.

In nominals, the yield on benchmark 10-year U.S. Treasury notes slipped three basis points to 1.26%, outperforming bunds and gilts by 2bp each as flight-to-quality favors Treasuries vs core Europe; 10-year German Bund yields dropped 2.6 basis points, close to a 5-1/2 month low set on Monday. Gains during Asia session were on light futures volumes, however. U.S. session highlights include 5-year note auction and, on the economic data slate, durable goods orders and consumer confidence.

In fx, the Japanese yen and U.S. dollar rose amid a broad risk-off tone as concerns about a crackdown in China rippled through global markets The dollar rose 0.18% against a basket of currencies and the euro slipped 0.2% versus the dollar. The dollar also fell 0.2% against the yen. The yen rose against all its Group-of-10 peers as a rout in Chinese shares fueled by Beijing’s regulatory crackdown extended into global bond and currency markets. Ned Rumpeltin, head of foreign-exchange strategy at Toronto-Dominion Bank, said the dollar may have further to rise. “We’ve seen a general pattern of risk reduction over the last several weeks, with USD shorts dialed back,” he said. “The optics of that would suggest that broader trends favor some further near-term USD strength”.

In commodities, crude oil dropped 0.45% to $71.60 a barrel amid concern surging COVID-19 cases worldwide could impact demand. Gold was steady at $1,798.86 per ounce. Bitcoin was trading around $37,100 from a Monday peak of $40,581 after Amazon.com offered a qualified denial of a weekend news report that said it was preparing to accept cryptocurrencies.

Looking at the day ahead, there’ll be a number of earnings reports of interest, including Apple, Microsoft, Alphabet, Visa, UPS, Starbucks and General Electric. Otherwise, data releases from the US include the Conference Board’s consumer confidence indicator for July, preliminary durable goods orders for June, the FHFA’s house price index for May, and the Richmond Fed’s manufacturing index for June. In Europe, there’s also the Euro Area M3 money supply for June. Finally, the ECB’s Hernandez de Cos will be speaking, and the IMF will be releasing their World Economic Outlook Update.

Market Snapshot

- S&P 500 futures down 0.4% to 4,395.75

- STOXX Europe 600 down 0.6% to 458.20

- MXAP down 1.1% to 196.16

- MXAPJ down 2.0% to 642.46

- Nikkei up 0.5% to 27,970.22

- Topix up 0.6% to 1,938.04

- Hang Seng Index down 4.2% to 25,086.43

- Shanghai Composite down 2.5% to 3,381.18

- Sensex down 0.6% to 52,552.29

- Australia S&P/ASX 200 up 0.5% to 7,431.36

- Kospi up 0.2% to 3,232.53

- German 10Y yield fell 1.8 bps to -0.436%

- Euro down 0.2% to $1.1775

- Brent Futures up 0.4% to $74.77/bbl

- Gold spot down 0.1% to $1,795.97

- U.S. Dollar Index up 0.16% to 92.80

Top Overnight News

- Unverified rumors swirled that U.S. funds are offloading China and Hong Kong assets. The speculation, which included talk that the U.S. may restrict investments in China and Hong Kong, circulated among traders late afternoon in Asia, spurring a renewed bout of selling

- Around the globe, people and governments are finding out that Covid won’t be thrashed into extinction, but is more likely to enter a long, endemic tail

- European Central Bank policy makers have acknowledged that their new push to boost inflation expectations could take quite a while to kick in, according to officials familiar with the discussions

A more detailed look of global markets courtesy of newsquawk

Asian equity markets traded mostly positive as the region found inspiration from Wall St. where all major indices extended on record highs, led by outperformance in cyclicals and with earnings in focus including the looming results from the mega cap tech giants Apple, Alphabet and Microsoft that are due to report after-market on Tuesday. ASX 200 (+0.5%) was underpinned by strength in the commodity-related sectors following further production updates and with BHP lifted after it reached a deal related to port infrastructure for handling of potash which spurred hopes the Co. may proceed with the multi-billion-dollar Jansen mining project. There was also some encouragement from reports that South Australia and Victoria states will exit their lockdowns, although the most-populous state of New South Wales continued to suffer from increasing infections. Nikkei 225 (+0.5%) remained positive and re-tested the 28k level to the upside as earnings results began to trickle in but with gains limited amid concerns of PM Suga’s approval rating which slipped to a nine-year low beneath the 35% level that is seen as a “point of no return” and which has historically resulted in most LDP PMs stepping down within a year. KOSPI (+0.3%) was buoyed by the latest GDP data which despite missing expectations at 5.9% vs exp. 6.0%, it was still the fastest pace of growth in a decade and above the 4.2% government projection for this year, while it was also reported that South Korea and North Korea reopened their hotline and that their leaders exchanged several letters since April. Hang Seng (-4.2%) and Shanghai Comp. (-2.4%) were varied with the mainland temperamental following the prior day’s regulatory-triggered sell-off and with the continued downturn in Hong Kong led by underperformance in healthcare and heavy losses in tech, while Evergrande shares saw double-digit declines after it scrapped its special dividend proposal – pressure for the indexes became more pronounced going into the European session. Finally, 10yr JGBs were marginally lower after the recent pullback in T-notes and amid mild gains in Japanese stocks, while softer demand at the 40yr JGB auction later also added to the headwinds for prices.

Top Asian News

- Hong Kong Court Issues Guilty Verdicts in First Security Trial

- Two Koreas Agree to Rebuild Ties in Possible Opening for Biden

- Yuan May Fall Further Amid Concerns of Regulatory Risk: OCBC

- Virus Cases in Tokyo Leap to New Record of 2,848 Amid Olympics

Stocks in Europe trade lower across the board (Stoxx 600 -0.4%) as early losses in futures markets were exacerbated ahead of the cash open amid another decline in Chinese stocks. The downside in China was partly a continuation of the moves seen yesterday which, were triggered by the ongoing regulatory crackdown by the government. News flow overnight was also downbeat for the region after a US SEC official stated that US-listed Chinese companies must disclose risks of interference by the Chinese government as part of their regular reporting responsibilities. Furthermore, Evergrande shares saw double-digit declines after it scrapped its special dividend proposal. In terms of the damage, the Shanghai Composite closed lower by 2.5%, the Hang Seng was softer by 4.2% (lowest since 4th November 2020) with its Tech Index declining nearly 8% to a record low close. This added to the selling pressure at the open in Europe with US futures also succumbing to the deterioration in sentiment. As a reminder, US indices were able to close at record highs yesterday with some desks suggesting the China-inspired declines were overblow with focus switching to a slew of large-cap earnings reports. Tesla (+2.2%) are higher in the pre-market post-results with attention now turning to earnings from GE, UPS, 3M and Raytheon ahead of the Wall St open, whilst Alphabet, Apple, Microsoft, AMD, Visa and Starbucks report after-hours. Back to Europe, sectors are all softer with defensive names fairing marginally better than peers whilst Autos, Basic Resources and Retail names lag. Earnings in Europe have continued to pick up pace with French luxury heavyweight LVMH (+0.5%) bucking the downbeat trend amid strong sales metrics for Q2. Elsewhere, Reckitt (-8.9%) sit the near the foot of the Stoxx 600 as sales numbers and margins disappointed investors at its Q2 results release. Finally, Just Eat Takeaway.com (+2.3%) sit near the top of the Stoxx 600 with Cat Rock Capital (4.2% stake) calling on the Co. to take urgent action to increases its share price in order to avoid a possible hostile takeover.

Top European News

- ECB Is Said to Have Discussed Fed’s Inflation Policy Shift

- Nordic Capital Is Said In Talks to Buy Health Tech Firm Inovalon

- Falling Covid Cases Are Welcome Surprise for U.K. Scientists

- City of London Staff Return in Highest Numbers for 16 Months

In FX, the Dollar Index and Japanese Yen have been firming throughout the European morning as the deterioration in sentiment prompt flows into the traditional safe-havens. However, the DXY remains somewhat contained within a relatively tight range sub-93.000 with a plethora of risk events ahead, including the FOMC, US GDP, PCE alongside a slew of large-cap earnings. From a fiscal standpoint, US Senate Democratic Leader Schumer said he is committed to passing the bipartisan infrastructure bill and the Senate may stay in session through the weekend to finish the bill. Despite the positive noises out of The Hill, participants remain sceptical regarding a swift and seamless passage as some Dems are adamant that a reconciliation bill should also be at hand. From a technical perspective, DXY’s 50 DMA (91.435) and 200 DMA (91.352) diverge further after forming a “golden cross”, and near-term resistance levels include yesterday’s 92.959 high ahead of the round figure. USD/JPY meanwhile probes 110.00 having had waned from its 110.39 overnight peak, with the 21st July trough at 109.85 and 100 DMA seen around 109.54. Japan’s COVID situation remains in focus as the Tokyo Olympics are underway, with positive cases more than doubling D/D to 3,000. Japanese ministers are meeting at the PM’s official residence to discuss the COVID situation.

- CNH – The Yuan has been the marked EM laggard, with investors skittish over China’s crackdown on onshore and offshore domestic firms (with speculation that the US may restrict investments in China and Hong Kong), whilst three districts in north-eastern Beijing issued red alerts for a rainstorm on Tuesday – following the fatal flooding in the Henan province last week. The Yuan saw sideways trade overnight following a steady PBoC fix and shrugged off a slower-paced rise in Industrial profits, but the Chinese currency yielded as losses across Chinese assets accelerated heading into the European open – with the Hang Seng posting intraday losses in excess of 5% at one point. USD/CNH popped higher to a three-month high of 6.5224 (vs low 6.4772), with gains exacerbated by an upside breach of the 200 DMA (6.4988) and the psychological 6.5000.

- CAD, AUD, NZD, SEK, NOK – The non-US Dollars underperform and the Scandis are pressured amid the soured risk mood and losses across commodities. The petro-G10s CAD and NOK are pressured by the losses across the crude complex, albeit off worst levels as oil prices stage a mild rebound at the time of writing. USD/CAD stopped short of the 1.2600 handle before pulling back – with similar action seen across NOK pairs after EUR/NOK tested 10.4900 to the upside. The SEK sees losses to a lesser magnitude, whilst a rise in Sweden’s June trade balance surplus provided no reprieve. Turning to the antipodeans AUD and NZD lag with the latter the G10 underperformer as AUD/NZD climbs back above 1.0550 (vs 1.0538 low), whilst the former seems less pronounced losses as Australia’s Victoria state Premier announced the decision to ease lockdown restrictions in the state from midnight tonight and reports noted that South Australia will also exit lockdown. AUD/USD declined from a 0.7389 overnight peak to a 0.7340 base. NZD/USD has dipped under 0.6950 from a 0.7006 peak.

In commodities, WTI and Brent front month futures have experienced choppy trade within a tight range, with losses seen heading into the European open as stocks in China continue to bleed, keeping upside capped for the oil contracts via broader sentiment. That being said, the overarching force remains the supply/demand balance – with the supply side unlikely to see many updates until at least early-to-mid August, whilst demand tracks COVID and vaccine developments. Of course, the FOMC and tier-1 US data later in the week will likely sway prices at that point. On the travel front, the UK is reportedly to consider easing travel restrictions from the EU and the US, which would provide a rosier outlook for fuel demand. WTI prints on either side of USD 72/bbl whilst its Brent counterpart forfeited the USD 75/bbl handle and resides around mid-74/bbl. Elsewhere, spot gold and silver are relatively flat but see a mild divergence, with the yellow metal just south of USD 1,800/oz having had printed a current high a Dollar above the psychological mark awaiting this week’s upcoming risk events. LME copper is softer on the day amid general risk aversion, but prices came to under USD 100/t away from the USD 10k/t level. The sentiment is also dented by overnight reports that China is reportedly mulling steel export levies to curb domestic prices. Finally, reports suggested that BHP reached a deal related to port infrastructure for the handling of potash which spurred hopes the Co. may proceed with the multi-billion-dollar Jansen mining project.

US Event Calendar

- 8:30am: June Durable Goods Orders, est. 2.1%, prior 2.3%; -Less Transportation, est. 0.8%, prior 0.3%

- June Cap Goods Orders Nondef Ex Air, est. 0.8%, prior 0.1%;

- June Cap Goods Ship Nondef Ex Air, est. 0.8%, prior 1.1%

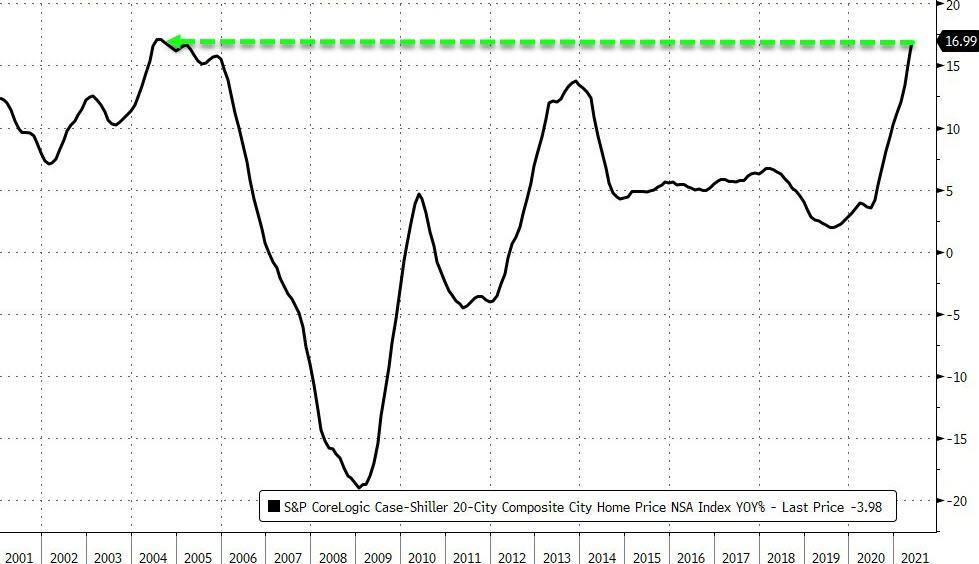

- 9am: May S&P/Case-Shiller US HPI YoY, prior 14.59%

- S&P CS Composite-20 YoY, est. 16.30%, prior 14.88%

- 10am: July Conf. Board Consumer Confidence, est. 123.8, prior 127.3; Expectations, prior 107.0; Present Situation, prior 157.7

- 10am: July Richmond Fed Index, est. 20, prior 22

DB’s Jim Reid concludes the overnight wrap

Markets were in something of a holding pattern much of yesterday as they awaited tomorrow’s Federal Reserve decision and a raft of corporate earnings releases this week. By the end of the session though the S&P 500 and the Dow Jones had both managed to grind out a +0.24% gain to reach new all-time highs. We earlier had a risk off start to the week with the highlight being real yields on 10yr US Treasuries hitting an intraday all-time low (since TIPS used from 1997) of -1.131%. We still closed -3.4bps at -1.106% which demonstrates how well bid Treasuries are irrespective of the inflation story. It’s likely a combination of extraordinary treasury technicals and concerns over global growth.

However, overall US Treasury yields reversed course as the session developed and rose marginally on the day to be up +1.3bps to 1.290% (1.2196% at the early London lows), as the decline in the real yields (-3.5bps) was overridden by rising inflation breakevens (+4.9bps), which finished at their highest level in just over 7 weeks. So higher inflation expectations are back in vogue just as real yields are collapsing.

That decline in real yields came amidst a number of underwhelming data prints in yesterday’s session that led to further angst about the strength of the economy’s growth momentum into the second half. To start with, the Ifo’s business climate indicator from Germany unexpectedly fell in July, seeing a decline to 100.8 (vs. 102.5 expected), with the expectations measure falling to 101.2 (vs. 103.6 expected). Separately in the US, we then found out that new home sales in June had also fallen unexpectedly, coming in at an annualised rate of 676k (vs. 796k expected), which is the lowest number since April 2020, whilst the previous month’s number was also revised down -45k. On top of that, the Dallas Fed’s manufacturing index also unexpectedly fell for a 3rd consecutive month to 27.3 (vs. 31.6 expected).

On the flipside of the Delta worries, the UK reported further good news yesterday with the number of new cases at 24,950. This means that the total number of cases over the last 7 days is now down -21.5% relative to the week before, and marks the fastest weekly reduction since April 12. If the UK can make it through the summer with barely any legal restrictions on daily life, then it will start showing a path towards living with covid without crippling the domestic health system. Hence we think it’s a great case study. Only 9 days ago many experts were expecting a pattern that would see new cases hit 100,000 per day fairly soon. That they’ve suddenly fallen is remarkable even if there is some element of voluntary mobility restrictions and a heatwave to counterbalance the good news. As a minimum cases can now go up from a much lower base and perhaps a weaker trajectory than looked possible little more than a week ago.

Back to markets and US equities managed to hit new highs as mentioned, with the S&P 500 (+0.24%) advancing in anticipation of various earnings releases. After the close last night, Tesla reported earnings well above consensus (2Q EPS of $1.45 vs $0.75 expected) causing the stock to gain nearly 1% in post-market trading after already rising +2.2% during the day. The company cited robust demand both domestically and abroad, but also added to the drumbeat of supply chain issues. The automaker cited “port congestion” and the “global semiconductor shortage” as key risks that they expect to continue. Tesla also indicated they plan to keep production “running as close to full capacity as possible” for the immediate future. The earnings focus will continue today with Apple, Microsoft, Alphabet, Visa, UPS, Starbucks and General Electric all reporting. So a big day.

In terms of sectors, Energy companies (+2.50%) led the way yesterday as the reopening trade did fairly well even in light of cratering real rates. Airlines (+3.17%), materials (+0.88%), and banks (+0.91%) were among the best performing industries, while biotech (-0.52%) and health care equipment (-0.73%) lagged.

Asian markets are trading mostly up this morning with the Nikkei (+0.51%), Shanghai Comp (+0.14%) and Kospi (+0.67%) all higher while the Hang Seng (-1.03%) is down. Futures on the S&P are marginally weaker at -0.13% while those on the Stoxx 50 (+0.04%) are broadly unchanged. Yields on 10y USTs are slightly lower.

The bipartisan infrastructure talks took one step back yesterday, as CNN’s chief congressional correspondent, Manu Raju, tweeted that the Republicans had rejected the Democrats “global offer” on the infrastructure deal, and that talks were in a “precarious state”. Late Sunday night Democrats sent their Republican colleagues an offer to bridge the remaining divide in the bill. They sought to resolve some funding provisions for “physical” infrastructure, the creation of an infrastructure bank, and how much unspent Covid money can be re-appropriated to infrastructure. However Republican lawmakers felt the offer was reopening closed issues between the two sides. While the vote didn’t happen yesterday, some lawmakers still expect it will get a vote this week. Senators are set to begin a 5-week recess on August 9, but Majority Leader Schumer has already said he would keep members of his chamber past that date in order to pass this legislation.

Here in Europe, markets had a relatively weaker performance, with the STOXX 600 (-0.08%) posting a small loss in spite of a strong performance from energy (+2.10%) and banks (+1.72%). Sovereign bonds also underperformed their US counterparts, with yields on 10yr bunds (+0.2bps), OATs (+1.1bps) and BTPs (+1.1bps) all moving higher in yield. However gilts (-1.3bps) had a relatively better performance thanks to dovish remarks from the BoE’s Vlieghe. In a speech, he said that he hadn’t changed his view that the current bout of inflation would prove temporary, and pointed out that the economy “remains an average recession away from full employment” and also faced the end of various government support schemes soon. As a result, he said he thought it would “remain appropriate to keep the current monetary stimulus in place for several quarters at least, and probably longer.”

Another outperformer yesterday was Bitcoin (+9.48%) which traded above $40,000 for the first time since back in mid-June. The move followed a job advert from Amazon, which said that they were looking for an executive to develop their “digital currency and blockchain strategy”, raising hopes among investors that cryptocurrencies could be accepted as a means of payment more widely. Crypto-assets in general had a strong performance on the back of the news, with Ethereum (+4.97%), XRP (+5.19%) and Litecoin (+6.59%) all posting solid advances by the close. Bitcoin is down -2.47% this morning as Amazon have said that this move does not indicate that they are close to accepting Bitcoin as a means of payment.

Elsewhere, coffee prices (+9.95%) followed up their advances over the last two weeks as further frost was headed for Brazil, which is something that has the potential to affect production for many years into the future as trees need to be replaced. Commodities more broadly saw further gains yesterday, with the Bloomberg Commodity Spot index seeing a further +1.00% gain to close in on its highest level in the last decade. Oil was little changed – WTI down -0.22% and Brent crude up +0.54% – after a volatile day of trading as delta variant concerns weighed on the growth outlook of emerging markets in particular, where vaccinations rates lag. We’ve broadly reversed these losses in the Asian session.

Debate about vaccination passports and requirements are becoming an increasing live debate across countries. In the US, California yesterday announced that all state employees would have to prove they are vaccinated or wear a mask in offices and be subjected to weekly testing. In addition, all health care facility workers, public or private, will have to provide proof of vaccinations or wear masks and be subjected a test twice a week. New York City extended its vaccine mandate to all city government employee, which follows a mandate last week that sought to get all health care workers in public hospitals and clinics vaccinated. Furthermore, yesterday the US Justice Department said that the vaccine’s emergency status does not disqualify state and local mandates.

To the day ahead now, and there’ll be a number of earnings reports of interest, including Apple, Microsoft, Alphabet, Visa, UPS, Starbucks and General Electric. Otherwise, data releases from the US include the Conference Board’s consumer confidence indicator for July, preliminary durable goods orders for June, the FHFA’s house price index for May, and the Richmond Fed’s manufacturing index for June. In Europe, there’s also the Euro Area M3 money supply for June. Finally, the ECB’s Hernandez de Cos will be speaking, and the IMF will be releasing their World Economic Outlook Update.