Biden Embraces ‘Green New Deal’ In Newly Released “Biden-Sanders” Policy Platform Tyler Durden

Wed, 07/08/2020 – 15:48

While Joe Biden was hanging out in the basement, his team was hard at work liaising with the remnants of the Bernie Sanders campaign people to craft a policy agenda that, they hope, will motivate the young people who came out in droves for Bernie to come out and vote for Biden.

And unsurprisingly, Biden’s plan is a hodge-podge of mostly incompatible ideas obviously intended to pander to the white working class swing voters in the Midwest, and the young AOC-worshipping DSA members and crypto-marxists who powered Sanders to his second straight second-place finish in a Democratic presidential primary.

According to information released by the campaign, the outline of Biden’s plan covers four areas: A push to ‘buy American’ and incentivizing American jobs, as well as embracing ‘clean energy’ (mostly via extreme policy proposals outlined in the Green New Deal), while also working to boost the “caring” economy – whatever that means. The Biden campaign said it would commit to bolstering child care and elder care, as well as racial equity.

Here’s one quote from the policy paper released by the campaign:

Ensure the U.S. achieves a 100% clean energy economy and reaches net-zero emissions no later than 2050. On day one, Biden will sign a series of new executive orders with unprecedented reach that go well beyond the Obama-Biden Administration platform and put us on the right track. And, he will demand that Congress enacts legislation in the first year of his presidency that: 1) establishes an enforcement mechanism that includes milestone targets no later than the end of his first term in 2025, 2) makes a historic investment in clean energy and climate research and innovation, 3) incentivizes the rapid deployment of clean energy innovations across the economy, especially in communities most impacted by climate change.

He followed this up with a video promising to take “drastic action” to confront climate change.

Biden will follow this all up with a speech on Thursday’ detailing his agenda in the run up to the Aug. 17 Democratic convention.

“Biden wants to get to the same place that many to his left want to get to but he firmly believes that it will take an incremental path to get there and that you can’t leapfrog the political reality that he has come to know in many decades in politics,” said Jared Bernstein, who is advising the campaign after serving as Biden’s chief economic adviser in the vice president’s office.

Some in the media described the proposals as an attempt to address areas discussed by the right and the left.

* * *

But we see it as what it truly is: A clumsy attempt to pander to swing voters. For those who want to learn more, they can check out the full policy sheet below:

1. Ensure the U.S. achieves a 100% clean energy economy and reaches net-zero emissions no later than 2050. On day one, Biden will sign a series of new executive orders with unprecedented reach that go well beyond the Obama-Biden Administration platform and put us on the right track. And, he will demand that Congress enacts legislation in the first year of his presidency that: 1) establishes an enforcement mechanism that includes milestone targets no later than the end of his first term in 2025, 2) makes a historic investment in clean energy and climate research and innovation, 3) incentivizes the rapid deployment of clean energy innovations across the economy, especially in communities most impacted by climate change.

2. Build a stronger, more resilient nation. On day one, Biden will make smart infrastructure investments to rebuild the nation and to ensure that our buildings, water, transportation, and energy infrastructure can withstand the impacts of climate change. Every dollar spent toward rebuilding our roads, bridges, buildings, the electric grid, and our water infrastructure will be used to prevent, reduce, and withstand a changing climate. As President, Biden will use the convening power of government to boost climate resilience efforts by developing regional climate resilience plans, in partnership with local universities and national labs, for local access to the most relevant science, data, information, tools, and training.

3. Rally the rest of the world to meet the threat of climate change. Climate change is a global challenge that requires decisive action from every country around the world. Joe Biden knows how to stand with America’s allies, stand up to adversaries, and level with any world leader about what must be done. He will not only recommit the United States to the Paris Agreement on climate change – he will go much further than that. He will lead an effort to get every major country to ramp up the ambition of their domestic climate targets. He will make sure those commitments are transparent and enforceable, and stop countries from cheating by using America’s economic leverage and power of example. He will fully integrate climate change into our foreign policy and national security strategies, as well as our approach to trade.

4. Stand up to the abuse of power by polluters who disproportionately harm communities of color and low-income communities. Vulnerable communities are disproportionately impacted by the climate emergency and pollution. The Biden Administration will take action against fossil fuel companies and other polluters who put profit over people and knowingly harm our environment and poison our communities’ air, land, and water, or conceal information regarding potential environmental and health risks. The Biden plan will ensure that communities across the country from Flint, Michigan to Harlan, Kentucky to the New Hampshire Seacoast have access to clean, safe drinking water. And he’ll make sure the development of solutions is an inclusive, community-driven process.

5. Fulfill our obligation to workers and communities who powered our industrial revolution and subsequent decades of economic growth. This is support they’ve earned for fueling our country’s industrial revolution and decades of economic growth. We’re not going to leave any workers or communities behind.

* * *

Oh, and Biden for America has committed to not accepting contributions from oil, gas and coal industry, and their executives.

via ZeroHedge News https://ift.tt/2W0ukhR Tyler Durden

Plunge In Consumer Credit Continues As Americans Repay Record Amounts Of Credit Card Debt Tyler Durden

Wed, 07/08/2020 – 15:28

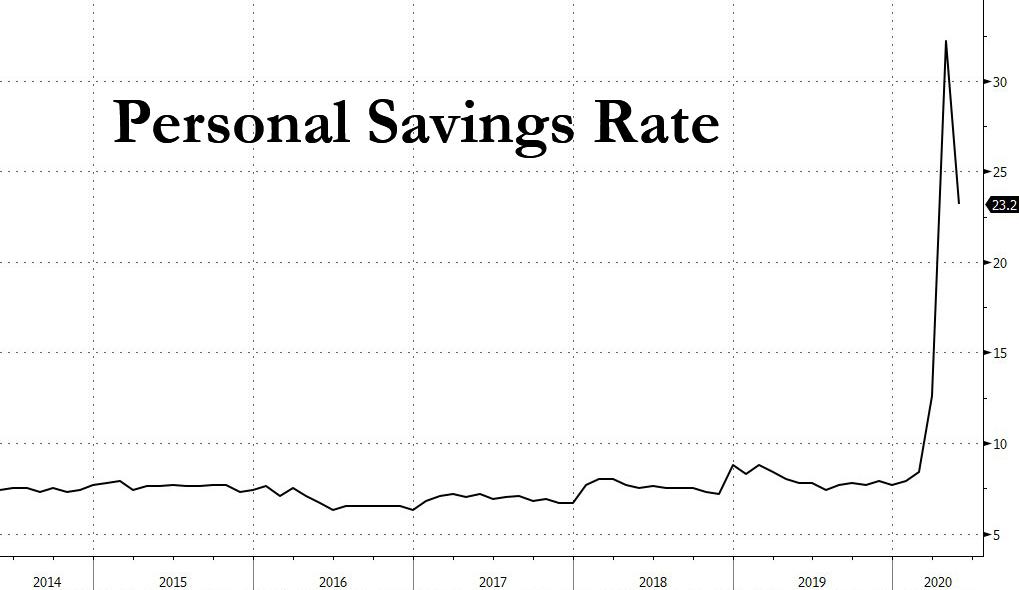

One of the striking changes to US consumer behavior spawned by the economic shutdowns from the coronavirus pandemic, was the unprecedented surge in personal savings which exploded to a record 32% of disposable personal income before easing modestly last month to 23.2%.

Now, thanks to the latest consumer credit data released by the Fed, we know what much of that saving went to: paying down debt.

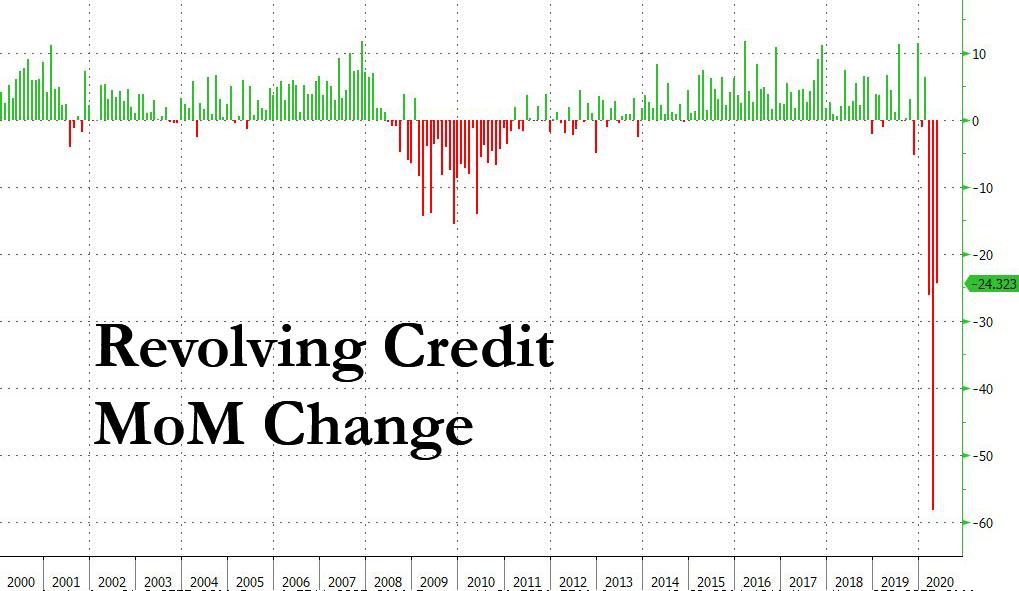

According to the Fed’s latest G.19 statement, in May, total consumer credit tumbled by another $18.28 billion, which while less than the record $68.8 billioncrash in April, was far below expectations for $15 billion drop.

Just like March and especially April, most of the credit repayment took place in revolving credit which shrank by another $24.3 billion in May (after declines of $21.5BN in March and $58.2BN in April) as US consumption literally went into reverse and instead of spending wildly as it does every other month, usually spending what it can’t afford, US consumers repaid the most on their credit cards ever.

In fact, over the past three months, US consumer have paid down a staggering $104 billion in credit card debt, bring the total outstanding credit card debt below below $1 trillion. Indicatively, the first time total credit card debt hit $1 trillion was back in December 2007, which means that the deleveraging of the past 3 months has sent US credit card balances to a 13 year low!

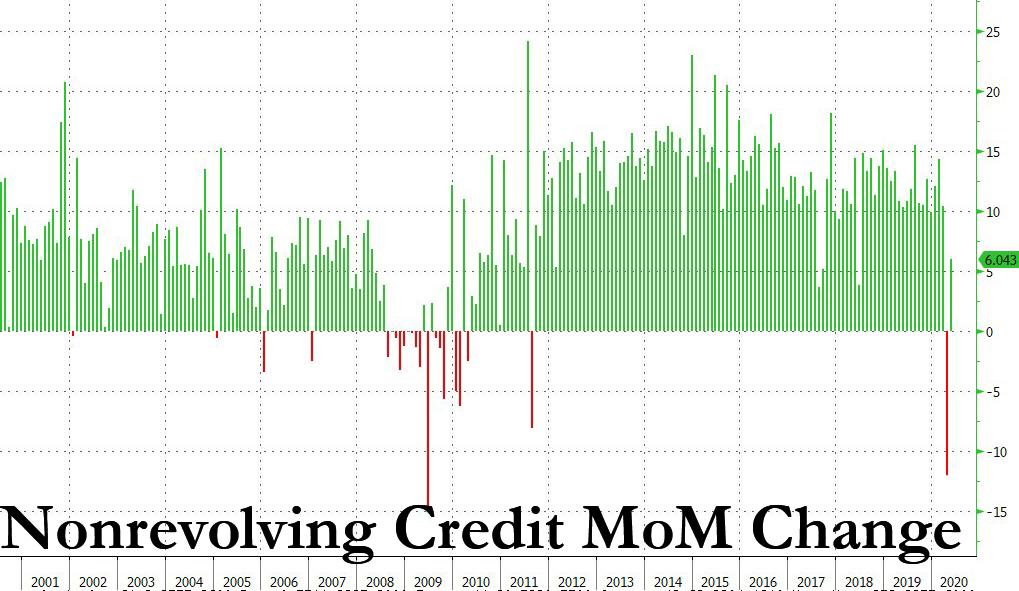

At the same time, there was a modest return to normalcy in non-revolving debt, i.e., student and auto loans, which after plunging by a near record $12 billion last month, has again rebounded and was up $6 billion in May.

Going back to the aggressive repayment of credit card debt, that is quite an ominous development for a US economy which is 70% reliant on stable – in many cases credit-card funded – consumer spending. Ominous, but not unexpected, because in a time of virtually no visibility on job prospects and how the pandemic is resolved, instead of doing what they do best, i.e. spend, Americans not only saved money but also went into credit paydown mode, crippling an economy where 70% of total output is a direct result of consumer spending; and needless to say, the tens of millions of Americans (depending on whether one believes the initial claims or the BLS jobs report) who have lost their jobs are not going to go out and spend like drunken sailors any time soon.

So how long until this shocking plunge in consumer spending reverses? The answer is that nobody knows, but until US consumers feel comfortable enough to once again “charge it”, there can be no recovery.

What we find most surprising, however, is that in this day and age when the Fed has effectively institutionalized moral hazard and where failure is no longer punished as capitalism is now officially dead and zombie existence is rewarded, Americans still care enough about their credit rating to pay down their own debt even as corporations and the country go on a historic debt issuance spree which everyone knows will never be repaid.

Our advice to Americans with credit cards: go crazy, after all if everyone defaults – and gets a default – it’s the same as nobody defaulting.

via ZeroHedge News https://ift.tt/31XTcuz Tyler Durden

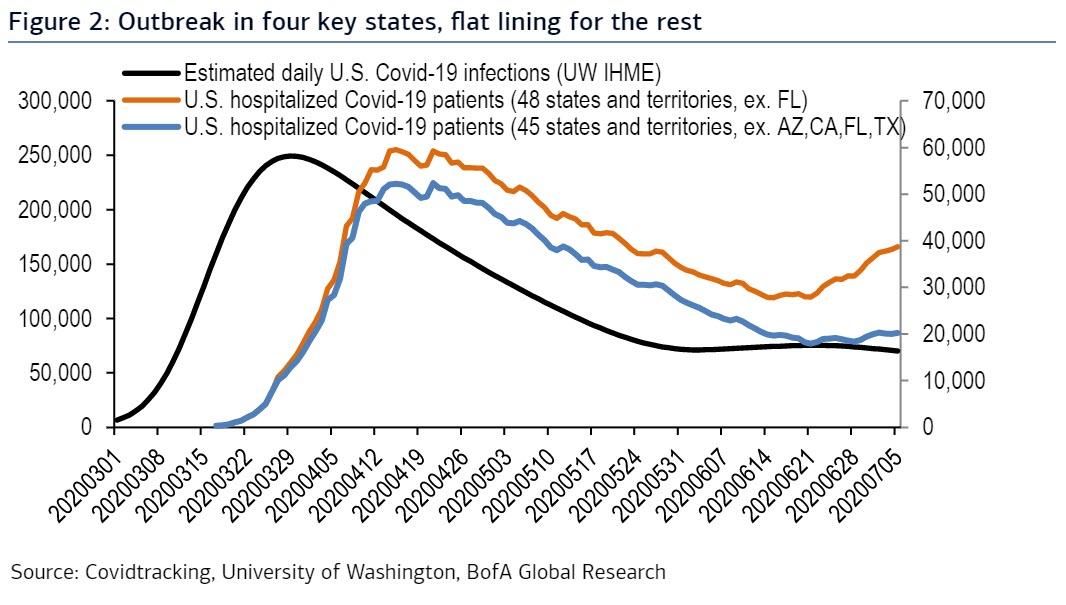

BofA Calculates That Today Marks The Day Of Peak US Coronavirus Hospitalizations Tyler Durden

Wed, 07/08/2020 – 15:16

Several months ago, the coronavirus pandemic mutated from a purely epidemiological phenomenon and became a full-blown political issue, with clear ideological divisions forming along the lines of whether or not to pursue strict shutdowns (and in some cases, whether to engage in another round of economic closures) all the way down to whether masks should be worn. The drivers here were self-evident: opponents of Trump and the current administration demanded even more caution, in some cases arguably in pursuit self-serving hopes of further economic pain (and more stimulus payments) that would make a Trump re-election difficult; in light of this it is understandable why the president hoped to put the pandemic in the rearview mirror and to accelerate the reopening of the economy which has cost tens of millions in jobs and trillions in new debt.

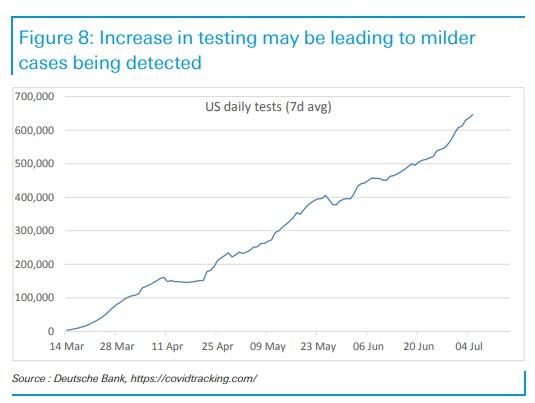

In recent weeks, a similar divide has also emerged on Wall Street, where bears such as Goldman have been emphasizing the recent surge in new cases across sunbelt states, warning that these would result in another spike in deaths, as well as reduction in mobility and overall cosumption and thus a fresh hit to the economy, as a new round of shutdowns – either mandatory or voluntary – were enacted. Bulls, meanwhile, would note that higher cases are merely a function of widespread testing…

… and point to the continued decline in covid-linked deaths which despite the jump in new cases, have failed to inflect higher, and underscoring that the mortality rate appears to be much lower for younger covid patients.

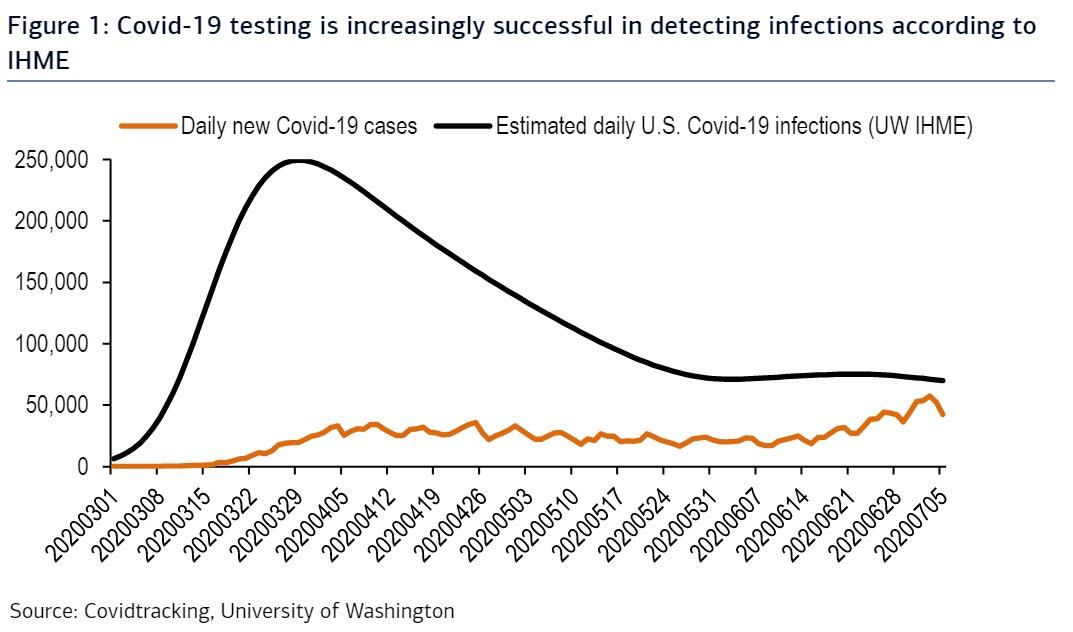

In a note that appears to be firmly in the bullish camp, overnight BofA’s Hans Mikkelsen writes that sharply elevated new daily Covid-19 case numbers highlight first and foremost more successful testing strategies (more tests, contact tracing, etc.,), according to the University of Washington IHME model.

BofA also notes that are active virus outbreaks in four major states – AZ, CA, FL and TX. However, instead of merely looking at new cases, Mikkelsen says that “to gauge the spread of Covid-19 we prefer to look at number of hospitalized people that, although a bit lagged (in March/April the peak in number of hospitalized came 17 days after the peak in newly infected, according to the IHME model), is less dependent on testing strategy.”

While clearly hospitalizations are up sharply in the U.S., BofA points out that if one excludes the four states “we find they are more accurately described as flat lining.”

Moreover, BofA calculates that in the new outbreak the daily number of infected people peaked on June 21st at 75,179, up from 71,112 on June 1st, and sharply above yesterday’s 69,987 estimate, again according to the IHME model.

The optimistic conclusion: “Should hospitalizations again be lagged 17 days that would imply (local) peak hospitalizations on July 8.” Or, in other words, today.

For the sake of the US economy, political and ideological considerations aside, one can only hope that BofA is right.

via ZeroHedge News https://ift.tt/2ZUbl9K Tyler Durden

Economist Irving Fisher famously said just before the 1929 stock market crash, “Stock prices have reached what looks like a permanently high plateau.” Whoops. Fisher wasn’t just any old economist. Joseph Schumpeter called him “the greatest economist the United States has ever produced.” Milton Friedman and James Tobin agreed.

After the sharp March COVID crash, stocks have come roaring back: nevermind the pandemic, protests in the streets, shuttered businesses, and double-digit unemployment rates. In Fisher’s day the Federal Reserve was but a pup; now Chairman Powell decided to print and ask questions later, expanding his central bank’s balance sheet by $3 trillion dollars in four months, a 75 percent increase.

Now a lesser light than Fisher is repeating the eminent economist’s famous gaffe. In a MarketWatch piece entitled “We’re in a new paradigm for stocks, this analyst argues. Get ready for permanently higher valuations,” Nicholas Colas, cofounder of DataTrek Research, claims it’s a whole new world because the ten-year Treasury bond is yielding a paltry 67 basis points, meaning that “A new model for assessing stocks may include higher valuations, as the old paradigm is no longer valid,” writes Andrea Riquier.

Led by Barstool Sports entrepreneur Dave Portnoy, daytrading is back in vogue to take advantage of the Powell put. “I’m trading my own money and lots of it,” Portnoy told Fox Business. “I’m having fun. As long as we’re still kind of with nothing else to do, I’ll keep day trading.”

“Portnoy has become the poster child of the day-trading craze,” writes Jonathan Garber for Fox Business, “livestreaming his daily trading sessions on Twitter, giving followers a glimpse into both his successes and failures as he slings positions worth hundreds of thousands of dollars.”

A few hours ago as I write, Portnoy tweeted, “A couple things to remember: Nobody has ever traded through a global pandemic. I have as much experience as the suits here. The market has no connection to reality. And stocks always go up.”

The Barstool businessman says in the video that he is “kicking the market’s ass.” In a craps reference, he says he’s been “rolling numbers for months without a seven in sight.” “Bernie Maddoff is smiling,” Portnoy rants. “Stocks only go up.”

Market pros are skeptical of Portnoy and his trading skills, to which he responds, “If these people were so smart and as good as they say, they wouldn’t be spending all day tweeting at me,” Portnoy said. “They’d be on a yacht somewhere.”

The Fed is not going to hit the brakes, but could the social mood be changing? The nightly news looks like 1968. Could markets follow? In ‘68 it was the Hong Kong flu that killed seventy thousand while the stock market peaked. The Vietnam War accelerated, the National Guard killed students at Kent State, the Weather Underground formed, and the Beatles broke up. The stock market then headed down to a 1970 bottom.

Peter Atwater spoke with Dee Smith on Real Vision about the end-of-cycle phenomena of overconfidence, fraud, and an eventual recovery.

Unlike Portnoy, Atwater, when asked how long this market can keep going up, said, “ I think it can go on not nearly as long as folks expect it to. The reason for that is exactly what you just talked about, which is this decoupling of the financial markets from the economic reality around us.”

Like the folks at Elliott Wave and The Socionomist, Atwater told Dee Smith,

I believe if we act as we feel, we feel as we act, there’s reflectivity to it. In many ways, we are driven by our mood and so I’m always looking for indicators in terms of behaviors: What are they saying about our sentiment, about our underlying mood? Because it’s such a critical element of human behavior. I think an example today is all of this constant daily news from the media and from advertisers that the world is uncertain today. To me, the world is no more nor no less uncertain than it’s ever been. What we’re finding is that there was a deteriorating sentiment in terms of our perceptions of certainty. When we think the future is uncertain, we don’t plan and so it has a real bearing on not only the economy but also the financial markets. I care an awful lot about how people feel.

In the wake of the Wirecard scandal in Germany and Tesla shares hitting an all-time high, Atwater addresses frauds in a bubble.

When confidence is extreme, there’s no scrutiny. There’s a sense—there’s always a this time it’s different mindset, the belief that anything is possible. It’s amazing to me how regularly we are captivated by these Harold Hill-like figures who are promising enormous fortune. One of my favorite stories is about this about [?], this fake country that existed in Central America that was—the proponents were able to raise an inordinate amount of money based on nothing but hubris. We get captured by these magical stories of illusion.

Why are investors or traders too lazy to uncover frauds and do their research? “Physiologically, the brain is the largest consumer of glucose in the body,” says Atwater. “To the extent that we can minimize that and not pay attention and be lazy, Kahneman and others who create wonderful pieces about this, we will gladly fall into the environment of overconfidence.”

Atwater sees mood changing over the summer. And he doesn’t believe the media manipulates the public mood. “People talk about the media manipulating mood. I think that, again, that our relationship with media is reflexive,” Atwater explains.

Atwater is more than a little cynical about the public’s investing skills.

Yeah, I don’t think markets ever reflect reality to begin with. I don’t think markets are rational or irrational. I think we make decisions that are rationalized. We’re constantly choosing based on our mood, and then reaching for whatever low hanging information we can find to support that. We are glad when we’re happy to buy things optimistically and to sell things when we’re pessimistic.

“At the top,” says Atwater, “there’s this saturating sense of certainty and control and optimism ahead.”

Mr. Portnoy must be sending us a signal.

via ZeroHedge News https://ift.tt/3gEj6Y7 Tyler Durden

Former Fox News Anchor Shep Smith Heads To CNBC Tyler Durden

Wed, 07/08/2020 – 14:57

In the middle of an otherwise relatively slow post-holiday weekend afternoon, CNBC has just announced that former Fox News anchor Shep Smith will be joining the network, where he will report on a wide range of topics beyond the cable news channel’s typically markets-focused coverage.

Smith abruptly left Fox News, where he built a large following, in October after his criticism of Donald Trump made him sort of an odd-man-out at the conservative-leaning cable news network.

Surprise! Shep Smith is heading back to TV, but not to CNN or MSNBC – he is joining CNBC to host a 7pm newscast starting this fall. @JBFlint has the full story herehttps://t.co/IhmHRjcl1z

Smith is signing on to host a new show, entitled “The News with Shepard Smith”, which will debut this fall in the 7-8pm time slot. The Monday through Friday newscast marks a significant shift in the evening programming strategy for CNBC, which is essentially re-runs of “Shark Tank” and “the Profit” after Jim Cramer wraps up the popular “Mad Money”.

CNBC Chairman Mark Hoffman said Smith’s show will try to “look for the signal in all the noise”.

“Information is coming at us from every direction,” Mr. Hoffman said in a statement. “If we’re not careful life-altering decisions will be made based on half-truth, rumor, misdirection or worse. We aim to deliver a nightly program that, in some small way, looks for the signal in all the noise.”

Shep will make his debut tomorrow at 10am on “Squawk on the Street”.

Of course, given his legacy at Fox News, media reporters will be curious to see whether Smith suffers from what some have informally dubbed “The Fox News Effect” – the tendency for the network’s stars to crash and burn after leaving the network, like Megyn Kelly, Glenn Beck and a handful of others.

via ZeroHedge News https://ift.tt/38BpLQc Tyler Durden

Now Even Major Defense Firms Are Pushing For COVID Stimulus Money Tyler Durden

Wed, 07/08/2020 – 14:37

Major defense firms which have for years especially since the post-9/11 so-called war on terror raked in billions in lucrative (and very often wasteful) government contracts are begging the federal government for more COVID-related stimulus.

Ultra-wealthy CEOs of the these major defense contractors are citing the potential for record job loss among their massive work force, though it’s likely few among the American public will sympathize with the idea of bailouts and taxpayer handouts to names like Lockheed Martin or Raytheon.

Brazen and unbelievable as it sounds, Bloomberg reports Wednesday that “CEOs of major defense companies, including Lockheed Martin, General Dynamics, Boeing and Raytheon, urge the Pentagon’s acquisitions chief and the White House’s acting budget director to press for stimulus money as the Senate is poised to consider another rescue package to ease damage caused by coronavirus pandemic.”

The Pentagon, AFP file image.

Without the stimulus, the defense firm execs say, the end result will be “significant job losses in pivotal states just as we are trying to recover from the pandemic,” Bloomberg continues.

The July 7 letter also detailed there would be a serious setback in development of cutting edge technologies, also given continuing layoffs, making it “of the highest urgency”. Additionally a letter was send to the Undersecretary of Defense for Acquisition and Sustainment Ellen Lord urging action, after Lord estimated pandemic disruptions could see up to a $10 billion setback.

A little over two weeks ago, the Pentagon acquisitions chief announced what she described as a devastating“three-month slowdown to all programs due to COVID-19.”

She said the hardest hit defense areas beset by delays include aviation, shipbuilding and small space launch sectors.

Other major names like the execs of Huntington Ingalls, Textron Inc., L3Harris Technologies and BAE Systems are also lobbying for stimulus.

“I won’t discuss any programs specifically, but we have seen inefficiencies across most programs. COVID-19 is shutting down defense manufacturing facilities and production lines, disrupting supply chains and distressing the financial stability of the companies DoD relies on to protect the nation,” Lord said during her June comments.

via ZeroHedge News https://ift.tt/2W0BpPw Tyler Durden

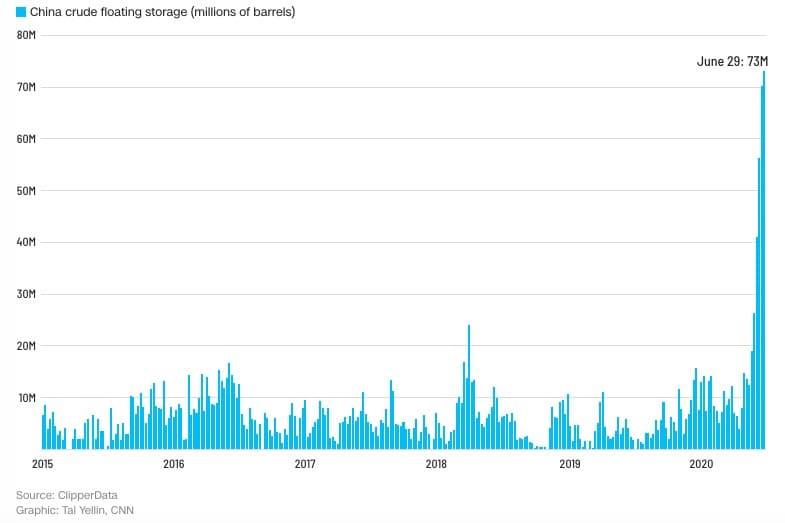

When the bottom fell out of international crude oil markets earlier this year, global oil storage was at a premium. In the United States, finding sufficient crude oil storage became such a challenge that the West Texas Intermediate crude benchmark plummeted below zero on April 20, ending the day at -$37.63 per barrel, meaning that you would essentially be paid $40 to take a barrel of oil off of someone’s hands. China, however, soon busied itself stocking up on cheap oil, to the extent that Beijing played a key role in the global oil market’s recovery by helping to buy off a significant portion of the world’s severe oil glut. This is not to say that China’s government was alone in taking advantage of historically low oil prices or buying up oil in an attempt to salvage their own struggling energy sector. Back in March, the United States government pledged to support domestic oil producers by buying 30 million barrels of oil for the nation’s Strategic Petroleum Reserve.

“But analysts said that China’s stockpiling dwarfs what other nations have done in response to cheap prices,” writes CNN. Matt Smith, director of commodity strategy at ClipperData, told CNN’s reporters that “China is the only country that has been buying like crazy. They went out and bought the dip.”

In fact, China went out and snapped up cheap crude at such a breakneck place that they now have their own critical oil storage issue. International news has been reporting for weeks on China’s jam-packed waterways filling up with crude tankers. On July 1 CNN reported that “China bought so much foreign oil at dirt-cheap prices this spring that a massive traffic jam of tankers has formed at sea waiting to offload crude” as the country’s purchases begin to arrive.

“China’s so-called floating storage — defined as barrels of oil on vessels waiting for seven days or longer — has nearly quadrupled since the end of May, according to ClipperData. Not only is that the most on record going back to early 2015, it’s up seven-fold from the monthly average during the first quarter of 2020.”

The vast majority of the oil arriving to China in recent weeks was purchased in April and May, when low prices spurred a shopping spree. “The hoarding of oil at sea is a reflection of China’s bargain-hunting during a time of extreme stress in the energy market,” writes CNN. According to the report, the oil tanker issue crowding China’s seas is not, however, because mainland storage is already at capacity, but simply because they can’t get it there fast enough. ClipperData’s Smith said that onshore storage could still take on a lot more crude, and that the current issue is “simply related to terminal congestion. They’ve got so much coming in that they can’t bring it onshore quickly enough.”

This week, however, at least one Chinese news outlet is telling a different story. While China’s onshore storage may not be full, they say, it’s getting dangerously close. Just this week, Beijing-based media group Caixin reported that “China is almost out of space to hold the oil that domestic traders bought at bargain-basement prices earlier this year when the Covid-19 pandemic crushed global crude demand.”

Caixin’s reporting is based on numbers provided by Oilchem China, which show that, as of Wednesday, Chinese crude oil storage was at 69 percent capacity “with the 33.4 million tons it had stockpiled, up by 24% from the previous year.” This is dangerously close to overflow. “That’s only 1 percentage point away from the 70% threshold that experts view as the country’s capacity limit,” reports Caixin.

And this stockpile will likely continue to grow, surpassing even May’s massive intake. “The situation, which has also been exacerbated by low turnover, is most prominent in East China’s Shandong province, one of the country’s oil refining hubs. Oil tankers have to wait 15 to 20 days there before they are able to offload their cargos,” says Caixin. The amount of oil held in storage may peak later this month as the country’s demand for fuel continues its slow march to recovery, but if not, this could spell big trouble for China’s storage sector.

via ZeroHedge News https://ift.tt/2ZWf7zI Tyler Durden

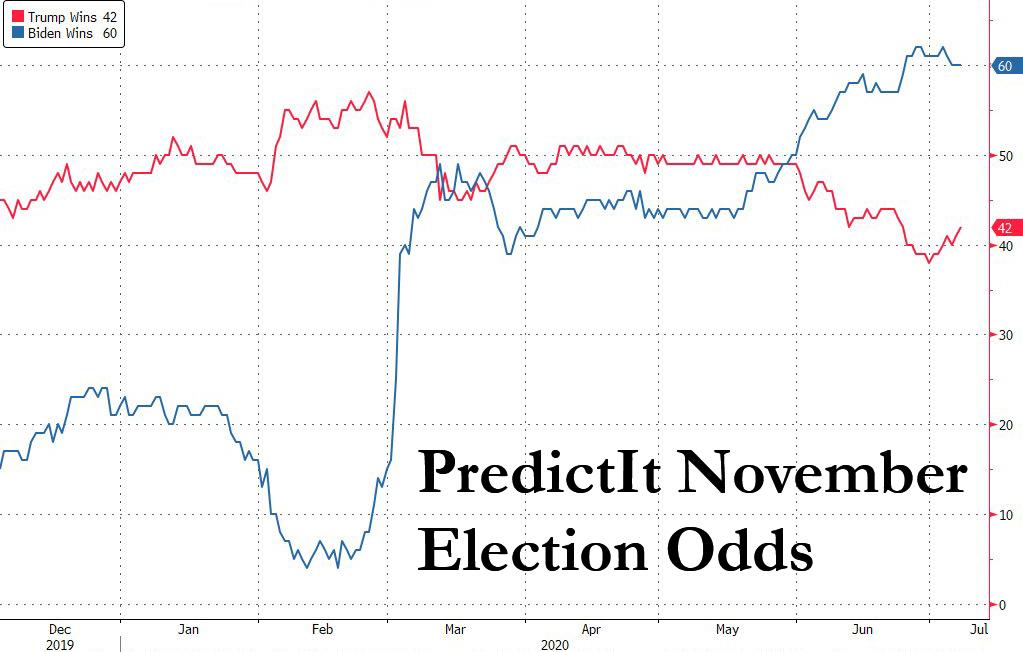

Here’s What Stock Markets See As The Outcome Of The Nov 3 Presidential Election Tyler Durden

Wed, 07/08/2020 – 13:54

If one believes online bookmakers such as PredictIt, the November 3 election will be an open and shut case, where Biden just has to show up and say absolutely nothing in order to win.

Of course, there are two problems with taking the above at face value: i) it is surprisingly easy to manipulate the highly illiquid PredictIt contracts, and an “entity” with deep pockets can push the odds dramatically in a preferred direction with just a $10-20K in bets; ii) public opinion is extremely fickle and while Biden has so far been completely missing from the public spotlight – an it will be difficult for the vice president to continue doing so until November 3.

That said, public polling also continues to show Biden with a substantial lead less than 4 months ahead of the elections.

Here too, however, everyone remembers the complete disaster that polling was ahead of the 2016 elections, where formerly reputable media outlets such as the NYT gave Hillary Clinton a 91% chance to win just weeks before the election.

Oops.

Shifting away from openly biased and propaganda attempts to sway voting outcomes, leaves us with just one option: askingwhat do markets think?

After all, the one place that will be very clearly affected by the election outcome is stock prices. Just one month ago we observed that Goldman’s clients were becoming rather nervous by the possibility of a Democratic sweep, one which according to Goldman’s chief equity strategist David Kostin would result in a substantial increase in corporate tax rates and a 20 point hit to the bank’s 2021 S&P EPS forecast.

So with the Nov 3 election drawing closer, Kostin has readdressed this issue, and in a report published overnight titled “Voting Machine: With four months to go, how US equities are trading the 2020 elections”, the Goldman strategist looks at the possible election outcomes as inferred by various markets, all of which suggest three different 2020 election perspectives:

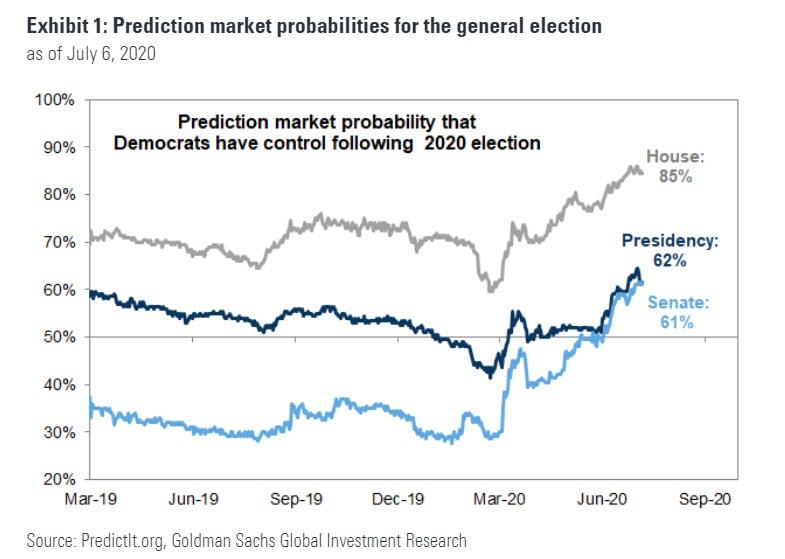

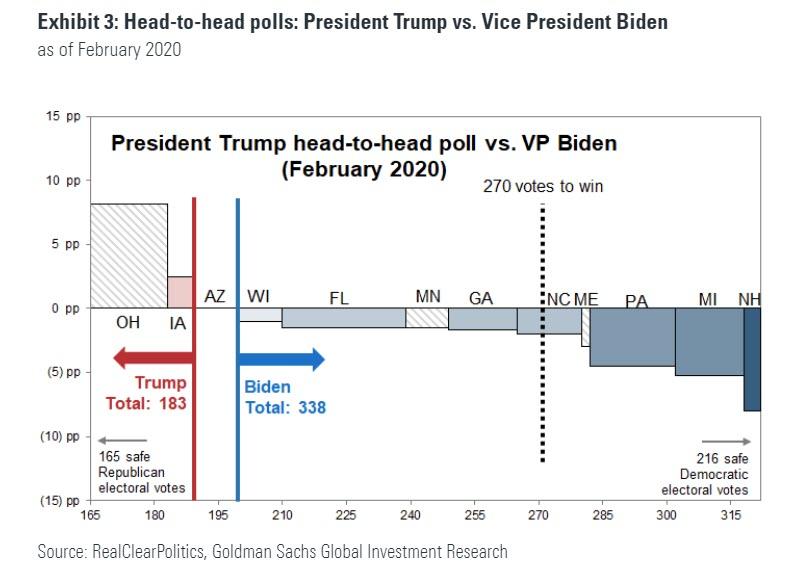

Prediction markets suggest a Democratic sweep. Market pricing currently implies the Democrats will control the White House, Senate, and House of Representatives. The current probabilities equal 62%, 61%, and 85%, respectively, compared with 43%, 30% and 61% in late February.

Options market pricing suggests that the winning presidential candidate and control of the Senate may not be known on Election Day and it may take additional time to count all the votes and finalize the results. Implied volatility for the period around the November 3rd election is extremely high compared with prior cycles, primarily because of the coronavirus, but the particularly high level of implied volatility in the periods before and after the election imply an extended period of election-related uncertainty. Although the 20-Nov option expiration offers two additional weeks of cushion beyond 3-Nov, the potential for delayed results, a precedent for extended vote-counting, and a slightly inverted term structure lead us to prefer extending hedges to the 18-Dec quarterly expiration.

Equity market trading patterns are inconsistent. The current S&P 500 index level and valuation suggest investors are comfortable with the outcome reflected in the polls and prediction markets. However, investors exhibit mixed views inside the market. The performance of stocks sensitive to a potential increase in corporate tax rates has not reflected changing probabilities of the election outcome. In contrast, Health Care stocks have underperformed as the prospect of Democratic control of Washington, DC has increased. One policy initiative that overlaps both parties is infrastructure spending, and stocks likely to benefit have outperformed.

Below we look in further detail at the various market-implied considerations ahead of the elections:

Polls and prediction markets

Prediction market-based pricing – such as that derived from PredictIt – implies the Democrats will control the White House, Senate, and House of Representatives. The current probabilities are 62%, 61%, and 85%, respectively, compared with 43%, 30%, and 61% on February 26th, just before Super Tuesday (March 3) and the spread of the coronavirus across the US.

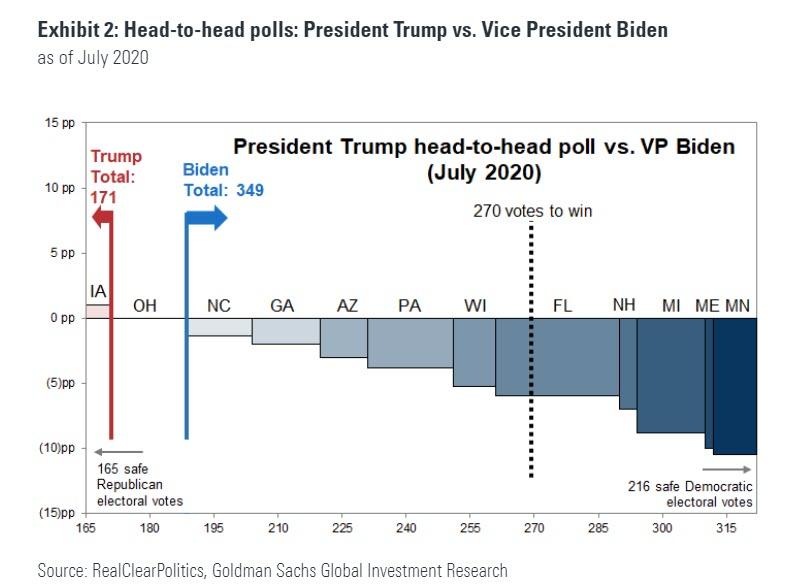

The Real Clear Politics poll average shows presumptive Democratic party nominee Joe Biden with an 8.8 point spread over the incumbent Republican Donald Trump (49.3% vs. 40.5%). FiveThirtyEight shows Biden ahead in a head-to-head election by 9.6 points (51.1% vs. 41.5%).

One additional source of equity market uncertainty in 4Q is that the coronavirus introduces a major complication in the timely tabulation of voting results. Voting and registration data reported by the Current Population Survey show that the proportion of voting done on Election Day has declined from 90% in 1996 to 60% in 2016.

In the 2016 general election, 140.1 million citizens voted, representing a national turnout rate of 63% of the citizen voting age population. Pre-election voting has increased in popularity during the past 20 years. Four years ago, 41% of the ballots were cast before Election Day, with 17% in the form of in-person early voting and 24% via by-mail absentee voting.

Health concerns and social distancing protocols suggest that more voters than ever will decide not to cast ballots at traditional polling stations on Election Day and instead vote by mail. In the case of a close election, it will take time to count – and invariably re-count – all the absentee and mail-in ballots. The deadline for each state to certify its result and finalize electors is December 8th (35 days after the election) or six days before the Electoral College convenes on December 14th (first Monday after the second Wednesday in December). For context, it took 34 days for the winner to be decided in the 2000 contest between George W. Bush and Al Gore.

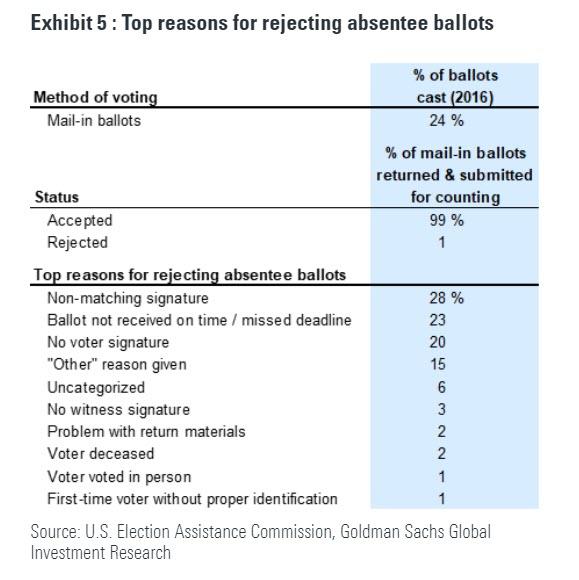

In its report to Congress on the 2016 election, the US Election Assistance Commission noted that nationally by-mail voting accounted for 24% of all votes cast in the election. The Commission estimates that 99% of ballots “returned and submitted for counting” were ultimately counted in the 2016 election. Exhibit 5 lists the top reasons for rejecting absentee ballots.

However, the resolution of equity market uncertainty is not related exclusively to the presidential election result but is also conditional on the outcome of the various Senate races. Although Presidents can implement executive orders, legislation requires Congressional approval, hence the importance of unified control under a single party of both the legislative and executive branches.

As Goldman reminds its clients, its 2020 US equity outlook report was titled “United we fall, Divided we rise” and refers to the policy uncertainty that may result when one party controls Washington, DC. In contrast, split control suggests gridlock, status quo, and lower uncertainty.

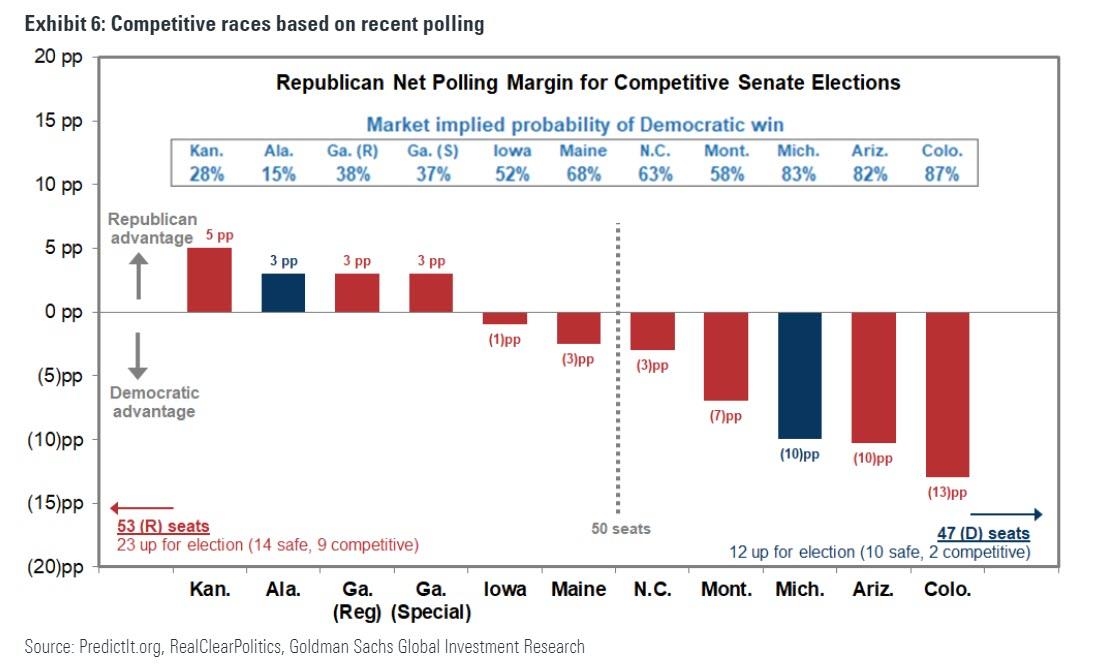

The Republicans currently have a 53-47 Senate majority but have 23 seats up for re-election in November while Democrats have just 12 seats up for re-election.

The latest polls and prediction market pricing indicate the Democrats are likely to capture six seats and lose one seat for a net gain of five seats — enough to gain majority control of the Senate for the first time since 2014. However, as in the case of the presidential election, the winners of close Senate races may not be known until well after Election Day when all the mail-in votes have been counted.

The volatility market’s pricing of election risk

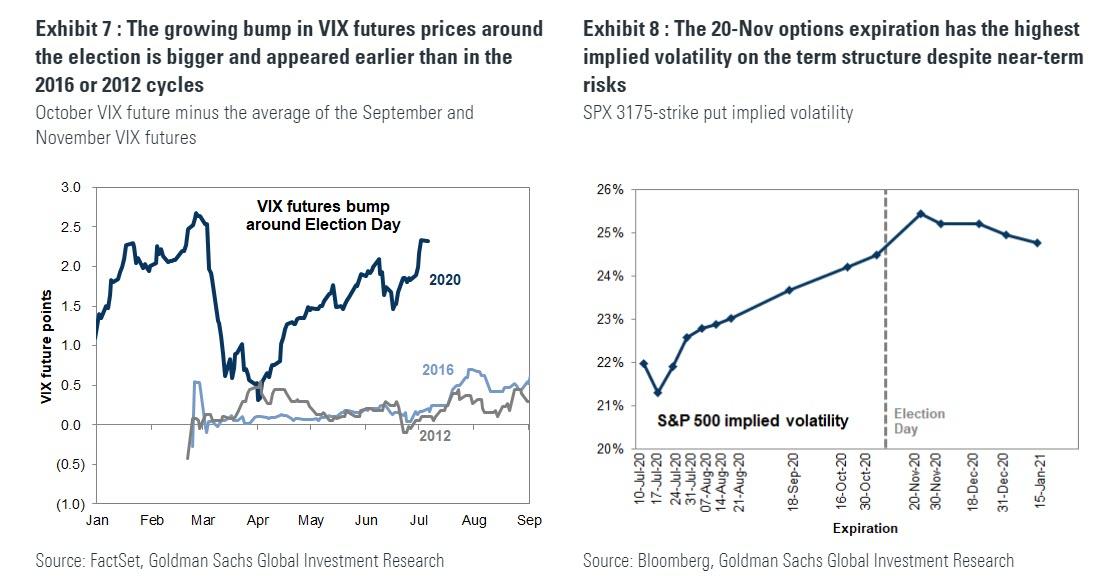

According to Kostin, option markets have been pricing in larger election risk than in prior cycles, and have started pricing election risk earlier. The bump in the VIX futures curve around the November election, which was already unusually large in January but faded during the height of the coronavirus crisis, is now close to its pre-virus high, and much larger than it ever was in the 2012 or 2016 election cycles. This implies that investors expect a close and important election and that more election-related risk is priced into the 21-Oct to 20-Nov period the October VIX future references than any other monthly period this year. Despite heightened near-term risks, including the Covid resurgence and the upcoming expiration of fiscal measures, option markets are expecting volatility to rise between now and November, peaking in the weeks around the November election.

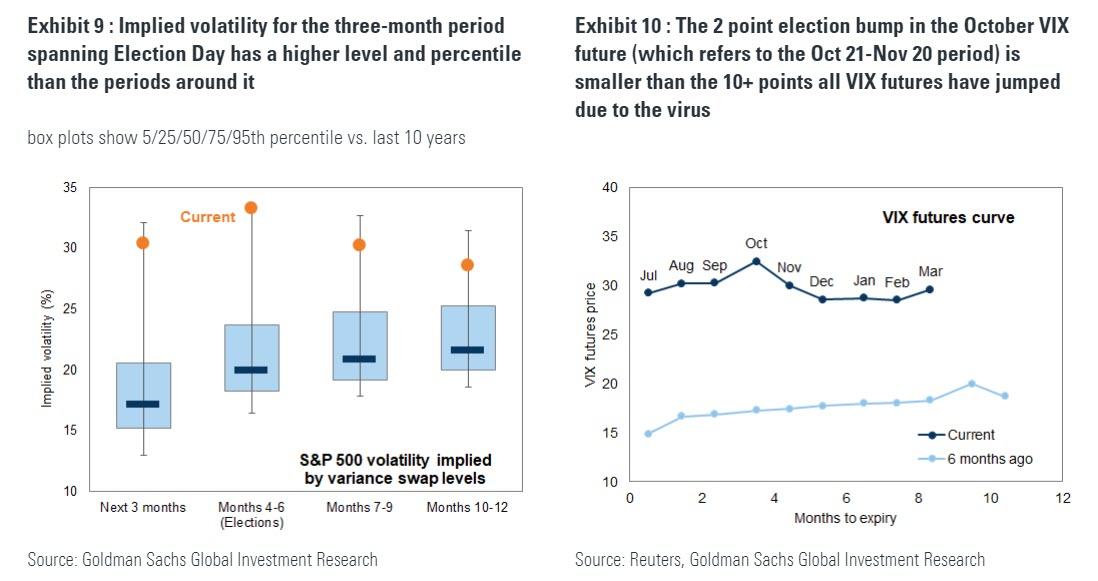

As Goldman adds, election-period hedges are very expensive, primarily because of the market impact of the coronavirus. Implied volatility for the period around November’s election is extremely high, with forward-starting volatility metrics for the three-month period spanning the election in its 97th percentile compared with the last 10 years. Both the level of implied volatility for the period spanning the election and its 10-year percentile are higher than the periods before and after it; however, implied volatility is extremely high across tenors. VIX futures of all maturities are 10-12 points higher than comparable futures were prior to the coronavirus crisis, compared with 2-3 points of extra volatility around the election – implying that most of the extra 4Q implied volatility is a result of the economic impact of the coronavirus.

Although options are pricing more risk in early November than for any other period, they are also pointing toward a volatile election season. The date when election results are known is important to option market participants because it determines which expiration traders should use for hedges. With Election Day less than four months away, the only November expirations that are listed are the third Friday (20-Nov) and the end-of-month (30-Nov), so option markets do not yet contain week-by-week information for the window around the election. Currently, derivative markets are pointing toward a peak level of volatility in the several-week period ending 20-Nov (the highest VIX future references the 21-Oct to 20-Nov period, and the highest implied at-the-money implied volatility in the SPX option market is the 20-Nov maturity, as no earlier expirations in November are listed yet).

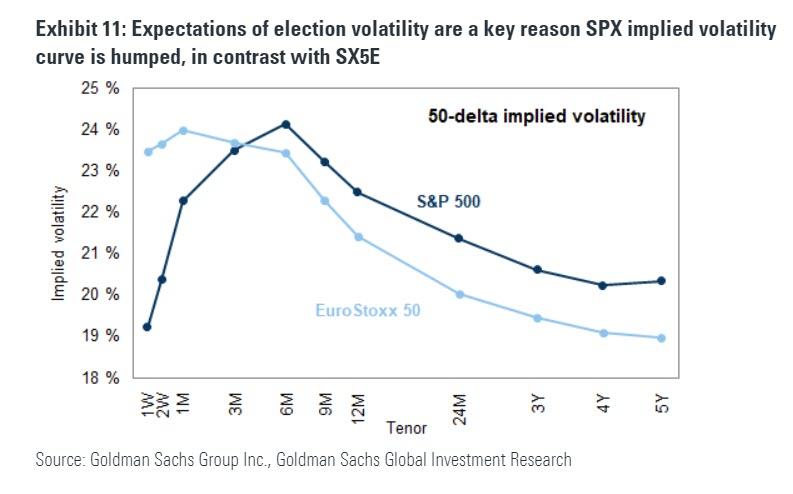

During the last two months, option markets have increased the level of risk expected after 20-Nov relative to the level of risk expected before the elections, indicating that an extended period of high volatility is anticipated. A severe market shock like the coronavirus crisis is typically followed by downward-sloping implied volatility curves as markets price in slow normalization; the unusual humped shape of the SPX curve (upward-sloping between now and the end of 2020, downward-sloping thereafter) points toward high volatility throughout the period around elections. Election risk is a key driver of the difference between the shape of the SPX implied volatility curve and the downward-sloping shape of the EuroStoxx 50’s.

Delayed primary results, a precedent for extended vote-counting, and a slightly inverted term structure lead Goldman to prefer December hedges to November hedges. Given the several-week delay in finalizing the results of the 2000 presidential election (in addition to the contentious 1876 election), the elevated volumes of mail-in ballots used in recent primary elections, and potential for increased mail in ballots this November, Kostin sees heightened risk that election-related volatility could extend beyond Election Day, and while the 20-Nov option expiration offers two additional weeks of cushion beyond 3-Nov, the strategist prefers extending hedges to the 18-Dec quarterly expiration. Currently, the December expiration has somewhat lower implied volatility than the November expiration.

Tax reform

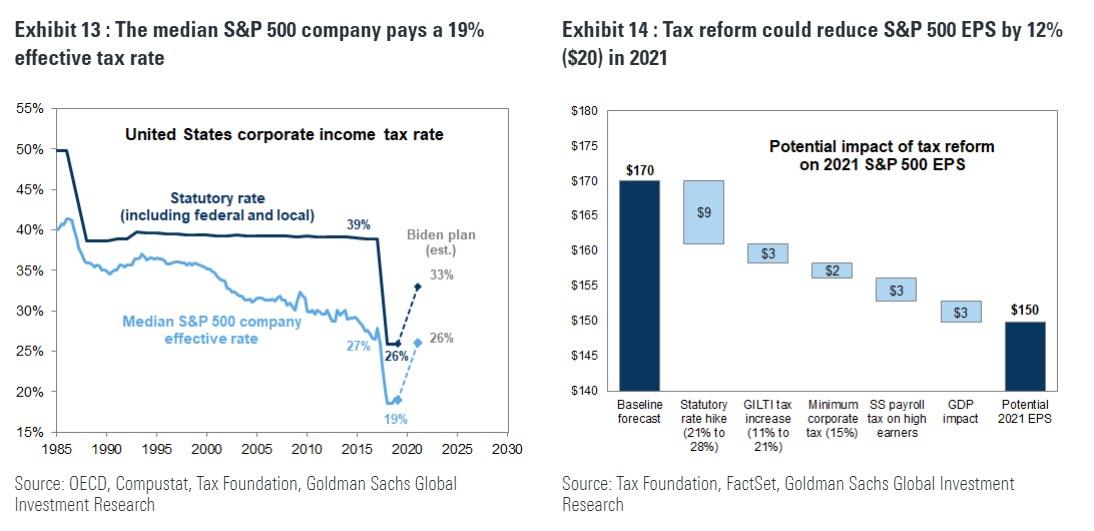

As noted at the top of this article, tax policy has been the potential consequence of the 2020 elections that has garnered the most focus from equity investors thus far. If enacted, Goldman estimates that the Biden tax plan would reduce our S&P 500 earnings estimate for 2021 by roughly $20 per share, from $170 to $150. According to the Tax Foundation, the former Vice President’s plan would raise the statutory federal tax rate on domestic income from 21% to 28%, reversing half of the cut from 35% to 21% instituted by the 2017 TCJA. In addition, the plan would double the GILTI tax rate on certain foreign income, impose a minimum tax rate of 15%, and add an additional payroll tax on high earners. Combined with a drag on US GDP of a similar magnitude to the boost that the TCJA created in 2018, this would reduce Goldman’s 2021 EPS estimate by roughly 12%. Of course, in addition to corporate tax policy, corporate earnings will be sensitive to regulation, trade policy, government spending, and other policy measures.

The recent performance of tax-sensitive stocks does not appear to fully reflect the tightening election race. A basket of stocks that experienced the largest boosts to earnings as a result of lower effective tax rates following the TCJA has outperformed the market in recent months despite surging Democratic odds. Stocks potentially exposed to the minimum tax rate and GILTI rate hike proposals have performed similarly.

The performance of tax-sensitive stocks is not surprising given extremely elevated uncertainty. In late 2017, high tax stocks outperformed sharply only once the TCJA legislation reached its final stages of Congressional ratification despite months of negotiation and drafting beforehand. Today, investors face not only uncertainty regarding the specifics of potential tax reform but also four more months of market volatility before the resolution of a close political race that could eliminate the likelihood of tax reform altogether.

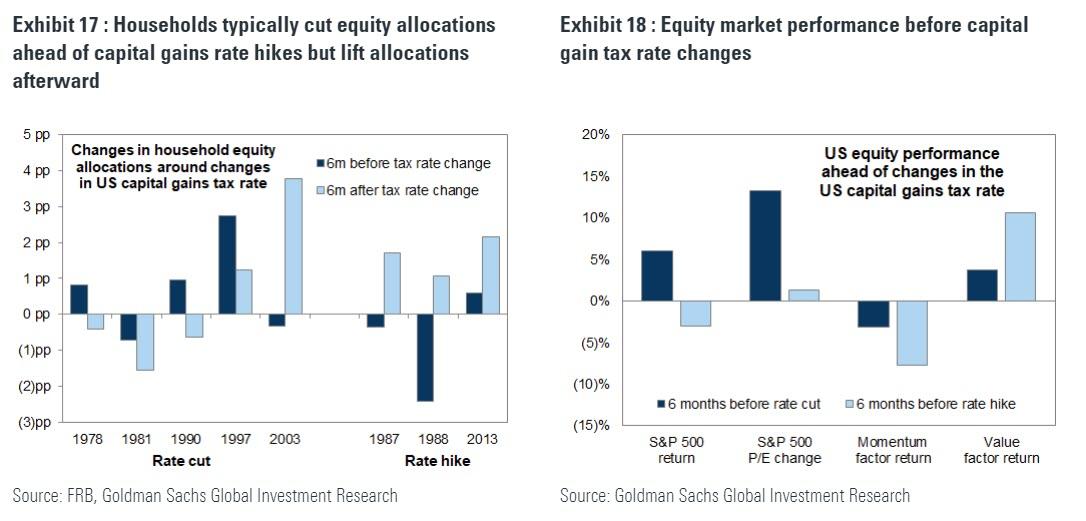

The Biden plan’s proposed changes to the corporate tax code would be complemented by a variety of changes to the personal tax code. These include an increase in the tax rate applied to capital gains and dividends for the highest income individuals. Although the historical sample is small and noisy, more often than not households have decreased equity allocations ahead of capital gains tax rate hikes in the past. Past capital gains tax hikes have also been associated with short-term declines in equity prices as well as the underperformance of high-momentum “winners” that had delivered the largest taxable gains to investors ahead of the rate hike.

If implemented, any equity market impact of a capital gains rate hike would likely be short lived. Many investors would likely adjust their portfolios in advance of the rate change, particularly if it went into effect late enough to capture the returns for investors who bought near the market bottom in March 2020. However, even with higher tax rates, the growth and yield of equities would remain attractive enough relative to most other asset classes that investors would likely reestablish any equity positions they sold ahead of the tax change (see Valuation at the Lower Bound, June 29, 2020). History supports this view: Household equity allocations have risen during the six months following each of the three capital gains tax rate hikes during the past 40 years.

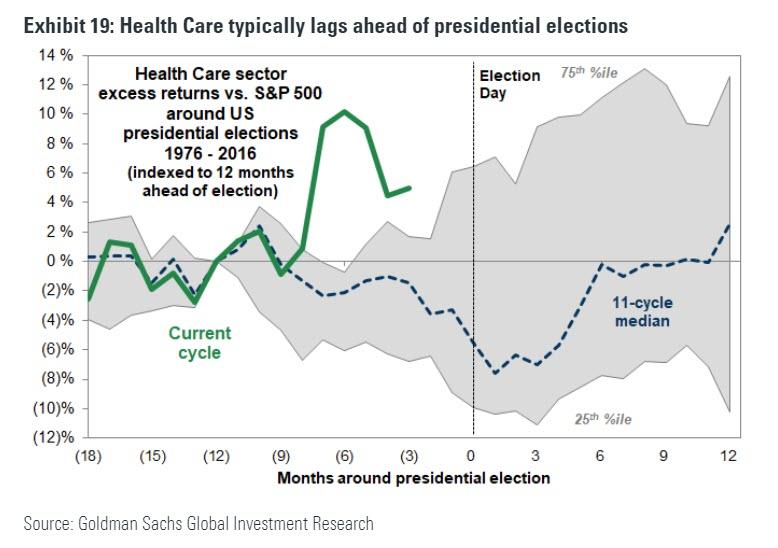

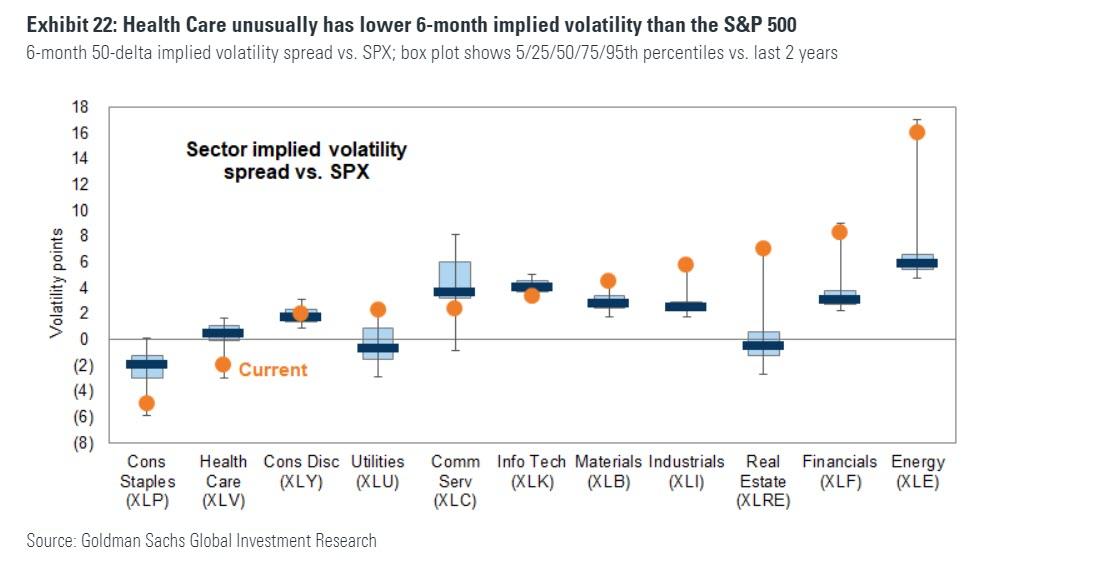

Health Care policy

The Health Care sector is one part of the equity market that appears to be pricing election risk. Due to the sector’s elevated exposure to government policy, uncertainty typically weighs on Health Care stocks ahead of presidential elections. This year, the sector has outperformed on the back on its earnings resilience during the pandemic. Bottom-up consensus forecasts current show Health Care EPS growing at a 6% CAGR between 2019-2021, second only to the 7% estimate for the Info Tech sector.

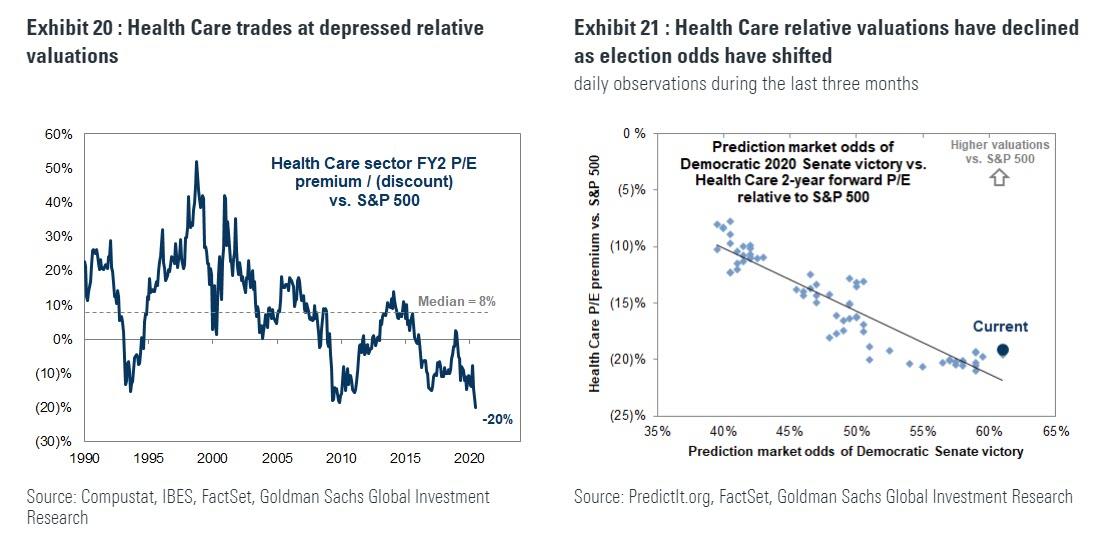

While earnings strength has supported the performance of Health Care stocks so far this year, the sector trades at nearly its lowest relative valuation multiples on record. Its valuations have correlated in recent months with the rise in Democratic election odds, and today the sector appears to be pricing roughly the same likelihood of Democratic Senate victory as the prediction markets. Within the sector, however, the relationship between political risk and stock valuations is less clear. Our Health Care sector specialist has highlighted the difficulty investors face in weighing the impact of the pandemic on earnings against the uncertainty of potential post-election policy changes.

In contrast with stock valuations, the volatility market does not appear to be pricing elevated political risk in the Health Care sector relative to the broad equity market. The XLV Health Care ETF currently has lower implied volatility than the S&P 500, which is unusual relative to history. In fact, the sector has lower implied volatility than any sector except for the defensive Consumer Staples.

via ZeroHedge News https://ift.tt/3ed0aOL Tyler Durden

New research from Yelp shows that as of June 15, there were nearly 140,000 total business closures on the website since March 1. When compared to similar research released in April, which showed more than 175,000 business closures, these latest numbers indicate that more than 20% of businesses closed in April have reopened.

In March, restaurants had the highest numbers of business closures listed on the app compared to other industries, and the rate of closure has remained high. Of the businesses that closed, 17% are restaurants, and 53% of those restaurant closures are indicated as permanent on Yelp. Retail, however, is the hardest hit overall.

During the peak of the pandemic, the number of diners seated across Yelp Reservations and Waitlist dropped essentially to zero. In early June, numbers of diners seated are down 57% of pre-pandemic levels.

Predictions about the restaurant industry’s fate in a post-pandemic world have been abundant throughout the crisis. The National Restaurant Association estimated that 15% of restaurants could close, while Barclay’s estimate is more optimistic, predicting approximately 10% of restaurants will shutter permanently.

Though it’s hard to find a silver lining in Yelp’s data, some predictions have been more dire still. In May, OpenTable said one in four restaurants were at risk for closure, for example, though those numbers focus on restaurants that use the reservations platform. Casual or fine dining sit-down restaurants and mom-and-pop concepts that are not well capitalized are expected to experience the brunt of this crisis. The Independent Restaurant Coalition, for example, forecast that as many as 85% of independent restaurants could permanently close by the end of the year.

Yelp’s data does illustrate how some restaurants have been able to weather the storm, however, reporting a 10-fold increase in searches for takeout since March 10, for example. Takeout and delivery searches are up 148%, with Yelp predicting this off-premise trend could be here to stay.

The research also shows that restaurants catering to group dining are making a comeback, with fondue searches up 123%, tapas bars up 98%, hot pot up 49% and buffets up 17%. Conversely, searches for cuisines that were popular during the past three months have begun to wane, including pizza (down 28%), Chinese (down 26%) and fast food (down 18%).

While the pendulum has swung toward group dining, perhaps due to pent up demand after three-plus-months of safer at home orders and dining room closures in some markets, this interest could be short lived. This data was released before a number of states — New Jersey, New York and California among them — have delayed or re-closed some or all of their restaurants due to spiking coronavirus cases. Extended closures will further challenge operators who are burning through cash to maintain rent, labor and other costs. Restaurants with the strongest balance sheets and best access to capital have the best chance to endure sustained closures. The industry will favor the haves and weed out the have-nots, a trend that has become clearer as major chains like Taco Bell, Domino’s and McDonald’s have announced massive hiring sprees.

via ZeroHedge News https://ift.tt/3f6VsDk Tyler Durden

{kind=link}