In February, Selene Saavedra Roman, a Texas-based flight attendant, took what should have been an uneventful work trip—a round-trip flight to Mexico and back. But when she landed in Houston, Immigration and Customs Enforcement (ICE) detained her and placed her in a detention center. She was released this past Friday after six weeks in custody.

Saavedra Roman is a Deferred Action for Childhood Arrivals (DACA) recipient, having come to the U.S. illegally when she was 3 years old. Otherwise known as a “dreamer,” she is among 700,000 others who arrived in the States as young children and who are temporarily protected from deportation.

Even still, when she accepted a job with the regional Mesa Airlines, it was because she thought they would not require her to travel internationally. Anxious over the complex web of immigration policies that affect Dreamers, she told the company that she preferred not to leave the continental U.S., according to The Washington Post.

In the past, DACA recipients have been able to apply to travel outside of the country, so long as they could show it was for humanitarian, educational, or employment purposes (and as long as they could come up with the $575 application fee). But those pleas now fall on deaf ears. New restrictions under the Trump administration forbid Dreamers from leaving and reentering the country under any circumstances.

Belinda Arroyo, Saavedra Roman’s attorney, says that her client shouldn’t have bypassed the government. But she adds that Saavedra Roman was unaware of the specific travel stipulations. After receiving notice of her Mexico flight, she voiced her general uneasiness with company superiors at Mesa Airlines, who incorrectly told her she had no reason to worry.

In that vein, Arroyo argues that Saavedra Roman is a “poster child” for the immigration system’s ills, particularly with the confusing changes that have taken place since President Trump took office. “They’ve been lost in legal limbo, and it’s getting quite ridiculous,” she tells The Washington Post.

So ridiculous that neither employers nor DACA recipients are quite certain what the rules are. “It is patently unfair for someone to be detained for six weeks over something that is nothing more than an administrative error and a misunderstanding,” Mesa Airlines CEO Jonathan Ornstein said in a statement.

“Basically the administrative error is that they told her she could travel,” Arroyo toldThe Hill.

Although Saavedra Roman has since been released from detention, the threat of deportation still looms. Arroyo says that, while her client was still in custody, she was notified that ICE has asked the United States Citizenship and Immigration Services (USCIS) if her DACA status could be rescinded.

Saavedra Roman is married to an American citizen who was already in the process of seeking a green card on her behalf when she was detained by ICE. They were reunited on Friday.

“I cried and hugged my husband and never wanted to let go,” she said in a statement following her release. “I am thankful and grateful for the amazing people that came to fight for me, and it fills my heart. Thank you to everyone that has supported. I am just so happy to have my freedom back.”

There is nothing intrinsically profitable about either robotics or AI.

At the request of colleague/author Douglas Rushkoff (his latest book is Team Human), I’m publishing last week’s Musings Report, which was distributed only to subscribers and patrons of the site.)

The core assumption of Universal Basic Income (UBI) and other plans to redistribute wealth and income more broadly is that the world is becoming wealthier, and so the pool of income and wealth that can be taxed is always expanding.

This pool of available wealth and income is so vast, we’re assured, that taxing the super-wealthy will not really dent their wealth or the economy as a whole.

But what if the world is rapidly becoming poorer in every important sense? What if the decline in the standard of living of the bottom 90% of households that I’ve often addressed is not simply the result of the top 10% taking a greater share of the output (gains), but of the entire pie shrinking?

I believe the steady decline of the purchasing power of labor–the source of most households’ income–is not just the result of way income is distributed, but of a steadily diminishing pool of real-world wealth.

We must start any discussion of total wealth/income by asking: what are we measuring with currencies such as dollars? What’s not being measured?

As often noted in my writings, we optimize what we measure, and so since we measure financial accounts embedded in markets, we maximize the accumulation of currency and measure what it buys in markets.

But as I’ve explained in my books, markets only price goods and services in the here and now. They lack mechanisms to measure the lifecycle costs of the goods, the degradation of wild fisheries, the loss of soil fertility (depletion), the opportunity cost of what could have been done with money squandered on consumption, and so on.

The decline of fresh water tables and the shrinkage of glaciers that feed fresh water rivers don’t make it into “price discovery” of markets.

As a result, the expansion of “money” creates an illusion of rising wealth when in fact the natural capital we depend on is declining rapidly. But since we don’t measure this in “price,” it’s ignored.

If we combine the loss of purchasing power of labor with the tremendous loss of natural capital/wealth, it becomes self-evident that adding a zero to financial “wealth” hasn’t made us actually wealthier in terms of what we can buy with our labor and what resources are still available to us for future “growth.”

A second assumption of UBI/redistribution proponents is that robotics and artificial intelligence (AI) will greatly increase humanity’s wealth by replacing human labor at a fraction of the cost.

This assumption is made so easily and often, it’s easy to overlook that the claims never seem to originate from those actually manufacturing robots–a very capital and resource-intensive enterprise, and labor-intensive once maintenance and repair are added in.

There are a number of key economic assumptions being made beneath the surface of this claim that ignore all sorts of inconvenient realities.

Take the simple example of a Roomba robot vacuum. The presumption is this labor saving device will replace human labor. But since I don’t pay myself to clean my own house, there is no reduction in labor costs; there is only an additional consumption of resources and capital.

Proponents of the idea that robotics/AI will generate vast new wealth that we can all tap without trade-offs overlook the enormously deflationary impact of technology in general and of commoditized technology specifically: once robotics and AI become commoditized (i.e. the bits and pieces and coding are available everywhere at a steadily decreasing cost), prices will drop, reducing profits to razor-thin margins.

This is the story of commoditized manufacturing in China, where few companies reap significant profits and most scrape by on extremely thin margins.

“The profits earned by 1,444 listed companies on the SME board and growth enterprise board are not even equal to one and half times the profit of the Industrial and Commercial Bank of China.”

Why would commoditized robotics and AI software be any different?

Consider Uber and Lyft, both of which are losing billions of dollars operating at their current scale. Profits are presumed to emerge at some magical point when their incomes rise and the expenses drop. But given the presence of competition and the cost structure, how can these services raise prices enough to turn a profit?

As for eliminating the expense of drivers via self-driving cars: if we look at commoditized business models like Uber and Lyft, we find the labor component is actually rather marginal. Cutting $1 billion in costs by eliminating drivers presumes a monopoly and equipment and software that are proprietary, i.e. a means to push higher prices on a customer base with few other options.

But if we know anything about the push to self-driving cars, we know the competition in fierce and global, and all the necessary parts–sensors, artificial vision software, etc.– are rapidly being commoditized.

The truth is these services are not inherently profitable: the cost of operating a very complex vehicle will never be near-zero, and neither will the liability. Many other transport options will always be available to customers, starting with walking, public transport, biking, arranging a ride with a friend and the “black market” ride-sharing that will inevitably arise to cut out Uber’s share of the fee.

Technology that can be commoditized is fantastically deflationary: costs decline and profit margins soon go to near-zero.

For this reason alone, robotics and AI may well cut the cost of various goods and services but at the expense of profits.

There is an exception, of course: people will pay more for status. People pay inordinate sums for an Apple phone because it has intangible but oh-so coveted status. But there is no equivalent in the vast majority of commoditized sectors. Very few people will pay extra for an Uber ride based on the company’s brand. What unique and highly coveted status is associated with Uber or Lyft? The answer is none, just as it is for digital memory, mobile phone cameras and thousands of other commoditized technologies.

Apple has status because it protects its proprietary integration of software and hardware which make it difficult to commoditize. But Android and cheap components are chipping away at the functional advantages of Apple’s proprietary offerings.

There is only one Apple globally. Very few enterprises escape the commoditization of their business, and these generally have high barriers to entry. Semiconductor fabrication plants cost upwards of $2 billion each; that’s a high barrier of entry to a highly volatile and uncertain market. Few companies are willing to gamble the $2 billion in a field already crowded with competitors.

Counting on hundreds of super-profitable corporations to generate vast new wealth to be taxed and redistributed ignores the real-world dynamics of technology, competition, and most importantly commoditization.

Let’s summarize:

1. The problem is we have based our entire civilization on “growth,” the never-ending expansion of consumption of resources, energy and capital, the the permanent expansion of everything: jobs, consumers, credit and so on.

Robotics and AI simply add to the planet’s burden. They don’t reduce it. Robots are intrinsically energy and resource-intensive, capital-intensive and complex. Every robot is one product cycle or one component failure away from being just another piece of industrial junk bound for the landfill or perhaps the recycling yard–but there’s no guarantee the robot will be disposed of properly, either, as recycling complex manufactured goods is intrinsically costly.

AI software code may be “free” but the system to manifest AI in the real world is enormously resource and capital intensive: the cost of manufacturing chips is non-trivial, and power-hungry processors require huge amounts of energy to operate and replace.

2. Just as the high cost and complexity of robotics and AI is intrinsic, there is nothing intrinsically profitable about either robotics or AI. Merely replacing human labor doesn’t automatically generate vast profits for decades; competitors will also eliminate their human labor. The more capital intensive the business, the more marginal the role of labor in the production process. Replacing human labor only generates profits until competitors eliminate their laborers, or until new technology obsoletes the entire business model.

3. The planet’s natural capital and buffers are being exploited and consumed at a rate that guarantees disruption of essentials such as grain and fresh water. There are no cheap technological fixes to the depletion of natural capital. No robot or AI software can restore depleted soil or replace soil that washed away.

If we add in the loss of natural capital and the full lifecycle costs of our “growth”-dependent global system, we;re losing ground and becoming poorer by the day. Having central banks create more “money” can generate a phantom wealth for a short time, but as the saying has it, Nature Bats Last. Counting on phantom wealth to power an unsustainable system is delusional.

We are adding knowledge and information to the pool of humanity’s knowledge, but if we don’t use that “wealth” to change the fundamental flaws in “growth” and a dependency on phantom wealth, we’re still becoming poorer by the day.

Controversy has struck the Southern Poverty Law Center, the formidable progressive law firm best known for tracking hate groups in the U.S. Co-founder Morris Dees, President Richard Cohen, and other top executives are exiting the organization amidst a staff uprising over alleged sexual and racial harassment in the work place.

The leadership shakeup, fueled by allegations that black staffers were shut out of key positions and that Dees personally harassed female staffers, has brought the SPLC considerable media scrutiny, and it’s about time. Regardless of whether these specific accusations have merit, the SPLC should face a reckoning over its extremely shoddy work, which has mistakenly promoted the idea that fringe hate groups are a rising threat.

Peddling this false narrative has long been the SPLC’s business model, and the Trump years have been especially profitable, since the group was almost perfectly positioned to capitalize on growing liberals fears about hate crimes, resurgent white nationalism, and the alt-right. Over the course of the Trump campaign and presidency, the SPLC has added dozens of staffers, saw its social media following rise dramatically, ramped up its fundraising, and built a $200 million endowment. Its role has been to provide intellectual support for a central narrative of the #Resistance: Hate, broadly defined, is surging across America, and Trump is to blame.

But the SPLC’s hate tally is incredibly suspect, as left-of-center writer Nathan Robinson explained in a terrific article for Current Affairs. According to the SPLC’s hate map, there were more than 1,000 hate groups in the U.S. in 2018—nearly twice as many as existed in 2000. The number has increased every year since 2014.

The map is littered with dots that provide more information on each specific group, and this is where the SPLC gives away the game. Consider a random state—Oklahoma, for example, is home to nine distinct hate groups, by the SPLC’s count. Five of them, though, are black nationalist groups: the Nation of Islam, Israel United in Christ, etc. The SPLC counts each chapter of these groups separately, so the Nation of Islam counts as two separate hate groups within Oklahoma (its various chapters in other states are also tallied separately). The map makes no attempt to contextualize all of this—no information is given on the relative size or influence of each group.

In his piece, Robinson describes the map as an “outright fraud,” and it’s hard to argue with him:

In fact, when you actually look at the hate map, you find something interesting: Many of these “groups” barely seem to exist at all. A “Holocaust denial” group in Kerrville, Texas called “carolynyeager.net” appears to just be a woman called Carolyn Yeager. A “male supremacy” group called Return of Kings is apparently just a blog published by pick-up artist Roosh V and a couple of his friends, and the most recent post is an announcement from six months ago that the project was on indefinite hiatus. Tony Alamo, the abusive cult leader of “Tony Alamo Christian Ministries,” died in prison in 2017. (Though his ministry’s website still promotes “Tony Alamo’s Unreleased Beatles Album.”) A “black nationalist” group in Atlanta called “Luxor Couture” appears to be an African fashion boutique. “Sharkhunters International” is one guy who really likes U-boats and takes small groups of sad Nazis on tours to see ruins and relics. And good luck finding out much about the “Samanta Roy Institute of Science and Technology,” which—if it is currently operative at all—is a tiny anti-Catholic cult based in Shawano, Wisconsin.

Sloppily tallying hate in service of a greater narrative is par for the course at the SPLC. The group’s report on Trump-inspired schoolyard bullying is similarly flawed: Its survey was unscientific, and based on anecdotes reported by members of the SPLC’s mailing list.

When it comes to misleading hate crime data, the SPLC is far from the only offender. Many in the media have exaggerated a finding by the Anti-Defamation League that anti-Semitic hate has increased 57 percent under Trump. (Bomb threats made by an Israeli teenager were largely responsible for the perceived increase: anti-Semitic assaults actually decreased substantially.) The FBI’s hate crime data has also been widely mischaracterized.

Still, the SPLC stands out. It previously characterized Maajid Nawaz as an anti-Muslim extremist—but Nawaz is a progressive whose work is aimed at de-radicalizing Muslim extremists. To this day, the SPLC lists Charles Murray’s ideology as “white nationalist.”

Over at National Review, David French urges the SPLC to “rediscover its roots.” The organization used to do much more work aligned with its name: representing impoverished death row inmates, for example, and battling the KKK in court. It has plenty of money, and could hire an army of lawyers to really make a difference in the lives of criminal defendants. But first, the organization needs to give up on the project of inflating the threat posed by fringe nutcases.

There is nothing intrinsically profitable about either robotics or AI.

At the request of colleague/author Douglas Rushkoff (his latest book is Team Human), I’m publishing last week’s Musings Report, which was distributed only to subscribers and patrons of the site.)

The core assumption of Universal Basic Income (UBI) and other plans to redistribute wealth and income more broadly is that the world is becoming wealthier, and so the pool of income and wealth that can be taxed is always expanding.

This pool of available wealth and income is so vast, we’re assured, that taxing the super-wealthy will not really dent their wealth or the economy as a whole.

But what if the world is rapidly becoming poorer in every important sense? What if the decline in the standard of living of the bottom 90% of households that I’ve often addressed is not simply the result of the top 10% taking a greater share of the output (gains), but of the entire pie shrinking?

I believe the steady decline of the purchasing power of labor–the source of most households’ income–is not just the result of way income is distributed, but of a steadily diminishing pool of real-world wealth.

We must start any discussion of total wealth/income by asking: what are we measuring with currencies such as dollars? What’s not being measured?

As often noted in my writings, we optimize what we measure, and so since we measure financial accounts embedded in markets, we maximize the accumulation of currency and measure what it buys in markets.

But as I’ve explained in my books, markets only price goods and services in the here and now. They lack mechanisms to measure the lifecycle costs of the goods, the degradation of wild fisheries, the loss of soil fertility (depletion), the opportunity cost of what could have been done with money squandered on consumption, and so on.

The decline of fresh water tables and the shrinkage of glaciers that feed fresh water rivers don’t make it into “price discovery” of markets.

As a result, the expansion of “money” creates an illusion of rising wealth when in fact the natural capital we depend on is declining rapidly. But since we don’t measure this in “price,” it’s ignored.

If we combine the loss of purchasing power of labor with the tremendous loss of natural capital/wealth, it becomes self-evident that adding a zero to financial “wealth” hasn’t made us actually wealthier in terms of what we can buy with our labor and what resources are still available to us for future “growth.”

A second assumption of UBI/redistribution proponents is that robotics and artificial intelligence (AI) will greatly increase humanity’s wealth by replacing human labor at a fraction of the cost.

This assumption is made so easily and often, it’s easy to overlook that the claims never seem to originate from those actually manufacturing robots–a very capital and resource-intensive enterprise, and labor-intensive once maintenance and repair are added in.

There are a number of key economic assumptions being made beneath the surface of this claim that ignore all sorts of inconvenient realities.

Take the simple example of a Roomba robot vacuum. The presumption is this labor saving device will replace human labor. But since I don’t pay myself to clean my own house, there is no reduction in labor costs; there is only an additional consumption of resources and capital.

Proponents of the idea that robotics/AI will generate vast new wealth that we can all tap without trade-offs overlook the enormously deflationary impact of technology in general and of commoditized technology specifically: once robotics and AI become commoditized (i.e. the bits and pieces and coding are available everywhere at a steadily decreasing cost), prices will drop, reducing profits to razor-thin margins.

This is the story of commoditized manufacturing in China, where few companies reap significant profits and most scrape by on extremely thin margins.

“The profits earned by 1,444 listed companies on the SME board and growth enterprise board are not even equal to one and half times the profit of the Industrial and Commercial Bank of China.”

Why would commoditized robotics and AI software be any different?

Consider Uber and Lyft, both of which are losing billions of dollars operating at their current scale. Profits are presumed to emerge at some magical point when their incomes rise and the expenses drop. But given the presence of competition and the cost structure, how can these services raise prices enough to turn a profit?

As for eliminating the expense of drivers via self-driving cars: if we look at commoditized business models like Uber and Lyft, we find the labor component is actually rather marginal. Cutting $1 billion in costs by eliminating drivers presumes a monopoly and equipment and software that are proprietary, i.e. a means to push higher prices on a customer base with few other options.

But if we know anything about the push to self-driving cars, we know the competition in fierce and global, and all the necessary parts–sensors, artificial vision software, etc.– are rapidly being commoditized.

The truth is these services are not inherently profitable: the cost of operating a very complex vehicle will never be near-zero, and neither will the liability. Many other transport options will always be available to customers, starting with walking, public transport, biking, arranging a ride with a friend and the “black market” ride-sharing that will inevitably arise to cut out Uber’s share of the fee.

Technology that can be commoditized is fantastically deflationary: costs decline and profit margins soon go to near-zero.

For this reason alone, robotics and AI may well cut the cost of various goods and services but at the expense of profits.

There is an exception, of course: people will pay more for status. People pay inordinate sums for an Apple phone because it has intangible but oh-so coveted status. But there is no equivalent in the vast majority of commoditized sectors. Very few people will pay extra for an Uber ride based on the company’s brand. What unique and highly coveted status is associated with Uber or Lyft? The answer is none, just as it is for digital memory, mobile phone cameras and thousands of other commoditized technologies.

Apple has status because it protects its proprietary integration of software and hardware which make it difficult to commoditize. But Android and cheap components are chipping away at the functional advantages of Apple’s proprietary offerings.

There is only one Apple globally. Very few enterprises escape the commoditization of their business, and these generally have high barriers to entry. Semiconductor fabrication plants cost upwards of $2 billion each; that’s a high barrier of entry to a highly volatile and uncertain market. Few companies are willing to gamble the $2 billion in a field already crowded with competitors.

Counting on hundreds of super-profitable corporations to generate vast new wealth to be taxed and redistributed ignores the real-world dynamics of technology, competition, and most importantly commoditization.

Let’s summarize:

1. The problem is we have based our entire civilization on “growth,” the never-ending expansion of consumption of resources, energy and capital, the the permanent expansion of everything: jobs, consumers, credit and so on.

Robotics and AI simply add to the planet’s burden. They don’t reduce it. Robots are intrinsically energy and resource-intensive, capital-intensive and complex. Every robot is one product cycle or one component failure away from being just another piece of industrial junk bound for the landfill or perhaps the recycling yard–but there’s no guarantee the robot will be disposed of properly, either, as recycling complex manufactured goods is intrinsically costly.

AI software code may be “free” but the system to manifest AI in the real world is enormously resource and capital intensive: the cost of manufacturing chips is non-trivial, and power-hungry processors require huge amounts of energy to operate and replace.

2. Just as the high cost and complexity of robotics and AI is intrinsic, there is nothing intrinsically profitable about either robotics or AI. Merely replacing human labor doesn’t automatically generate vast profits for decades; competitors will also eliminate their human labor. The more capital intensive the business, the more marginal the role of labor in the production process. Replacing human labor only generates profits until competitors eliminate their laborers, or until new technology obsoletes the entire business model.

3. The planet’s natural capital and buffers are being exploited and consumed at a rate that guarantees disruption of essentials such as grain and fresh water. There are no cheap technological fixes to the depletion of natural capital. No robot or AI software can restore depleted soil or replace soil that washed away.

If we add in the loss of natural capital and the full lifecycle costs of our “growth”-dependent global system, we;re losing ground and becoming poorer by the day. Having central banks create more “money” can generate a phantom wealth for a short time, but as the saying has it, Nature Bats Last. Counting on phantom wealth to power an unsustainable system is delusional.

We are adding knowledge and information to the pool of humanity’s knowledge, but if we don’t use that “wealth” to change the fundamental flaws in “growth” and a dependency on phantom wealth, we’re still becoming poorer by the day.

European markets were volatile today but UK’s FTSE continues to underperform as various Brexit deadlines loom…

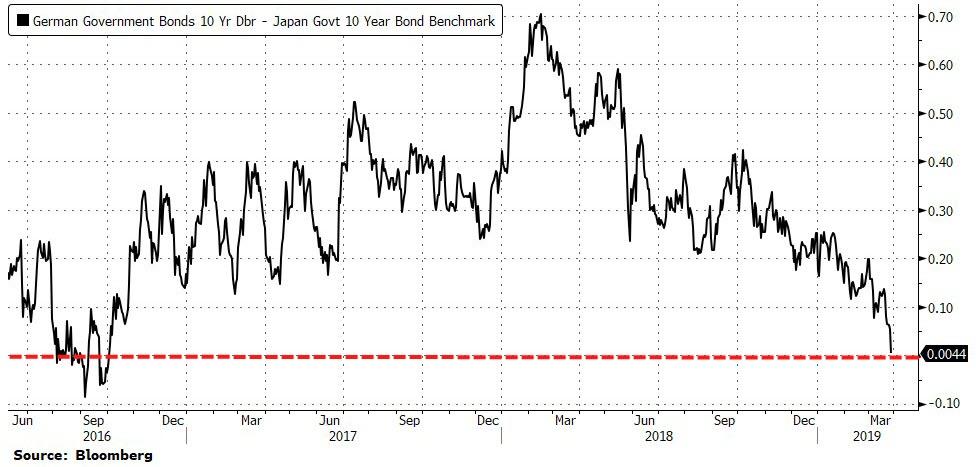

Meanwhile, German bund yields dropped back below JGB 10Y yields for the first time since 2016…

US markets tumbled shortly after the ubiquitous opening ramp, but reversed the downswing at the EU close. Nasdaq was the laggard today… (Dow was ramped to unchanged but all markets faded into the close)

S&P battled with 2800 all day…

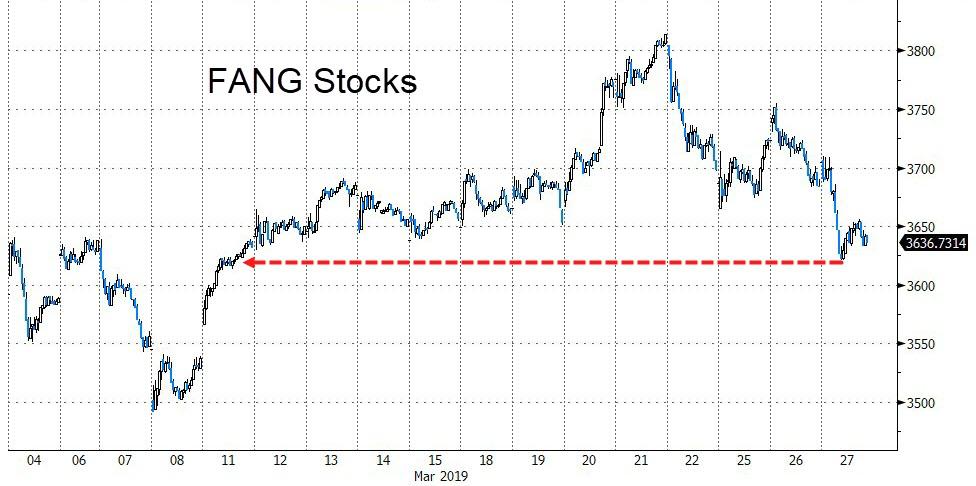

Banks and Big Tech were both lower on the day…

With FANG stocks ugly…

Semis closed at 10-day lows.

If the yield curve is right, banks have a lot further to fall…

Before we leave stock-land, let’s take a peak at Brazil which topped 100,000 for the first time ever and has plunged over 7% since…

Treasury yields continued to tumble (down 4-5bps across the curve today)…

10Y tumbled to its lowest close since Dec 2017…

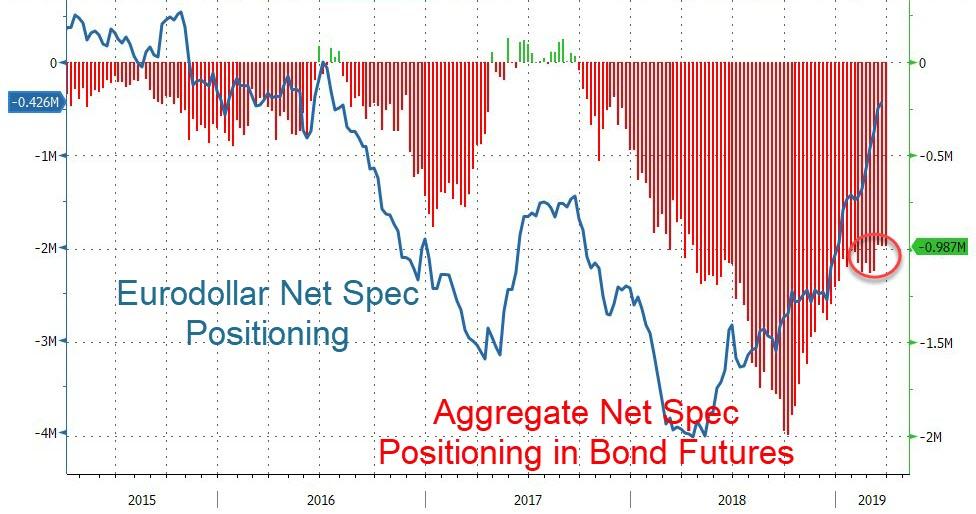

And arguably there is a lot more bond shorts to squeeze before this run is over…

Pick your point on the yield curve and it’s inverting (or inverting further). Here is the 3m-18m T-Bill curve (shown – in academic papers – to have highest tracking for future Fed path)…

The Dollar rallied for the second day in a row but failed twice to break the 97.00 level…

Cable trod water around 1.32 for the 3rd day in a row until May resignation and BoJo flip-flop headlines sparked a late rally…

EM FX plunged today – its been a wild ride recently…

Cryptos rallied on the day with Bitcoin Cash leading the way…

Weakness across all commodities today even as the dollar only managed modest gains…

Some ‘fiduciary’ decided that 0945ET was the exactly right time to dump just under a billion dollars of paper gold…

But Gold futures found support at their 200DMA

Silver broke below its 100DMA and found support at its 50DMA.

Permian natgas prices plummeted to record lows after a pipeline failure…

Finally, and burying the lead, after Moore’s sycophantic op-ed, the market is now pricing in over 40bps of Fed rate-cuts in 2019 – dramatically more dovish than The ECB…

As Fed credibility is well and truly buried – so what is keeping this chasm alive?

via ZeroHedge News https://ift.tt/2FDYzTQ Tyler Durden

Robert Mueller’s investigation is over, but questions still abound. Not about collusion, Russian interference or obstruction of justice, but about the leading lights of journalism who managed to get the story so wrong, and for so long. It wasn’t merely an error here or there.

America’s blue-chip journalists botched the entire story, from its birth during the presidential campaign to its final breath Sunday – and they never stopped congratulating themselves for it.

Last year the New York Times and Washington Post shared a Pulitzer Prize “for deeply sourced, relentlessly reported coverage in the public interest that dramatically furthered the nation’s understanding of Russian interference in the 2016 presidential election and its connections to the Trump campaign, the President-elect’s transition team and his eventual administration.” A 2017 Time magazine cover depicted the White House getting a “makeover” to transform it into the Kremlin.

All based on a theory—that the president of the United States was a Russian asset—produced by a retired foreign spy whose work was funded by the Democratic National Committee and Hillary Clinton’s campaign. An unbiased observer would have taken the theory’s partisan provenance as a red flag, but most political journalists saw nothing but green lights. No unverified rumor was too salacious and no anonymous tip was too outlandish to print. From CNN to the Times and the Post, from esteemed and experienced reporters to opinion writers and bloggers, everyone wanted a share of the Trump-treason beat. What good is the 21st-century Watergate if you don’t at least make an effort to cast yourself as the fearless journalist risking it all who got that one big tip that brought down a president?

Not only did the press fail to destroy Donald Trump’s presidency; it provided voluminous evidence for his repeated charge of “fake news.”

Take CNN. The network reported in December 2017 that Donald Trump Jr. received special email access to stolen documents before their public release by WikiLeaks—an accusation that, if true, could have proved the president’s inner circle was colluding with Russian hackers intent on taking down Mrs. Clinton. But it turned out “the most trusted name in news” misreported the dates on the unsolicited emails to the president’s son. They had been sent to him days after WikiLeaks had published the pilfered documents. CNN still hasn’t explained why it failed to do basic due diligence on such an important story.

Another CNN foul-up came in June 2017, the month after President Trump fired James Comey as director of the Federal Bureau of Investigation. Mr. Trump said Mr. Comey had assured him three times that he wasn’t under FBI investigation. The network reported Mr. Comey would directly refute the president’s claim under oath. In reality, Mr. Comey’s own memos explicitly confirmed Mr. Trump’s statement.

A December 2016 Washington Post story “incorrectly said that Russian hackers had penetrated the U.S. electric grid,” as a later editor’s note acknowledged. “Authorities say there is no indication of that so far.” Slate falsely claimed in October 2016 that Mr. Trump’s computers were secretly sharing information with a Russian bank as part of a scheme to avoid detection.

Each new claim, true or not, became fodder for political pundits. Sure, there may be no actual smoking gun or verified information or anything even approximating evidence, but if you take all the disparate pieces and put them on the same corkboard, stand back at just the right distance, and squint really hard, you can almost make out a barrel and a plume of smoke.

Enter Jonathan Chait of New York magazine, author of the classic 2003 article “Why I Hate George W. Bush.” (“I hate the way he walks. . . . I hate the way he talks. . . . I even hate the things that everybody seems to like about him.”) Last July, before Mr. Trump met Mr. Putin in Helsinki, Mr. Chait penned a nearly 8,000-word piece titled “Will Trump Be Meeting With His Counterpart—or His Handler?” Mr. Chait’s speculation—that “Trump has been a Russian asset since 1987”—was worthy of the late Lyndon LaRouche.

In a January 2019 Twitter thread, meanwhile, New York Times columnist Paul Krugman asserted that “the failure to connect the dots on Trump-Russia” was one of the “big failures of 2016 campaign coverage.” He added:

“There is no sin quite as offensive as challenging conventional wisdom early, and then being proved right.”

Many in Washington and around the country believed Mr. Mueller’s investigation would put the entire issue to rest. If there was collusion, he’d find it. If there was obstruction of justice, he’d prosecute it. Whatever he found, the nation would accept it and move on.

“The best thing for our country is that Trump is innocent and that Mueller tells us he’s found nothing,” Garrett Graff of Wired tweeted Thursday, the day before Mr. Mueller submitted his report to Attorney General William Barr. “Mueller got everything he wanted,” Mr. Graff wrote Friday. “Never blocked by DOJ in pursuing something he requested. That’s big.”

But the next day, Mr. Graff excoriated Nikki Haley for agreeing: “No, everyone does not have to acknowledge that Trump didn’t interfere with Mueller,” Mr. Graff tweeted Saturday at the former United Nations ambassador. By Monday Mr. Graff was insisting that “a million questions” about Trump-Russia collusion remain.

Likewise, on Monday the irrepressible Mr. Chait insisted the president could still be guilty: “People who want to demonstrate their innocence make displays of cooperation with investigators,” he wrote. “His flamboyant refusal to cooperate deprives Trump of any claim to having been cleared.”

So much for accepting Robert Mueller’s conclusions and recommendations. If your objective is to bring down Mr. Trump, nothing Mr. Mueller or anyone else finds—or fails to find—makes a difference. Mr. Trump didn’t collude with Russia, but he did defeat Mrs. Clinton. From their behavior it is evident that many in the media view that as sufficient to establish his guilt. For them, the Trump-Russia investigation was never about protecting democracy or securing elections—never mind telling the truth, which is supposed to be their job.

via ZeroHedge News https://ift.tt/2FDB3Gx Tyler Durden

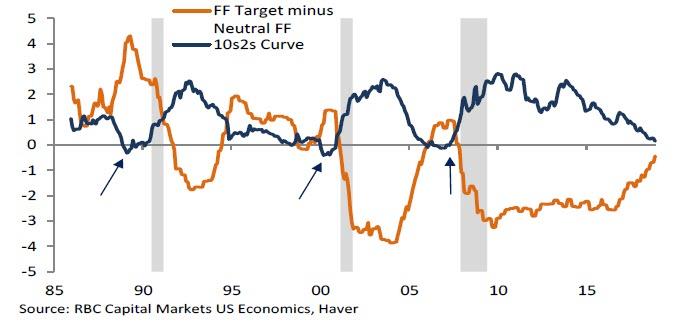

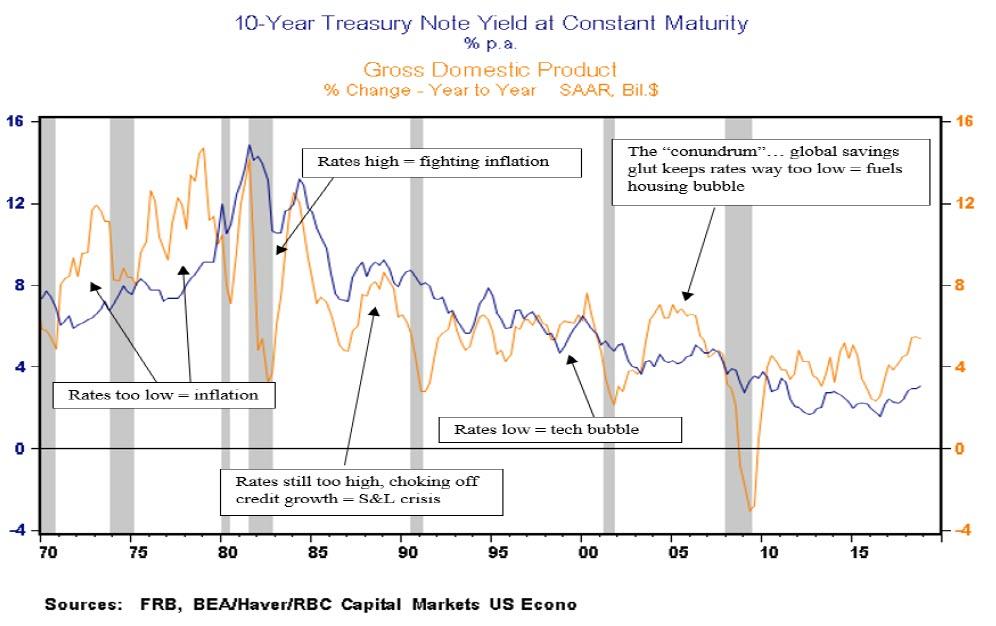

While much has been said about the inversion of the 3M-10Y yield curve (even as the 2s-10s remain “normal”) with one bank after another presenting its pitch why the historical track record is no longer applicable and why “this time may be different” for this fail-safe recession indicator which has correctly predicted 6 of the past 6 recessions, less has been said about the actual mechanics of what curve inversion actually means.

As BMO chief economist Tom Porcelli writes in a note from this week, the reasons this metric “works” historically is because the long-end of the curve is supposed to reflect some longer-run speed limit for nominal GDP growth. Traditionally when the economy overheats, as the Fed tightens short-run policy too much to avert an overheating economy, long-run growth prospects will slip below current growth trends and a reflection of this in the rates-world would be an inversion.

However, the problem with the current inversion and the historical record is that according to BMO, “the yield curve at present is not a referendum on the path of economic growth in the United States, but rather a function of goings on globally.” As evidence, Porcelli says to look no further than the strong correlation between US and German 10-year yields (or any other DM benchmark paper) in recent months.

The other issue, of course, is the prevailing argument that the Fed has overtightened which as Porcelli correctly observes is “almost laughable”, especially when considering that just in October, Powell said that the Fed Funds rate is a “long way” from neutral. Even using the Fed’s (rapidly dropping) estimate of the neutral rate, which as we noted recently is largely a function of the excessive debt in the system…

… policy right now is nowhere near past cyclical endpoints. And, when looking at the chart below, the BMO economist tells readers to note how the inversions that did lead to downturns lined up with a Fed Funds well north of neutral (unless of course netural is far lower than BMO’s generous estimate).

There is another “critical reason” why BMO believes the signal from the yield curve inversion this cycle is irrelevant.

As touched on above, historically the inverted curve works as a good recession signal “because the 10yr part of the curve theoretically reflects nominal growth prospects going forward.” However, this cycle, yields have decoupled from growth in a very material way. In fact, as shown in the next chart, nominal GDP growth in the US right now is running at about 5% and 10s are sitting at just 2.5%. This is why Porcelli repeats that in his view, yields have become more a function of global growth dynamics and have become anchored to low/negative sovereign yields abroad.

The immediate implication is that the United States is able to finance relatively good rates of growth at artificially suppressed interest rates, a beneficial development for an economy that runs on debt. But while the US may not be facing an imminent recession, at least according to the yield curve – which as a reminder has to begin steepening after the inversion for the real alarm bells to go off in the stock market…

… what the yield curve is telegraphing may be just as bad if not worse: according to BMO, contrary to conventional wisdom, this type of dynamic where GDP is running well above the 10Y yield has historically been very positive for asset inflation, “it was a big reason why the housing bubble was allowed to form – recall the conundrum,” and inflation in general.

So, to summarize BMO’s position, the bank is not on recession watch because of the yield curve inversion. Quite the opposite: “We are, more than any other point this cycle, on bubble watch.“

via ZeroHedge News https://ift.tt/2usC8uG Tyler Durden

In September 2018, a Montana jury found Stanley Patrick Weber—formerly a pediatrician who worked with Indian Health Service (IHS)—guilty of four charges related to his abuse of young Native American boys under his care. He was sentenced to 18 years in prison in January, and is currently in a jail cell in South Dakota awaiting trial on yet more child abuse charges.

According to a joint investigation by the Wall Street Journal and Frontline today, Weber will be costing taxpayers a lot of money while he is behind bars. In addition to the costs of incarcerating him, the Journalreports that taxpayers will continue to foot the bill for Weber’s pension.

By virtue of his 25 years working as a captain in the U.S. Public Health Service Commissioned Corps—one of seven uniformed services that funnels doctors to other federal agencies—plus five years’ service in the Army, Weber is entitled to an annual pension of roughly $100,000.

Absent a change to federal law, Weber could receive $1.8 million in pension benefits while serving out his current sentence. Periodic cost of living increases could raise that figure higher still.

Public Health Service officers, the Journal/Frontlinearticle notes, can be stripped of their pensions only if they’re found guilty of committing crimes while still on active duty. The only exception would be for treason, or if their crime was related to endangering national security.

Government officials have reportedly been pouring over the laws to see if there is any exemption or loophole that would allow them (or allow us) to stop paying Weber, but none has presented itself. Absent a change to federal law, Weber will receive a pension until he dies.

That Weber wasn’t arrested, tried, and convicted during his 25 years on the job—despite numerous complaints and whistleblower reports—is itself a huge failure on the part of the federal government. Had they gotten that part right, they wouldn’t have to pay Weber a pension now.

That the government is still forced to pay out his pension, however, is an extreme illustration of a separate problem with government pensions, whether offered at the local, state, or federal level: they are often treated as sacrosanct regardless of conduct on the part of individual employees that should disqualify them from receiving a pension.

Recall Scott Peterson, the Sheriff’s Deputy who failed to engage the Parkland shooter, who is still receiving an annual $104,000 pension despite his abject failure to protect students under his care.

Back in 2014, the Massachusetts Supreme Court ruled that a teacher who had been convicted of 11 counts of purchasing or possessing child pornography was still entitled to collect retirement benefits. A subsequent investigation by the Boston Heraldrevealed that at least five former teachers were still receiving pension benefits despite having been convicted of child pornography-related crimes.

Then there are the numerous court rulings that have prevented lawmakers in places like Oregon and Illinois from trimming back pension benefits for large masses of public employees whose benefits are busting budgets at unsustainable rates.

Weber’s case is uniquely awful and absurd. It nevertheless serves as an admittedly extreme example of how the laws governing public pensions often treat them as sacrosanct even when an employee’s individual conduct or basic fiscal reality demands they be trimmed back.

Bernie Sanders believes that FREE university education a “right, not a privilege.”

His fellow Bolshevik, Alexandria Ocasio-Cortez, also believes that tuition-free university “forms the basis of human dignity” and should be provided for free by any “moral society.”

They aren’t alone in holding these beliefs.

A recent survey conducted by CNBC shows that 60% of Americans support free university.

But what most of these people fail to realize is that there’s an enormous difference between an education and a university degree.

There’s obviously nothing wrong with a university degree. And for some professions they’re vital.

But a university degree is just an expensive piece of paper; it doesn’t actually confer any real knowledge.

An education, on the other hand, develops skills and mental agility to create real value in the world.

And while a university degree can cost you an enormous amount of money (students in America have taken out $1.4 trillion in student debt), an education can be completely free.

There are thousands of free resources out there that people can take advantage of to learn valuable skills.

For example, companies like Microsoft will teach you programming languages – for FREE – and then encourage you to apply for a job with them.

That’s an incredible opportunity to learn real-world, applicable skills that you can use to create an income for yourself.

In the same vein, Google recently announced a partnership with 120,000 libraries across the US to teach people how to code.

And 96% of Americans live near a library.

(That is not counting the thousands of other books you can learn from – for free – at the library.)

There are also websites (like edX.org) where you can take dozens of courses from places like MIT, Stanford, Harvard, etc., all for free.

So every time I hear someone whining about wanting free university education, I always ask them how many online courses they’ve taken. How many books have they read?

I typically receive nothing more than a confused look in return.

But that’s the nature of entitlements: people feel that they should have everything provided for them without having to lift a finger to help themselves.

This mentality is becoming an epidemic in the West.

The Bolsheviks like to talk about education as an ‘investment’. And, to be fair, a more educated society is likely more productive, safer, and prosperous.

But to demand that the entire country invest in people who refuse to invest in themselves first – that’s absolutely ludicrous… and almost guarantees a BAD investment.

Personally I have a number of philanthropic activities and genuinely enjoy doing what I can to help people.

Not too long ago I helped out a wounded US Army veteran who had lost his leg in Afghanistan.

He had been abandoned by the Department of Veteran’s Affairs, and was trying to raise close to $100,000 to have a new surgical procedure performed overseas.

(It was a ridiculous story– the FDA had banned the procedure in the US because they had deemed it ‘unsafe’. Unlike being deployed to Afghanistan, which they apparently think is perfectly safe.)

This guy Joe didn’t wallow in self-pity. He was busting his ass, using every resource he could find to fix his own problem.

That’s exactly the type of person I like to invest in– because you know they won’t squander your investment. They’ll cherish it and grow from it.

I invested in Joe… and as a result of his surgery, he not only danced at his wedding and participated in a 5K, but the FDA has now approved the procedure in large part to his success.

That was a great investment.

Let’s be honest– a lot of people waste away in university. They skip classes, drink beer, and learn nothing.

Others work their butts off to learn and live as much as they can, and genuinely become better people as a result.

This notion of treating them all the same, and investing equally in each of them, is beyond insane.

As a final point, I do want to remind you about another investment in education that I make each year.

For the past ten years, I’ve been sponsoring a 5-day long entrepreneurship workshop in Lithuania.

It’s free to attend– I pay for all of it. Again, it’s an investment. But I only accept people who demonstrate that they’re working hard to help themselves first.

The application deadline is coming up this Sunday (and we already have tons of applications for the year).

But I wanted to send out one final reminder– if you or anyone you know is a bright, talented, self-starter, check out the camp’s website here.

For many of our attendees, it’s been absolutely life-changing.

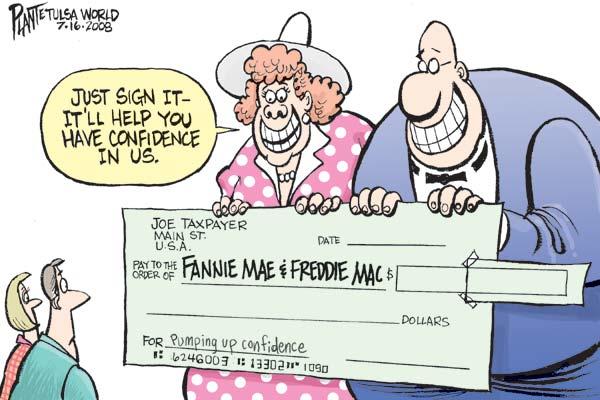

After months (or years) of on-again, off-again headlines, President Trump is expected to sign a memo on an overhaul of Fannie Mae and Freddie Mac this afternoon, kick-starting a lengthy process that could lead to the mortgage giants being freed from federal control.

The White House has been promising to release a plan for weeks, and its proposal would be the culmination of months of meetings between administration officials on what to do about Fannie and Freddie.

Bloomberg reports that while Treasury Secretary Steven Mnuchin has said it’s a priority to return the companies to the private market, such a dramatic shift probably won’t happen anytime soon.

In its memo, the White House sets out a broad set of recommendations for Treasury and HUD, such as increasing competition for Fannie and Freddie and protecting taxpayers from losses.

President Donald J. Trump Is Reforming the Housing Finance System to Help Americans Who Want to Buy a Home

“We’re lifting up forgotten communities, creating exciting new opportunities, and helping every American find their path to the American Dream – the dream of a great job, a safe home, and a better life for their children.”

President Donald J. Trump

REFORMING THE HOUSING FINANCE SYSTEM: The United States housing finance system is in need of reform to help Americans who want to buy a home.

Today, the President Donald J. Trump is signing a Presidential memorandum initiating overdue reform of the housing finance system.

During the financial crisis, Fannie Mae and Freddie Mac suffered significant losses and were bailed out by the Federal Government with billions of taxpayer dollars.

Fannie Mae and Freddie Mac have been in conservatorship since September 2008.

In the decade since the financial crisis, there has been no comprehensive reform of the housing finance system despite the need for it, leaving taxpayers exposed to future bailouts.

Fannie Mae and Freddie Mac have grown in size and scope and face no competition from the private sector.

The Department of Housing and Urban Development’s (HUD) housing programs are exposed to high levels of risk and rely on outdated business processes and systems.

PROMOTING COMPETITION AND PROTECTING TAXPAYERS: The Trump Administration will work to promote competition in the housing finance market and protect taxpayer dollars.

The President is directing relevant agencies to develop a reform plan for the housing finance system. These reforms will aim to:

End the conservatorship of Fannie Mae and Freddie Mac and improve regulatory oversight over them.

Promote competition in the housing finance market and create a system that encourages sustainable homeownership and protects taxpayers against bailouts.

The President is directing the Secretary of the Treasury and the Secretary of Housing and Urban Development to craft administrative and legislative options for housing finance reform.

Treasury will prepare a reform plan for Fannie Mae and Freddie Mac.

HUD will prepare a reform plan for the housing finance agencies it oversees.

The Presidential memorandum calls for reform plans to be submitted to the President for approval as soon as practicable.

Critically, the Administration wants to work with Congress to achieve comprehensive reform that improves our housing finance system.

HELPING PEOPLE ACHIEVE THE AMERICAN DREAM: These reforms will help more Americans fulfill their goal of buying a home.

President Trump is working to improve Americans’ access to sustainable home mortgages.

The Presidential memorandum aims to preserve the 30-year fixed-rate mortgage.

The Administration is committed to enabling Americans to access Federal housing programs that help finance the purchase of their first home.

Sustainable homeownership is the benchmark of success for comprehensive reforms to Government housing programs.

* * *

Because what Americans need is more debt and more leverage at a time when home prices are at record highs and rolling over.

Hedge funds that own Fannie and Freddie shares have long called on policy makers to let the companies build up their capital buffers and then be released from government control.

It’s unclear whether the White House would be willing to take such a significant step without first letting lawmakers take another stab at overhauling the companies.

But not everyone is excited about the recapitalizing Fannie Mae and Freddie Mac. Edward DeMarco, president of the Housing Policy Council, warned that releasing them from conservatorship would do nothing to fix the mortgage giants’ charters or alter their implied government guarantee:

“I’m not sure what is good about recap and release,” DeMarco, a former acting director of the Federal Housing Finance Agency, said in a phone interview.

DeMarco also noted that the government stepped in to save the companies in 2008, and they continue to operate with virtually no capital. On Tuesday, DeMarco told the Senate, during the first of two hearings on the housing finance system that “recap and release should not even be on the table.”

But shareholders in the firms were excitedly buying… once again.

Deciding the fate of Fannie and Freddie, which stand behind about $5 trillion of home loans, remains the biggest outstanding issue from the 2008 financial crisis.

via ZeroHedge News https://ift.tt/2HUo19j Tyler Durden

In February, Selene Saavedra Roman, a Texas-based flight attendant, took what should have been an uneventful work trip—a round-trip flight to Mexico and back. But when she landed in Houston, Immigration and Customs Enforcement (ICE) detained her and placed her in a detention center. She was released this past Friday after six weeks in custody.

In February, Selene Saavedra Roman, a Texas-based flight attendant, took what should have been an uneventful work trip—a round-trip flight to Mexico and back. But when she landed in Houston, Immigration and Customs Enforcement (ICE) detained her and placed her in a detention center. She was released this past Friday after six weeks in custody.

Controversy has struck the Southern Poverty Law Center, the formidable progressive law firm best known for tracking hate groups in the U.S. Co-founder Morris Dees, President Richard Cohen, and other top executives are exiting the organization amidst a staff uprising over alleged sexual and racial harassment in the work place.

Controversy has struck the Southern Poverty Law Center, the formidable progressive law firm best known for tracking hate groups in the U.S. Co-founder Morris Dees, President Richard Cohen, and other top executives are exiting the organization amidst a staff uprising over alleged sexual and racial harassment in the work place.

In September 2018, a Montana jury found Stanley Patrick Weber—formerly a pediatrician who worked with Indian Health Service (IHS)—guilty of four charges related to his abuse of young Native American boys under his care. He was sentenced to 18 years in prison in January, and is currently in a jail cell in South Dakota awaiting trial on yet more child abuse charges.

In September 2018, a Montana jury found Stanley Patrick Weber—formerly a pediatrician who worked with Indian Health Service (IHS)—guilty of four charges related to his abuse of young Native American boys under his care. He was sentenced to 18 years in prison in January, and is currently in a jail cell in South Dakota awaiting trial on yet more child abuse charges.