There has been a 180-degree reversal in market sentiment overnight, when at first US futures and global stocks ramped higher for much of the session following a SCMP report late on Thursday (US time) that US and China had agreed on a “truce” to avoid further tariffs, only for the WSJ to pour cold water on the report just before 6am EDT when it noted some of the key items the SCMP “missed” on purposes, namely that China had very specific demands to agree to a ceasefire, including the removal of the Huawei ban, something that Trump would almost certainly not agree to (and yet the Chinese publication made it seem like it was Beijing that was oh so generous, when in reality it was setting up Trump to be the guilty party when in reality it was China that once again held an untenable position going into the Trump-Xi talks).

In addition to the WSJ report, overnight China’s Commerce Ministry urged the US to immediately cancel sanctions on Chinese firms, including Huawei, and warned it would consider placing firms on a unreliable list if they implement discriminatory measures on Chinese entities, and firms that threaten the national security of China adding that the details are to be released soon.

In any case, the WSJ’s report immediately doused any positive market sentiment, with Bloomberg’s Heather Burke noting that “equities are waking up to the reality that this weekend’s meeting may not bring a shiny, happy trade solution”, which has sent S&P futures sharply lower, wiping out all overnight gains…

… and global markets lost much of their sparkle, with Europe turning sharply lower…

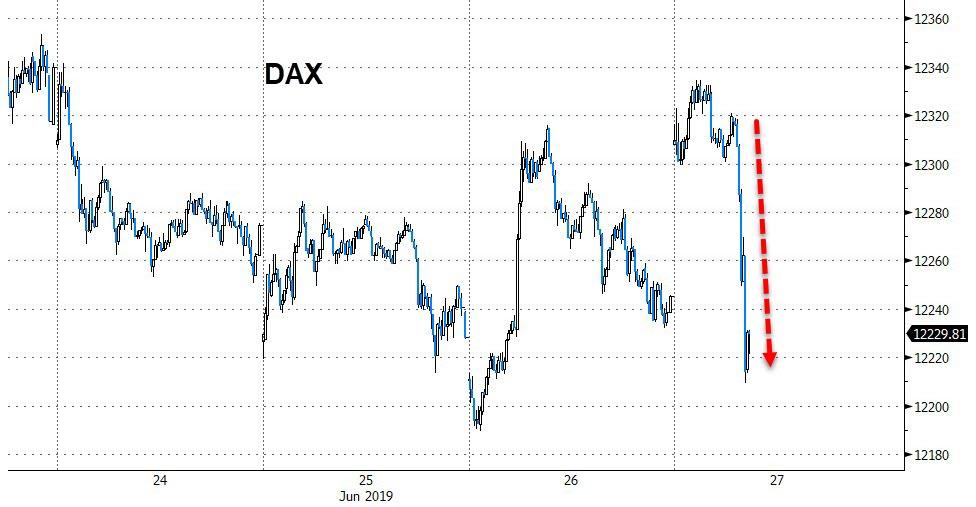

… led by the German Dax, which suffered a dramatic drop in minutes after the WSJ report refuted the SCMP.

“We should not expect too much from the Osaka meeting,” Christian Nolting, global chief investment officer at Deutsche Bank Wealth Management told Bloomberg TV. “To be overly optimistic could be on the wrong side for this weekend.”

Not helping US futures (or European stocks which slumped in the red) was the latest Boeing news, according to which the 737 MAX was prone to “uncontrolled nosedives” after new tests revealed a fresh software glitch, which in turn assured that the grounded Boeing planes would stay in parkling lots that much longer, and also sent Boeing stock plunging, which thanks to its biggest impact on the Dow has sent the “industrial” index into the red.

While both the US and Europe were scrambling to make sense of all the latest headlines, Asian stocks – which mostly closed ahead of the WSJ report – benefited from the earlier trade euphoria, and tech and material firms led Asian stocks higher. Almost all markets in the region rose, with Japan, Taiwan and Hong Kong leading gains. The Topix closed 1.2% higher, with SoftBank Group and Daikin Industries among the biggest boosts. Japan Display surged as much as 32% following a report that Apple is considering further financial support for the company. As noted above, Europe’s Stoxx 600 Index, which had gained led by retailers following H&M results, reversed.

Over in China, the Shanghai Composite Index rose 0.7%, driven by large banks and insurers, as investors cheered the probability of a China-U.S. trade deal (if only they had waited a few more hours, the cheering would have ended abruptly). Kweichow Moutai closed at a record high after climbing above the 1,000 yuan level for the first time on an intra-day basis. The outlier was Vietnam, whose stocks dropped 1.7%, bucking the regional trend, after Trump indicated that he might impose tariffs on the nation. The S&P BSE Sensex Index advanced 0.3%, rallying for a third day, with HDFC Bank and Housing Development Finance providing the biggest support to the gauge

In other assets, the dollar initially rose against the yen on hopes of a truce in U.S.-China trade war ahead of the Group of 20 summit, before losing traction amid quarter-end flows and the WSJ rejection. The euro rebounded on German regional inflation data even as a gauge of economic confidence in the region dropped to its lowest in nearly three years. Bunds dropped, Treasuries steadied and equities lost their bullish momentum as the London session progressed. European bonds were mixed after data showed economic confidence in the region declined more than forecast.

In other news overnight, Trump said he looks forward to speaking to India PM Modi about how India have placed very high tariffs on US for years and recently increased them further, while Trump added this is unacceptable and tariffs must be withdrawn. In response, Indian government sources noted that India’s tariffs on the US are well within the WTO bound rates.

And while the world is focused on the US-China meeting, President Trump will also meet with Russia President Putin on Friday at 1400 local time, ahead of Trump’s meeting with Chinese President Xi, which will take place on Saturday at 1130 local time in Osaka, according to a spokesman.

In other geopolitical news, Iran’s Parliament Speaker Larijani stated that the reaction from Tehran will be stronger in the event that the US repeats the mistake of violating Iran’s borders. Iran is still short of the nuclear deals limit on enriched uranium stocks, and are on course to reach the limit at the weekend., as according to diplomats citing IAEA data.

West Texas Intermediate crude declined 1% to $58.81 a barrel, the largest drop in more than a week. Gold dipped 0.2% to $1,405.64 an ounce.

Economic data include initial jobless claims, pending home sales and the third print of first-quarter GDP. Scheduled earnings include Nike, Accenture and Walgreens.

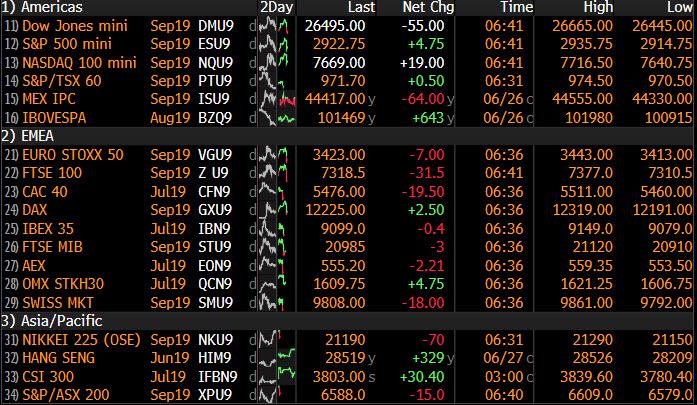

Market Snapshot

- S&P 500 futures up 0.2% to 2,923.00

- STOXX Europe 600 down 0.1% to 381.78

- MXAP up 0.9% to 160.15

- MXAPJ up 0.9% to 528.69

- Nikkei up 1.2% to 21,338.17

- Topix up 1.2% to 1,553.27

- Hang Seng Index up 1.4% to 28,621.42

- Shanghai Composite up 0.7% to 2,996.79

- Sensex up 0.3% to 39,709.40

- Australia S&P/ASX 200 up 0.4% to 6,666.31

- Kospi up 0.6% to 2,134.32

- German 10Y yield rose 1.3 bps to -0.29%

- Euro up 0.02% to $1.1371

- Brent Futures down 0.8% to $65.96/bbl

- Italian 10Y yield fell 1.8 bps to 1.779%

- Spanish 10Y yield rose 0.9 bps to 0.402%

- Brent Futures down 0.8% to $65.93/bbl

- Gold spot down 0.4% to $1,403.77

- U.S. Dollar Index up 0.03% to 96.24

Top overnight news from Bloomberg

- The first Democratic president debate in the U.S. exposed ideological fissures within the party over how to remake the economy, fix immigration and confront big companies — and whether the path to defeating Trump veers toward liberal solutions or hews to the middle

- Trump said India’s recent increase in tariffs on U.S. goods is “unacceptable” and should be withdrawn, ratcheting up tension before a planned meeting with Prime Minister Narendra Modi

- The European Central Bank will deliver a cut in September as policy makers step up their efforts to revive the euro-zone economy, economists predict

- Several Huawei Technologies Co. employees have collaborated with Chinese armed forces personnel on research projects, indicating closer ties to the country’s military than previously acknowledged by the smartphone and networking powerhouse

- Turkey is preparing a bill that would boost the Treasury’s cash flow through the use of central bank lira reserves, just weeks after policy makers refrained from proposing a similar measure for fear it could roil financial markets, Bloomberg HT reported on Thursday. The lira fell.

Asian equity markets traded higher after the region shrugged off the uninspiring lead from Wall St where participants were tentative heading into the G20 and amid mixed US-China trade commentary. ASX 200 (+0.4%) was positive in which outperformance in the energy sector just about kept the index afloat following the recent bullish oil inventory data, while Nikkei 225 (+1.2%) was underpinned by the JPY-risk dynamic and with Japan Display the front runner in Tokyo after reports that Apple will infuse USD 100mln into the Co. and also raise its orders. Elsewhere, Hang Seng (+1.4%) and Shanghai Comp. (+0.7%) inspired the turnaround in the region on several factors including the State Council’s recent announcement of measures to cut financing costs for smaller firms and with Industrial Profits back in the black, while the trade-related headlines were more constructive in which SCMP noted the US and China agreed a tentative truce before the G20 summit and that US President Trump’s decision to delay additional tariffs was Chinese President Xi’s price for holding this week’s meeting with him. Finally, 10yr JGBs were lower with demand dampened by the improved risk sentiment and after similar weakness in T-notes, but with downside limited amid a mixed 2yr auction in which most metrics improved despite a weaker bid to cover.

Top Asian News

- Trump Asks India to Reverse ‘Unacceptable’ Tariffs on U.S. Goods

- Trade-War Winner Vietnam Finds Itself in Trump’s Crosshairs

- Singapore to Review 2019 Growth Forecasts as Trade War Spreads

European equities have given up earlier gains [Eurostoxx 50 -0.3%] amid reports that Chinese President Xi is intending on presenting US President Trump with a set of terms that the US needs to meet before Beijing will be prepared to settle the trade dispute. Beijing is insisting that the U.S. removes its ban on the sale of U.S. technology to Huawei, according to a Chinese Official (which was noted earlier in the session by MOFCOM) whilst also asking for the removal of all punitive tariffs and for the US to drop its efforts to get China to buy more U.S. goods. Equity futures reacted negatively to the report as the conditions from China signal the gulf in demands between the two sides ahead of this weekend’s showdown. Germany’s DAX (-0.1%) is faring slightly better than its peers as the index heavyweight Bayer (+8.0%) surges amid reports of support from Elliott as the Co. reviews its legal strategy on weed killers. Sectors are mixed with some underperformance experienced in defensive sectors. In terms of individual movers, H&M (+9.3%) shares spiked higher at the open following results in which Q2 sales rose 11%. Meanwhile, CHR Hansen (-12.2%) fell to the foot of the Stoxx 600 after cutting its revenue guidance.

Top European News

- H&M Surges as Retailer Shows Early Progress Toward Turnaround

- European Car Market Forecast to Shrink 1%, Acea Says in Revision

- Johnson Zigzags Again, Says No-Deal Exit Unlikely: Brexit Update

- Macron’s G-20 Climate Threat Melts Away Just Like the Ice Caps

In FX, there has not been much deviation from established or recent ranges in major pairings, and the narrow DXY band (96.390-156) illustrates the subdued and cautious tone ahead of the eagerly awaited Summit in Osaka and US-China trade showdown. Indeed, there is still little sign of strong Dollar selling for month, quarter and half year end portfolio balancing purposes, although the Fed has intervened to an extent via Powell and Bullard’s efforts to manage dovish market expectations.

- AUD/NZD – The Aussie and Kiwi are still riding high on improved risk sentiment following some signs that relations between Washington and Beijing have cooled, albeit temporarily and conditionally pending the outcome of aforementioned G20 meeting where Presidents Trump and Xi will attempt to resolve issues that led to a breakdown in negotiations. Meanwhile, a welcome rebound in Chinese industrial profits has also lifted the mood down under, with Aud/Usd and Nzd/Usd both within a whisker of big figures at 0.7000 and 0.6700 respectively, and the latter not unduly ruffled by a deterioration in ANZ’s NZ activity outlook overnight.

- GBP – The Pound is looking perky again as Cable reclaims the 1.2700 handle that has been tested several times this week, but proved unsustainable. Encouraging comments from Japan on the prospect of a post-Brexit trade deal with the UK along TPP lines may be supporting Sterling that is also firmer vs the Euro (cross pivoting 0.8950), but a hefty 1bn option expiry at 1.2700 in Cable could still cap that pair.

- EUR/CAD/CHF/JPY/NOK – All narrowly mixed vs the Greenback and more confined, with the single currency remaining in a circa 1.1350-80 band and holding above key technical support in the form of the 200 DMA (1.1344) with the aid of firm-to-relatively frothy German state inflation data that puts an upside bias on the pan print consensus towards 1.6% from 1.4% and steady from the previous month. Conversely, the Loonie has lost some momentum ahead of 1.3100 due to a dip in oil prices, while the Franc pivots 0.9800 and Yen straddles 108.00 after dovish/downbeat remarks from BoJ’s Wakatabe. Elsewhere, the Norwegian Krona has retreated in wake of weaker than expected retail sales and the recoil in crude, with Eur/Nok back up around 9.6900.

- EM – Bucking the generally firmer regional trend, reports that Turkey is looking to syphon CBRT reserves have resurfaced and undermined the Lira alongside headlines about changes to tax policy, with Usd/Try up over 5.7900 at one stage.

In commodities, WTI and Brent futures are consolidating following this week’s geopolitics-inspired gains which were exacerbated by declining US stockpiles. WTI futures hovers around the USD 59/bbl level ahead of a cluster of DMA (50 DMA – 59.25, 100 DMA – 59.41 and 200 DMA 59.48) while its Brent counterpart trades just above the USD 65/bbl mark. On the OPEC+ front, Russia’s Energy Minister sounded somewhat upbeat in regard to reaching a consensus with Russia’s OPEC counterparts at next week’s meeting, adding that he will be meeting Saudi’s Energy Minister Al-Falih at the G20 this weekend. The energy producers will be heading into the meeting with full knowledge of the fallout from US-China talks. Market consensus is that a rollover of the current deal is the likely outlook (also mentioned by the Iraqi Oil Minister), although it is still not clear if any revisions will be made (Iraqi Oil Minister touted deeper cuts). Elsewhere, the gold rally has fizzled out as the DXY remains buoyed above 92.00, with the yellow metal now in close proximity to USD 1400/oz (vs. recent high of USD 1439/oz). Meanwhile, copper prices are little changed on the day ahead of the risk-packed weekend, with prices hovering just above USD 2.7/lb ahead of its 50 DMA at 2.73/lb. Finally, Dalian Iron ore has resumed its rally amid renewed concerns of tightening supply whilst Rebar steel continued its upwards trajectory amid pollution-related production curbs in China.

US Event Calendar

- 8:30am: GDP Annualized QoQ, est. 3.2%, prior 3.1%

- 8:30am: Initial Jobless Claims, est. 220,000, prior 216,000;Continuing Claims, est. 1.67m, prior 1.66m

- 9:45am: Bloomberg Consumer Comfort, prior 61.8

- 10am: Pending Home Sales MoM, est. 1.0%, prior -1.5%; YoY, est. 0.4%, prior 0.4%

- 11am: Kansas City Fed Manf. Activity, est. 1, prior 4

DB’s Jim Reid concludes the overnight wrap

As we await the G-20 none of us are any closer to knowing what the aftermath of the Trump/Xi meeting will be. If we weren’t confused enough, we had to try to decipher the following comments from Mr Trump yesterday, “my plan B’s maybe my plan A, my plan B is that if we don’t make a deal I will tariff, and maybe not at 25%, but maybe at 10%”. This certainly required a few re-reads but the ultimate takeaway from his interview was that the underlying threat of additional tariffs was still very much in place even if there were no greater insights into which way the upcoming talks will go. Trump also continued his now-customary attacks on the Fed and Chair Powell, saying he “should never have raised the rates to the level that he raised it” and that “we should have Draghi instead of our Fed person.”

Earlier in the day there appeared to be a bit of excitement about slightly more upbeat trade comments from Trump’s Treasury Secretary Mnuchin suggesting that a trade deal was 90% complete. However, after some initial giddiness, the market reappraised the remarks to appreciate that Mnuchin said the two sides “were” 90% of the way there. In other words, Mnuchin was referencing where talks were before they broke down. His remarks were live direct to CNBC immediately after I was a guest speaker in the London studio. Indeed I couldn’t help think that I was a filler as the studio was a whirl of activity, stress, and anticipation that they had Mnuchin on live at any moment. Earpieces were a constant stream of noise. Indeed I was told I could be booted off if he came through early. So I was the support act to the main event.

Anyway, the end result for equities was a small retreat for the S&P 500 (-0.12%) and DOW (-0.04%) after sliding steadily throughout the session, notably below the +0.58% and +1.18% peaks that futures hit after the misinterpreted Mnuchin comments. The NASDAQ (+0.32%) posted bigger gains, but the real standout was the Semi-Conductor Index (+3.21%). Two notable laggards were Google (-0.60%) and Facebook (-0.62%), possibly as a result of President Trump’s statement that ” we should be suing Google and Facebook.” European markets faded from earlier highs with the STOXX 600 ending -0.31% while in rates Treasuries continued their post Bullard and Powell move higher with 10y yields up +6.4bps (a further +1bps this morning). At the short end 2y yields rose ‘only’ +3.9bps (+1.7bps this morning) which caused the curve to steepen +2.66bps to 27.5bps (26.8bps this morning).

Breakevens assisted the move higher for rates with oil rallying hard again. WTI closed up +2.42% and has now posted 5 daily moves of at least 2% up or down in the last 11 sessions. Brent also rose +1.84% and is now +10.5% off the recent lows. The spike yesterday appeared to be triggered by the latest EIA inventories data, which showed a 12.8 million barrel drawdown in inventories, the biggest since 2016 and 5th biggest on record going back to 1982. There have been some concerns lately about oversupply, so the initial strong start to the summer driving season sends a bullish signal for oil prices.

Bond markets were a bit less exciting in Europe where 10y Bund yields in particular edged up +2.9bps, similar to the rest of the continent with the exception of BTPs (-1.9bps). Part of that outperformance may well have reflected the Reuters story which hit just after midday suggesting that the ECB was looking at ways to circumvent the issuer limit constraint, potentially by stripping central banks of their voting rights through a clause known as “disenfranchisement”. Clearly there are policy and legal arguments to both sides of this and therefore it’s unlikely to be a decision that is made overnight. There has been more chatter on it recently, especially since Draghi signalled his potential willingness to change the program’s parameters, so it’s a topic worth following closely.

Gold prices slipped -0.99%, their first decline after six straight sessions of gains, though they remain near recent highs. We had highlighted earlier this week how gold and bitcoin were both rising in unison, perhaps as speculators retreated from fiat currencies ahead of expected rate cuts, but that correlation snapped yesterday. While gold fell, bitcoin prices rocketed up another +21.87% at one point to $13,852 before collapsing most of the way back into the close but then spiking again to be +12.03% higher. In Asia it’s gone through a sizeable range again. It feels to H2 2017 all over again.

Elsewhere in Asia this morning markets are heading higher on optimism that a temporary truce might be the most likely outcome of the Trump/Xi meeting at G20. The Nikkei (+0.98%), Hang Seng (+1.13%), Shanghai Comp (+0.89%) and Kospi (+0.83%) are all up c. 1%. The Japanese yen is down -0.287% this morning Elsewhere, futures on the S&P 500 are up +0.28%.

We got confirmation overnight that the Trump/Xi meeting will start at 11:30am (Japan time) on Saturday, with a 90mins slot provided after which Trump is scheduled to meet Turkish President Erdogan. Meanwhile, the Washington Post has reported that President Trump’s top China critic, senior adviser Peter Navarro, is also part of the US delegation visiting G20. He was a last minute addition to the team which includes the U.S. Trade Representative Robert E. Lighthizer, Treasury Secretary Steven Mnuchin and Commerce Secretary Wilbur Ross. Navarro’s inclusion reduces the possibility of any quick deal between the presidents, which was never the base case anyway. Meanwhile, Reuters has reported that Lighthizer and Mnuchin are expected to meet with China’s Liu He ahead of the meeting between Trump and Xi. Staying with trade, Bloomberg reported (citing EU officials) that if talks at the G20 meeting and in the coming weeks fail to head off US tariffs on Europe’s car industry, then they are confident that their response will be sharp enough to “hit the president where it hurts”.

Back to yesterday now. As for the data, in the US headline durable goods orders slumped a lot more than expected in May based on the preliminary reading. The headline was -1.3% mom compared to expectations for -0.3%. However the ex-transportation number was a lot more positive (+0.3% mom vs. +0.1% expected) while core capex orders also rose more than expected (+0.4% mom vs. +0.1% expected). Elsewhere, the advance goods trade deficit widened to $74.5bn in May and more than expected to a five-month high. Finally wholesale inventories rose +0.4% mom in May and a little less than expected. In aggregate, the data should signal a modest increase in second quarter growth expectations.

In the UK, Bank of England Governor Carney generated some headlines when testifying to a Parliamentary committee. On the policy front, he emphasised that Brexit is the key risk, with “the degree of uncertainty high” and was sanguine about the disconnect between markets and the BoE’s own forecasts. Markets are resistant to pricing hikes, he said because investors ascribe “some possibility to no deal,” in which case there would be easing. Carney seemed to ratify this view, but cautioned that “we would do what we could to support the transition to no deal, but there’s no guarantee on that.” Relatedly, he pushed back on the view – recently espoused by Boris Johnson among others – that the UK could retreat to the relationship under article 24 of the GATT, which would maintain existing rules while negotiations continue. Carney said such an arrangement would need to be multilaterally agreed and the EU has showed no signs of interest. Boris Johnson said last night that he thought the chances of a no deal Brexit were a “million to one” but that he was prepared for one. He is going to have some tough times squaring this if and when he gets elected!

Across the pond, the Fedspeak calendar was light, with the only major remarks coming from San Francisco Fed President Mary Daly, who leans toward to dovish side of the committee but is relatively centrist. She said that “the labour market is strong. I believe it’s tighter than it’s been in a while, but there might be more room to run.” She also said she is “uncomfortable with not only the level of inflation currently but the direction.” So her comments would be consistent with her support for a July cut, but didn’t really offer any new info.

Looking at the day ahead, this morning we’re due to get June confidence indicators for the Euro Area before the preliminary June CPI report is out in Germany. Also out this afternoon in the US is the third and final Q1 GDP reading (which is expected to be revised up one-tenth to +3.2%) and Q1 core PCE, jobless claims, May pending home sales and the June Kansas Fed manufacturing survey. Elsewhere, the ECB’s Nowotny is due to speak this evening while the Fed will release part two of its bank stress test results.

via ZeroHedge News https://ift.tt/31SEHWd Tyler Durden