This is one of those morning where bad news is good news for stocks while good news is bad news for bonds… or in other words, any news is good for stocks.

Despite fresh all time highs in US equities, where the S&P is set to open above 3,000 after closing at 2,999.9 on Thursday, world shares came within a whisker of posting their first weekly loss since May on Friday and the dollar was down for a third day, even as a stronger-than-expected U.S. inflation print failed to shake bets on Federal Reserve interest rate cuts.

With U.S. equity futures rising further after the S&P 500 Index closed Thursday at a record high on hopes the global economy will slow even more, forcing the Fed to cut by 50bps and more thereafter, European stocks ticked higher in early trade following the latest dismal trade data out of Asia, with gains in auto and chemical shares pushing the benchmark Stoxx 600 toward its first increase this week.

Earlier in the session, the MSCI index of Asia-Pacific shares outside Japan was down 0.1%, with the regional benchmark set for its first weekly decline since May, as investors continued to monitor trade tensions between the U.S. and China. Markets in the region were mixed, with China, Hong Kong and South Korea advancing and Indonesia, Australia and Japan dropping. Financial firms gained while communications and technology companies retreated. The Topix slipped 0.2%, with Bandai Namco, Keyence and Fanuc among the biggest drags. South Korea called for an international probe into Japanese claims that it allowed the export of sensitive materials to North Korea, as disputes escalated between Seoul and Tokyo. The Kospi gauge closed 0.3% higher. The Shanghai Composite Index rose 0.4%, supported by large insurers and banks. Beijing said trade talks with the U.S. will restart, while stressing its core concerns. The S&P BSE Sensex Index was little changed. After recent elections, India is positioned to overhaul a regulatory environment that could deter foreign investments, U.S. Commerce Secretary Wilbur Ross said.

As reported earlier, following a dismal GDP print out of Singapore, where the economy unexpectedly contracted by 3.4% with consensus expecting an increase…

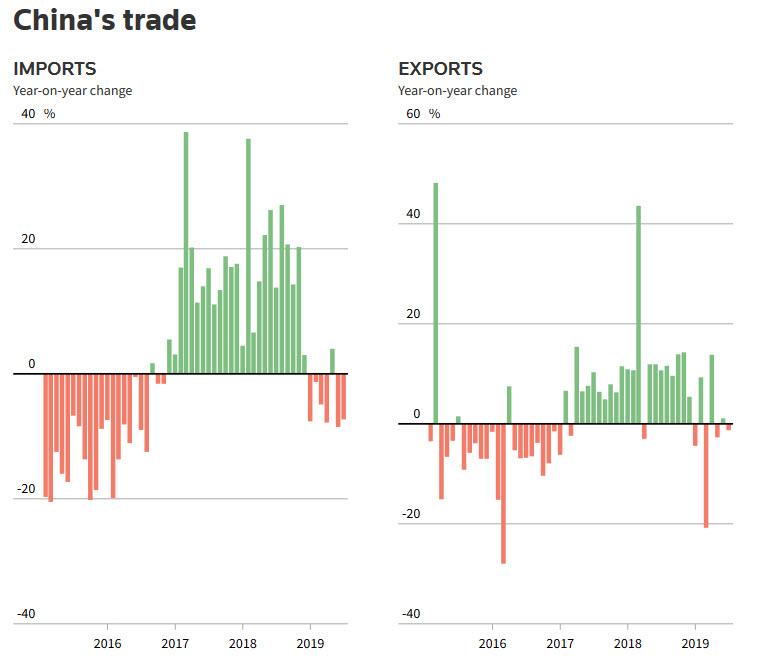

… investor attention then turned to China, whose export growth slowed in June and imports shrank more than expected: specifically, exports fell 1.3% in June from a year ago and imports shrank a more-than-expected 7.3%. On top of that its trade surplus with the United States, a major source of friction with its biggest trading partner, rose to $29.92 billion in June from $26.9 billion in May.

The latest poor trade data comes after a string of disappointing economic reports from around the globe, which showed that the global economy suffered from a protracted U.S.-China trade war that forced major central banks to take a more accommodative stance, which in turn has pushed US stocks to fresh all time highs. China is also due to release second-quarter GDP figures on Monday which are expected to show the world’s second-largest economy slowing to its weakest pace in at least 27 years.

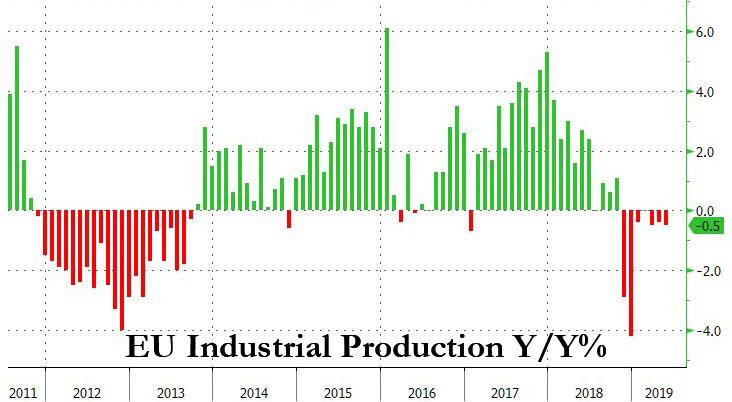

There was a modest silver lining in the latest industrial production figures for the euro zone, which contracted -0.5%, stronger than the -1.6% expected, even if this was the 3rd consecutive negative print leaving economists split on whether the numbers will reveal any meaningful signs of recovery, and whether it would have any impact on the ECB’s dovish state of mind, as consensus now expected a 0.10% rate cut and return of QE.

European Central Bank policymakers gathering last month agreed on the need to be ready to provide more stimulus to the euro zone economy in an environment of “heightened uncertainty”, official minutes of the meeting showed on Thursday.

In FX, the dollar was lower for a third straight day, down 0.1%. A stronger-than-expected inflation print failed to shake convictions that the Federal Reserve will start cutting interest rates at a policy meeting later this month. On Thursday, the core CPI index rose 0.3% in June, the largest increase since January 2018, data on Thursday showed. The reading pushed U.S. Treasury yields higher, but money markets still indicated one rate cut at the end of July and a cumulative 64 basis points in cuts by the end of 2019. The lira weakened after Turkey said it started receiving parts of a Russian-made missile defense system, a move opposed by the U.S.

Comments by Chicago Fed President Charles Evans scheduled later on Friday and New York Fed President John Williams on Monday will provide a chance to gauge how dovish the central bank is, said Masafumi Yamamoto, chief forex strategist at Mizuho Securities. “If these Fed officials are not as dovish as Powell, and if the New York Fed’s manufacturing survey on Monday proves stronger than forecast, they could show that the dollar weakening in response to Powell’s congressional testimony was overdone.” Elsewhere in currencies, the euro got a boost from a selloff in the German bond market, rising 0.1% to $1.1270.

In rates, the recent rout continued as European government bonds extended their declines, heading for the worst week since at least October, after the industrial output print beat. German government bonds were set for their biggest weekly selloff in nearly one-and-a-half years, as yields jumped from -0.40% to -0.24% and the French 10Y yield has risen from -0.14% to +0.06%, as signs of economic strength in the United States and parts of Europe suggested fears of a downturn may be overdone.

Meanwhile, in the latest blow to the US-China trade ceasefire, President Donald Trump complained that China hasn’t increased its purchases of American farm products, a promise he said he had secured at his G-20 meeting with the country’s president Xi Jinping last month. That did not stop Trump’s trade advisor Peter Navarro to lie to the world, declaring that US-China trade talks are going great.

In commodities, Elsewhere, WTI oil headed for its sixth advance in seven sessions and hovered near six-week highs as operators in the Gulf of Mexico braced for Tropical Storm Barry.

Global benchmark Brent crude gained 0.77% to $67.03 per barrel. U.S. West Texas Intermediate (WTI) crude was up 0.68% to $60.57 a barrel. Gold prices regained their shine thanks to renewed trade worries and rate cut expectations. Spot gold last traded up 0.5% at $1,410.99 per ounce. Cryptos rose after Trump’s trash talking tweet.

It’s a quiet calendar, with the only expected data coming from US PPIs. MTY Food Group is reporting earnings

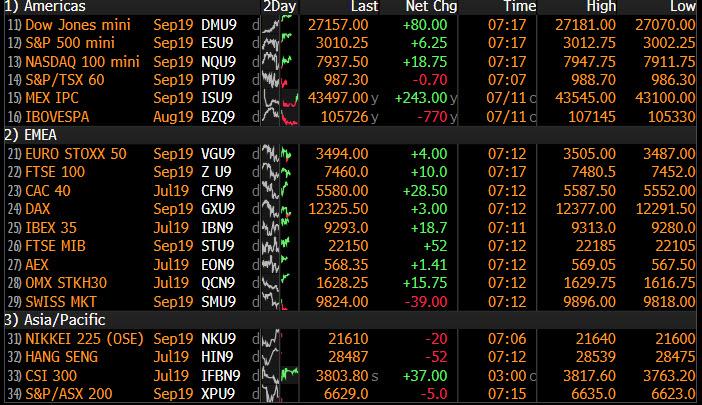

Market Snapshot

- S&P 500 futures up 0.2% to 3,011.00

- STOXX Europe 600 up 0.2% to 387.43

- MXAP down 0.09% to 160.16

- MXAPJ down 0.1% to 525.49

- Nikkei up 0.2% to 21,685.90

- Topix down 0.2% to 1,576.31

- Hang Seng Index up 0.1% to 28,471.62

- Shanghai Composite up 0.4% to 2,930.55

- Sensex up 0.3% to 38,949.50

- Australia S&P/ASX 200 down 0.3% to 6,696.55

- Kospi up 0.3% to 2,086.66

- German 10Y yield rose 0.4 bps to -0.221%

- Euro up 0.09% to $1.1264

- Italian 10Y yield fell 3.6 bps to 1.345%

- Spanish 10Y yield rose 6.0 bps to 0.536%

- Brent futures up 1.1% to $67.22/bbl

- Gold spot up 0.5% to $1,410.31

- U.S. Dollar Index down 0.1% to 96.94

Top Overnight News from Bloomberg

- China’s export growth slowed in June and imports shrank more than expected, as the continuing trade war with the U.S. and a global slowdown hurt trade

- Deeply negative yields on Europe’s highest-rated bonds are driving investors seeking the right mix of returns and safety into assets such as interest-rate swaps

- Turkey says it received on Friday the first major cargo of a Russian missile-defense system whose purchase has drawn the threat of U.S. sanctions over its potential to undermine NATO’s military capabilities. The lira weakened

- Britain raised the threat level to the highest possible for ships operating in the Persian Gulf as tensions escalate in a region accounting for a third of seaborne petroleum trade

- Europe’s economy got a shot in the arm on Friday with a report showing the biggest jump in industrial production in four months. Output jumped 0.9% from the previous month, beating the 0.2% median estimate of economists

- Federal Reserve Chairman Jerome Powell suggested that the central bank has room to ease monetary policy as the tie between the inflation and jobless rates has broken down

- Donald Trump complained that China hasn’t increased its purchases of American farm products, a promise he said he had secured at a meeting with the country’s president, Xi Jinping, at the Group of 20 summit last month

- German Economy Minister Peter Altmaier sees a 50% chance of the European Union striking a trade agreement on industrial goods with the U.S., possibly this year

- S&P Global Ratings is the first foreign credit-rating company to rate domestic Chinese bonds after awarding its top score to a unit of the country’s largest bank

- The Trump administration will hold off on imposing sanctions against Iranian Foreign Minister Javad Zarif, two people familiar with the matter said on Thursday evening

- Japan’s Government Pension Investment Fund bought about 1.3 trillion yen ($12 billion) of foreign bonds on a currency- hedged basis during the fiscal year ended March 31, according to its annual report. This is the first time it has bought debt overseas with currency hedging already in place, according to a person with knowledge of the matter

- China may remain the “primary threat” to the U.S. military for as long as a century after learning how to fight more effectively by watching American wars in the Middle East, President Donald Trump’s nominee to lead the Joint Chiefs of Staff said

Asian equity markets were somewhat cautious as the region awaited the latest Chinese trade data and following a mixed performance on Wall St. where markets were tentative amid a plethora of Fed speakers, although the DJIA outperformed and rose above the previously uncharted 27K level. ASX 200 (-0.3%) was dragged lower by most mining-related sectors but with downside stemmed by resilience in the largest-weighted financials industry and strength in energy after news Santos is considering a takeover of rival Oil Search, while Nikkei 225 (+0.2%) mirrored an indecisive currency with index giant Fast Retailing the outperformer after it posted 9-month profit growth. Hang Seng (+0.2%) and Shanghai Comp. (+0.4%) were choppy ahead of the Chinese trade figures and after PBoC inaction resulted to a net weekly drain of CNY 220bln, although Chinese press reports continued to suggest potential for lower rates in China and more room for easing. Finally, 10yr JGBs followed suit to the weakness of their counterparts in US where the curve bear steepened in the aftermath of firmer than expected CPI data, while the tentative risk tone and BoJ presence for JPY 940bln of JGBs also failed to provide support for prices.

Top Asian News

- JPMorgan’s $50 Billion Fund Halves EM Holdings on Trade Risk

- Jokowi Vows Sweeping Indonesia Reforms: ‘I Have Nothing to Lose’

- China Trade Slows, Imports From U.S. Slump as Tariffs Take Toll

- AB InBev Asia Unit Is Said to Struggle to Price Hong Kong IPO

Major European Indices are little changed, and haven’t substantially deviated from their mildly positive opening levels [Euro Stoxx 50 +0.1%]. The Dax (U/C) was waylaid in pre-market trade where the future was initially higher by around 0.4%, however, following Daimler (-1.3) stating that their Q2 EBIT is to be significantly below expectations, at EUR -1.6bln vs. Prev. EUR +2.6bln, futures then indicated a lower open for the bourse. The profit warning from Daimler did impact the opening calls and initial cash levels for its major counterparts though the likes of Volkswagen (1.0%) and BMW (U/C) have largely recovered. Other notable movers this morning include, Ab InBev (-2.0%) who are subdued following a sources report that Budweiser’s Hong Kong unit will not price its IPO before Friday; follows on from reports earlier in the week that the pricing is to be at the lower end of the indicative range. A beat on EBIT Exp. has pushed EMS-Chemie (+6.0%) to the top of the Stoxx 600, with Swatch (+3.6%) just below this after being upgraded to buy at Goldman Sachs. Finally, and perhaps this mornings largest mover is Thomas Cook (-44.0%) after the Co. announced they are seeking a GBP 750mln injection from the Fosun Group, which would give the group a controlling stake in the tour operator and a minority interest within the airline its self; with the majority of the Co’s GBP 1.4bln in debt to be written off and converted into shares diluting the value for existing shareholders, hence the overwhelmingly negative reaction to this news.

Top European News

- Thomas Cook Seeks $940 Million Rescue Led by Investor Fosun

- European Industry Shows Signs of Life as Output Beats Estimates

- Swedish Bank SEB Tops Estimates as Rivals Mired in Scandal

- Russia’s 22% Returns Leave Sanctions-Wary Investors In the Dust

In FX, we start with AUD/NZD/CAD/CHF – The non-US Dollars continue to prosper at the expense of their major counterpart, with the Aussie back on the 0.7000 handle, albeit just, Kiwi inching closer towards 0.6700 and Loonie not far from 1.3000 where big barriers reside having breached last week’s pre-NFP and prior 2019 peak of 1.3038. Usd/Cad continues to decline on Fed/BoC policy divergence as the former seems almost certain to deliver an insurance cut at the end of the month, while the latter is sticking to a neutral stance. Similarly, Aud/Usd is realigning after the RBA’s consecutive 25 bp OCR reduction and shift to wait-and-see mode, while Nzd/Usd appears to be biding time ahead of next week’s Q2 NZ inflation data that will be a key driver for the RBNZ. Elsewhere, the Franc is also gaining further ground vs the Buck after surpassing 0.9900, but also outperforming against the Euro with the cross eyeing 1.1100 following a break below 1.1150.

- GBP/JPY/EUR/SEK/NOK – All moderately firmer, as Cable holds above 1.2500 and the Yen pivots 108.50 in close proximity to decent expiry options (1.2 bn between 108.50-40). However, the Pound has drifted back down from recovery highs closer to 1.2600 amidst dovish comments from BoE’s Vlieghe in the event of a no deal Brexit when he believes rates could be set near zero, while Usd/Jpy remains reluctant to venture too far under 108.00. By the same token, the single currency is still confined below 1.1300 amidst an array of expiries spanning 1.1250 (1 bn), 1.1270-75 (1.1 bn) and the big figure (1.1 bn), with no real boost from better than expected Eurozone ip data even though EGB yields have rebounded further in response. Hence, Eur/Sek has now slipped through 10.5500 and Eur/Nok is straddling 9.6100, though the Swedish Krona has been underpinned to an extent by Riksbank minutes retaining guidance for a repo hike around the turn of the year and its Norwegian neighbour is underpinned by firm oil prices.

- EM – Although the Greenback is off lows and the DXY is probing 97.000+ levels again, the latest leg up in Usd/Try is mainly due to heightened US/EU-Turkey angst and anticipation that tougher sanctions are on the way. Note also, the Lira’s lurch towards 5.7150 at one stage also came amidst reports that the first batch of S-400 missile system components have arrived from Russia.

In commodities, WTI and Brent are in positive territory and adding to the weeks gains of around USD 4.0/bbl on the back of significant drawdowns in weekly crude data, ongoing geopolitical tensions including the seizure of Iran’s Grace 1 which is carrying 2.1mln/bbl of light crude and the Gulf of Mexico storm. On the latter, the NHC have most recently stated that Storm Barry may become a hurricane by Friday night or early Saturday, in terms of production, reports are indicating that around 53% of the Gulf’s production is shut; the concern/focus may switch more towards refineries as the storm approaches land with Louisiana representing 20% of the US’ refinery capacity. This morning saw the release of the final monthly oil market report, where the IEA maintained their 2019 global oil demand growth estimate at 1.2mln BPD; for reference, earlier in the week OPEC also maintained their forecast at 1.14mln BPD while EIA cut theirs to 1.07mln BPD. Gold (+0.1%) Is modestly firmer this morning benefiting from the dollars ongoing weakness. However, the metal has drifted back towards the USD 1400/oz mark and if this mornings relatively rangebound trade continues is set to finish the week within a few dollars an ounce of where it started; and indeed in a similar area to the last two weeks closing figures. Elsewhere, copper prices have continued to trade sideways post the key Chinese data, which had little impact on the metal.

US Event Calendar

- 8:30am: PPI Final Demand MoM, est. 0.0%, prior 0.1%; PPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%

- 8:30am: PPI Final Demand YoY, est. 1.6%, prior 1.8%; PPI Ex Food and Energy YoY, est. 2.1%, prior 2.3%

- 9:45am: Bloomberg July United States Economic Survey

- 10am: Fed’s Evans to Speak on Trade and Economy in Chicago

DB’s Jim Reid concludes the overnight wrap

Just to make sure everyone is up to speed, a final reminder about DB Research at the top today. After some difficult decisions were announced last weekend about the firm’s direction, we want to reiterate that DB Research will remain at the forefront of the firm with strong backing from senior management. As well as FIC, Macro, QIS, Data Science, and Thematic research, DB is still committed to providing extensive and top-quality Company Research coverage in Europe and the US. DB will combine Equity Research and Research Sales into a newly formed Company Research and Advisory Group to strengthen ongoing connectivity with institutional clients. So if you are a consumer of any of our research and have any questions, please let me know and we can try to answer them.

One publication we will continue to publish is our flagship Thematic magazine “Konzept” where we take a big picture theme and use our expertise across research to delve deeper into the relevant issue. The latest edition was out on Wednesday and was entitled “How 5G will change your life” ( link ). In this we look behind the hype of the 5G rollout and examine the unexpected impact on everything from smartphones to factories to politics and Smart Cities. Although to balance things out, do we have a data addiction crisis? We highlight in the report that a third of millennials spend two hours or more each work day looking at their phones for personal activities, according to some reports. Is this part of our current global productivity problem?

Not even 4G could come to my rescue yesterday as all day meetings stopped me seeing a monumentally destructive performance by England’s cricketers to beat Australia in the semi-final of the World Cup. To the uninitiated (most of our global readers), the final is on Sunday against New Zealand at home at Lords in London. So how will I be watching this weekend’s once-in-a-lifetime event? In the ground? In a pub with friends? On the sofa with the children bringing me regular refreshments? No. I’ll be out of the loop on a plane to Asia. What awful planning on my behalf.

Outside of a rare England semi-final win in any sport, yesterday’s main event was the slightly higher-than-expected US CPI report, which surely reduces the chances of a 50bps cut at the end of the month even if market pricing didn’t change too much. The market still implies around 31bps of cuts this month, or around a 17.5% chance for a 50bps cut. That’s just slightly lower than where we were after Powell’s statement was initially released on Tuesday. 10-year yields rose sharply though as we’ll discuss below. Despite the pretty calm Fed pricing, we actually got a slew of new information yesterday.

Apart from day two of Powell’s congressional testimony, in which he largely reiterated his remarks from Tuesday, we also heard from FOMC members Barkin, Bostic, Williams, and Quarles. The first two gave hawkish comments, with Barkin saying “I don’t see the current levels of inflation or inflation expectations as a trigger for additional accommodation” and Bostic responding affirmatively to a question about whether he opposes a rate cut. While hawkish, this could perversely raise the odds for a cut later this month. By illustrating that Barkin and Bostic, two non-voters, are not in favor of easing, it actually raises the odds that voting members are in the pro-cut camp. One of those is likely NY Fed President Williams, who said that “the arguments for adding policy accommodation have strengthened.” Quarles, who focuses more on financial regulation, largely reiterated the comments from Powell.

Through all that noise, ten-year treasury yields grinded higher throughout the session, getting two separate boosts, first from the inflation report and subsequently from a soft 30-year auction. Yields rose +9.9bps from their morning lows, with around +3.2bps happening in the minutes after the CPI data and another +2.8bps immediately following the weak auction and ultimately closed +7.5bps on the day at 2.136%. The 30-year auction, which was held after Europe had already closed up for the day, had a notably largely large tail. The $16bn reopening ended up yielding more than 2bps higher than the when-issued trading level.

At our big FIC forum two weeks ago where there was over $25trn of investable money represented, less than 10% thought we would see 10yr yields at 2.25% before 1.75%. It perhaps shows how stretched things might have got a couple of weeks back. Maybe some of that is unwinding a bit at the moment.

Just on the US inflation data itself, the core printed at an unrounded +0.2942%, which compared with expectations for +0.2%. That pushed the year-on-year rate up a tenth to +2.1% with most of the move driven by payback to some of the outliers from earlier softer data. Of less coverage but of no less interest we had an unexpected upward revision to June CPI in Germany (+0.3% mom from +0.1%) even if France was left unchecked at +0.3% mom. However, the upside was partially driven by calendar effects, so it’ll be important to see if the rise is sustained in the July print.

It was also a fairly weak day for European bonds yesterday as well, with 10y Bunds up +4bps to -0.225% and to the highest level in a month, with yields also up a similar amount across the rest of the continent with the exception of BTPs (-3.7bps) and GGBs (-1.8bps), which seemed to get more of a lift from the risk-on moves. The surprise upward revision to German CPI perhaps played a role in the moves before the US CPI report gave them an extra jolt. Attention also focused on comments from ECB board member Coeure, who downplayed the significance of falling market-based measures of inflation expectations. He said that ECB staff analysis suggests that the recent decline in 5y5y inflation swap rates (-35.6bps this year) have been driven by changes in risk premiums, not actual inflation expectations. If true, this would reduce the pressure on the ECB to ease policy. The ECB meeting minutes, which showed “broad agreement” for action if conditions deteriorate, didn’t really move the needle. Equity markets were certainly a lot more sanguine with the STOXX 600 finishing -0.12% but down for a fifth consecutive session.

In equity markets, the S&P 500 again traded above 3000 intra-day but ultimately ended at 2999.89, so we’ll have to wait for another session to finally close above it. The index slipped between gains and losses during the afternoon but eventually ended +0.23%. The rise in yields and the poor auction slightly held back sentiment, as did a tweet from President Trump attacking China for “letting us down in that they have not been buying the agricultural products from our great farmers that they said they would.” HY spreads tightened -3bps to their narrowest level in over seven weeks, while the dollar and oil both finished close to flat.

This morning in Asia equity markets are trading higher, with the Nikkei (+0.11%), the Hang Seng (+0.55%), the Shanghai Comp (+0.46%) and the Kospi (+0.30%) all trading higher. Meanwhile, S&P 500 futures are +0.26% at 3011.75, suggesting we may have another attempt at closing above the 3,000 mark again today. The moves in Asia come ahead of the release of Chinese trade data this morning, where consensus expectations are that the country’s trade balance will rise to $45.00bn in June, up from $41.65bn in May. Data released overnight also showed the Singaporean economy unexpectedly contracted in the second quarter, by -3.4% (vs +0.5% expected) on an annualized basis, bringing the yoy growth rate down to +0.1% (vs +1.1% expected), the lowest since Q2 2009. Given the country’s dependence on trade, its economy is vulnerable to escalations in the US-China trade war.

Moving on. In Europe yesterday, there was some interest in comments out of the IMF given Lagarde’s incoming presidency at the ECB with the headlines quoting the IMF as saying that if further accommodation was required “the ECB should consider a new asset purchase programme anchored by capital key and possibly broadened to a larger set of assets”. At the same time, it said there may be only “limited room to cut rates further as diminishing returns set in” and that a “possible tiered deposit rate would have a very small impact on aggregate bank profitability and questionable impact on credit conditions”. Food for thought then.

To more fully recap Powell’s comments, he again said the economy is in “a very good place” but stressed concern about “crosscurrents such as trade tensions and concerns about global growth.” He also said that the neutral rate of interest and the neutral rate of unemployment are likely lower than the Fed had previously thought, which means that “monetary policy hasn’t been as accommodative as we had thought.” This adds further evidence in favour of a rate cut at the end of this month.

As for the other data that was out yesterday, in the US, jobless claims declined 13k last week to 209k and the lowest since April. It’s worth noting that there might be some volatility in this data at the moment due to retooling in the auto sector; however, it still continues to underscore the point that the labour sector remains upbeat. Later on, the June monthly budget statement showed a -$8.5bn fiscal deficit for June, as spending (+12.5% yoy) vastly outpaced revenues (+5.6%).

To the day ahead now, which this morning includes May industrial production data for the Euro Area before the June PPI report in the US is due out this afternoon. Away from that and next in line for the Fed is Evans this afternoon when he speaks in Chicago on trade and the economy, while over at the ECB we’re due to hear from Visco while at the BoE Vlieghe is due to speak.

via ZeroHedge News https://ift.tt/2XMuAPE Tyler Durden