While the overarching consensus is that in 10 minutes the Fed will announce a 25bps rate cut, markets are discounting a non-trivial probability of the Fed cutting 50bps (i.e., the market is currently pricing in a ~20% probability that Fed Funds will be below 2% following the FOMC meeting with spot being currently at 2.4%). As such, if consensus is right, the FOMC meeting could surprise markets, making the case for owning gamma ahead of the meeting.

But how does the “Fed premium” embedded in option market prices compare across asset classes ahead of the meeting? And how does it compare vs. recent market-moving Fed announcements?

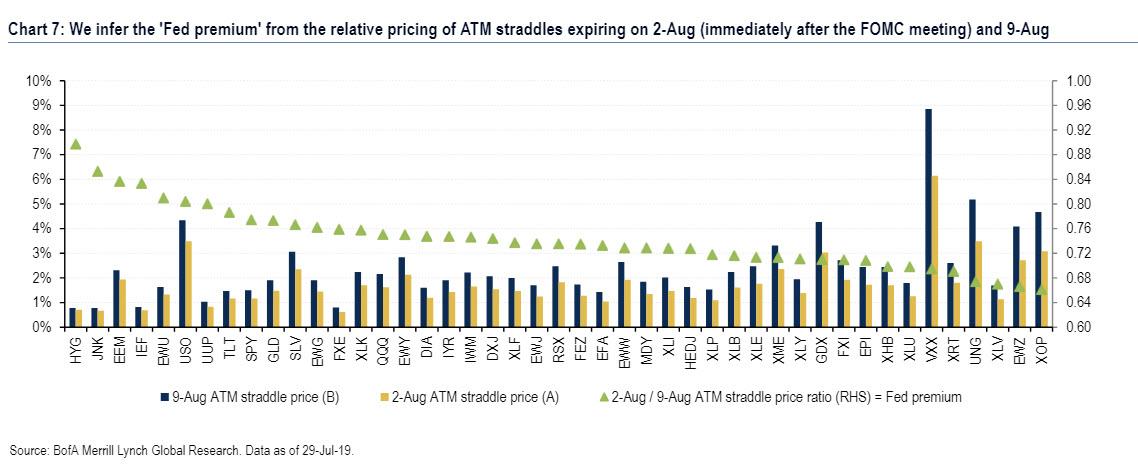

An analysis conducted by BofA’s derivatives team led by Benjamin Bowler looking at a pool of 45 ETFs with liquid option markets across five asset classes, reveals the ‘Fed premium’ from the relative pricing of ATM straddles expiring on 2-Aug (shortly after the meeting) and on 9-Aug. ETFs where the 2-Aug straddles look expensive vs. 9-Aug reflect markets that are pricing in a larger FOMC-related move.

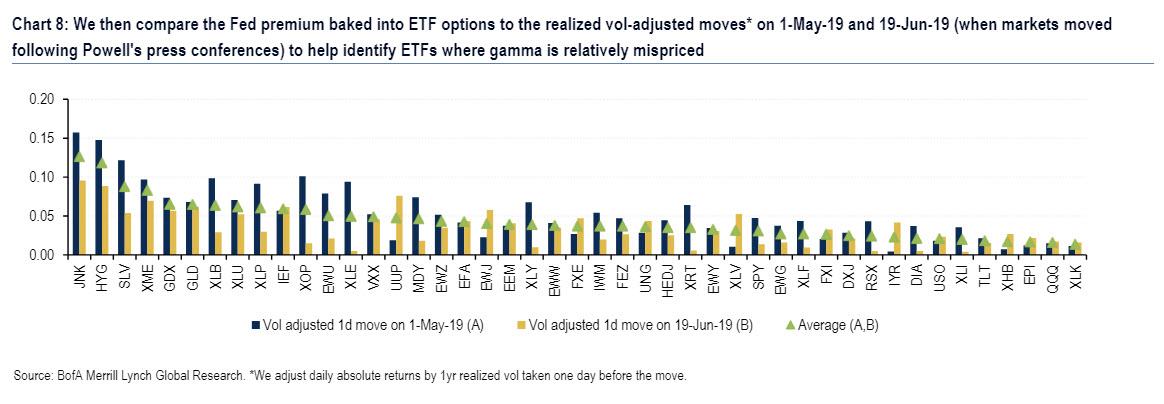

The bank then looked at the average vol-adjusted 1-day moves on 1-May-19 and 19-Jun-19, when markets reacted following Powell’s press conferences.

From this analysis, BOfA draws the following conclusions:

- Options on high-yield bond ETFs (HYG and JNK) have baked in the richest Fed premium. However, this appears to be warranted, given that they also recorded the largest moves on 1-May-19 and 19-Jun-19.

- Options on ‘safe haven’ assets (IEF, TLT, GLD) are all pricing in large moves (relative to other ETFs). However, BofA notes that while TLT barely moved on 1-May-19 and 19-Jun-19, gold recorded a sizable move on both days (as did IEF), and its Fed gamma is still cheaper today than IEF. As such, BofA would have a preference for owning gamma on the yellow metal rather than on Treasuries.

- RV opportunities: the Bank also finds a number of RV trading opportunities among pairs that traditionally are highly correlated but where Fed premium have diverged significantly today. For instance, the Fed premium is relatively large/small on EEM (EM equity)/FXI (China equity), GLD (Gold)/GDX (Gold Miners), and USO (WTI)/XOP (Oil&Gas E&P). Hence, within each pair, it would make sense to sell gamma on ETFs where the Fed premium is large and use the proceeds to buy gamma on ETFs where the Fed premium is small.

- The Fed premium is relatively low currently on rates-sensitive XLU (Utilities) and XHB (Homebuilders). However, these ETFs both recorded sizeable moves, and as such, they stand out as good candidates to own gamma on ahead of the FOMC.

via ZeroHedge News https://ift.tt/2GBYjoM Tyler Durden