If Powell Is Serious About No More Cuts In 2019, “Expect A Forceful Campaign” To Convince Investors

Commenting on yesterday’s FOMC announcement, BMO’s Jon Hill points out that whereas the dot plot suggests the Fed is now down cutting for 2019, “consensus remains a 1990s-style 75 bp of aggregate easing followed by an on-hold period to assess the impact of the recent moves.” And while the dot plot showed a dramatic schism within the FOMC, with 7 members expecting more rate cuts, while 10 happy with rates either where they are or higher, “in its own way, the Fed has tacitly endorsed this assumption by not shifting to a data-dependent stance this week.”

To be sure, as Hill notes, “it was a formidable communications challenge and given the muted market response to yesterday’s events, Powell can chalk this one up to a win; or at least a non-loss.”

Furthermore, it’s not as if the dot plot is indicative of anything: back in June, the Fed’s Summary of Economic Projections did not expect any rates cuts for 2019; three months later it had already delivered two.

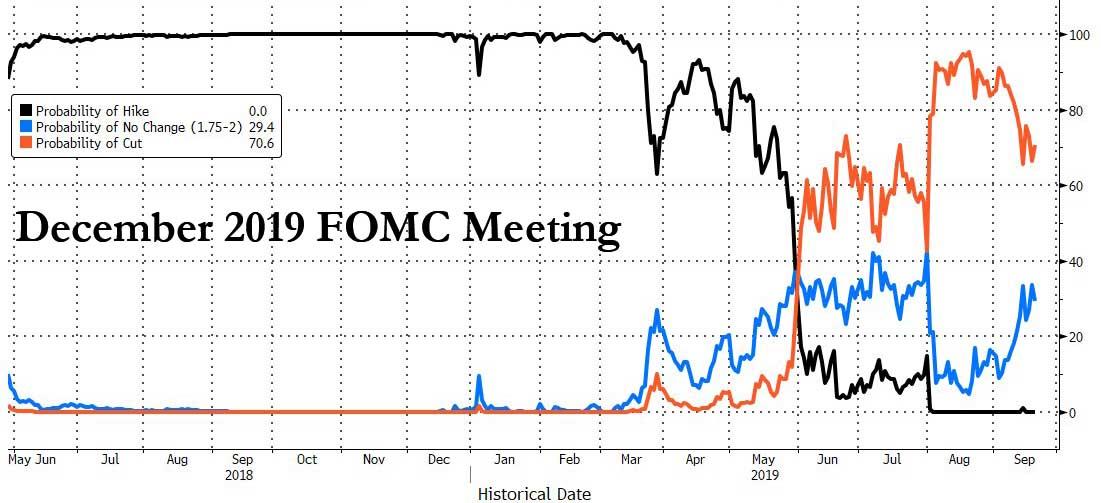

In any case, the degree to which additional 2019 easing is priced in or out in the near-term will be useful in gauging how one might expect policymakers to respond via any coordinated Fed-speak. As such, according to the BMO strategist, “In the event a final 25 bp cut isn’t the default position of core Committee members, then a campaign to dissuade investors from this assumption will begin in earnest.” To be sure, one look at the Fed Funds market shows that while the odds of a December 2019 cut are still well above 50%, they are shrinking fast, with the probability of not change up to 30%.

Of course, the same is true in the other direction, and if the market starts to reflect growing expectations for more than a final quarter-point cut in this ‘fine tuning’ endeavor, that’s an environment in which BMO would look for more intermeeting guidance from Fed officials. “Watch this space.”

Meanwhile, looking at the bond market, the fallout on the rest of the US rates complex from any clarity vis-à-vis the path of policy comes down to the ongoing debate in the shape of the curve; policy-error flattening versus reflationary-steepener.

This dynamic according to Hill, is not new, although it is one which will come back into focus as the competing global ‘uncertainties’ meet the reality of firming domestic data.

All of this contributes to our assumption that the broader tone for the market for the balance of 2019 will be established as we enter the fourth quarter. Our temporary bearish inclinations persist; with the caveat that there is a very real chance the 47 bp selloff in 10s thus far in September might represent the extent of the weakness we’ll see from the pendulum of pessimism’s trip out of the danger zone.

In this case, BMO predicts that the stage would be set for another round of consolidation with 1.80% as the interim focal-point until the time at which there is further clarification on the trade war, geopolitical tensions, Brexit, the dimming global outlook, and the flagging domestic manufacturing sector.

Said differently, if the market fails to stage another foray toward incrementally higher rates after a period of consolidation between now and the October FOMC meeting, it becomes increasingly difficult to envision any such backup given the low-to-negative global rate environment.

In short, the Treasury selling – which we believe was largely a by-product of the record IG issuance at the start of the month as a result of some $100BN in rate locks – has now ended, alongside the scramble to refi investment grade corporate debt.

What if we are wrong? Well, then according to Hill, “even an attempt to reach 2.25-2.50% 10s at this point in the policy and economic cycle would presumably be short-lived and met by a round of dip-buying interest from a variety of different investor bases.”

In short, buy the dip… in rates.

Tyler Durden

Thu, 09/19/2019 – 16:45

via ZeroHedge News https://ift.tt/30x2bhQ Tyler Durden