Punishing The Herd

Via Monday Morning Macro blog,

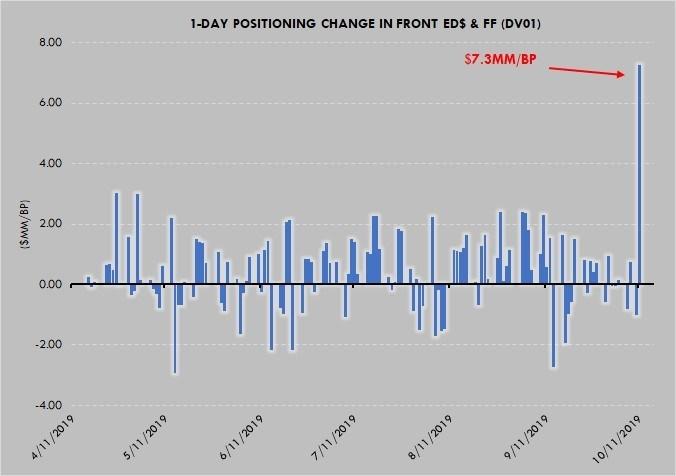

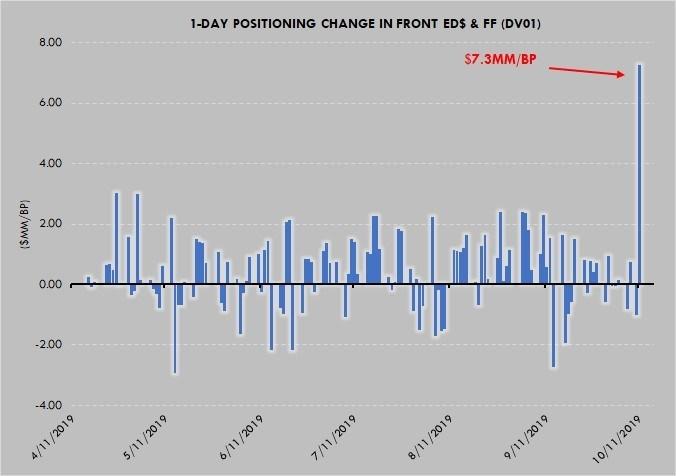

Friday’s change in positions across the front-end of the interest rates curve was the single largest swing in the last 6 months – a period marked by monster moves in rates – by a multiple of 2.5x+. The subsequent reaction this morning (triggered by the “inevitable” negative trade headline we all have come to expect as the new normal) is nothing more than a brutal punishment of that behavioral bias most innate in all of us.

Consider this chart for a moment. Think about what a huge mass of positions trying to get thru a small window on a holiday might look like. If you haven’t seen the chaos taking place in the futures-only trading session this morning, rest assured: everything is proceeding according to plan.

Almost.

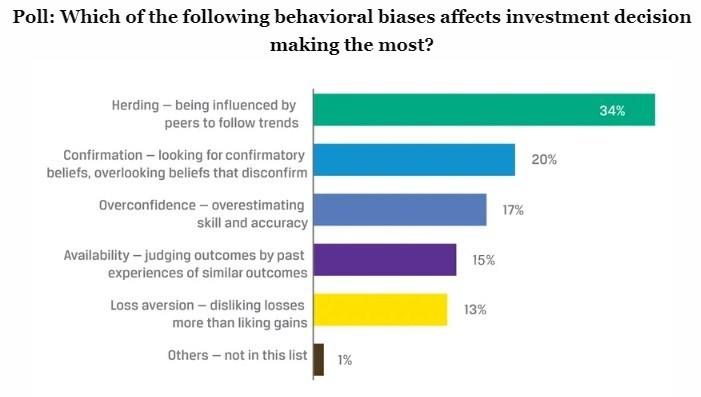

In 2015, a study by the CFA Institute found that “herding bias” was ranked as the most powerful behavioral bias affecting decision making for investments.

Incidentally, “confirmation bias” (a close cousin of “herding”) was ranked second on the list.

Yes, the irony is delicious – not to mention, I happened upon this lovely gem just about 10 minutes before the second stage unwind of Friday’s “Phase 1” euphoria began in earnest…

Am I the only one who sees it? https://t.co/jmTjsb76uF

— Clifford Asness (@CliffordAsness) October 14, 2019

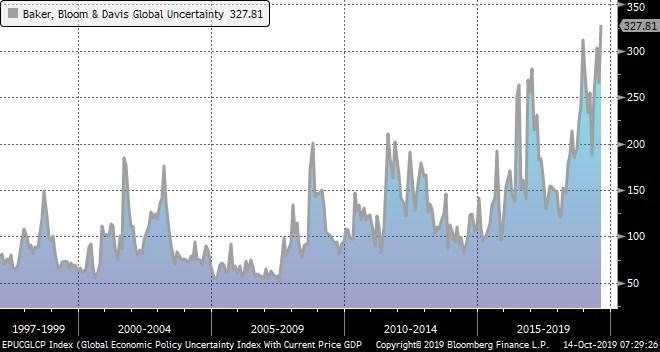

The relevance of these biases should not be understated in today’s markets. A high degree of uncertainty around both monetary policy & political outcomes has become the norm, even more so than in similar historical periods.

Friday’s Herding Bias

Thus, when Friday’s headlines hit regarding a kitchen-sink approach to monetary policy (albeit, emphatically – at least according to the Fed: “Not QE…”) & a trade-truce of sorts cum impeachment smokescreen from the administration in DC, there was a certain cathartic feel to the proceedings.

Nowhere was that more evident than in the front-end of the interest rates market where 2yr yields saw their 2nd largest 1wk selloff in the last 4 years+ (bested only by the move at the start of September).

Now, as you’ll note from that chart above, the LARGEST weekly selloff in the last 4 years (and in the past decade+, for that matter) came about at the start of September – and was quickly followed by a roaring rally back in the front-end of the curve. Notice, in fact, the degree to which these monster swings are evidently increasing meaningfully – especially in the past 6 months.

Naturally, the question becomes: have investors learned from these enormous swings, tactfully fine-tuning their approach, positioning & risk-allocation in response – minimizing the effects of “herding”?

Well, here’s a quick hint.

Remember that chart at the top?

This morning, we received the positioning data from Friday’s move. Here’s what positions did in the first 6 Eurodollar & FF contracts, as measured in DV01 terms.

It was easily the largest 1-day swing in those positions in the last 6 months, easily eclipsing the swings seen around those previously measured monster selloffs & roaring rallies from late summer & early fall.

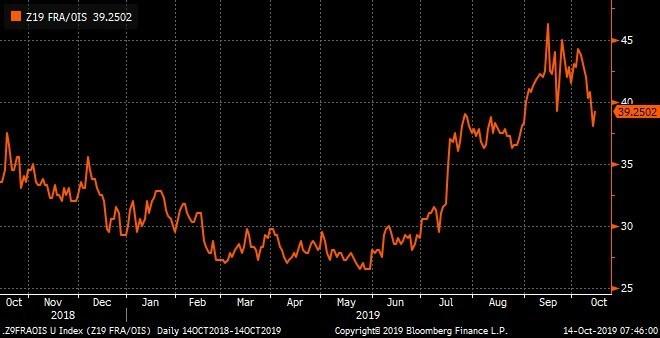

Furthermore, as Z19 FRA/OIS (a reasonable proxy for year-end “funding stress”) broke below 40bps, here’s what the corresponding futures positions did (EDZ9 + FFF0 + FFG0).

Move in Z19 FRA/OIS…

…and here’s what positions did in those contracts.

When in trouble…

In other words, people didn’t just unwind their “funding stress” hedges – they doubled down on their “de-stress” trades.

It’s the equivalent of the market taking a quick gander at the flaming carcass of year-end funding markets & deciding after Friday’s announcement from the Fed that “sure, let’s start getting short vol & short convexity at the worst levels of the last month & a half..”

Of course, that’s not to say that Friday’s announcement from the Fed wasn’t important. As we’ve noted previously, the only way out of this mess was QE4 – and $60bn/month buys a lot of bills, more than the total net supply over the corresponding period, for that matter. But was it really time to turn the ship around on year-end funding stress?

Today, early indications from the market are pretty clear. It was too soon to assume that everything’s all better again. The punishing move this morning in futures is evidence of this, taking a sledgehammer to the enormous position build that Friday witnessed. It’s far from over, yet.

Tyler Durden

Mon, 10/14/2019 – 09:23

via ZeroHedge News https://ift.tt/35yGce3 Tyler Durden