Party Like It’s 1999!?

Authored by Sven Henrich via NorthmanTrader.com,

Has the Fed been forced into the type of asset price inflation that actually will be the cause of the next recession? And may that recession be unavoidable despite everybody now ringing the all clear on recession risk? Perhaps the ultimate contrarian question to ask, but I assure you it’s not just a theorem, it’s actually based on historical precedence and that precedence was the year 1999.

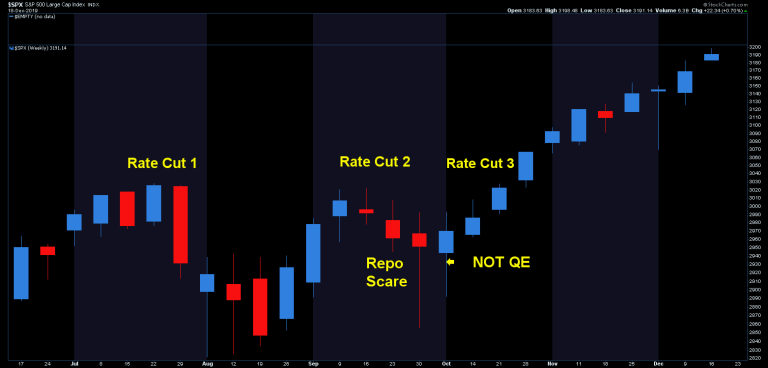

2019 was obviously about avoiding the global recession and central banks went berserk trying to prevent it with the renewed liquidity injections. System failure. In the real word system failure has consequences and ironically it may well be the central banks who have planted the seeds of destruction.

Remember the Fed’s initial plan in reacting to market pressure was to cut rates and stop QT, but then they were forced into repo and balance sheet expansion.

As a result markets blew higher and perhaps too high. Far above the earnings picture and underlying fundamentals. And by blowing asset prices too high they are setting the stage for the reversion and it is the reversion that brings about the recession. The Fed knows the economy and asset prices are very much intertwined these days, hence all the intervention programs.

But repo was forced upon them and the result we all know, the massive run into Q4:

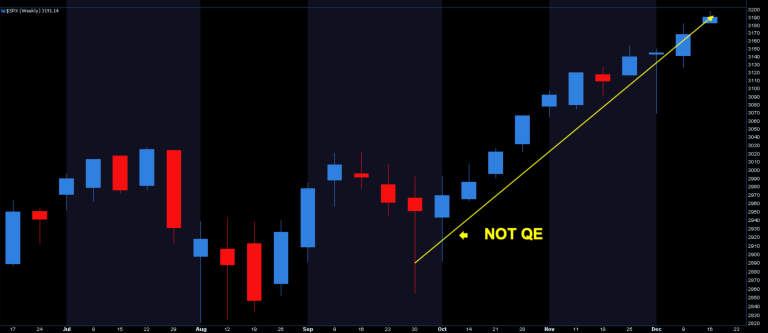

Cut away all the previous actions which still saw two way price discovery and you’re left with this:

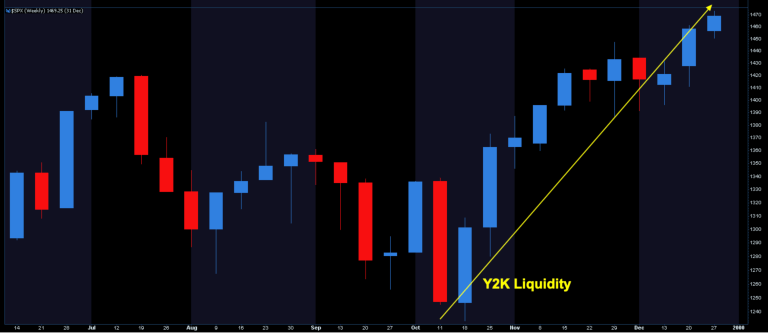

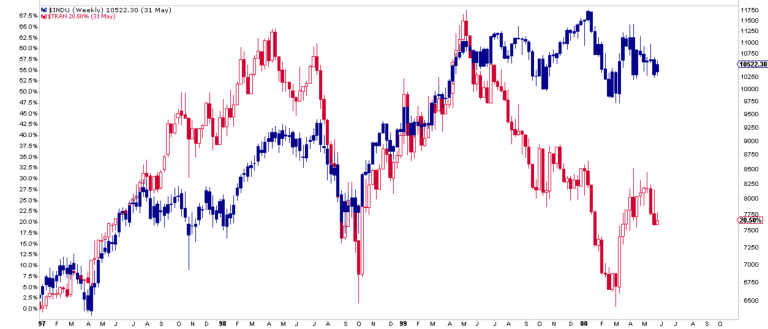

And this is in essence exactly what happened in 1999:

These 2 weekly charts are almost like for like. Same structure, same backdrop, same result.

This is the point I made on CNBC Fast Money last night where I tried to put everything in realistic perspective:

Alan Greenspan added liquidity to markets in anticipation of Y2K. A lot. And note the headlines today are very much the same headlines as back then.

Here from Wired Magazine in 1999:

“THE STOCK MARKET just keeps on climbing and Federal Reserve boss Alan Greenspan is making a massive amount money available for the economy. Greenspan has engineered the biggest expansion of money supply in the Fed’s history in the weeks leading up to the end of the year. The Fed’s move has been explosive on Wall Street because a free flowing money faucet at the Fed is the stuff that makes bull markets get fatter.

M3, the Fed’s broad definition of money, which includes currency, travelers’ checks, bank deposits, and money market mutual funds, has climbed an incredible US$194 billion over the past 13 weeks – the biggest increase ever. The money supply increased at an annualized rate of 15 percent, which is well above the Fed’s target growth rate of only 5 percent.

Just a week ago, M3 went up a whopping $36 billion, which would seem to indicate that the central bank is buying insurance against some possible disruptions as the calendar changes from 1999 to 2000, analysts said.”

Different time, different issues, same principle. In 1999 the Fed was anticipating issues with Y2k and flooded the market with liquidity. In 2019 the Fed is flooding markets with liquidity to deal with overnight funding issues. Another common thread: Both events were following 20% corrections (1998 & 2018) and in both cases the Fed reacted by cutting by 75 bp, and in both time frames the Fed added massive liquidity reacting to outside issues placed upon them. And in both cases markets started flying far above economic reality. How’s that for a common thread?

Liquidity is liquidity.

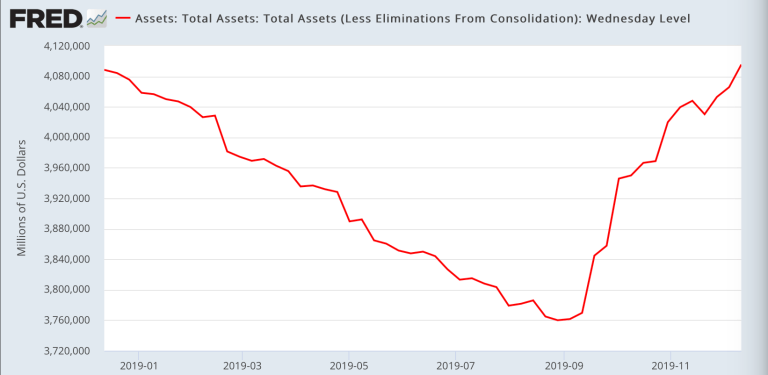

Well, what’s the Fed doing now? Adding massive amounts of liquidity to insure against overnight rates spiking. The similarity is striking, but perhaps even more frightening in its speed, breadth and scope:

None of this is normal. It’s historic, it’s outsized and it’s made its way into equity markets. The Fed is blowing an asset bubble.

And just like in 2000, here we are:

May I point out that the previous times the Fed was forced to spike repurchase agreements where associated with market excess, crashes & recessions.

This here is off the charts and reeks of a systemic crisis. https://t.co/paw0wFjiaX pic.twitter.com/KecPDzRJIF— Sven Henrich (@NorthmanTrader) December 17, 2019

Well done.

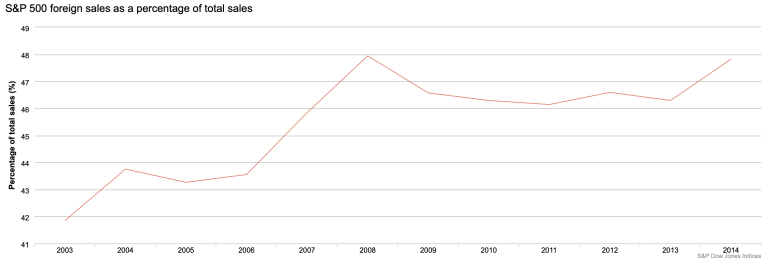

I keep getting questions about how international sales are now much larger than they were in 2000 hence a higher valuation would be perhaps justified. Not buying it. Sorry. The ratio hasn’t really done much in recent years. While a bit up from 2000 it’s been actually pretty steady, here are a chart to 2014:

And here’s what happened in the years after:

“In 2018, the percentage of S&P 500 sales from foreign countries decreased, after slightly increasing last year, and declining the prior two years. The overall rate for 2018 was 42.90%, down from 2017’s 43.62% and 2016’s 43.16%. The recent high mark was 2014’s 47.82%, and the recent low mark was 2003’s 41.84%.”

2014 was the high and it’s actually declined since then. Bottomline: 150% market cap to GDP is massively expensive and vastly disconnected from the underlying size of the economy.

And there in lie the seeds of destruction. Unless you get a growth acceleration to justify these valuations you are staring at massive reversion risk and given the size of the reversion with markets and economy so interlinked and with central banks already having blown their collective wads it won’t be enough to stop what is to come.

Greenspan couldn’t stop it until he cut rates by 500bp.

Bernanke couldn’t stop it until he cut rates by over 500bp.

Powell barely has 200 bp to play with.

Everybody is now ignoring the steepening of the yield curves. WHY? It’s aways been about the steepening, not the inversion. It’s the steepening following the inversion that seals the deal and these puppies are steepening:

What are we looking at here? 6 months to recession? 12 months? 18 months?

Who are you gonna believe? CFOs who run companies or the Fed who’s never seen a recession coming in its history:

CFOs: Recession coming

Fed: No risk of recession https://t.co/SU4kOlT2Dm— Sven Henrich (@NorthmanTrader) December 11, 2019

So no, this rally has been artificial, liquidity induced and the evidence suggests it’s the side effect of the Fed’s repo crisis management. They can’t reduce this liquidity now or markets fall apart.

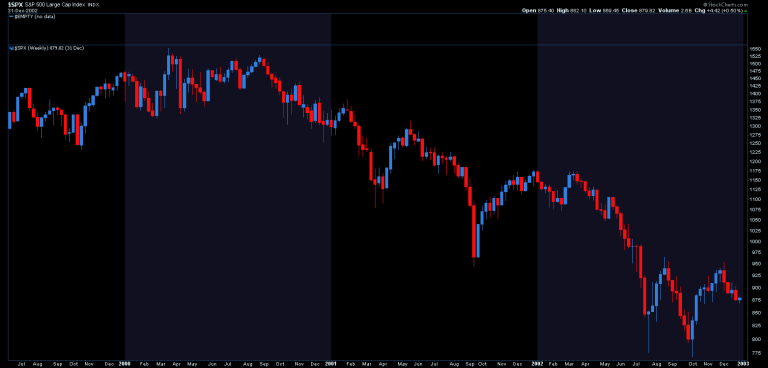

But note what may come may not be advertised with an obvious notable big crash. Yes the Nasdaq crashed in 2000, but other indices actually held in for a while.

Here’s the S&P 500 during the 2000:

Spike and drop, then lots of chop and tradable action for months. It was not until the end of the year when things got iffy. The recession came at the end of the year, and then the real fun began:

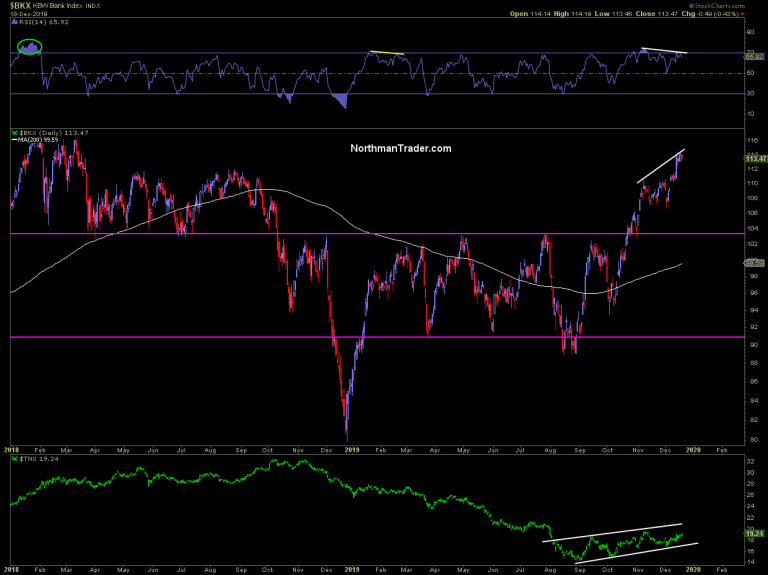

The Fed tried to prevent a recession with a supposed mid-cycle strategy, but then repo came and forced it to exacerbate the asset bubble. This bubble is now a clear and present danger to the fragile global economy. The next larger sell-off may well tip the scale as the bond market has not confirmed this rally at all.

Banks may have rallied, but the 10 year has been languishing in a bear flag:

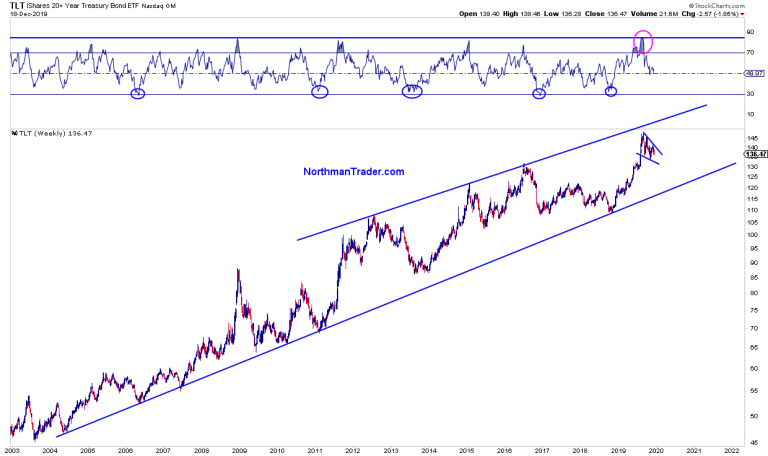

And $TLT is maintaining a sizable bull flag suggesting lower rates to come, the deflation scenario:

What these charts suggest is risk of a further slowing in the economy to come, not a bottoming and any signs of improvement may prove to be temporary.

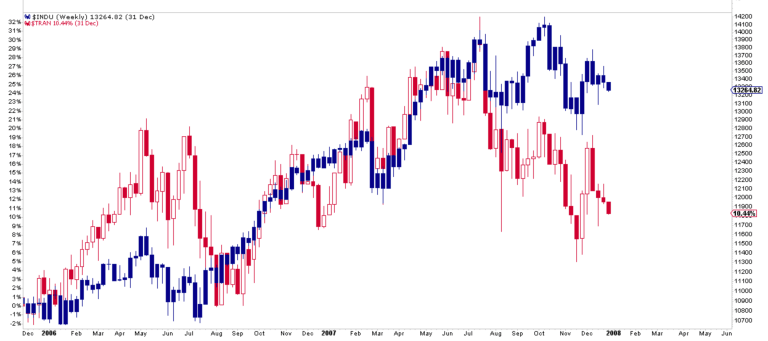

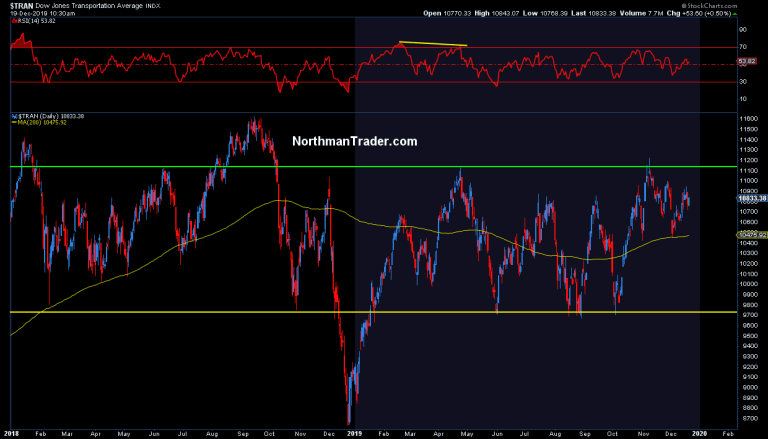

One sector that seems to confirm this is transports. In a world where everybody says it’s different this time it’s another one of these indicators that’s dismissed. Market cap to GDP 150%? It’s different this time. Yield curve steepening after inversion? It’s different this time. Transports lagging markets? It’s different this time.

Really? It better be because these signals are very profound. Note how transports along with yield curves sent out warning signs during the most recent bubble bursts:

2000:

2007:

2019:

Considering all the pumping and easing and printing transports had every opportunity in the world to make new highs and break out, but they haven’t:

Maybe that will change. After all the 2000 script calls for further rallies and new highs, but also increased volatility and quick snap corrections of the 5%-10% type that may well be initially bought. In 2000, markets went on to a final blow-off top in March and then dropped hard. Why? Because Y2K was over and the Fed reduced liquidity and it popped the bubble.

This Fed here has now made markets dependent on ever increased liquidity. On December 31 and January 2nd $150B in repo facilities are supposed to keep markets calm. Since October the Fed has been forced to keep increasing its liquidity injections to maintain calm. Markets have shown they can rally with ever increased liquidity injections. What they have yet to prove is that they can rally or sustain recent gains without them. The 1999 script suggests that they can’t and investors should well be aware that they are sitting on an artificial construct that is not only desperately disconnected from the size of the economy, but is reliant on ever larger liquidity injections to keep the momentum going. Investors are partying like 1999 but may not realize that they are. Any sizable correction from here and the linkage between markets and the economy is likely to come back to haunt given the size of the extension that has just taken place. That message is in the charts, in the data and in the footprint of history.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

Tyler Durden

Thu, 12/19/2019 – 14:30

via ZeroHedge News https://ift.tt/2EwTUC5 Tyler Durden