Goldman Trader: Here Is The Most Bullish Market Scenario, And The Most Bearish

In his latest note on markets, Goldman’s head of hedge fund sales, Tony Pasquariello, muses on the dog days of summer where “market volumes have receded to their lowest levels of the year and 1-month realized volatility on S&P has leaked into single digits.” And given the lack of tactical action – i.e., the Goldman flow desk is dry as a bone – Pasquariello, takes a “step back to think bigger picture on where the markets are headed.”

To do that, the Goldman trader writes that “at the risk of severe over-reduction, here’s one of the most bullish scenarios that I can sketch out for the next year or so … and, one of the most bearish”:

-

Bullish: Chinese policymakers are marking a clear shift that should drive public capital elsewhere. In turn, EM is a tricky asset class, writ large. Alongside this, there’s an obvious dearth of available yield to be harvested in Fixed Income (high yield has been superb over the past year, but at 4%, no thank you). As a client argued last week, a bubble forms when you suck in capital from everywhere else and put it in one place. So, if I were to dream the dream, it’s that US equities – led by mega cap tech – just don’t come off the current pace.

-

Bearish: We’ve been living in an era of unbounded government policy. Since last March, the Fed balance sheet has doubled and over $5tr of incremental fiscal spending has come to pass. With the FOMC edging towards tapering and the fiscal debates getting far more complicated, it’s fair to assert that the period of extraordinary policy conditions is ebbing. In the context of valuation and investor sentiment, it’s not totally obvious how we smoothly transition from all of that to a policy regime that is, ahem, something less.

Naturally, working for Goldman Sachs, Pasquariello writes that “in the end, I’m still inclined to “find the freight trains, and get on them.” Where that leads me is to be more positive on NDX than anything else on the board.” Yet even he concedes that this is “not a particularly original thought, and it comes with the admission that nothing is cheap these days and QE has been very friendly for long duration assets.” So, as the Goldman strategist concludes, “with appreciation for the heightened risk from the Fed into Jackson Hole and September FOMC, I’ll meet myself in the middle and advocate for carrying length via calls and call spreads on QQQ.”

* * *

Pasquariello then shares a few one-liners from 2013 — a year that brought us the Taper Tantrum and a 32% total return in S&P — with an application to the present day (he adds that “these are not intended to cut in one cohesive direction, but to stimulate some thought on the path ahead (yes, they tilt bullish, but you probably guessed that already”):

-

“Contrarians forget years like 1997: once these rallies get going, and the public gets really involved, they can run.” – while my hope is 2021 proves to more strongly resemble 1995 than 1997 or 1998, the moral of the story is the same: the largest investor on planet Earth is US retail, and in comparison to the prior cycle, over the past 12 months they have embraced stocks in a very different way.

-

“Two things provoke a major turning point in the markets: (1) an abrupt policy change; (2) an extreme shift in flow-of-funds.” – while I don’t see anything major on the horizon, at this stage of the game, the probability of a major surprise is more likely to work against investors than for. Said another way, it’s hard for me to see another Draghi circa 2012 or Abe circa 2013 or Powell circa 2020 right now. But, that’s not a reason to run for the hills, more a signpost for your overall level of risk taking.

-

“A few men sitting around a table and deciding how to allocate capital goes against everything I’ve ever believed.” – you can take this in a lot of directions; my personal view is it clearly favors the US.

-

“Pre-crisis, the ratio of mutual fund holdings of fixed income to dealer balance sheets was 3:1. now, it’s nearly 8:1.” – at the end of last year, this ratio stood at … 12:1. while knowing the world didn’t end on the move from 3:1 to 8:1, it shouldn’t make one comfortable, either.

-

“As deficits become cheaper to finance, they became harder to resist.” – despite the largest federal budget deficit since WWII, current interest expense — as a share of US GDP — remains at a historically normal level (link). this makes me think the transitory inflation debate looms very large in the grand scheme of things.

A few parting points from the note:

1. Commodities: GIR published a well-reasoned note evaluating the current landscape; to my eye, this is the punch line: “with the macro reflation tailwind rescinding over the past quarter, micro trends are likely to take up an even greater role in commodity pricing dynamics going forward. critically, these micro trends continue to point to ongoing, and in places steepening, commodity inventory declines that should continue to support prices and timespreads in the next 12-18 months”.

2. Japan: part of the bullish call on Japanese equities last fall was predicated on Mr. Suga’s ambitious growth agenda. at last check, things haven’t been going overly well for him. this note from Japanese Economics lays out the election dynamics for the upcoming period: link. the Japan buffs will recall that over the past two decades, the only PMs to establish long-term administrations of more than five years were Koizumi and Abe (second time).

3. Software: it’s been ten years — to the week — since Marc Andreesen penned his seminal op-ed, “Why Software Is Eating The World,” and it’s worth a revisit: link. note the IGV software ETF was trading at $48 back then … last print > 400

4. flows/positioning: a very simple framework for near-term flow-of-funds:

-

i. retail: inflows continue to be strong (money is still pouring into most everything).

-

ii. corporates: I know the broader seasonal is bad, but August is typically a healthy month for buybacks (as new issue wanes into what should be a very active Sep).

-

iii. systematic: our models estimate non-discretionary funds will continue to be on the bid in most short-term scenarios (in modest size).

-

iv. dealers: long option gamma is near multi-year highs; so too is top-of-book liquidity (both factors should provide ballast to price action).

-

where I’m going with this: as volumes fall to YTD lows, the activity that we see is still biased to the buy side.

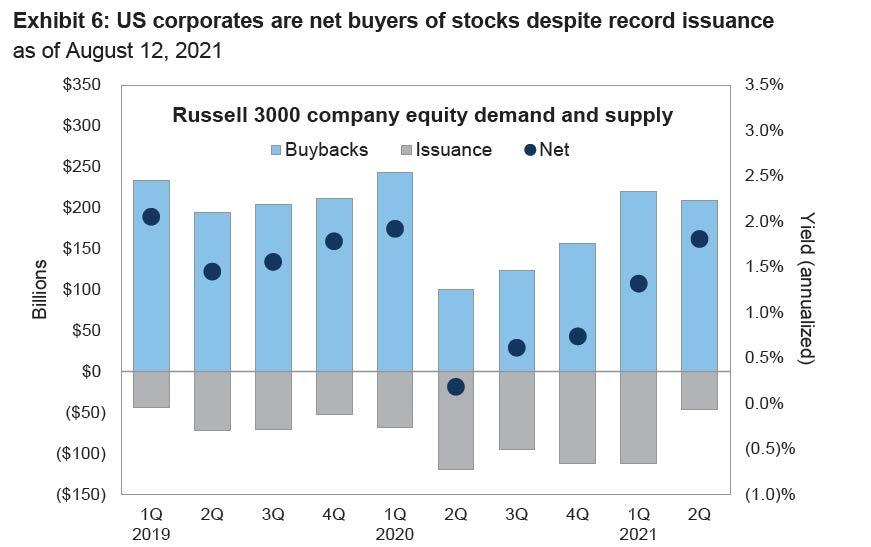

5. Corporate Technicals: To underline the prior point, this note from Ben Snider and US Portfolio Strategy is a superb look into supply and demand within the US equity market: link. the most surprising piece to me was, despite the recent boom in new issue, US corporations were still net buyers of stocks in H1:

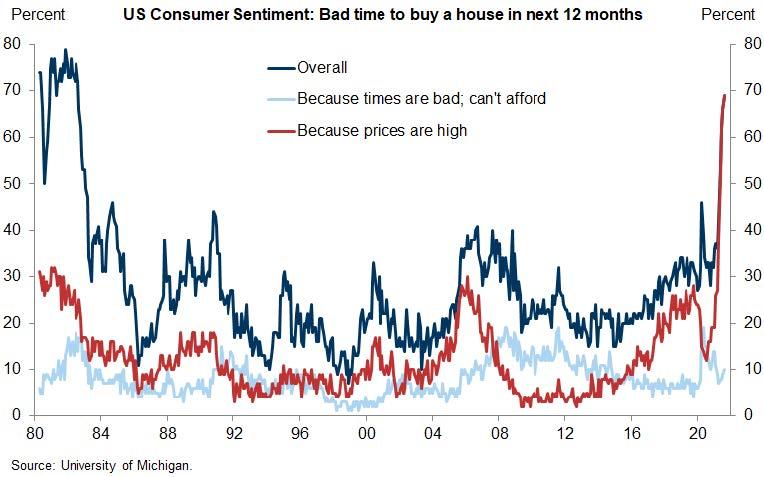

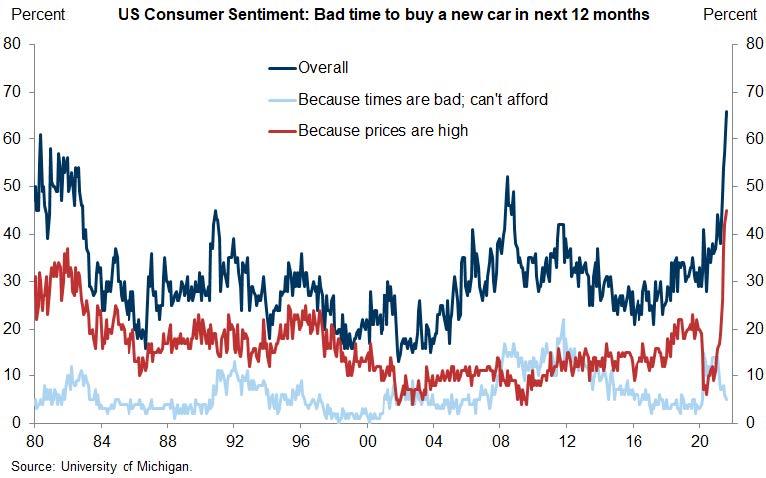

6. consumer confidence: As you can see in these charts, if you look under the hood of last week’s University of Michigan data, it’s vividly clear that people are not at all happy with the increased cost of cars and housing (credit to Mike Cahill in GIR). I’m not sure exactly what to do with this, but when nearly 70% of your economy is driven by the consumer, I don’t think you can dismiss it out of hand (link). I’d also note that the broad tone on earnings from the big US retailers this week suggests early signs of a potential slowdown.

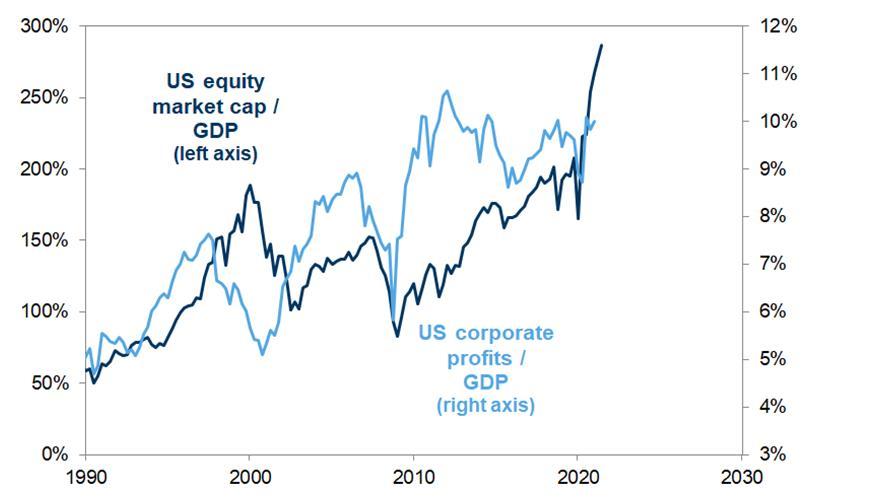

7. It’s no secret that the ratio of equity market cap to GDP is well above where it stood during the tech bubble (dark blue line). while that needs to be taken seriously, I’d note the ratio of US corporate profits to GDP looks healthy (light blue line):

8. this was the aforementioned 1995 overlay. while I wouldn’t stake my life on these analogs, it’s too good not to reference:

Tyler Durden

Tue, 08/24/2021 – 14:20

via ZeroHedge News https://ift.tt/3jawdV4 Tyler Durden