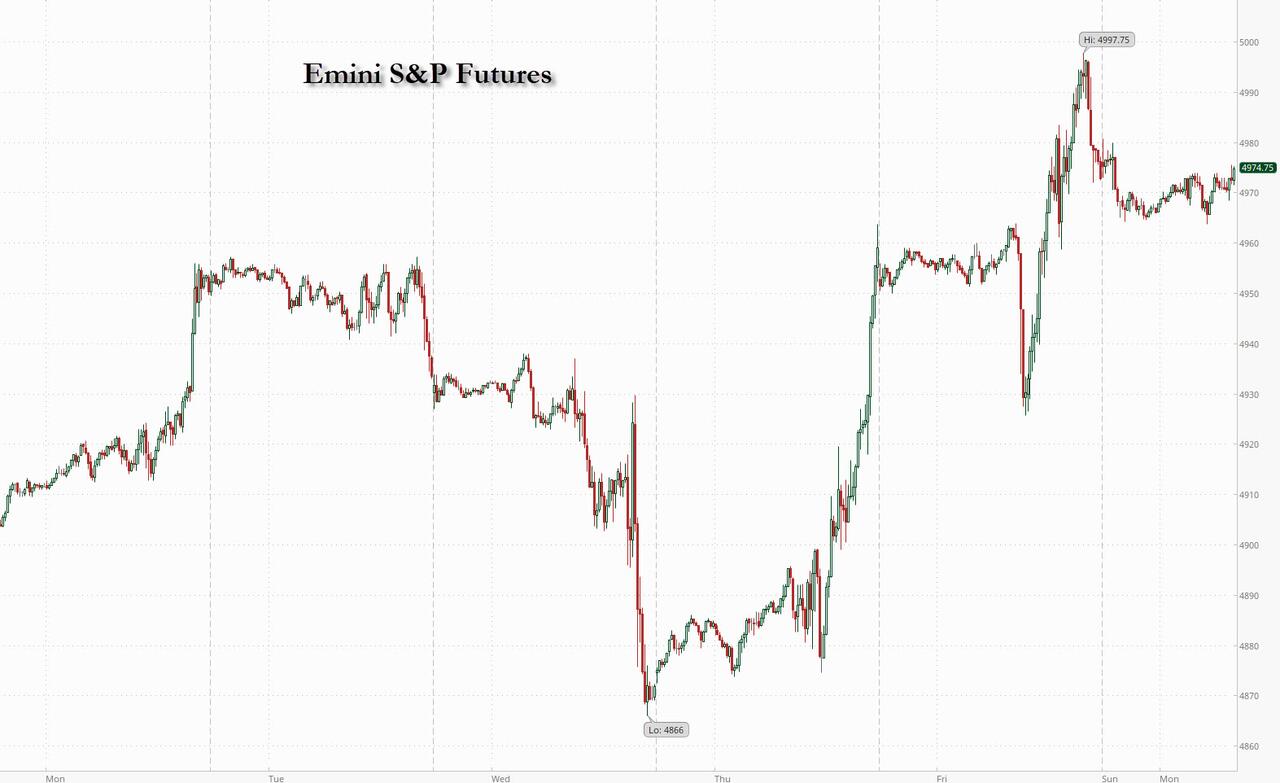

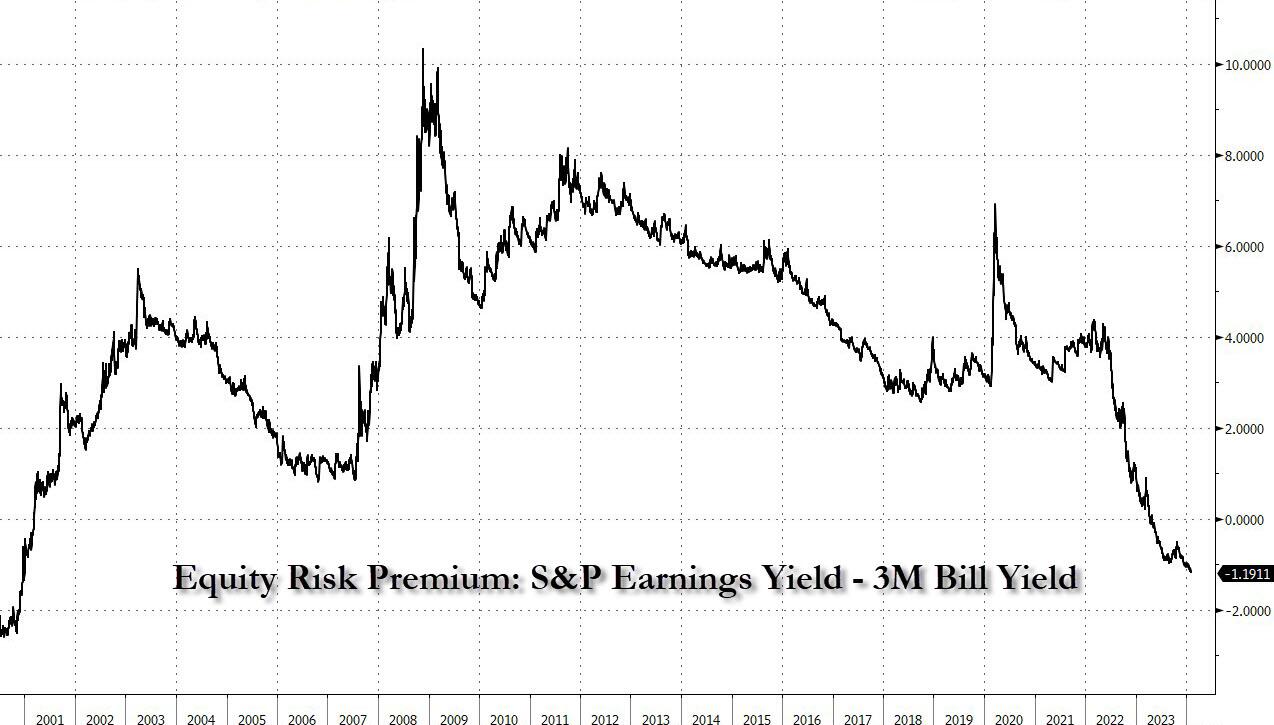

US equity futures and bonds fell while the dollar rose after Fed Chair Jerome Powell again pushed back against any hopes of lower interest rates during his 60 Minutes interview, saying it’s “not likely” the Fed would cut in March (which was to be expected after Friday’s blowout jobs number). As of 7:40am ET S&P futures dropped 0.1% after closing at an all time high on Friday when they rose as high as 4998. Meanwhile, European shares edged higher, supported by strong earnings from Italian lender UniCredit SpA while Asia closed red after a rollercoaster session in China which first plunged then saw another stabilization bid from the plunge protection team. 10-year Treasury yields climbed nine basis points to 4.11%, extending a move that started after Friday’s blockbuster jobs report as yields on debt from Australia to Germany rose. Meanwhile, the Bloomberg Dollar Index traded near a two-month high and oil and gold prices retreated, and bitcoin reversed a weekend selloff

In premarket trading, Caterpillar gained 3.2% after posting fourth-quarter profit that exceeded analysts expectations. On the other end, McDonalds dropped 2% after the fast food giant reported revenue and comparable sales for the fourth quarter that missed the average analyst estimates:

- Revenue $6.41 billion, +8.1% y/y, estimate $6.45 billion

- US comparable sales +4.3% vs. +10.3% y/y, estimate +4.45%

- International operated markets comparable sales +4.4% vs. +12.6% y/y, estimate +5.03%

- International developmental licensed markets comparable sales +0.7% vs. +16.5% y/y, estimate +5.06%

Boeing shares dropped 2.1% after the cursed company found more misdrilled holes on its 737 Max jet, which could further delay deliveries. Fuselage supplier Spirit AeroSystems was also down 3.0% as the latest manufacturing slip originated with a supplier and will require rework on about 50 undelivered 737 jets to repair the faulty rivet holes, Boeing commercial chief Stan Deal said in a note to staff. Here are some other notable premarket movers:

- 4D Molecular Therapeutics jumps 63% after the biotech reported interim data from its phase 2 clinical trial for a treatment for wet AMD, an eye disease.

- Air Products slides 7.9% after cutting its outlook for the year’s adjusted earnings per share.

- Cano Health plunges 51% after the company filed for Chapter 11 bankruptcy.

- Catalent gains 11% after a deal to be bought by Novo Holdings.

- Caterpillar Inc. rises 4.4% as higher sales in its energy and transportation business in the 4Q helped the company post profit that topped analysts’ expectations.

- Elanco Animal Health gains 5.2% after the company said it is selling its fish health business to Merck & Co for $1.3 billion in cash.

- Estée Lauder soars 15% after saying it’s cutting as many as 3,000 positions as part of a restructuring plan.

- Everbridge shares rise 18% after the company announced a deal to be acquired by Thoma Bravo.

- Haynes International gains 3.4% after agreeing to be purchased by Spanish stainless steelmaker Acerinox SA.

In a highly anticipated interview on CBS’s 60 Minutes, Powell said that the “danger of moving too soon is that the job’s not quite done.” The comments add evidence to a view that traders have been over-eager in pricing in interest rate cuts and now need to dial back those expectations. Brom Goldman to Barclays are among those that have pushed back their predictions for the timing of the Fed’s first reduction.

“There’s still a lot of uncertainty as to how quickly they cut,” said James Rossiter, head of global macro strategy at Toronto Dominion Bank. “It’s a quiet week for data, so we’ll be watching central bankers very closely.”

After March rate cut odds tumbles after last week’s FOMC, the chance of a quarter-point of easing in March fell to just 10% after Powell’s comments. Compare this to just four weeks ago, when a move by then was considered a near certainty by investors.

Investors said they’ll be paying close attention to the line up of central bank speakers this week for more clues about the direction of monetary policy. Chicago Fed President Austan Goolsbee is scheduled to speak on Bloomberg TV later today, while Cleveland Fed President Loretta Mester and Minneapolis Fed President Neel Kashkari are due to provide remarks on Tuesday.

European stocks bucked the global selling, and the Stoxx 600 rose 0.2%, near session highs, with food and beverage and personal care sectors are the best performers while automakers underperformed. UniCredit soars as profit beat estimates, allowing the bank to boost shareholder returns, while Nordea Bank falls after reporting fourth-quarter earnings and giving new profitability goals. Here are some of the biggest movers on Monday:

- Shares in UniCredit jump as much as 10% after the Italian lender reported earnings that beat estimates and boosted shareholder returns on 2023 profit to €8.6 billion, with analysts expecting consensus estimates to rise. Italian peers reporting later this week, including Intesa, gain.

- Shares in Lotus Bakeries rise as much as 15% to hit a new record high, after the cake and pastry maker’s full-year results beat expectations. As annual sales hit €1 billion for the first time, analysts were impressed by the company’s ability to keep growing its volumes.

- Shares in Renault climb as much as 4.7% as speculation about possible consolidation in the auto industry is fanned by a press report and analyst notes. The shares pared their gain after Stellantis chairman John Elkann said there’s “no plan” concerning merger operations with other competitors.

- Shares in Jeronimo Martins jump as much as 3.2% after the retailer was upgraded to overweight from equal-weight at Barclays, which expects another year of double-digit earnings per share growth for the company.

- Shares in National Grid rise as much as 3.4% after Jefferies upgrades its rating on the power transmission and distribution company to buy, saying it looks set to deliver “highly attractive growth” in both the UK and US.

- Shares in Nordea fall as much as 4.9%, the most since March 2023, after the Nordic lender reported results. Analysts say the numbers fell short of expectations on profits, but it’s not likely to weigh on estimates going forward.

- Shares in Atos fall as much as 30% as French IT company said it’s seeking a court-appointed mediator to assist in its refinancing discussion with banks. A planned €720 million ($777 million) rights issue will no longer take place. The news is seen as a blow for equity holders given the risk of significant dilution, according to Oddo.

- Shares in Delivery Hero fall as much as 10%, extending Friday’s 23% plunge on concern about an Asian deal, even as the German food delivery company pre-released fourth-quarter results that analysts called reassuring.

- Shares in Vodafone fall as much as 2.1% as analysts looked past the telecom firm’s third-quarter sales beat to highlight uncertainties such as revenue headwinds posed by cable television regulation in Germany and the failed merger of its Italian business.

- Shares in Barco drop as much as 5.5% after ING cut its rating on the stock to hold from buy, citing a lack of short-term catalysts.

- Shares in Banco Santander and Lloyds fell after a Financial Times report that Iran was able to covertly move money using accounts at the lenders. Santander told the FT it was “highly focused on sanctions compliance” while Lloyds said it complied with sanctions laws.

In Asia, Chinese stocks saw another volatile session as investors assessed the latest pledges by policymakers to stabilize the slumping equity market. The benchmark CSI 300 index swung between losses of 2.1% and gains of 1.7%. The MSCI Asia Pacific Index declined as much as 0.7%, with Tencent, Samsung and BHP among the biggest drags. Benchmarks declined more than 1% in Australia, South Korea and Singapore. Japanese equities climbed after the yen weakened. The China Securities Regulatory Commission vowed on Sunday to prevent abnormal fluctuations, though the plan was short on specifics and sparked another early liquidation in China. The CSI 300 Index slumped 4.6% in chaotic trading last week to its lowest level in five years.

“Whether or not today marks the floor to Chinese equities is yet to be seen, but it sure feels as though we’re bumping along the bottom,” said David Chao, a strategist at Invesco Asset Management in Singapore.

- Hang Seng and Shanghai Comp were initially both pressured from early on in a continuation of the equity rout after Chinese stocks plunged to five-year lows despite the PBoC’s previously announced RRR cut taking effect, while the securities regulator pledged to stabilise the market and prevent abnormal market fluctuations although refrained from announcing specific measures. As such, Chinese markets later recovered from their lows which saw both benchmarks briefly turn positive.

- ASX 200 was dragged lower by underperformance in the commodity-related sectors and as participants await tomorrow’s RBA decision, while Australian Services and Composite PMI data improved but remained in contraction territory.

- Nikkei 225 was underpinned by recent currency weakness and with the biggest movers influenced by earnings.

- Indian stocks declined, erasing all of their initial gains as Reliance Industries Ltd. and lenders retreated. The S&P BSE Sensex fell 0.5% to 71,731.42 as of 03:45 p.m. in Mumbai, while the NSE Nifty 50 Index declined 0.4% to 21,771.70. In comparison, the MSCI Asia Pacific index finished 0.2% lower. Nine of the 15 NSE sectors closed in the red, with the consumption and fast-moving consumer goods gauges leading on the way down. Out of 30 shares in the Sensex, 8 rose and 22 fell.

In FX, the Bloomberg Dollar Spot Index rose 0.3% to its highest level since Dec. 12, while Treasuries bear-flattened, as traders moved to pricing only a 10% chance of a quarter-point Fed cut in March following Powell’s CBS interview.

- The Norwegian krone, Swedish krona and Australian dollar led G-10 losses against the dollar on dampened risk appetite

- USD/JPY rose as much as 0.3% to 148.82, the highest level since November; Currency pair saw a 1.3% daily gain on Friday after strong US payrolls data, the biggest daily move in three months

- EUR/USD slumped as much as 0.4% to 1.0747, the lowest level since Dec. 11; European government bonds fell in tandem with Treasuries

In rates, treasuries bear-flattened with two-year yields climbing as much as 10bps to a one-month high of 4.46% while the 10Y rose 9bps to 4.12% after Powell said Americans may have to wait beyond March for the central bank to cut interest rates, adding to gains seen on Friday after the blockbuster jobs report. European bonds have followed suit. Treasury auctions resume Tuesday with $54b 3-year note sale, followed by $42b 10-year and $25b 30-year on Wednesday and Thursday.

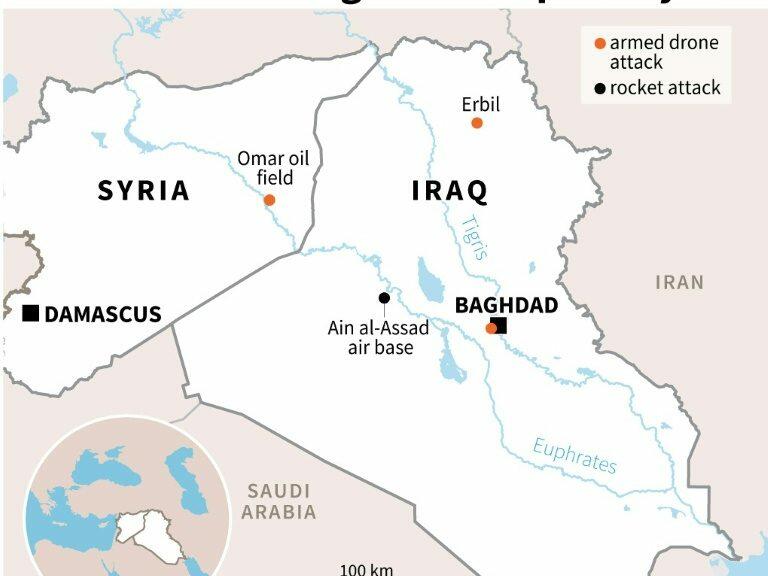

In commodities, oil prices declined, with WTI falling 0.5% to trade near $71.90 overlooking geopolitical tension after American forces launched attacks against the Houthis, following strikes on Iranian forces and militias in Syria and Iraq late last week. Spot gold falls 0.7%.

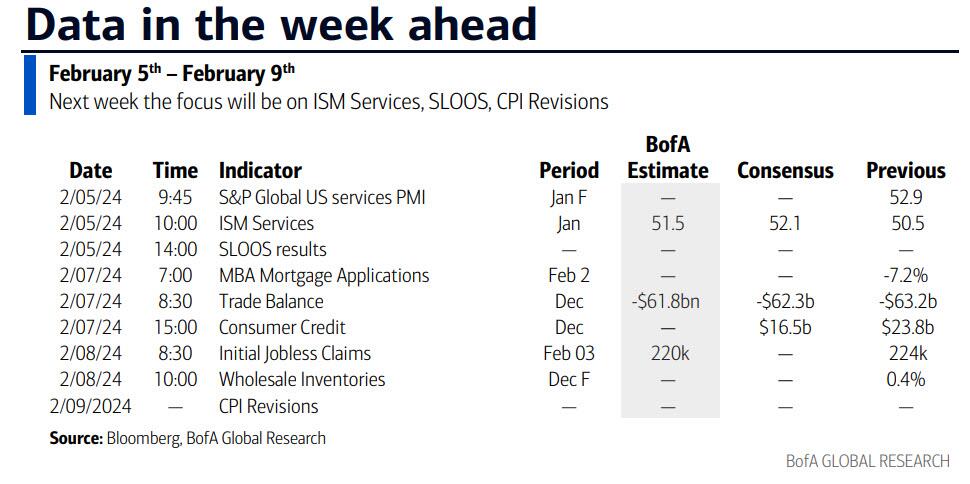

On today’s calendar, we have January S&P services PMI (9:45am), ISM services index (10am); The senior loan officer opinion survey is scheduled for release at 2pm.Federal Reserve members scheduled to speak include Goolsbee (10am) and Bostic (2pm); busy week for Fed speakers also includes Mester, Kashkari, Collins, Harker, Kugler, Barkin, Bowman and Logan.

Market Snapshot

- S&P 500 futures down 0.3% to 4,967.50

- STOXX Europe 600 little changed at 483.80

- MXAP down 0.2% to 166.08

- MXAPJ down 0.6% to 505.32

- Nikkei up 0.5% to 36,354.16

- Topix up 0.7% to 2,556.71

- Hang Seng Index down 0.2% to 15,510.01

- Shanghai Composite down 1.0% to 2,702.19

- Sensex down 0.4% to 71,777.05

- Australia S&P/ASX 200 down 1.0% to 7,625.85

- Kospi down 0.9% to 2,591.31

- German 10Y yield up 3 bps at 2.27%

- Euro down 0.3% to $1.0761

- Brent Futures down 0.4% to $76.99/bbl

- Gold spot down 0.9% to $2,021.03

- US Dollar Index up 0.25% to 104.19

Top Overnight News

- Federal Reserve Chair Jerome Powell said Americans may have to wait beyond March for the central bank to cut interest rates as officials look for more economic data to confirm that inflation is headed down to 2%.

- US bonds fell after Federal Reserve Chair Jerome Powell pushed back against the prospect of an interest-rate cut in March, further dashing hopes of a speedy pivot toward easier monetary policy.

- Chinese stocks were caught in another volatile session Monday following last week’s rout, as investors assessed the latest pledges by policymakers to stabilize the slumping equity market.

- The US vowed more strikes against Iran’s forces and its proxies in the Middle East after three straight days of punishing attacks, even as Washington insisted it won’t be pulled into a prolonged regional conflict.

- President Joe Biden implored Nevada voters to make Republican frontrunner Donald Trump a “loser,” part of a two-day swing designed to gain an advantage in a battleground state he hopes to win again later this year.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly subdued after last Friday’s red-hot jobs report and the latest comments from Fed Chair Powell who reiterated the expectation that a March cut is likely too soon. ASX 200 was dragged lower by underperformance in the commodity-related sectors and as participants await tomorrow’s RBA decision, while Australian Services and Composite PMI data improved but remained in contraction territory. Nikkei 225 was underpinned by recent currency weakness and with the biggest movers influenced by earnings. Hang Seng and Shanghai Comp were initially both pressured from early on in a continuation of the equity rout after Chinese stocks plunged to five-year lows despite the PBoC’s previously announced RRR cut taking effect, while the securities regulator pledged to stabilise the market and prevent abnormal market fluctuations although refrained from announcing specific measures. As such, Chinese markets later recovered from their lows which saw both benchmarks briefly turn positive.

Top Asian News

- China’s securities regulator vowed to stabilise the market and prevent abnormal market fluctuations although refrained from announcing specific measures, while it will crack down on ill-intended short-selling and attract more investment by long-term capital. It was also reported that China is to step up financing support for major private projects, according to Bloomberg.

- Indonesia Central Bank Governor Warjiyo said there should be room to cut rates, but they are waiting for the IDR to strengthen and stated that Indonesia’s economy is in an upward cycle with a peak seen in 2026.

- Foxconn (2317 TW) January sales down 20.9% Y/Y; the outlook for the first quarter of this year is expected to decrease Y/Y

European equities are mixed, Stoxx600 (+0.1%); though the FTSE MIB outperforms, lifted by gains in UniCredit (+8.7%), post-earnings. European sectors also hold onto a mixed footing; Optimised Personal Care and Grocery is lifted by Jeronimo Martin (+2.5%) whilst Energy lags in tandem with broader weakness in the crude complex given sentiment/USD strength. US equity futures (ES -0.2%, NQ -0.2%, RTY -0.8%) hold just below the unchanged mark and within a relatively tight range; with the exception of the RTY, which significantly underperforms in a continuation of Friday’s price action.

Top European News

- UK seeks to end the Northern Ireland impasse and unveiled a plan to reduce trade friction on goods flowing from Great Britain to Northern Ireland, according to Bloomberg.

- Sinn Fein’s Michelle O’Neil was formally appointed as Northern Ireland’s First Minister to become the first Irish nationalist to hold the post, according to Reuters.

- ECB’s Elderson said that they see a lot is going well for banks in the area of climate risks even if no single bank has currently met all expectations.

- ECB’s Vujcic said patience is needed and need to ensure there aren’t any second-round effects on inflation from wages before cutting interest rates, according to Bloomberg.

- UK ONS Labour Force Survey re-weighting: Unemployment Rate in three-months to November 3.9% (prev. estimate 4.2%).

- German Ifo writes that the lack of orders within manufacturing is becoming an increasing burden on the domestic economy

- OECD raises 2024 global growth forecast to 2.9% from 2.7%, holds 2025 forecast at 3%. US 2024 forecast raised to 2.1% from 1.5%, 2025 held at 1.7%. EZ 2024 forecast cut to 0.6% from 0.9%, 2025 lowered to 1.3% from 1.5%. Chinese 2024 forecast held at 4.7%, 2025 held at 4.2%. Japan 2024 growth held at 1.0%, 2025 lowered to 1% from 1.2%. UK 2024 forecast held at 0.7%, 2025 held at 1.2%. Expects Fed to cut rates in Q2, ECB in Q3; policy will remain restrictive for some time.

FX

- The Dollar is still enjoying the spoils from the post-NFP bounce printing a 104.29 high for the session thus far; next level to the upside goes back to 104.50 ahead of a cluster of highs between 104.50-60 from mid-Nov.

- EUR is still hampered by the USD with the pair at its lowest level since mid-Dec., 1.0750 is the trough today; 11th December low at 1.0740.

- JPY is steady vs. the USD but near Friday’s levels with upside in USD/JPY running out of momentum at the 28th Nov. high of 148.83.

- AUD remains the laggard of the antipodes amid cautious sentiment surrounding China. Downtrend since late Dec continues to extend with AUD/USD low today of 0.6487 the lowest since mid-Nov.

- PBoC set USD/CNY mid-point at 7.1070 vs exp. 7.2088 (prev. 7.1006).

US Headlines

- Fed Chair Powell said with the economy strong, they feel that they can approach the rate cut timing question carefully but repeated expectation that the March meeting is likely too soon to have confidence to start rate cuts and want more confidence before taking the very important step of starting rate cuts. Powell said they are making good progress on inflation and could move sooner if they saw labour market weakness or inflation persuasively coming down but added that more persistent inflation could mean a later move and that there is no easy, simple, obvious path, according to 60 Minutes interview. Furthermore, FT reported that Powell said the Fed expects to make three cuts this year and a CBS reporter noted that Powell suggested the first cut could occur around mid-year.

- Fed’s Bowman (voter) said on Friday that she expects inflation to decline further with the policy rate held steady and it will eventually become appropriate to gradually cut rates if inflation continues to decline. Bowman also stated that upside risks to inflation include labour market tightness, easing financial conditions and geopolitics, while she will remain cautious on policy and watchful on data and revisions. Furthermore, she said reducing the policy rate too soon could mean more hikes will be needed in the future and she remains willing to raise the policy rate at a future meeting if needed, according to Reuters.

- US Senate Majority Leader Schumer announced a bipartisan bill that toughens border security and grants new aid to Ukraine, Taiwan and Israel, while the national security supplemental package totals USD 118bln and includes USD 60bln in military support to Ukraine and USD 14bln in security assistance for Israel, while it includes USD 30bln to strengthen US border security, according to a Reuters source.

- US President Biden said he strongly supports the bipartisan deal and that it is the toughest and fairest set of border reforms in decades, but added that there is more work to be done to get it over the finish line, while it was separately reported that US Senator Murphy said the bill also authorises a quarter of a million more visas which will reunite thousands of families, according to Reuters.

- US House Majority Leader Scalise said the Senate border bill will not receive a vote in the House, while House Speaker Johnson also said if this bipartisan bill reaches the House, it will be dead upon arrival.

- US President Biden is reportedly weighing joining Las Vegas hotel workers if they go on strike on Monday, according to the union chief.

Fixed Income

- USTs are slumping in a continuation of the post-Payroll move with Chair Powell factoring, alongside Bowman & Goolsbee also being unwilling to commit to a specific period; voter Bowman adding that she “remains willing to raise the policy rate” if required, currently 111-07 towards session lows.

- Bunds are unreactive to the morning’s Final Composite & Services PMIs, which were subject to modest revisions. Within them, concern over wages/prices in the service sector remain a highlight and potentially influenced action on the margin; thus far, narrow 60 tick band which is well within Friday’s 134.82-135.88 extremes.

- Gilts are similarly pressured, with further hawkishness filtering through post-BoE as we are yet to hear from those who voted for unchanged (ex-Pill) for any insight into when to expect the first cut; currently trading towards the session trough at 98.20.

Commodities

- Modest pressure in the crude benchmarks as the USD continues to strengthen post-NFP/Powell. Attention is still firmly on geopols. after US/UK strikes against the Houthi’s and Kirby announcing more action will follow.

- Gold is unable to derive any benefit from geopolitical risk as the USD firms and yields lift across the board. Action which has sent XAU below its 50- & 21-DMAs of USD 2034/oz and 2029/oz respectively.

- Base metals are pressured given the overall risk tone and USD strength with little on the docket near-term to change this narrative before the afternoon’s US data points.

- Two Ukrainian drones hit a primary oil processing facility at the Volgograd oil refinery in southern Russia.

Geopolitics – Middle East

- US and UK carried out strikes against 36 Houthi targets which included missile systems, launchers, air defence systems, radar and buried weapons storage facilities, while the UK government said this was not an escalation, according to Reuters. US Central Command also announced its forces conducted a strike on four anti-cruise missiles which were prepared to launch against ships in the Red Sea.

- Yemen’s Houthi spokesperson said the continuation of US-British aggression will not achieve any goal for the aggressors and Yemen’s decision to support Gaza will not be affected by the attacks, while the spokesperson added that Yemeni military capabilities are not easily destroyed and were rebuilt during years of tough war, according to Reuters.

- White House’s Kirby said strikes on Friday against Iran-backed groups were just the first round of action and more action will follow, according to an interview with Fox News.

- US National Security Adviser Sullivan said there will be more steps in the US response to the drone strike in Jordan and that the US would not describe it as an open-ended military campaign but added that if the US continues to see threats and attacks, they will respond to them. Sullivan also stated that Gaza humanitarian issues will be the top priority for Secretary of State Blinken on his trip and that the ball is in Hamas’ court on the hostage proposal, according to Reuters.

- Iraqi military spokesperson said US air strikes constitute a violation of Iraqi sovereignty and pose a threat that could lead Iraq and the region into dire consequences. It was also reported that the Iraqi PM denied the US had coordinated air strikes with the Iraq government and called those claims lies, while the Iraqi PM said 16 were killed including civilians and 25 were wounded in the US aggression against Iraq’s sovereignty. Furthermore, Iraq’s Foreign Ministry summoned the US Charge D’Affaires to Baghdad and handed a note of protest against US attacks in Iraq, according to Reuters.

- Iran strongly condemned the US military strikes which it said were violations of the sovereignty and territorial integrity of Iraq and Syria, while it added that US attacks represent another adventurous and strategic mistake by the US that will result only in increased tension in instability in the region. Syria’s Foreign Ministry also condemned the US attack on Syrian territory and stated that the US is fuelling conflict in the region in a very dangerous way.

- Israeli army said its warplanes bombed an operational headquarters and military infrastructure of Hezbollah in the area of the village of Yaron and they also targeted a Hezbollah observation point in the village of Maroun al-Ras in southern Lebanon, according to Al Jazeera.

Geopolitics – Other

- Ukrainian President Zelensky said he was considering replacing several officials including state leaders and in the military.

- G7 countries are reportedly drawing up plans to issue debt to help fund Ukraine using Russian assets as a backstop for the repayment, according to FT.

- South Korea summoned the Russian envoy over Moscow’s comment criticising President Yoon’s remarks on North Korea.

US Event Calendar

- 09:45: Jan. S&P Global US Services PMI, est. 52.9, prior 52.9

- 09:45: Jan. S&P Global US Composite PMI, est. 52.4, prior 52.3

- 10:00: Jan. ISM Services Index, est. 52.0, prior 50.6, revised 50.5

- 14:00: Senior Loan Officer Opinion Survey on Bank Lending Practices

DB’s Jim Reid concludes the overnight wrap

Well, that was some week we just had. To very briefly front-run our own regular full weekly recap at the end, 2yr US yields rose +16.1bps on Friday (the largest since March), a March Fed cut pricing fell to 22% (from 50% a week earlier), the Magnificent Seven rose +5.45% on Friday alone with Meta adding the most amount of daily market cap ever ($197bn), this sent the S&P 500 to a fresh all-time high even though 73% of the Russell 2000 fell on Friday, while the US Regional Bank index fell -7.23% on the week. That opening para is enough to wear anyone out.

Meta’s +20.3% increase on Friday after their results was the biggest micro story on Friday but the jobs report was also a big boost to market cap weighted indices, helping them shrug off the implications for monetary policy on smaller companies, and also the renewed Regional Bank fears.

Digging into that data, January’s strong payrolls report was driven by headline (+353k vs +185k expected) and private (+317k vs+170k expected) numbers massively beating expectations, alongside 126k of upward revisions to the prior two months. In addition, average hourly earnings surprised to the upside (+0.6% vs. +0.4%) but with a two-tenths drop in hours worked (34.1 vs. 34.3) which was the one inconsistent part of the report, even if bad weather could have been an influence. Elsewhere, the unemployment rate of 3.7% (3.8% expected) was a basis point from rounding down to 3.6%.

Fed Chair Powell wouldn’t have seen these numbers before the FOMC and before his taped interview aired last night on “60 minutes” where he indicated that the March meeting is likely too soon to have confidence in starting rate cuts. He added that the Fed will likely move at a considerably slower pace than the market expects. To be fair nothing much new here, but the confirmation that he wasn’t going to use the broadcast for a big dovish turnaround has caused 2yr and 10yr treasuries to back up 4-5bps overnight, adding to Friday’s big climb. Following this interview, there are lots of Fed speakers this week to give their take on the FOMC and payrolls. See the list in the calendar at the end.

Chinese stocks have been on a wild ride this morning with the small cap CSI 1000 down -8% at one point before halving those losses as I type. The Shanghai Composite was down over -3.5% but is now closing in on flat in a very volatile session. Small caps have been sold against large caps recently as the market views intervention as helping the larger indices. Perhaps some triggers or short covering came in to support the bounce back. This vol came even after the Chinese securities regulator (CSRC) vowed to maintain market stability on Sunday.

Elsewhere in Asia, the Nikkei (+0.52%) is outperforming with even the Hang Seng now up +0.49% after opening around -1.3% lower. S&P 500 (-0.27%) & NASDAQ 100 (-0.29%) futures are drifting lower. The impact of Treasury declines on Friday and this morning can be seen across Asian bond markets as well, with 10yr yields on Australian government debt up +12.3bps to 4.10% while 10yr JGB yields are +5bps at 0.72% as we go to press.

Early morning data showed that China’s services activity expanded at a slightly slower pace in January, as the Caixin services PMI edged down to 52.7 from 52.9 in December as new orders fell.

There’s not a huge amount of US data this week, as is usually the case post payrolls, but the highlight could be the annual BLS revisions to the seasonal factors for CPI on Friday. Both Waller (pre FOMC blackout) and Powell (at the FOMC) noted that these are an important landmark to get past before potential rate cuts can be better calibrated. Last year, these revisions lowered H1 inflation and increased H2 which changed the momentum profile of inflation.

Before we get there, today sees the services ISM (consensus 52.0) which negatively surprised a month ago (at 50.6 and below all estimates), with the employment series the lowest since July 2020 (down from 50.7 to 43.3). That clearly was completely at odds with payrolls on Friday, so we’ll find out today if that was an anomaly. Also anomalous has been the recent creep higher in initial jobless claims of late with continuous claims only having been higher for one week since November 2021. So another number to watch.

Today’s Fed Senior Loan Officer’s survey (SLOOS) should be very important but very tight bank lending in recent quarters hasn’t so far translated into reduced activity as it has done in the past. We don’t know why this is the case. It’s possible that excess savings or cash are still high enough in the economy that business and consumers don’t need much access to what would be very tight bank lending. This wouldn’t be able to carry on forever so the survey results today are still important to see if banks are becoming less restrictive after some improvements last quarter. You can find the other US data in the diary at the end.

Outside the US, China inflation numbers on Thursday are worth watching. Current estimates on Bloomberg suggest the CPI is expected to fall further into negative territory from -0.3% YoY in December to -0.5% YoY in January. The PPI is seen marginally edging higher but staying in negative territory (-2.6% vs -2.7% YoY in December). The Chinese CSI index closed at 5-yr lows on Friday so marching to a very different beat to the US at the moment.

In Europe, the focus will be on economic activity in Germany with indicators due including industrial production (Wednesday), factory orders (tomorrow) and the trade balance (today). There will also be industrial production (Friday) and retail sales for Italy (Wednesday) and trade balance data for France (Wednesday). From the ECB, investors will keep an eye on the consumer expectations survey (CES) on Tuesday and the economic bulletin will be due on Thursday.

Elsewhere earnings season soldiers on but after the mega caps from last week, the main highlights this week, which we detail in the calendar at the end, are not going to move the macro needle.

Recapping last week in more detail now, the large beat in payrolls led to a sharp sell-off in US fixed income on Friday as 10yr yields rose +14.1bps. Investors responded by paring back expectations of Fed cuts in 2024, with the expected Fed rate for December rising +21.2bps on Friday, and +9.6bps over the week. The pricing of a 25bps cut by the March meeting fell to 22%, down from 50% a week earlier and a still sizeable 38% as of Thursday despite Powell’s pushback against a March cut at Wednesday’s press conference. This sent 2yr Treasury yields +16.1bps higher on Friday, their largest rise since last March. 2yr yields were up a marginal +1.6bps over the week after their earlier decline amid renewed concerns over the US regional banking sector. 10yr yields were down -11.6bps over the week to 4.02%. The dollar rallied off the prospect of a higher terminal rate, with the dollar index up +0.85% on Friday (+0.47% over the week).

Even as Treasuries sold off, the S&P 500 rallied +1.07% on Friday, and +1.38% in weekly terms. However, less than half of S&P 500 companies were actually up on Friday with gains led by tech megacaps as the Magnificent Seven index rose +5.45% (+4.87% on the week) after earnings from Meta, Amazon, and Apple the evening before. Meta posted a stunning +20.32% rise on Friday, with the $197bn rise in its market cap being the largest daily gain on record for any company. Amazon also gained a strong +7.87% on Friday. The NASDAQ rose by a more moderate +1.74% (+1.12% over the week). On the other hand, the US regional banking index slumped last week, falling -7.23% (+0.20% on Friday) after shares for the New York Community Bancorp dropped -42.03% (+5.04% Friday).

Equity markets were muted elsewhere in the world. The STOXX 600 traded flat on the week (+0.02%), whilst the German DAX and French CAC retreated -0.25% and -0.55%, respectively. In Asia, Chinese equities were very weak last week driven by property sector woes following the court decision to liquidate Evergrande. The Shanghai Comp fell -6.19% (and -1.46% on Friday), its largest weekly decline since October 2018. The CSI 300 slipped -4.63% (and -1.18% on Friday) to 5-yr lows, and the Hang Seng also retreated -2.62% (and -0.21% on Friday).

Lastly, in commodities, crude retreated after Exxon and Chevron announced their second-largest annual profits in a decade despite a fall in oil prices, alongside strong supply from the Permian Basin. This added to the bearish narrative that had begun earlier in the week after data showed that some OPEC+ members may be pumping above their agreed limits and amid reports that we could be getting closer to a cease-fire deal in Gaza. Brent crude futures retreated -7.44% (and -1.74% on Friday) to $77.33/bbl, and WTI crude fell -7.35% (and -2.09% on Friday), the worst weekly slump since October.