In recent years, we have cited several reports, including a Reuters report from late January, explaining how Tesla Motors was preparing to debut a mass-market electric vehicle for under $25,000.

According to a new Reuters report, citing “three sources,” Tesla has canceled plans for a “long-promised inexpensive car that investors have been counting on to drive its growth into a mass-market automaker.” Instead, Tesla plans to focus on “developing self-driving robotaxis on the same small-vehicle platform,” the sources said.

Tesla shares tumbled as much as 5% on the report.

So far, shares have slid 34% on the year.

Short interest also jumped from 80 million shares to 102 million shares from mid-January. Current Bloomberg data shows that about 3.69% of the float is short.

Elon Musk repeatedly told investors that Tesla planned to start producing an affordable model at its Texas factory next year. This was detailed in a Reuters report earlier this year.

Sources said in the earlier report that the new mass-market EV would be a “compact crossover” that would compete with cheaper petrol-powered cars and inexpensive Chinese EVs, such as those made by BYD.

Tesla’s Model 3 sedan is the cheapest EV the automotive company offers at $39,000 in the US. Tesla initially planned for the affordable EV, dubbed Model 2, to start around $25,000.

Two Reuters sources said they heard about the plan to scrap the Model 2 in meetings attended by employees, one of which occurred in late February.

“Elon’s directive is to go all in on robotaxi,” that person said.

Another source with knowledge of Tesla’s plans said that pivoting away from the Model 2 strategy for robotaxis is a good idea. They cautioned that Tesla’s product changes could be altered again based on economic conditions.

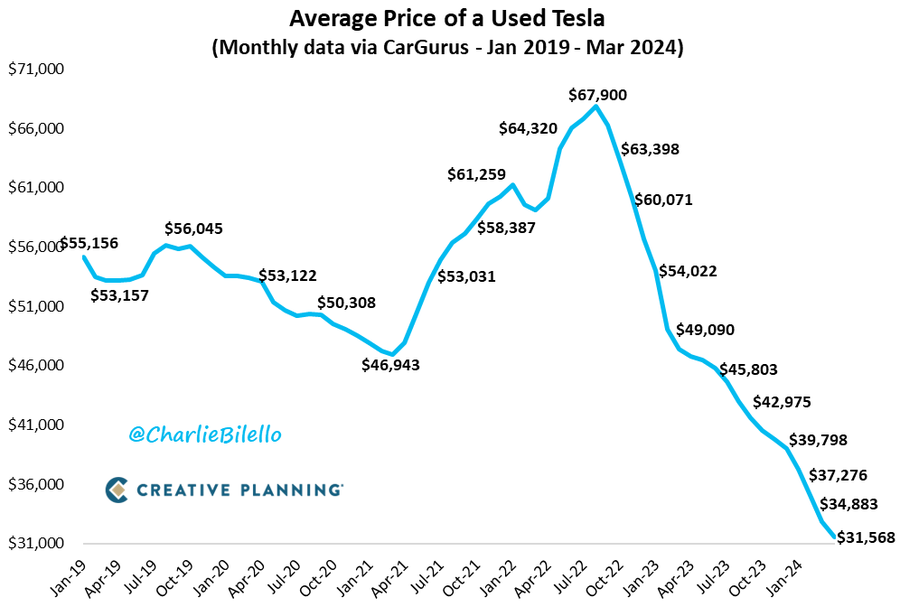

Tesla’s delay of the Model 2 comes as the average price of a used Tesla has been more than halved since peaking at $67,900 in late 2022.

Meanwhile, the Xiaomi SU7 EV launch was a huge success in China as the Chinese company took on Tesla.

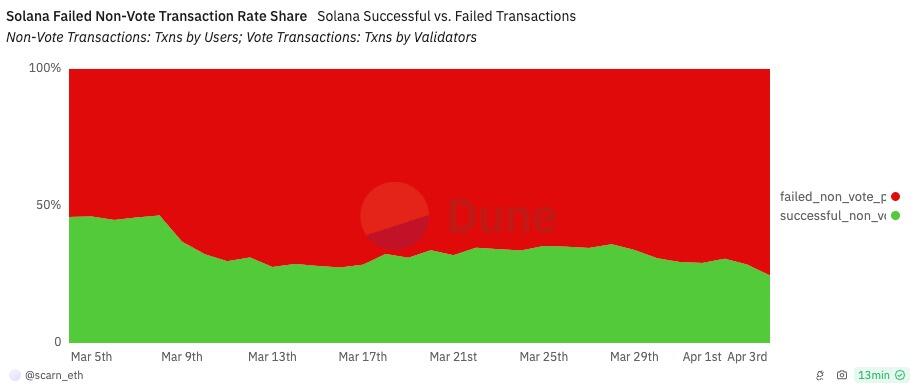

The Solana network appears to be struggling to keep up with a ravenous demand for memecoins, with data showing roughly 75% of transactions on the network currently failing.

Roughly three-quarters of all transactions on the Solana network have been failing amid a deluge of activity brought by the recent memecoin mania on Solana; however, proponents say the data is being widely misinterpreted.

Dune Analytics data shows that on April 4, just over 75% of all “non-vote” Solana transactions failed, the highest failure rate on record.

75.4% of non-vote transactions on Solana have failed. Source: Dune Analytics

The uptick has been paralleled by a recent uproar from Solana users on social media, complaining of failed transactions and degraded user experience.

In an April 4 post to X, pseudonymous trader Altcoin Sherpa said that while he still believed Solana would cement itself as the blockchain network for retail adoption, he noted that the current user experience was currently less than ideal.

“As much as I think that SOL is the chain for retail this cycle — the experience is f—ing brutal lately.”

Or maybe it’s bot spam

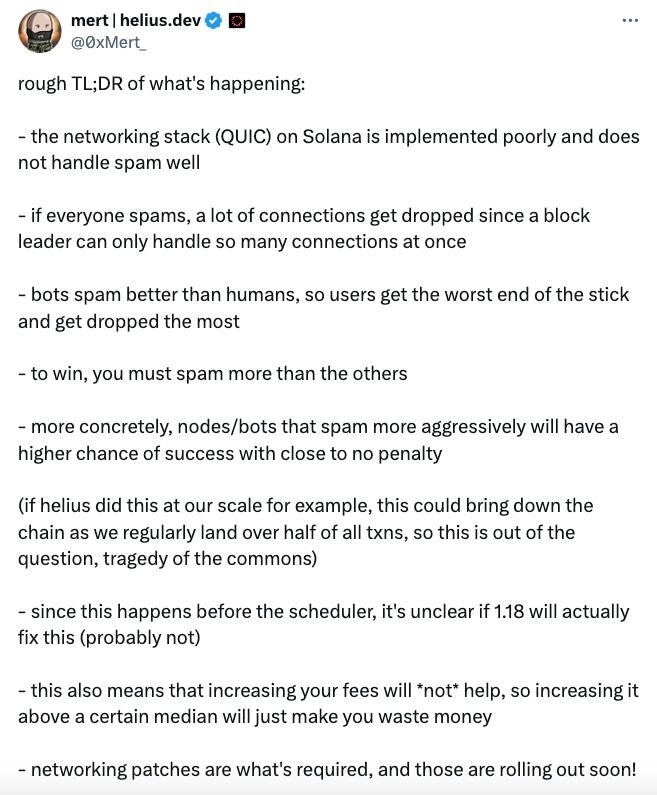

However, in an April 4 post to X, vocal Solana proponent and Helius CEO Mert Mumtaz took issue with the claim that 75% of transactions were failing, noting that the vast majority of failed non-vote transactions were simply “bot spam.

“This is usually not a big problem for users because your wallet will simulate the [transaction] and let you know that it will not work beforehand anyway,” he said.

Mumtaz claimed that the failed transactions chart was “not a good way of assessing user impact as most users don’t make it there to begin [with].”

“About 95% of that entire chart is just bots failing arbitrage attempts,” he added.

Additionally, Mumtaz explained that because much of this spam activity occurs before the scheduling process, increasing transaction priority fees won’t help and that “increasing it above a certain median” will see users “waste money.”

He added that it was unlikely that the upcoming 1.18 Solana network upgrade would fix these issues, hinting that user experience on Solana could remain degraded for some time.

“Networking patches are what’s required, and those are rolling out soon.”

Solana CEO Anatoly Yakovenko took to social media to express his frustration at the process of improving congestion bugs on the network.

“Dealing with congestion bugs sucks so much more than total liveness failure. The latter is one and done, bug is identified and patched and chain continues. The former has to go through the full release and test pipeline. Shipping fast is impossible,” wrote Yakovenko in an April 5 post to X.

The price of Solana’s SOL has fallen around 3% in the last week, stumbling slightly after a 45% rally in the last month. Its recent weekly drawdown has seen it fall back to being the fifth-largest cryptocurrency by market capitalization, per CoinGecko data.

SOL currently commands a total value of $81 billion, trailing behind Binance’s BNB at $89 billion.

The former bodyguard of Sean ‘Diddy’ Combs’ claims the music mogul had blackmail tapes of politicians, princes and other prominent individuals who were involved in his sex parties.

Combs, who has been hit with a barrage of physical abuse, rape and sexual trafficking allegations, had his homes in Miami and Los Angeles raided by the Department of Homeland Security last month, during which federal agents seized computers and other electronic devices.

Gene Deal, who was present the night when Notorious B.I.G. was fatally shot in 1997, made the sensational comments during an interview with ‘The Art of Dialogue’ YouTube channel.

NEW: Diddy’s former bodyguard Gene Deal suggests that Diddy may have tapes of politicians, princes and even preachers which could now be in the hands of the feds.

“I don’t think it’s only celebrities gonna be shook. He had politicians in there, he had princes in there. He also… pic.twitter.com/hheJPwrKMe

“I don’t think it’s only celebrities gonna be shook. He had politicians in there, he had princes in there. He also had a couple of preachers in there,” said Deal.

“Can you imagine, he had every room bugged,” he added.

When asked why Combs’ media department had stayed silent on the allegations against him, Deal responded, “Either they took part in some of the stuff that happened, or they’re scared that it may mess up their brand.”

Fox News host Jesse Watters speculated that the tapes, if they exist, are now in the hands of the feds and “that’s a lot of blackmail.”

Deal’s comments echo those of rapper Rodney ‘Lil Rod’ Jones, who claimed Combs had hidden cameras throughout his home to record sex tapes involving celebrities during his “freak off” parties.

Combs has denied all the allegations against him and hasn’t been hit with any criminal charges as of yet.

* * *

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

About as good as it gets for the economy, not so good for Fed cuts.

Not only were the headline jobs better than the top estimates on Bloomberg (303k jobs). We also revised prior job reports up by 22k.

Wages are doing reasonably, with monthly wages coming in 0.3%.

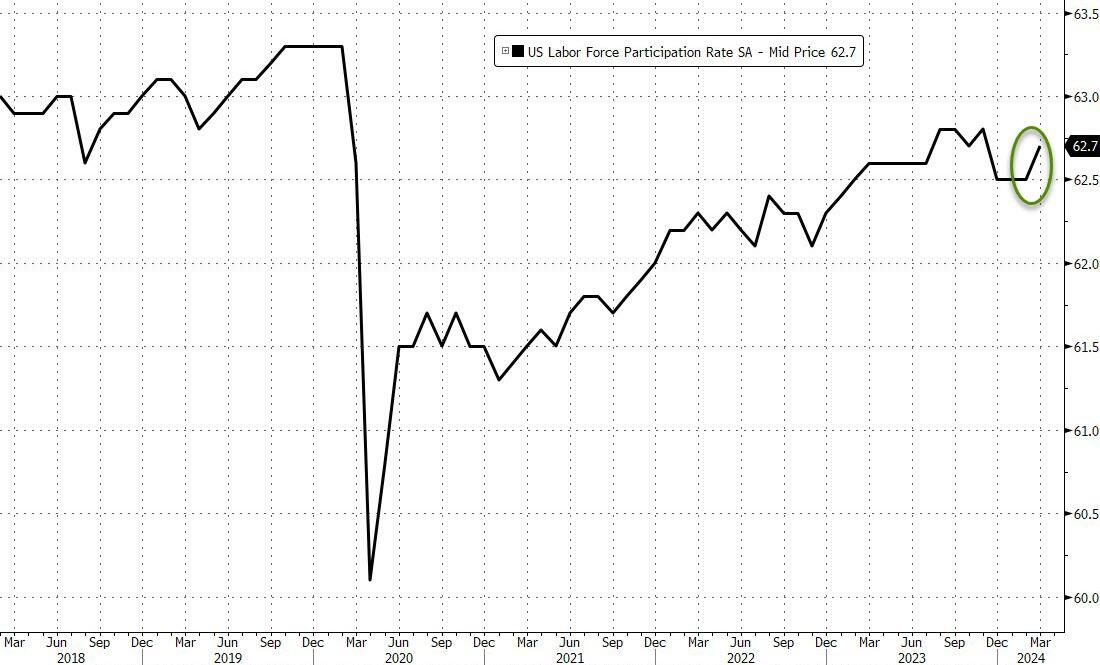

What is most impressive to me is the unemployment rate coming down to 3.8%. That occurred while participation rate increased nicely. At 62.7%, it is just a smidge below the post covid high of 62.8%. The Household Survey (which is used for unemployment) added 498k jobs!

Definitely not “goldilocks” for the Fed, but good for the economy.

Yields should rise a bit and curves should be less inverted.

Stocks should probably react slightly negatively to the report as yields rise. But offsetting that yield rise is the sheer strength of the economy and the fact that the consumer should be in good shape.

What Does MOAB Have to do with Anything?

Nothing and everything. MOAB or Mother Of All Bombs isn’t front and center but Escalation and Expansion is. Thursday’s big drop in stocks was precipitated by fears that Iran was preparing to attack Israel. Part of why stocks were higher overnight and are still strong post NFP is because nothing happened overnight in terms of escalation and expansion (you can see that in oil too, which is hovering around unchanged).

We dealt with our thoughts on Hedging Geopolitical Risk at the start of the year and remain convinced of two things:

Long energy and energy stocks is the best hedge, since we like that sector already for a variety of reasons, and the next potential shoe to drop, would be cracking down on Iran’s 3.5 million barrels of oil being sold daily.

Flight to safety is unlikely to work well. Yes, on Thursday afternoon, bonds showed a “flight to safety” trade, but I suspect that will be short lived, because the rising cost of oil and the realization that globally, deficits will rise to increase military spending, will weigh on bond yields, especially out the curve.

Make no mistake, the global Game of Chicken continues, and in my analysis, the “enemy” sees weakness and thinks we will veer.

So, once the market is done digesting the payroll data (which was truly exceptional), look for risky assets to trade poorly (lower stocks and wider credit spreads).

I think enough support has been broken on the longer end of the yield curve (and most people seem bullish bonds) that we could see that crack, especially if oil does gap higher.

The talk from the start of the year has been about Geopolitical Risk, it is definitely time to act and not just talk as the risk of clear and present danger is very high at the moment.

So, for me, MOAB as a euphemism for the geopolitical risk outweighs the NFP report today.

Samsung To Double Chip Factory Investments In Texas As Chips Act Supercharges Reshoring Efforts

The Biden administration’s fast approach to industrial policy and re-shoring of semiconductor production has been through the Chips and Science Act.

The United States is progressing down the path of rebuilding its semiconductor manufacturing base after the Biden administration awarded $8.5 billion in grants and $11 billion in loans to tech giant Intel last month to build the next generation of manufacturing facilities across several states.

A new report from The Wall Street Journal, citing “people familiar with the matter,” revealed South Korean tech giant Samsung Electronics is planning to double its total semiconductor factory investment in Texas to a whopping $44 billion.

Samsung is already building a semiconductor hub in Taylor, Texas. The new investments will include a new chip-making factory plus a facility for advanced packaging and research and development.

The people said Samsung plans to announce the mega-investment in Texas on April 15. They expect the Biden administration to hand the company billions of dollars in subsidies from the Chips Act to support the efforts.

“Samsung’s additional investments add to the $17 billion that the company had previously committed more than two years ago to Taylor, located just outside of Austin, for a cutting-edge chip-making plant,” WSJ pointed out.

The second Taylor-based chip factory is estimated to cost around $20 billion, the people said, adding the company’s research and development efforts are expected to be warehoused inside the new plants.

Samsung is only one of three firms, including Taiwan Semiconductor Manufacturing and Intel, capable of producing advanced logic semiconductors for national defense and artificial intelligence. The re-shoring effort under the Chips Act is an effort to mitigate China’s influence on US supply chains.

At the current rate, Commerce Secretary Gina Raimondo recently said the Chips Act is allowing the US to capture about 20% of the world’s most advanced logic chips production by 2030. As a reminder, the US once had 37% of the world’s chip production in 1990 and has since plummeted to about 12% in recent years due to the West’s globalist leaders who offshored America’s manufacturing capacity. It’s time to bring the production back as the world fractures into a dangerous multi-polar state.

Recently released Jan. 6 U.S. Capitol Police security video shows a suspected FBI special agent clapping and cheering as crowds surged up steps to the Columbus Doors and another meeting with an FBI tactical team just before it entered the Capitol after the fatal shooting of Ashli Babbitt.

The videos were first identified by defendant William Pope of Topeka, Kansas, in court filings in his own Jan. 6 criminal case. Exhibits Mr. Pope originally filed under seal have become public since the release of thousands of hours of Jan. 6 security video by the Committee on House Administration Subcommittee on Oversight.

Two possible FBI special agents and a third unknown colleague were with John D. Guandolo, the FBI’s former liaison with U.S. Capitol Police, at the Women for a Great America event on the East Front of the Capitol on Jan. 6, 2021, according to Mr. Pope.

In sworn testimony in a December 2022 Alaska civil court trial and in numerous media appearances, Mr. Guandolo said he was with two FBI special agents and a colleague with whom he traveled to Washington on Jan. 6. Mr. Guandolo has indicated that he was also introduced to other FBI personnel at the Capitol that day.

Mr. Pope is seeking to compel federal prosecutors to identify them all. He said even if the men were at the Capitol on personal time, their free movement around the grounds shows they did not believe the Capitol was off limits to the public.

Mr. Guandolo, who handled counterterrorism and criminal investigations for nearly 13 years—from 1996 to 2008—as an FBI special agent, has said he was at the Capitol in a personal capacity and went primarily to pray.

He was interviewed by the FBI about his Jan. 6 visit on July 6, 2022. A heavily redacted copy of the FBI 302 interview summary has been made public.

‘This Is Huge’

Security video shows that as the crowd broke through the police line on the East Plaza and surged up the steps to the Columbus Doors, one of Mr. Guandolo’s colleagues clapped enthusiastically.

“Oh, oh, oh man, this is huge,” the man said, heard on Mr. Guandolo’s cell phone video that showed the crowd ascending the east steps.

On Capitol Police security Camera 7231, which looks out at the House Egg on the East Front, Mr. Guandolo was seen filming while standing on a chair just before 2:05 p.m. The clapping man, wearing a grey knit cap and dark coat, is identified in Mr. Pope’s court filing as “the Clapper” and “Colleague 2.”

While Colleague 2 cheered the protesters’ advance on the Capitol, a man on Mr. Guandolo’s left, “Colleague 1,” had his phone raised, presumably capturing his own video of the advancing crowd. He wore a brown knit cap and blue jacket, and carried a backpack, video showed.

Mr. Pope asked U.S. District Judge Rudolph Contreras to compel the Department of Justice to identify all FBI agents “who were material witnesses at the Capitol.” Mr. Pope wants the FBI “to produce all photographs, videos, and records related to their presence.”

The DOJ has filed opposition to Mr. Pope’s motion, saying it has “no obligation to investigate” who the men in the videos are.

Some of the exhibits in Mr. Pope’s Feb. 12 motion were redacted, but the recent release of thousands of hours of Jan. 6 security video by the Subcommittee on Oversight allows them to be released publicly, Mr. Pope said.

Capitol Police security video shows Mr. Guandolo, Colleague 1, and Colleague 2—often trailed by a third unidentified man, “Colleague 3”—moving about the Capitol grounds.

“For the record, my friend and colleague with me for most of the day on January 6th was not working,“ Mr. Guandolo told The Epoch Times in an April 2 email. ”He was there with his family to experience the event like most of us.”

Subsequently asked to clarify which of the men shown on CCTV he was referring to, Mr. Guandolo did not reply before press time.

“The other FBI guys I saw there I cannot speak about their capacity that day,” Mr. Guandolo added.

Mr. Guandolo said he testified for the defense in the criminal trial of Jan. 6 defendant Rebecca Lavrenz on March 29 and has been “asked to testify in several upcoming cases.”

Mr. Guandolo said his statements about Jan. 6 have been “very public and very clear.”

“There was an insurrection and revolution, and it was not done by the participants of January 6th but by senior government officials of the U.S. government,” he said.

‘Right to Be There’

The video from Mr. Guandolo and security cameras “also indicates that active-duty FBI agents perceived events at the Capitol to not be criminal,” Mr. Pope wrote in his motion. “From the clapping and celebratory expression we can conclude that these FBI agents were in favor of people accessing the building and that they believed the people had a First Amendment right to be there.”

At 2:28 p.m., Camera 7202 captured footage of Colleague 2 walking across the East Plaza and climbing the House steps. He stopped to shoot video or photos just a few feet from a group of Capitol Police officers, the video showed.

He appeared to be filming or photographing a group of five—two young men and three young women or teens—standing about a dozen steps above him. The five then descended the stairs and walked off camera with Colleague 2.

The group of five young adults was also seen walking immediately in front of Mr. Guandolo and his three colleagues on the House Plaza Egress—Camera 0811—at 2:55 p.m. and on Camera 0681 on the Southwest Walk at 2:57 p.m., video shows. One of the young adults carried on a conversation with Colleague 2 during part of the walk.

“Since this FBI Agent has professional law enforcement training, and since he found it permissible to walk up on the steps while three Capitol Police officers looked on nearby … it is reasonable for me to conclude that this FBI agent will provide favorable testimony about the permissive actions of police that is likely to sway a jury away from a determination of guilt,” Mr. Pope wrote.

At 2:32 p.m., an FBI tactical team drove onto the East Plaza in an MRAP (Mine Resistant Ambush Protected) vehicle. After the dark green vehicle was parked, Colleague 1 came from the area of the Women for a Great America event, walked around the front of the vehicle and spoke to someone inside the front passenger door for approximately five minutes, video showed.

“This could indicate that FBI Colleague 1 was indeed on the clock at the Capitol on January 6, or that the uniformed FBI SWAT team did not consider the events at the Capitol to be a pressing matter and that they had time to shoot the breeze with an off-duty FBI colleague,” Mr. Pope wrote.

Members of the FBI SWAT team were seen on security video entering the South Door of the Capitol just before 2:50 p.m. They immediately turned right down a side hallway and helped Capitol Police carry a mortally wounded Ms. Babbitt, who’d been shot outside the Speaker’s Lobby minutes earlier.

Ms. Babbitt was set on the floor near the south entrance and emergency care was provided by FBI medics and Capitol Police until paramedics from the District of Columbia Fire and EMS Department took over.

At about 2:55 p.m. Camera 0948 on the southeast roof of the Capitol showed Mr. Guandolo and his three colleagues walking away from the east steps. Camera 0811 on the House Plaza Egress sidewalk showed the men walking past just before 2:56 pm. Mr. Guandolo looked to his right and appeared to be speaking to someone just before he disappeared from view, Mr. Pope wrote.

A few seconds later, a man known only by the hashtag #FenceCutterBulwark walked into view from the opposite direction. The identity of #FenceCutterBulwark has been a longstanding mystery after he was shown on public video cutting down the green plastic security fencing erected by Capitol Police to keep crowds away from the Capitol.

Mr. Guandolo told The Epoch Times, “I do not know #FenceCutterBulwark.”

While he was carrying out his fence destruction, #FenceCutterBulwark was filmed by Metropolitan Police Department undercover officer Ryan Roe, who said to him, “Appreciate it, brother.”

A man claiming to be #FenceCutterBulwark appeared on the Patriot Punk Network podcast in September 2023, saying he was not a provocateur or a federal informant, and did not know Officer Roe.

“If he said, ‘Thanks, brother,’ then our, I’m assuming our exchange would have been, you know, me just basically saying, ‘Hey, I’m just trying to get this out of the way. It’s a hazard. It’s dangerous, or whatever. I don’t want people getting hurt,’” the man told Patriot Punk host Chase Matheson.

Mr. Pope has petitioned Judge Contreras to order the release of video shot by all members of the Metropolitan Police Department Electronic Surveillance Unit (MPD ESU) who captured video on Jan. 6 using cell phones, camcorders and GoPro cameras.

Nearly 30 ESU officers were assigned for duty on Jan. 6, organized into eight teams. Some of the men used their phones to live stream to the MPD command center, according to court records.

One of the undercover officers allegedly acted as a provocateur in the crowd on the Northwest Steps, according to previous court filings by Mr. Pope.

Officer Nicholas Tomasula confirmed in an interview with defense attorneys in the Proud Boys case that he was heard on Jan. 6 video chanting, “Whose House? Our House!” and “Stop the Steal!”

Mr. Tomasula was identified as “Officer 1” in Mr. Pope’s February 2023 motion seeking to make Officer 1’s undercover video public.

At the foot of the Northwest Steps, as a protester climbed up a makeshift ladder onto the balustrade, Mr. Tomasula shouted: “C’mon, man, let’s go! Leave that [expletive],” his video showed. Mr. Tomasula got help from a protester climbing onto the balustrade, then shouted to protesters moving up the steps, “C’mon, go, go, go!”

Mr. Pope said that Mr. Tomasula was not alone in encouraging protesters on Jan. 6.

“MPD’s internal investigation on Tomasula and my own research has identified that other undercover MPD officers were, in real time, praising protesters who broke windows at the Capitol and thanking persons who removed fencing,” he wrote in a motion on Aug. 21, 2023.

Mr. Guandolo and his three colleagues were seen on two security cameras on the southwest drive, passing by at 2:57 p.m.

“It is significant that there were several agents present. The testimony of these FBI agents who believed it was acceptable to be in this alleged restricted area will weigh favorably on the minds of the jury against any contrary testimony brought by the government,” Mr. Pope wrote.

“For this reason, the court should compel the government to identify all FBI agents who directly witnessed events at the Capitol since the exculpatory testimony of many, many agents will lend strength in numbers to my defense.”

It’s not some AI sensor system, or even a newfangled airbag.

Nope. In the minds of literally several hundred lawmakers (from both parties!) the most essential safety feature that should be in your vehicle is… AM RADIO!

The “technology” behind AM radio is so old it even predates Joe Biden. In fact it almost predates the automobile itself.

But while the automobile has undergone tremendous evolution over the past 100+ years, AM radio is still essentially the same as it was back during the first broadcast on Christmas Eve, 1906: fuzzy and low quality.

Perhaps that’s why most consumers abandoned AM radio long ago, ditching it for FM, then satellite, and now streaming.

So few consumers listen to AM radio that many cars don’t even come equipped with it anymore; for manufacturers, it’s not worth spending on a part that consumers don’t want.

And for some cars— specifically electric vehicles— AM radios can cause dangerous interference with sensitive electronic components… so some EV manufacturers have removed analogue AM receivers to make their vehicles safer.

Of course, consumers who really want to listen to AM radio programs can always subscribe to digital AM streaming services.

But that’s not good enough for politicians who have a history of ignoring what US consumers want. If you’re not interested in AM Radio, well too bad. AOC and Joe Biden are going to decide for you.

The “AM Radio for Every Vehicle Act” was first introduced in Congress last May to force every vehicle manufacturer to include an analog AM radio receiver.

Their entire reasoning was captured in just a single line:

“AM broadcast stations are often used to deliver emergency alerts and news and entertainment programming; some newer vehicles do not include AM equipment”

Is it 1955? When was the last time that anyone received an emergency alert on AM radio? Totally nuts.

Fortunately the bill went absolutely nowhere at first.

But bad legislative ideas are like cockroaches. They never actually die. They linger forever and multiply until they eventually take over the House.

Fast forward nearly a year later, and it turns out that 47 Senators and 237 Representatives have signed on in support of the deal.

And Joe Biden (probably the only guy in America who still listens to AM radio) is ready to sign it. It’s almost assured to become law.

Now, this is not the most destructive legislation in US history. In fact the main consequence of the AM radio mandate is that vehicles will cost a bit more.

But it does provide hilarious insight into their short-sighted thinking… if they’re even capable of thinking at all.

Remember, about a week ago, the Biden administration decreed that 50% of all new cars sold in the US by 2030 will have to be electric vehicles (even though only 8% of consumers choose to buy them today).

But wait— AM radio produces dangerous interference for in sensitive EV components, making electrical vehicles LESS SAFE.

So this AM radio bill, which aims to make people more safe, will actually make Electric Vehicles less safe. And Mr. Biden has decreed that at least half of Americans will be driving these less safe EVs in six years.

You just can’t make up this level of stupidity.

There’s a common line of thinking these days that the people in charge are deliberately trying to destroy America.

Well, with such idiotic and conflicting mandates, it’s getting harder to ignore that conclusion.

Politicians are forging ahead with idiotic priorities as if the country isn’t barreling towards the edge of a cliff.

They’re doing nothing about the border. Nothing about the budget deficit. Nothing about Social Security. Nothing about decline of America’s military power. Nothing about the dollar’s rapid loss of credibility. Nothing about the mountain of regulations that debilitate economy productivity. Nothing about preventing World War III.

But hey, when it comes to the REALLY important issues like AM radio, these ‘leaders’ really get down to business.

And by the way, the AM mandate is a bipartisan bill.

Republicans are in favor because there are plenty of conservative talk shows on AM radio.

Democrats are in favor because they use AM radio to reach Spanish speaking voters.

Never mind what’s good for the country, or good for producers, or good for consumers. Congress has its own agenda.

This should come at no surprise; with an abysmal 12% approval rating, everyone seems to know how terrible Congress is.

Yet, quite bizarrely, 96% of incumbents were reelected to Congress in 2020. So voters seem to agree that Congress is terrible. But it’s apparently all the other Congressmen who are incompetent. Their guys is doing a great job.

This is why I have such little confidence that politicians will turn this ship around; voters keep sending the same people to Washington… who have once again proven that they are totally out of touch with America’s priorities.

This is the most critical point to understand: politicians are most likely not going to solve the problems that they themselves have created.

And yet there are solutions that each of us, as individuals, can use.

If the Inspired Idiots are bent on engineering higher energy prices and higher inflation, there are ways we can reduce those consequences and even benefit financially.

If the Inspired Idiots are going to raise taxes through the roof, there are completely legitimate ways to reduce those as well.

If the Inspired Idiots are going to bankrupt Social Security (which the program itself anticipates within a decade), there are ways to structure a robust retirement account to offset the impact.

Whatever destruction they come up with, there are ways around it. It just takes a little bit of education and the will to take action.

Mainstream Media Reluctantly Admits Elon Musk’s Ukraine Takes Are Proving Correct

“So, Musk may not be too wide of the mark after all”: Politico. Something which could hardly be imagined a year ago or even six months ago has happened this week: a Politico op-ed voices agreement with Elon Musk on Ukraine.

Of course, the Wednesday piece still takes customary shots at the “wayward” billionaire and owner of X:

Wayward entrepreneur Elon Musk’s latest pronouncements regarding the war in Ukraineset teeth on edge, as he warned that even though Moscow has “no chance” of conquering all of Ukraine, “the longer the war goes on, the more territory Russia will gain until they hit the Dnipro, which is tough to overcome.”

“However, if the war lasts long enough, Odesa will fall too,” he cautioned.

Statements like these, and Musk’s supposedly ‘alternative’ view of the crisis in general, have long invoked the wrath of mainstream media pundits. Yet publications like Politico now sing a different tune, but only after President Zelensky himself has signaled just how dire the battlefield situation actually is for his forces.

Politico has previously featured headlines like‘Elon Musk Is Transmitting a Message for Putin’. Musk in his recent Odesa commentary did no such thing, but merely urged the Ukrainians to find a way forward towards peace at the negotiating table before it’s too late.

Again, lines such as the below coming out of the heart of the media establishment would have been impossible to come across a year ago… from Politico:

With a history of urging Ukraine to agree to territorial concessions — and his opposition to the $60 billion U.S. military aid package snarled on Capitol Hill amid partisan wrangling — Musk isn’t Ukraine’s favorite commentator, to say the least. And his remarks received predictable pushback.

But the billionaire entrepreneur’s forecast isn’t actually all that different from the dire warnings Ukrainian President Volodymyr Zelenskyy made in the last few days. According to Zelenskyy, unless the stalled multibillion-dollar package is approved soon, his forces will have to “go back, retreat, step by step, in small steps.” He also warned that some major cities could be at risk of falling.

But we should point out that Musk has been a realist from the start, more in line with analysts such as John Mearsheimer, voicing positions which have proven right time and again, despite contradicting the bandwagon mainstream consensus at every turn.

And here’s the kicker in the conclusion, from the Politico op-ed…

“We don’t only have a military crisis — we have a political one,” one of the officers said. While Ukraine shies away from a big draft, “Russia is now gathering resources and will be ready to launch a big attack around August, and maybe sooner.”

So, Musk may not be too wide of the mark after all.

Of course, it’s more convenient at this moment to make such admissions. To review, not only has last summer’s Ukrainian counteroffensive been universally acknowledged as a failure, but more grim developments for Kiev have emerged just this week, seen in some of the following fresh headlines:

Zelensky Signs Law Lowering Conscription Age to 25

Ukraine loses 80,000 soldiers since January, Kremlin claims

Ukraine losing so many troops can’t retrieve bodies, soldier says

Elon Musk says “the longer the war goes on, the more territory Russia will gain.”

“Ukraine tragically wasted the lives of soldiers by attacking a larger army with deep defenses, minefields and more powerful artillery, while lacking armor and lacking air superiority! Any fool… pic.twitter.com/gz3JIF4WH2

Yet still, Washington is pressing forward (or rather throwing more Ukrainian troops to needless, tragic slaughter by promising things it can’t deliver), with US top diplomat Antony Blinken on Thursday saying from Brussels…

“Ukraine will become a member of NATO. Our purpose at the summit is to help build a bridge to that membership” — in reference to NATO’s annual meeting set for July. Sadly, things are set to get bloodier and more unpredictable, raising the spectre of a WW3 scenario, before they get better.

If a formula spits out a number you don’t like, just change the formula so you get a better number!

That’s exactly what the Bureau of Labor Statistics did to the Consumer Price Index formula in the 1990s. Because the CPI kept indicating price inflation was too high, the BLS tweaked the formula to spit out a lower inflation number.

Now the International Swaps and Derivatives Association (ISDA) is trying to talk the Federal Reserve into changing the formula for the supplementary leverage ratio (SLR) to make bank balance sheets look better.

This proposal sends some alarming messages about the stability of the banking system and confidence in U.S. government debt.

What Is the SLR and Why Do They Want to Change It?

The SLR is calculated by dividing the bank’s tier 1 capital (capital held in a bank’s reserves and used to fund business activities for the bank’s clients) by all assets on the bank’s balance sheet, including U.S. Treasuries and deposits at Federal Reserve Banks.

Banks use the SLR to calculate the amount of equity capital they must hold relative to their total leverage exposure. Regulations imposed after the 2008 financial crisis require category I, II, and III banks to maintain an SLR of 3 percent. “Globally Systemically Important Banks” are required to keep an extra 2 percent SLR buffer.

During the pandemic, the Fed temporarily altered SLR requirements, allowing banks to exclude Treasuries and reserves from the formula’s denominator. This made it easier to maintain the required SLR ratio.

As a Federal Reserve note explained, the banking system “exhibited considerable strains” during the reign of COVID-19. As the pandemic unfolded and governments began shutting down economies, banks quickly liquidated risky assets and increased their cash holdings. This resulted in a “sharp increase in bank deposits.”

According to the Fed note, “The associated rise in the overall balance sheets had the potential of causing their tier 1 capital levels to fall below the amount required by the SLR, which could have resulted in banks limiting their provision of financial services.”

To provide some relief, the central bank made temporary changes to the SLR formula effective April 1, 2020. The emergency rule allowing banks to exclude U.S. Treasuries from the calculation expired a year later.

In a letter addressed to the Federal Reserve, along with the FDIC, and the Office of the Comptroller of Currency, the ISDA urged these government agencies to make that “temporary, emergency” rule change permanent.

“To facilitate participation by banks in U.S. Treasury markets—including clearing U.S. Treasury security transactions for clients—the Agencies should revise the SLR to permanently exclude on-balance sheet U.S. Treasuries from total leverage exposure, consistent with the scope of the temporary exclusion for U.S. Treasuries that the Agencies implemented in 2020.”

The proposed rule change would allow banks to exclude both “on-balance sheet U.S. Treasuries that a bank holds in inventory or as part of its liquidity portfolio, as well as U.S. Treasuries the bank has received in a repo-style transaction to the extent the bank records the U.S. Treasuries on its balance sheet.”

This raises a question: does this indicate that the banking system is under “considerable strain?”

What Would a Change to the SLR Mean in Practice?

According to the ISDA, the change would “promote the stability of the U.S. Treasury market.” The organization also said it would more broadly “help support market liquidity in the context of projected increases in the size of the U.S. Treasury market and the importance of bank participation in the market.”

From a practical standpoint, it would incentivize banks to buy and hold more U.S. Treasuries by allowing them to hold them on their balance sheet without impacting their SLR. This would be good news for the U.S. Treasury Department, given that is selling billions of dollars in Treasuries every month to cover the massive government budget deficits.

The impact would be similar to quantitative easing.

In effect, the proposed change in the SLR would boost demand for Treasuries, driving prices higher and interest rates lower than they otherwise would be. Given the impact of Treasury yields on the broader bond market, it would also likely push other borrowing costs lower.

It would also enable banks to lend more money than they otherwise could under the current SLR scheme. This is a form of money creation and would have an inflationary effect.

European Investment Bank senior policy analyst Antonio Carlos Fernandes called this proposal “alarming.”

In an article published by Medium, Fernandes identifies several reasons banks would love to adjust the SLR requirements to exclude U.S. Treasuries.

Treasuries are generally considered “risk-free” assets because they are backed by the “full faith and credit” of the U.S. government. The proposal to exclude them from the leverage ratio requirement implies banks perceive them as more risky. This could “potentially undermine confidence in U.S. government debt.”

The SLR is intended to backstop risk-based capital requirements and to ensure banks don’t become overleveraged, even with “safe” assets. The carveout for Treasuries would weaken these protections.

The formula change would incentivize banks to load up on U.S. Treasuries. Fernandes called this a “concentration of risk” that would “heighten the interconnectedness between the banking system and government debt, posing systemic risks.”

The request to exclude Treasuries from the SLR could signal “broader anxiety” about the U.S. fiscal situation and government debt levels. Given the spending problem in Washington D.C., this anxiety is certainly justified.

Fernandes summed up the situation this way:

“Any perception that banks require special exemptions for holding U.S. government debt could shake global confidence in Treasuries as a safe haven asset and could impact the status of the U.S. dollar.”

Trouble in the Banking System?

This proposal also casts doubt on the notion that the banking system is “sound and resilient.”

A year ago, rising interest rates precipitated a banking crisis kicked off by the collapse of Silicon Valley Bank. The Fed managed to paper over the problem with a bailout program.

Through the Bank Term Funding Program (BTFP), banks, savings associations, credit unions, and other eligible depository institutions were able to take out short-term loans (up to one year) using U.S. Treasuries, agency debt, mortgage-backed securities, and other qualifying assets as collateral.

Instead of valuing these collateral assets at their market value, banks were able to borrow against them “at par” (Face value). It would be like the bank extending you a second mortgage based on the original value of your house after a flood caused significant damage. Normal people would never get this kind of sweetheart deal.

The BTFP was set up to address a specific problem that took down Silicon Valley Bank and two other financial institutions.

SVB went under because it tried to sell its undervalued bonds to raise cash. The plan was to sell the longer-term, lower-interest-rate bonds and reinvest the money into shorter-duration bonds with a higher yield. Instead, the sale dented the bank’s balance sheet with a $1.8 billion loss driving worried depositors to pull funds out of the bank.

The BTFP gave banks facing similar problems an alternative. They could quickly raise capital against their bond portfolios without realizing big losses in an outright sale. It gave banks a way out, or at least the opportunity to kick the can down the road for a year.

Fernandes said the timing of this ISDA proposal should raise some questions about the global banking system.

“With the conclusion of the BTFP, are banks signaling a potential banking crisis on the horizon? Or perhaps, even more significantly, are they indicating concerns about an impending international financial crisis, given the central role that U.S. Treasuries play in the global financial markets?”

Money Metals President Stefan Gleason said these are just “more games” to try to make banks look safer than they really are, “even though they have a lot of exposure to U.S. bonds.”

“Especially after they’ve experienced big value declines and an erosion in bank equity, causing their measured leverage to increase.”

Gleason is right. When you dig beneath all of the technical, regulatory mumbo-jumbo, this is just another example of the powers that be moving the goalposts to keep the game tilted in their favor.

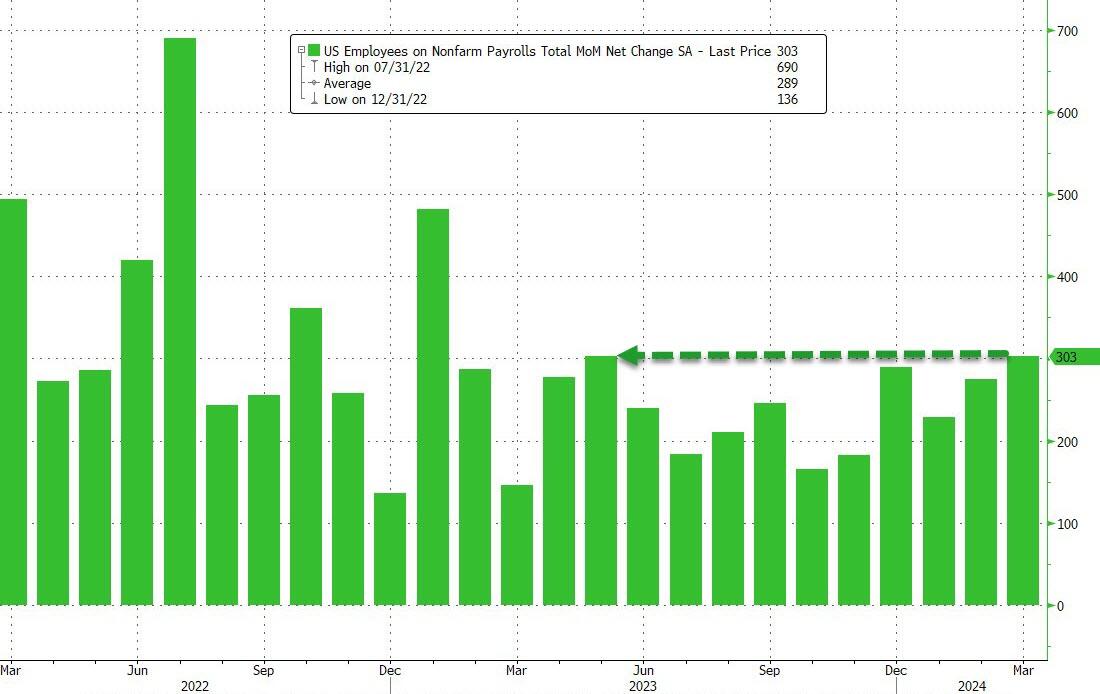

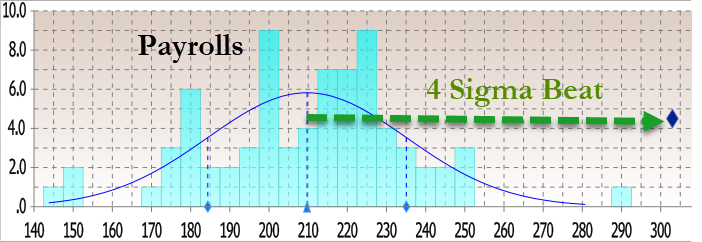

March Jobs Come In Red-Hot At 303K, Above Highest Estimate, As Unemployment Rate Drops

As we wrote in our preview, while big data hinted at a weaker than expected March jobs print, the relentless influx of immigrants would lead to a hotter than expected payrolls number.

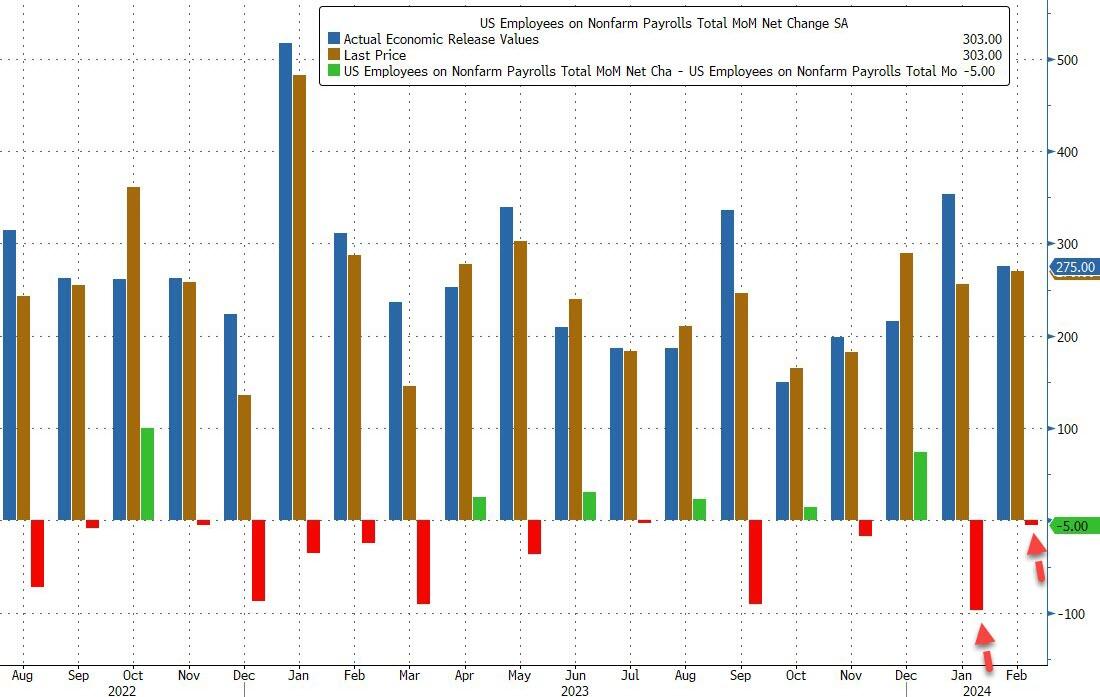

Sure enough, the illegals won again when moments ago the BLS reported that in March, the US added a whopping 303K jobs, tied for the highest since Jan 2023!

The number was not only hotter than last month’s (downward, of course) revised number of 270K (was 275K) but was above the highest Wall Street estimate of 290K (from Jobdig, Inc) and as shown below this was the latest multiple-sigma beat to expectations, this month coming in at 4x.

The March number, which will be revised substantially lower next month, follows two downward revisions, follows a 5,000 downward revision to the February number from +275,000 to +270,000, and a 27,000 upward revision to January from +229,000 to +256,000.

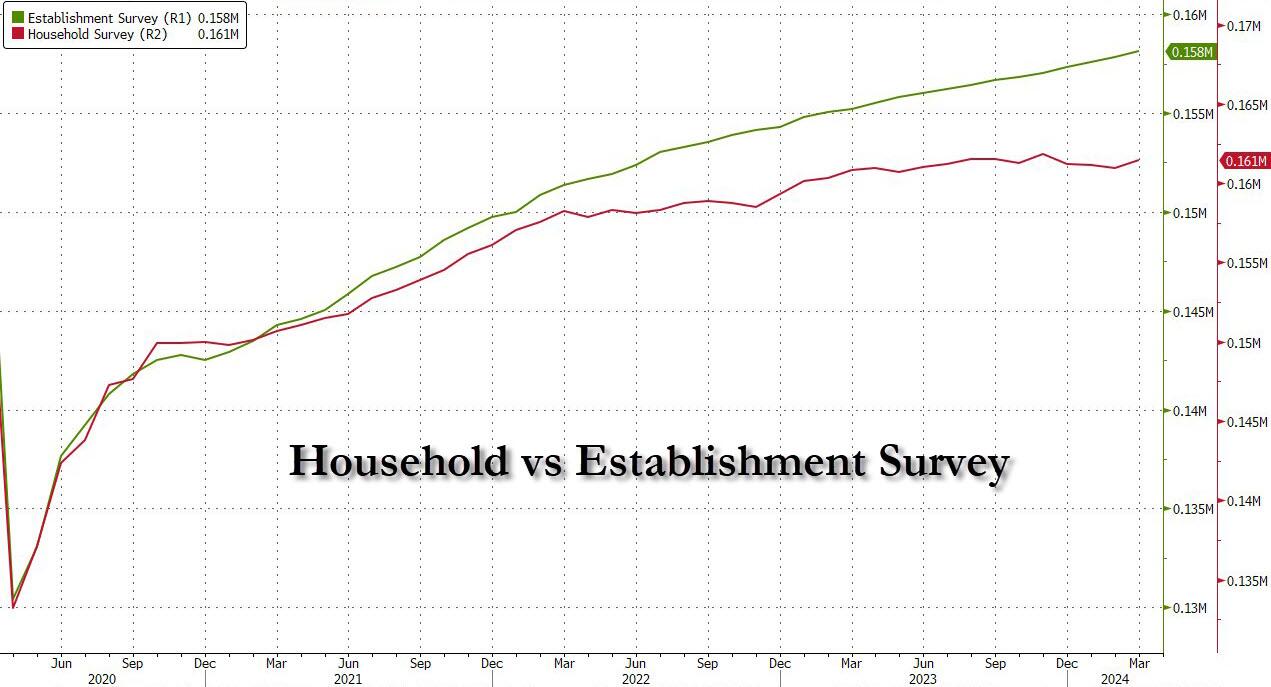

What is perhaps more notable is that after several months of declines in the Household survey, in March the number of people actually employed finally rebounded rising by 498K, to 161.466 million from 160.968 million. Still, as shown below, the data series has a lot of catching up to do.

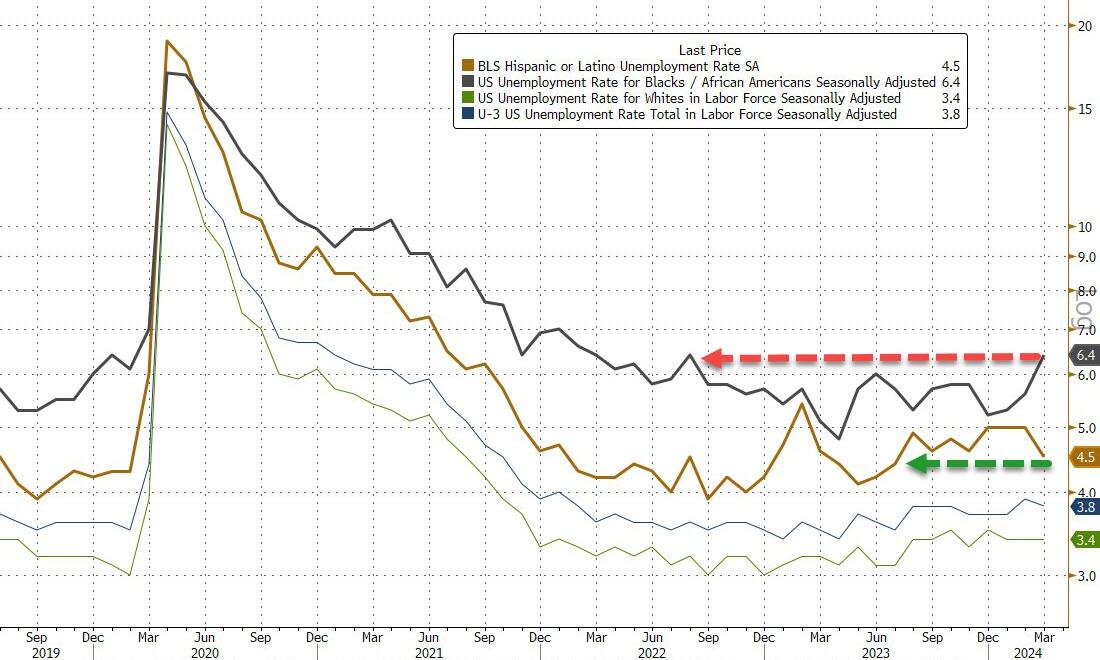

Turning our attention to the unemployment rate, it unexpectedly dipped again, dropping to 3.8%, from 3.9%, in line with estimates, as the number of unemployed workers dipped modestly from 6.458 million to 6.429 million while the number of employed workers rose by almost half a million workers; the unemployment rate for Blacks (6.4 percent) increased in March to the highest level in almost two years, while the rates for Asians (2.5 percent) and Hispanics (4.5 percent) decreased. The jobless rates for adult men (3.3 percent), adult women (3.6 percent), teenagers (12.6 percent), and Whites (3.4 percent) showed little or no change over the month.

In contrast, the participation rate rose from 62.5% to 62.7%, above the 62.6% expected, as the overall civilian labor force increased slightly less than the number of employed people.

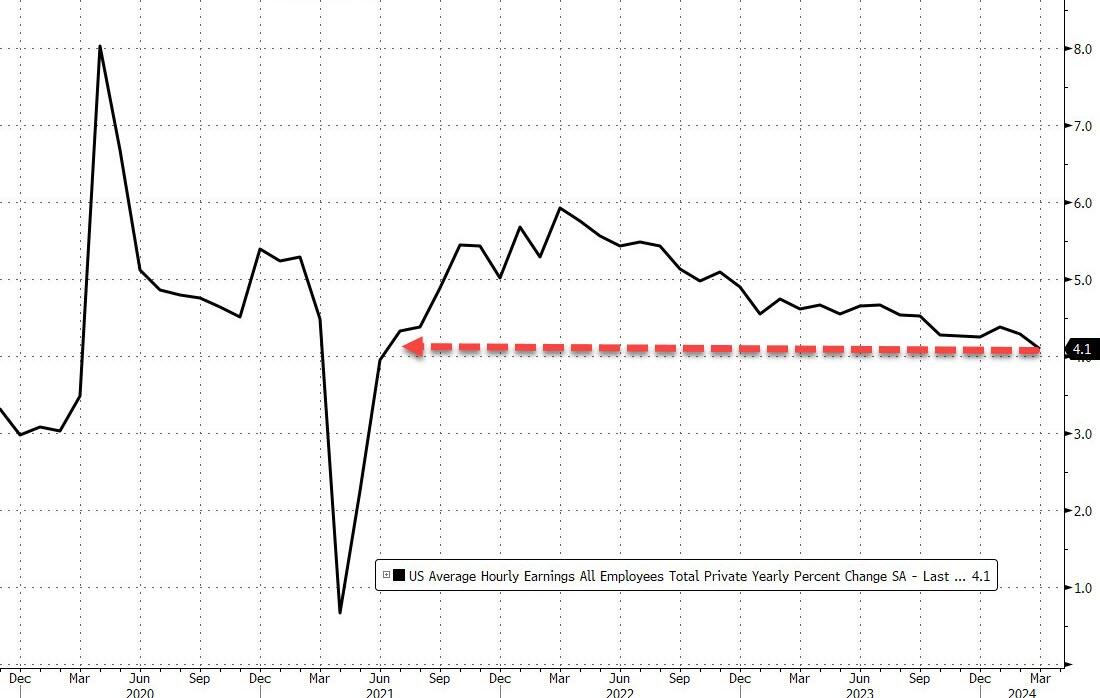

The silver lining to today’s jobs report is that despite the hot print, the average hourly earnings came in as expected, rising 0.3% MoM, up from last month’s upward revised 0.2% sequential increase (revised from 0.1%), On an annual basis, the hourly earnings rose 4.1%, as expected, and down from 4.3%. This was the lowest print in almost three years: the last time wages rose by this much was the summer of 2021.

Taking a closer look at wages, In March, average hourly earnings for all employees on private nonfarm payrolls increased by 12 cents, or 0.3 percent, to $34.69. Over the past 12 months, average hourly earnings have increased by 4.1 percent. In March, average hourly earnings of private-sector production and nonsupervisory employees edged up by 7 cents, or 0.2 percent, to $29.79.

One reason why average hourly earnings did not increase is that in March, the average workweek for all employees on private nonfarm payrolls edged up by 0.1 hour to 34.4 hours. In manufacturing, the average workweek was unchanged at 40.0 hours, and overtime edged down by 0.1 hour to 2.9 hours in March. The average workweek for production and nonsupervisory employees on private nonfarm payrolls also edged up by 0.1 hour to 33.9 hours.

* * *

According to the BLS, the number of people not in the labor force who want a job came in little changed at 5.4 million.

“These individuals were not counted as unemployed because they were not actively looking for work during the 4 weeks preceding the survey or were unavailable to take a job.”

Also according to the report, the number of people employed part time for economic reasons, at 4.3 million. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs.

Finally, the BLS reports that among those not in the labor force who wanted a job, the number of people marginally attached to the labor force, at 1.6 million, was little changed in March. These individuals wanted and were available for work and had looked for a job sometime in the prior 12 months but had not looked for work in the 4 weeks preceding the survey. The number of discouraged workers, a subset of the marginally attached who believed that no jobs were available for them, was little changed at 337,000 in March.

* * *

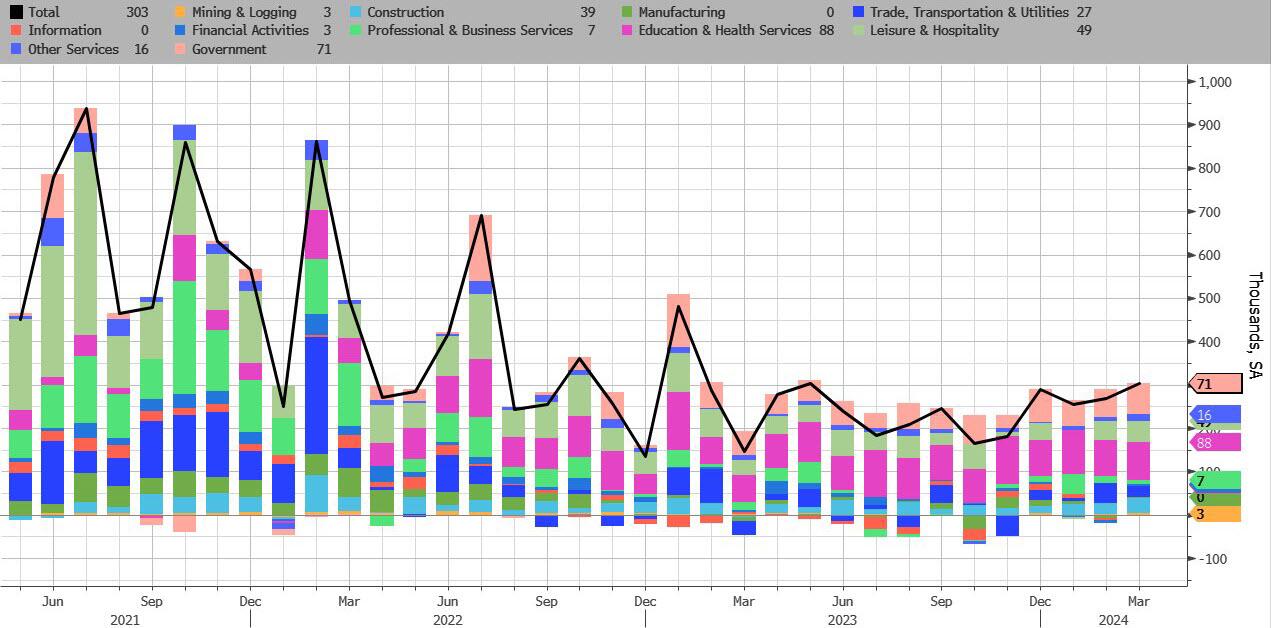

Taking a closer look at the composition of jobs by industry we find the following:

Health care added 72,000 jobs in March, above the average monthly gain of 60,000 over the prior 12 months. In March, job growth continued in ambulatory health care services (+28,000), hospitals (+27,000), and nursing and residential care facilities (+18,000).

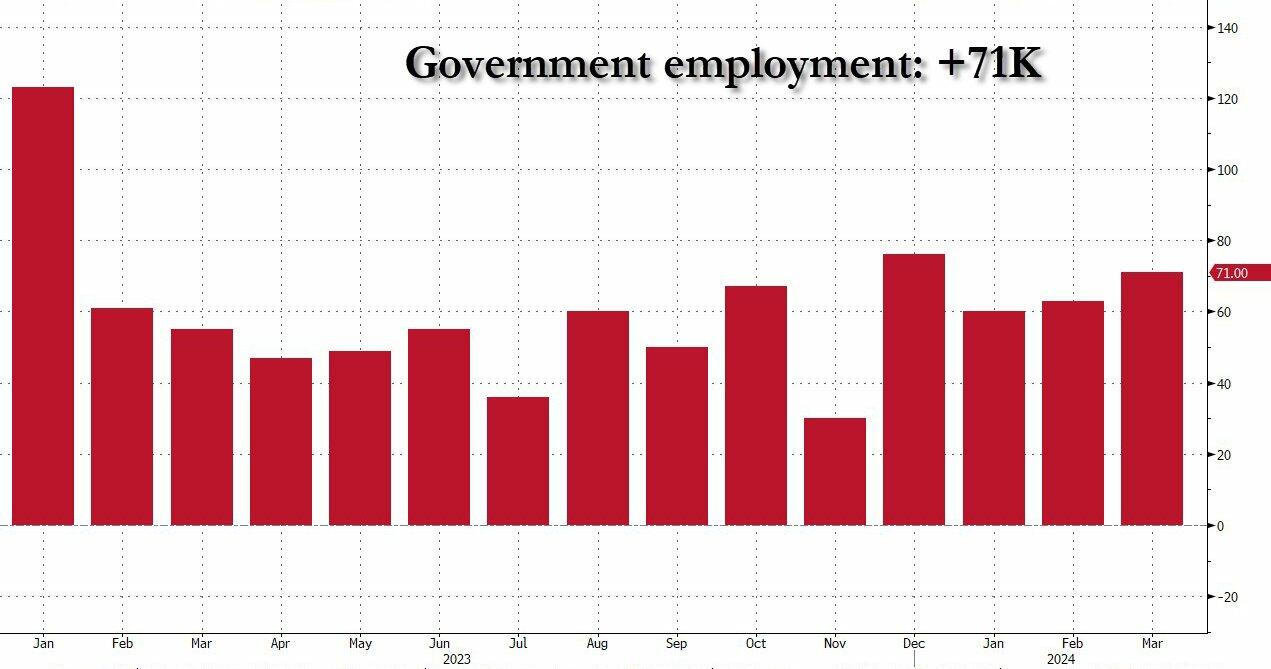

In March, employment in government increased by 71,000, higher than the average monthly gain of 54,000 over the prior 12 months. Over the month, employment increased in local government (+49,000) and federal government (+9,000).

Construction added 39,000 jobs in March, about double the average monthly gain of 19,000 over the prior 12 months. Over the month, employment increased in nonresidential specialty trade contractors (+16,000).

Employment in leisure and hospitality trended up in March (+49,000) and has returned to its pre-pandemic February 2020 level. Over the prior 12 months, job growth in the industry had averaged 37,000 per month.

Employment in the other services industry continued its upward trend in March (+16,000). The industry had added an average of 8,000 jobs per month over the prior 12 months. Employment in other services remains below its February 2020 level by 40,000, or 0.7 percent.

Employment in social assistance continued to trend up in March (+9,000), below the average monthly gain of 22,000 over the prior 12 months.

In March, employment was little changed in retail trade (+18,000). A job gain in general merchandise retailers (+20,000) was partially offset by job losses in building material and garden equipment and supplies dealers (-10,000) and in automotive parts, accessories, and tire retailers (-3,000).

Employment showed little or no change over the month in other major industries, including mining, quarrying, and oil and gas extraction; manufacturing; wholesale trade; transportation and warehousing; information; financial activities; and professional and business services.

A visual breakdown shows that the bulk of jobs was in Education/Health and Government jobs, which accounted for more than half of all March jobs.

And a closer look at the best performing job category under Biden: government. In March, this added 71K, the second most since the start of 2023.

In sum: health care added 72,000 jobs; government roles increased by 71,000; other notable gains were construction, adding 39,000, and leisure and hospitality, adding 49,000.

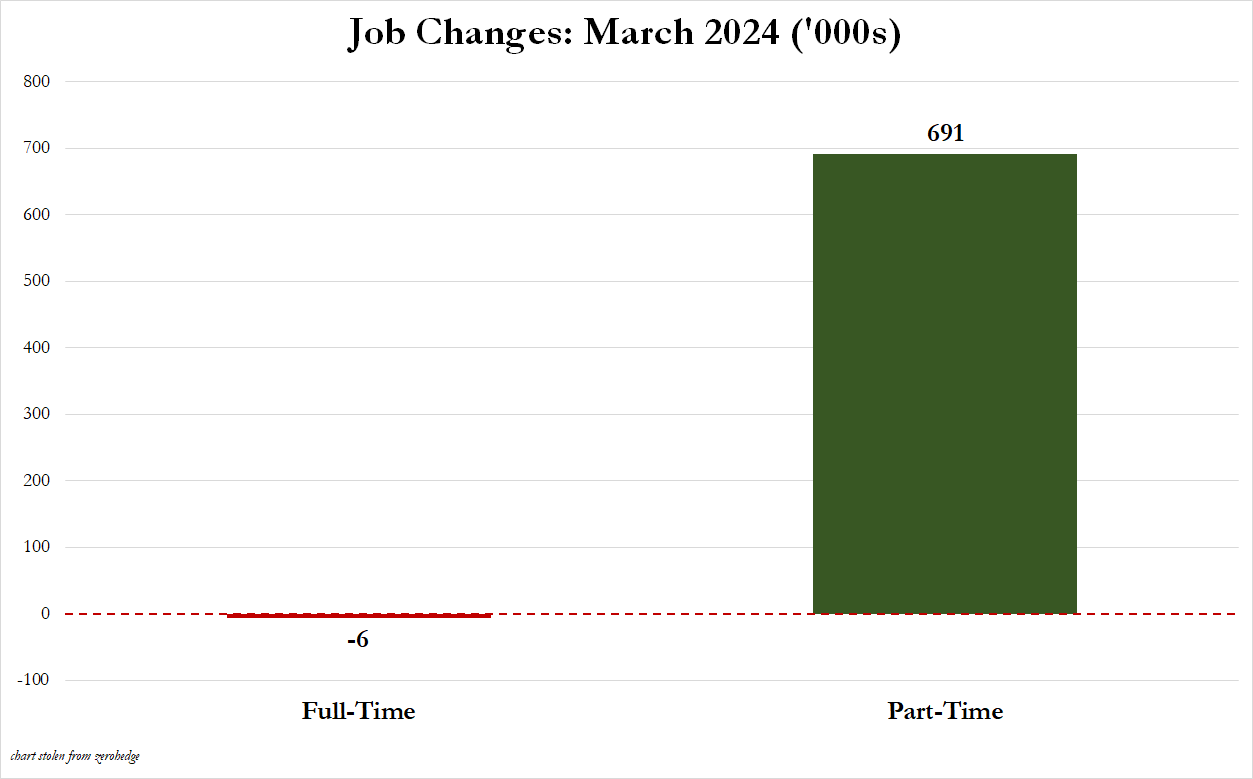

Finally, for those wondering if the jobs were all part-time, the answer is a resounding yes: in March, full-time jobs dropped by 6,000 as Part-time jobs soared by 691,000.

What was Wall Street’s reaction? Here are some hot takes, starting with Bloomberg’s Enda Curran who writes that since it’s an election year, these numbers will be trumpeted by the White House as evidence of their stewardship. The downside however is that they lean against calls for a rate cut, “something of a double-edged political sword.”

Echoing this, Torsten Slok, Apollo’s resident in house permabear who will never relax until you have sold all your assets to, well, Apollo writes that the number confirms the Fed will not cut rates this year:

“The source of this strength is easy financial conditions. The stock market is up +$10trn over the past five months, which is a significant wealth gain for household balance sheets. Credit spreads are tighter for IG, HY, and loans. Big rebound in IG issuance and HY issuance in January, February, and March. IPO activity is coming back and M&A activity is coming back. These factors will all support consumer spending, capex spending, and hiring over the coming quarters… We are sticking to our view that the Fed will not cut interest rates this year.”

Here is Seema Shah, chief global strategist, Principal Asset Management:

“At first sight, the jobs report leans against three cuts. Yet the average hourly earnings figures are in line with expectations and, as Powell has made quite clear in recent speeches, a strong labor market is not a concern if price pressures are moderating… Next week’s CPI report is the one that is pivotal for rate expectations. But today’s report should reassure markets that, if the Fed does not cut in June, it’s because the economy is still strong and earnings should remain in an upswing.”

Priya Misra, portfolio manager at JP Morgan Investment Management, says:

“If service inflation shows signs of picking up in the CPI and PCE reports later this month, Fed ‘patience’ might run thin. The market reaction makes sense to me – higher rates and weaker risk sentiment. I think risk assets are paying attention to rates now. Risk assets ignored the rates move until this week since Jan and Feb could be glossed over as noise. But if the economy is staying too hot, the market should question Fed cuts and the specter of Fed hikes comes back to the market.”

Ed Al-Hussainy, rates strategist at Columbia Threadneedle Investment, says:

“The key question is whether the combination of higher demand growth, momentum in employment, and the easing of financial conditions since last October start to show up in inflation. We’ll get another look at that in CPI/PPI data next week.”

Ali Jaffery, an economist at CIBC Capital Markets, sees immigration playing a role in today’s numbers:

“This has raised the sustainable level of job gains from 100K before the pandemic to about 180K. Today’s data is likely more evidence of that trend and supports the Fed’s view that the increase in labor supply is driving growth in the job market and the economy more broadly. Overall, the March employment report leans against an earlier cut by the Fed.”

Bryce Doty of Sit Investment Associates:

“Incredibly strong jobs data puts the bond market in panic mode over Fed cuts being delayed.”

But…

“I keep scratching my head wondering why so many people are deciding to get jobs now when millions of job openings have been available for at least a couple of years. It’s not as though the economy suddenly produced these jobs. So people joining the workforce now must need the jobs. As a result, I’m cautious about how strong the jobs data really is for the economy. We expect a quarter point cut in the third quarter and a half point cut in the fourth quarter.”

We close again with Bloomberg’s Enda Curran who writes that “at face value, these job numbers hardly lend themselves to a near-term rate cut.“

Bottom line: strong report, until you look under the surface. For now, however, it will serve the White House to pitch Bidenomics as some miraculous economic panacea, while the market will try to soothe itself that the number was good, but not hot enough to prevent Powell from cutting rates in June.