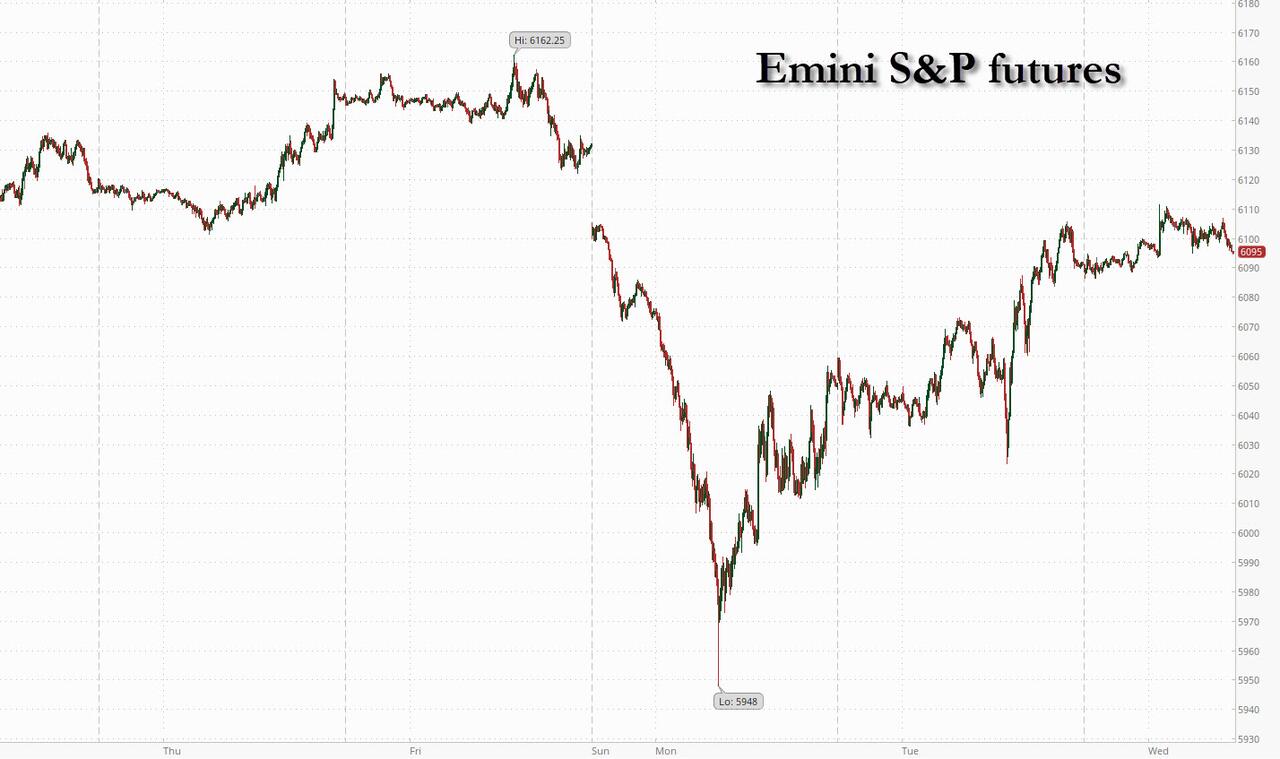

Futures are flat with Tech/Small-caps big higher as the market looks to recover from Monday’s tech plunge. As of 8:00am S&P futures are unchanged, erasing a modest earlier gain during the European session; Nasdaq futures extend their Tuesday rebound and rise 0.4% after rising 2.0% on Tuesday; Mag7 names are mixed (GOOGL +0.5%, AMZN +0.9%, AAPL -1%, MSFT flat, META +0.5%, NVDA -0.7% and TSLA -0.2%) with semis rallying but this may not mean the end of the Semis-to-Software rotation which is +10% this week. Europe’s Stoxx 600 index rose 0.6% after chip giant ASML soared 11% after order bookings beat estimates, spurring gains for semiconductor stocks. Bond yields are flat to down 2bps to 4.52% ahead of what is expected to be a dovish pause by the Fed today (full preview here). USD strength continues, given the likelihood of new tariffs announced this week or weekend. Commodities are mixed as Ags and Metals are bid. Looking to the day ahead, the main highlight will be the Federal Reserve’s policy decision, along with Chair Powell’s subsequent press conference, while the Bank of Canada will also be making their own policy decision. Data releases include December advance goods trade balance and wholesale inventories (at 8:30am ET). Finally, today’s earnings releases include tech giants Tesla, Microsoft and Meta.

In premarket trading, T-Mobile jumped 8% after reporting fourth-quarter results that beat analysts’ projections, benefiting from continued growth in wireless subscribers and home internet customers. Starbucks rose 2% after the coffee chain reported better-than-expected quarterly results, luring back lapsed customers with coffee-focused ads and by removing extra charges for nondairy milk. LendingClub plunged 21% after the operator of peer-to-peer loan website gave a first-quarter forecast that missed estimates. A Piper analyst said higher provisions drove a miss to his estimates. Here are some other notable movers:

- American Axle (AXL) slips 3% after entering a deal to combine with Dowlais. Shareholders of American Axle will own 51% of the combined company, with Dowlais shareholders controlling the rest.

- Danaher (DHR) falls 5% after the life-sciences firm posted quarterly profit that missed estimates.

- F5 Inc. (FFIV) jumps 14% after the network security company raised its forecast for full-year growth.

- Henry Schein (HSIC) rises 3% after KKR & Co. has taken a 12% strategic stake in the company.

- Manhattan Associates (MANH) tumbles 23% after the supply-chain software company gave a profit forecast for 2025 that disappointed.

- NEXTracker (NXT) surges 21% after the solar equipment maker boosted its earnings guidance for the full year.

- Packaging Corp. (PKG) falls 4% after the containerboard producer provided a disappointing first quarter profit forecast.

- Paragon 28 (FNA) climbs 10% after Zimmer Biomet Holdings agreed to buy the medical device company.

- Qorvo (QRVO) declines 6% after the semiconductor device company’s 2026 revenue forecast underwhelmed.

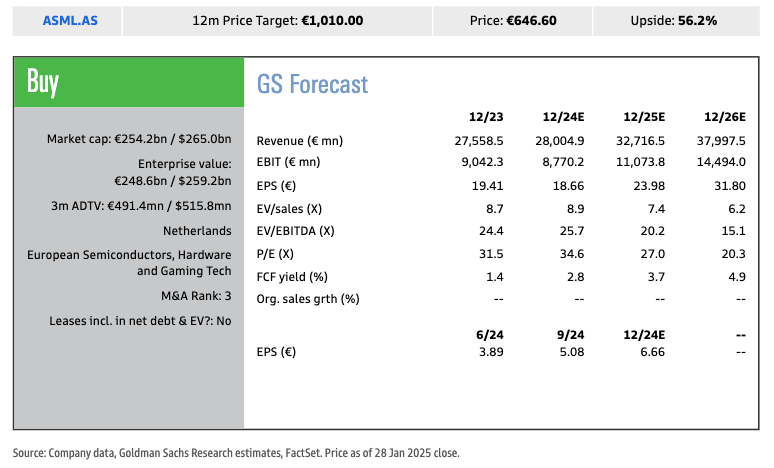

- Semiconductor-related stocks rise after chip-equipment maker ASML reported quarterly bookings well above analyst estimates, easing concerns over potentially weaker demand due to challenges at key clients including Samsung and Intel.

- Applied Materials (AMAT) +2%, Lam Research (LRCX) +3%, KLA Corp (KLAC) +3%

- Stride Inc. (LRN) gains 3% after the online education company boosted its year revenue forecast.

- VF Corp. (VFC), parent to brands including Vans, North Face and Timberland, rises 2% after reporting sales that beat expectations, a sign that its transformation plan is showing results.

It’s a busy day today when not only the Fed is expected to keep rates on hole in a “dovish pause” but we get three of the Mag 7 names report. Indeed, traders will be scouring results from Microsoft, Meta and Tesla later for signs of weakness after Chinese startup DeepSeek’s cheaper AI model rattled markets. While the Fed is widely expected to hold rates, Chair Jerome Powell is likely to be pressed on the inflationary impact of potential trade tariffs and other policies from President Donald Trump’s White House. See our preview here.

“I don’t think there’s any great desire for the Fed to become overly hawkish in their messaging, nor do I think they’re going to pre-commit to dovish loosening,” Guy Miller, chief strategist at Zurich Insurance Co., said. “They’ll say ‘look, we need a period to take stock of things.’

Traders have ratcheted up bullish bets in the hope that Powell signals a cut in March is firmly on the table. JPMorgan’s latest client survey released Tuesday shows the biggest net long position in US government debt in almost 15 years. Open interest in futures — or the amount of new risk held by traders — is increasing in 10-year note contracts. Meanwhile, central banks elsewhere remain on an easing path, with the Bank of Canada likely to reduce rates by a quarter point Wednesday. The European Central Bank is also expected to cut tomorrow.

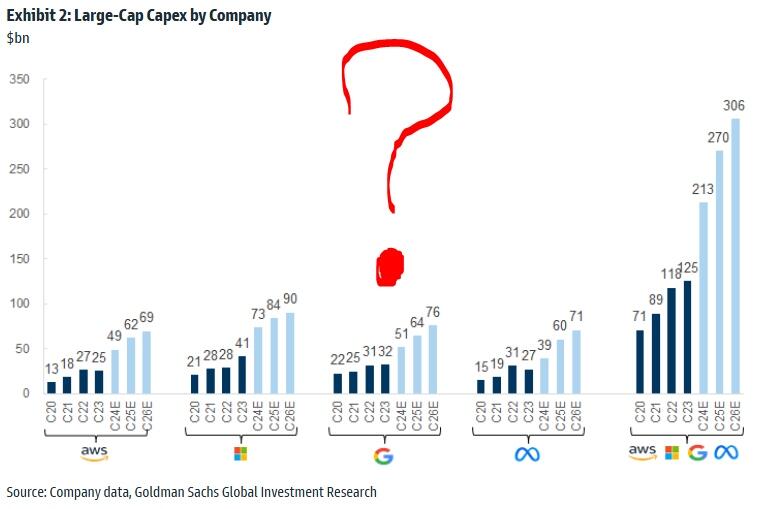

While profits from the Magnificent Seven tech companies are still rising — and far outpacing the rest of the market — growth is projected to come in at the slowest pace in almost two years. After the DeepSeek news, Microsoft’s AI spending will be in tight focus when the company reports. The company is expected to update investors on its progress in selling artificial intelligence products — and the massive infrastructure buildout making that possible. Separately, Microsoft and OpenAI are investigating whether data output from OpenAI’s technology was obtained in an unauthorized manner by a group linked to DeepSeek, according to people familiar with the matter.

“DeepSeek was a welcome reminder that there are risks, but “the way for equities is still up,” Miller said. “Investors still have a buy-the-dip mentality.”

In Europe, the Stoxx 600 index rose 0.6% with tech leading gains, while luxury shares dropped after LVMH reported underwhelming sales compared to peers. European semiconductor stocks are soaring Wednesday after Dutch chip giant ASML booked more than twice as many orders as analysts expected in the fourth quarter, sending its stock 11% higher. Here are some of the biggest movers on Wednesday:

ASML shares soar 12% after the chip-equipment maker reported quarterly bookings well above analyst estimates, easing concerns over potentially weaker demand due to challenges at key clients including Samsung and Intel.

- Volvo gains as much as 6.9% after the Swedish truckmaker reported stronger-than-expected order intake in its 4Q report.

- Logitech shares jump as much as 9.4%, the most in nine months, after the Swiss computer and gaming accessory maker reported results that beat estimates and raised its guidance.

- WH Smith shares rise as much as 7.2% as investors welcome the retailer’s acceleration in like-for-like revenue growth in the key North America market.

- Dowlais shares jump as much as 12% after the automotive engineering firm recommended a deal with American Axle, priced at a 25% premium to yesterday’s closing price. Shares remain well below the offer price this morning, which analysts at Jefferies said may be deemed as disappointing.

- LVMH shares fall as much as 6.7%, trimming recent lofty gains, after the luxury-goods maker’s earnings underwhelmed compared with recent strong updates from peers. European luxury stocks decline as analysts say LVMH’s earnings failed to live up to expectations that had been raised in recent weeks following strong updates from peers.

- Remy Cointreau shares drop as much as 4.1% after the high-end spirits maker said that it expects a drop in full-year sales to come in at the lower end of its guidance range, as its US business still struggles with destocking as well as a high basis of comparison.

- SEB dropped 4.1% after the Swedish lender’s net profit missed estimates and dividend per share of the year was also below estimates.

- Akzo Nobel shares fall as much as 6.1% after the Dutch specialty chemicals company posted full-year results where its decorative paints division weighed on its fourth quarter earnings.

- Lonza shares drop as much as 3.4%, the most since Nov. 27, after the Swiss maker of drug ingredients reported results for the full year that was hurt by its capsules & health ingredients business.

- Continental shares fall as much as 1.9% after the German car parts manufacturer hosted a pre-close call late on Tuesday where it warned of a tough sales climate for its automotive unit, which it plans to spin off in 2025.

Earlier in the session Asian stocks gained, led by advances in Australia, Japan and India while most markets were shut for the Lunar New Year. The MSCI Asia Pacific Index rose as much as 0.5%, with Sony and Toyota among the biggest boosts. Most of the shares listed on the regional benchmark were not trading Wednesday. Australia’s main equity gauge climbed nearly 1%, as data showing cooler-than-expected inflation was seen paving the way for an interest-rate cut as soon as next month. Japanese shares advanced as the DeepSeek-driven tech selloff subsided, following a rebound in Nvidia and other US AI stocks overnight. Equities in India extended their rebound from recent selloffs, fueled by gains in bank stocks and shares of software exporters Infosys and Tata Consultancy Services.

In rates, treasuries inched higher ahead of the Fed decision, with US 10-year yields falling 1 bps to 4.52%. Gilts and bunds outperformed following German 10-year bond sale that had highest oversubscription rate in eight months on a reduced allotment; as a result German and UK 10-year borrowing costs falling 3-4 bps each. Ahead of Fed decision, no change is priced in, putting focus on the outlook for March, with around 7bp of easing priced in; investors have been leaning bullish into the meeting, including Monday’s rally where a wave of new long positions were added in Treasury futures

In FX, the Bloomberg Dollar Spot Index rises 0.1%. The Aussie dollar is the weakest of the G-10 currencies, falling 0.4% against the dollar after core inflation eased by more than expected. The Swedish krona weakens 0.1% after the Riksbank cut interest rates 25 bps as expected.

In commodities, oil prices decline, with WTI falling 0.9% to $73.10 a barrel. Spot gold is steady near $2,760/oz. Bitcoin rises 2% and is above $102,000.

Looking to the day ahead, and the main highlight will be the Federal Reserve’s policy decision, along with Chair Powell’s subsequent press conference. The Bank of Canada will also be making their own policy decision. Data releases include December advance goods trade balance and wholesale inventories (8:30am). Finally, today’s earnings releases include Tesla, Microsoft and Meta.

Market Snapshot

- S&P 500 futures little changed at 6,097.25

- STOXX Europe 600 up 0.4% to 533.93

- MXAP up 0.4% to 183.29

- MXAPJ up 0.1% to 574.83

- Nikkei up 1.0% to 39,414.78

- Topix up 0.7% to 2,775.59

- Hang Seng Index up 0.1% to 20,225.11

- Shanghai Composite little changed at 3,250.60

- Sensex up 0.8% to 76,507.72

- Australia S&P/ASX 200 up 0.6% to 8,447.01

- Kospi up 0.8% to 2,536.80

- German 10Y yield little changed at 2.54%

- Euro down 0.1% to $1.0416

- Brent Futures down 0.8% to $76.85/bbl

- Brent Futures down 0.8% to $76.85/bbl

- Gold spot down 0.0% to $2,763.16

- US Dollar Index up 0.13% to 108.00

Top Overnight News

- US DOGE said it is saving the federal government about USD 1bln per day but added that the federal government savings needs to increase to over USD 3bln per day.

- US judge temporarily paused the Trump administration’s freeze of federal loans and grants with a pause to Trump’s halt on funding of open programs to last until February 3rd, while it was also reported that a state attorney general group sued the Trump administration after earlier saying it would challenge the federal funding pause.

- OpenAI said Chinese companies are ‘constantly’ trying to distil US AI models, while it engages in ‘countermeasures’ to protect its intellectual property and will work with the US government to protect US technology. It was separately reported that Microsoft (MSFT) is probing if a DeepSeek-linked group improperly obtained OpenAI data, while OpenAI said it has found evidence that Chinese artificial intelligence start-up DeepSeek used the US company’s proprietary models to train its own open-source competitor, according to FT.

- Japan’s Advantest on Wednesday hiked its full year operating profit forecast by 37% due to strong demand for its testing tools for chips used in artificial intelligence tasks. They highlighted continued growth in tester demand for AI related, high performance semiconductors. Advantest forecasts operating income of 226 billion yen ($1.46 billion) in the financial year ending March 31. RTRS

- ASML +7% (ADR kind) on a BIG bookings beat (€7.1bn) + upbeat commentary (HE of FY doable if AI remains strong).. As it relates to DeepSeek… ASML said “Anyone that lowers cost is good news for ASML … Lower cost means AI can be used in more applications, more applications mean more chips.” (H/T Peter Callahan, Peter Bartlett)

- Traders are betting the ECB will have to ease more aggressively amid political turmoil and risk of US tariffs. Markets are positioning for the euro to weaken and for bonds to gain. A 25-bp cut is widely expected tomorrow. BBG

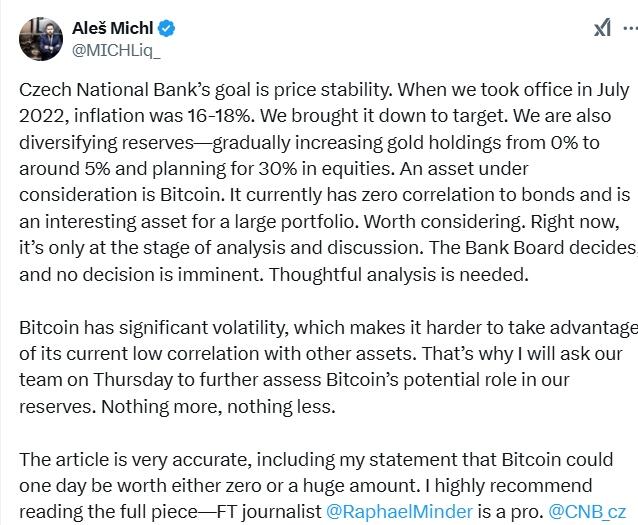

- Czech National Bank wants to put billions of euros of its reserves into bitcoin (this would represent the first time a western central bank purchases crypto). FT

- Sweden’s central bank lowered its key interest rate on Wednesday, with policymakers signaling they might be finished with their monetary policy easing. WSJ

- US crude stockpiles rose by 2.86 million barrels last week, the API is said to have reported. That would be the first increase in 10 weeks if confirmed by the EIA today. Gasoline supplies also gained. BBG

- Alibaba launched a new AI model (a new version of its Qwen 2.5 model) it claims is superior to DeepSeek’s V3 and Meta’s Llama. BBG

- Apple, SpaceX and T-Mobile have been working to add support for Starlink to the iPhone. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher following the positive handover from Wall St where tech clawed back some of the DeepSeek-related losses, although the conditions were quiet in Asia amid mass closures for the Chinese New Year. ASX 200 was led higher by outperformance in tech and utilities, while softer-than-expected Australian CPI data for Q4 also spurred increased rate cut bets for the RBA’s meeting in February (cut now priced at around 76% vs. 64% pre-release). Nikkei 225 took impetus from US counterparts but with gains capped amid few fresh drivers and after outdated BoJ minutes.

Top Asian News

- BoJ December meeting minutes stated members agreed inflation expectations are heightening moderately and agreed the BoJ should raise the interest rate if the economy and prices move in line with forecasts. Many members said the economy and prices are moving in line with forecasts and agreed the BoJ must decide the timing for raising rates by looking carefully at various data and information. Furthermore, members also agreed they wanted a bit more data on wage momentum and saw uncertainty over the next US administration’s economic policies.

- US State Department spokesperson said part of Secretary of State Rubio’s trip to Central America is about countering China, according to Fox Business.

European bourses (Stoxx 600 +0.5%) began the European session mostly firmer and traded rangebound, at elevated levels throughout the morning. The CAC 40 -0.1% is the clear underperformer in Europe today, with the index weighed on by post-earning losses in LVMH (-5%); the AEX is the day’s outperformer, with sentiment in the Tech sector lifted following blockbuster results in ASML (+8.7%). European sectors hold a slight positive bias. Tech is by far and away the clear outperformer in today’s session, lifted by post-earning strength in ASML (+11%). The Co. reported strong rev. for Q4, and its Bookings were exceptionally strong; it came in well above expectations at EUR 7.09bln (exp. 3.53bln). It also raised its Q1 net sales guidance above consensus. Consumer Products is underperforming today, weighed on by losses in LVMH (-6%). The Co. beat on its FY Revenue figure, though its Net Profit fell short of expectations. The Q4 figures were a little more positive, which generally topped expectations.

Top European News

- Swedish Riksbank Rate 2.25% vs. Exp. 2.25% (Prev. 2.5%); forecast for the policy rate made in December essentially holds, but the Executive Board is prepared to act if the outlook for inflation and economic activity changes.

- Riksbank Governor Thedeen says best judgement is that rates have reached the bottom, but the outlook is genuinely uncertain.

- German equipment investment seen growing 1.1% in 2025, according to annual government economic report cited by Reuters. Expects exports to decline by 0.3% in 2025. Expects imports to grow by 1.9% in 2025.

- UK Chancellor Reeves says the government has begun to turn things around. Solution is for the government to systematically remove barriers. Will work with the US to deepen the UK’s economic relationship in the months and years ahead. Will prioritise proposals with the EU that are consistent with Labour’s manifesto. Business and Trade minister to travel to India to resume talks on a trade deal

Earnings Summary

- ASML (ASML NA) +8.7%, Earnings Call at 14:00GMT/09:00EST: Q4 metrics beat, Bookings stood out at EUR 7.09bln (exp. 3.53bln). Q1 Guidance: Net Sales between 7.5-8.0bln (exp. 7.25bln), Gross Margin between 52-53% (exp. 51.2%). CEO: Revenue “was primarily driven by additional upgrades. We also recognized revenue on two High NA EUV systems.” & “Consistent with our view from the last quarter, the growth in artificial intelligence is the key driver for growth in our industry”. CEO/CFO: still very bullish; seeing increased demand for advanced technology in logic and DRAM markets, continues to invest in advanced EUV and mainstream DUV technologies. ASML (ASML NA) on DeepSeek, says anything that drives cost down is good news for ASML; AI cost reduction will lead to increased use and higher volumes

- Akzo Nobel (AKZA NA) -4.9%: Q4 metrics mixed, FY24 slight beat. FY25 guidance slightly short. Co. does not expect a significant market rebound in 2025.

- Remy Cointreau (RCO FP) -5.8%: Q3 & 9-month sales beat. FY guidance confirmed at lower-end of range.

- Logitech (LOGN SW) +6.2%: Q3 metrics beat. FY25 guidance lifted. Gaming sales near COVID peaks. Notable progress in China.

- Volvo (VOLVB SS) +6.9%: Q4 mixed. Cuts China truck market outlook, but notes that North America is gradually improving.

- Fresnillo (FRES LN) Production Report, Q4: Another solid year of production, with gold production ahead of guidance, whilst “Lead and zinc production were also up strongly over the year again”.

FX

- DXY is marginally higher with the USD stronger vs. most peers (ex-JPY). Today is of course Fed day which is set to see the FOMC pause its rate cutting cycle. As it stands, markets currently price around 50bps of loosening by year-end. Elsewhere, markets remain alive to the risk of potential tariff announcements by the Trump admin. DXY is currently oscillating around the 108 mark and briefly matched the top end of Tuesday’s 107.68-108.05 range.

- EUR is now softer vs. the USD after a bout of selling pressure early doors alongside a disappointing outturn for German GfK Consumer Sentiment. Greater focus lies on tomorrow’s ECB policy announcement and the looming threat of tariffs from the Trump administration. As it stands, the odds of a 25bps cut in March are at around 80% with a total of 90bps of loosening seen by year-end. EUR/USD briefly slipped below Tuesday’s and the 24th Jan lows at 1.0414.

- JPY is slightly firmer vs. the USD. BoJ Minutes from the December meeting did little to shift the dial given that there was a more recent meeting last week where the central bank delivered a widely expected 25bps rate hike. Furthermore, JPY was unreactive to news that Japanese Finance Minister Kato held a videoconference with new US Treasury Secretary Bessent in which they confirmed close cooperation on FX. USD/JPY is currently within Tuesday’s 154.45-155.97 range and holding above its 50DMA at 154.86.

- GBP is a touch softer vs. the USD but mildly firmer vs. the EUR with fresh macro drivers for the UK on the light side. On today’s docket, BoE Governor Bailey is to attend the TSC hearing on the November Financial Stability Report at 14:15GMT. Cable currently sits towards the lower end of yesterday’s 1.2415-98 range. Chancellor Reeves in her “Kickstart Economic Growth” press conference, said “the government has begun to turn things around”. She set forth a few additional investments, but steered clear of any major announcements; as such, the Pound was little changed.

- Antipodeans are both on the backfoot vs. the USD for a third consecutive session. AUD was hampered overnight by soft Australian CPI metrics in which all figures for Q4 printed softer-than-expected and resulted in increased bets for a cut at the next RBA meeting (cut now priced at around 76% vs. 64% pre-release).

- SEK was trivially softer against the EUR post-Riksbank, where a 25bps cut was delivered as expected. The accompanying statement noted that “the forecast for the policy rate made in December essentially holds, but the Executive Board is prepared to act if the outlook for inflation and economic activity changes”. Since, the Governor has said it looks like they are at the bottom in rates but the outlook is uncertain, a remark which has lifted the SEK.

- CAD marginally softer vs. the USD in the run up to today’s BoC rate decision which is set to see policymakers pull the trigger on another 25bps rate reduction, bringing the total quantum of cuts to 200bps for the current cycle

Fixed Income

- USTs are firmer into the FOMC. Derived support from a strong 7yr Note auction on Tuesday, an outing which followed mixed results across Monday’s lines. As it stands, USTs are at a 109-09 peak which is just below Monday’s 109-12 best. If the move continues then there is a bit of a gap until the 110-00 mark and then the 110-03+ peak from mid-December.

- Bunds are moving in tandem with USTs and as such find themselves at a 131.81 peak, stopping shy of the figure and then Monday’s 132.14 best. A 2035 auction garnered decent demand, which sparked some very modest upside.

- OATs are firmer, but modestly underperforming core peers. Underperformance which is on account of increasing attention on tensions between the French PM and the Socialist party. Tensions which stemmed from the PM’s remarks around immigration at the start of the week. In response, Socialist member Brun said they have suspended negotiations with the PM on the budget.

- Gilts are directionally in-fitting with the above; the Green Gilt outing was a little weaker than the prior, but b/c remained above 3x. Into the Chancellor Reeves “Kickstart Economic Growth” press conference, Gilts traded near highs at 92.47. The presser, thus far has been as expected, and as such has spurred little move in Gilts; UK paper has continued its upward bias to a current 92.54 peak.

- UK DMO announces new March 2035 Gilt syndication; transaction planned to take place in the week beginning 10th Feb, subject to demand and market condition.

- UK sells GBP 0.875% 2033 Green Gilt: b/c 3.1x (prev. 3.55x), avg. yield 4.473% (prev. 3.731%) & tail 0.7bp (prev. 0.9bp).

- Germany sells EUR 3.439bln vs exp. EUR 4.5bln 2.50% 2035 Bund: b/c 2.8x (prev. 2.12x), average yield 2.54% (prev. 2.51%) & retention 23.58% (prev. 24.4%)

Commodities

- Softer trade across the crude oil complex amid a firmer dollar and following a choppy session yesterday. Desks suggest the overall weakness in the oil market seen over the past few sessions likely emanate from US prepares to impose tariffs on imports from Canada, Mexico and China from Saturday, with the WTI discount to Brent also narrowing as higher tariffs could tighten US supply. Brent near the lower end of a USD 75.69-76.65/bbl parameter.

- Mixed/flat trade across precious metals in the run-up to the FOMC policy announcement and Fed Chair Powell’s press conference later today. Spot gold resides in a narrow USD 2,757.46-2,766.26/oz range.

- Mixed trade across base metals with upside hampered by the firmer dollar and cautious sentiment amid Trump’s ongoing tariff threats, as also cited by several desks. 3M LME copper dipped under USD 9,000/t and resides in a USD 8,961.00-9,023.23/t range at the time of writing.

- Private inventory data (bbls): Crude +2.9mln (exp. +3.2mln), Distillate -3.8mln (exp. -2.3mln), Gasoline +1.9mln (exp. +1.3mln) Cushing -0.1mln

- Peruvian Economy Minister says the country has to open more copper mines to take advantage of growth; Anglo American (AAL LN) committed to resolving water issues in northern city before moving ahead with USD 2bln copper-gold project.

Geopolitics: Middle East

- “Israeli army: monitoring a march that penetrated the airspace from Egyptian territory in an attempt to smuggle weapons”, according to Sky News Arabia.

- “Iranian Foreign Minister Abbas Araqchi: We have not received any message from Trump regarding the negotiations”, according to Sky News Arabia.

- US Secretary of State Rubio reiterated in a call with the Egyptian Foreign Minister the importance of close cooperation to advance post-conflict planning to ensure Hamas can never govern Gaza or threaten Israel again.

- Russia and Syria are to hold further talks on Russian military bases in Syria, while there are no changes so far to the presence of Russian military bases in Syria, according to Russia’s Deputy Foreign Minister cited by TASS.

Geopolitics: Ukraine

- Ukrainian President Zelensky commented that Ukraine needs broader guarantees and that Russian President Putin is not afraid of Europe, while he added that Ukraine cannot recognise the Russian occupation.

- Ukrainian drone attack at an industrial facility in Russia’s Nizhny Novgorod region sparked a fire at an oil refinery, according to Russian Telegram news outlets.

- Russia’s Smolensk regional Governor said Russian air defence systems destroyed a Ukrainian drone attempting to attack a nuclear power facility in the Smolensk region, while it was later reported that the Smolensk nuclear power plant is operating in normal mode after a drone attack on the region, according to RIA.

- EU is proposing new Russian sanctions including an aluminium ban that would phase in over one year, while it also proposes new measures against Russian banks and dark fleet tankers, according to Bloomberg.

Geopolitics: Other

- North Korean leader Kim inspected a nuclear material production base and called for bolstering nuclear forces this year, as well as boosting production of weapons-grade nuclear materials, according to KCNA. It was separately reported that an NSC spokesperson said US President Trump is to pursue a complete denuclearisation of North Korea, according to Yonhap.

- Estonia’s Defence Minister says Shipping firms may need to pay a fee to use Baltic Sea to cover cost of protecting undersea cables.

US Event Calendar

- 07:00: Jan. MBA Mortgage Applications -2.0%, prior 0.1%

- 08:30: Dec. Retail Inventories MoM, est. 0.2%, prior 0.3%

- 08:30: Dec. Wholesale Inventories MoM, est. 0.2%, prior -0.2%

- 08:30: Dec. Advance Goods Trade Balance, est. -$105.5b, prior -$102.9b

- 14:00: Jan. FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap

After the tech-led slump on Monday morning, markets continued to unwind those moves over the last 24 hours, with little sign of broader contagion from tech stocks to the rest of the market. That meant the S&P 500 recovered +0.92%, bringing the index back within 1% of its all-time high. And if you consider that S&P 500 futures were down -3% on Monday at the height of the slump, the index has effectively now unwound the bulk of that initial selloff. Tech stocks led the recovery, with the NASDAQ (+2.03%) and the Mag-7 (+2.70%) reversing most of Monday’s decline, whilst in Europe the STOXX 600 (+0.36%) and the DAX (+0.70%) even managed to hit another record high. So in terms of the headline moves, it’s clear that investors are feeling more optimistic, and we’re not seeing the sort of repeated selloffs that happened when the dot com bubble began to burst in early 2000.

That said, even as most indices posted a decent advance, it was far from a universally rosy picture. For instance, 70% of stocks within S&P 500 were actually lower on the day, with the equal-weighted version of the index down -0.47% as defensive stocks underperformed. And whilst all of the Mag-7 moved higher, semiconductor stocks were still feeling the aftershocks of Monday’s slump. Indeed, the Philadelphia Semiconductor Index (+1.11%) only pared back a fraction of its -9.15% slump on Monday. And even though Nvidia bounced back +8.93%, that’s still less than half of its -19.56% decline over the previous two sessions. So it’s clear there are still a lot of jitters, not least given the growing comparisons being made to the dot com bubble. However, it’s worth noting that when the dot com bubble began to burst from March 2000, the NASDAQ slumped by more than a third in the space of just over a month, so it was on a scale well beyond anything we’ve seen today. We should get plenty more on the tech side later, as there are earnings announcements from Tesla, Microsoft and Meta after the close tonight, ahead of Apple’s announcement tomorrow.

Shortly before those earnings announcements, today will also bring the Federal Reserve’s first policy decision of 2025, along with Chair Powell’s subsequent press conference. For the headline decision, it’s widely expected the Fed will keep rates on hold, ending a run of 3 consecutive rate cuts since September. That follows on from a hawkish rate cut in December, where they upgraded their inflation forecasts and only signalled two further cuts in their dot plot for 2025, which was fewer than expected. Indeed, the S&P 500 slumped by -2.95% that day, which was its second-biggest decline in the last two years, so the extent of their hawkishness came as a major surprise for markets. For today, our US economists are also anticipating the Fed will stay on hold, but think they’ll only provide limited guidance about upcoming decisions. As it stands this morning, market pricing is broadly in line with that dot plot for 2025, with futures pricing in 51bps worth of cuts by the December meeting. For more info, see our economists’ full preview here.

Ahead of the Fed, Treasuries largely held their ground yesterday. Initially, the pickup in equities had seen 10yr Treasury yields move +4bps high intra-day, as investors became less concerned that an equity correction and negative wealth effects would lead to a broader slowdown in consumer spending. However, this move reversed later on, in part thanks to a decent 7yr auction, with 10yr yields closing -0.2bps lower at 4.53%, their lowest level since Christmas. Similarly, 2yr yields (-0.2bps to 4.20%) fell to their lowest since December 12, before the last Fed meeting.

Over in Europe, the focus has also been on central banks ahead of the ECB’s decision tomorrow, and unlike the Fed, they’re widely expected to deliver another 25bp cut, taking their deposit rate down to 2.75%. We also received the ECB’s latest Bank Lending Survey yesterday, which showed that credit standards for firms tightened in Q4, with a net +7% reporting tighter credit standards, the highest in a year. In the meantime, sovereign bonds moved broadly in line with their US counterparts, with yields on 10yr bunds (+3.1bps) and OATs (+2.4bps) both moving higher. Yields on 10yr BTPs (+2.7bps) also saw a sharp move up towards the end of the session, which came after Italy’s PM Giorgia Meloni said she’d received a notice of investigation by prosecutors.

Overnight in Asia, that positive momentum has continued in markets, with gains for the Nikkei (+0.76%) and the S&P/ASX 200 (+0.57%), although several markets are closed for holidays, including in China and South Korea. Otherwise though, there’s been a rally in Australian government bonds after their CPI print for Q4 was a bit softer than expected, falling to +2.4% last quarter (vs. +2.5% expected). That was seen as raising the likelihood of a rate cut from the RBA in February, and 10yr government bond yields are down -4.5bps this morning. That’s also helped weaken the Australian Dollar, which is down -0.13% against the US Dollar. Looking forward, futures suggest that positive momentum should continue, with those on the S&P 500 (+0.01%) and the NADSAQ 100 (+0.09%) pointing modestly higher.

Looking at yesterday’s data releases, the US Conference Board’s consumer confidence indicator fell by more than expected in January, moving down to a four-month low of 104.1 (vs. 105.7 expected). The labour market indicators also weakened, and the difference between those saying jobs were plentiful and hard to get fell to its lowest level in four months.

To the day ahead now, and the main highlight will be the Federal Reserve’s policy decision, along with Chair Powell’s subsequent press conference. The Bank of Canada will also be making their own policy decision. Data releases include the Euro Area M3 money supply for December. Finally, today’s earnings releases include Tesla, Microsoft and Meta.