Bank of America Jumps On Record Equity Trading Revenue, Net Interest Income Forecast Increase, Offset By FICC Miss

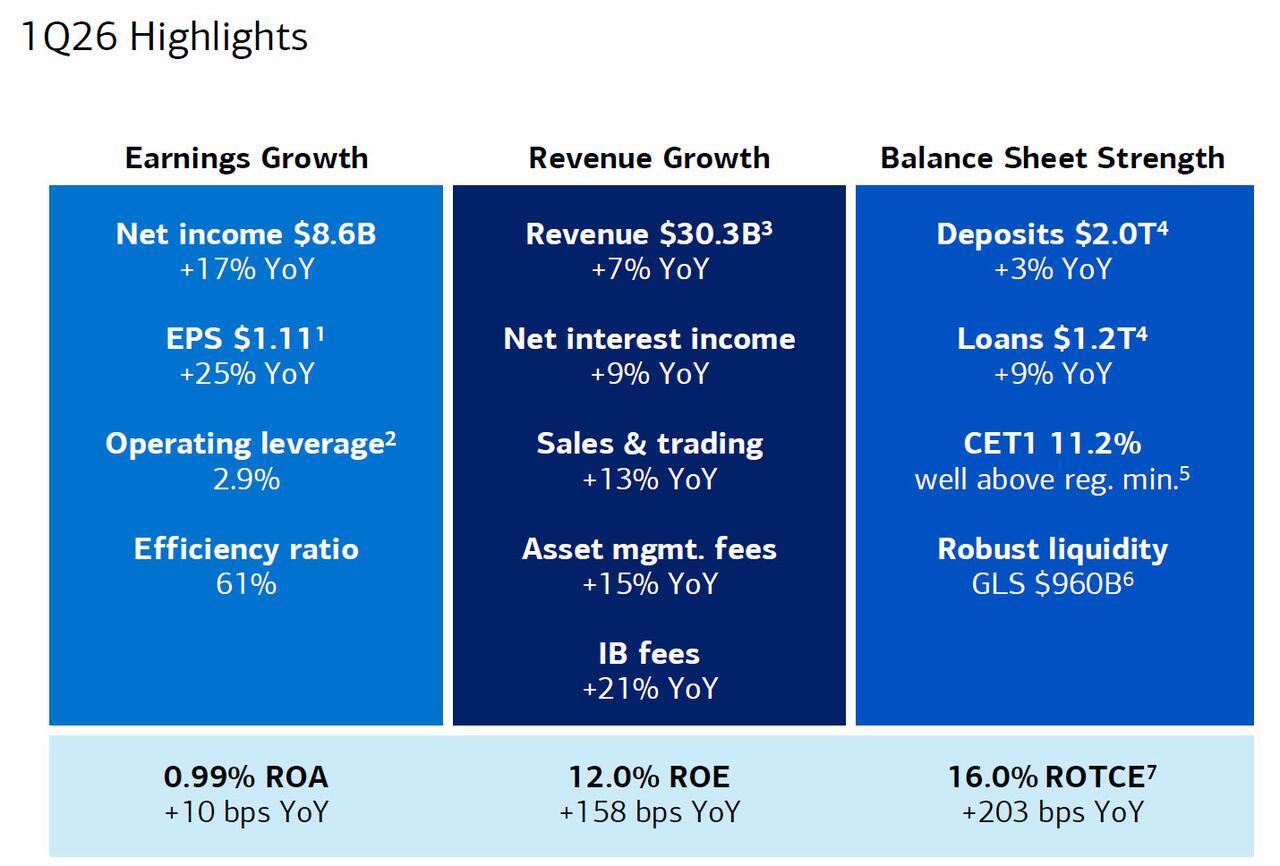

Following stellar equity trading results from Goldman and JPMorgan, this morning Bank of America reported that its traders also pulled in the business’s highest quarterly revenue in more than a decade, riding a wave of volatility that pushed the firm’s stock-trading desk to an all-time record. Bank of America said Q1 profit rose 17% from a year earlier, while net income came in at $8.58 billion. That amounted to $1.11 a share, above analyst estimates of $1.01. Revenue was 7% higher at $30.27 billion, driven by solid net interest income, sales and trading and investment banking fees.

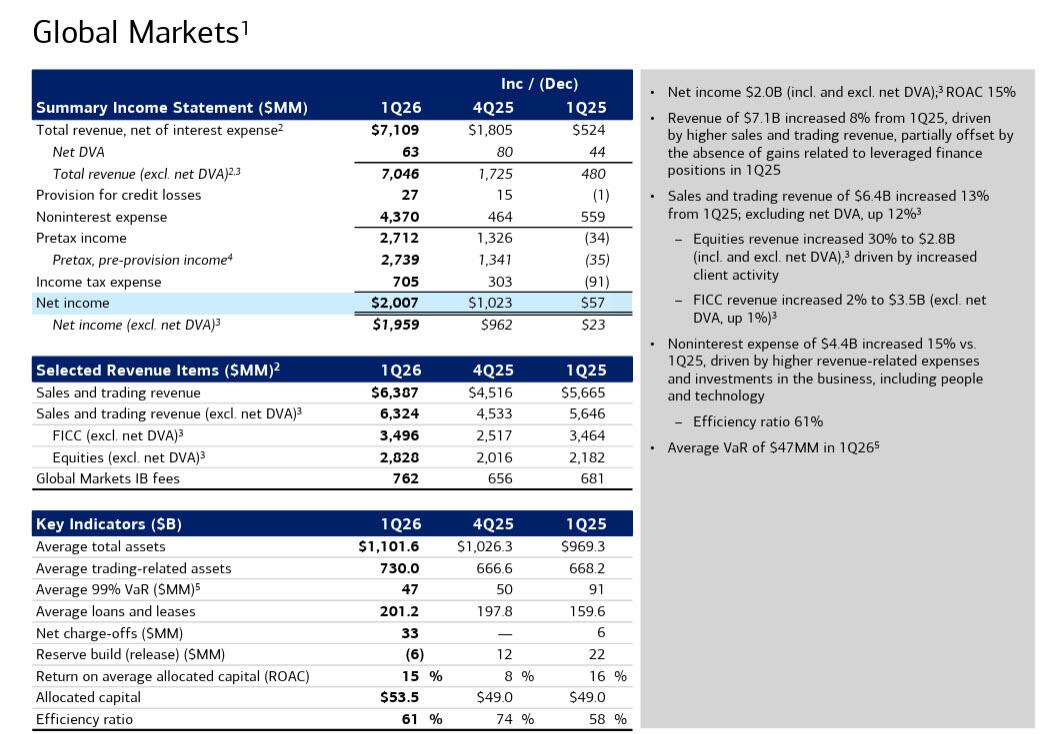

Revenue from equity trading climbed 30% to $2.8 billion in the first quarter, beating expectations, while fixed-income trading, which fell short of a consensus of analyst estimates, rose less than 1% to $3.5 billion, similar to Goldman’s FICC miss. Bank have benetted from a volatile quarter, when the Iran war sent oil prices surging and concerns about artificial intelligence and private credit whipsawed stocks. Trading desks were already on a roll since President Donald Trump won the 2024 election, as his policy moves often spurred reactions across stocks, commodities and rates. The total trading haul helped push revenue to $30.3BN, above the $29.92BN consensus estimate, while adjusted EPS rose 25% to $1.11 a share, also beating the $1.01 analyst estimate. Overall, Bank of America’s net income was up 17.3% to $8.16 billion.

Here are the Q1 highlights

- EPS $1.11, beating ests of $1.01

- Revenue net of interest expense $30.27 billion, beating estimates of $28.63 billion

- Trading revenue excluding DVA $6.32 billion, estimate $6.34 billion

- Equities trading revenue excluding DVA $2.83 billion, beating estimate $2.51 billion

- FICC trading revenue excluding DVA $3.50 billion, missing estimate $3.78 billion

- Trading revenue excluding DVA $6.32 billion, estimate $6.34 billion

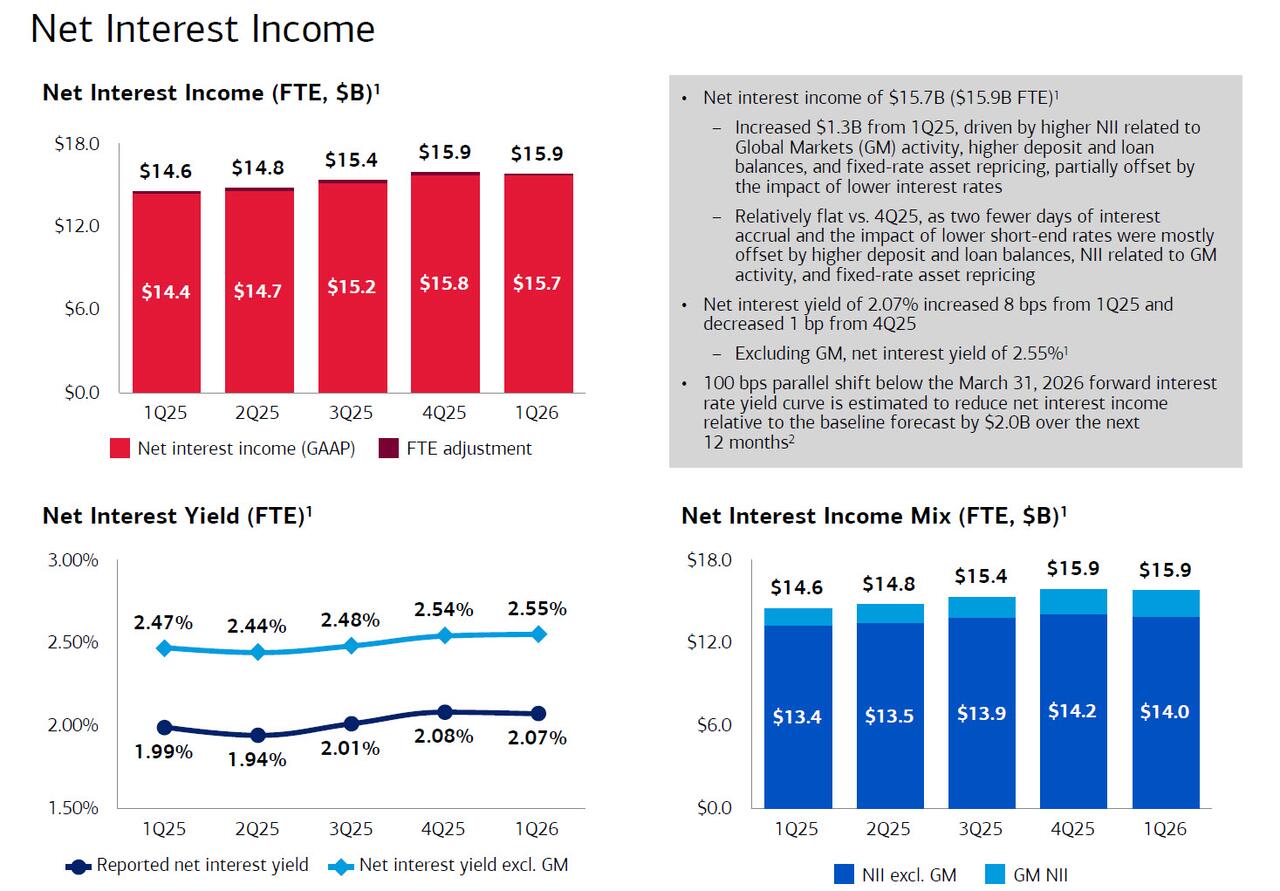

- Net interest income FTE $15.91 billion

- Wealth & investment management total revenue $6.71 billion, beating estimate $6.59 billion

Last month, BofA Co-President Dean Athanasia said that he was feeling good about net interest income, expecting growth of at least 7%. Well, the final number was even stronger, and the bank reported NII of $15.7 billion, up 9% from the first quarter of 2025 (more below). Just as importantly, BofA raised its full-year NII forecast, now expecting it to grow 6%–8%, up from previous estimates of 5%–7%, driven by strong first-quarter performance, and suggesting the Fed’s rate cuts won’t negatively impact the bank.

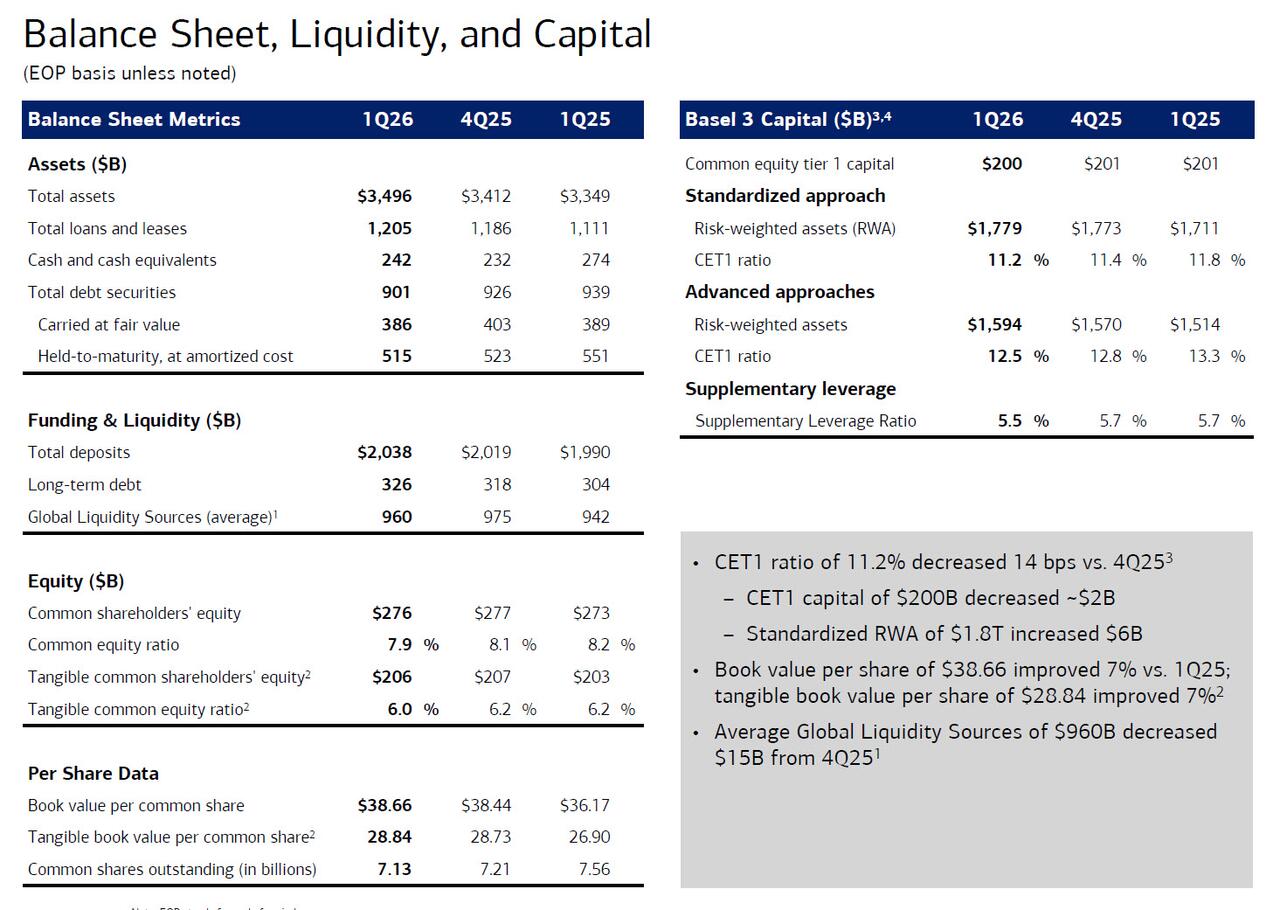

Balance sheet metrics were also solid

- Return on average equity 12%, estimate 10.8%

- Return on average assets 0.99%, estimate 0.92%

- Return on average tangible common equity 16%, estimate 14.5%

- Basel III common equity Tier 1 ratio fully phased-in, advanced approach 12.5%, estimate 12.7%

- Standardized CET1 ratio 11.2%, estimate 11.4%

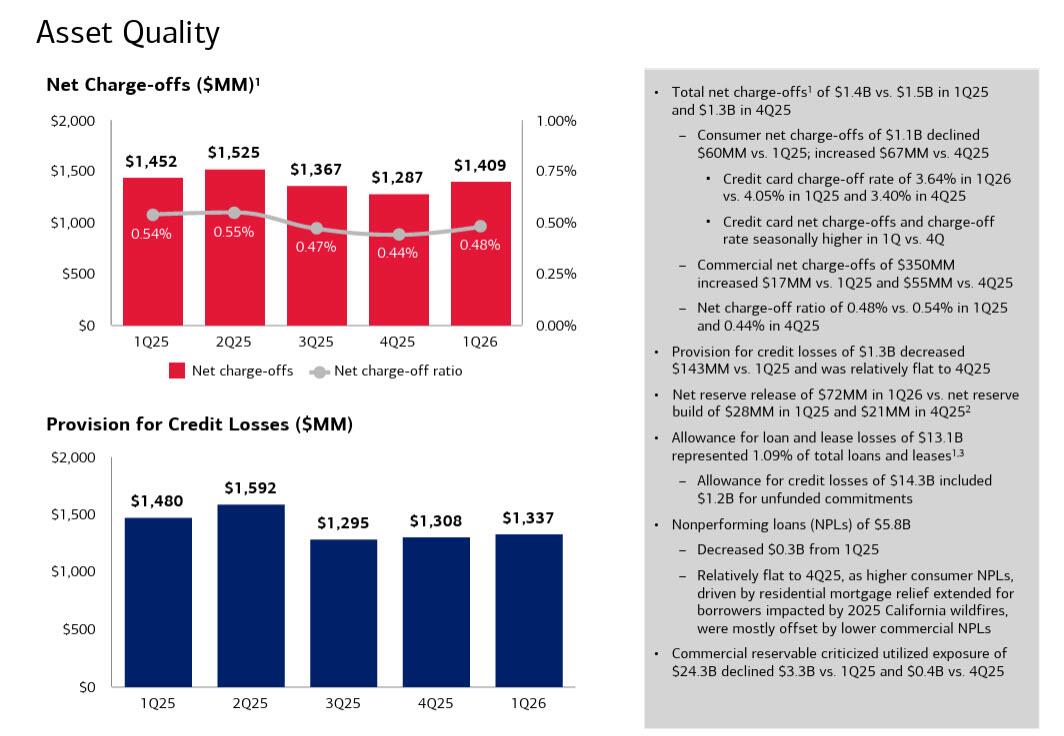

Turning to asset quality, aside from some concerns about Private Credit (see below), the results were solid with BofA’s net charge-offs down 3% to $1.41 billion, below the estimate of $1.42 billion while the provision for credit losses also dropped to $1.34 billion, and also below estimates of $1.5 billion, and down $143MM YoY. As BBG notes, the number “came in way below estimates, offsetting larger-than-expected numbers for some of its peers. Overall, the combined tally is tracking lower than feared, helping soothe concerns about private-credit contagion into financials.” BofA also announced a net reserve release of $72MM in 1Q26 vs. net reserve build of $28MM in 1Q25 and $21MM in 4Q25. Meanwhile, the allowance for loan and lease losses of $13.1B represented 1.09% of total loans and leases. Nonperforming loans (NPLs) of $5.8B decreased $0.3B from 1Q25, and were flat to 4Q25, as higher consumer NPLs, driven by residential mortgage relief extended for borrowers impacted by 2025 California wildfires, were mostly offset by lower commercial NPLs.

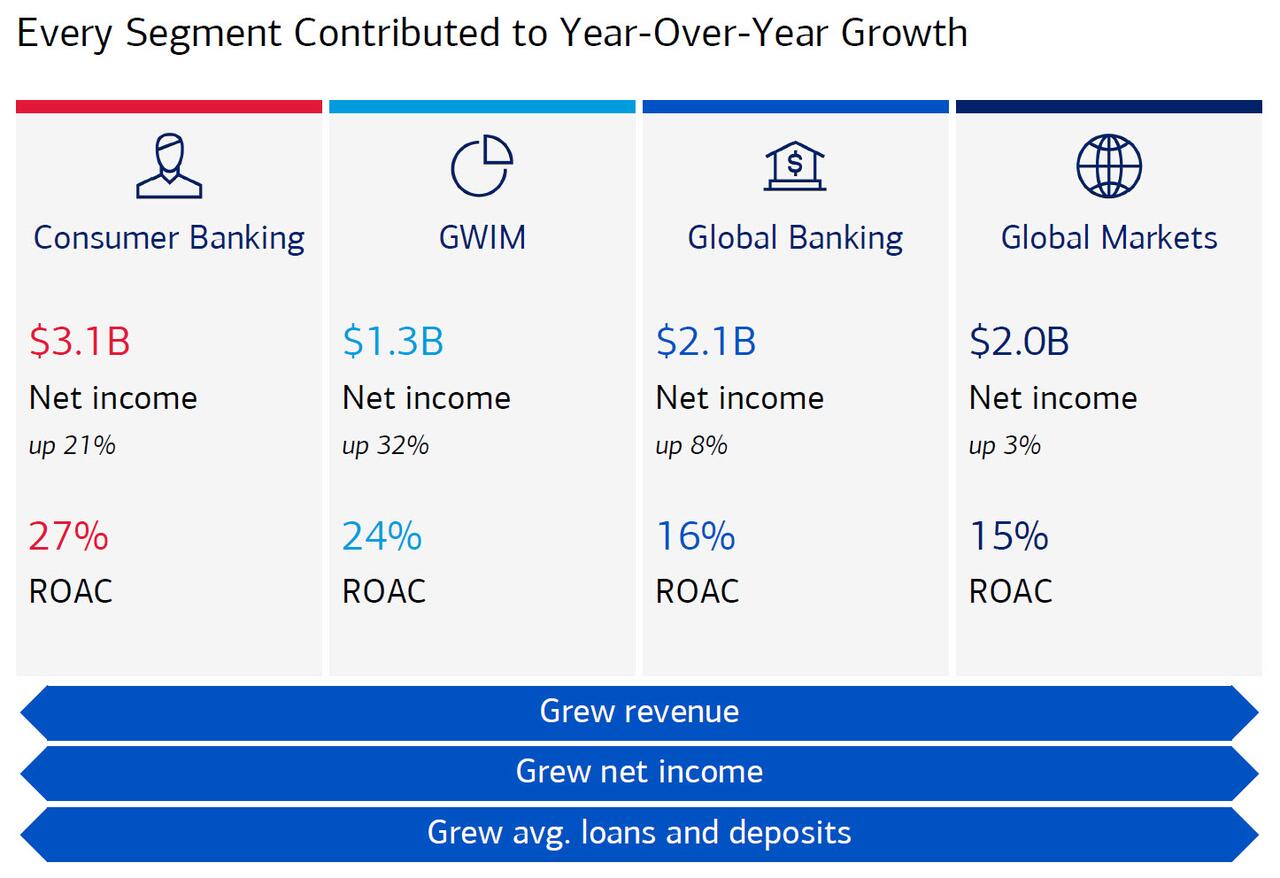

In its earnings presentation, BofA highlighted solid growth across most segments…

… and noted that every segment contributed to YoY growth.

Looking at the bank’s high margin trading businesses, results here were stellar in equities, and subpar in credit. Total revenue ex net DVA of $7.1B increased 8% from 1Q25, driven by higher sales and trading revenue, partially offset by the absence of gains related to leveraged finance positions in 1Q25. Sales and trading revenue of $6.4B increased 13% from 1Q25; excluding net DVA, up 12%

- Revenue net of interest expense $30.27 billion, beating estimates of $28.63 billion

- Trading revenue excluding DVA $6.32 billion, estimate $6.34 billion

- Equities trading revenue excluding DVA rose 20% to $2.83 billion, beating estimate $2.51 billion

- FICC trading revenue excluding DVA rose 2% to $3.50 billion, missing estimate $3.78 billion

- Trading revenue excluding DVA $6.32 billion, estimate $6.34 billion

As an aside, noninterest expense of $4.4B increased 15% vs. 1Q25, driven by higher revenue-related expenses and investments in the business, including people and technology. Lastly, average Q1 VaR tumbled to just $47MM in 1Q26 as even trading desks retrenched.

Momentum in markets was coupled with a comeback in dealmaking: this boosted investment-banking revenue to $1.89 billion, above the average estimate of $1.79 billion. Fees for advising on mergers and acquisitions rose to $553 million. The bank’s equity-capital markets business generated $353 million in revenue, while debt-underwriting revenue totaled $986 million, with both beating estimates. Analysts had expected revenue of $312 million and $963 million, respectively.

The second-largest US bank said that net interest income, a key source of revenue for the company, rose 9% to $15.7 billion. Analysts had expected a 6.5% increase for NII, the revenue collected from loan payments minus what depositors are paid. Net Interest Yield dropped from 2.08% to 2.07% as a result of declining interest rates.

The company’s loan balances rose 8.5% to $1.21 trillion at the end of the first quarter, above analysts’ estimates of $1.19 trillion. Lending has been a key focus for investors, with interest rates holding steady.

Bank of America’s noninterest expenses were up 4.3% to $18.5 billion from a year earlier. Charges and costs are another focal point for investors, with persistent inflation putting pressure on spending. Analysts had expected a 4% increase to $18.47 billion.

Earlier in the week, JPMorgan and Citigroup reported earnings that were boosted by record trading results. Wall Street banks have also been tallying and detailing their exposure to the private-credit industry, with many investors on edge over valuations and the growing impact of artificial intelligence.

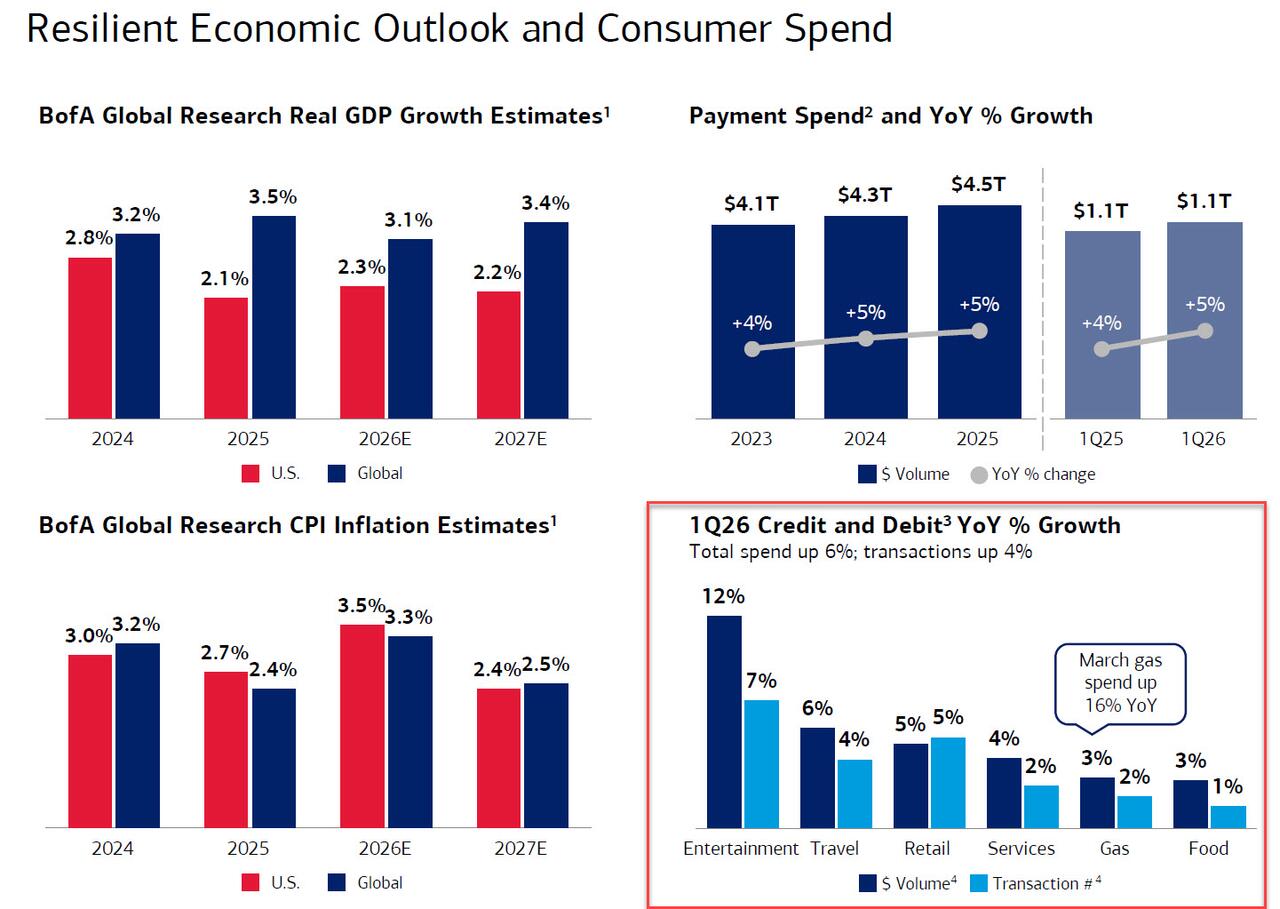

Commenting on the state of the US consumer, CEO Brian Moynihan said consumer spending points to a “resilient American economy”, while also warning of risks. Earlier, JPMorgan CEO Jamie Dimon said “the U.S. economy remained resilient in the quarter, with consumers still earning and spending and businesses still healthy.” Wells Fargo CEO Charlie Scharf: “While markets have been volatile, we still see continued resiliency in the underlying economy and the financial health of the consumers and businesses we serve remains strong, though the impact of higher oil prices will likely take some time to materialize.”

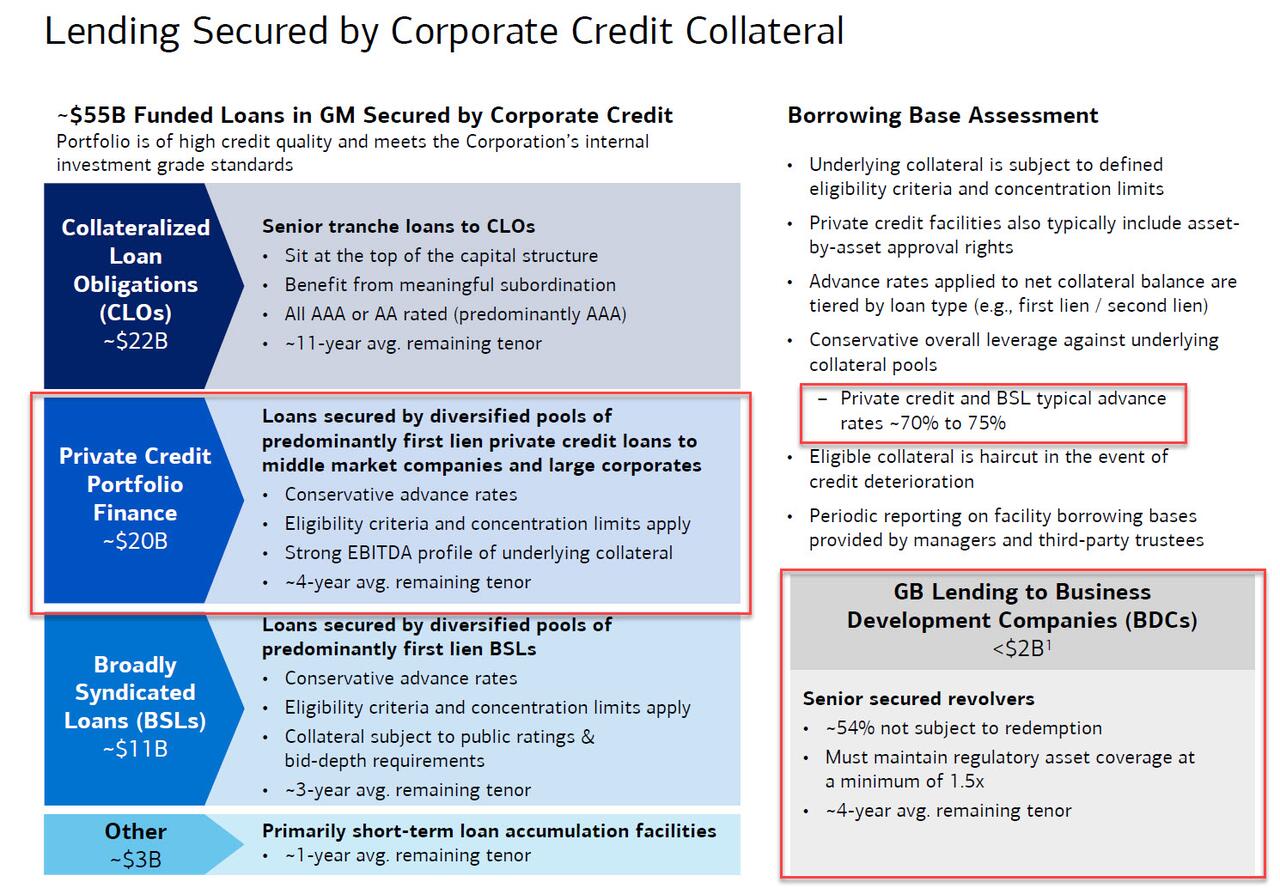

Turning to the number one topic in banking these days, Bank of America disclosed $20 billion of private credit exposure, noting that typical advance rates on private credit and broadly syndicated loans are between 70% to 75%. The company said the underlying collateral of those loans are showing “strong” earnings and are often senior in the credit stack. BofA also noted that it has less than $2 billion in lending to BDC companies which have been the epicenter of the private credit meltdown.

Bank of America’s results also offered a look at how US consumers fared during the first three months of the year with investors eager to hear details on the national economy from bank executives whose firms cater to America’s consumers and businesses. The bank noted that total credit and debit-card spending was up 6% in the first quarter, while consumers are facing pressure from higher gas prices: spending on gas was up 16% in March from a year earlier.

“We remain watchful of evolving risks,” CEO Brian Moynihan said in a statement. “However, we saw healthy client activity, including solid consumer spending and stable asset quality, indicating a resilient American economy.” Earlier this week, JPMorgan, Citigroup and Wells Fargo also said consumer spending was holding up despite surging gas prices.

Shares of Charlotte, North Carolina-based Bank of America, rose about 4% to $55 in early trading Wednesday, a two month high. They’ve gained 45% in the 12 months through Tuesday, outpacing the 9.8% increase in the S&P 500 Financials Index.

The full BofA Q1 presentation is below (pdf link)

Tyler Durden

Wed, 04/15/2026 – 10:24

via ZeroHedge News https://ift.tt/lWDaxgZ Tyler Durden