Key Events This Week: Warsh Nomination Hearing, Retail Sales, Fed Blackout, Earnings

As the war in Iran enters its 8th week, Deutsche Bank’s Jim Reid says that recent developments can be framed in two ways: either five steps forward towards peace and three back (seems more apt than three and two), or as evidence that the two sides remain far enough apart that a lasting deal will be extremely hard to achieve and markets have become far too optimistic. Reid leans more towards the former, but the comparison with recent history is uncomfortable. Remember the 10%+ S&P 500 rally in the early weeks of the war in Ukraine, when hopes briefly grew of an early negotiated settlement, only to be disappointed. That episode is a clear warning sign.

That said, the political calculus around Iran may be different. According to Nate Silver’s Silver Bulletin, President Trump’s approval rating dipped notably after the war began but appears to have stabilised since the two-week ceasefire was announced on 7 April—possibly reflecting the subsequent fall in petrol prices. A renewed deterioration in negotiations would therefore be unlikely to help approval ratings if oil and gas prices were to rise again.

The headline news over the weekend was Iran stating that the Strait of Hormuz was shut less than 24 hours after indicating on Friday that it would reopen. Shipping through the strait has now again ground to a halt after picking up on Saturday. On Friday afternoon in London, Polymarket had priced the probability of Strait traffic returning to normal by the end of May as high as 84%. That has now fallen back to around 66%, close to last Thursday’s level, but still well above the 37% probability priced this time last week.

The current ceasefire is due to expire at some point on Wednesday. President Trump struck a more hawkish tone yesterday, posting that while his negotiators will be in Islamabad for talks tonight (with possible talks reported for Tuesday), if Iran does not accept the deal on the table the US will “knock out every single power plant and every single bridge in Iran”. Iran’s state TV reported last night that Iran has “no plans for now to participate” in another round of talk with the US. Meanwhile, we heard that the US Navy had intercepted and boarded an Iranian cargo vessel in the Gulf of Oman, marking the first such seizure since the US announced its blockade of Iranian shipping.

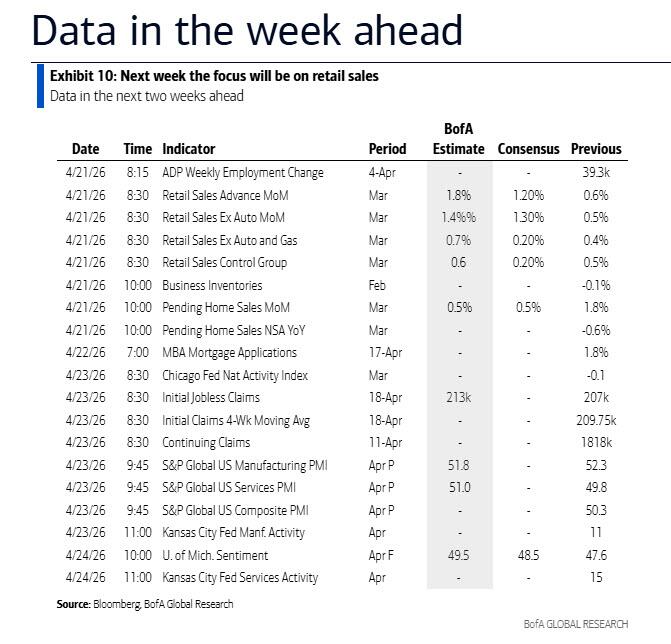

So while all eyes will be focused on the middle east, in terms of the week ahead, in the US, the main event in a quiet week for data and for Fedspeak given the media blackout has now started, comes tomorrow morning at 10:00am ET, when Kevin Warsh, President Trump’s nominee to become the next Chair of the Federal Reserve, appears before the Senate Banking Committee for his confirmation hearing. Although Warsh has said little publicly since being nominated, his earlier remarks offer important clues. He has previously argued that the US economy faces powerful disinflationary forces stemming from deregulation and the rapid diffusion of artificial intelligence, a mix that should ultimately allow interest rates to move lower. That narrative is likely to feature prominently in his testimony. However, the economic backdrop has shifted in recent months, making the case for near term easing less straightforward. The labor market has stabilized, inflation measures such as PCE have surprised to the upside, and the conflict in Iran has introduced renewed upside risks to prices via energy channels. See our economists’ latest forecasts here from the end of last week where they have removed the one cut in 2026 that they previously had.

While Warsh has spoken in favor of rate reductions over time, he is not generally viewed as structurally dovish. If anything, his instincts have historically leaned more hawkish than many of his peers’. The delicate balancing act on Tuesday will be how he frames a longer-term desire to lower rates while acknowledging that current conditions do not necessarily justify imminent cuts. Treasury Secretary Scott Bessent’s recent comment that he would “understand if the Fed needs to wait on rate cuts” may give Warsh some political cover, allowing him to argue that temporary inflation risks require near term vigilance before policy can ease later on.

Beyond rates, senators are likely to probe Warsh on several other fronts. He has long been critical of the Fed’s balance sheet policies, though expectations of rapid change have faded, with consensus now favoring a gradual approach that first requires regulatory adjustments to reduce banks’ demand for reserves — a view shared by several current Fed officials. He is also expected to revisit his criticism of forward guidance, particularly its detailed use outside of crisis periods, potentially signalling a desire to simplify how the Fed communicates policy intentions. Fed independence will loom large too, especially at a time when inflation has remained above target for an extended period, oil prices have surged again, and political pressure to cut rates has intensified. Even assuming Warsh ultimately secures confirmation, risks remain, with Senator Thom Tillis reiterating that he intends to block progress on Fed appointments until the Department of Justice investigation into Chair Powell is resolved.

With Fed officials in their pre meeting communications blackout, economic data will do what it can to fill the void. Tomorrow also brings the most important release of the week in the form of March retail sales. Headline sales are expected to rebound by 1.2% month on month (DB forecast), up from 0.6% previously, helped by a recovery in auto sales. Excluding autos, sales are forecast to rise by a still solid 0.8%, compared with 0.5% last month, though much of that strength is likely to reflect higher petrol prices rather than a broad resurgence in discretionary spending. The retail control group, which feeds directly into GDP calculations, is expected to grow by a more modest 0.2%, down from 0.5% previously, suggesting that underlying goods demand remains steady but unspectacular.

Later in the week, Thursday brings a handful of releases that will help round out the picture. Initial jobless claims are expected to edge up to 210,000 from 207,000, a move that will be watched closely as the data coincide with the survey window for April’s employment report. While monthly payroll numbers have been volatile, most broader measures point to a labor market that has largely stabilized over the past year and looks in better shape now than it did to many prior to the Iran War. The same day also delivers preliminary S&P Global PMIs, with manufacturing expected to ease slightly to 52.1 from 52.3, while services are forecast to recover to 51.4 from 49.8. Any commentary on supply chains or pricing pressures linked to Middle Eastern developments will be scrutinized, even if the surveys only partially capture the latest geopolitical shifts.

Across the globe, Thursday also sees the global flash April PMIs which will give a sense on how companies are viewing the current conflict, even if newsflow, net net, has improved of late. The prices paid components will be worth a watch.

There are plenty of indicators due in the UK, including labour market data tomorrow and March inflation on Wednesday. Our UK economist forecasts headline CPI to jump to 3.3% YoY, with core staying roughly steady at 3.2% (see full preview here). There will also be the March retail sales report and the April GfK consumer confidence indicator due Friday.

Sentiment data is also a theme for next week in the rest of Europe, with releases featuring the ZEW survey (tomorrow) and the Ifo survey (Friday) in Germany, as well as consumer confidence in the Eurozone (Wednesday) and France (Friday). Briefly turning to European political events, the list includes the EU leaders’ informal summit on Thursday and EU foreign affairs council meeting tomorrow. Elsewhere, March inflation will be in the spotlight in Japan on Friday when the national CPI is due. There will also be the March CPI report in Canada (today) and the Q1 CPI (tomorrow) in New Zealand.

Rounding out with corporate earnings, there will be a number of companies across defence (RTX and Lockheed Martin), energy (SLB, Baker Hughes and Halliburton) and the materials (Newmont, Freeport-McMoRan) sectors reporting, whose results and outlook will be of interest amidst the Iran conflict. A number of airlines also post results. Tech names for this week will include Tesla, SK Hynix, Intel and SAP. Other highlights are Procter & Gamble, General Electric, American Express and Blackstone. See the full day-by-day week ahead at the end for more.

Day-by-day calendar of events courtesy of DB

Monday April 20

- Data: Japan February Tertiary industry index, Germany March PPI, Eurozone February construction output, Canada March CPI

- Central banks: China 1-yr and 5-yr loan prime rates, BoC business survey

Tuesday April 21

- Data: US April Philadelphia Fed non-manufacturing activity, March retail sales, pending home sales, February business inventories, UK February average weekly earnings, unemployment rate, March jobless claims change, Germany April Zew survey, France March retail sales, Eurozone April Zew survey, New Zealand Q1 CPI

- Central banks: ECB’s Nagel, Guindos and Kocher speak

- Earnings: General Electric, UnitedHealth, RTX, Intuitive Surgical, Danaher, Interactive Brokers, Capital One Financial, ASM, DR Horton, MSCI,EQT, Halliburton, United Airlines

- Other: US-Iran ceasefire to expire, the Senate Banking Committee’s confirmation hearing for Kevin Warsh, EU foreign affairs council meeting

Wednesday April 22

- Data: UK March CPI, RPI, PPI, February house price index, Japan March trade balance, Eurozone April consumer confidence

- Central banks: ECB’s Lagarde, Lane, Nagel and Sleijpen speak

- Earnings: Tesla, Lam Research, GE Vernova, Philip Morris, IBM, Texas Instruments, AT&T, Boeing, CME, ServiceNow, Boston Scientific, Moody’s, CSX, Kinder Morgan, Sandvik, Southwest Airlines, Evolution

- Auctions: US 20-yr Bond (reopening, $13bn)

Thursday April 23

- Data: US, UK, Japan, Germany, France and the Eurozone April flash PMIs, US March Chicago Fed national activity index, April Kansas City Fed manufacturing activity, initial jobless claims, UK March public finances, France April business confidence, EU27 March new car registrations, Canada March industrial product, raw materials price index

- Central banks: ECB’s Nagel speaks

- Earnings: SK hynix, Intel, American Express, SAP, Thermo Fisher Scientific, NextEra Energy, Blackstone, Union Pacific, Honeywell International, Lockheed Martin, Newmont, Sanofi, Comcast, Freeport-McMoRan, Digital Realty Trust, Baker Hughes, Nokia, Orange, Nasdaq, DNB Bank, PG&E, Saab, Keurig Dr Pepper, Dassault Systemes, Dow, American Airlines

- Auctions: US 5-yr TIPS ($26bn)

- Other: EU leaders’ informal summit in Cyprus (through April 24)

Friday April 24

- Data: US April Kansas City Fed services activity, UK April GfK consumer confidence, March retail sales, Japan March national CPI, PPI services, Germany April Ifo survey, France April consumer confidence, Canada February retail sales

- Earnings: Procter & Gamble, HCA Healthcare, Keyence, Eni, SLB, Volvo, Yara

* * *

Finally, looking at just the US, Goldman writes that the key economic data release this week is the retail sales report on Tuesday. Fed officials are not expected to comment on monetary policy this week, reflecting the blackout period ahead of the May FOMC meeting. Fed Chair nominee Kevin Warsh will have his nomination hearing on Tuesday.

Monday, April 20

- There are no major economic data releases scheduled.

Tuesday, April 21

- 08:30 AM Retail sales, March (GS +1.0%, consensus +1.2%, last +0.6%); Retail sales ex-auto, March (GS +1.1%, consensus +1.3%, last +0.5%); Retail sales ex-auto & gas, March (GS +0.1%, consensus +0.2%, last +0.4%); Core retail sales, March (GS +0.1%, consensus +0.2%, last +0.5%): We estimate core retail sales increased 0.1% in March (ex-autos, gasoline, and building materials; month-over-month SA), reflecting mixed alternative data and a headwind from potential residual seasonality. We estimate headline retail sales increased 1.0%, reflecting sharply higher gasoline prices and an increase in auto sales. On an inflation-adjusted basis, we forecast a 1.0% decline in headline retail sales and a 0.1% decline in the control group.

- 10:00 AM Business inventories, February (consensus +0.3%, last -0.1%)

- 10:00 AM Pending home sales, March (GS +0.5%, consensus -0.2%, last +1.8%)

- 10:00 AM Federal Reserve Chair nominee Warsh nomination hearing: Federal Reserve Chair nominee Kevin Warsh will give prepared testimony and answer questions from members of the Senate Banking Committee in a nomination hearing. A livestream of the hearing is expected.

Wednesday, April 22

- There are no major economic data releases scheduled.

Thursday, April 23

- 08:30 AM Initial jobless claims, week ended April 18 (GS 220k, consensus 210k, last 207k); Continuing jobless claims, week ended April 11 (consensus 1,820k, last 1,818k)

- 09:45 AM S&P Global US manufacturing PMI, April preliminary (consensus 52.5, last 52.3); S&P Global US services PMI, April preliminary (consensus 50.1, last 49.8)

Friday, April 24

- 10:00 AM University of Michigan consumer sentiment, April final (GS 47.5, consensus 48.4, last 47.6); University of Michigan 5-10-year inflation expectations, April final (GS 3.4%, last 3.4%): We estimate that the University of Michigan consumer sentiment index ticked down to 47.5 and that the survey’s measure of long-term inflation expectations remained at 3.4% in the final April reading, reflecting roughly unchanged gasoline prices and the timing of the announcements of the US-Iran ceasefire and the subsequent US blockage of the Strait of Hormuz within the interview period for the final survey.

Source: DB, Goldman

Tyler Durden

Mon, 04/20/2026 – 10:05

via ZeroHedge News https://ift.tt/82UTg13 Tyler Durden