Tesla Surges After Beating Expectations, Says “Rebound Of Demand” For EVs

Heading into today’s TSLA earnings, Wall Street was braced for a miss, with debate only around how big it would be. Well, it wouldn’t be an Elon Musk joint if there wasn’t some big twist, and sure enough, the stocks is soaring after hour on what can only be described as a very big, and very unexpected beat.

Here is what the company reported for the first quarter:

- Rev. $22.39B, beating Est. $22.19B

- Adj EPS 41c, beating Est. 34c, the second straight quarter Tesla’s earnings beat expectations.

- EPS 13c vs. 12c Y/Y

- Gross Margin 21.1%, beating Est. 17.7%

- Auto Gross Margin Ex-Reg Credit 19.2% vs 12.5% Y/Y

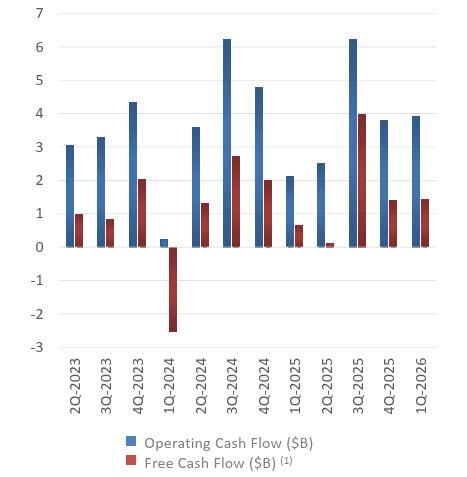

- Free Cash Flow positive $1.44B, beating est. Negative $1.86B

Perhaps the most interesting of the above, besides the modest beats in revenue (which benefited from positive FX impact of about $900 million in the quarter translating into $200 million at the bottom line; as well as higher average selling prices) and EPS, is that despite weak EV and energy unit sales, Tesla’s reported gross margins in both businesses are up. Generally, fixed costs spread over fewer units puts pressure on GPM, all else equal. The auto margin, less credits, of 19.2% is up q-o-q and y-o-y. In energy, despite lower revenue both sequentially and versus last year, Tesla reports what looks like a record gross margin for that business of almost 40%.

Yet while Tesla turned in higher auto gross margins than expected, given weak sales, that fades away when reading down the P&L: operating margin of just 4.2%.

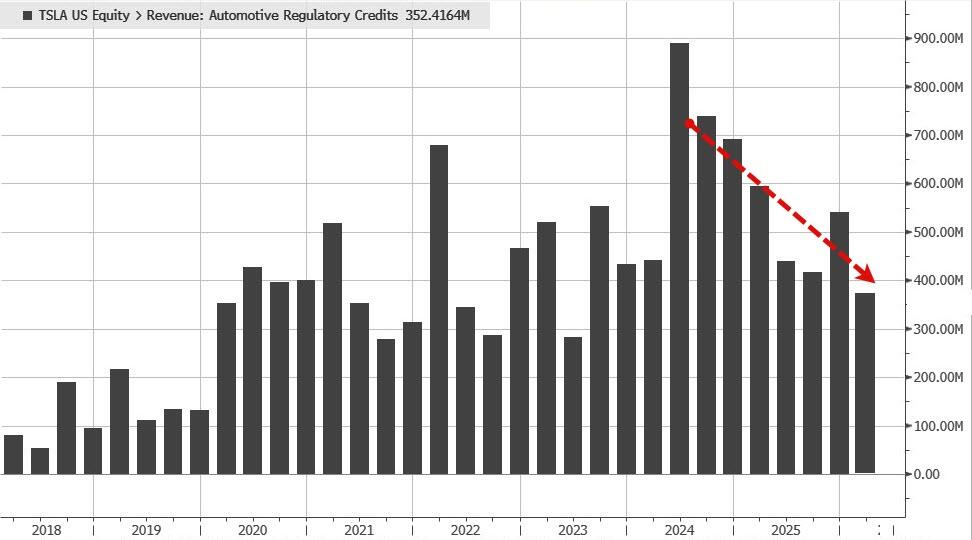

Meanwhile, earnings continue to subsist heavily on a diet of regulatory credit sales, which in Q1 dropped to 381 million from $337 million a year ago, and net interest income.

And visually:

Starting at the top, it’s no surprise that that TSLA likes soaring gas prices, which have helped a “rebound in demand” in the core US market, to wit: “We saw continued growth in demand for our vehicles in markets in APAC and South America, while also seeing a rebound of demand in both EMEA and North America.”

The surprisingly optimistic comments come several weeks after the automaker reported one of its worst quarters of auto sales in years.

Here is how TSLA laid out its automotive business” We are focused on optimizing our vehicle product portfolio, with an emphasis on vehicles designed for a fully autonomous future. We continued the launch of Model 3 and Model Y trims globally, including the roll-out of the Model YL in markets outside of China and more affordable trims of both models. We also began deliveries of Cybertruck in the UAE.“

Unlike recent quarters, we didn’t have an “other updates” section with a surprise investment, there’s minimal change in language and if anything it projects a lot of confidence in core business. In short, a “no surprises, no drama” print.

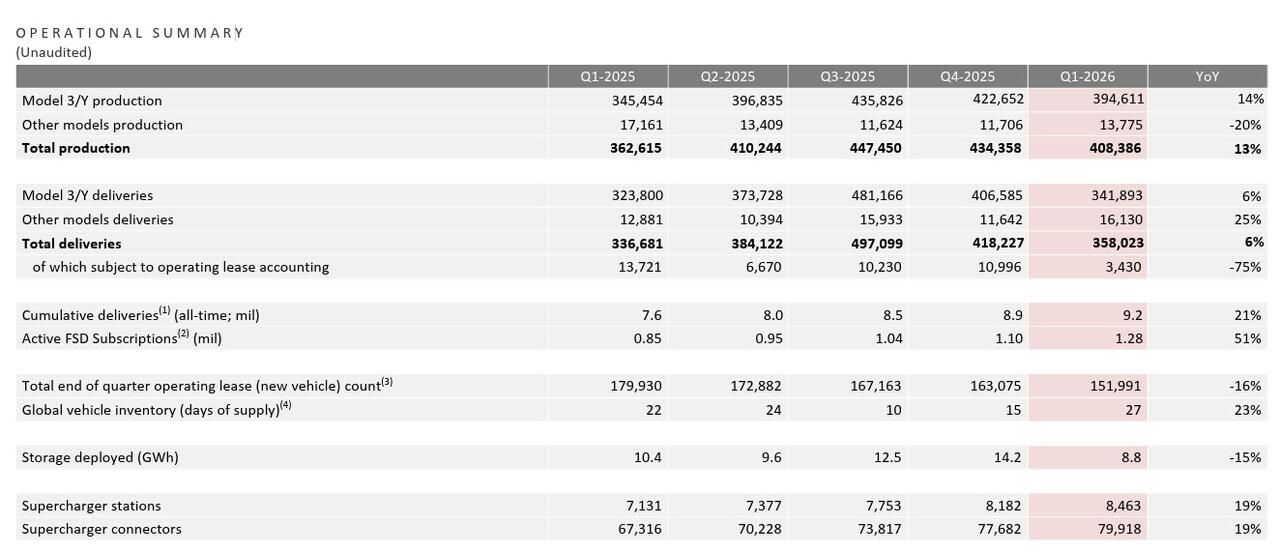

One key metric that is also key to Elon Musk’s pay package, is active FSD subscriptions. They were up slightly this quarter to 1.28 million from 1.1 million at the end of 4Q, and up a whoppint 51% YoY.

There were some working capital issues: global inventory spiked to 27 days, up from 15 days, which was to be expected given that Tesla produced more than 50,000 cars than it delivered in 4Q, but still that’s a lot of inventory to clear.

And speaking of inventory, Tesla has overcapacity in its factories, so now the company is rolling out the Model YL (Long) in “markets outside of China” and more affordable trims of both models. It also began deliveries of cybertruck in the UAE.

While energy storage had been Tesla’s fastest-growing sector but that trend failed to continue into the first quarter, when year-over-year revenue slipped 12% and quarterly deployments of 8.8 gigawatt-hours were the lowest in a year. This is what it had to say about the business:

“Progress continued at the new Megafactory outside Houston, which will produce the Megapack 3 for Megablock. Start of production is on track for later this year. We began meaningful customer deployments of Tesla’s first in-house designed solar panel produced at Gigafactory New York. The new panel has 18 individual power zones – 3x more than a conventional residential panel – enabling it to reliably produce more energy in shady conditions. Other innovations include improved aesthetics and faster and simpler installation.”

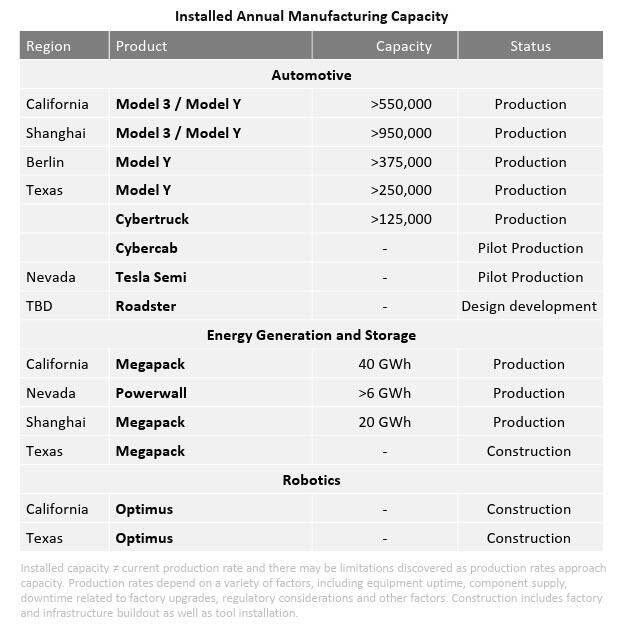

Turning to the far more important robotics business, the company expects the first large-scale Optimus factory to start in Q2. The first generation line, designed for 1 million robots a year, will replace the Model S and Model X lines in Fremont. The company is also preparing Gigafactory Texas for the second-generation line, which is being designed for long-term annual production capacity of 10 million robots.

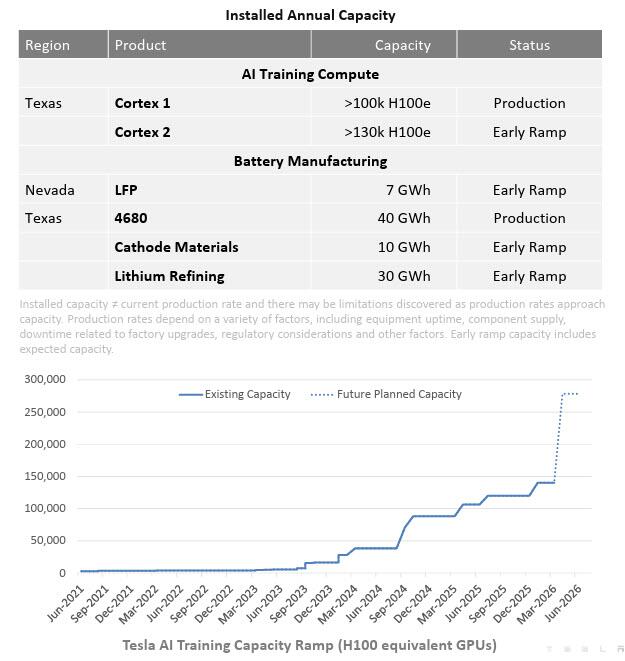

Turning to AI, Tesla said that “Cortex 2 is now online and has started running training workloads.” Tesla continues to ramp its onsite training infrastructure to ensure sufficient compute resources for the development of our AI products and services and “are also continuing our custom silicon development with Dojo 3 in an effort to reduce the cost of training over time.“

In the battery business, “ramp has begun across our new battery and material factories, including LFP cells in Nevada, cathode material and lithium refining in Texas.” Battery pack capacity continues to be the limiting factor on ramping our vehicle production the company said.

What is the company’s other supporting infrastructure? This is what it had to say: “Gigafactory New York is now producing V4 Supercharging cabinets, which boast 3x the power density and 2x the number of stalls per cabinet compared to V3. Alongside the ramp of Tesla Semi, we are deploying public Megachargers, including our first one in Southern California. While we aim to leverage as much of our existing investments as possible, we continue to build out our supporting infrastructure for our vehicle and mobility businesses, including Robotaxi expansion, across established and growth markets around the world. In Q1, we added over 2,200 net new Supercharging stalls, growing the network 19% year-over-year. This year we look to increase our presence in Japan by doubling our service centers and expanding our Supercharger coverage in the world’s third largest vehicle market”

The company’s outlook was generally very favorable:

- Volume: “We are focused on maximum capacity utilization at our factories. Deliveries and deployments will be impacted by aggregate demand for our products, supply chain readiness and allocation decisions between sale to customers or use for our owned and operated fleet.”

- Cash: “We will manage the businesses such that we ensure a strong balance sheet, maintaining sufficient liquidity to fund our product roadmap, long-term capacity expansion plans – including further vertical integration – and other expenses.”

- Profit: “While we continue to execute on innovations to reduce the cost of manufacturing and operations, over time, we expect our hardwarerelated profits to be accompanied by an acceleration of AI, software and fleet-based profits.”

- Product: “We continue to evolve and augment our product lineup with a focus on cost, scale and future monetization opportunities via services powered by our AI software. We remain focused on growing our sales volumes through a differentiated and efficiently managed product portfolio, which includes leveraging and optimizing our existing production capacity before building new factories and production lines. Cybercab, Tesla Semi and Megapack 3 are on schedule for volume production starting in 2026. First-generation production lines for Optimus are being installed in anticipation of volume production. Capacity build out and ramp related to our multi-year infrastructure initiatives, including AI compute, solar, battery material and semiconductor manufacturing are underway.”

There was yet another sign of convergence between Elon Musk’s companies:

“Our partnership with SpaceX aims to build the largest chip fab ever: vertically integrating logic, memory and advanced packaging to allow for rapid iteration as we anticipate greater chip demand than what existing and planned industry capacity can accommodate. This begins with the Tesla-owned Research Fab on our Gigafactory Texas campus.”

As for Terafab, we already knew that this mega project would start with a pilot line. But what’s interesting is this is Tesla’s and not a part of the joint-venture with SpaceX/xAI. Here’s what the deck says:

“This begins with the Tesla-owned Research Fab on our Gigafactory Texas campus.”

Last but not least, TSLA surprised the market by reporting a positive free cash flow…

… but Tesla pulled a number of levers:

- Stock-based comp nearly 2x, year-over-year

- Big swing in accounts payable and receivables add ~$1.9B, offsetting much of the big inventory headwind

- Most of all, capex at just $2.5B, or only about half the run-rate implied by guidance

Also don’t expect free cash flow to remain positive: Tesla is working to ramp up production as part of a more than $20 billion spending plan this year. For the first three months of the year, however, Tesla spent less than $2.5 billion, half the outlay the company will need to average per quarter to reach its expenditure forecast for the year. This contributed to Tesla posting $1.4 billion in positive free cash flow for the quarter, far better than analysts’ expectation that the carmaker would burn through almost $1.9 billion.

Looking ahead the company is excited “about Tesla’s positioning in 2026 with tailwinds persisting for the autos business, our continued progress on FSD (Supervised), the ramp of Robotaxi, progress on Optimus ahead of mass production and the growth of our energy production capacity”

Judging by the stock reaction, the market is also excited, and as Interactive Brokers Chief Strategist Steve Sosnick writes, this print is “good enough.” He highlighted the adjusted profit and revenue beats as well as the “surprise” positive flip to free cash flow. “The car business improved, and there is nothing that disrupts the futurism that juices Tesla’s valuation. Now it’s up to what Musk says on the call”

Others, like Adam Sarhan, of 50 Park Investments, were also happy: “The real story isn’t just these numbers — it’s the execution on the roadmap. The trajectory feels constructive. Longer term, I’m still very bullish on Tesla’s positioning in AI, robotics, and energy. These results show resilience and set up better comps ahead. The market will digest the forward commentary tonight, but the fundamentals are pointing up.”

That said, the initial euphoric reaction may moderate if analysts interrogate this idea of rebounding demand on the earnings call, given that Tesla has loads of cars in inventory right now.

Tyler Durden

Wed, 04/22/2026 – 16:46

via ZeroHedge News https://ift.tt/VW8H0CI Tyler Durden