Futures Rebound, Trade At All Time Highs On, What Else: Tech And Iran Optimism

US equity futures are higher and just shy of a new record, with technology names leading futures higher ahead of April jobs report, after Trump’s assertion that the Iran ceasefire is still holding despite an exchange of weapons between the US and Iran overnight, and a deep weekly loss for oil help futures regain positive momentum. Markets are higher ahead of NFP data later this morning following yesterday’s very ‘unwindy’ session (High Beta Momo -7.96%, Software vs Semis +5.83%, Power -3.44%, HF VIP Longs -1.36%). As of 8:00am ET, S&P futures rise 0.5% and are back over 7,400 while Nasdaq futures gain 0.7%. Pre-market, Mag 7 are all higher led by NVDA +0.9% and TSLA +0.9%.Sentiment reversed from Thursday’s drop after Trump last night said the recent US strikes on Iranian military facility does not affect the ceasefire status. This morning there are reports that Iran seized an oil tanker for violations (one which was carrying Iranian oil). The Ocean Koi tanker attempted to “disrupt oil exports and the interests of the Iranian nation.” (Tasnim) Trump’s 10% global tariff under the Section 122 was found unlawful by the US Court of International Trade, but the outcome was mostly irrelevant. A busy night with AI headlines: (i) NVDA and IREN announce strategic partnership on AI infra; (ii) CoreWeave fell on weak revenue guidance and higher spending forecast; (iii) SK Hynix reported that they have received offers to invest in chip production lines. (iv) TSMC posted 17.5% growth in April sales, slowest in six months. Oil (WTI Crude) is unchanged at $94.80; bond yields are 1-3bp lower the 10Y yield at 4.38%; The dollar headed for a second straight week of losses. precious metals erased earlier gains with ags all higher. Today’s economic data slate includes April jobs report (8:30am), May preliminary University of Michigan sentiment and March wholesale trade sales (10am).

In premarket trading, all Mag 7 stocks are higher (Tesla +1.4%, Alphabet +0.05%, Nvidia +0.9%, Microsoft +0.03%, Amazon +0.3%, Meta Platforms +0.3%, Apple +0.8%)

- Akamai (AKAM) rises 25% after the company announced that a leading frontier AI model provider had committed to $1.8 billion over seven years for its Cloud Infrastructure Services. The company also reported its first-quarter results and gave an outlook.

- Block (XYZ) gains 7% after the digital payments company forecast adjusted operating income for the second quarter that beat the average analyst estimate.

- Expedia (EXPE) drops 7% after the online travel company forecast tepid gross bookings for the second quarter, with analysts pointing to macroeconomic pressures weighing on guidance.

- Fluence Energy (FLNC) rises 23% as Roth analyst Justin Clare raised the recommendation to buy on growing orders.

- Forward Air (FWRD) plunges 45% after the transportation services firm said it received no actionable proposals for a sale.

- JFrog (FROG) rises 14% after the software company reported first-quarter results that beat expectations and gave an outlook that is seen as conservative. Analysts highlighted an acceleration in cloud revenue growth as a highlight.

- Innodata (INOD) climbs 39% after the professional services company boosted its revenue forecast for the full year.

- Monster Beverage (MNST) rises 7% after the drinks company reported first-quarter adjusted earnings per share that beat the average analyst estimate. JPMorgan raised its price target.

- NLight shares (LASR) rise 13% after the maker of semiconductor laser products reported adjusted earnings per share for the first quarter that beat the average analyst estimate.

- Rocket Lab (RKLB) climbs 7% as the space company reported revenue for the first quarter that beat the average analyst estimate.

- Trade Desk (TTD) falls 12% after the advertising-technology company reported adjusted first-quarter earnings that missed expectations.

- Wendy’s (WEN) rises 4% after the fast-food chain reported adjusted earnings per share for the first quarter that beat the average analyst estimate.

In AI-related news, TSMC posted its slowest pace of monthly revenue expansion since October, highlighting the potential challenges of sustaining a torrid AI-fueled pace of growth. AI data center operator CoreWeave gave a disappointing forecast for the current quarter, sparking concerns about slowing growth at a time when the company is spending heavily to bolster its operations. SoftBank Group has downsized plans for a $10 billion margin loan backed by its OpenAI stake after facing hesitation from some creditors, people familiar with the matter said. And a key company behind Thailand’s national AI effort is suspected of helping to smuggle billions of dollars worth of Super Micro Computer servers containing advanced Nvidia chips to China, with Alibaba one of multiple end customers. In other corporate news, Toyota Motor forecast an abrupt drop in operating profit due to higher raw material costs from disruptions stemming from the Iran war. Citigroup is expanding its foreign-exchange business with hedge fund and private-equity clients as global trading volumes rise

US stocks rose at the end of a week in which optimism that the conflict is nearing an end and blowout earnings from major tech firms drove the S&P 500 to a succession of records. Hopes that oil flows would soon resume through the Strait of Hormuz also eased inflation worries, even as uncertainty remains over how soon the US and Iran can reach an agreement. US markets were the standout performers on a tough day for stocks elsewhere as clashes in the Middle East risked undermining efforts to secure a permanent end to the war. Stock indexes in Europe and Asia fell. Brent advanced as much as 2.9% before trimming the move to trade just above $100 a barrel. Treasuries rose ahead of April’s payroll numbers, with the two-year yield falling one basis point to 3.90%. UK government bonds advance, led by longer-dated maturities after UK Prime Minister Keir Starmer said he had no plans to step aside as Labour leader after early results in local elections showed losses for his party.

“For now, investor sentiment remains strong as the equity market is looking through high oil prices,” said Marija Veitmane, head of equity research at State Street Global Markets. “We continue to stress that the strength of earnings is heavily concentrated in IT sectors. These sectors are also the least exposed to physical supply chains and commodity pass-through.”

In the latest developments in the Middle East, Iran said it seized a tanker that appeared to be a sanctioned vessel carrying its own oil. Meanwhile, US forces targeted missile and drone launch sites and other military assets in Iran that they said were responsible for attacking US warships transiting the strait. The clashes came as the US awaited a response from Iran on a proposed deal to open Hormuz and end the war. President Donald Trump threatened more intense strikes if Iran refuses his terms.

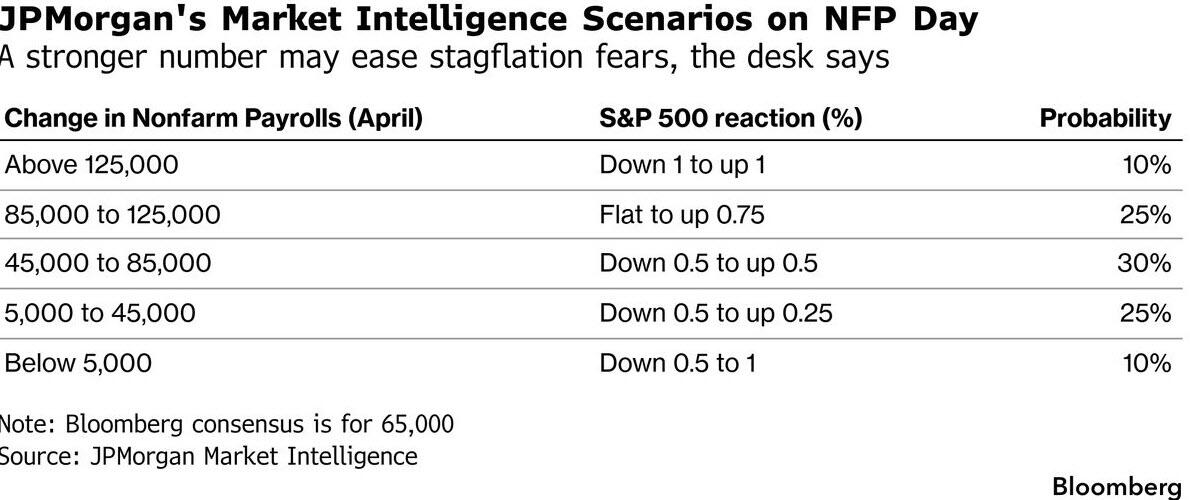

A pause in worrying headlines out of the Middle East would allow markets and the Fed to focus on nonfarm payrolls at 8:30 a.m. New York for fresh clues about US economic resilience. Bloomberg Economics expects 57,000 jobs were added in April, slightly below sellside consensus for 65,000, while the “whisper” number is 71,000. Options pricing around the print continues to drift lower, with S&P 500 options implying only about a 0.6% move on the release (our full preview is here).

“I would expect a stronger-than-expected set of figures to keep Fed hawks in charge, without necessarily taming equity appetite,” wrote Ipek Ozkardeskaya, senior analyst at Swissquote. Softer-than-expected figures “could revive dovish Fed expectations and provide further support to equity valuations, provided that war headlines leave some room for reaction.”

Jobs are a hot topic in more ways than one this Friday. Block offered a sunnier outlook for profits and growth after orchestrating layoffs linked to AI that executives said were painful but necessary. Cybersecurity firm Cloudflare plans to cut one-fifth of workers as it accelerates its shift to an agentic AI-first operating model. Upwork intends to reduce its workforce by about 24%, while Fidelity is overhauling its tech and product teams. In all cases “the increased adoption of AI tools is a huge factor,” Vital Knowledge founder Adam Crisafulli said on the recent bout of job cuts. He cautioned “this type of behaviour tends to be contagious.”

Meanwhile, investors flocked to cash and bonds last week and emerging market stocks saw their biggest outflows since January, according to Bank of America. The US had its sixth week of equity inflows at $9.3 billion, BofA’s Michael Hartnett said. Elsewhere, aggregate retail investor equity flows on Citadel Securities’ platform surged back to elevated levels last week. In other investing news, 43% of large cap active funds are outperforming their benchmarks, according to a BofA analysis of US mutual fund performance, better than the 29% that outperformed last year. Separately, some hedge fund categories, such as macro funds, appear to still have room to increase their equity exposures, according to JPMorgan strategists.

A pillar of support for equities may not be quite what it seems, according to Bloomberg Macro Strategist Simon White. Buyback announcements are surging this year. However, the risk of disappointment is rising as actual repurchases heavily lag the original commitments made, Simon writes.

Jeffrey Gundlach said he was repositioning some of DoubleLine Capital’s funds for the scenario that the US government could restructure its debt in response to a potential future recession. A publicly-traded private credit fund managed by Goldman Sachs put two additional companies on non-accrual status in the first quarter, as the industry grapples with mounting concerns over exposure to businesses vulnerable to AI-driven disruption.

With earnings season in its tail end, of the 425 S&P 500 companies to have reported thus far, 84% have beaten analysts’ estimates, while 11% have missed.

In Europe, the Stoxx 600 falls 0.5%, led by declines in insurance and travel stocks while media and energy outperformed. Here are the biggest movers Friday:

- Bechtle rises as much as 6.9% following its first-quarter results as Jefferies says the IT services provider’s positive momentum has continued

- Brembo shares rise as much as 8.5% and are set for a record weekly gain after robust first-quarter results that prompted Banca Akros to raise its recommendation on the Italian auto parts firm

- Ferrovial rises as much as 3.6%, the most in a month, after the infrastructure group beats first-quarter expectations, with US managed lanes driving performance and construction also seen as solid

- Pirelli advances as much as 3.4% after delivering an in-line performance in the first quarter and slightly boosting its revenue guidance for the full year

- Rheinmetall shares fall 2.7% on Tradegate versus Germany’s Thursday close after JPMorgan cut its rating to neutral from overweight and slashed its price target by almost 30%

- Deutsche Lufthansa falls as much as 2.7% after Barclays downgraded the airline to underweight from equal-weight, saying tailwinds from routes typically served via Gulf hubs are likely to fade as capacity returns

- Commerzbank falls as much as 2.4% after its latest earnings. Analysts say the lender’s upgraded targets are ambitious, but also viewed with some skepticism as the bank steps up its defense against a hostile takeover attempt by UniCredit

- Intertek shares fall as much as 7.9%, the most in two months, as the testing and inspection company rejects EQT’s latest takeover proposal of £58.00 per share in cash

Earlier, Asian stocks fell to trim weekly gains as renewed tensions in the Middle East weighed on sentiment. The MSCI Asia Pacific Index dropped as much as 1.6% following a two-day rally as some investors took profit ahead of Iran’s response to a US peace proposal. Samsung Electronics, TSMC and SoftBank weighed the most on the regional decline. Still, the index has risen more than 5% for the week and was poised for its longest winning streak since January, driven largely by a sustained tech rally. The MSCI AC Asia Pacific Information Technology Index has surged over 13%, its best week since late 2022. Across the region, markets saw renewed risk-off sentiment on Friday after the US struck military targets in Iran in response to attacks on three Navy destroyers in the Strait of Hormuz. Australia, Indonesia and Hong Kong were among the hardest hit.

In FX, the pound gains 0.4% after PM Keir Starmer said he had no plans to step aside as Labour leader after early results in local elections showed losses for his party; the dollar falls across the board. The Norwegian krone is leading gains among the G-10 currencies, rising 1.2%.

In rates, treasuries hold small gains in early US session, led by front-end and belly sectors as oil prices stabilize. Oil prices partially unwind Thursday’s rebound despite escalation of Middle East war, with US and Iran clashing near the Strait of Hormuz. US yields richer by 1bp-2bp in belly of the curve with 5s30s spread steeper by about 1bp; 10-year near 4.37% is down 1bp with UK counterpart outperforming by around 5bp. Gilts outperform as UK Prime Minister Starmer vows to stay on despite election setback. Gilts rallied over early London session after Starmer said he’d remain as Labour leader despite the party’s election losses

In commodities, oil prices are little changed with Brent crude futures near $100 a barrel. Precious metals rise with spot silver up almost 3% and on course for a fourth day of gains. Bitcoin rises 0.5%.

Today’s economic data slate includes April jobs report (8:30am), May preliminary University of Michigan sentiment and March wholesale trade sales (10am). Fed speaker slate includes Goolsbee (11:05am and 2:20pm). Waller, Bowman, Daly and Goolsbee are panelists at Hoover Institution Monetary Policy Conference (7:30pm)

Market Snapshot

- S&P 500 mini +0.5%

- Nasdaq 100 mini +0.7%

- Russell 2000 mini +0.4%

- Stoxx Europe 600 -0.5%

- DAX -0.7%

- CAC 40 -0.6%

- 10-year Treasury yield -2 basis points at 4.37%

- VIX -0.1 points at 17.03

- Bloomberg Dollar Index -0.2% at 1188.44

- euro +0.4% at $1.1769

- WTI crude -0.8% at $94.08/barrel

Top Overnight News

- President Donald Trump said Thursday that attacks on Iran after it targeted U.S. destroyers in the Strait of Hormuz were a “love tap,” and said the ceasefire between the two countries is still in effect. ABC

- Iran is ramping up trade with China via rail to blunt the impact of a US blockade of its ports. The number of cargo trains going from Xi’an to Tehran has risen to one every three or four days from around one per week before the conflict BBG

- US prosecutors suspect a Thai AI company of helping smuggle Nvidia chips to China, with Alibaba one of multiple end customers, people familiar said. BBG

- The White House has invited a scaled-back CEO delegation to accompany President Donald Trump to Beijing next week, reflecting divisions in the administration on economic policy toward China and limited expectations for the summit. RTRS

- Sir Keir Starmer has refused to quit after a disastrous night for Labour at the polls, insisting: “I’m not going to walk away . . . and plunge the country into chaos.” With the first results in, Labour is heading for the worst local election results by any party this century. FT

- A federal trade court ruled that President Trump didn’t have the authority to impose new global tariffs after a previous set of levies was struck down by the Supreme Court in February. The decision on Thursday from the Court of International Trade invalidated Trump’s attempt to impose a new 10% tariff on goods from virtually every nation by invoking authority under Section 122 of the Trade Act. WSJ

- Big Tech’s record $725bn AI investment strategy is beginning to strain the resources of America’s largest companies, leaving them with less cash left over this year than at any point in the past decade. The combined free cash flow of the four “hyperscalers” — Amazon, Alphabet, Microsoft and Meta — is expected to fall to roughly $4bn in the third quarter, according to Wall Street’s forecasts, down from an average of $45bn in each quarter since the Covid-19 pandemic six years ago. FT

- Anthropic is weighing raising tens of billions of dollars this summer to fund a vast expansion in computing capacity, in a move that would catapult it past rival OpenAI to a valuation of almost $1tn. FT

- Ukrainian President Zelensky said Russian forces struck Ukrainian positions during the night and shows no attempt to hold the cease fire.

- US VP Vance expressed concern to tech CEOs over new AI models which can autonomously find software vulnerabilities. The White House is considering an executive order to create a formal oversight process for advanced AI models and has asked Anthropic to limit access to Mythos for organisations managing critical digital infrastructure: WSJ

- Increased hyperscaler capex has come at the expense of buybacks, which fell by 64% year/year for the group during 1Q. The hyperscalers now allocate 20% of total spending to buybacks and dividends compared with an average of 34% from 2017-2022. We expect minimal hyperscaler buyback growth through 2027. Consensus estimates show hyperscaler capex amounting to 100% of cash flows from operations this year, which in turn leaves little room to return cash to shareholders without a sharp deceleration in capex growth, a large drawdown of cash balances, or a major increase in debt. Some of the buyback headwind from the hyperscalers will likely be offset by increased buyback activity among the beneficiaries of that capex, such as semiconductor firms: Goldman Sachs

Iran Latest: Reports surrounding a potential deal:

- Iran is reviewing the US response to the 14-point proposal and is expected to formally respond on Friday, according to CCTV citing Pakistani sources.

- Any agreement with Iran would be bad for Israel, even if it includes an agreement to eliminate enriched uranium, Israeli press reported citing an official.

- Iran and the US are discussing a one-page plan for both sides to reopen the Strait of Hormuz and end hostilities for 30 days while they try to reach a comprehensive deal, NYT reported. Three senior Iranian officials say Tehran and the United States are discussing a one-page plan for both sides to reopen the Strait of Hormuz and end hostilities for 30 days while they try to reach a comprehensive deal. The talks over a short-term agreement are continuing, the officials said, with negotiators trading proposals over how to describe the framework for a potential permanent deal. The three Iranian officials said a key obstacle was the US demand for commitments in advance on the fate of Iran’s nuclear program and its stockpile of highly enriched uranium.

- “A diplomatic source told Al Arabiya: Ensuring the safe passage of ships through the Strait of Hormuz is imminent.”, Al Arabiya reports.

Iran Latest: Commentary following the US-Iran strikes:

- Iran’s Top Joint Military Command said US violated the ceasefire by targeting Iranian oil tanker and another ship entering the Strait of Hormuz; Iran will respond powerfully and without the slightest hesitation to any attack.

- US President Trump said the Iran ceasefire is still on and that the US is negotiating with the Iranians; Pakistan asked the US not to do Project Freedom during the negotiations. On energy, said we do not need to export curbs on oil and fuel.

- US President Trump posted that there was no damage done to the three US destroyers that came under fire; states that Iran is led by lunatics and that the US will knock out Iran more violently if no deal is signed fast.

- US President Trump tells ABC that the retaliatory strikes against Iranian targets are just a ‘love tap’ and the ceasefire continues to be in effect.

- US military said US forces intercepted Iranian attacks and responded with self-defence strikes on Iranian military facilities; Iranian attacks were unprovoked but no US assets were hit; do not seek escalation.

- The situation on Iranian islands and coastal cities by the Strait of Hormuz is back to normal, according to Press TV.

- Saudi Arabia has not permitted the use of its airspace to support offensive military operations, Al Arabiya reported citing sources.

- There is a high state of alert in anticipation of retaliatory attacks from Hezbollah following the assassination of the Radwan Force Commander, Israeli Channel 12 reported citing sources.

- Saudi Arabia has imposed restrictions on some aspects of US activity related to military operations in the region due to fears of possible Iranian attacks without direct US support or response, ISNA reported citing a i24 sources report.

Iran Latest: Reports of overnight strikes:

- “US military attacked Iranian targets in the Strait of Hormuz, an American official told me. The American official claimed that the attacks do not constitute a renewal of the war with Iran”, Axios’ Ravid posted.

- A massive fire at the site of Iran’s attacks last night; large fire previously detected in the Strait of Hormuz, Musandam province, has moved; another big fire has been detected 30km west of Lark Island, Tasnim reported.

- UAE announces that air defence systems are responding to a missile threat.

- Hearing explosions in Abu Dhabi and Dubai, ISNA reported.

- Reactivation of air defence in western areas of Tehran, Mehr News reported.

- Several explosions were heard in Abu Dhabi, IRIB News reported.

- Explosion was heard in Abu Dhabi, Fars News reported citing Arab sources.

- Three American destroyers were attacked by the Iranian Navy near the Strait of Hormuz, Tasnim sources say.

- An explosion was heard in Minab, SNN reported.

- Further explosions heard in Bandar Abbas, Mehr news reported.

- Air defences have been activated in West Tehran, Mehr News reported.

- Air defences shot down two hostile drones over Bandar Abbas and Qeshm, Mehr News reported.

- Explosions heard in Qeshm due to the confrontation of defences with small birds, ISNA reported.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded entirely in the red as geopolitical tensions rose, with the US Military and the Iranian Navy exchanging fire. Despite US President Trump announcing that the ceasefire remains in place, bourses failed to see any positivity. ASX 200 opened on the softer side and extended lower, nearly wiping out the gains seen in the past 2 sessions. Real estate and Financials weighed on the index, with Macquarie being dragged down despite reporting FY earnings that beat estimates. Nikkei 225 pulled back from the ATH formed in Thursday’s session amid the negative risk tone. SoftBank has dragged the Nikkei lower after ARM tumbled on smartphone market weakness and AI chip supply concerns. Sony reported FY25/26 earnings, with operating income missing estimates, however announced a JPY 500bln share buyback programme. KOSPI slipped, as investors profit-take following the recent strength in the index, primarily driven by Samsung Electronics and SK Hynix.Shanghai Comp. and Hang Seng followed the broader risk-off tone, as Shanghai Comp. outperformed its Asia-Pac peers with only modest losses.

Top Asian News

- Japan intervened in the FX market during the May holidays, according to sources.

- Singapore is to implement new curbs on executive condos, making them fully privatised after 15 years, CNA reported.

- China’s Finance Ministry conducts issuance of CNY 45.8bln to support the development of pre-school education, CCTV reported.

- Japanese S&P Global Composite PMI Final (Apr) 52.20 (Prev. 53.0).

European bourses (STOXX -0.7%) are almost entirely in the red, with sentiment today pressured by recent flare-ups between US-Iran, whereby US struck Iranian ports which led to retaliatory attempts from the Iranian side. Though, indices are attempting to clamber off lows, with markets focusing on President Trump downplaying the attacks, calling them nothing but a “love tap”, noting that the ceasefire remains in place. European sectors are entirely in the red, display a market fearful of the current geopolitical environment; with cyclical sectors (Travel & Leisure/Consumer Products) residing at the foot of the list, whilst Energy is amongst the top performers. As for key movers this morning: Commerzbank (-0.5%, in-line metrics, raised targets and plans to cut 3k jobs), IAG (-2.7%, strong metrics but cut FY26 capacity outlook; sees strong demand), Intertek (-3%, rejects EQT’s GBP 9bln offer) US equity futures are broadly modestly firmer this morning, in contrast to the downbeat mood in Europe. In terms of key pre-market movers: CoreWeave (-6.6%, Q1 profit miss, Q2 revenue guidance missed expectations, and it raised capex forecasts), Gilead (-0.8%, mixed guidance, despite beating Q1 sales expectations).

Top European News

- UK PM Starmer said he will not be walking away and will be PM into the next general election.

- UK PM Starmer said results do not weaken his resolve, and takes responsibility for outcome.

- Labour may end up losing less than 1500 council seats in England, which may come as some relief for No.10, Journalist Schofield writes citing a poll guru.

- Reform UK Leader Farage said his party is so far exceeding his election results predictions.

- UK’s Milliband reportedly told PM Starmer he should consider setting out a timeline for his departure, via Times. The sources said Miliband made the suggestion during a private meeting with the prime minister about a fortnight ago.

FX

- DXY is on a softer footing after gaining in the prior session as geopolitics heated up. To recap. US and Iran had a brief skirmish, although the US later downplayed it and suggested the ceasefire is not broken, whilst Iran said the US broke the ceasefire, but said the situation around the islands has gone back to normal, although commentary from Iran has been somewhat sparse vs the US. Ahead, participants will be on the lookout for further geopolitical update, and then the US jobs report (full preview available in the Research Suite) and with a few central bankers on the docket, including Fed’s Cook, Waller, Goolsbee and Bowman. DXY resides towards the bottom of a 97.90-98.27 range.

- GBP benefits from a softer USD and digests the initial results from the Local Election. The initial readout from the UK local elections is not as bad as some feared for Labour, potentially providing limited/temporary respite to PM Starmer. Reminder, numerous key councils are yet to report. GBP/USD towards the top end of a 1.3543-1.3622 range.

- EUR/USD is firmer and trades towards the upper end of a 1.1721-1.17736 range, underpinned by the softer Buck. In trade, President Trump said the EU had promised to deliver its side of the deal and cut tariffs to zero, adding the bloc has until July 4th or tariffs would immediately rise to higher levels.

- JPY is flat intraday vs the USD in a narrow 156.63-156.99 band following another volatile week, although the pair remains under its 100 DMA at 157.33. The pair consolidates in a tight range just shy of the 157.00 handle, as talks of FX intervention calmed, with Japanese markets looking ahead to US Treasury Secretary Bessent’s visit to Japan.

- Antipodeans post modest gains amid high-beta properties, a rebound in commodities, although gains are capped by the cautious tone across markets awaiting clarity on the US-Iran situation.

Fixed Income

- USTs began the European day near-enough flat. Since, as energy wanes a touch, the benchmark has lifted more convincingly into the green. However, the current 110-22 high is someway shy of Thursday’s 111-03+ peak. For the US, the day is dominated by NFP, but of course, geopolitics remains in focus and we await an update on yesterday’s activity which, according to the US, did not violate the ceasefire.

- Bunds spent the morning lower by around 20 ticks, as the residual global energy bid, Dutch TTF gains and the potential for elevated US tariffs from July kept yields modestly elevated. However, as above, the magnitude of this has waned across the morning thus far, with around half of that downside trimming, to a 125.72 high. But, as with USTs, still someway shy of Thursday’s 126.14 best.

- Gilts initially opened with losses of 15 ticks and then slipped to a 87.21 low, down by 33 ticks at most but just above Thursday’s 87.13 base and by extension comfortably clear of 86.52 and then 85.76 from earlier in the week. Initial pressure in reaction to the late-Thursday geopolitical escalation, and as the UK local elections show a shift from Labour to Reform, alongside marked Conservative losses and a significant but somewhat less-than-expected move toward the Green Party (though, we await key London areas for more data). Note, we still have a lot of the count to go, with key areas reporting from 12:30BST onward; however, the scale of Labour losses is not as bad as feared and will likely provide PM Starmer with some respite.

- A point which, alongside Starmer confirming he will not resign and intends to lead the UK into the next general election, has allowed Gilts to move into the green and actually outperform peers with gains of nearly 40 ticks to a new WTD high of 87.89. Strength spurred by the market’s preference for stability. However, we await the Manchester numbers around 12:30BST which could be a momentum for Burnham to set out his case. Followed by key councils from 16:00BST onward, including Starmer’s own Camden council around 18:00BST, in addition to the Senedd and Holyrood. As such, the modest Gilt strength we are seeing and the easing of UK yields may yet prove fleeting in the days/weeks ahead.

- Australia sold AUD 1.0bln 1.25% 2032 AGBs: b/c 4.01x, average yield 4.7406%.

Commodities

- In geopolitics, US and Iranian forces exchanged major attacks near the Strait of Hormuz after Iran allegedly targeted three US Navy destroyers with missiles, drones, and fast boats; the US said it intercepted all threats and retaliated with strikes on Iranian military sites. The US military carried out strikes in Iran’s Qeshm port and Bandar Abbas, according to Fox News, citing a US official. The official said it was not a restart of the war or the end of the ceasefire. The UAE was simultaneously hit by renewed Iranian missile and drone attacks, most were intercepted by air defences, though several injuries and disruptions were reported. Despite the escalation, President Trump said the April ceasefire still stands, while warning that failure to reach a broader deal with Iran could lead to much heavier bombing and further regional instability. Meanwhile, Iran’s Press TV said conditions on Iranian islands and coastal cities near the Strait of Hormuz had returned to normal. Seemingly the lack of continued attacks seen as “more positive than feared”, with energy initially gapping higher at the resumption of trade before gradually waning as attacks stopped.

- WTI and Brent futures waned from overnight highs, and now post incremental losses. WTI currently trades at the lower end of a USD 93.82-98.64/bbl range, with Brent hovering around USD 99.60/bbl, within a USD 99.55-102.92/bbl range.

- Dutch TTF has fallen back towards EUR 44/MWh from earlier prices north of EUR 45/MWh. Traders are on the lookout for clarity from the Iranian side on whether the ceasefire still stands and whether diplomacy will continue.

- Spot gold is firmer as the DXY eases with oil. The bullion trades towards the top end of USD 4,673-4,734.90/oz parameters, off yesterday’s USD 4,775/oz. Gold also sees underlying support on renewed buying interest after the PBoC’s purchases, with China raising gold reserves for an 18th straight month in April, adding 260k ounces.

- Base metals are mostly firmer and benefit from the broader losses in the USD amid a lack of further US-Iran escalation following the initial skirmish. 3M LME copper resides towards the top end of USD 13,273.60-13,616.70/t.

- China to raise retail diesel and gasoline prices by CNY 310/Mt and CNY 320/Mt respectively from May 9th; part of regular price review, CCTV reported.

- Freeport Indonesia (FCX) has pushed back the full restart of its Grasberg copper mine by a year.

- Taiwan is reportedly finalising a 25-year US LNG deal valued at USD 15bln with Cheniere Energy (LNG).

- Marathon Petroleum’s Galveston Bay refinery (630k BPD) has returned to normal operations, according to reported.

Trade/Tariffs

- China and US are in communication on US President Trump’s visit, according to Chinese Foreign Ministry spokesperson.

- US reportedly suspects that a Thai firm smuggled chips to Alibaba (BABA) , Bloomberg reported.

- The US and South Africa have started preliminary discussions over potential resources deals including bilateral investments in mining, energy and infrastructure, FT reported citing sources.

- The US Trade Court has ruled against President Trump’s 10% global tariffs.

US Event Calendar

- 8:30 am: United States Apr Change in Nonfarm Payrolls, est. 65k, prior 178k

- 8:30 am: United States Apr Change in Manufact. Payrolls, est. 2.5k, prior 15k

- 8:30 am: United States Apr Unemployment Rate, est. 4.3%, prior 4.3%

- 10:00 am: United States May P U. of Mich. Sentiment, est. 49.5, prior 49.8

- 10:00 am: United States Mar F Wholesale Inventories MoM, est. 1.4%, prior 1.4%

Central Bank Speakers

- 11:05 am: United States Fed’s Goolsbee on CNBC

- 2:20 pm: United States Fed’s Goolsbee on Bloomberg TV

- 7:30 pm: United States Fed’s Waller, Bowman, Daly and Goolsbee on Panel

DB’s Jim Reid concludes the overnight wrap

As we go to press this morning, markets have slipped back thanks to questions about whether the US-Iran ceasefire is holding. Indeed, there’s been a clear escalation in the last few hours, with the US striking targets in Iran after they fired on three US warships in the Strait of Hormuz. And in turn, Trump posted that “we’ll knock them out a lot harder, and a lot more violently, in the future, if they don’t get their Deal signed, FAST!” So Brent crude is back up +1.58% this morning to $101.64/bbl, having been beneath $100/bbl for a good chunk of yesterday’s session. However, markets still aren’t pricing in the worst-case scenario, as Trump told ABC News that “the ceasefire is going. It’s in effect”, referring to the US strikes as a “love tap”.

Questions around the ceasefire have already had a market impact in Asia overnight, where all the major equity indices have lost ground. That includes the Nikkei (-0.69%), the KOSPI (-0.73%), Hang Seng (-1.17%), CSI 300 (-0.90%) and the Shanghai Comp (-0.43%). Moreover, European equity futures are down, with those on the FTSE 100 (-0.70%) and the DAX (-0.87%) both lower, although US futures have picked up a bit after yesterday’s losses, with S&P 500 futures up +0.21%.

Prior to all that, Brent crude (-1.19%) had posted a modest decline yesterday to $100.06/bbl, but that was a decent recovery from the intra-day lows of $96/bbl given there were no obvious signs of progress towards a deal. Moreover, as reports of explosions in Iran came through, that pushed oil prices even higher, so whilst Brent crude spent much of the day beneath $100/bbl, it was just above that mark by the close.

These more negative headlines weighed on broader risk sentiment, leading the S&P 500 (-0.38%) to pull back from its record high. And on top of the geopolitical headlines, we also had a hawkish batch of US data, with numbers on the labour market and inflation both surprising on the upside. For instance, the NY Fed’s latest survey showed 1yr inflation expectations up to 3.64% in April (vs. 3.5% expected), which is the highest since September 2023. So that raised expectations about a more hawkish response from the Fed. And that came on top of strong labour market data, with the weekly initial jobless claims at 200k in the week ending May 2 (vs. 205k expected), which took the 4-week moving average down to a two-year low of 203.25k.

That hawkish newsflow continued with various Fed speakers. In particular, Boston Fed President Collins (a non-voter this year) said she agreed with the hawkish dissenters who didn’t want to include the easing bias in the statement. So that added to the sense there was wider scepticism around further rate cuts. We also heard from two of the hawkish dissenters. Cleveland Fed President Hammack said her own outlook was that “interest rates will be on hold for quite some time.” And Minneapolis President Kashkari said that “if the Strait of Hormuz is closed for an extended period of time, it may well be that the next move might need to be up in interest rates.” So investors priced in a more hawkish outlook, with markets pricing a 38% chance of a rate hike by March 2027 at the close, up from 21% the previous day. And in turn, Treasury yields rose across the curve, with the 2yr yield (+4.6bps) up to 3.91%, whilst the 10yr yield (+3.8bps) rose to 4.39%.

This backdrop meant it was a tough one for equities as well, with the S&P 500 (-0.38%) falling back from its Wednesday record. Indeed, the losses would have been even bigger were it not for the Mag 7 (+0.71%) reaching another record. So the equal-weighted S&P 500 (-0.67%) saw its largest decline in almost four weeks, whilst the small-cap Russell 2000 (-1.63%) struggled even more. And over in Europe, there were also broad declines, with the STOXX 600 (-1.10%) posting its biggest decline in over a month, alongside losses for the DAX (-1.02%), the CAC 40 (-1.17%) and the FTSE 100 (-1.55%).

Looking forward, we’ll get more data today with the US jobs report for April. That’s an important one, as Fed pricing has already shifted in a hawkish direction given the energy shock, and last month’s payrolls were at a 15-month high of +178k. This time round, our US economists are looking for payrolls to come in at +50k, which would actually mark the first back-to-back positive reading since May last year. Meanwhile, they see the unemployment rate steady at 4.3%.

Elsewhere today, the UK will be in focus, as we’ve just started to get the results from the local elections overnight. We’ve only got a few results so far, but the governing Labour Party have suffered heavy losses in the seats they were defending, whilst Nigel Farage’s Reform UK party has seen major gains. Today, it’ll be important to watch what Labour MPs and cabinet ministers are saying, as gilt markets are focused on whether PM Keir Starmer will remain in post following the results. That’s because of expectations that a new Labour leader might ease the fiscal rules and raise gilt issuance, so when Starmer’s position has come into question, that’s coincided with selloffs for gilts.

Before all that, sovereign bonds were fairly steady across Europe yesterday, with the 10yr bund yield (+0.1bps) remaining at 3.00%. There had been more of a rally earlier in the session, but that unwound as oil prices moved higher again, with yields tracking those moves. So yields on 10yr gilts (+0.9bps) and OATs (+0.4bps) also saw a modest increase, although those on BTPs (-0.6bps) came down slightly. Otherwise, investor expectations of an ECB rate hike in June were also steady yesterday, with markets pricing in an 80% chance of a hike by the close, up from 79% on Wednesday.

Finally, there were a couple of noteworthy headlines on US trade yesterday. First, the 10% global tariff currently in place was found to be unlawful by the US Court of International Trade. That’s the one the administration had imposed under the Trade Act of 1974, after the Supreme Court ruled against the previous IEEPA tariffs earlier this year. But for now, at least, the Court of International Trade only blocked them from enforcing it against the companies that sued and Washington State. The second story was that Trump set a deadline of July 4 for the EU to “deliver their side of the Deal”, or tariffs would be raised.

Looking at the day ahead, data releases include the US jobs report for April, the University of Michigan’s preliminary consumer sentiment index for May, and German industrial production for March. Central bank speakers include ECB President Lagarde, ECB Vice President de Guindos, the ECB’s Nagel, the Fed’s Cook, Waller, Bowman, Daly and Goolsbee, BoE Governor Bailey, and BoE Deputy Governor Breeden.

Tyler Durden

Fri, 05/08/2026 – 08:23

via ZeroHedge News https://ift.tt/BXCzqv9 Tyler Durden