Winning? Do We Need To Understand UBI

Submitted by Peter Tchir of Academy Securities

Winning? Do We Need To Understand UBI

Iran (and the potential for a deal) has continued to move markets. As the 30-year bond rose above 5% earlier this week, we got news that we have a new approach to resolving the conflict – a one-page MOU. Markets (ex-oil) rallied around various “deal” headlines all week.

Spider, Bret, and I spent some time discussing this on Friday’s Podcast – The U.S. Proposal to End the War (also available on Spotify and iTunes).

Information continues to leak out in dribs and drabs about how those negotiations are doing. There continue to be conflicting messages. In the back of my mind, I’m increasingly forced to remember what we mentioned at the start of the conflict – Iran has never won a war but has never lost a negotiation.

There was a time when that statement didn’t seem likely to be reflective of this conflict. From “unconditional surrender” to various other metrics (especially surrounding nuclear weapons capabilities) we seem to be drifting to – let’s open the Strait and figure out the rest later?

The U.S. has displayed exceptionalism on every military task that it has been asked to undertake during this conflict. While we have had a limited presence in the Strait, our maritime efforts have been successful in accomplishing the missions that have been defined. Yes, Project Freedom was short lived. Not so much because the U.S. couldn’t deal with the threat (we successfully defended ourselves against Iranian missiles, drones, and small boats), but because it became pretty clear that not many commercial vessels were ready, under current circumstances, to risk challenging Iran.

We did argue, earlier in the week, that the admin’s assertion that Iran only has a few weeks before its economy collapsed, was underestimating the Iranians. They in all likelihood have prepared for this economic pressure and likely have significant IOUs with countries like China (and possibly even crypto holdings) to survive months not weeks. A regime that will shoot 40,000 or more citizens in a week for protesting is not going to be overly concerned with “standard of living” issues. Finally, all the “hype” around the fact that Iran’s ability to store oil is running out and this is causing them to shut the pumps (resulting in long-lasting damages) seemed “optimistic” at best. Iran has been decreasing the pressure, reducing the flow, and giving more leeway to when their reservoirs fill up. They also have the ability to just pump oil back onto the sand (and there are some reports of oil slicks in the Gulf). So, yes, if they left their facilities on full pressure, and were worried about “dumping” oil, it might be a week or two before irreparable damage is done. But they aren’t doing that. Also, according to many in the oil industry, other countries in the region are employing the same tactics. It isn’t just Iran that faces an inability to load oil onto transportation systems (pipelines or tankers). Much of the region faces similar challenges from the inability/unwillingness to transit the Strait.

A deal would be good, but a good deal would be better.

We discuss our views, options, and even highlight a couple of possibly great outcomes in the podcast (linked above), but we do seem to be drifting towards expediency rather than something more comprehensive.

I am still in the camp that the U.S. will once again become frustrated with Iran and launch another set of attacks, to truly push this conflict to a conclusion that leaves the world much safer.

Do We Need to Understand UBI?

With the release of some formerly classified information, I probably should be talking about UFOs, but somehow I’m here thinking about UBI. UBI or Universal Basic Income is a topic I haven’t paid much attention to.

It reminds me a bit of some other economic theories that I paid little attention to, without doing much damage to my work.

- Mint the Coin was a movement “predicting” or “encouraging” the government to mint a trillion dollar coin to avert the debt ceiling. It would get some traction periodically and every once in a while made me wish I spent some time even thinking about this “absurd” (in my opinion) “solution” to our debt ceiling.

- Brexit. Yes, Brexit eventually happened, but it took so long to play out (as does everything in Europe including their “inevitable” adoption of ProSec ) that it was at best an undercurrent of markets, and I would argue (as someone who largely ignored it), not an undercurrent to the global economy. Important for the U.K. for sure, but I think I saved myself a lot of time and effort by largely ignoring it.

The point here is that I’ve been “dismissive” of any conversation around UBI. The concept has seemed anti-capitalist and almost “un-American.” The U.S. has “safety nets” of all sorts. Every “capitalist” country has their own version of “safety nets” – some more robust than others. UBI always seemed “a step too far,” especially in the U.S., but I cannot help thinking about it, as I struggle to digest the data this week – the “hard” data as well as the anecdotal data.

For the second month in a row, we had (at least on the surface) very strong job growth – Back to Back Dingers.

If the only piece of economic data I had was the Establishment survey of jobs, I’d be pretty pumped for the economy.

But that is NOT the only piece of data we have. There are so many ways I could express concern, that it would take too long to write, and would become repetitive, so I will stick to what some other people said recently. Here are “paraphrased” comments that caught my attention:

- Recession-level demand slump in North America. (Whirlpool)

- Consumer sentiment is certainly not improving, and it may be getting a little bit worse. (McDonald’s)

- Consumers are literally running out of money toward the end of the month. (Kraft Heinz)

There are many stocks we can look to, in order to gauge the state of the consumer. HD (Home Depot), for example, is almost 25% off of its high from last October. LOW (Lowe’s) is off 20% from its high set in February. That tells me there is something off with the consumer (rather than something company specific). If people are not spending money on home improvement, that indicates a lack of optimism from consumers.

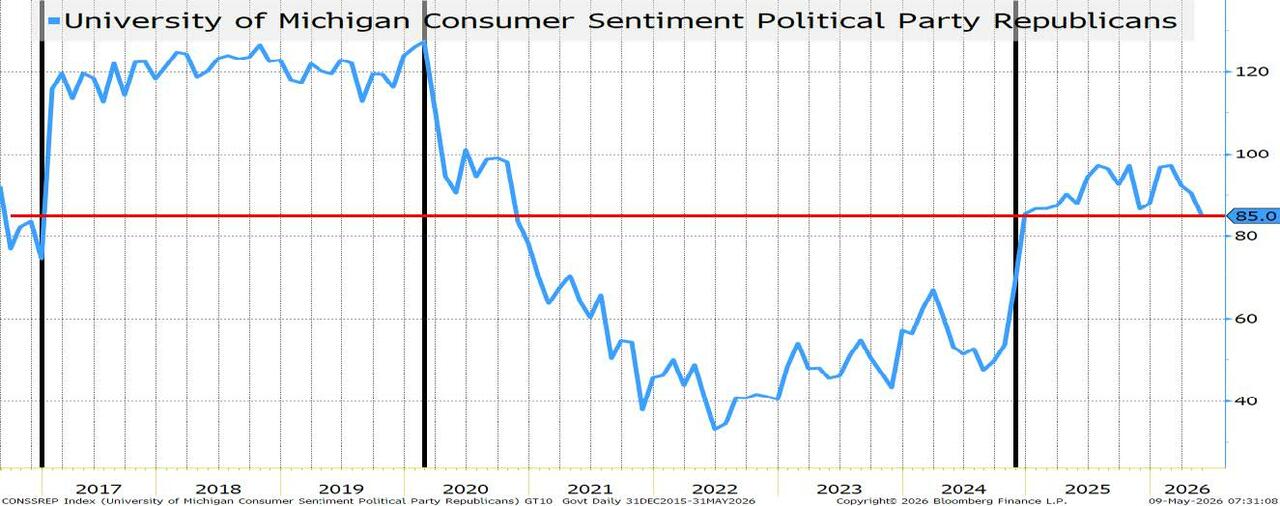

Since I’m not a huge fan (or even a small fan) of the various CONsumer CONfidence surveys, I feel almost bad referencing it for the 2nd month in a row. Yes, it hit all-time lows, but that isn’t what caught my eye. Okay, it caught my eye, but everyone saw that. This is the chart from that survey that I find most interesting.

Here we get the responses from the Republicans for the University of Michigan Survey. It is 85. Far above the 48.2 headline number (which is the one that set a new record low). At 85 it is well above the lows during the Biden administration.

But this is the lowest Republican sentiment while President Trump has been in office.

That, to me, is important.

I have never understood how or why Republicans and Democrats would have such a different view of the economy. Maybe, if somehow, it was picking up differences in regional economies (areas where Republicans reside are booming, and vice versa), but it seems counterintuitive that the difference on economic outlook is so tied to party. Which is why I largely ignore this entire CONsumer CONfidence set of data, but the recent erosion in the chart makes me think twice.

AI versus Affordability

I really, really, want to bring up the line from Apocalypse Now – “Charlie Don’t Surf.” Maybe I’ve been spending too much time fixated on the war.

But I really want to write something along the lines of “AI Don’t Spend.” Or “one person’s expense, is another person’s revenue.”

So far any concerns about job losses due to AI don’t seem to be showing up in the jobs data. This is likely because:

- The buildout of AI requires a lot of hiring. Not just making the components necessary to run a data center (chips, cooling, electricity, etc.) but also the actual construction of the data centers and all the “picks and shovels” around data center construction.

- AI, in most cases, seems to have slowed hiring, rather accelerated the firing of employees. Attrition is playing the biggest role in adjusting headcount to offset AI spending (and productivity, to the extent it is being productive).

I’m stuck believing that the pressure on the consumer, so far, is primarily due to affordability, rather than job losses.

Concern about the future of jobs or pay may be influencing consumer sentiment and spending (I’m going to keep making T-Reports so confusing that AI cannot replicate them any time soon), but the bulk of the issue is affordability right now. What the heck will happen if job losses, especially due to AI, increase?

Let’s use some “water” analogies here (to try to link into the surf comment).

- A rising tide lifts all boats. This is the sort of economic growth we are all used to. Everything does better. It doesn’t really matter what you do, or where you are, you do better. This economy does not currently have that “vibe” to me.

- We see who is swimming naked when the tide goes out. Always a good one, but not sure how relevant it is to today’s economy. I think we are more about all boats not lifting, than we are about a tide going out.

- If the water is rising and you are anchored to the ground, you are in trouble. Okay, I just made that one up. But we’ve all seen it in movies.

- The water level is rising in a room, where the “hero” cannot get out. There is real fear. If there wasn’t some fear of this, Harry Houdini probably wouldn’t be as famous as he is.

I think this latter analogy may be the most apt:

- The water is rising (affordability). More and more people are getting sucked into the daily, weekly, monthly, and annual struggle of making ends meet. If we want to go down the “k”- shaped analogy, more and more of the k is underwater. Maybe it was only the lower leg of the k that was struggling, but as the water rises (affordability), more of the k is being covered. We may well be into the upper leg of the k. I guess we better hope that is a K rather than a k where the upper leg is long and goes high, but I’m concerned it is not (I still stick with the i-shaped economy, where a handful is doing extremely well and the rest of us are seeing the water rise).

On that pleasant note…

Bottom Line

Anyone with a job that can be disrupted by AI should own AI stocks as a “hedge.” I cannot tell if I’m being facetious or serious, but it is something to think about.

It is too early to spend a lot of time trying to understand how UBI would work, but I suspect we will start hearing more about this rather than less as affordability remains an issue. The issue will decline once we get a deal with Iran, but the affordability issue is not going away (I restrained myself from calling it a crisis, but…).

On credit, I continue to think credit will do fine and like owning private credit as marks seem to be adjusting to a new reality. More for a “trade” than being married to the position. I will get a detailed report out this week, as I am actually not on the road this week!

On rates, our more detailed analysis from last weekend’s Living in an AI World stands. Largely rangebound, with 4.35% to 4.4% as the middle of the range on 10s.

Continue to focus on ProSec themes, here and in Europe. If we get a deal, expect the admin to turn more attention to things like electricity production and the processing, refining, and smelting of commodities (as well as their extraction). A lot is being done in the background, but the President remains a key driver and while his attention has been diverted, we haven’t seen as much progress on ProSec as we’d like (away from domestic-focused chip manufacturing). That should change!

Thanks for everything and best wishes to all the moms out there! Hope you and your family and friends have an amazing day today! (Hopefully, every day is amazing, but today everyone should focus on the importance of family, more than the average day, where things like “work” get in the way).

Tyler Durden

Sun, 05/10/2026 – 11:05

via ZeroHedge News https://ift.tt/K0C2ytf Tyler Durden