Key Events This Week: CPI, PPI, Retail Sales, Trump-Xi Summit

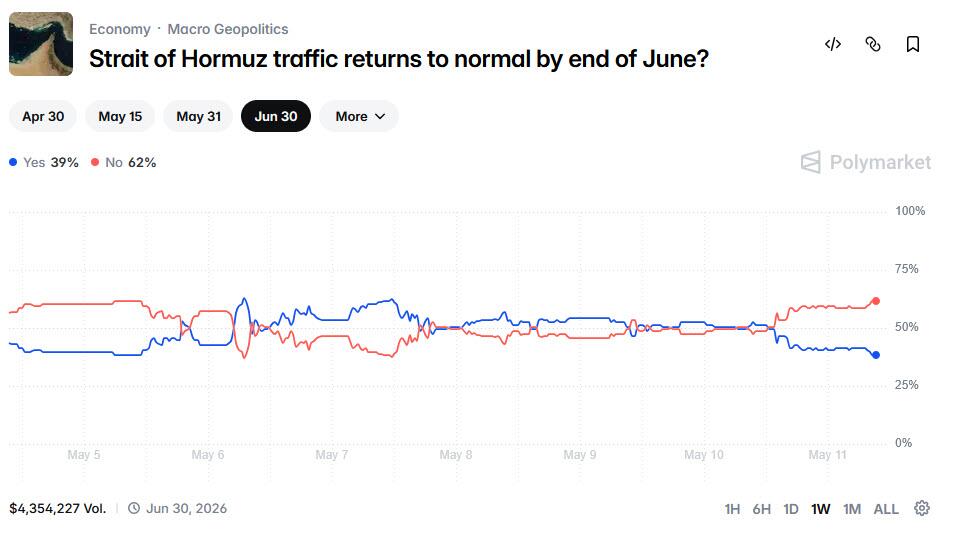

As DB’s Jim Reid tallies overnight, it has now been 73 days since the war in Iran began, with the past 32 marked by a stalemate characterized by a mix of truce and ongoing ceasefire. The absence of any meaningful kinetic activity for over a month suggests a firm US preference for reaching a deal. However, a counterpoint is that uncertainty over who holds negotiating authority in Iran may be complicating progress and delaying more difficult times ahead. It remains an unusual conflict with little action now for a month. In simple terms though, as long as the Strait of Hormuz stays closed, markets remain on a knife edge. Polymarket currently assigns a 39% probability to it fully reopening by 30 June.

The latest is that oil and yields are up again this morning as President Trump has posted that “I have just read the response from Iran’s so called ‘Representatives'” which he went on to call “TOTALLY UNACCEPTABLE”. This was based on a WSJ report that suggested Iran was offering to transfer some of highly enriched uranium to another country but wouldn’t dismantle its nuclear facilities. Iran’s official news agency has disputed the report anyway. Brent is up +4.23% and 10yr US yields are up +3.5bps. However, US and European equity futures are largely flat and Asian equities are largely higher on the AI trade. The KOSPI is on fire again with the index up +4.0% as semiconductors surge again. The index has crossed +85% YTD.

This comes ahead of the planned mid-to end week meeting between US President Donald Trump and China’s President Xi Jinping in Beijing. It’ll be interesting to see whether this meeting does anything to shape negotiations in the war. Both leaders would clearly like to show their influence on the world stage. So certainly the biggest headline event of the week (full preview here).

Before that, the new week arrives with markets still processing last Friday’s US payrolls report, which came in broadly firm and reinforced the view that labor market conditions remain resilient. While not strong enough to decisively alter the policy outlook, the release did little to ease concerns that underlying inflation pressures could persist, especially given still-solid wage dynamics. Against this backdrop, outside of the Iran War developments which will of course take center stage, the coming week will remain centered on the US, with a dense run of data and policy developments.

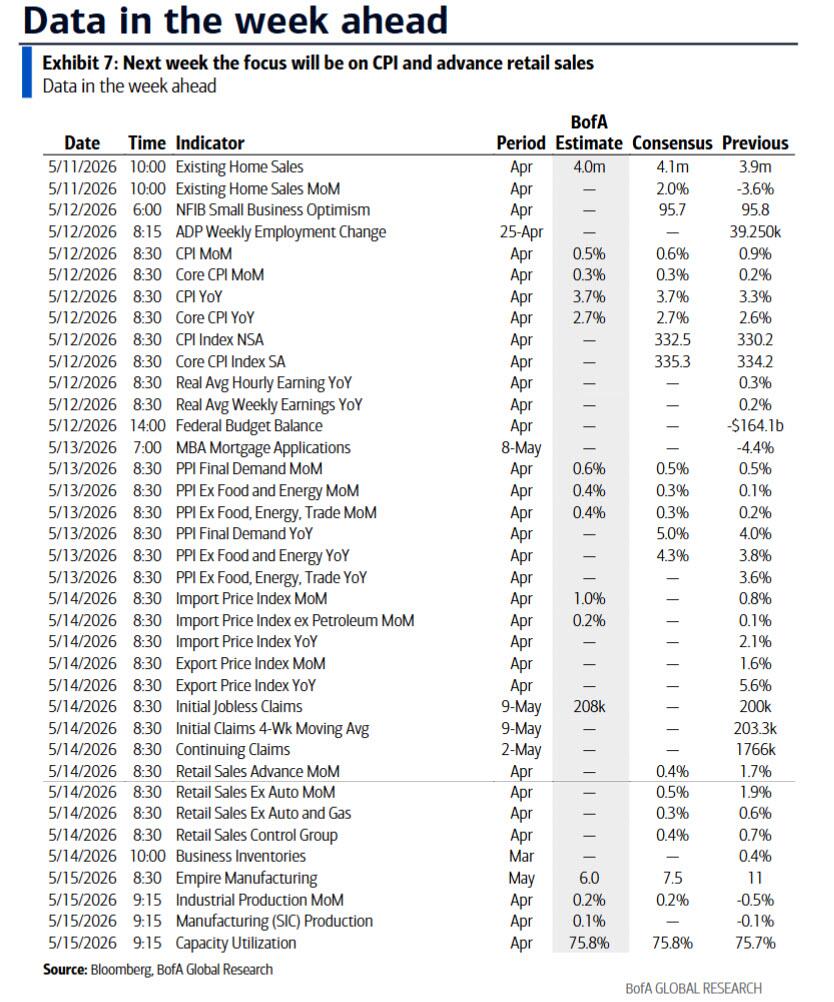

This week’s focal point will be tomorrow’s April CPI report. DB economists expect headline inflation to rise by +0.58% month-on-month, moderating from March’s +0.9%, but still relatively firm. In contrast, the core measure is projected to accelerate to +0.39% MoM from +0.2%, suggesting underlying price pressures remain sticky even as energy-related effects fade. The YoY rates would move from 3.3% to 3.8% for the former and from 2.6% to 2.8% for the latter.

Producer price data follows on Wednesday and then the remainder of the week shifts towards activity indicators. DB economists expect retail sales to decline by -0.3% MoM after March’s strong +1.7% increase, pointing to some payback in consumer spending. Meanwhile, industrial production is forecast to rise modestly by +0.2% MoM following a -0.5% drop previously, suggesting a tentative stabilization in manufacturing output.

Policy and politics will also be important. A Senate vote on Kevin Warsh’s nomination as Fed Chair is scheduled for today, just days before Jerome Powell’s term is set to expire at the end of the week. It’s possible the vote could get pushed back a day or so due to other Senate business but by the end of the week you would expect Warsh to have taken Miran’s seat on the board with Powell staying on the committee.

In Europe, inflation readings from Denmark and Norway today are followed with Germany’s ZEW survey tomorrow with sentiment darkening even with the nation’s extraordinary fiscal package. Later in the week, the ECB’s economic bulletin may offer additional context on the central bank’s assessment of inflation and activity trends.

In the UK, attention will be split between politics and macro. The State Opening of Parliament and the King’s Speech on Wednesday will outline the government’s legislative agenda for the year ahead. With PM Starmer under tremendous pressure following the very poor (but broadly as expected) local election results on Thursday there is talk of a leadership challenge as soon as today. Backbench MP Catherine West has said she will stand, which would be a stalking horse nomination. However, many left-wing MPs (as she is) have urged her not to as their preferred candidate Andy Burnham is not currently an MP. They fear an election now might be a bit too early and may allow a more moderate candidate like Wes Streeting to prevail. So timing tactics could prolong Starmer’s reign. A reminder that in September last year, Mr Burnham said that the UK should no longer be “in hock to the bond markets”. This caused a spike in Gilt yields and although he subsequently downplayed the remarks, this is something to watch carefully as we navigate the politics of the next few days and weeks. On the data side, Q1 UK GDP on Thursday will offer up the latest state of play growth wise.

In Asia, Japan’s schedule includes household spending data tomorrow, alongside the Economy Watchers survey and bank lending figures on Wednesday. In addition, the Bank of Japan will publish its summary of opinions from the April meeting, which should provide greater insight into policymakers’ thinking and any emerging shifts in the policy stance.

There are multiple appearances from Fed, ECB, BoE and BoJ officials throughout the week, and on the corporate front, earnings continue at a steadier pace. In the US, Cisco and Applied Materials are among the key names, while internationally the focus includes major firms such as Tencent, Alibaba, Siemens and Bayer. See the day-by-day calendar at the end as usual for a fuller week ahead preview.

Courtesy of DB, here is a day-by-day calendar of events

Monday May 11

- Data: US April existing home sales, China April CPI, PPI, Denmark April CPI, Norway April CPI

- Earnings: Petroleo Brasileiro, Constellation Energy, Barrick Mining, Compass, AST SpaceMobile

- Auctions: US 3-yr Notes ($58bn)

- Other: US Senate vote on Kevin Warsh’s nomination for Fed Chair

Tuesday May 12

- Data: US April CPI, federal budget balance, NFIB small business optimism, Japan March household spending, leading index, coincident index, Germany May Zew survey, Italy March industrial production, Eurozone May Zew survey

- Central banks: Fed’s Goolsbee speaks, ECB’s Dolenc speaks, BoJ Summary of Opinions April MPM

- Earnings: Siemens Energy, Mitsubishi Heavy Industries, MunichRe, Bayer, Vodafone, Venture Global, On Holding, thyssenkrupp

- Auctions: US 10-yr Notes ($42bn)

Wednesday May 13

- Data: US April PPI, Japan April bank lending, Economy Watchers survey, March BoP current account balance, BoP trade balance, Germany April wholesale price index, March current account balance, Eurozone March industrial production, Q1 employment

- Central banks: Fed’s Collins and Kashkari speak, ECB’s Lagarde, Lane and Radev speak, BoE’s Mann speaks

- Earnings: Tencent, Cisco, Alibaba, Siemens, SoftBank, Allianz, Deutsche Telekom, E.ON, RWE, Alstom

- Auctions: US 30-yr Bonds ($25bn)

- Other: UK King’s Speech and the State Opening of Parliament

Thursday May 14

- Data: US April retail sales, import price index, export price index, March business inventories, initial jobless claims, UK April RICS house price balance, Q1 GDP, Japan April M2, M3, Canada April existing home sales, March wholesale sales ex petroleum

- Central banks: Fed’s Hammack and Barr speak, BoJ’s Masu speaks, BoE’s Pill speaks

- Earnings: Applied Materials, National Grid, Figma

- Other: US President Trump travels to China (through May 15)

Friday May 15

- Data: US May Empire manufacturing index, April industrial production, capacity utilisation, Japan April PPI, April machine tool orders, Italy March general government debt, Canada April housing starts, March international securities transactions, manufacturing sales

- Central banks: Fed Chair Powell’s term ends, ECB’s economic bulletin

Finally, looking at just the US, the key economic data releases this week are the CPI report on Tuesday and the retail sales report on Thursday. There are several speaking engagements by Fed officials this week, including events with Presidents Williams, Goolsbee, Collins, Kashkari, Schmid, and Hammack and Governor Barr on Thursday.

Monday, May 11

- 10:00 AM Existing home sales, April (GS +3.0%, consensus +2.0%, last -3.6%)

Tuesday, May 12

- 03:15 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will participate in a monetary policy panel at a conference jointly organized by the Swiss National Bank and the International Monetary Fund in Zurich, Switzerland. A Q&A session is expected. On May 4, Williams said, “The elevated levels of inflation, mixed signals from the labor market, and heightened uncertainty from the Middle East conflict present an unusual set of circumstances, but the current stance of monetary policy is well positioned to balance the risks to our maximum employment and price stability goals.”

- 08:30 AM CPI (MoM), April (GS +0.58%, consensus +0.6%, last +0.9%); Core CPI (MoM), April (GS +0.31%, consensus +0.3%, last +0.2%); CPI (YoY), April (GS +3.68%, consensus +3.7%, last +3.3%); Core CPI (YoY), April (GS +2.67%, consensus +2.7%, last +2.6%): We estimate a 0.31% increase in April core CPI (month-over-month SA), which would raise the year-over-year rate to 2.67%. We expect mixed autos inflation, reflecting a 0.4% decline in used car prices, a 0.1% increase in new car prices, and a 0.4% increase in the car insurance category. We forecast a jump in the shelter categories—a 0.50% increase in the OER category and a 0.44% increase in the rent category—reflecting the unwind of the downward bias in the index level from missed data collection during the government shutdown. The panel group that should have been sampled in October will be sampled in April and compared to prices from twelve months prior (i.e. April will effectively show two months’ worth of increases). We expect mixed readings for the travel services categories (airfares: +3%; hotels: flat), reflecting signals from alternative price data. We expect diminishing upward pressure from tariffs on categories that are particularly exposed (such as recreation) worth +0.04pp. We estimate a 0.58% rise in headline CPI—reflecting higher food prices (+0.3%) and sharply higher energy prices (+4.6%)—which would raise the year-over-year rate to +3.68% from +3.26%. Our forecast consists of a 0.26% monthly increase in the core PCE price index in April.

- 01:00 PM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will speak at the Greater Rockford Chamber of Commerce Luncheon in Rockford, Illinois. A Q&A session is expected. On May 8, during an interview in which he was asked whether inflation is the main danger now given that the labor market appears to have stabilized, Goolsbee responded, “I am optimistic that rates can go down, if we get some progress on inflation, [showing] we are headed back to the 2% inflation, [but] we just haven’t had [progress on inflation] for some time, and that makes me less optimistic.” When asked about the easing bias in the April FOMC statement, Goolsbee responded, “I was always skeptical of the value and appropriateness of using forward guidance [on things] that the committee doesn’t think it is going to do for some number of months or committing to actions well in the future.”

Wednesday, May 13

- 08:30 AM PPI final demand, April (GS +0.6%, consensus +0.5%, last +0.5%); PPI ex-food and energy, April (GS +0.5%, consensus +0.3%, last +0.1%); PPI ex-food, energy, and trade, April (GS +0.3%, consensus +0.3%, last +0.2%);

- 11:30 AM Boston Fed President Collins (FOMC non-voter) speaks: Boston Fed President Susan Collins will give remarks and participate in a fireside chat at the Boston Economic Club. Speech text and Q&A are expected. On May 7, Collins said she preferred to adjust the text of the post-meeting statement to “not be as closely aligned with language that has been associated with the presumption that the next move will be a cut.” She also added, “I do think that there are scenarios in which it would be important to strongly consider a hike.”

- 01:15 PM Minneapolis Fed President Kashkari (FOMC voter) speaks: Minneapolis Fed President Neel Kashkari will participate in a moderated discussion at a St. Paul Area Chamber event. A Q&A session is expected. On May 7, Kashkari said, “We voted against the forward guidance because we just didn’t want to signal that the next move was likely down.” He also added, “We cannot let elevated inflation be the new normal.”

Thursday, May 14

- 08:30 AM Import price index, April (consensus +1.0%, last +0.8%); Export price index, April (consensus +1.1%, last +1.6%)

- 08:30 AM Initial jobless claims, week ended May 9 (GS 205k, consensus 205k, last 200k); Continuing jobless claims, week ended May 2 (consensus 1,785k, last 1,766k)

- 08:30 AM Retail sales, April (GS +0.2%, consensus +0.6%, last +1.7%); Retail sales ex-auto, April (GS +0.3%, consensus +0.6%, last +1.9%); Retail sales ex-auto & gas, April (GS +0.1%, consensus +0.4%, last +0.6%); Core retail sales, April (GS +0.2%, consensus +0.4%, last +0.7%): We estimate core retail sales increased 0.2% in April (ex-autos, gasoline, and building materials; month-over-month SA), reflecting mixed alternative data and a headwind from potential residual seasonality. We estimate headline retail sales increased 0.2%, reflecting higher gasoline prices but lower auto and food services sales.

- 10:15 AM Kansas City Fed President Schmid (FOMC non-voter) speaks: Kansas City Fed President Jeff Schmid will speak on payments innovation and community banking at the Future of Banking Conference hosted by the Federal Reserve Bank of Kansas City. Speech text and Q&A are expected. On April 1, Schmid said, “With inflation already running hot, now is not the time to assume that the inflation from higher oil prices will be transitory.” He also added, “We must remain focused on our headline inflation objective, otherwise, I believe there is a real risk that inflation will get stuck closer to 3 percent than 2 percent in the long run.”

- 01:00 PM Cleveland Fed President Hammack (FOMC voter) speaks: Cleveland Fed President Beth Hammack will deliver opening remarks at the Cleveland Fed Conversations on Central Banking event. On May 7, Hammack said, “The statement that we put out is that interest rates were on hold, but we have the signal in there that it’s more likely that the next move will be down, [and] I thought that was a little bit misleading, just given my view of where the economy is.” She also added that her “baseline outlook is that interest rates will be on hold for quite some time.”

- 05:30 PM Fed Governor Barr speaks: Fed Governor Michael Barr will deliver remarks at an event organized by the Money Marketeers of New York University. Speech text and Q&A are expected. On May 5, Barr said, “The duration of the conflict matters a lot, and the longer it goes on, the greater the risk that the inflation we are seeing in these prices becomes embedded in the economy.”

- 05:45 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will participate in a moderated discussion at a conference organized by Moody’s. A Q&A session is expected.

Friday, May 15

- 08:30 AM Empire State manufacturing index, April (consensus +7.5, last +11.0)

- 09:15 AM Industrial production, April (GS +0.4%, consensus +0.2%, last -0.5%); Manufacturing production, April (GS +0.1%, consensus +0.2%, last -0.1%); Capacity utilization, April (GS 75.8%, consensus 75.8%, last 75.7%): We estimate industrial production increased 0.4% in April, largely reflecting strong natural gas and oil production. We estimate capacity utilization edged up to 75.8%.

Source: DB, Goldman

Tyler Durden

Mon, 05/11/2026 – 09:35

via ZeroHedge News https://ift.tt/wRM2uz1 Tyler Durden