Parabolic Semiconductor Rally Is Pricing In 2028 Already

Authored by Lance Roberts via RealInvestmentAdvice.com,

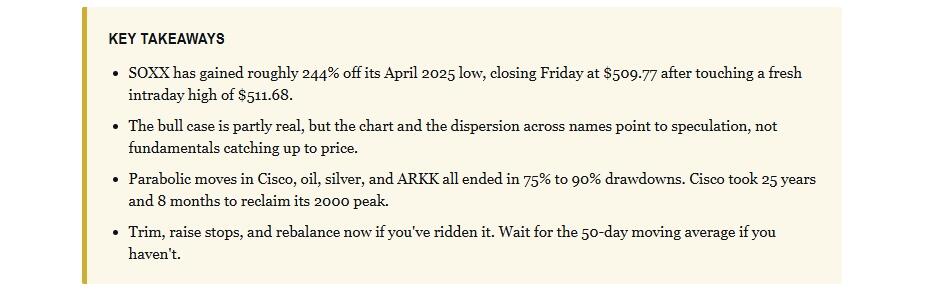

The parabolic semiconductor rally crossed a line this week. SOXX, the iShares Semiconductor ETF, closed Friday at $509.77 after touching a fresh intraday high of $511.68. That’s a gain of roughly 244% from the April 2025 low of $148.31. Most of that move has been compressed into the last two months alone. Since mid-March, SOXX has tacked on another 58%. The chart is now textbook parabolic. And parabolic charts almost never end politely.

If you wanted a real-time stress test of how fragile this move is, you got one this week. Semiconductors took a -2.86% hit on Thursday on softer Iran headlines, with Broadcom and Micron dragging. By Friday’s open, the dip was already being bought aggressively. A stronger-than-expected April jobs report (115,000 vs. 65,000 expected) and renewed peace-deal optimism sent the Nasdaq up 1.71% on the day, with SOXX printing a new intraday high before the close. That’s not a market digesting risk. That’s a market refusing to take “no” for an answer.

I’ve watched this movie before. After 30 years of cycles, the ending is rarely a surprise. The setup, however, is almost always sold as “this time is different.” It isn’t. In fact, every parabolic semiconductor rally in modern memory has ended the same way, and there’s no reason to expect a kinder math this round.

Where The Parabolic Semiconductor Rally Stands Today

Start with the math, because it’s doing the talking. SOXX is currently trading 62% above its 200-day moving average and 34% above its 50-day. Readings that stretched are the back end of a move, not the middle. The slope of the advance has steepened in each successive month. That is the signature of a momentum trade pulling in late buyers, not of fundamentals catching up to price.

Look across the complex, and the dispersion is striking. Micron is up nearly 1,000% off its April 2025 low. AMD is up roughly 450%. Nvidia, the index’s anchor, is up “only” 140%. Notably, the stocks that crashed hardest a year ago have rallied the most in the recovery. That’s exactly how late-cycle chase trades behave. The trash leads the way up because it has the largest short position to cover and the most leverage to a narrative. In other words, this parabolic semiconductor rally is now being driven by the names with the worst fundamentals, not the best.

Notice in the chart above how the slope of the advance has steepened in each successive month. The early move off the April low was a recovery. The middle was a trend. What we have now is something else.

Real Demand Or A Speculative Frenzy?

I get the bull case. AI capex is real. Hyperscaler orders are real. Foundry utilization is real. Nvidia, Broadcom, and TSMC are delivering numbers that justify premium multiples. So far, so good. The shortage narrative around HBM memory and leading-node capacity has actual data to back it up, and that’s the part of the story bulls keep pointing to.

However, here is the problem with the current setup. A real fundamental story doesn’t require a parabolic chart to validate it. In fact, fundamentals tend to drag prices up the trend line, not push them through the ceiling. When a “shortage” narrative arrives at the same moment that the worst-quality names in the sector are leading the index higher, that’s not fundamentals at work. That’s the narrative being recycled to justify a move that has already happened. Indeed, the parabolic semiconductor rally we’re seeing right now bears almost none of the hallmarks of a fundamentals-led advance.

Look at the dispersion again. If this were a shortage-driven, fundamentals-led rally, the leaders would be the names with the cleanest demand visibility. Instead, the laggards from a year ago are the runaway winners. Micron up 1,000%. AMD up 450%. Nvidia, the company that actually owns the AI capex story, up “only” 140%. Quality is being left behind because the chase is no longer about earnings. It’s about beta.

Here’s the part that should bother bulls the most. SOXX is trading at multiples that already reflect strong 2026 earnings. The current rally has likely already fully priced in 2026 earnings. From here, you are paying for 2027 and 2028 growth in a sector where the cycle has not been repealed. Semiconductors are still cyclical. Always have been. The day the AI capex cycle hiccups, even briefly, is the day this chart breaks.

Make no mistake, the rally has been spectacular. The exit will be too. Importantly, we have decades of data on what happens when speculative momentum compresses years of expected returns into months. The pattern is remarkably consistent across asset classes and across decades. As a result, the path forward for this parabolic semiconductor rally is not a mystery, even if the timing is.

The consistent thread is that parabolic charts don’t unwind through gentle rotation. They snap. The exit is faster than the entry, and the stocks that led the rally on the way up tend to lead the carnage on the way down. The investors most hurt are not the ones who avoided the move entirely. They’re the ones who showed up late, on the back of the same shortage narratives that are now circulating around semiconductors.

Recovery time is the part most investors underestimate. Cisco, the poster child of the dot-com semiconductor adjacency, only reclaimed its March 2000 peak on December 10, 2025. That’s 25 years, 8 months, and 13 days from peak to recovery. The business kept growing throughout. Earnings kept compounding. Revenues nearly quintupled. The stock simply paid forward too many years of growth at the top, and the math demanded a quarter century to absorb the excess.

Anyone who bought at the 2000 peak earned a nominal break-even after factoring in dividends, but lost meaningfully to inflation along the way. That’s not a recovery story. That’s a generational opportunity cost. ARKK, which ran +360% into its 2021 peak, still trades below it five years later. Different decades, different assets, but the pattern holds. Speculative tops resolve through painful, prolonged drawdowns, not graceful rotations.

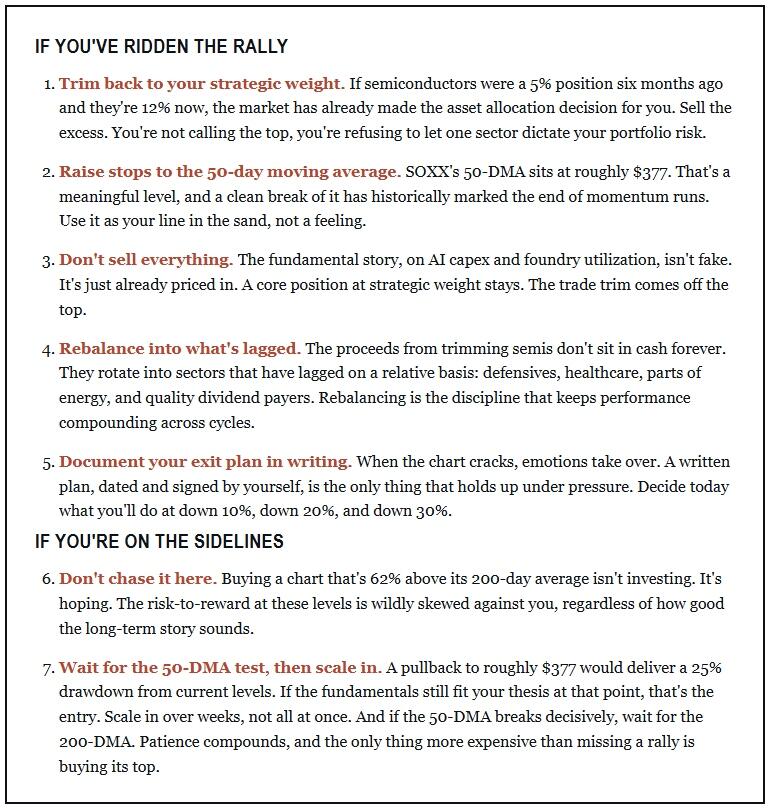

The Risk Management Playbook

So what do you actually do? Of course, the answer depends on whether you’ve ridden this rally or you’re staring at the chart wondering if it’s too late to participate. Honestly, the answer for most investors is the same in either case. You don’t have to be all-in or all-out. You just can’t let the position size make the decision for you.

Here is the playbook we’re using for clients right now. First, five points if you’re already invested. Then, two if you’re not.

The Bottom Line

The semiconductor rally has been one of the most extraordinary moves of the post-COVID era. The fundamentals supporting the early stages of the move were real. The fundamentals supporting the most recent leg are increasingly imaginary. SOXX has likely fully priced in 2026 earnings already, and the stocks leading the index higher are no longer the ones with the cleanest demand stories.

Of course, parabolic charts rarely give back gracefully. Cisco, oil, silver, and ARKK all showed that exits come faster than entries, and recovery can take years to decades. The parabolic semiconductor rally has been spectacular. The exit will be too. The question isn’t whether the chart cools off. The question is whether you’ve prepared your portfolio for it before it does.

Tyler Durden

Mon, 05/11/2026 – 11:45

via ZeroHedge News https://ift.tt/5kSAP2j Tyler Durden