Millions Of Student Borrowers Are Defaulting: They Are 40 Years Old On Average

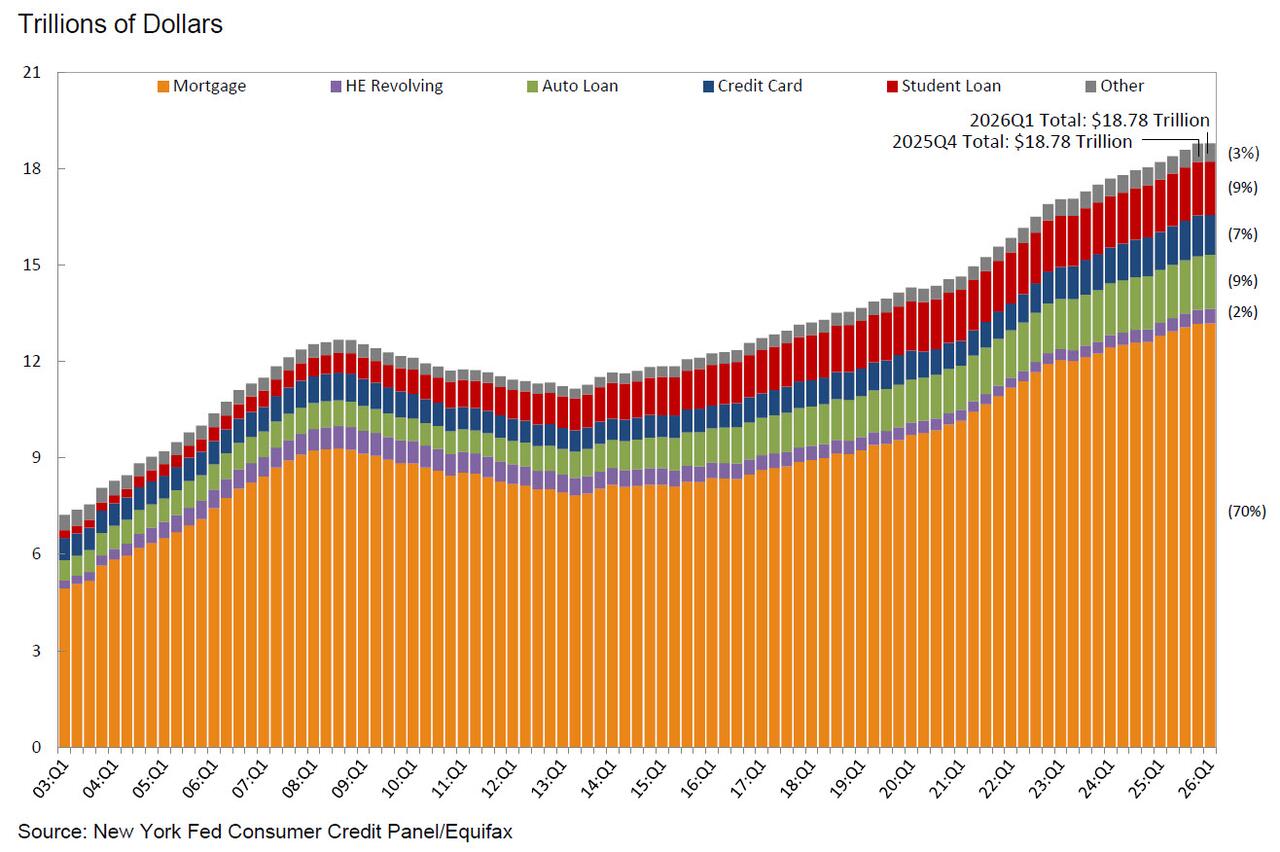

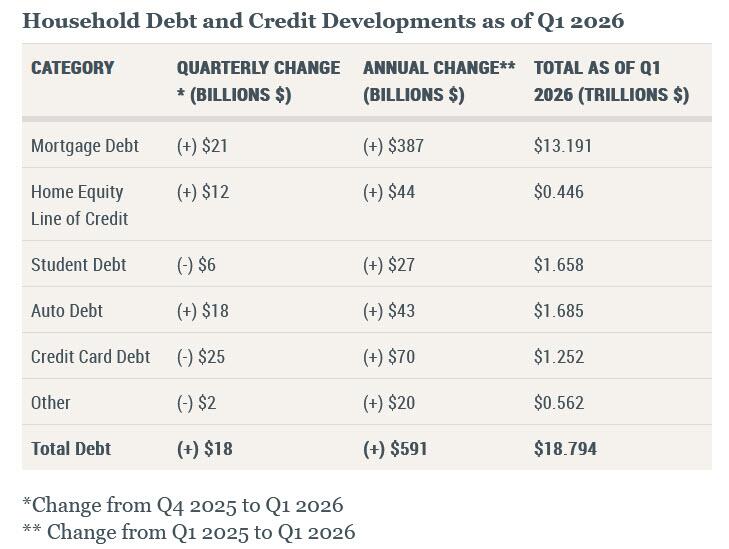

The NY Federal published its latest report on Household Debt and Credit for the first quarter: the report showed total household debt increased by $18 billion, just a 0.1% increase, in Q1 2026, to $18.8 trillion.

Some details:

- Mortgage balances shown on consumer credit reports grew slightly by $21 billion during the first quarter of 2026 and totaled $13.19 trillion at the end of March.

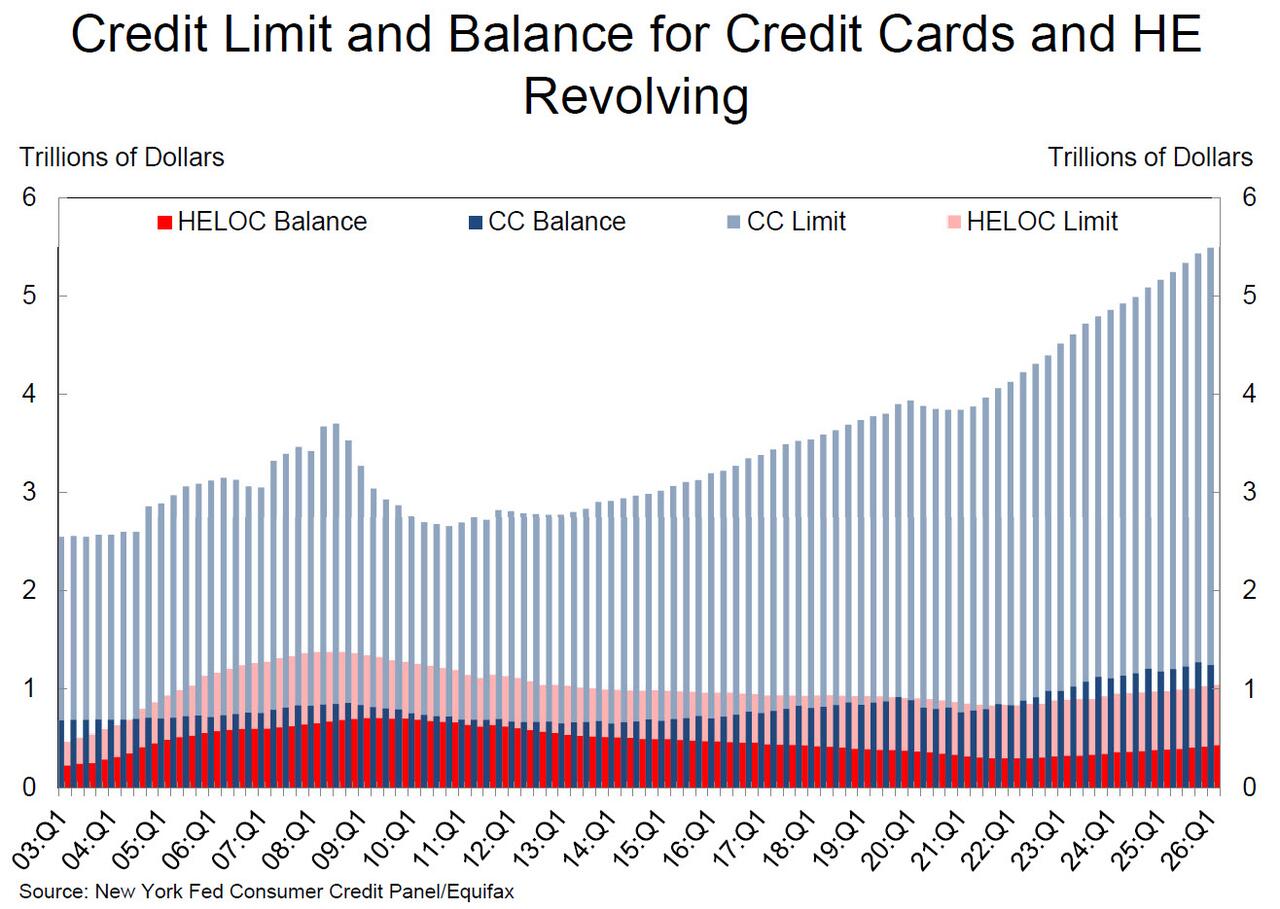

- Balances on home equity lines of credit (HELOC) rose by $12 billion, marking the 16th consecutive quarterly increase. Outstanding HELOC balances now total $446 billion, $129 billion above the low reached in 2022Q1.

- Non-housing debt balances declined by $15 billion, or 0.3%, from 2025Q4. This decline was driven primarily by a seasonal decrease in credit card balances, which fell by $25 billion and now stand at $1.25 trillion.

- Student loan balances were essentially flat, decreasing by $6 billion and standing at $1.66 trillion.

- Auto loan balances grew by $18 billion, to $1.69 trillion.

- Other balances, which include retail cards and consumer finance loans, edged down by $2 billion to $562 billion.

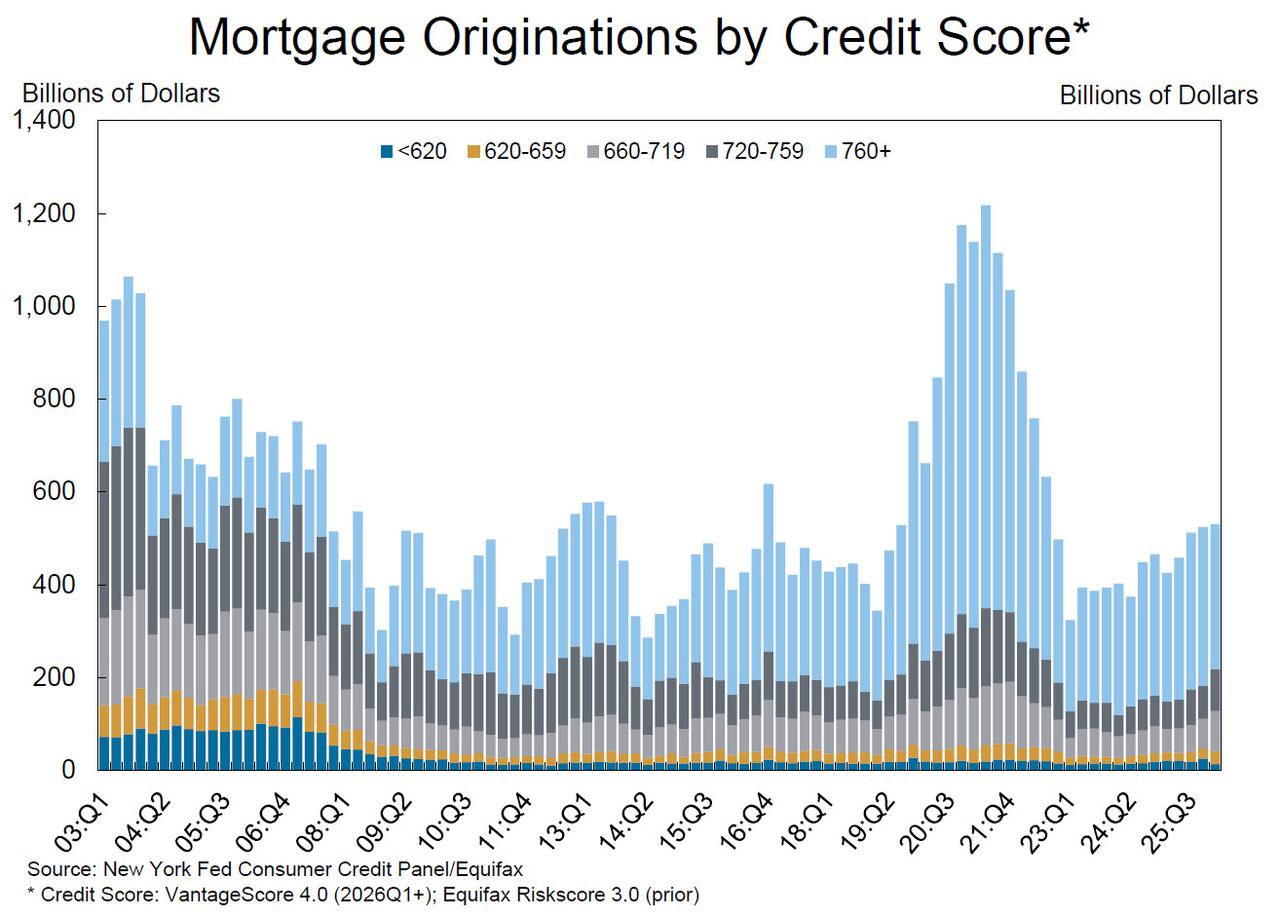

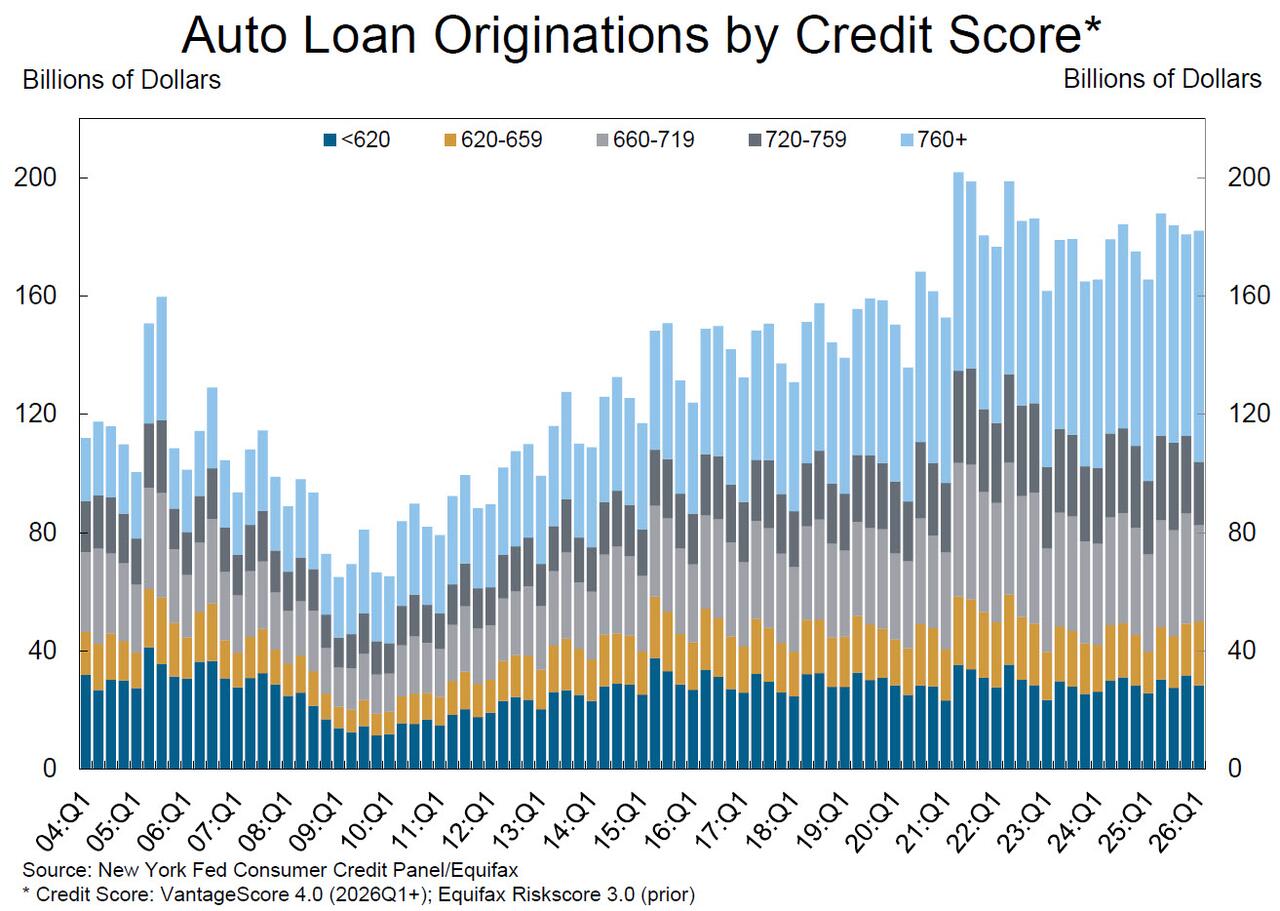

The volume of newly originated credit held steady in the first quarter of 2026 for both mortgages and auto loans. Mortgage originations, measured as appearances of new mortgages on consumer credit reports and including both refinance and purchase originations, were largely steady with $530 billion newly originated in 2026Q1.

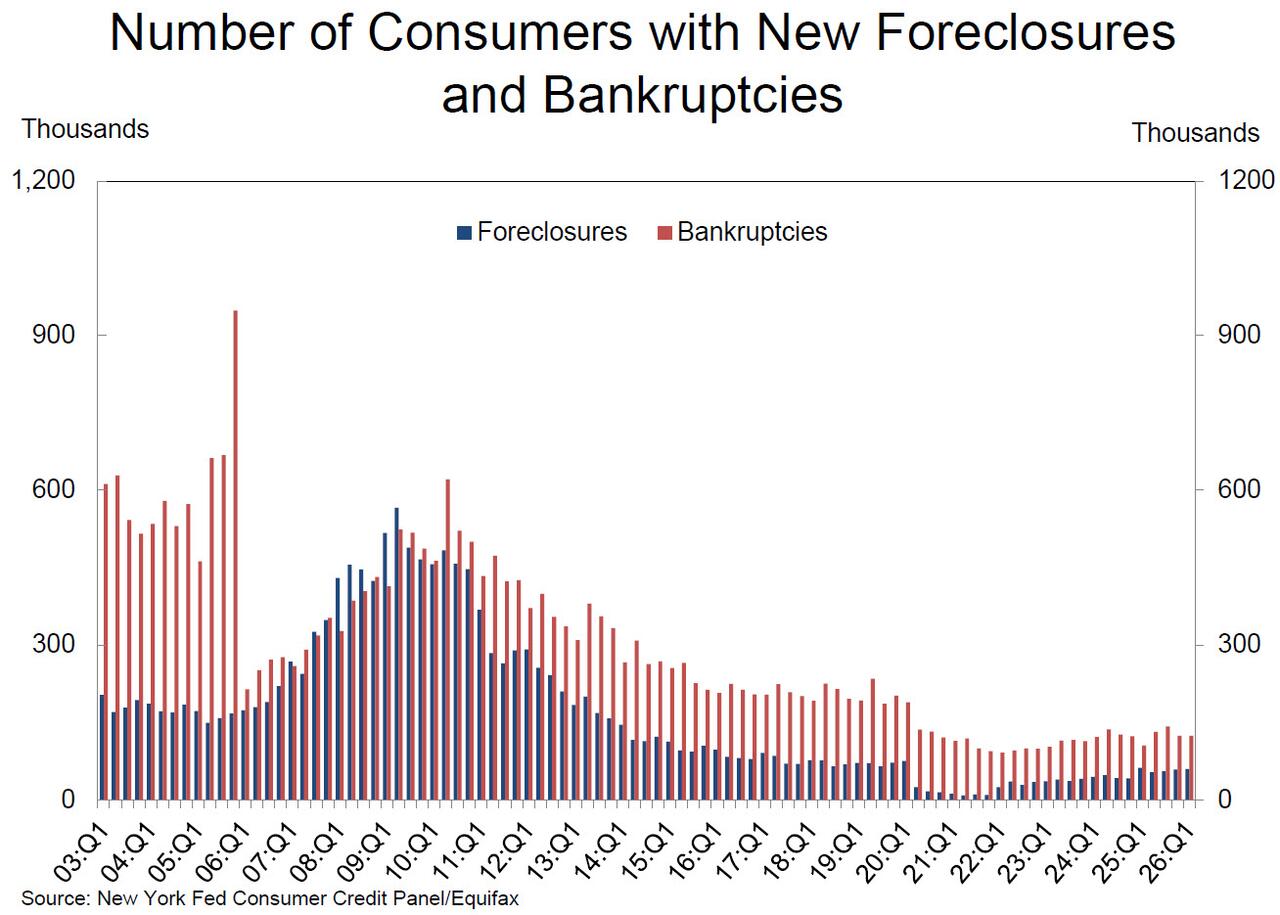

About 59,000 individuals had new foreclosures on their credit reports, a slight increase from the previous quarter.

There were $182 billion in new auto loans appearing on credit reports during the first quarter.

Aggregate limits on credit cards continued to rise, with a $60 billion (1.1%) uptick in the first quarter, to ~$5.5 trillion. Home equity lines of credit (HELOC) limits rose, albeit at a slightly slower pace, by $14 billion (1.4%), continuing an expansion in HELOCs that began in 2022.

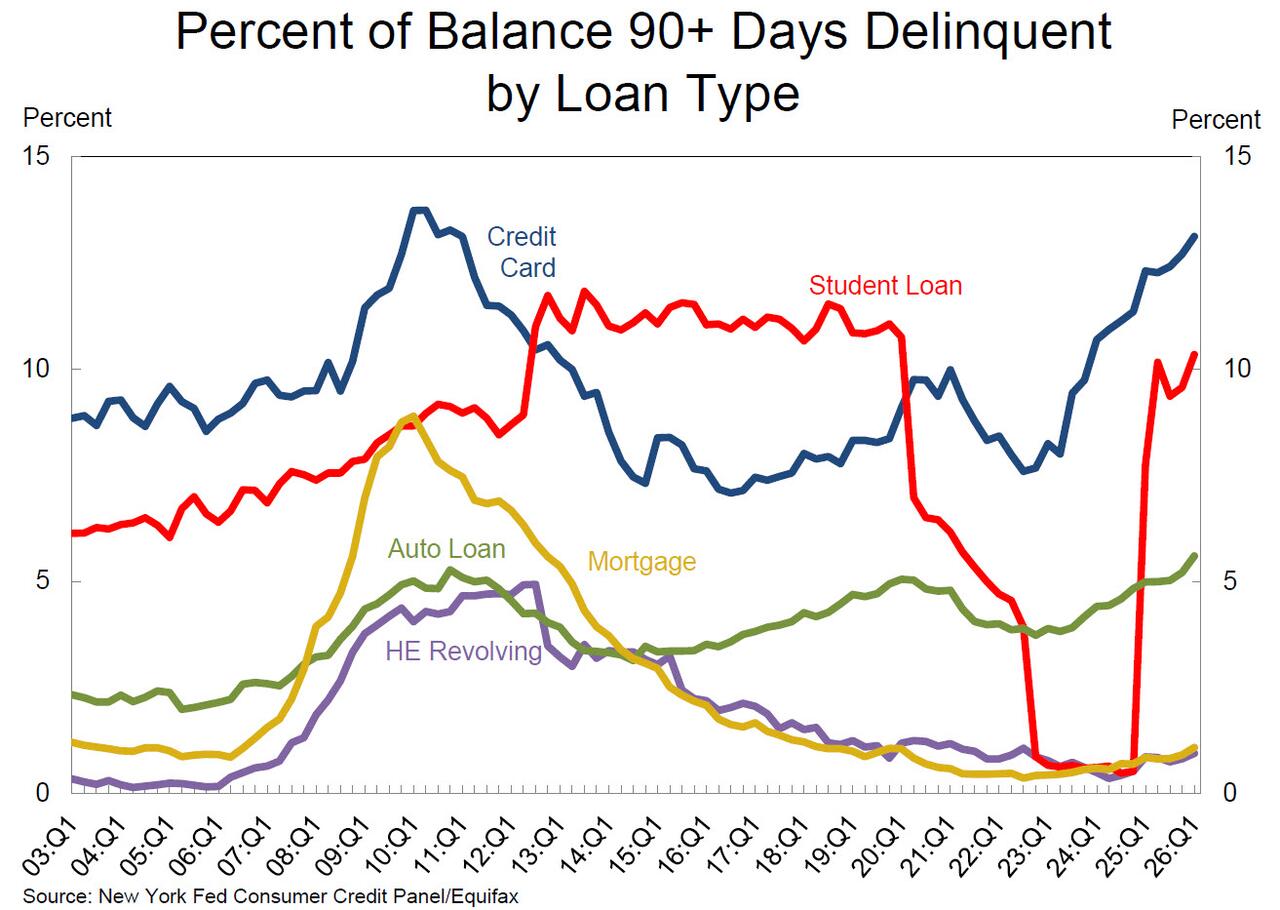

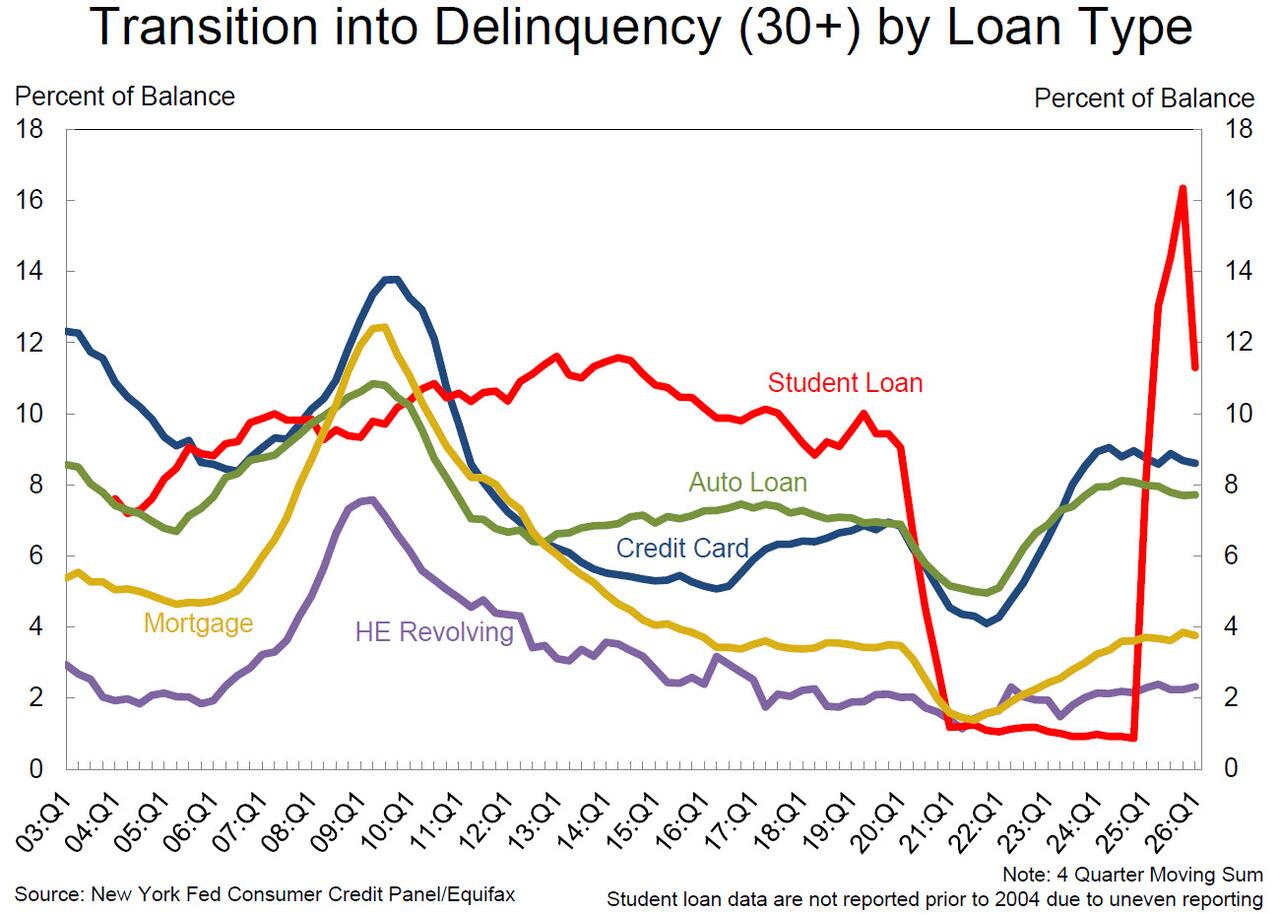

The total balance of loans delinquent at least 30 days remained unchanged at 4.8% from the prior quarter after six quarters of steady increase. Still, the overall delinquency rate matched the highest level reported since 2017. Transition into early delinquency held steady for auto loans, but ticked down for credit cards, from 8.7% annually to 8.6%, and for mortgages from 3.9% to 3.8%.

![]()

“Aggregate household debt levels rose slightly, with modest increases in most debt types offsetting a seasonal decline in credit card balances,” said Daniel Mangrum, Research Economist at the New York Fed. “Delinquency transition rates were mostly steady, while student loan delinquencies are returning to pre-pandemic levels.”

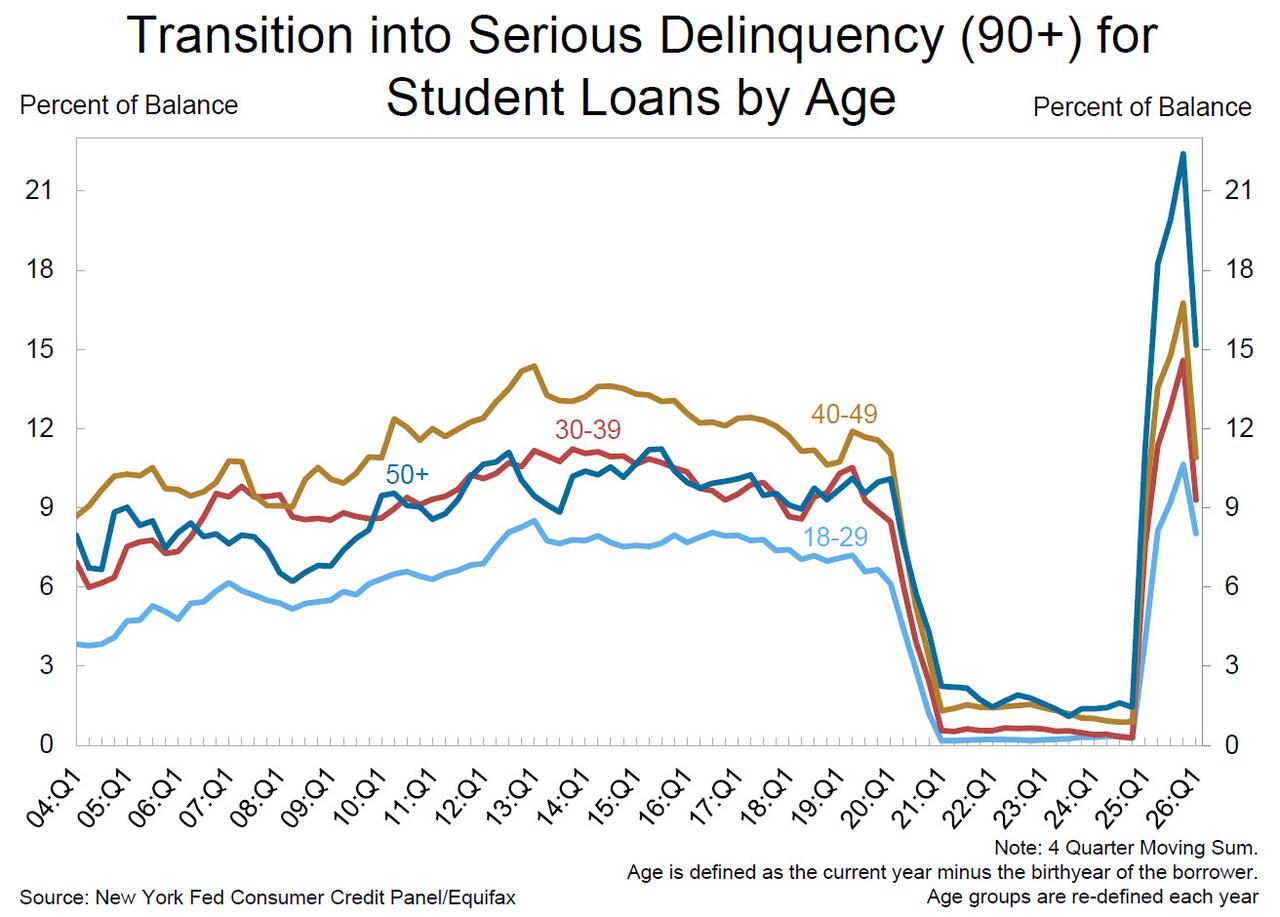

More concerning is that the percentage of loan balances that are seriously delinquent and set to transition to default/discharge continues rising – student loan delinquency rate increased to 10.3% of balances 90+ days delinquent, up from the 9.6% observed in 2025Q4 – and while it hit a new post-covid high for student loans after the Biden moratorium ended last year, the credit card picture is most dire, with the percentage there on pace to surpass the financial crisis record in the next few quarters. As shown below, transition rates into serious delinquency were mostly unchanged for auto loans and credit cards, but increased slightly for mortgages from 1.4 % annually to 1.5%. The student loan delinquency rate increased to 10.3% of balances 90+ days delinquent, up from the 9.6% observed in Q4 2025.

Some more details:

- The student loan transition rate into serious delinquency, measured as a four-quarter moving sum, declined from 16.2% in Q4 2025 to 10.9% this quarter, reflecting a slower pace of new student loan delinquencies in the first quarter relative to the previous year.

- 2.6 million student loan borrowers who were more than 120 days past due had their loans transferred to the U.S Department of Education’s Default Resolution Group.

About 124,000 consumers had a bankruptcy notation added to their credit reports in 2026Q1, a pace unchanged from the previous quarter. The percentage of consumers with a third-party collection account on their credit report worsened slightly to 5.0 percent

Taking a closer look at the army of defaulting “students”, the WSJ writes that millions of borrowers are defaulting on their student loans, and they are nearly 40 years old on average. That is nearly 2½ years older than the profile of a student-loan defaulter before the pandemic. Borrowers 50 and older are now at higher risk of default than younger borrowers.

Since a pandemic-era pause on student-loan repayments ended in 2023, the federal government has been pushing people to start repaying their loans. In the fourth quarter of last year, those who failed to restart payments began defaulting, meaning they hit 270 days past due on their payments. The New York Fed estimated that more than 3.5 million people defaulted between October and March.

The Fed report offers a look at who is defaulting:

- Most recently, the share of student-loan balances past due increased to just over 10%, nearing prepandemic levels.

- The average borrower in default is more likely to live in the South, though borrowers are defaulting across the country.

- Most of the newly defaulted borrowers weren’t past due on their student loans before the pandemic.

- Borrowers who have defaulted on their student loans are struggling to make other debt payments, too. Nearly 40% of those with auto loans are past due, 56% with at least one credit card are past due and 20% with a mortgage are past due. Loan delinquencies have been broadly trending higher.

- Some of these borrowers are likely parents who borrowed on behalf of their children, New York Fed researchers said.

The report found that Gen X borrowers, including those age 50 to 61, have the highest average student-loan balance of any age group. Many of them either reached college age as the modern federal student-loan system was forming or borrowed later, likely on behalf of their children.

Just as concerning is that in late 2024, borrowers who missed their student-loan payments saw steep drops in their credit scores for the first time in years.

The Trump administration has been revamping the federal student-loan system, emphasizing repayment. It is a reversal from the Biden administration, which pushed policies to reduce monthly payments for borrowers and get them closer to student-loan forgiveness.

The biggest consequence for defaulted borrowers is that they could have their wages, tax returns and Social Security garnished. But the Education Department has delayed its garnishment plans.

Finally, the Saving on a Valuable Education plan, or SAVE, one of the more affordable student-loan repayment plans introduced by the Biden administration, is ending, forcing millions of borrowers to transition to new plans. The new Repayment Assistance Plan, or RAP, is being introduced in July. As millions of borrowers transition out of SAVE, they will see their monthly payments increase under other income-based repayment plans. Many of them could also default on their student loans in the coming months, according to the Fed.

Source: NY Fed

Tyler Durden

Tue, 05/12/2026 – 15:40

via ZeroHedge News https://ift.tt/y7inEfl Tyler Durden