AI vs Affordability And Rates

By Peter Tchir of Academy Securities

Last week, we contemplated, for the first time, that we might need to Understand Universal Basic Income. The timing was very good as on Monday, South Korea floated the idea of transferring some AI-driven tax revenue to its citizens. As uncertainty around jobs, income, and costs continue to weigh on overall confidence, expect this subject to get more airtime in the political arena. The concept of UBI does go hand in hand with two competing themes: AI and Affordability.

China, Iran, and a Whole Lotta Nothing

Iran took a backseat to the Summit in China. We had relatively low expectations for the Summit. The cards were stacked somewhat in China’s favor as examined in China and Trade. It turns out that even our low expectations seemed to have set the bar too high. Friday’s title pretty much sums it up: My President Went to Beijing and all I got was this Crummy T-Shirt. There may yet be some deals announced, either with Iran or with China, but it looks like we are starting the week roughly where we started the prior week, but with even lower expectations.

The Oil Curve

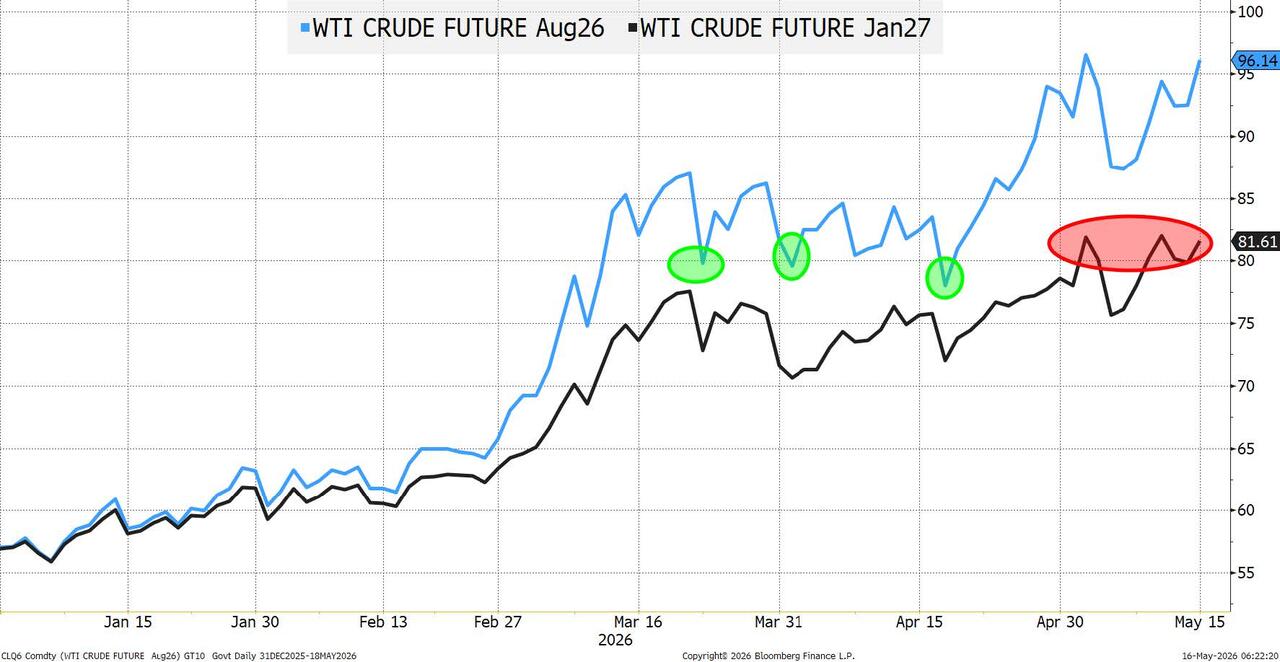

While Brent crude is most impacted by the ongoing problems in the Middle East, we will stick with WTI because that is what affects Americans the most.

One of the talking points for the admin had been that the oil market was predicting a “quick” resolution. Some officials pointed to the August contracts as demonstrating that $100 oil was a blip and things would “normalize” quickly. While $80 was still higher than pre-war, the argument had some legs. But now, the August contract is up to $95, and we are seeing $80 priced in all the way into 2027. This is certainly “higher for longer.” What is increasingly concerning is that it is difficult to tell if this is pricing in a re-opening or not. It was entirely plausible, a month or more ago, to believe that with the Strait of Hormuz getting back to normal levels of transit, global energy prices would “normalize” quickly. It is increasingly unclear what the “new” normal is. How much damage has been done to the “organism” that is energy? How quickly can things be fixed? Is the “new” normal the same as the “old” normal (see “Why One Bank Thinks It’s “Magical Thinking” That Hormuz Reopens In June“)?

Increasingly there are more and more questions about how long the damage will last, and if that damage will continue to elevate not just the price of oil, but also gasoline, diesel, jet fuel, etc.

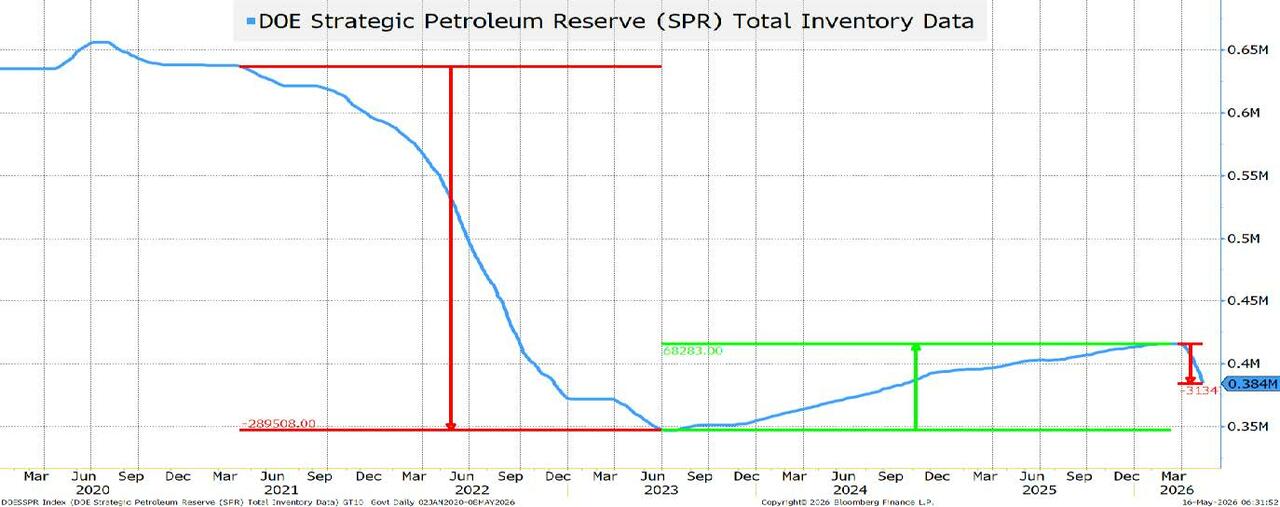

The U.S. can continue to release its Strategic Petroleum Reserves (SPR). It is unclear how low the reserves can go (I’m told that some amount needs to be left in place for structural integrity). We have released about ½ of what was added back to the SPR. Keep an eye on this, as it does limit our options over time. No one is expecting the problems to last that long, yet here we are, 3 months into the conflict, and transit through the Strait remains limited. Higher for longer in the oil market is the single biggest issue for Global Affordability.

AI versus Affordability

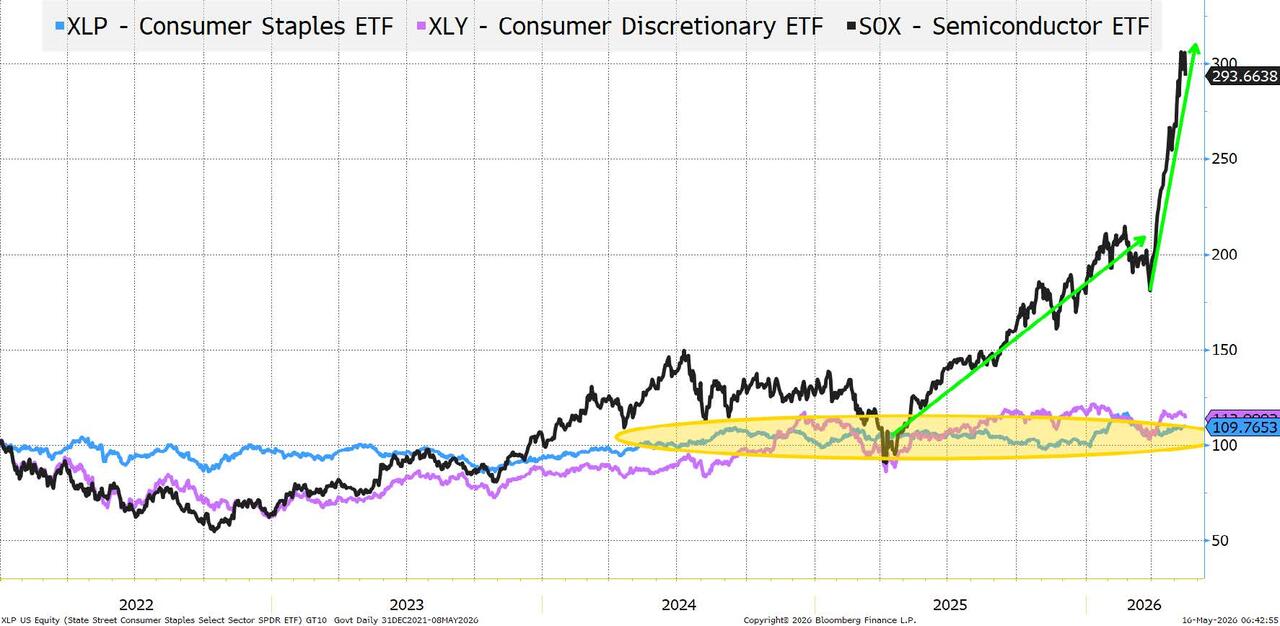

We received some consumer spending data this week which wasn’t too bad. It did seem to highlight, yet again, the problems facing people in the lower income brackets. I’m not convinced it doesn’t obfuscate that we are spending more to get less, but that is for another day. But here is a “simplified” version of a chart I’ve seen in various formats.

Companies servicing the consumer are not seeing much appreciation in their stock price.

Companies making chips are growing like gangbusters!

Is this sustainable? That question is being asked with increased urgency. The “parabolic” rise is raising some concerns. Without a doubt, this is the sector experiencing growth. It does seem to justify not only today’s prices, but also possibly even higher multiples. The earnings engine (and growth) is there, but this market has had a habit of hitting “high-conviction” trades.

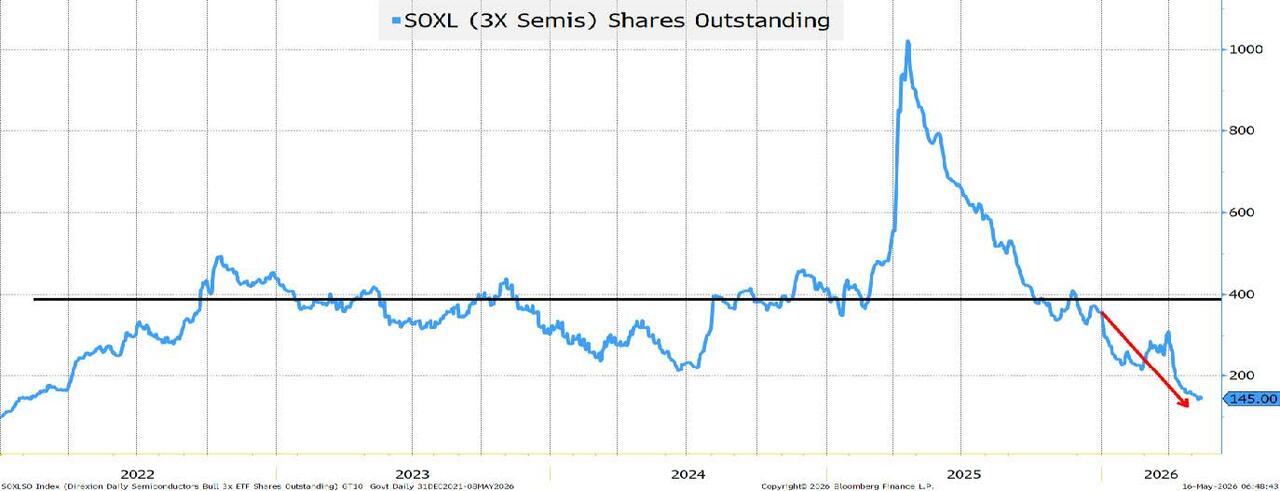

I find this chart extremely weird, but also interesting.

SOXL is a 3x leveraged SOX ETF. The assets in this ETF are about $20 billion, but the shares outstanding have been declining. While it may be inappropriate to label SOXL as a “degen” trade, I’m going to go there. “Degen” is an “affectionate” way of describing a group of very aggressive investors. Whether it is day trading leveraged ETFs, making bets in crypto altcoins, or playing in 0DTE options, there is a crowd of very aggressive traders that I will call “degen” for now (Warren Buffett would probably just call them gamblers).

I do think this crowd represents the “tip of the spear” on retail sentiment. If that assessment is correct, then it might indicate that retail is done (or almost done) fueling this trade.

The SOXX ETF weighs in at $33 billion (I had to do a double take, that it is “only” $33 billion while SOXL is $20 billion). The share count here tends to be more correlated with price. If anything, the last decline in SOXX was possibly telegraphed by a declining share count.

My view is that retail is slowing down on the semi-trade, just as institutions, including hedge funds, are treating it as a “must-have” position.

Retail, unlike funds, don’t have stop losses. Is this setting up for a pullback? Based more on positioning, and who is positioned, rather than the fundamentals?

Without the AI and semi story, market averages would be much lower. That is a fact. Is there anything to indicate that this trade cannot continue? No. But, I am curious what retail is up to here, and whether we are seeing enough of a pullback to create a reasonable pullback?

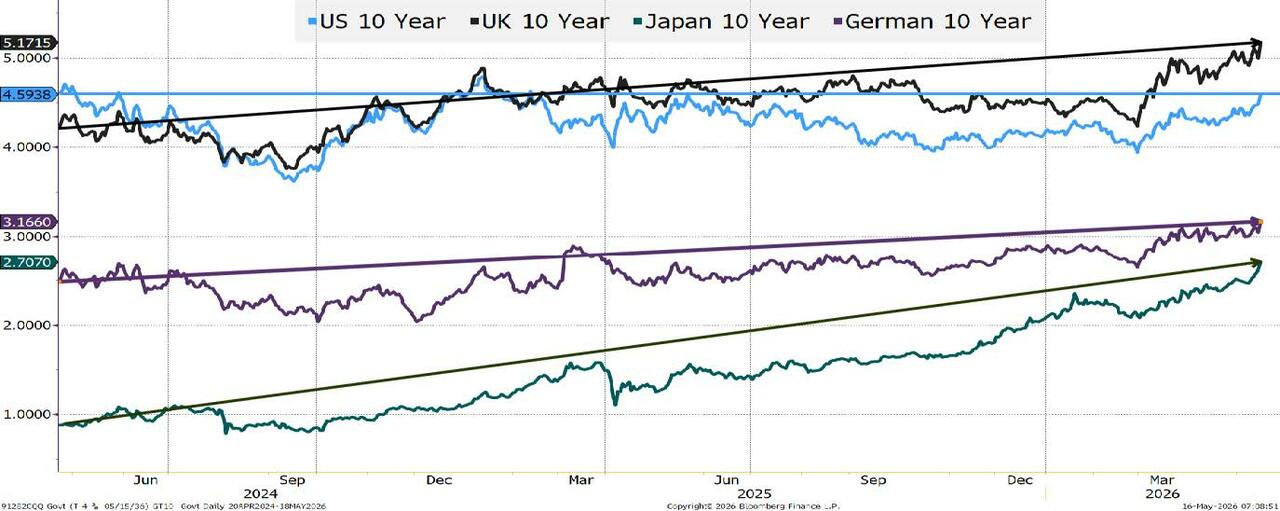

Which Brings Us To Rates

Yes, I “cherry picked” April 2024 as a starting point, because the 10-year U.S. Treasury yield is unchanged, while rates across the globe have risen. Most noticeably for Japan. In 2 years, the 10-year JGB went from yielding less than 1% to almost 3%. This is incredibly important. Japan as a “nation of savers” has been funding much of the world’s debt. I remain convinced that “at or near-zero” bond buyers of all levels of sophistication will take steps to get positive yield. So, when Japan hovered near 0% on rates, many investors would find alternatives to their domestic market to get yield. That has changed.

Globally, U.S. Treasuries, are fairly “generic.”

- If you do not need dollar exposure, you have local FX bonds that can serve your needs.

- All countries face a variety of risks to their economy. All central banks are trying to navigate the data, their expectations, and their mandate. It is less certain today how the U.S. central bank will respond to data than it was a few months ago – so that uncertainty should have a cost?

- It is likely one reason why our agency debt team is seeing agency and super sovereign debt spreads to Treasuries at very low levels.

Defense Spending Requires Money

- While ProSec is about far more than defense spending, it certainly incorporates the need to spend more. Japan – spending more. Europe/NATO – spending more and it seems inevitable that they will have to ramp that up.

The AI and Data Center Build Out Competes for Money

- The semiconductor valuations depend heavily on data center and AI spending. That is being funded in a large part by debt.

We have been arguing for “range-bound” Treasury trading, while slowly raising the midpoint of the range.

I’m a bit hesitant to be very bearish on bonds here, as 5% or so on 30s (we are well above 5.12% as of Friday’s close) has been a level where this admin has taken steps to drive yields lower.

I could see an “Operation Twist” sort of announcement (the Fed selling shorter-dated bonds they own, to buy longer-dated bonds), but I’m not sure they are prepared to act.

What I find “interesting” is that Bessent no longer seems to be able to do “no wrong.” At the height of Liberation Day fears, Bessent could appear on TV and calm things instantaneously. I heard of the TACO BELL trade. Trump Always Chickens Out. Bessent Explains Longer Later. It was pretty clever (I did not come up with that).

Maybe it is because the Iran conflict is so far removed from what a Treasury Secretary does, that his latest appearances haven’t had the same impact? Maybe I have Bessent Delusion Syndrome? (Anything is possible).

But as many market participants seem to be waiting for some sort of “intervention” to helps bonds, I’m left wondering if they can accomplish that easily now?

Global bond yields are not helping. Higher for Longer on oil is not helping (that seems easier to correct – via peace with Iran, but that doesn’t seem imminent).

Bottom Line

Not “pound the table” bearish on bonds or stocks, but certainly not bullish. Not even really bullish for a trade. With the President likely looking for some “wins” and the admin likely exploring what they can do on the yield front, we could see relief in bond yields and higher stock prices, but I want hedges and would fade any such bounce. Price action in stocks seemed almost “sickly” on Thursday and Friday where every bounce/rally met some serious selling. Maybe all the AI-trained algos have read Sell in May and Go Away? Sorry, had to go there.

Caution into the summer seems warranted. Markets have priced in a lot of good news (China, Iran, and Semis), often multiple times (at some point is an earnings surprise really a surprise when everyone surprises the same way?).

Maybe it is time to “unprice” some of the good news? Affordability remains an issue and it seems to be becoming increasingly entrenched, which is a problem for bonds and stocks as a whole, if not just for the AI/data center spend, where my bigger questions are around positioning, than anything else.

Tyler Durden

Sun, 05/17/2026 – 12:50

via ZeroHedge News https://ift.tt/wjMN6kR Tyler Durden